Category: Business

Corrugated Board Packaging Market Global Industry Dynamics, Growth & Forecast 2032

By ameliasss, 2025-09-19

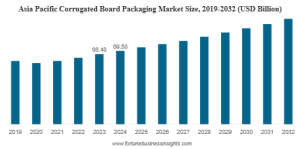

According to Fortune Business Insights, The global corrugated board packaging market was valued at USD 134.74 billion in 2024 and is expected to grow to USD 140.11 billion in 2025, further reaching USD 191.50 billion by 2032. This growth represents a CAGR of 4.56% over the forecast period. In 2024, Asia Pacific held the largest share of the market, accounting for 51.64% of the global revenue.

The global corrugated board packaging market size is expected to display exceptional growth during the forecast period of 2024-2032. Corrugated board packaging is a versatile and budget-friendly method of packaging, safeguarding, and transporting a vast variety of products. There are several advantages of using these boards, such as lightweight nature, recyclability, and biodegradability, which make them a popular packaging item in many industries. This factor will play a key role in boosting the demand for this form of packaging, thereby accelerating the market’s growth.

Segments:

By board type, the market is divided into single face corrugated board, single wall (double face) corrugated board, double wall corrugated board, and triple wall corrugated board.

By flute type, the market is segmented into A flute, B flute, C flute, E flute, F flute, BC flute, and EB flute.

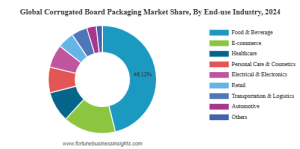

By end-user, the market is segregated into food & beverage, personal care & cosmetics, e-commerce, electronics & electrical, healthcare, and others.

With respect to geography, the market is studied across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/corrugated-board-packaging-market-108360

Major Players Profiled in the Report:

- Mondi Group (U.K.)

- Smurfit Kappa (Ireland)

- Sealed Air Corporation (U.S.)

- Wertheimer Box Corp. (U.S.)

- Arabian Packaging Co. LLC (Dubai)

- Klingele Papierwerke GmbH & Co. KG (Germany)

- Pregis LLC (U.S.)

- DS Smith (U.K.)

- John Hargreaves (U.K.)

- IPS Packaging and Automation (U.S.)

- Hughes Enterprises (U.S.)

Report Coverage

The report has conducted a detailed analysis of the market and focused on several critical aspects, such as leading end-users, board types, flute types, and top market players. It has also highlighted the most recent market trends and the key developments in the industry. In addition to the factors mentioned above, the report delves into several other factors that have helped the market grow.

Drivers:

Increasing Demand for Eco-Friendly Packaging Solutions to Fuel Market Growth

Customers are becoming increasingly conscious about their overall impact on the environment. This has increased their preference for eco-friendly packaging products to reduce their carbon footprint. Moreover, the ever-expanding food & beverage industry is also fueling the adoption of corrugated board packaging products to safely transport food products without compromising on their quality and freshness.

However, low mechanical strength and endurance do not make these products suitable for packing heavy items, which can impede their demand.

Regional Insights

North America Leads Global Market Growth Due to Increasing Sales of Consumer Electronics

North America is dominating the global corrugated board packaging market share as the region is witnessing high sales of consumer electronics, such as smartphones and laptops. Rapid urbanization and digitization are some of the key factors bolstering the sales of these products, which will positively impact the demand for corrugated board packaging solutions.

Asia Pacific is recording the fastest growth due to rising eco-consciousness and growing demand for sustainable packaging solutions.

Europe will also witness steady growth due to major advancements in the electronics industry and robust demand for processed foods.

Latin America and the Middle East & Africa will showcase moderate progress due to the growing need for corrugated boards with plastic coatings, lightweight flutes, and other features.

Information Source: https://www.fortunebusinessinsights.com/corrugated-board-packaging-market-108360

Competitive Landscape

Key Players to Enter Acquisitions and Launch New Products to Expand Market Share

Some of the leading market players include Mondi Group, Smurfit Kappa, Sealed Air Corporation, Wertheimer Box Corp., Arabian Packaging Co. LLC, Kingele Papierwerke GmbH & Co. KG, Pregis LLC, DS Smith, John Hargreaves, IPS Packaging and Automation, and Hughes Enterprises, among others. These firms are signing merger & acquisition agreements and launching novel products to expand their market share and customer base.

Key Industry Development

- In January 2025, Biedronka partnered with Mondi in a circular program aimed at supplying, collecting, and recreating its corrugated packaging in accordance with the retailer’s goals for plastic usage and CO2 emissions. The produced paper is then sent to one of Mondi’s six factories in Poland, where it is converted into corrugated cardboard packaging, such as crates for fruits and vegetables.

- In June 2024, Saica Group, a prominent player in packaging solutions, partnered with Mondelez, a major manufacturer of fast-moving consumer goods, to introduce a new paper-based product aimed at multipack items in the confectionery, biscuits, and chocolate sectors. This new packaging made from paper is intended to be recyclable within the paper waste stream. It is compatible with heat-sealable packing processes, offering the choice to be produced either coated or uncoated based on the desired final look.

According to Fortune Business Insights, The global dyes and pigments market was valued at USD 42.64 billion in 2023 and is expected to expand from USD 44.68 billion in 2024 to USD 56.91 billion by 2032, reflecting a CAGR of 5.1% over the forecast period. In 2023, Asia Pacific led the market, accounting for 41.3% of the global share. Meanwhile, the U.S. dyes and pigments market is anticipated to experience notable growth, projected to reach USD 11.12 billion by 2032, largely fueled by the strong expansion of the country’s textile industry.

The rising population, economic development, and the growing e-commerce industry are expected to propel the industry's growth. Fortune Business Insights ™ presents this information in its report titled “ Dyes and Pigments Market, 2024-2032. ”

Segments

By type, the market is segmented into reactive, dispersive, vat, others, and acid dyes; and inorganic and organic pigments. By end-user, it is classified into textiles, leather, paper, paints, plastics, and other dyes; and printing ink, paints & coatings, plastics, and other pigments. Geographically, it is clubbed into Asia Pacific, Latin America, North America, Europe, and the Middle East & Africa.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/dyes-pigments-market-102333

List of Key Players Profiled in the Report

- BASF SE (Germany)

- DIC CORPORATION (Japan)

- Clariant (Switzerland)

- Sudarshan Chemical Industries Limited (India)

- Huntsman International LLC. (U.S.)

- Atul Ltd (India)

- Cabot Corporation (U.S.)

- DuPont (U.S.)

- Kiri Industries Ltd. (India)

- KRONOS Worldwide, Inc. (U.S.)

Report Coverage

The report provides a detailed analysis of the top segments and the latest trends in the market. It comprehensively discusses the driving and restraining factors and the impact of COVID-19 on the market. Additionally, it examines the regional developments and the strategies undertaken by the market's key players.

Drivers and Restraints

Robust Demand from the Coatings & Paints Industry to Propel Market Growth

Dyes and pigments are substances used to provide a material with color. The rising demand for the product from the coatings & paints industry is likely to foster industry growth. Further, rising awareness regarding the corrosion resistance, mechanical strength, toughness, clarity, and color of the solids will likely propel their demand. Moreover, the rising applications of the chemical from the decorative, automotive, and architectural industries are expected to bolster its sales. Also, the rising demand for coatings in the manufacturing industry is expected to propel the industry’s progress. These factors may drive the dyes and pigments market growth.

However, the strict government regulations regarding waste generation are expected to hinder the market progress.

Regional Insights

Rising Middle-Class Population May Foster Industry Growth in Asia Pacific

Asia Pacific is expected to dominate the dyes and pigments market share due to the rising middle-class population. The market in Asia Pacific stood at USD 15.91 billion in 2021 and is expected to grow positively during the upcoming years. Further, the development of the textile industry in the region may foster market progress.

In North America, the rapidly growing textile industry in the U.S. is expected to propel dyes and pigments’ adoption. Further, the rising adoption of titanium dioxide as a pigment in manufacturing is expected to boost industry growth.

In Europe, the rising product consumption in leather is expected to boost dyes and pigments adoption. Further, its increasing demand in clothes, furniture, footwear, and the automotive industry is expected to propel market development.

Information Source: https://www.fortunebusinessinsights.com/dyes-pigments-market-102333

Competitive Landscape

Major Players Engage in Acquisitions to Expand Product Line-up

The prominent companies operating in the market engage in acquisitions to expand their market presence. For example, Sun Chemical DIC Corporation completed the acquisition of BASF’s global pigments business in June 2021. This development may enable the company to extend its DIC portfolio in several applications such as inks, paints, coatings, cosmetics, and electronic displays. Further, companies adopt research and development, partnerships, acquisitions, mergers, and expansions to enhance their market stance.

Key Industry Development

- June 2021 - Sun Chemical and DIC Corporation acquired BASF’s global pigments business. This acquisition will extend DIC's portfolio as a global manufacturer of pigments for various applications such as electronic displays, cosmetics, coatings, paints, and inks.

- December 2020 - Asahi Songwon Colors started the commercial operations at the Dahej plant of Asahi Tennants Color, its 51:49 joint venture with Tennants Textile Colours Limited (TTC) of the U.K. This acquisition will widen Asahi’s presence as a global pigments supplier.

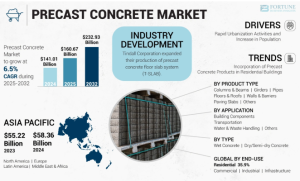

The global precast concrete market size was valued at USD 151.49 billion in 2024. The market is projected to grow from USD 160.53 billion in 2025 to USD 246.07 billion by 2032, at a CAGR of 6.3% during 2025-2032. Asia Pacific dominated the precast concrete market with a market share of 38.52% in 2024.

Precast concrete is manufactured off-site in a controlled environment using reusable molds, allowing the material to cure under optimal conditions with close monitoring. Unlike conventional on-site casting, this process enhances efficiency since the same molds can be reused multiple times. Key benefits include improved quality control, superior craftsmanship, and enhanced safety, as production is carried out at ground level.

The increasing urbanization and construction activities will have an outstanding effect on the market, states Fortune Business Insights, in a report, titled “ Precast Concrete Market Size, Share & Industry Analysis, By Product Type (Building Components, Transportation, Water & Waste Handling, and Others), By End-Use (Residential, and Non-Residential), and Regional Forecast, 2025-2032.”

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/precast-concrete-market-103301

The Report Lists the Key Companies in the Precast Concrete Market:

- Boral (Australia)

- LafargeHolcim (Switzerland)

- Gulf Precast (UAE)

- Olson Precast Company (U.S.)

- Larson & Turbo Limited (India)

- CEMEX (Mexico)

- Forterra (U.S.)

- Tindall Corporation (U.S.)

- Spancrete (U.S.)

- Elementbau Osthessen GmbH & Co., ELO KG (Germany)

- Bouygues Construction(France)

- Balfour Beatty(U.K.)

- Oldcastle Precast (U.S.)

- Other Key Players

The report on the precast concrete market highlights:

- Exceptional insights into the market

- Methodical data with detailed analysis

- Market dynamics and aspects demonstrating the development

- Meticulous information about vital players in the market

- Procured statistics about dominant regions

- Competitive landscape

Market Overview :

Ever-increasing Population to Contribute Growth

The surging population along with rapid urbanization are factors expected to enable speedy expansion of the market. The increasing requirement for non-residential establishments such as airports, sports complexes, malls, and commercial spaces can have a tremendous impact on market growth. The growing population has resulted in heavy demand for residential spaces, which, in turn, will aid the expansion of the market. The increasing government initiatives for residential housing for the Economically Weaker Section (EWS) will spur lucrative opportunities for the market in the forthcoming years. Similarly, the growing government support for commercial spaces and offices will subsequently bolster the healthy growth of the market in the foreseeable future.

Regional Analysis :

Heavy Investments in Residential Sector to Boost Market in Asia Pacific

The market in Asia Pacific is expected to hold the largest share in the global market owing to the growing investments in construction projects by countries such as China, India, and Japan. The developing residential sector in developing nations will fuel demand for precast concrete, in turn aiding the growth of the market in the region. North America is expected to experience a significant growth rate owing to the adoption of advanced and sustainable construction practices. Europe is expected to rise exponentially owing to the demand for concrete products in non-residential and infrastructural development. The Middle East & Africa is expected to observe a substantial growth rate during the forecast period owing to the growing investments for the development of malls, airports, hotels, and public places. The booming tourism industry will contribute significantly to the market in the Middle East.

Competitive Landscape :

Adoption of Strategies by Prominent Companies to Consolidate Industry

The key players in the market are investing heavily in R&D to develop sustainable products for the market. The industry players are focused on partnerships and collaborations to strengthen their position in the market. Moreover, the adoption of various business strategies prominent companies will have an excellent impact on the global market during the forecast period.

Information Source: https://www.fortunebusinessinsights.com/precast-concrete-market-103301

KEY INDUSTRY DEVELOPMENTS

- November 2024: Boral collaborated with the Gamuda and Laing O’Rourke Consortium (GLC) to develop an innovative precast mix aimed at reducing the embodied carbon footprint of the Sydney Metro West project. This mix incorporates 50% supplementary cementitious material (SCM), an Australian first for precast tunnelling segment production.

- October 2024: Larsen & Toubro (L&T) reached a significant milestone in the construction of the Delhi-Meerut RRTS, with the completion of casting for the final 6290 precast box segments for Package 7 of the project.

The global bamboo packaging market was valued at USD 501.52 million in 2024 and is expected to expand from USD 531.30 million in 2025 to USD 827.15 million by 2032, reflecting a CAGR of 6.53% over the forecast period. In the United States, the market is anticipated to witness strong growth, reaching USD 188.33 million by 2032. This expansion is primarily fueled by the increasing demand for sustainable, eco-friendly, and biodegradable packaging alternatives. In 2024, Asia Pacific led the global market, accounting for 38.91% of the overall share.

As sustainability becomes a central concern for consumers, businesses, and regulators, bamboo packaging is rapidly gaining ground as an eco-friendly alternative to traditional packaging materials like plastics, paper, and glass. With its fast renewability, strength, and biodegradability, bamboo is ideally positioned to address growing environmental pressures and help reduce plastic pollution. The global bamboo packaging market was valued at USD 501.52 million in 2024 and is forecast to grow significantly through 2032.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/bamboo-packaging-market-109987

Market Size & Forecast

2024: USD 501.52 million

2025: USD 531.30 million

2032 Forecast: USD 827.15 million

CAGR (2025-2032): ~6.53%

This steady growth reflects rising adoption of bamboo packaging driven by increasing environmental consciousness, regulatory pressure, and advances in production technology.

Key Drivers of Growth

Sustainability & Environmental Concerns

Bamboo is renewable, biodegradable, and offers a way to reduce dependency on plastics. Growing awareness among consumers and stricter government regulations on plastic waste and single-use packaging strongly favor bamboo alternatives.

Advances in Processing & Materials Technology

Innovations in fiber extraction, pulp technologies, and composites enhance durability, moisture resistance, and design flexibility. These improvements allow bamboo packaging to compete with established materials.

Cost Improvements & Scaling

As bamboo packaging production scales, costs are expected to decrease through efficiencies in harvesting, pulping, and molding. This makes bamboo packaging more commercially feasible.

Regulatory & Corporate Sustainability

Policies promoting circular economy and bans on plastics are encouraging industries such as food & beverages, cosmetics, and electronics to switch to bamboo packaging. Brands are also leveraging sustainable packaging as a part of their identity.

LIST OF TOP BAMBOO PACKAGING COMPANIES:

- NCD Corporation (China)

- APC PACKAGING (U.S.)

- Kinghome (Taiwan)

- RyPax (China)

- Three Bamboo (China)

- Bloom Eco Packaging Co. Ltd. (China)

- Golden Arrow, Inc. (U.S.)

- OtaraPack (China)

- APackaging Group (U.S.)

- Meysher Industrial Group (China)

- Oceans Republic Company Limited (Vietnam)

- Ningbo Gidea Packaging Co., Ltd. (China)

Challenges

Supply Chain Complexity : Sourcing high-quality bamboo and establishing reliable processing capacity remain challenges in some regions.

Competition from Established Materials : Plastics, paperboard, and glass still dominate due to cost and familiarity.

Regulatory & Certification Barriers : Obtaining eco-certifications and ensuring compliance increases costs.

Market Segmentation

By Material :

Virgin Pulp (leading segment due to higher performance)

Recycled Pulp (gaining traction for sustainability appeal)

By Type :

Trays & Clamshells

Boxes & Cartons (dominant category due to versatility)

Caps & Closures

Bottles (increasing demand as plastic alternatives)

Others

By End-use Industry :

Food & Beverages (largest segment, driven by bans on single-use plastics)

Cosmetics & Personal Care (second largest, leveraging bamboo’s natural aesthetic)

Pharmaceuticals, Electronics, and Others

Regional Insights

Asia Pacific : Dominates with about 38.91% share in 2024, supported by strong bamboo cultivation, lower costs, and a growing food service sector.

North America : Second largest market, driven by sustainability initiatives and consumer demand. The U.S. bamboo packaging market is projected to reach USD 188.33 million by 2032.

Europe : Strong regulatory push for eco-friendly packaging and bans on plastics fuel adoption.

Latin America and Middle East & Africa : Emerging markets with growth potential, supported by rising green infrastructure and awareness.

Trends & Innovations

Composite Materials : Combining bamboo with other biodegradable materials to improve moisture resistance and durability.

Manufacturing Advances : New processing technologies that lower costs and enhance product uniformity.

Circular Economy : Increasing focus on compostability, reusability, and certified sustainable sourcing.

Opportunities

Food & Beverage : Strong demand for eco-friendly takeaway and delivery solutions.

Cosmetics & Personal Care : Premium brands using bamboo packaging as part of eco-branding.

Regulatory Incentives : Policies and subsidies promoting biodegradable packaging.

Emerging Markets : Countries with abundant bamboo resources gaining a cost advantage.

Outlook & What to Watch

The bamboo packaging market is set to reach USD 827.15 million by 2032 at a CAGR of about 6.5%.

Cost vs. performance will remain a key factor in adoption.

Consumer education and certification will drive trust in bamboo packaging’s eco-claims.

Supply chain standardization and scaling will be critical to meeting rising demand.

Information Source: https://www.fortunebusinessinsights.com/bamboo-packaging-market-109987

The bamboo packaging market is on a strong upward path, fueled by environmental awareness, government regulations, and innovation. With robust growth expected through 2032, bamboo packaging is poised to play a crucial role in replacing traditional plastics and advancing the circular economy. Companies that innovate in design, certification, and cost efficiency will be best positioned to lead this market.

KEY INDUSTRY DEVELOPMENTS:

- May 2024 - Gidea PAC announced the launch of its new line of cosmetic packaging, which underscores the sustainability of bamboo. The new packaging solutions are designed to provide eco-friendly alternatives to traditional materials while maintaining high-quality standards for cosmetic products.

- April 2024 – Clement Packaging developed compostable bamboo packaging solutions for beauty and personal care.

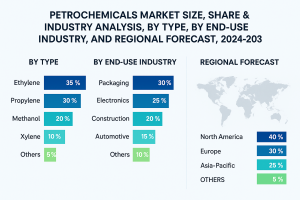

The global petrochemicals market is witnessing steady growth, driven by rising demand across industries and advancements in production technologies. According to Fortune Business Insights, the market was valued at USD 623.83 billion in 2023 and is projected to increase from USD 649.16 billion in 2024 to USD 900.91 billion by 2032, reflecting a compound annual growth rate (CAGR) of 4.2% throughout the forecast period. Among regions, Asia Pacific dominated the market in 2023, holding a commanding 52.16% share. The United States market is also set for strong expansion, with the petrochemical sector expected to achieve USD 105.76 billion by 2032, supported by government-backed recycling initiatives and sustainability programs.

Petrochemicals, derived mainly from natural gas, crude oil, and coal, form the backbone of several industries. They are crucial in the production of plastics, synthetic rubber, solvents, and numerous chemical intermediates. End-use industries such as electronics, automotive, packaging, and construction rely heavily on these materials to develop innovative products and meet growing consumer demand. With urbanization, industrialization, and lifestyle changes increasing worldwide, petrochemicals are expected to remain indispensable to modern economies.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/petrochemicals-market-102363

List of Key Players Mentioned in the Report:

- BASF SE (Germany)

- LyondellBasell Industries Holdings B.V. (Netherlands)

- INEOS (K.)

- Shell plc (K.)

- SABIC (Saudi Arabia)

- Reliance Industries Limited (India)

- Mitsubishi Chemical Corporation. (Japan)

- Dow Chemical Company (U.S.)

- LG Chem (South Korea)

- Chevron Phillips Chemical Company LLC. (U.S.)

- China National Petroleum Corporation (China)

- Maruzen Petrochemical Co., Ltd. (Tokyo)

Market Segmentation

By Type

The petrochemicals market is segmented into methanol, propylene, ethylene, xylene, and others .

Ethylene has historically dominated the market and continues to lead due to its extensive use in producing ethylene glycol, vinyl chloride, and polyethylene . These derivatives serve as essential raw materials for plastics, fibers, and packaging solutions.

Other types, such as propylene and methanol , are also witnessing strong demand in applications ranging from fuel additives to adhesives and coatings.

By End-Use Industry

Based on application, the market is categorized into electronics, automotive, construction, packaging, and others .

Packaging emerged as the largest segment in 2022 , primarily fueled by the rising use of plastic packaging materials across both food and non-food sectors. Flexible packaging, bottles, containers, and films continue to be in high demand, particularly in emerging economies with booming retail and e-commerce sectors.

The automotive industry is another important consumer, using petrochemical-based products for lightweight vehicle components, tires, coatings, and interiors. Similarly, construction and electronics sectors are increasing their dependence on petrochemicals for insulation materials, cables, and structural applications.

Regional Insights

Asia Pacific remains the undisputed leader in the global petrochemicals market. Rapid industrial growth in China, India, and Southeast Asia , coupled with a robust automotive sector and expanding manufacturing activities, has strengthened the region’s dominance.

North America is showing significant progress due to technological advancements in shale oil extraction and hydraulic fracturing , which have enhanced domestic feedstock availability. This has boosted the region’s petrochemical production capacity, making it a strong global competitor.

Europe and the Middle East also contribute significantly, with investments in advanced facilities and integrated refinery operations supporting steady growth.

Market Drivers and Restraints

Drivers: The industry is benefitting from the expansion of the packaging sector, rapid urbanization, and the rising demand for consumer goods globally. Innovation in material science and growing adoption of plastics in diverse industries are also fostering growth.

Restraints: On the flip side, environmental concerns and the ecological impact of petrochemical products are posing challenges. Governments and organizations are increasingly regulating plastic use and encouraging recycling, which may restrict unchecked growth in the sector.

Information Source: https://www.fortunebusinessinsights.com/petrochemicals-market-102363

Competitive Landscape

The global petrochemicals market is highly competitive, with leading companies focusing on mergers, acquisitions, joint ventures, and technological innovations to enhance profitability and maintain market presence. Firms are also prioritizing sustainable production methods to align with global environmental goals.

Notable Development

In January 2024 , LyondellBasell announced plans to acquire a 35% stake in Saudi Arabia’s National Petrochemical Industrial Company (NATPET) for more than USD 500 million . Backed by its Spheripol polypropylene technology , this acquisition is expected to provide LyondellBasell with access to competitive feedstocks while boosting its polypropylene production capacity in the Middle East.

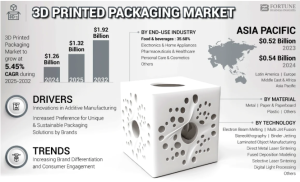

According to Fortune Busines Insights, The global 3D printed packaging market was valued at USD 1.26 billion in 2024 and is projected to reach USD 1.32 billion in 2025, before climbing to USD 1.92 billion by 2032, expanding at a CAGR of 5.45% during the forecast period. Asia Pacific dominated the market in 2024, capturing 42.86% of the global share, driven by strong adoption in food, cosmetics, and consumer goods industries.

The 3D printed packaging industry is transforming the packaging landscape with its ability to deliver sustainable, customized, and cost-efficient solutions. Unlike traditional methods, additive manufacturing enables personalized designs, rapid prototyping, reduced material waste, and shorter production cycles, making it a game-changer for businesses. Growing demand for eco-friendly packaging, coupled with the rise of luxury, pharmaceutical, and food & beverage sectors, is fueling market expansion.

With innovation, sustainability, and brand differentiation at the forefront, the 3D printed packaging market is set to witness strong growth through 2032, reshaping how companies design and deliver packaging solutions worldwide.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/3d-printed-packaging-market-111126

List of Key 3D Printed Packaging Companies Profiled:

- Stratasys Ltd. (U.S.)

- 3D Systems Corporation (U.S.)

- Materialise NV (Belgium)

- EOS GmbH (Germany)

- SLM Solutions Group AG (Germany)

- Nexa3D (U.S.)

- Protolabs Inc. (U.S.)

- GE Additive (U.S.)

- Carbon, Inc. (U.S.)

- Desktop Metal, Inc. (U.S.)

Market Growth Drivers

Customization & Personalization – 3D printing enables brand owners to design packaging with unique textures, shapes, and labels, improving consumer engagement.

Sustainability Focus – The use of biodegradable and recyclable 3D printing materials aligns with the global shift toward eco-friendly packaging.

Rapid Prototyping & Efficiency – Businesses can quickly design, test, and modify packaging without high tooling costs.

E-commerce Expansion – The surge in online shopping is pushing demand for innovative, lightweight, and protective packaging.

Technological Advancements – Development in additive manufacturing, smart packaging, and biopolymers is accelerating adoption.

Market Segmentation

By Material

Bioplastics

Polymers (PLA, PET, ABS)

Paper-based composites

Others

By Application

Food & Beverages Packaging

Pharmaceutical & Healthcare Packaging

Cosmetics & Personal Care Packaging

Electronics & Consumer Goods Packaging

By Region

North America – Early adoption of 3D printing in packaging with strong R&D investment.

Europe – Strong focus on sustainability and eco-friendly packaging regulations.

Asia-Pacific – Fastest-growing market driven by manufacturing hubs in China, Japan, and India.

Rest of the World – Emerging markets adopting 3D printed packaging in niche industries.

Key Industry Trends

Growing use of smart 3D printed packaging with QR codes, RFID, and NFC tags for better traceability.

Increasing collaboration between 3D printing companies and packaging manufacturers .

Adoption of on-demand packaging production models to reduce warehousing costs.

Rising demand for luxury and premium packaging solutions in cosmetics and high-end beverages.

Competitive Landscape

Leading players in the 3D printed packaging market are investing in R&D, partnerships, and eco-friendly material innovation . Companies are also focusing on scaling production technologies to meet the growing demand for mass customization and sustainable packaging .

3D printed packaging refers to the creation of packaging materials using additive manufacturing, where objects are built layer by layer from a digital model. The market is witnessing strong growth, driven by advancements in 3D printing technologies and the increasing demand for sustainable and customized packaging solutions across industries. Both businesses and consumers are seeking unique designs that reflect individual preferences and brand identity. With its exceptional design flexibility, 3D printing enables the production of intricate, personalized packaging that traditional methods often cannot achieve. This trend is particularly evident in sectors such as cosmetics, luxury goods, and food & beverages, where packaging plays a crucial role in enhancing product appeal.

The 3D printed packaging market is set to expand significantly, supported by sustainability mandates, digital manufacturing innovations, and consumer-driven personalization trends . As industries continue to embrace additive manufacturing , the market is projected to play a crucial role in shaping the future of packaging .

Information Source: https://www.fortunebusinessinsights.com/3d-printed-packaging-market-111126

KEY INDUSTRY DEVELOPMENTS:

- In May 2024, Unilever—the consumer goods giant housing brands, such as Dove, Persil, and Ben & Jerry’s—adopted additive manufacturing to fulfill its prototyping requirements. Instead of printing prototypes of its product packaging directly, it has opted for a different approach by utilizing SLA 3D printing to create blow molding tools. This strategy, implemented in collaboration with packaging producer Serioplast and Formlabs, has significantly reduced product development timelines for new plastic bottle packaging and tooling expenses.

- In April 2024, Baralan partnered with 3D printing expert Stratasys and coatings specialist ICA to introduce GP3DPrint, a water-soluble 3D decoration service for cosmetic packaging. The initiative makes personalized, distinctive, and high-end decor available to a broader range of brands.

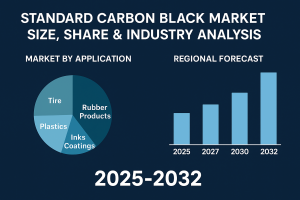

The global standard carbon black market was valued at USD 24.45 billion in 2024 and is expected to increase from USD 25.54 billion in 2025 to reach USD 35.21 billion by 2032 , reflecting a CAGR of 4.7% during the forecast period. In 2024, Asia Pacific emerged as the leading region , accounting for 58.11% of the total market share .

The Standard Carbon Black Market plays a crucial role in several industrial applications, ranging from tires and automotive components to plastics, coatings, and inks. Carbon black is produced through the partial combustion or thermal decomposition of hydrocarbons and is primarily used as a reinforcing agent, pigment, and performance enhancer. Unlike specialty carbon black, standard carbon black is widely consumed in bulk across multiple industries, making it a critical commodity in the global chemical and materials sector.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/standard-carbon-black-market-113664

LIST OF KEY STANDARD CARBON BLACK COMPANIES PROFILED

- Birla Carbon (India)

- Beilum Carbon Chemical Limited (China)

- Cabot Corporation (U.S.)

- Tokai Carbon Co., Ltd. (Japan)

- Omsk Carbon Group (Russia)

- OCI COMPANY Ltd. (South Korea)

- Orion Engineered Carbons SA (Luxembourg)

- Imerys (France)

- Himadri Speciality Chemical Ltd. (India)

- Longxing Chemical Stock Co., Ltd (China)

- Mitsubishi Chemical Group Corporation (Japan)

Market Dynamics

Drivers

Growing Tire and Rubber Industry – Standard carbon black is predominantly used in tire manufacturing as a reinforcing filler, enhancing strength, durability, and resistance. With the rising demand for automobiles globally, tire production is significantly boosting market growth.

Expanding Plastics and Coatings Applications – Its role as a black pigment in plastics, paints, coatings, and inks continues to drive market adoption.

Urbanization and Industrialization – Increasing construction activities and infrastructure projects stimulate demand for rubber-based products, construction coatings, and adhesives, all of which require standard carbon black.

Restraints

Volatility in Raw Material Prices – Dependence on petroleum-based feedstock leads to cost fluctuations, impacting overall production economics.

Environmental Concerns – Carbon black manufacturing emits greenhouse gases and particulate matter, leading to stringent environmental regulations that may hinder market expansion.

Opportunities

Sustainable Alternatives and Green Production Methods – Companies are investing in eco-friendly production technologies to reduce carbon footprints.

Emerging Economies – Rapid industrialization in Asia-Pacific, Latin America, and Africa offers significant untapped market potential.

Market Segmentation

By Grade

Furnace Black

Thermal Black

Channel Black

Acetylene Black

By Application

Tires & Industrial Rubber Products

Plastics

Coatings & Inks

Others (adhesives, sealants, etc.)

By End-Use Industry

Automotive

Construction

Packaging

Electronics

Others

By Region

Asia Pacific – Largest consumer, driven by tire manufacturing hubs in China, India, and Southeast Asia.

North America – Strong demand from automotive and construction industries.

Europe – Adoption of eco-friendly carbon black production processes.

Latin America & Middle East & Africa – Growing demand for rubber products and industrial applications.

Recent Industry Developments

Expansion Projects : Several manufacturers are setting up new production plants in Asia to meet the rising tire demand.

Sustainability Initiatives : Companies are investing in carbon capture technologies and renewable energy-based production processes.

The global Standard Carbon Black Market is expected to witness steady growth over the next decade, fueled by the continuous expansion of the tire industry, rising industrial applications, and increasing demand from emerging economies. With sustainability becoming a central theme, manufacturers are likely to invest heavily in cleaner technologies and green alternatives, shaping the future of this vital market.

Standard carbon black is a fine black powder produced through the partial combustion of hydrocarbons such as oil or natural gas. It serves as both a black pigment and a reinforcing agent across multiple industries, including rubber, plastics, inks, and coatings. Its importance lies in enhancing product durability, UV resistance, and color quality, making it especially valuable in applications like tires, rubber seals, and molded components.

Information Source: https://www.fortunebusinessinsights.com/standard-carbon-black-market-113664

KEY INDUSTRY DEVELOPMENTS

- January 2025: Mitsubishi Chemical, in collaboration with Sumitomo Rubber, launched a joint initiative to commercialize sustainable carbon black by recycling end-of-life tires using coke ovens, making the world’s first-ever commercialization of such a process.

- May 2023: Orion Engineered Carbons expanded its gas black production capacity at Dortmund and Cologne, Germany. This move reinforces the company’s leadership in specialty-grade carbon black solutions.

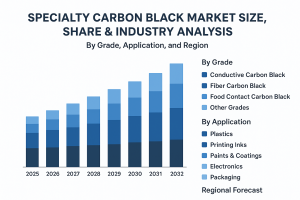

According to Fortune Business Insights, The global specialty carbon black market size was valued at USD 3.14 billion in 2024. The market is projected to grow from USD 3.31 billion in 2025 to USD 4.89 billion by 2032, exhibiting a CAGR of 5.7% during the forecast period. Asia Pacific dominated the specialty carbon black market with a market share of 57.00% in 2024.

The Specialty Carbon Black Market is witnessing robust growth, driven by rising demand across industries such as plastics, coatings, inks, and batteries. Unlike standard carbon black, specialty carbon black offers unique properties including enhanced tinting strength, UV protection, conductivity, and dispersibility, making it an essential material for advanced industrial applications. Specialty carbon black is a type of engineered carbon material designed with precisely controlled properties such as surface area, particle size, structure, and chemical composition. Produced through the regulated thermal decomposition of hydrocarbons, it differs from standard carbon black by offering advanced performance characteristics. These unique features make it ideal for demanding applications like conductive polymers, UV-protective coatings, and high-quality specialty inks.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/specialty-carbon-black-market-113665

What is Specialty Carbon Black?

Specialty carbon black refers to engineered carbon particles produced with precise control over parameters such as surface area, particle size, structure, and chemistry. Unlike commodity carbon black, specialty types are tailored for high-performance applications, offering benefits like conductivity, UV resistance, and enhanced color properties.

Key Market Drivers

Rising demand for high-performance plastics

Industries such as automotive, electronics, and packaging are adopting specialty carbon black to enhance properties like UV stability, conductivity, and durability.

Growth of electric vehicles (EVs) and electronics

EV batteries and advanced electronics require conductive and ultra-pure specialty carbon blacks to improve performance.

Sustainability and regulations

Growing environmental awareness and government regulations are encouraging the development of bio-based and recovered carbon black production methods that reduce emissions and reliance on fossil feedstocks.

Challenges & Restraints

High production costs due to the use of expensive feedstocks and advanced processing technologies.

Strict regulatory frameworks related to emissions, workplace safety, and carcinogenicity, increasing compliance costs for manufacturers.

Market Segmentation

By Grade : Conductive, Fiber, Food Contact, and Specialty Grades

By Application : Plastics, Printing Inks, Coatings, Batteries, Others

By End-Use Industry : Automotive, Packaging, Electronics, Construction, Textiles

Regional Insights

Asia-Pacific dominated in 2024 with a 57% market share, led by China’s large-scale manufacturing base and premium product demand in Japan and South Korea.

North America showed strong demand for advanced applications, particularly in electronics and automotive sectors.

Europe emphasized sustainable and regulatory-compliant grades, particularly for food contact and low-PAH applications.

Latin America and Middle East & Africa showed moderate growth, primarily relying on imports for high-end products.

Competitive Landscape

Major players shaping the specialty carbon black industry include:

- Cabot Corporation (U.S.)

- Birla Carbon (U.S.)

- Mitsubishi Chemical Group Corporation. (Japan)

- Continental Carbon Company (U.S.)

- Tokai Carbon Co., Ltd. (Japan)

- International CSRC Investment Holdings Co., Ltd (China)

- Imerys (France)

- Zaozhuang Jiarun Chemical Co., Ltd. (China)

- Orion Engineered Carbons GmbH (Germany)

- Beilum Carbon Chemical Limited (China)

Recent developments include Birla Carbon launching sustainable, battery-grade conductive carbon blacks and Cabot introducing masterbatches and reinforcing grades for EV tires that enhance tread durability and reduce rolling resistance.

Opportunities Ahead

Expanding use in EV batteries and charging infrastructure.

Scaling sustainable carbon black production through recovered materials and biomass-based feedstocks.

Growth in premium applications such as electronics, food packaging, and UV-resistant plastics.

The specialty carbon black market is projected to grow from USD 3.31 billion in 2025 to USD 4.89 billion by 2032, at a CAGR of 5.7%. Asia Pacific will remain the global growth engine, supported by rapid industrialization, rising EV adoption, and demand for both premium and cost-effective grades. The Specialty Carbon Black Market is poised for significant expansion as industries shift towards high-performance, sustainable, and technologically advanced materials. With its versatile applications in plastics, coatings, batteries, and inks, specialty carbon black is becoming a critical material for the future of automotive, electronics, and packaging sectors.

Information Source: https://www.fortunebusinessinsights.com/specialty-carbon-black-market-113665

KEY INDUSTRY DEVELOPMENTS

- April 2025 – Birla Carbon announced to showcase advanced, sustainable carbon-based solutions at Chinaplas 2025, targeting high-performance applications in plastics, electronics, cables, and fibers. These innovations aim to enhance product durability, aesthetics, and conductivity.

- February 2025 – Birla Carbon declared to introduce its latest battery-grade conductive carbon black, Conductex, at InterBattery in Seoul. Produced at its South Korean plant, it is designed for energy-intensive applications.

Nanocoatings Market Size and Opportunities in Automotive and Aerospace 2032

By ameliasss, 2025-09-12

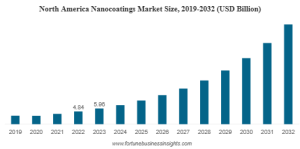

According to Fortune Business Insights, the global nanocoatings market was valued at USD 14.32 billion in 2023. The market is projected to grow from USD 17.54 billion in 2024 to USD 90.29 billion by 2032, registering an impressive CAGR of 22.7% during the forecast period. In 2023, North America dominated the market, accounting for 41.62% of the global share.

Nanocoatings are ultra-thin protective layers applied on surfaces to safeguard against dirt, dust, corrosion, water, bacteria, friction, and heat radiation. Increasing adoption across industries—particularly construction and automotive—is driving market expansion. Their role in promoting sustainability and energy efficiency further strengthens growth opportunities.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/nanocoatings-market-105023

Quick snapshot

2023 market value: USD 14.32 billion .

Forecast: USD 17.54 billion in 2024 → USD 90.29 billion by 2032.

CAGR (2024–2032): 22.7% .

2023 regional leader: North America ( 41.62% share).

List of Key Players Mentioned in the Report:

- P2i Ltd (U.K.)

- Nanovere Technologies LLC (U.S.)

- Nanofilm Ltd. (U.S.)

- ACTnano (Massachusetts, U.S.)

- Nanophase Technologies Corporation (U.S.)

- Tesla Nanocoatings Inc. (U.S.)

- Cleancorp (Australia)

Report Coverage

This report delivers comprehensive insights into the global nanocoatings market , backed by extensive primary and secondary research. Market size estimations were derived through in-depth interviews with key stakeholders across the value chain, combined with access to both global and regional paid databases. The study provides reliable data at country, regional, and global levels , helping businesses make well-informed investment and strategic decisions.

Market Segmentation

By Type

Antimicrobial

Self-Cleaning (expected to hold the largest share)

Anti-Fingerprint

Anti-Corrosion

Others : includes photocatalytic, hydrophobic, superhydrophobic, anti-fouling, abrasion-resistant, thermal barrier, and anti-icing coatings

By Application

Building & Construction (dominant segment)

Automotive

Aerospace

Electronics

Marine

Others : includes medical, healthcare, food packaging, and energy applications

By Region

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Market Drivers and Restraints

Key Growth Driver

Strong demand from building & construction :

Nanocoatings are increasingly adopted in the construction industry due to their self-assembly properties and superior performance compared with conventional coatings. They provide effective protection for surfaces such as glass, concrete, marble, and limestone against staining, corrosion, abrasion, and other environmental factors.

Major Restraint

High equipment and technology costs :

Advanced machinery and processes are required for the effective application of nanocoatings. The relatively high investment costs may hinder adoption, particularly in cost-sensitive markets.

Regional Insights

North America – Market Leader

North America accounted for USD 3,188.6 million in 2020 and is projected to maintain its leading position throughout the forecast period. Growth in the region is strongly influenced by government subsidies, interest rate trends, construction activity, and consumer spending , all of which play a significant role in shaping GDP and driving nanocoatings adoption.

Asia Pacific – Fastest Growing Market

Asia Pacific is expected to secure a substantial share of the global nanocoatings market, supported by rapid growth in construction projects and industrial sector expansion . Rising infrastructure development and manufacturing activity will continue to stimulate demand in this region.

Europe – Strong Automotive Base

Europe represents another key region, underpinned by its well-established automotive industry . Countries such as Germany, Italy, France, and the U.K. remain major automobile producers, creating steady demand for nanocoatings to enhance durability, protection, and performance.

Competitive Landscape

The competitive environment of the nanocoatings market is shaped by strategic moves from key players , including:

Mergers and acquisitions to expand market reach.

Product launches to introduce advanced, sustainable coatings.

Collaborative partnerships to strengthen technology integration.

Agreements with government bodies to secure large-scale projects.

Such business developments directly influence market dynamics, either accelerating growth opportunities or reshaping the competitive balance.

Market highlights

Construction is a major growth engine due to demand for durable, low-maintenance surfaces and energy-saving finishes.

Automotive uptake is rising, particularly for abrasion-resistant and protective coatings.

Sustainability and lifecycle extension of products are key value propositions boosting market adoption.

Information Source: https://www.fortunebusinessinsights.com/nanocoatings-market-105023

Key Industry Developments

December 2023 – NANOFILM Technologies International expanded into the European market through a USD 9.9 million partnership with AxynTeC Dunnschichttechnik (Germany) . AxynTeC specializes in coating solutions for industrial and medical applications using its patented thin-film technologies. With this collaboration, Nanofilm aims to strengthen its presence in Europe while offering advanced coating services and thin-film equipment solutions.

January 2020 – P2i introduced a new halogen-free barrier coating range designed for PCB-enabled OEMs. This sustainable and reworkable solution is targeted at the automotive and consumer electronics sectors . By eliminating hazardous chemicals and extending product lifespans, the new coating helps OEMs reduce their environmental footprint while enhancing durability and performance.

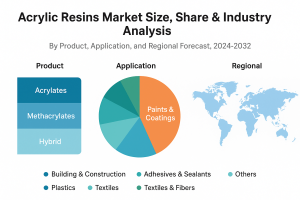

According to Fortune Business Insights, The global acrylic resins market was valued at USD 22.36 billion in 2023 and is expected to expand from USD 23.46 billion in 2024 to USD 33.84 billion by 2032, registering a CAGR of 4.8% during the forecast period. In 2023, Asia Pacific led the market, accounting for 44.81% of the global share. Meanwhile, the U.S. market is anticipated to witness substantial growth, projected to reach USD 5.54 billion by 2032, fueled by robust demand in the paints and coatings industry and ongoing infrastructure development projects.

The global Acrylic Resins Market is witnessing significant growth due to its wide applications in paints & coatings, adhesives, construction, automotive, and packaging industries. Acrylic resins, known for their durability, transparency, weather resistance, and excellent adhesion, are increasingly being adopted in industrial and consumer applications. Rising demand for sustainable and high-performance materials is expected to drive market expansion during the forecast period.

Market Size & Forecast

In 2023, the market was valued at USD 22.36 billion.

It is projected to grow to around USD 23.46 billion in 2024.

By 2032, the market is forecast to reach USD 33.84 billion, at a CAGR of ~4.8% between 2024 and 2032.

This reflects robust but not explosive growth, suggesting stable demand across industries with certain drivers pushing upward.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/acrylic-resins-market-105159

LIST OF KEY COMPANIES PROFILED

- Dow (US)

- BASF SE (Germany)

- Arkema S.A. (France)

- Mitsubishi Chemical Holdings (Japan)

- Nippon Shokubai (Japan)

- DSM (Netherlands)

- Mitsui Chemicals (Japan)

- DIC Corporation (Japan)

- Sumitomo (Japan)

Market Growth Drivers

Booming Construction and Infrastructure Sector: Acrylic resins are widely used in architectural coatings, sealants, and adhesives, supporting urbanization and infrastructure development.

Automotive Industry Growth: Increasing vehicle production and the rising need for high-performance coatings are fueling demand.

Sustainability Focus: Shift towards eco-friendly, water-based, and bio-based acrylic resins is creating new opportunities.

Packaging Industry Expansion: Strong demand for lightweight, durable, and flexible packaging materials is boosting market growth.

Key Market Trends

Shift to Waterborne Acrylic Resins – Growing environmental regulations are driving the adoption of low-VOC and sustainable resins.

Increased R&D Investments – Manufacturers are focusing on innovative formulations to enhance UV resistance, adhesion, and durability.

Rising Popularity in 3D Printing and Electronics – Acrylic resins are finding emerging applications in advanced manufacturing.

Market Segmentation

By Type

Thermoplastic Acrylic Resins

Thermosetting Acrylic Resins

By Application

Paints & Coatings (largest segment)

Adhesives & Sealants

Packaging Materials

Automotive Parts & Components

Construction Materials

Others

Regional Insights & Dominance

Asia Pacific is the dominant region, accounting for ~44.81% of the global market share in 2023.

The region’s dominance stems from rapid infrastructure growth, urbanisation, rising automotive production, and strong demand in paints & coatings, especially in China, India, and Southeast Asia.

United States is expected to see significant growth, with market size projected to reach USD 5.54 billion by 2032 , powered by demand for high-durability coatings and infrastructural development.

Other regions—Europe, Middle East & Africa, and Latin America—also present opportunities, primarily in applications like adhesives & sealants, specialty coatings, and innovations in resin chemistry.

Competitive Landscape

The market is moderately fragmented, with global and regional players focusing on product innovation and strategic partnerships. Major companies are investing in sustainable resin production to meet evolving environmental regulations. Mergers, acquisitions, and collaborations are common strategies to expand global reach.

The Acrylic Resins Market is projected to grow steadily through 2032, supported by increasing demand for high-performance, durable, and eco-friendly materials. With strong adoption in paints & coatings, automotive, construction, and packaging, the industry is set to witness robust expansion globally.

Information Source: https://www.fortunebusinessinsights.com/acrylic-resins-market-105159

KEY INDUSTRY DEVELOPMENTS

- March 2024 – DIC Corporation's subsidiary, IDEAL CHEMI PLAST PRIVATE LTD., opened a new production facility for coating resins in Maharashtra's Supa Japanese Industrial Zone. The facility tripled the production capacity of IDEAL CHEMI PLAST, positioning it to expand its business in India, South Asia, and the Middle East.

- March 2021 – BASF doubled its capacity for acrylic dispersions at its new production line in Pasir Gudang, Malaysia. The line features condensate stripping recovery technology that reduces freshwater consumption and wastewater generation, contributing to the company's environmental commitment.