According to Fortune Business Insights, The global biodegradable mulch film market size was valued at USD 63.8 million in 2023. The market is projected to grow from USD 68.0 million in 2024 to USD 126.8 million by 2032 at a CAGR of 8.1% during the 2024-2032 forecast period. Asia Pacific dominated the biodegradable mulch film market with a market share of 35.89% in 2023.

Growth in the consumption of agricultural produce globally is driving the demand for mulch films which can be easily decomposed in the soil. Biodegradable mulch films market size is set to gain traction as mulching has become a core foundation for growing vegetables, grains, fruits, flowers, and other various crops. Mulching has the ability to cover the soil which creates a promising environment for plant growth. These films have proven themselves to be a solid alternative to polyethylene films in the agriculture industry.

Fortune Business Insights presents this information in their report titled " Biodegradable Mulch Films Market, 2024–2032."

Request a FREE Sample Copy Of Biodegradable Mulch Film Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/biodegradable-mulch-film-market-102759

List of Top Biodegradable Mulch Film Companies:

- BASF SE (Germany)

- Kingfa Sci & Tech Co Ltd (China)

- BioBag International AS (Norway)

- Novamont AB (Italy)

- SOLOS POLYMERS PVT. LTD. (India)

- Ved Industries (India)

- Tilak Polypack (India)

- Olive Industries (India)

Segments:

Based on the material, the market is studied startch, PBAT (poly(butylene adipate-co-terephthalate)), PBS (polybutylene succinate), PLA (polylactic acid), cellulose, and others. PLA (polylactic acid) bags the leading share as they are highly stretchable and can be blended easily with vegetable waste. Easy decomposition makes this material a preferred one amongst the consumers.

On the basis of application, the market is segmented into fruits & vegetables, flowers & plants, grains & oilseeds. The fruits & vegetables leads the market share with escalated demand for consuming food products. Increase in the levels of disposable income of the population is also driving the demand for nutritious food.

From the regional ground, the market is segmented into North America, Latin America, Europe, Asia Pacific, and Middle East & Africa.

Report Coverage

The comprehensive market research report delves into crucial elements, including the competitive landscape, end-users, and product type. The document provides valuable insights into prevailing market trends and significant industry advancements. It also encompasses a wide range of variables that have contributed to the recent expansion of the market. With a thorough examination of these factors, the report offers a holistic view of the market's current state and future potential. Stakeholders can leverage this information to make informed decisions and formulate effective strategies for success.

Drivers & Restraints

Easy Decomposition And Reduced Labor Effort To Fuel The Market Augmentation

Biodegradable mulch films are proving themselves to a perfect alternative to polyethylene films which are used for weed control and improve crop productivity. The decomposing of these mulch films takes around 30-120 days which reduces the labor costs as the effort to remove the films after the harvesting gets eliminated. In addition, these films reduces the plastic waste which is usually generated when traditional films are used. These above factors are responsible for fueling the biodegradable mulch films market growth.

On the other hand, market growth gets hampered with the high prices allocated to these films which can create a burden on small-scale farmers.

Regional Insights

Asia Pacific Dominates the Market Owing to the High Levels of Population

Owing to augmenting levels of population in the developing countries such as India and China, the Asia Pacific region takes the lead in the biodegradable mulch films market share. The region is the powerhouse for largest agricultural food producing countries which is also propelling the market growth.

Latin America depicts the noteworthy growth owing to the presence of established food importers. Brazil and Mexico are the leading food importers of this region.

European market is set to growth moderately with growing awareness for the use of these mulch films amongst the farmers

Information Source: https://www.fortunebusinessinsights.com/biodegradable-mulch-film-market-102759

Competitive Landscape

New Product Launched by Key Market Players to Enhance Their Market Positions

The leading players of the biodegradable disposable plate market are adopting various strategies to extend their product portfolio by launching new products and collaborating with other organizations. They are expanding their production capacity and partnering up to boost their brand presence and gain edge over the competition.

Key Industry Development

- October 2023: Mondi and Cotesi collaborated for the development of Advantage Kraft Mulch which is a paper alternative to plastic mulching film commonly used to protect plants from birds and weather impacts. It is made with 100% kraft paper manufactured from wood with no plastic or coating.

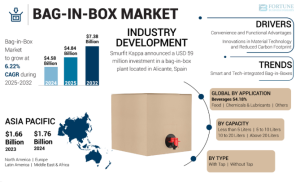

According to Forrtune Business Insights, In 2024, the global bag-in-box market was valued at USD 4.58 billion. It is expected to increase to USD 4.84 billion in 2025 and further reach USD 7.38 billion by 2032, registering a compound annual growth rate (CAGR) of 6.22% throughout the forecast period. The United States is poised to experience substantial growth in this sector, with its market projected to hit USD 1.82 billion by 2032. This upward trend is primarily driven by the rising need for affordable, lightweight, and eco-friendly packaging options, especially in the food and beverage sectors. In 2024, Asia Pacific led the global bag-in-box market, capturing a dominant share of 38.43%.

The bag-in-box (BIB) industry encompasses the manufacturing, distribution, and usage of flexible packaging systems designed for storing and dispensing liquid and semi-liquid products. This packaging format features a durable plastic bag—often constructed from multiple layers of metalized films or other plastic materials—housed within a robust outer box made of corrugated fiberboard.

Request a FREE Sample Copy of Bag-in-box Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/bag-in-box-container-market-102313

Segmentation & Dynamics

Capacity

Less than 5 liters holds the largest share, favored for its compact, lightweight design and portability.

5 to 10 liters follows, commonly used in institutional or commercial settings where larger but manageable volumes are needed.

Type

With tap formats dominate, enabling precise pouring and reducing waste—especially valuable in foodservice and hospitality environments.

Without tap versions are more cost-effective and serve markets where simplicity and pricing are priorities.

Applications

The beverages segment —including wine, dairy, juices—is the largest end-use category, as bag‑in‑box packaging offers superior shelf life and sanitary dispensing.

Food products like edible oils benefit from protection against light and oxygen, extending freshness.

Other applications extend to chemicals and lubricants , and a variety of non‑food uses.

Regional Landscape

The Asia Pacific region led the market in 2024 with a share of 38.43% , reflecting the rapid urbanization and growing middle class in China, India, and Southeast Asia.

Additional perspectives:

Europe accounted for over 43.8% of revenue in 2023, driven by strong consumer demand in food and beverage sectors, particularly in wine markets.

The Asia Pacific region is also growing fast, with a CAGR of around 7.9% predicted through 2030.

Growth Drivers & Challenges

Key Growth Drivers

Convenience and cost effectiveness : Lightweight design, ease of transport, efficient space usage, and functional dispensing (especially with taps) enhance appeal.

Sustainability trends : Bag‑in‑box systems use less material and reduce transportation emissions compared to rigid packaging, aligning with eco-conscious consumer preferences and sustainability goals.

Smart packaging innovations : The integration of RFID, QR codes, and sensor technologies helps monitor freshness and streamline inventory—especially important for perishables.

Restraining Factors

Recyclability concerns : Multilayer materials used in bag‑in‑box packaging can be hard to recycle in areas without sufficient waste infrastructure.

High upfront investment : Specialized filling, sealing, and handling equipment can pose barriers for smaller manufacturers or entrants.

Competitive Landscape & Market Players

Top companies shaping the space include:

Amcor plc

International Paper

Scholle IPN Corp

Sealed Air Corporation

DS Smith PLC

Smurfit Kappa

Notable developments:

In February 2024 , Smurfit Kappa invested €54 million (approx. USD 59 million) to build a bag‑in‑box plant in Alicante, Spain, emphasizing sustainability.

Other players like Aran Group and WestRock are also expanding through acquisitions and new facilities to strengthen market presence.

Summary

| Aspect | Insight |

|---|---|

| Market Size | USD 4.84 billion (2025) → USD 7.38 billion (2032) |

| Growth Rate | CAGR of 6.22% (2025–2032) |

| Top Regions | Asia Pacific (38.4%), Europe dominates in food/bev |

| Applications | Beverages lead; food, chemicals follow |

| Drivers | Convenience, sustainability, smart packaging |

| Challenges | Recycling complexity, capital investment |

| Leading Players | Amcor, Scholle IPN, Smurfit Kappa, etc. |

Information Source: https://www.fortunebusinessinsights.com/bag-in-box-container-market-102313

KEY INDUSTRY DEVELOPMENTS:

- February 2024 – Smurfit Kappa announced a €54 million (USD 59 million) investment in a bag-in-box plant located in Alicante, Spain. This investment is set to strengthen the sustainability of both the plant’s operations and the company’s product portfolio.

- February 2024 – Aran Group announced the completion of the acquisition of a majority stake in IBA Germany from previous owner Liquid Concept GmbH (LC).

The bag-in-box packaging market is poised for significant growth, driven by sustainability demands, technological progress, and increasing adoption in beverage, foodservice, and industrial sectors. Europe currently leads the market, but Asia-Pacific is rapidly emerging as a growth engine. With ongoing innovation and strategic investments, the BiB format is becoming an essential component of modern packaging solutions.

According to Fortune Business Insights, In 2023, the global home care packaging market was valued at USD 32.55 billion and is expected to grow to USD 34.11 billion in 2024, eventually reaching USD 52.22 billion by 2032, at a CAGR of 5.47% over the forecast period. North America led the market with a 33.49% share in 2023. The U.S. home care packaging market is anticipated to experience steady growth, projected to reach USD 14.52 billion by 2032. This growth is primarily driven by increasing consumer demand for eco-friendly and convenient packaging solutions for household cleaning and personal care products.

Home care packaging plays a vital role in protecting contents from microbial contamination while ensuring optimal safety and efficiency during storage and transportation. Growing health awareness has led consumers to spend more time at home, fueling demand for cleaning and disinfectant products and driving global market growth. Additionally, the increasing adoption of flexible packaging and a heightened focus on consumer-centric packaging solutions are further contributing to the expansion of the global market.

Fortune Business Insights presents this information in their report titled " Homecare Packaging Market , 2024-2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/homecare-packaging-market-108080

Major Players Profiled in the Report:

- Amcor PLC (Australia)

- Sonoco Products Company (U.S.)

- Ball Corporation (U.S.)

- Berry Global (U.S.)

- AptarGroup Inc. (U.S.)

- Silgan Holdings (U.S.)

- Constantia Flexibles (Austria)

- DS Smith PLC (U.K.)

- ProAmpac LLC (U.S.)

- Mondi Group (U.K.)

Segments:

By material, the market is divided into metal, glass, plastic, and paper & paperboard.

By packaging type, the market is segregated into jars & containers, bags & pouches, bottles, boxes, cans, and others.

By type, the market is classified into laundry, dishwashing, aifresheners, surface cleaners, toiletries, and others.

From the regional ground, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Report Coverage

The comprehensive market research report delves into crucial elements, including the competitive landscape, distribution channels, and notable product categories. The document provides valuable insights into prevailing market trends and significant industry advancements. It also encompasses various variables that have contributed to the recent market expansion. With a thorough examination of these factors, the report offers a holistic view of the market's current and future potential. Stakeholders can leverage this information to make informed decisions and formulate effective strategies for success.

Drivers and Restraints

Rapid Adoption of Flexible Packaging for Smooth Product Handling to Propel Market Expansion

People are more aware of hygiene and sanitation in developed countries. Infrastructural development is attributed to the rapid urbanization and rising disposable income. An increase in retail stores is boosting the demand for eye-catching packaging of products to entice consumers. Producers are also opting for innovative designs to enhance the aesthetics of homecare packaging and improve brand identity. There is an increased adoption of eco-friendly products and packaging, and governments are also encouraging the usage of such products and imposing limitations on non-recyclable and non-biodegradable products. The growing usage of paper and paperboard as raw materials for packaging and the rapid adoption of flexible packaging for the smooth handling and shipping of products are key factors boosting the homecare packaging market share.

On the other hand, chemicals used to make homecare products can harm the environment, damage the skin, and cause irritation and other health-related difficulties. All these factors are impeding market growth.

Regional Insights

Asia Pacific Commands the Market Due to Rising Disposable Income

Asia Pacific takes center stage in the global market. An increase in population and rising disposable income drive the demand for homecare products, bolstering market expansion in the region.

The market in North America is expanding rapidly owing to increasing consumer inclination toward a clean and better lifestyle.

Competitive Landscape

Top Companies Focus on Partnerships to Introduce Sustainable Homecare Packaging Solutions

Leading companies emphasize partnerships to increase their product offerings. They are investing in R&D programs to launch sustainable packaging solutions to reduce the environmental impact. Top homecare packaging solution providers are focusing on product improvements and acquisitions to hold dominance in the global market.

Information Source: https://www.fortunebusinessinsights.com/homecare-packaging-market-108080

Key Industry Developments

- February 2024 – Mondi, a global leader in sustainable packaging and paper, announced the expansion of its innovative range of paper-based EcoWicketBags. The new range comes in response to the rising demand for sustainable packaging in the home & personal care (HPC) sector, especially for products such as diapers and feminine hygiene products.

- January 2024 – M&S partnered with Reposit and declared the expansion of its Refilled scheme for own-brand cleaning & laundry products with an intent to cut down plastic packaging and offer its consumers sustainability-minded alternatives. The consumers can choose from ten pre-filled, own-brand homecare products such as washing liquids, laundry detergents, cleaning sprays, and fabric conditioners.

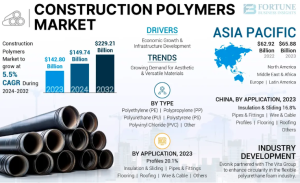

According to Fortune Business Insights, The global construction polymers market size was valued at USD 142.80 billion in 2023. The market is projected to grow from USD 149.74 billion in 2024 to USD 229.21 billion by 2032 at a CAGR of 5.5% during the forecast period. Asia Pacific dominated the construction polymers market with a market share of 46.13% in 2023.

Construction polymers, including elastomers, resins, and plastics, are vital in modern construction due to their durability and versatility. They withstand harsh conditions while promoting sustainability, such as improving energy efficiency in insulation. The market is expected to ramp up owing to rising adoption of such products in diverse applications, such as profiles and wire & cable.

Fortune Business Insights™ provides this information in its research report, titled “ Construction Polymers Market, 2024-2032”.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/construction-polymers-market-110702

List of Key Players Mentioned in the Report:

- B. Fuller Company (U.S.)

- Solvay S.A. (Belgium)

- BASF SE (Germany)

- Evonik Industries AG (Germany)

- Reliance Industries Limited (India)

- SABIC (Saudi Arabia)

- Exxon Mobil Corporation (U.S.)

- Eni S.p.A (Italy)

- TotalEnergies (France)

- Avient Corporation (U.S.)

Segmentation:

Polyvinyl Chloride (PVC) Segment Dominated due to Technological Advancements

On the basis of type, the market is fragmented into Polyethylene (PE), Polypropylene (PP), Polyurethane (PU), Polystyrene (PS), Polyvinyl Chloride (PVC), and others. In 2023, the Polyvinyl Chloride (PVC) segment secured the key construction polymers market share as advances in polymer technology enhanced PVC's functionality and environmental profile.

Pipes & Fittings Segment Dominated owing to Diverse Applications

In terms of application, the market is fragmented into profiles, pipes & fittings, insulation and sliding, flooring, roofing, wire & cable, and others. In 2023, the pipes & fitting segment captured the key construction polymers market share. The wide range of applications, including water supply, plumbing, and HVAC systems, supports continued demand for polymer-based pipes and fittings.

Polymers can be tailored to a variety of specifications, making them suitable for a vast array of construction applications, from insulation, sealants, and coatings to more structural components such as polymer concrete and composites.

In terms of region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The research report offers:

- Detailed examination of market trends and notable industry developments.

- Comprehensive coverage of factors contributing to recent market growth.

- Identification of emerging opportunities and challenges within the market.

- Evaluation of key market players, their strategies, and market positioning.

- Analysis of technological advancements shaping the market landscape.

Drivers and Restraints:

Economic Growth and Infrastructure Development to Impel Market Growth

The growing number of infrastructure developments, such as highways, bridges, and high-rise buildings, drives up demand for versatile and lightweight construction polymers. Moreover, economic growth boots the need for new residential, commercial, and public infrastructure, further increasing the demand for the product.

However, new government regulations aimed at environmental sustainability and safety may restrict the use of certain polymers, increasing costs and limiting construction polymers market growth.

Regional Insights:

Asia Pacific Dominated the Market Owing to Increasing Polymer Consumption in India

In 2023, Asia Pacific region led the construction polymers market and was valued at USD 65.88 billion in 2023. The region’s market growth is driven by China's manufacturing dominance and India’s increased polymer consumption due to industrialization and rising incomes.

Latin America's market growth is attributed to the rising demand for roofing and profiles in new construction projects, particularly in Mexico, Argentina, and Brazil, which are major market drivers.

Competitive Landscape:

Industry Participants Focus on Investments to Boost Product Performance

The competitive landscape shows a consolidated market where global players invest heavily in advanced technologies to enhance product performance. Key strategies include developing novel technologies and pursuing acquisitions and expansions to boost market share.

Information Source: https://www.fortunebusinessinsights.com/construction-polymers-market-110702

Key Industry Development:

- December 2023 – Reliance Industries Limited (RIL) became the first Indian company to chemically recycle plastic waste-based pyrolysis oil into International Sustainability & Carbon Certification (ISCC)-Plus certified Circular Polymers. This milestone demonstrates its commitment to reducing plastic waste and supporting the Circular Economy in India.

- September 2023 – ExxonMobil's Baytown Texas facility started new chemical production units. The new performance polymers line would produce 400,000 metric tons per year of Vistamaxx and Exact branded polymer modifiers, enhancing the performance of various chemical products used in automotive parts, construction materials, and packaging applications.

Bio-Based Polypropylene Market Investment Opportunities and Risk Analysis 2025-2032

By ameliasss, 2025-08-06

According to Fortune Business Insights, The global bio-based polypropylene market size was USD 183.5 million in 2023 and is projected to grow from USD 255.8 million in 2024 to USD 3,824.1 million by 2032 at a CAGR of 39.9% during the forecast period (2024-2032). Europe dominated the bio-based polypropylene market with a market share of 51.5% in 2023.

Bio-based polypropylene (PP) is a polymer compound derived from plants and has balanced properties as standard polypropylene. This polymer is manufactured from materials such as corn, vegetable oils, and sugarcane. This polymer is a sustainable alternative to traditional synthetic polypropylene that is used with other material such as fiberglass for several applications. These applications include injection molding, and films for packaging, textiles.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/bio-based-polypropylene-market-102758

LIST OF KEY COMPANIES PROFILED

- Mitsui Chemicals, Inc. (Japan)

- LyondellBasell Industries Holdings B.V. (The Netherlands)

- NaturePlast (France)

- Neste Oyj (Finland)

- Borealis AG. (Austria)

- Braskem (U.S.)

Braskem America Introduces Green Polypropylene

Braskem, one of the leading bio-polymer producers in the world, announced the release of ‘I’m green’ recycled green polypropylene (PP) in October 2019. Representing one of the first bio-based polypropylene formulations under the ‘I’m green’ portfolio, the recycled PP offering is aimed at advancing Braskem’s commitment to transform the linear economy of plastics into a circular one. The ‘I’m green’ umbrella brand of Braskem also includes post-consumer-recycled (PCR) resins, bio-based resins, and a mix of bio-plastics and PCR solutions. The launch of the novel bio-based PP will enable Braskem to firmly secure its position in the bio-plastics industry as well as cater to a wide range of end-user industries.

Widening Application of Bio-based PP in Auto Manufacturing to Fuel the Market

Conventionally formulated polypropylene has been one of the mainstay raw materials adopted by vehicle manufacturers to make cost-efficient interior components. However, with an increasing emphasis on improving the sustainability quotient in the auto industry, auto companies are steadily transitioning towards biodegradable materials to make their vehicles lightweight and energy-efficient. Bio-based polypropylene is speedily becoming the preferred choice of material for automakers due to its high recyclability and biodegradability. For example, General Motors has been utilizing bio-based PP for seatbacks in its Cadillac DeVille and PP derived from flax for its trim and shelving in the Chevrolet Impala. Similarly, Toyota uses bio-PP for injection molded parts such as scuff plates and interior trims. The opportunities for organically derived PP are, thus, immense in the auto industry.

Packaging Segment to Dominate Market Share

On the basis of application, the market has been segregated into building & construction, consumer goods, packaging, and others. Among these, the packaging segment dominated the market in 2020 and will retain its commanding position due to the increasing demand for eco-friendly packaging materials from the food & beverage industry. The automotive segment is also anticipated to enlarge its share of 12.32% in the global market and a share of 11.83% in the Germany market in the forthcoming years.

By region, this market has been grouped into North America, Europe, Asia Pacific, and the Rest of the World.

Europe Market Registers USD 29.7 Million in Value in 2020

- Among regions, Europe is forecasted to lead the bio-based polypropylene market share on account of the growing adoption of naturally derived polymers in the region’s robust auto sector. This adoption trend is also fuelled by the EU’s commitment to becoming carbon neutral within the next couple of decades. In 2020, the Europe market size stood at USD 29.7 million .

- The booming demand for individual passenger cars in developing nations will foster enduring growth of the market in Asia Pacific.

- In Brazil, rapid urbanization and the sterling growth of the domestic consumer goods industry will propel the demand for bio-based polypropylene in Latin America.

Information Source: https://www.fortunebusinessinsights.com/bio-based-polypropylene-market-102758

Strategic Partnerships to Enable Key Players to Expand Geographic Presence

Key players in this market are strategically partnering with different companies in a bid to expand their presence and operations across diverse geographies. Moreover, companies are also making heavy investments in research & development activities to create inventive bio-PP solutions and widen their business horizons, both regionally and internationally.

Industry Development

- March 2023: Borealis started production of polypropylene based on Neste-produced renewable feedstock at the production facilities in Kallo and Beringen, Belgium. Borealis has replaced fossil fuel-based feedstock in large-scale commercial production of PP.

- June 2019: LyondellBasell, a producer of plastics, and Neste, the producer of renewable diesel from waste and residues, announced the parallel production of bio-PP and bio-based low-density polyethylene at a commercial scale. The joint project used Neste's renewable hydrocarbons derived from sustainable bio-based raw materials, such as waste and residue oils.

The global pultrusion market size is projected to experience dynamic growth in the forthcoming years owing to the increasing demand for light-weight materials across the world, finds Fortune Business Insights™ in its report, titled “ Pultrusion Market, 2025-2032 ”.

Pultrusion process is a highly automated incessant fiber laminating process used to produce high fiber volume profiles with a constant cross section. There has been an increasing demand for light-weight materials across the world owing to the economic way of impregnating and curing materials. This has resulted in the increasing demand for pultrusion across several regions of this market.

However, the cost of raw materials is very expensive, which is projected to hinder the growth of this market.

List of Key Players Covered in Pultrusion Market Report :

The global pultrusion market consists of global & regional players operating. Some of the key players in the market include and Strongwell Corporation, Bedford Reinforced Plastics, Excel Composites, Diversified Structural Composites, Faigle Kunstsoffe GmbH others .

Request Sample PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/pultrusion-market-104580

Market Segmentation:

On the basis of type, this market is divided into carbon fiber, glass fiber, and others. Based on application, the market is classified into housing, industrial, civil engineering, consumers, and others. By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America and the Middle East & Africa.

Highlights/Summary:

This research report offers an in-depth study of the driving factors, restraints and trends influencing the growth of the market. In addition, this report offers a detailed evaluation of the market segments and regional developments in the market. Further, this report also incorporates a comprehensive analysis of the strategies adopted by market players to strengthen their position.

Drivers/Restraints:

Rising Demand for Pultruded Parts across the World to Fuel the Market

There has been an increasing demand for pultruded parts around the world owing to their utilization in several industries such as housing, industrial, chemicals, and others, which is anticipated to augment the growth of this market. Further, the rising investments by key companies in the chemicals industry have led to the propelling of this market across several regions.

Regional Insights:

Growing Demand for Pultrusion Procedure to Boost the Asia Pacific Market Growth

Asia Pacific region is considered to dominate in the pultrusion market share on account of the increasing demand for pultrusion process from the countries such as India and China.

North America region is projected to grow steadily in this market due to the increasing initiatives of the manufacturing companies present in the U.S.

Europe is expected to grow rapidly in this market due to the fast growth of the chemicals and materials industries in this region.

Competitive Landscape:

Strategic Alliances to Feed Market Competition

Key market players are actively collaborating with their competitors to strengthen their manufacturing and production capabilities for the pultrusion process. Moreover, such partnerships are allowing the key companies to widen their position in the market and expand their business foothold.

Information Source: https://www.fortunebusinessinsights.com/pultrusion-market-104580

Industry Developments:

April 2018 : Excel Composites announced the acquisition with DSC, a subsidiary of Teijin Carbon America. DSC primarily uses pultrusion for carbon fiber and glass fiber reinforced thermoset products.

March 2017 : Diversified Structural Composites Inc., (DSC) announced the exhibition of its pultruded composites at JEC World 2017. The products include pultruded composite profiles known as pultrusions for automobile applications.

N-Propanol Market Value to Reach USD 2.37 Billion by 2032, Key Drivers Explored

By ameliasss, 2025-08-05

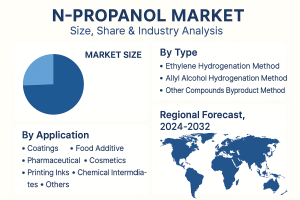

According to Fortune Business Insights, The global n-propanol market size was USD 1,613.1 million in 2023 and is projected to grow from USD 1,684.9 million in 2024 to USD 2,374.1 million in 2032 at a CAGR of 4.3% during the forecast period (2024-2032). Asia Pacific dominated the N-propanol market with a market share of 33.3% in 2023. Moreover, the n-propanol market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 634.0 million by 2032, driven by increasing demand for paints & coatings from the building & construction and automotive industries.

The increasing demand for paints & coatings from the building & construction and automotive industries is the primary factor driving market growth. The need for alcohol in emerging economies is projected to grow rapidly due to rising industrialization and urbanization activities.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/n-propanol-market-105137

LIST OF KEY COMPANIES PROFILED

- BASF (Germany)

- Dow (U.S.)

- Eastman (U.S.)

- Oxea (Germany)

- Sasol (South Africa)

- Wu Jiang Chemical (China)

- Nanjing Rongxin Chemical (China)

- Chang Chun Group (China)

- Ningbo Juhua Chemical (China)

- Zibo Nalcohol Chemical (China)

Market Segmentation

By Production Method

The ethylene-hydrogenation method dominates the market due to its better efficiency and yields. The allyl-alcohol hydrogenation and by-product routes are also expanding, particularly in the coatings and adhesive sectors.

By Application

Coatings and solvents (automotive and industrial paints, inks, adhesives) command a primary share, driven by packaging, construction, and textile inks.

Pharmaceuticals follow, using N-propanol as a high-purity solvent, antiseptic, intermediate, and excipient.

Cosmetics and personal care, food additives, and printing inks also represent significant growing segments.

By Product Grade and Purity

Pharmaceutical-grade accounted for approximately 35% of revenue in 2023. Industrial-grade is projected to grow fastest in the forecast period.

High-purity forms (99.5–99.99%) are increasingly demanded in electronics and semiconductor applications.

Regional Outlook

Asia-Pacific leads with over 45% global market share in 2023, supported by China and India’s expanding chemical, construction, pharmaceutical, and automotive industries. Growth rates in APAC are strong, with India showing a 14% rise in pharmaceuticals.

North America holds roughly 21% share, driven by U.S. demand in coatings, printing inks, specialty chemicals, and industrial cleaning.

Europe, with approximately 28% share, benefits from the demand for low-VOC and bio-based solvents, reinforced by REACH regulation and green chemistry policies.

MEA and Latin America are emerging markets, projected at around 6% share, supported by infrastructure investment in petrochemical diversification across regions such as the GCC, South Africa, and Brazil.

Key Growth Drivers

Industrial Demand : Widespread use in coatings, adhesives, inks, cleaners, and intermediates such as propylene oxide for polyurethane and plastics.

Pharmaceutical and Personal Care Expansion : Rising drug production and cosmetics formulations are driving solvent usage at high purity levels.

Sustainability Trends : Increasing shift to bio-based production routes of N-Propanol appeals to eco-conscious consumers and is supported by regulatory initiatives.

Restraints and Challenges

Stringent environmental regulations on VOC emissions and solvent handling limit use in conventional petro-based solvents.

Volatility in raw-material costs, such as acetone, propylene, and crude oil, can hamper profitability.

Competition from green alternatives like water-based coatings and bio-derived chemicals is increasingly strong.

Competitive Landscape and Recent Developments

Notable industry players include BASF SE, Dow, Eastman, Oxea, Sasol, Solvay, Dairen Chemical, and major Chinese producers like Nanjing Rongxin, Zibo Nalcohol, and Ningbo Juhua Chemical.

Oxea (Germany) tripled its European capacity in early 2023 to meet rising demand from hand sanitizer, printing, and coatings sectors.

- Ningbo Juhua Chemical (China) began operations at a new 50-kiloton plant in September 2023, boosting local and export capacity.

Outlook Summary

| Metric | Estimate / Trend |

|---|---|

| 2024 Market Size | USD 1,684.9 million |

| 2032 Forecast | USD 2,374.1 million |

| CAGR (2024–2032) | 4.3% |

| Leading Region | Asia-Pacific (33.3%) |

| Top Applications | Coatings, pharma, cosmetics |

| Key Growth Drivers | Industrial growth, sustainability, pharma expansion |

| Major Constraints | Regulation, raw-material volatility, green alternatives |

Strategic Implications

-

Invest in bio-based or renewable feedstock routes to align with sustainability incentives and regulatory trends.

-

Expand production footprint in Asia-Pacific, particularly in India and China.

-

Focus on specialty grades (≥99.5% purity) targeted at pharma and electronics markets.

-

Innovate low-VOC solvent blends or hybrid formulations to retain market share in strictly regulated regions like Europe and North America.

Despite moderate headwinds from regulation and raw material volatility, the N-Propanol market is poised for steady expansion—especially fueled by growing demands in coatings, pharmaceuticals, and eco-friendly manufacturing. Companies aligning with sustainability trends, targeting high-purity curations, and expanding in high-growth regions will likely capture the greatest opportunity in the coming decade.

Information Source: https://www.fortunebusinessinsights.com/n-propanol-market-105137

KEY INDUSTRY DEVELOPMENTS

- April 2023 - Oxea tripled its production capacity of 1-propanol in Europe. This is due to high demand from manufacturers of hand sanitizers and the printing industry. With this expansion, the company will be able to serve its customer requirements efficiently.

- September 2023- The 1-propanol plant of Ningbo Juhua Chemical was put into operation. This new plant has an annual capacity of 50 kilotons and will also produce products including propionaldehyde. Hence, this development will help the company to enter this market.

Automotive NVH Materials Market Revenue Projections and Investment Trends 2032

By ameliasss, 2025-08-05

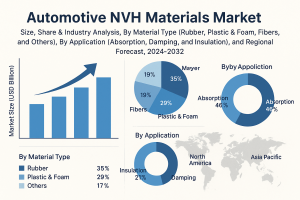

According to Fortune Business Insights, The global automotive NVH materials market was valued at USD 12.52 billion in 2023 and is projected to be worth USD 13.34 billion in 2024 and reach USD 21.70 billion by 2032, exhibiting a CAGR of 6.4% during the forecast period. Asia Pacific dominated the automotive NVH materials market with a market share of 55.99% in 2023. Factors such as rising demand for automobiles and stringent government requirements for safer cars are expected to fuel the market growth during the forecast period. Also, factors such as rising demand for porous materials coupled with increasing awareness regarding curbing noise pollution will increase the footprint of the market.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/automotive-noise-vibration-and-harshness-nvh-materials-market-103629

List of Key Players Present in the Market-

- Dow (Midland, Michigan, U.S.)

- 3M (Minnesota, U.S.)

- Huntsman International LLC (Texas, U.S.)

- Solvay (Brussels, Belgium)

- NITTO DENKO CORPORATION (Osaka, Japan)

- NVH KOREA (Ulsan, South Korea)

- Exxon Mobil Corporation (Texas, U.S.)

- Celanese Corporation (Texas, U.S.)

- Henkel Corporation (Düsseldorf, Germany)

- Sumitomo Riko Company Limited (Nagoya, Japan)

- Borgers SE & Co. KGaA (Bocholt, Germany)

- Covestro AG (Leverkusen, Germany)

Segments

On the basis of material, the market can be segmented into classified into rubber, plastic & foam, fibers, and others.

By application, the market can be divided into absorption, damping, and insulation.

In terms of geography, the market can be categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Report Coverage

The automotive NVH material report discusses a comprehensive analysis of the market and focuses on leading companies, products, and products. Additionally, the study also contains upcoming market trends and highlights vital industry developments that will guide our readers carving insightful business plans. An estimation for the market path is drawn from historical models by encompassing factors at the global, regional, and country levels.

Drivers & Restraints

Stringent Regulations for Curbing Noise Pollution to Bolster Growth

Rising demand towards operational vehicles coupled with stringent regulations imposed by governments to reduce noise pollution will drive the automotive NVH material market growth during the forecast period. Also, expanding electric vehicle industry rising investment opportunities will boost the growth of the market. Additionally, rising consumer awareness regarding significance of regulating noise pollution from automobiles will increase the footprint of the market.

However, increasing interest towards lighter vehicles will limit the growth of the market during the forecast period. Also, technical transition towards alternative technologies and material will hinder the growth of the market.

Regional Insights

Asia Pacific to Hold Largest Market Share Due to Expanding Automotive Industry

Asia Pacific will contribute the largest automotive NVH material market share due to an expanding automobile sector along with rising demand for effective mobility solutions to name a few. Factors such as increasing purchasing power & improving standard of living of middle class will further push the boundaries of the market. Rising demand for improving passenger comfort will boost the growth of the market.

North America will contribute a significant share towards the global contribution due to constantly expanding automotive industry and rising electric vehicle sales.

The European market will retain exceptional growth during the forecast period due to high production standards and rising utilization of automotive NVH materials to name a few.

Information Source: https://www.fortunebusinessinsights.com/automotive-noise-vibration-and-harshness-nvh-materials-market-103629

Competitive Landscape

Novel Product Launches and Mergers & Acquisitions to Help Capture Maximum Market Share

The dominant players in the automotive NVH material sector are investing heavily for creating materials that will increase passenger comfort right from the design phase. Primary strategies integrated by leading players is merging and collaborating for creating a varied product line for a larger consumer base. Other players are rushing towards launching novel product launches for capturing maximum revenue. For example, in June 2021, Free Field Technologies and Autoneum collaborated for developing products aimed at assisting OEMs accelerate vehicle acoustic design. The newly developed product will help manage noise and vibration by maximizing the usage of acoustic treatments inside Actran acoustic simulation software.

Industry Development-

- December 2022 – Vibracoustic developed a battery isolation pack isolation system for the body on the chassis of electric vehicles. This includes vehicles, such as light commercial vehicles, large SUVs, and off-road vehicles. The company developed the system to address the issue of damaging torsional bending forces associated with rigidly mounted battery packs. The system includes multiple mounts with elastomer dampers that enhance NVH performance and ensure the safety of the battery pack, which is among the most expensive components in an electric vehicle.