According to a report by Fortune Business Insights, titled “ Sulfuric Acid Market Size, Share & Industry Analysis, By Application (Fertilizers, Chemical Manufacturing, Metal Processing, Textile, Paper & Pulp, Automotive, Others) and Regional Forecast, 2025-2032 ,” the market will benefit from recent advances in product manufacturing. The global sulfuric acid market size significantly explores a striking CAGR forecast till 2032. Sulfuric acid is an odorless and colorless chemical that is soluble in water. It has strong acidic nature, dehydrating and oxidising property. The global sulphuric acid market is likely to derive growth from increasing applications across diverse industries.

Sulfuric acid is a colorless and odourless chemical that possesses favourable properties, among which water solubility stands out above the rest. The substance is widely used in applications across diverse industries, including agriculture, consumer goods, automotive and transportation, and chemicals and materials. Sulfuric acid is derived from sulphuric dioxide. A few variants are also derived from sulphate waste solutions. The increasing demand for sulphuric acid in the agriculture industry has contributed to the growth of the global market in recent years. The substance is used in the manufacturing of fertilizers. The increasing use of sulphuric acid in the manufacturing of chemicals will aid the growth of the market in the forthcoming years.

Request Sample PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/sulfuric-acid-market-101747

Key Players Covered:

Some of the key players in global sulfuric acid market are-

- BASF SE

- PVS Chemicals Inc.

- Aurubis

- Ineos Enterprises Limited

- Veolia

- Jiangsu Jihua Chemical

- Aarti Industries Limited

- Oriental Carbon & Chemicals Ltd.

- Amal Ltd.

- Dexo Fine Chem Pvt. Ltd.

- Cornerstore

The report offers insights into the ongoing sulphuric acid market trends. It highlights leading companies in the market and discusses the strategies that these companies have adopted in recent years. Forecast values for the market have been provided for the period of 2019-2026. The market has been segmented on the basis of several criteria including application and regional demographics. The competitive landscape scenario has been discussed in detail. Factual figures have been evaluated through trusted sources. The data included in this report has been gathered through interviews and opinions of experienced market research professionals.

Increasing Number of Mergers and Acquisitions Will Aid Growth

The report encompasses several factors that have contributed to the growth of the market in recent years. Among all factors, the increasing number of company mergers and collaborations have made a huge impact on the growth of the market in recent years. Due to the massive potential held by this market, companies are looking to adopt newer strategies with a bid to establishing a stronghold in the market. In February 2016, Fanchem Ltd., a subsidiary of PVS Chemicals completed the acquisition of Benson Chemicals Ltd. The company took over the chemical operations of the company. With this acquisition, the company plans to extend its sulphuric acid production capacity. This acquisition will not only help the company establish a stronghold, but will have a direct impact on the growth of the market in the coming years.

Asia Pacific to Dominate the Market, Applications in F&B Industry to Aid Growth

The report discusses the ongoing cataract surgical devices market trends across North America, Latin America, Europe, Asia Pacific, and the Middle East and Africa. Among these regions, Asia Pacific is projected to emerge dominant in the coming years. The constantly rising population and the subsequent increase in the demand for food and food products will create several growth opportunities for the companies operating in this market. Besides Asia Pacific, the market in Europe and Asia Pacific will witness considerable growth in the coming years.

Information Souce: https://www.fortunebusinessinsights.com/industry-reports/sulfuric-acid-market-101747

Key Industry Developments:

- In June 2019, Veolia announced the expansion of the plant in Louisiana that converts sulfuric acid into commercial-quality sulfuric acid, and also produces sulfur-based products for the refining and other purpose. New equipment and upgradation on existing equipment will yield a 15 percent increase in sulfuric acid regeneration capacity.

- February 2016, Fanchem Ltd., subsidiary of PVS Chemicals, Inc., acquired Benson Chemicals Limited, and its chemical-distribution operations in the region. They are expected to increase the production capacity of sulfuric acid as well increase the global presence.

According to Fortune Business Insights, The global kaolin market size was valued at USD 4.21 billion in 2024 and is projected to grow from USD 4.40 billion in 2025 to USD 6.28 billion by 2032, exhibiting a CAGR of 5.2% during the forecast period. Europe dominated the kaolin market with a market share of 41.33% in 2024.

Kaolin, also referred to as china clay, is a soft white clay employed in producing paper, paints, porcelain, and rubber. Its utilization as a filler in rubber manufacturing enhances abrasion resistance and mechanical strength, contributing to the growth of the china clay industry. Fortune Business Insights presents this information in their report titled " Kaolin Market, 2025–2032."

Kaolin, also known as kaolinite or china clay (chemical formula: Al₂Si₂O₅(OH)₄), is a layered silicate mineral made up of a tetrahedral sheet of silica linked through oxygen atoms to an alumina sheet. This structure gives it unique properties, making it valuable in a variety of applications, including paper manufacturing, ceramics, sanitary ware, and more. Its chemical inertness and ability to function as an adsorbent are key characteristics that enhance its industrial utility.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/kaolin-market-102352

Major Players Profiled in the Report:

- Imerys S.A. (France)

- Ashapura Group (India)

- EICL Limited (India)

- Sibelco (Belgium)

- KaMin LLC (U.S.)

- Thiele Kaolin Company (U.S.)

- LASSELSBERGER Group (Hungary)

- Quarzwerke GmbH (Germany)

- Sedlecký kaolin a. s. (Czech Republic)

- I-Minerals lnc. (Canada)

- R. Grace & Co. (U.S.)

- 20 Microns (India)

Segments:

Paper Segment Leads Market Fueled by Packaging and E-commerce Demand

By application, the market is classified into paper, ceramic & sanitary ware, fiberglass, paints & coatings, rubber, plastics, and others. In 2022, the paper segment held the leading share in the kaolin market, driven by the substantial demand for paper in packaging and printing applications. The global rise in e-commerce activities also contributes to increased product demand.

From the regional ground, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage

The market research report presents a comprehensive market examination, emphasizing crucial elements, including the competitive environment, distribution channels, and prominent product categories. Furthermore, the report provides valuable observations on market trends and significant industry advancements. Apart from the aforementioned factors, the report encompasses numerous variables that have bolstered market expansion in recent times.

Drivers and Restraints

Paper Industry Fillers and Expanding Ceramic Sector Drive Market Growth

The growing need for fillers in the paper industry is a key driver for the china clay market. Additionally, using this material in coated papers reduces particle size, enhancing strength. Furthermore, the expanding ceramic sector is projected to elevate the demand for this product in producing ceramic tiles and sanitary ware. Consequently, the increasing demand from ceramic and paper industries will propel the kaolin market growth.

However, the accessibility of substitutes and government guidelines for environmental protection could potentially limit market growth.

Regional Insights

Asia Pacific Thrives due to Diverse Industry Demand and Ceramics Boom

Asia Pacific commanded the largest kaolin market share at USD 1.12 billion in 2022, driven by rising product consumption in cement, ceramics, paper, and refractories sectors. Economic progress in key countries is boosting ceramics demand in institutional and household applications, fueling market growth.

Europe is poised for notable market expansion in the upcoming period, driven by increasing component demand in industries such as glass, paper, plastic, and rubber.

Get full Information of this Report: https://www.fortunebusinessinsights.com/kaolin-market-102352

Competitive Landscape

Key Players Forge Paths Through Innovation, Partnerships, and Expansion

Prominent industry participants employ diverse tactics, including bolstering distribution networks, driving product innovation, pursuing acquisitions, fostering collaborations, and engaging in mergers. These strategies are pursued to secure a competitive advantage in the global market. Noteworthy enterprises provide china clay for numerous applications spanning adhesives, building products, ceramics, cosmetics, paints & coatings.

Key Industry Development

- January 2023: Sibelco announced that it had used different materials within the glass batch to help improve melting efficiency and reduce the overall carbon footprint of the glass manufacturing process. The company aims to reduce scope 1 and 2 emissions intensity by 5% annually from 2021 to 2030.

- September 2022: Imerys announced that the company had signed a binding agreement with Syntagma Capital to sell most of its assets serving the paper market. These activities represented less than 10% of Imerys's revenue in 2022.

Advanced Magnetic Materials Market Emerging Technologies & Applications 2025-2032

By ameliasss, 2025-07-21

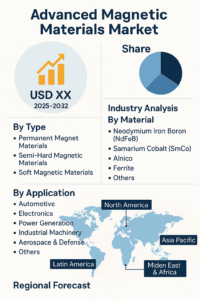

According to Fortune Business Insights, The global advanced magnetic materials market is witnessing strong growth, driven by innovations in rare-earth-free magnetic materials and expanding applications in the aerospace sector. Demand is accelerating across key industries such as electronics, automotive, and renewable energy, positioning the market for significant expansion.

The rising adoption of electric vehicles (EVs), wind turbines, and high-performance computing systems is fueling the need for advanced magnetic materials due to their superior performance and energy efficiency. Additionally, ongoing advancements in rare earth alternatives and nanostructured magnetic materials are expected to further propel market growth in the coming years. The Advanced Magnetic Materials Market is undergoing a significant transformation, driven by the increasing demand for high-performance materials across a variety of sectors, including automotive, electronics, energy, and healthcare. These materials, which include rare-earth magnets, ferrite magnets, and soft magnetic materials, play a vital role in the development of compact, energy-efficient devices and systems.

Request Free Sample PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/advanced-magnetic-materials-market-111751

Key Players Covered

The report includes the profiles of the following key players:

- TDK Corporation (Japan)

- Hitachi High-Tech Corporation (Japan)

- Daido Kogyo Co., Ltd. (Japan)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- VACUUMSCHMELZE (Germany)

- NINGBO YUNSHENG Co., Ltd. (China)

- Anhui Sinomag Technology Co., Ltd. (China)

- NEO (Japan)

- de (China)

- Arnold Magnetic Technologies (U.S.)

Key Drivers

1. Electrification of the Automotive Industry

The shift toward electric vehicles (EVs) and hybrid vehicles has significantly increased the demand for permanent magnets in motors, sensors, and powertrain systems. Advanced magnetic materials, particularly neodymium-iron-boron (NdFeB) magnets, are critical components in EV motors due to their high magnetic strength and efficiency.

2. Growth in Consumer Electronics

Smartphones, tablets, laptops, and other portable electronics rely heavily on miniaturized components powered by advanced magnetic materials. These magnets enable more compact, powerful, and lightweight designs.

3. Renewable Energy Expansion

Wind turbines and solar inverters depend on high-performance magnetic materials for efficient energy conversion and storage. The global push toward clean energy solutions is amplifying the need for reliable and durable magnetic systems.

4. Industrial Automation and Robotics

Increased automation across industries has led to a surge in demand for magnetic materials in actuators, sensors, and motors , which are essential for precise and efficient mechanical movements.

Market Segmentation

By Product Type:

Hard Magnetic Materials (e.g., NdFeB, SmCo)

Soft Magnetic Materials (e.g., silicon steel, permalloy)

Semi-Hard Magnetic Materials (e.g., Alnico, ferrites)

By Application:

Automotive

Consumer Electronics

Energy (Wind, Solar, Battery Systems)

Medical Devices

Aerospace & Defense

Industrial Automation

By Region:

North America – Technological advancement and strong defense sector

Europe – Strong automotive and renewable energy adoption

Asia-Pacific – Largest market share due to electronics manufacturing and EV production

Latin America & MEA – Emerging adoption in industrial and infrastructure sectors

Challenges

Supply Chain Dependence on Rare Earths: A significant portion of advanced magnets, especially NdFeB, depend on rare earth elements sourced mainly from China, raising concerns about supply security.

High Processing Costs: The production of high-purity magnetic materials requires specialized equipment and technologies, making the cost of manufacturing relatively high.

Environmental Concerns: The mining and processing of rare earth elements pose environmental challenges, leading to stricter regulations.

Recent Developments

R&D in Rare-Earth-Free Magnets: Companies are investing in the development of alternative magnetic materials, such as iron-nitride and manganese-based alloys, to reduce dependence on rare earths.

Partnerships and Acquisitions: Leading companies are forming strategic alliances to secure material sources and expand production capabilities.

Advancements in Recycling Technologies: Efforts are increasing to recycle rare earth magnets from end-of-life electronics and electric motors.

Information Source: https://www.fortunebusinessinsights.com/advanced-magnetic-materials-market-111751

Future Outlook

The Advanced Magnetic Materials Market is poised for dynamic growth over the next decade. The convergence of clean energy technologies, advanced mobility, and digitalization is expected to further accelerate demand. Governments worldwide are investing in localized manufacturing and recycling of magnetic materials to reduce supply risks, which may open new opportunities for innovation and sustainability.

Advanced magnetic materials are crucial enablers of modern technology. As industries continue to prioritize energy efficiency, miniaturization, and performance, the need for high-quality magnetic solutions will only intensify. Companies that invest in sustainable sourcing, material innovation, and global expansion will be best positioned to lead in this high-growth market.

According to Fortune Business Insights, The global ethylene marke t size was USD 166,520 million in 2019 and is projected to reach USD 245,005 million by 2027, exhibiting a CAGR of 5.6% during the forecast period. Asia Pacific dominated the ethylene market with a market share of 41.92% % in 2019. The growing utilization of plastics such as LDPE and HDPE coupled with technological advancement will bolster healthy growth of the market, states Fortune Business Insights, in a report, titled “ Ethylene Market Size, Share & Industry Analysis and Regional Forecast, 2020-2027.”

C2H4 is a colorless and flammable gaseous organic compound that contains double-bonded carbon atoms. It produces polyethylene (PE) , ethylene oxide, ethylene glycol, high-density polyethylene, 1,2-dichloroethane, vinyl acetate, and other compounds. Ethylene is a hydrocarbon compound with the chemical formula C2H4. It is a colorless, flammable gas with a sweet odor. Ethylene is one of the simplest unsaturated hydrocarbons and is widely used in industry.

Get a Free Sample Research Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/ethylene-market-104532

List of Key Players Profiled in the Ethylene Market Report:

- Reliance Industries Limited (Mumbai, India)

- China Petroleum & Chemical (Beijing, China)

- LyondellBasell Industries Holdings (Rotterdam, Netherlands)

- Exxon Mobil Corporation (Texas, United States)

- Shell International (The Hague, Netherlands)

- SABIC (Riyadh, Saudi Arabia)

- BOREALIS AG (Vienna, Austria)

- BRASKEM SA (São Paulo, Brazil)

- Chevron Phillips Chemical Company (Texas, United States)

- INEOS GROUP AG (London, UK)

- Other Key Players

Report Scope & Segmentation:

|

Report Attributes |

Details |

| Forecast Period | 2020 - 2027 |

| Forecast CAGR | 5.2% |

| 2027 Value Projection | USD 245,005 million |

| Market Size in 2019 | USD 166,520 million |

| Historical Data | 2016-2018 |

| No. of Pages | 100 |

| Report Coverage | Revenue Forecast, Company Profiles, Competitive Landscape, Growth Factors and Latest Trends |

| Segments Covered | · By Application· B |

| Regions Covered | · North America· Europe· Asia Pacific· Latin America· Middle East and Africa |

| Ethylene Market Growth Drivers | Rising Economic Development to Support Growth in Asia Pacific |

| Increasing Demand from Various End-use Industries to Propel the Product Demand |

Market Driver :

Inflated Demand for Packaging Solutions to Aid Market Growth

The growing consciousness for safe packaged products among consumers will have an excellent impact on the global market. The heavy demand for plastic packaging solutions for numerous applications such as e-commerce, healthcare products, convenience products, and transportation will further incite the development of the market. The growing demand for high-quality food with proper packaging solutions can promote the growth of the market. The surging application of plastic in the automotive and construction industries for the production of wiring, auto parts, pipes, and others will spur opportunities for the market. Similarly, the rising application in agriculture, medical, and other sectors will drive market growth.

Halt on Trade Activities to Boost Market Amid Coronavirus

The coronavirus pandemic has severely affected the chemical industry, resulting in halt on trade activities and operations. The disrupted supply chain has subsequently reduced the demand among industries. Nonetheless, the inflated demand for PE in packaging applications can stabilize the market amid covid-19. The growing awareness towards health and hygiene among consumers can enable speedy expansion of the market during the pandemic. Moreover, the increasing need for packaged food products will subsequently boost the production of polyethylene, which, in turn, will improve the prospects of the market.

The report on the ethylene market comprises of:

- All-encompassing scrutiny of the industry

- Valuable data about key players

- Emerging market trends

- Important insights into the competitive landscape

- Leading regions

Information Source: https://www.fortunebusinessinsights.com/ethylene-market-104532

Regional Analysis :

Rising Economic Development to Support Growth in Asia Pacific

The market in Asia Pacific is expected to hold the largest share in the global market during the forecast period owing to the growing demand for PE from the plastic and chemical industry in developing countries such as China, India, and Japan. The increasing economic development has led to an improved lifestyle of consumers, thus fueling the demand for quality-based plastic for daily use. The surging middle-class population coupled with increasing construction activities will enable speedy expansion of the market in the region. The plastic industry in China has experienced immense growth during the forecast period owing to the demand for new housing units and vehicles.

Key Development :

-

October 2019: Sinopec Sabic Tianjin Petrochemical Co. Ltd. and Saudi Arabia’s SABIC had a joint venture for an expansion project at Tianjin ethylene plant. The project will increase the production capacity to 1.3 million tons annually.

According to Fortune Business Insights, The global cosmetic packaging market size was valued at USD 55.38 billion in 2024. The market is projected to grow from USD 57.55 billion in 2025 to USD 79.99 billion by 2032, exhibiting a CAGR of 4.82% during the forecast period. Asia Pacific dominated the cosmetic packaging market with a market share of 42.09% in 2024. Metal cosmetic packaging solutions consist of containers that are used to store, safeguard, and showcase cosmetic products, such as makeup, skincare, and fragrances in an elegant manner. These packaging products, as the name suggests, are made from various metals, such as tinplate, aluminum, and stainless steel. These metals are known for their recyclability, durability, and high aesthetic appeal. The increasing demand for sustainable and durable packaging solutions will help the market grow at an appreciable pace.

In the dynamic and rapidly evolving cosmetics industry, packaging plays a crucial role in attracting consumers, conveying brand identity, and ensuring product safety. A standout innovation in this space is custom makeup packaging, especially in the form of cosmetic boxes. These packaging solutions do more than simply hold products—they serve as powerful tools for storytelling and brand communication. With compelling visuals, engaging taglines, and informative content, cosmetic packaging allows brands to share their values, mission, and unique narrative directly with consumers.

Fortune Business Insights presents this information in a report titled " Metal Cosmetic Packaging Market, 2025-2032 ."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/cosmetic-packaging-market-102130

Major Players Profiled in the Report

- Linhardt GmbH & Co. KG (Germany)

- AptarGroup Inc. (U.S.)

- Albea S.A. (France)

- Quadpack Industries (Spain)

- HCP Packaging Group (China)

- Silgan Holdings (U.S.)

- Crown Holdings Inc. (U.S.)

- Fusion Packaging (U.S.)

- Libo Cosmetics Company Ltd. (Taiwan)

- Tubex Aluminium Tubes (Austria)

- Big Sky Packaging (U.S.)

Segments

By material, the market is divided into aluminum, tin, and steel-spout.

By product type, the market is segmented into bottles, jars & containers, caps & closures, tubes, pumps & dispensers, and others.

By application, the market is classified into skin care, nail care, hair care, makeup, and others.

With respect to geography, the market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage

The report has conducted a detailed analysis of the market and focused on several critical aspects, such as leading materials, product types, applications, and top market players. It has also highlighted the most recent market trends and the key developments in the industry. In addition to the factors mentioned above, the report delves into several other factors that have helped the market grow.

Drivers & Restraints

Increasing Adoption of Eco-Friendly Packaging Solutions to Accelerate Market Expansion

Customers are becoming more conscious about their lifestyle choices as they are gaining more awareness regarding the concepts of carbon emissions and sustainability. They are opting for brands that are highly eco-conscious and use sustainable practices to manufacture their products. These factors have played a key role in compelling market players to adopt eco-friendly manufacturing methods to make sustainable metal packaging solutions for cosmetic products. This move will help them enhance their brand presence and attract new customers.

However, the high costs associated with manufacturing aluminum or steel-based packaging products can impede the metal cosmetic packaging market growth.

Regional Insights

Asia Pacific Leads Market Due to Presence of Diverse Customer Base

Asia Pacific is dominating the metal cosmetic packaging market share as the region has a diverse customer base due to the presence of different cultures. These cultures are also influencing customers’ purchase decisions and packaging preferences, which is why there is a high demand for mass-market and premium metal packaging products in the region.

North America is the second-dominating region in the global market as the region has a well-established cosmetics packaging industry and a vast presence of leading cosmetic brands.

Europe is also showcasing strong growth due to the presence of reputed cosmetic manufacturing companies and the implementation of strict packaging standards to ensure that customers get high-quality packaging solutions.

Latin America is expected to showcase rapid expansion in the global market as the region’s customers are quite price-sensitive, which will increase their preference for cost-effective packaging solutions.

The Middle East & Africa is predicted to display moderate growth due to the high demand for both conventional and futuristic metal packaging solutions.

Information Source: https://www.fortunebusinessinsights.com/cosmetic-packaging-market-102130

Competitive Landscape

Key Companies to Focus On New Product Launches, Collaborations, and Partnerships to Strengthen Their Brand Value

Some of the most reputed companies operating in this market include Linhardt GmbH & Co. KG, AptarGroup Inc., Albea S.A., Quadpack Industries, HCP Packaging Group, Silgan Holdings, Crown Holdings Inc., Fusion Packaging, Libo Cosmetics Company Ltd., Tubex Aluminium Tubes, and Big Sky Packaging. These market players are implementing a wide range of strategies, such as new product launches, partnerships, and collaborations to increase their brand value and expand their business operations.

Key Industry Developments

- June 2023: Albéa Tubes and Oriflame collaborated to launch the Duologi range, which is designed in alignment with Albéa’s sustainability goals for the packaging of Oriflame’s “Rich Creme Conditioner” and “Light Creme Conditioner.”

- February 2023: WWP Beauty launched SOS Ocean, EcoLuxe, MonoPump Airless packaging collections, and the Beauty Express Turnkey solution.

According to Fortune Business Insights, The global airless packaging market size was valued at USD 8.45 billion in 2024. The market is projected to grow from USD 8.99 billion in 2025 to USD 12.98 billion by 2032, exhibiting a CAGR of 5.38% during the forecast period. Europe dominated the airless packaging market with a market share of 27.93% in 2024.

The use of airless packaging solutions prevents the contact of the inside product with the air. The solutions offer numerous benefits, including extended shelf life and enhanced functionality. The market expansion can be attributed to the globally rising sales of cosmetic products and the escalating demand for natural skincare products. Airless packaging solutions are dispensing systems that do not allow air contact with the product inside. The packaging offers significant benefits, such as improved functionality and extended shelf life, which adds noteworthy value to the consumer experience.

Fortune Business Insights™ provides this information in its research report, titled “Airless Packaging Market, 2025-2032”.

List of Key Players Mentioned in the Report:

- AptarGroup Inc. (U.S.)

- Silgan Holdings Inc. (U.S.)

- Quadpack (Spain)

- HCP Packaging (China)

- APackaging Group (U.S.)

- LUMSON S.p.A (Italy)

- Hangzhou ABC Packaging Co. Ltd. (China)

- Albéa Group (France)

- PrimePac (Australia)

- The Packaging Company (U.S.)

- Berk (U.S.)

- SR Packaging (China)

- Evergreen Resources (U.S.)

- Eurovetrocap (Italy)

- Cosme Packaging (China)

Segmentation:

Plastic Segment Leads the Market Owing to Various Benefits Offered by the Material

By material, the market is fragmented into glass, plastic, aluminum, and others. The plastic segment dominates the market due to the high demand for the material. Plastic solutions offer excellent protection, helping the prevention of spoilage, leakage, and contamination of a product.

Bottles & Jars Segment Holds Major Share Due to Escalating Product Deployment

Based on product type, the market is segmented into tubes, bottles & jars, and others. The bottles & jars segment registers a key market share. This is due to the rising deployment of the product owing to the availability of various customized options.

Personal Care & Cosmetics Segment Registers Key Share Owing to Growing Product Usage to Increase Shelf Life of Cosmetics

On the basis of application, the market is fragmented into food & beverages, pharmaceuticals, personal care & cosmetics, and others. The personal care & cosmetics segment accounts for a leading market share. The product usage helps increase the shelf life of cosmetic products, which is a major factor driving segment growth.

Based on geography, the market for airless packaging has been studied across North America, Asia Pacific, Latin America, Europe, and the Middle East & Africa.

Report Coverage:

The report gives an account of the major trends in the global market. An analysis of the industry on the basis of various segments has also been presented in the report. The market has been studied based on material, product type, application, and geography.

Drivers and Restraints:

Market Value to Surge with Growing Demand for Cosmetic Products

The escalating cosmetic product demand has led to an increased demand for sustainable packaging solutions among manufacturers. Some of the products requiring effective packaging comprise skin care creams, serums, foundations, moisturizers, and anti-ageing products. These factors are poised to drive the airless packaging market growth.

Nonetheless, the fluctuating prices of raw materials may hinder the industry's expansion to a certain extent.

Regional Insights:

Europe Dominates the Market Due to Expanding Beauty Industry

Europe accounts for a dominating market share. In 2022, the market size in the region stood at USD 2.36 billion. The regional growth can be attributed to the presence of key manufacturing companies and the expanding beauty sector.

Latin America is the fastest-growing regional market. The regional airless packaging market share is set to expand, driven by the soaring airless technology demand from food & beverage manufacturers.

Information Source: https://www.fortunebusinessinsights.com/airless-packaging-market-106855

Competitive Landscape:

Companies Launch Advanced Products to Increase Customer Base

Major industry players are centered on the development and launch of advanced products. These initiatives are being deployed to expand their clientele base. Some of the leading industry players comprise Silgan Holdings Inc., AptarGroup, Inc., APackaging Group, and others.

Key Industry Development:

- October 2023 – Pinard Beauty Pack and Aptar Beauty jointly unveiled the Future Airless PET, an omnichannel and fully recyclable airless packaging solution. The product is anticipated to be launched in mid-2024.

- February 2023 – Quadpack declared the launch of a new refillable airless pen, Light Me Up. The refillable airless pen has several tips and can be utilized in both the skincare and makeup sectors. The refill system is also convenient and intuitive.

- November 2022 – Embelia introduced a new and refillable version of the Baia pouch airless system. The new airless system was manufactured in partnership with Lablabo, an expert in pouch airless packaging solutions.

Triethanolamine Market Future Trends in Cement & Concrete Applications 2025-2032

By ameliasss, 2025-07-17

Global Market Overview

According to Fortune Business Insights, The global Triethanolamine market size was valued at USD 1.33 billion in 2024. The market is projected to grow from USD 1.40 billion in 2025 to USD 1.98 billion by 2032, at a CAGR of 5.1% during 2025-2032. Asia Pacific dominated the triethanolamine market with a market share of 44.36% in 2024.

Triethanolamine (TEA) is a versatile organic compound with the chemical formula N(CH₂CH₂OH)₃, categorized as both a tertiary amine and a triol. It appears as a colorless, viscous liquid with a faint ammonia-like odor and exhibits excellent solubility in water and various organic solvents. TEA is produced by reacting ethylene oxide with aqueous ammonia, yielding a compound widely valued for its roles as a surfactant, emulsifier, and pH stabilizer across multiple industrial applications.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/triethanolamine-market-112907

List of Key Triethanolamine Companies Profiled

- BASF SE (Germany)

- DOW (U.S)

- Indorama Ventures Public Company Limited (Thailand)

- INEOS (U.K)

- Nouryon (Netherlands)

- SABIC (Saudi Arabia)

- Sintez OKA Group of Companies (Russia)

- OUCC (Taiwan)

- Kanto Kagaku (Japan)

- Shree Vallabh Chemical (India)

Key Drivers & Trends

Personal Care Boom

TEA remains a staple in cosmetics—used as an emulsifier, pH adjuster, and surfactant. The personal care segment constitutes around 29–40%+ of consumption.

Industrial & Infrastructure Growth

Increasing construction, cement grinding aids, and metalworking applications—particularly with global infrastructure activities—support demand.

Sustainability & Regulatory Push

A move toward bio-based TEA, influenced by stricter cosmetics and environmental regulations in the U.S. and Europe, is gaining traction.

Tech Innovation & Digital Integration

Adoption of energy-efficient production, digital monitoring, and automation are shaping operational efficiencies, especially in Europe.

⚠️ Market Challenges & Risks

Substitution Pressure : Alternatives such as monoethanolamine and diethanolamine present competitive challenges due to cost and regulatory advantages.

Raw Material Volatility : Fluctuating feedstock (ethylene oxide) prices increase production costs.

Regulatory Scrutiny : TEA’s toxicity concerns for environmental and aquatic life and stricter chemical regulations pose constraints.

Market Breakdown

By Purity Grade

99% TEA dominates (> 63% market share) due to its high purity demands across cosmetics, textiles, and pharmaceuticals.

By Application

Emulsifiers are the largest functional segment (~38%), bolstered by personal care and detergents.

Other sectors include home care , textiles , industrial cleaning , metalworking , pharmaceuticals , construction , and agrochemicals .

By Region

North America leads with ~47% share (~USD 0.8 billion), supported by production strength and demand.

Europe is the second-largest, driven by regulatory investment and tech innovation.

Asia-Pacific is set to see the fastest growth, fueled by urbanization, personal care consumption, and construction demand.

Price Dynamics

Asia & Europe saw declining TEA prices in Q1 2025, due to oversupply and weak end-use demand (e.g., construction, cosmetics).

North America experienced price spikes in late 2023–early 2024 due to supply disruptions (weather events, force majeure).

Competitive Landscape

Leading manufacturers include BASF, Dow, Evonik, Huntsman, AkzoNobel, SABIC, INEOS, LG Chem , and regional producers.

Key strategic moves involve bio-based TEA launches by BASF , plus M&A and partnerships aimed at sustainability and geographic reach expansion.

Future Outlook & Opportunities

Bio-based TEA : As sustainability trends accelerate, bio-derived TEA could capture growing market share.

New Applications : Demand in electronics, coatings, and biotech (pharmaceutical, agrochemical) offers growth potential.

Digital & Lean Production : Smart manufacturing and green processes will drive efficiency and differentiate players.

Triethanolamine remains a vital chemical in both consumer and industrial sectors. While demand is rising steadily—driven by personal care, construction, and regulatory shifts—the market also faces pressures from substitutes, costs, and environmental scrutiny. Companies that innovate toward sustainability (bio-based TEA) and capture emerging use-cases (like electronics, pharma, coatings) are best positioned to thrive.

Information Source: https://www.fortunebusinessinsights.com/triethanolamine-market-112907

KEY INDUSTRY DEVELOPMENTS

-

September 2024: BASF inaugurated a new world-scale production plant for alkyl ethanolamines, including TEA, at its Antwerp Verbund site in Belgium, increasing global annual production capacity by nearly 30% to over 140,000 metric tons. The facility strengthens BASF’s global network, which includes sites in Ludwigshafen (Germany), Geismar (Louisiana), and Nanjing (China).

Recycled Packaging Market Growth Fueled by Eco-Friendly Packaging Demand 2025-2032

By ameliasss, 2025-07-16

According to Fortune Business Insights, The global recycled packaging market size was valued at USD 48.69 billion in 2024. The market is projected to grow from USD 51.28 billion in 2025 to USD 77.16 billion by 2032, exhibiting a CAGR of 6.01% during the forecast period. Asia Pacific dominated the recycled packaging market with a market share of 35.51% in 2024. The Recycled Packaging Market is witnessing significant growth as global awareness around environmental sustainability intensifies. Driven by strict government regulations, rising consumer consciousness, and increasing corporate responsibility, the demand for recycled materials in packaging is on a steady upward trajectory.

The Recycled Packaging Market is projected to grow robustly from 2025 to 2032. The market includes a wide array of materials such as recycled plastics, paper, glass, and metals used to create sustainable packaging solutions. Industries including food & beverage, personal care, pharmaceuticals, and electronics are heavily investing in recycled packaging alternatives to reduce their carbon footprint and meet evolving regulatory and consumer demands.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/recyclable-packaging-market-108092

List of Key Companies Profiled:

- Amcor Plc (Switzerland)

- Mondi Group (U.K.)

- Berry Global Inc. (U.S.)

- Smurfit Kappa (Ireland)

- Ball Corporation (U.S.)

- Mauser Packaging Solutions (U.S.)

- WestRock Company (U.S.)

- Schütz GmbH & Co. KGaA (Germany)

- International Paper (U.S.)

- Huhtamaki Inc. (Finland)

- Tetra Pak (Switzerland)

- SIG Group (Switzerland)

Key Market Drivers

1. Environmental Concerns and Government Policies

Rising concerns about plastic waste and its environmental impact have led to strong regulatory actions. Governments worldwide are enforcing bans on single-use plastics and promoting circular economy models, fueling the demand for recycled packaging materials.

2. Shift in Consumer Preferences

Modern consumers are increasingly eco-conscious and prefer products with sustainable packaging. Brands that adopt recycled packaging not only attract more customers but also enhance their brand image and loyalty.

3. Corporate Sustainability Initiatives

Companies are aligning their operations with global sustainability goals (such as the UN’s SDGs), thereby integrating recycled packaging into their supply chains as part of ESG (Environmental, Social, and Governance) commitments.

Market Segmentation

By Material Type:

- Recycled Paper & Cardboard

- Recycled Plastics (PET, HDPE, LDPE, etc.)

- Recycled Glass

- Recycled Metals (Aluminum, Steel)

By Packaging Type:

- Bottles & Containers

- Boxes & Cartons

- Pouches & Bags

- Wraps & Films

By End-Use Industry:

- Food & Beverage

- Healthcare

- Personal Care & Cosmetics

- Electronics

- E-commerce & Retail

Regional Insights

North America

North America dominates the market due to advanced recycling infrastructure and strong consumer demand for green packaging. The U.S. has seen a surge in sustainable packaging solutions across food chains and supermarkets.

Europe

Europe follows closely, driven by the EU's Circular Economy Action Plan. Germany, the UK, and France lead the region with widespread adoption of recycled materials.

Asia Pacific

Asia Pacific is emerging as the fastest-growing region. Countries like China, India, and Japan are investing in waste management technologies and sustainable packaging amid rising urbanization and industrial growth.

Market Challenges

- Quality and Consistency of Recycled Materials: The recycled content must meet specific hygiene and safety standards, especially in food and pharmaceutical sectors.

- High Initial Investment Costs: Transitioning from traditional to recycled packaging requires capital for new technologies and restructured supply chains.

- Limited Recycling Infrastructure in Developing Regions

Information Source: https://www.fortunebusinessinsights.com/recyclable-packaging-market-108092

Opportunities

- Technological Innovation : Advancements in chemical recycling and biodegradable composites offer tremendous growth opportunities.

- Corporate Collaborations : Partnerships between packaging companies and recycling firms can enhance closed-loop systems.

- Growing E-commerce : The booming e-commerce sector demands sustainable packaging to cater to eco-conscious shoppers.

The Recycled Packaging Market is poised for transformative growth between 2025 and 2032. Sustainability is no longer optional—it's a critical business imperative. As stakeholders across the value chain embrace recycled solutions, the industry will continue to evolve, offering smarter, greener, and more circular packaging options for the future.

KEY INDUSTRY DEVELOPMENTS:

- June 2023 – Mondi partnered with Syntegon, a manufacturer of process and packaging machinery, to develop a recyclable paper packaging solution using recycled fibers for dried foods, such as flour, sugar, and pasta.

- May 2023 - Mauser Packaging Solutions expanded its global collection and reconditioning network with the opening of a new site in Tarsus, Turkey. Once packaging is collected through Recover Syst-M, the company’s global collection program, IBCs, and drums are reconditioned for reuse or recycled if they have reached the end of their usable life.