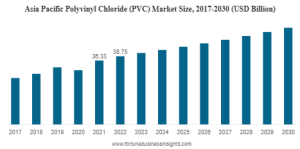

According to Fortune Business Insights, The global polyvinyl chloride (PVC) market was valued at USD 68.96 billion in 2022 and is projected to expand from USD 72.08 billion in 2023 to USD 95.88 billion by 2030, registering a CAGR of 4.2% during the forecast period. In 2023, Asia Pacific led the PVC market, accounting for 56.19% of the global share. Polyvinyl chloride (PVC) is among the most widely used polymers globally and ranks as the third-largest produced plastic. Its versatility makes it suitable for a diverse range of applications across industries such as construction, transportation, packaging, electrical & electronics, and healthcare. PVC is known for its durability and long service life, available in both rigid and flexible forms to meet varied application needs. Unlike many thermoplastics that rely solely on petroleum, PVC is produced from *two raw materials—salt and hydrocarbon feedstock—*which reduces its dependence on non-renewable fossil fuels. Consequently, PVC is considered less oil-dependent compared to other conventional plastics.

Polyvinyl chloride is deployed in an extensive range of applications including electrical & electronics, packaging, transportation, healthcare, and construction. The industry expansion can be attributed to its versatile nature of bonding with several polymers.

Fortune Business Insights™ provides this information in its research report, titled “Polyvinyl Chloride (PVC) Market, 2023-2030”.

Segmentation:

Rigid Segment Accounted for Major Share Considering Increasing Product Deployment for Water Supply and Irrigation

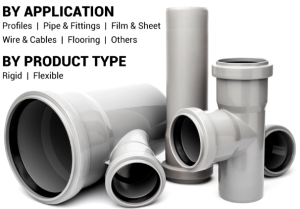

On the basis of product type, the market for polyvinyl chloride is bifurcated into flexible and rigid. The rigid PVC segment held a prominent market share in 2022. This can be credited to the extensive product usage for irrigation, drainage, and water supply on account of corrosion resistance and durability.

Pipe & Fittings Segment to Lead the Market Due to Rising PVC Usage on Account of Durability

On the basis of application, the market for polyvinyl chloride is subdivided into flooring, pipe & fittings, wire & cables, profiles, film & sheet, and others. The pipe & fittings segment is set to dominate the global market over the study period owing to its sustainability and durability, making it a suitable choice for water transportation.

Building & Construction Segment Accounts for Key Share Driven by Extensive Product Adoption

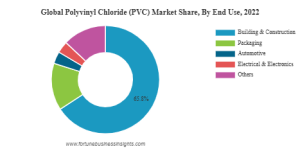

On the basis of end use, the market for polyvinyl chloride is fragmented into packaging, building & construction, electrical & electronics, automotive, and others. The building & construction segment holds the largest share due to its wide product deployment in the construction sector in roofing, cables, profiles, and accessories.

Based on geography, the market for polyvinyl chloride (PVC) has been analyzed across North America, Latin America, Asia Pacific, Europe, and the Middle East & Africa.

List of Key Players Mentioned in the Report:

- Ercros (Spain)

- Formosa Plastics Corporation (Taiwan)

- Hanwha Group (South Korea)

- Ineos (U.K.)

- KEM ONE (France)

- Occidental Petroleum Corporation (U.S.)

- Orbia (Mexico)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Vynova (Belgium)

- Westlake Corporation (U.S.)

Report Coverage:

The report gives an account of the key steps deployed by leading companies to strengthen their market share. It further gives an insight into the vital trends in the market. An analysis of the industry based on numerous segments has also been presented in the report: product type, application, end use, and geography.

Drivers and Restraints:

Surge in Market Value Owing to Growing Demand from Construction Sector

There has been a rise in product application across the construction industry, where it is used for cables, pipes, and roofing materials. The insulating properties of PVC make it a preferred material, ensuring reliability and safety in power distribution. These factors are expected to propel polyvinyl chloride (PVC) market growth.

However, regulatory concerns associated with the release of hazardous chlorine-based byproducts during the manufacturing process may restrain the industry expansion.

Regional Insights:

Asia Pacific to Dominate Owing to Surging Demand in Infrastructure Development and Construction

Asia Pacific polyvinyl chloride (PVC) market share is anticipated to hold a key position in the global market. The region has recorded an increasing product demand in the infrastructure development, construction, and manufacturing sectors.

The North America market size is set to surge considering the rise in construction activities in the region and the escalated product usage in an array of construction applications.

Competitive Landscape:

Industry Players Focus on Investing in Bio-based Products to Cater to Rising Demand

Major industry participants are investing in the development of products made from bio-based materials. These products are being introduced for meeting the soaring demand for green products. KEM ONE and Ineos are some of the key players in the market.

Key Industry Development:

- December 2023 – INEOS launched a new rage of PVC product that has 37% lower carbon footprint than the average carbon footprint of suspension PVC produced in the European Industry.

- July 2023 - Chemplast Sanmar Ltd. shared plans to invest USD 120 million to expand its production capacities of the Specialty Paste PVC unit at Cuddalore and the Custom Manufactured Chemicals Division’s (CMCD) unit at Berigai.