Blogs

Caustic Soda Market Industry Insights, Trends, Size & Forecast to USD 55,557.7 Million by 2027

By ameliasss, 2025-10-17

The global caustic soda market was valued at USD 44,959.2 million in 2019 and is expected to grow to USD 55,557.7 million by 2027, registering a CAGR of 3.1% during the forecast period. Asia Pacific emerged as the leading region, accounting for 56.23% of the total market share in 2019.

Caustic soda serves as a fundamental raw material in the production of various essential products, including plastics, pharmaceuticals, and water treatment additives. It is produced through the electrolysis of sodium chloride solution using technologies such as diaphragm cells or membrane cells. Major end-use industries driving demand for caustic soda include pulp and paper, detergents, alumina, oil and gas, textiles, and chemicals. The increasing demand for caustic soda across diverse industries such as paper & pulp, textiles, chemicals, and water treatment is expected to fuel market expansion globally.

Key Market Insights

Caustic soda, also known as sodium hydroxide (NaOH), is a vital industrial chemical used in a wide range of manufacturing processes. It serves as an essential raw material for producing alumina, soaps, detergents, and petroleum products. The growing demand for these end-use applications, coupled with expanding industrialization in emerging economies, drives the market’s steady growth trajectory.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/caustic-soda-market-104711

Driving Factors

Rising Demand from the Pulp and Paper Industry

Increasing consumption of paper-based products and packaging materials boosts caustic soda use for pulp digestion and paper bleaching.

Expanding Chemical Manufacturing Sector

Caustic soda acts as a key reactant in producing various chemicals, including solvents, plastics, and synthetic fibers, enhancing its market value.

Growing Application in Water Treatment

Rapid urbanization and rising concerns about clean water availability are increasing the adoption of caustic soda for pH regulation and water purification processes.

Restraining Factors

Despite positive growth prospects, fluctuations in raw material prices and stringent environmental regulations on chemical production may hinder market expansion to some extent.

Market Segmentation

By Form: Lye, Flake, Pellet

By Application: Alumina, Pulp & Paper, Organic Chemicals, Inorganic Chemicals, Textiles, Water Treatment, Others

By Region: North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Regional Insights

Asia Pacific dominated the caustic soda market in 2023, holding over 50% of the global share . The region’s strong industrial base in China, India, and Japan supports the growth of paper, textile, and alumina industries. Meanwhile, North America and Europe show steady demand due to the chemical and manufacturing sectors' stability and growing water treatment applications.

Competitive Landscape

Leading companies are investing in technological advancements and sustainable production methods to minimize environmental impact and enhance product efficiency. Major players operating in the global caustic soda market include:

- Olin Corporation (Clayton, Missouri, United States)

- Tata Chemicals Limited (India)

- Aditya Birla Chemicals (India) Limited (India)

- Gujarat Alkalies and Chemical Limited (India)

- Occidental Petroleum Corporation (OXY) (Houston, Texas, United States)

- Formosa Plastics Corporation (Taiwan)

- PPG Industries (Pittsburgh, Pennsylvania, United States)

- Xinjiang Zhongtai Chemical Co., Ltd. (China)

- Hanwha Chemical (South Korea)

- Brenntag North America, Inc. (North America)

Strategic mergers, capacity expansions, and innovations in membrane cell technology are helping these companies strengthen their market position.

Information Source: https://www.fortunebusinessinsights.com/caustic-soda-market-104711

Future Outlook

The caustic soda market is poised for steady growth over the next decade, driven by ongoing industrialization, the shift toward sustainable manufacturing, and consistent demand from key downstream sectors. The integration of green chemistry and energy-efficient production methods will further shape the market dynamics through 2032.

Conclusion:

The Caustic Soda Market continues to show promising potential, supported by growing applications in manufacturing and environmental sectors. With sustainability becoming a key focus, market players are expected to emphasize cleaner production processes and efficient resource utilization, ensuring long-term market stability and profitability.

KEY INDUSTRY DEVELOPMENTS:

- In May 2021, Olin Corporation announced the reduction in the Chlor alkali production capacity by shutting down 20% of its diaphragm grade at its Plaquemine facility.

- In January 2021 , the GACL-NALCO Alkalies & Chemicals Ltd (GNAL) delayed the commissioning of the new caustic soda production line to August 2021. The production facility is situated at Dahej and has a production capacity of 266667 tons/year for caustic soda.

Market Overview

The whey protein market Growth is set for a significant surge, with the global market size projected to expand from USD 11.79 billion in 2023 to USD 22.63 billion by 2032. This expansion, which starts from a base of USD 12.64 billion in 2024, represents a compound annual growth rate (CAGR) of 7.5% during the forecast period. In 2023, North America led the market with a dominant share of 35.96%. A key driver of this growth is the U.S. market, which is expected to reach an estimated USD 5.11 billion by 2032, fueled by heightened health awareness and consumer focus on daily protein intake.

Rising consumer awareness regarding a healthy diet is expected to boost consumer product demand. Further, growing innovations in protein manufacturing containing several amino acids may increase the product’s adoption. Moreover, robust demand for premium products may facilitate the product demand. In addition, the strong demand for premium products across the personal care industry is expected to propel industry development during the upcoming years.

List of Key Players Profiled in the Report

- Hilmar Cheese Company, Inc. (U.S.)

- Saputo Inc. (Canada)

- Glanbia plc (Ireland)

- Fonterra Co-operative Group Ltd. (New Zealand)

- Arla Foods (Denmark)

- Alpavit (Germany)

- Wheyco GmbH (Germany)

- Milk Specialties (U.S.)

- Carbery Group (Ireland)

- LACTALIS Ingredients (France)

Segments

By type, it is segmented into isolates, concentrates, and others. Based on application, it is classified into animal feed, food and beverages, and others. Geographically, it is clubbed into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Report Coverage

The report provides a detailed analysis of the top segments and the latest trends in the market. It comprehensively discusses the driving and restraining factors and the impact of COVID-19 on the market. Additionally, it examines the regional developments and the strategies undertaken by the market's key players.

Source: https://www.fortunebusinessinsights.com/whey-protein-market-106555

Drivers and Restraints

Strong Demand for Protein-Rich Diet to Nurture Industry Progress

The whey protein market is poised for significant expansion, fueled by a convergence of consumer trends. Key growth drivers include the rising demand for protein-rich diets, increased health consciousness regarding chronic conditions, and a growing preference for convenient food options. Furthermore, rising disposable incomes and a cultural shift toward healthier lifestyles are bolstering consumption. The expanding sports nutrition sector, catering to athletes and fitness enthusiasts, provides an additional catalyst for growth. However, the market faces a notable headwind from the increasing popularity of plant-based protein alternatives, which could temper future expansion.

Regional Insights

Rising Awareness Regarding Easy Usability and Convenience to Boost Growth in North America

North America is expected to dominate the whey protein market share due to rising awareness regarding easy usability and convenience. The market in North America stood at USD 3.73 billion in 2021 and is expected to gain a huge portion of the global market share. Further, evolving consumer preferences and tastes may boost the product demand. These factors may propel industry growth.

In Europe, increasing trends of preventive healthcare, rising emphasis on healthy living, and growing demand for protein supplements may foster the product’s demand. In addition, the adoption of proteins in naturally and synthetically derived foods may propel market growth.

In Asia Pacific, the rising domestic demand and exports for dairy-based products, such as whey and casein, may foster market development.

Competitive Landscape

Companies Announce Acquisition Strategies to Reinforce their Stance

Prominent companies operating in the market announce acquisition strategies to reinforce their market position globally. For example, Saputo Inc. declared two acquisitions in the value-added and dairy alternatives segment. The company invested nearly USD 146.94 million and acquired Wisconsin Specialty Protein, LLC’s Reedsburg facility. It produces value-added ingredients such as whey, goat, organic lactose, and others. This acquisition may enable the company to reinforce its market stance globally. Furthermore, companies adopt product launches, mergers, partnerships, and research and development strategies to boost their annual revenues.

Industry Development

November 2023: FrieslandCampina Ingredients, a leading global protein supplier, announced the launch of Nutri Whey ProHeat. The company's new ingredient is microparticulated and heat-stable, designed for the medical nutrition market.

Metal Pail Market Key Investment Opportunities and Market Potential Across Emerging Economies

By Apeksha More, 2025-10-17

Metal Pail Market is widely used in chemicals, paints, lubricants, adhesives, and food industries because of its durability, corrosion resistance, and recyclability. Industrial growth, regulatory compliance, and eco-friendly initiatives drive demand for high-quality packaging. Manufacturers focus on automation, advanced coatings, lightweight designs, and smart labeling to enhance production efficiency and product quality. Regional industrial expansion and growing awareness of sustainable packaging create strategic opportunities for market players. Despite challenges such as fluctuating raw material costs and competition from plastics, long-term growth prospects remain positive for global manufacturers.

Market Overview

Metal pails play a critical role in industrial packaging due to their strength, durability, and environmental benefits. Steel and tin provide excellent corrosion resistance and long-term usability. Industries use metal pails to safely store and transport chemicals, lubricants, paints, and food-grade products. Modern manufacturing and automation enhance production precision, reduce defects, and improve operational efficiency. Expanding industrialization and global production activities increase demand for reliable and sustainable packaging solutions. Metal pails protect product integrity, comply with safety standards, and support environmentally responsible practices, making them indispensable across multiple industrial sectors.

Key Market Drivers

Industrial Growth

Industrialization in chemical manufacturing, construction, automotive, and food processing sectors drives demand for durable packaging. Metal pails offer leak-proof designs, corrosion resistance, and safe handling of hazardous and non-hazardous materials. Infrastructure development and urbanization further strengthen market demand.

Technological Advancements

Technological innovations in metal pail manufacturing improve efficiency and product quality. Automated forming, welding, and sealing processes reduce defects and ensure uniformity. Advanced coatings enhance corrosion resistance and allow safe storage of chemicals and food products. Lightweight designs reduce transportation costs while maintaining durability. Smart labeling and RFID systems improve supply chain visibility, traceability, and operational efficiency.

Sustainability and Environmental Trends

Sustainability is a major driver for metal pail adoption. Fully recyclable and reusable, metal pails support circular economy principles and reduce environmental impact. Manufacturers adopt water-based coatings, solvent-free adhesives, and energy-efficient production methods. Government regulations and growing consumer demand for eco-friendly products further encourage adoption. Stackable and reusable designs optimize material use and minimize logistical challenges.

Food and Beverage Sector Growth

The food and beverage industry increasingly uses metal pails for bulk storage and transport of oils, syrups, sauces, and dairy products. Metal pails preserve product quality, prevent contamination, and comply with strict safety standards. This sector diversifies applications beyond traditional industrial usage, creating additional growth opportunities.

Market Challenges

The market faces challenges including fluctuating steel and tin prices, affecting production costs and margins. Plastic alternatives remain cheaper and lighter in price-sensitive regions. Heavier weight increases transportation and handling costs. Regional differences in recycling and waste management regulations add complexity. Manufacturers mitigate challenges through supply chain optimization, sustainable practices, and efficient material utilization.

Regional Insights

Asia-Pacific

Asia-Pacific dominates due to industrial growth, infrastructure development, and strong chemical and construction sectors. China, India, and Japan drive demand with cost advantages, local production, and rising domestic consumption.

North America and Europe

North America and Europe maintain growth supported by environmental regulations, recycling programs, and sustainability-focused manufacturing practices. Companies emphasize reusable designs, eco-friendly coatings, and regulatory compliance.

Latin America, Middle East, and Africa

Emerging regions experience growth due to industrial diversification, infrastructure investment, and expansion in chemical and food sectors. Metal pails provide safe storage, comply with international safety standards, and are suitable for long-distance transport.

Competitive Landscape

The market is moderately consolidated, with leading players focusing on innovation, sustainability, and global expansion. Product lines include lightweight, corrosion-resistant, and stackable designs. Strategic partnerships with raw material suppliers reduce costs and ensure operational stability. Regional players compete through customization, rapid delivery, and flexible production. Sustainability initiatives such as eco-friendly coatings and closed-loop recycling strengthen brand positioning. Mergers and acquisitions expand global reach, particularly in emerging economies, enhancing competitiveness.

Future Outlook (2025–2032)

The metal pail market is expected to grow steadily through 2032. Industrial production, chemical manufacturing, and construction activities continue to drive demand. Sustainability trends, regulatory support, and adoption of recyclable packaging will foster growth. Technological innovations, automation, and digital traceability enhance operational efficiency and competitiveness. Asia-Pacific will maintain dominance, while North America and Europe retain substantial market shares. Emerging regions such as Latin America, the Middle East, and Africa offer new opportunities. Manufacturers focusing on innovation, operational efficiency, and environmental responsibility are well-positioned for long-term growth.

Conclusion

The metal pail market is poised for sustained growth due to durability, recyclability, and its critical role in industrial packaging. Technological innovation, sustainability initiatives, and regional expansion ensure continued adoption. Rising industrial demand and regulatory support reinforce metal pails as essential packaging solutions, offering long-term opportunities for global manufacturers and stakeholders.

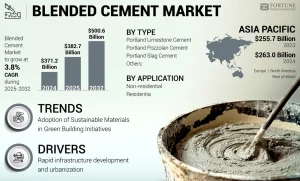

According to Fortune Business Insights, The global blended cement market is experiencing significant growth due to rising demand for sustainable construction materials, strict environmental regulations, and increasing global infrastructure development. Blended cement, made by combining Ordinary Portland Cement (OPC) with supplementary cementitious materials (SCMs) such as fly ash, slag, silica fume, or limestone, helps reduce CO₂ emissions while enhancing strength, durability, and workability.

As the construction industry focuses more on eco-friendly and cost-effective building materials, blended cement has become a vital component of modern infrastructure development worldwide.

Market Size and Growth Forecast

The global blended cement market size was valued at USD 371.2 billion in 2024. The market is projected to grow from USD 382.7 billion in 2025 to USD 500.6 billion by 2032, exhibiting a CAGR of 3.8% during the forecast period. Asia Pacific dominated the blended cement market with a market share of 70.85% in 2024.

This growth is driven by rapid urbanization, large-scale infrastructure projects, and the growing preference for low-carbon building materials across both developed and emerging economies.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/blended-cement-market-113035

Regional Insights

The Asia Pacific region dominated the global blended cement market with a 70.85% share in 2024. Strong construction activity in countries like China, India, and Indonesia, coupled with supportive government policies promoting sustainable development, has boosted demand.

Europe and North America are also witnessing substantial growth due to stricter carbon emission norms and increasing adoption of green building certifications such as LEED and BREEAM. Meanwhile, the Middle East and Africa are expected to show steady growth, supported by rising investments in smart city projects and industrial expansion.

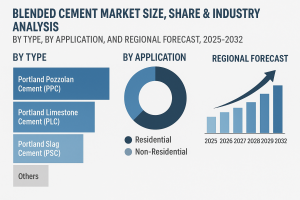

Segmentation Analysis

By Type

Portland Pozzolan Cement (PPC)

Portland Limestone Cement (PLC)

Portland Slag Cement (PSC)

Others

Among these, PPC held the largest market share in 2024 and is expected to retain dominance during the forecast period. Its wide availability, cost-effectiveness, and superior performance in infrastructure and housing projects make it a preferred choice.

PLC is anticipated to record the fastest growth due to its ability to significantly reduce clinker content and associated carbon emissions.

By Application

Residential

Non-Residential

The residential segment leads the market, driven by rapid urbanization, population growth, and increased demand for affordable housing. Blended cement offers enhanced durability and sustainability, making it ideal for residential construction.

The non-residential segment , including commercial, institutional, and industrial projects, is also growing rapidly due to rising infrastructure investments and the need for high-performance, low-carbon building materials.

Market Drivers

Sustainability and Emission Reduction

Blended cement significantly reduces CO₂ emissions by lowering clinker usage, aligning with global sustainability goals and green construction standards.

Government Regulations and Green Building Initiatives

Strict environmental regulations and increasing adoption of eco-friendly building certifications are encouraging the use of blended cement.

Utilization of Industrial By-Products

The use of fly ash, slag, and other industrial by-products not only enhances cement performance but also supports circular economy initiatives by minimizing waste.

Urbanization and Infrastructure Expansion

Rapid growth in infrastructure projects such as roads, bridges, and housing in emerging economies is fueling market demand.

Challenges

Inconsistent Raw Material Availability: Dependence on external industries for fly ash and slag can lead to supply fluctuations.

Standardization Issues: Some regions still rely on outdated standards favoring traditional Portland cement.

Higher Production Costs: Initial investments for adapting production processes and logistics can impact cost efficiency.

Competitive Landscape

Prominent players operating in the global blended cement market include:

- HOLCIM (Switzerland)

- UltraTech Cement Ltd. (India)

- Cemex S.A.B DE C.V. (Mexico)

- Heidelberg Materials (U.S.)

- TAIHEIYO CEMENT CORPORATION (Japan)

- JSW Cement (India)

- Dalmia Bharat Limited (India)

- Anhui Conch Cement Co., Ltd. (China)

- Martin Marietta Materials (U.S.)

- Votorantim Cimentos (Brazil)

These companies are focusing on expanding their blended cement portfolios, improving SCM integration, and investing in R&D to develop low-carbon and high-performance cement products.

Future Trends

The market is expected to reach USD 500.6 billion by 2032, supported by increasing infrastructure spending and environmental awareness.

Technological innovations in cement blending processes and SCM sourcing will further enhance product efficiency.

Growing popularity of Portland Limestone Cement (PLC) is expected to accelerate due to its superior carbon efficiency.

Governments and private sectors are likely to collaborate more closely to promote sustainable cement manufacturing practices.

Information Source: https://www.fortunebusinessinsights.com/blended-cement-market-113035

Key Takeaways

Market Size (2024): USD 371.2 billion

Market Size (2032): USD 500.6 billion

CAGR (2025–2032): 3.8%

Dominant Region: Asia Pacific (70.85% share in 2024)

Leading Type: Portland Pozzolan Cement (PPC)

The blended cement market is positioned for steady expansion over the next decade, driven by global sustainability goals, technological advancements, and increasing infrastructure demand. With governments and corporations prioritizing carbon reduction, the use of blended cement will continue to rise as a cornerstone of eco-friendly construction practices worldwide.

KEY INDUSTRY DEVELOPMENTS

- March 2025: Heidelberg Materials has announced that it will be commissioning an MVR vertical roller mill of the type MVR 5000 C-4 from Gebr Pfeiffer at its existing plant in Airvault, France. The mill will grind and produce ultra-fine Portland cement that will be used in blended cement and other products.

- February 2025: UltraTech commissioned an additional 0.6 Million Tons Per Annum (MTPA) capacity at its existing plant in West Bengal, India. The move is part of the company’s plan to meet the rising demand for cement.

Štiri težave, ki jih mora Hansi Flick rešiti, da bi rešil težave Barcelone na začetku sezone

By jordans1998, 2025-10-17

Pred oktobrskim reprezentančnim premorom je Nogometni dresi za otroke Barcelona v petih dneh dvakrat izgubila, kar je enako število porazov, kot jih je prej doživela v celotnem letu 2025 (brez podaljškov).

Na otvoritveni tekmi Lige prvakov doma proti branilcu naslova Paris Saint-Germainu so doživeli preizkus realnosti, nato pa so s 4:1 izgubili proti Sevilli, ekipi, ki se je v prejšnji sezoni borila za naslov prvaka v La Ligi.

Barcelona je sezono začela neporažena v sedmih tekmah. Vendar pa je ta pregled za temi pozitivnimi rezultati izpostavil vrsto težav, s katerimi se sooča ekipa, ki je v prejšnji sezoni osvojila domači trojček.

Te težave so postale očitne v prvem tednu oktobra. Zdaj, po dveh tednih počitka, se pričakuje, da bo Flick našel rešitve zanje pred sobotno domačo tekmo proti Gironi.

Katere pa so glavne težave, ki so ovirale napredek Barcelone na začetku sezone, in katere težave mora Flick rešiti?

Zloglasna visoka obrambna linija

Flickova napadalna igra, pogum in značilna visoka obrambna linija so pred sezono presenetili nasprotnike in se izkazali za neverjetno uspešne. Zdaj je to postalo problem.

Le tri tekme v sezoni je ekipa Rayo Vallecana pod vodstvom Iñiga Péreza odlično pokazala skrivnost, kako obiti obrambni sistem Barcelone: centralni napadalec se je lahko v prepovedanem položaju prebil za zadnjo linijo in nato diagonalno podal tekaču na krilu. Tekač je nato lahko podal centralnemu napadalcu, ki je bil zdaj v prepovedanem položaju in obrnjen proti vratarju. Bilo je tako preprosto.

Zmagovalec Gonzala Ramosa in drugi gol Seville sta si bila nenavadno podobna.

Vpliv poletnega odhoda Iñiga Martíneza ostaja neizpodbiten. Veteran je bil nekoč vodja in poveljnik Barcelonine obrambe. Dva meseca po začetku sezone je bila obramba Katalonov brez njega še vedno videti kaotična.

Flick mora najti način, kako izboljšati koordinacijo, razmik in komunikacijo med svojo trenutno postavo centralnih branilcev. Razmisliti bi moral tudi o raziskovanju drugačne obrambne oblike, še posebej v poznih fazah tekem, da njegovim branilcem ne bi bilo treba nenehno teči proti lastnim golom.

Skrivnost za prebijanje Flickovega obrambnega sistema že obstaja in najboljše ekipe na svetu je brez oklevanja izkoristijo. Barceloni primanjkuje branilcev, ki so vešči obrambe v nizkem bloku – njihov visoki blok je treba prilagoditi, sicer je Barcelona obsojena na to, da bo še naprej prejemala gole na enak način.

Intenzivnost pritiska

Večina težav z visokim blokom je v njenih napadalnih linijah. Pred sezono je bila intenzivnost pritiska Barcelone vrhunska. V tej sezoni pa so nasprotniki lahko napadali od zadaj z zaskrbljujočo pogostostjo.

Barcelona je ekipa, ki daje prednost osvajanju žoge visoko na igrišču. To jim omogoča, da osvojijo žogo nazaj v ugodnih položajih in s svojo močno napadalno igro ustvarjajo na videz nepredvidljive grožnje.

Morda še pomembneje pa je, da hitro osvajanje žoge Barceloni omogoča varčevanje z energijo. Tudi ko nevarne igre ne izvirajo iz osvajanja žoge nazaj znotraj sredinske črte, omogočajo Barceloni, da začne vzdržno posest. Če nasprotnik uspe obiti presing, mora vsak igralec nenehno porabljati energijo za vrnitev v obrambo.

Rafinhove predstave pred golom v prejšnji sezoni so bile med najboljšimi v njegovi karieri, a njegov prispevek brez žoge je bil morda še bolj ključnega pomena. Njegova odsotnost zaradi poškodbe na zadnjih treh tekmah je bila pomembna. Zdaj morajo drugi napadalci prevzeti svojo odgovornost.

Vse se začne z intenzivnostjo. Že od prve tekme sezone je bil Flick besen nad predstavo svoje ekipe in ta težava se je nadaljevala skozi prvih 10 tekem.

Če želi Barcelona uspeti in preseči merila, ki so jih postavili v prejšnji sezoni, je bistveno ponovno odkriti intenzivnost svojega presinga.

Vloga številke 10

To sezono položaj številke 10 Barceloni praktično ni prispeval ničesar.

Dan Olmo in Fermin López sta odigrala večino igralnega časa, a njunih pet golov je skupaj privedlo do dominantnih zmag nad Getafejem in Valencio – dvema najšibkejšima ekipama, s katerima se je Barcelona doslej pomerila.

Fermin je bil zadnje štiri tekme odsoten, saj se še naprej bori s poškodbo iz prejšnjega obdobja kariere. Pričakuje se, da se bo kmalu vrnil, kar bo spodbudilo napad Barcelone.

Največja skrb pa je Olmova zaskrbljujoča forma. Španski reprezentant se v svoji drugi sezoni pri Barceloni trudi doseči enako formo kot nekoč. Ta izkušeni organizator igre, spreten pri gradnji igre v tesnih prostorih, je v zadnjem času odsoten, saj se muči z ustvarjanjem in zaključevanjem akcij ter se ne odziva učinkovito na presing Barcelone.

Položaj številke 10 je ključnega pomena za napad Barcelone. Flick mora najti način, kako sprostiti svoje ustvarjalne igralce, sicer bo napad Barcelone izgubil ključno dimenzijo.

Olmo trenutno ni na voljo zaradi poškodbe, ki jo je utrpel med reprezentančnim delom. Kljub prejšnjim težavam ostaja Flickova glavna možnost. Barcelona tvega tudi, da bo po vrnitvi Fermina zaradi pomanjkanja razpoložljivih možnosti močno pritisnila nanj.

Gavijeva dolgotrajna odsotnost pomeni, da je 18-letni Dero Fernandez trenutno edina Ferminova zamenjava.

Kondicija igralcev

Poškodbe so Barcelono v zadnjih 10 tekmah precej pestile.

Kljub skorajšnji vrnitvi Najcenejši Lamine Yamal dresi z lastnim imenom in Fermina ostaja seznam poškodb Barcelone dolg. Juan García, Gavi, Rafinha, Olmo in Robert Lewandowski so vsi odsotni, slednja dva pa sta bila zadnji žrtvi.

Alejandro Balde in Frenkie de Jong sta bila prav tako odsotna v začetku te sezone. Tudi v prejšnji sezoni je bilo nekaj poškodb, vendar nikoli toliko kot na začetku.

Poleg tega so nekateri igralci, ki so bili v zadnjem času v formi, proti koncu tekem pokazali znake utrujenosti. Pedri, Marcus Rashford, Paulo Kubalci in Eric García so vsi kazali jasne znake utrujenosti, kar je zaskrbljujoč znak glede na zgodnje faze sezone.

Flick in njegova ekipa morajo oceniti, kako izboljšati splošno stanje ekipe. Na pozitivni strani je do zadnjih faz sezone še dolga pot.

Če pa se bo ta trend nadaljeval, se bo Barcelona mučila in ne bo mogla doseči vrhunca sezone.

Facial Cleanser Market To Be Driven By Wellness Drinks Industry In The Forecast Period Of 2025-2032

By Rushistellar, 2025-10-16

Facial Cleanser Market – Growth, Trends, and Strategic Outlook

Request Free Sample Report: https://www.stellarmr.com/report/req_sample/Facial-Cleanser-Market/1823

Market Overview

The global facial cleanser market is experiencing significant growth, driven by increasing consumer awareness of skincare, rising concerns about skin health, and a growing preference for natural and organic products. Projections indicate a robust expansion from an estimated USD 19.19 billion in 2024 to approximately USD 30.59 billion by 2032, reflecting a compound annual growth rate (CAGR) of 6% during the forecast period

Market Dynamics

Drivers:

Rising Skin Health Awareness: Consumers are becoming more conscious of the importance of skincare, leading to increased demand for facial cleansers that promote healthy skin.

Preference for Natural Ingredients: There is a growing trend towards using facial cleansers formulated with natural and organic ingredients, driven by concerns over skin sensitivity and environmental impact.

E-commerce Expansion: The proliferation of online shopping platforms has made facial cleansers more accessible to a broader audience, facilitating market growth.

Restraints:

Skin Sensitivity Issues: Some consumers experience skin irritation or allergic reactions to certain ingredients in facial cleansers, which may limit product adoption.

Counterfeit Products: The availability of counterfeit facial cleansers in the market poses a challenge to consumer trust and brand reputation.

Market Segmentation

By Product Type:

Foaming Facial Cleanser: Offers a rich lather that effectively removes dirt and oil, catering to consumers with oily or combination skin types.

Gel Facial Cleanser: Provides a lightweight and refreshing cleanse, suitable for acne-prone and sensitive skin.

Cream & Lotion Facial Cleanser: Delivers a moisturizing cleanse, ideal for dry or mature skin types.

Oil Facial Cleanser: Utilizes natural oils to dissolve makeup and impurities, beneficial for all skin types.

Micellar Water: Contains micelles that attract dirt and oil, offering a gentle cleanse without the need for rinsing.

By Skin Type:

Sensitive Skin: Facial cleansers formulated to minimize irritation and maintain the skin's natural barrier.

Oily Skin: Cleansers designed to control excess oil and prevent acne breakouts.

Dry Skin: Hydrating cleansers that replenish moisture and prevent dryness.

Combination Skin: Balanced cleansers that address both oily and dry areas of the face.

By Distribution Channel:

Offline Retail: Supermarkets, pharmacies, and specialty stores remain popular channels for purchasing facial cleansers.

Online Retail: E-commerce platforms offer convenience and a wide range of product options, contributing to the segment's rapid growth.

Regional Insights

North America: Dominates the market, accounting for a significant share due to high consumer awareness and demand for premium skincare products.

Asia-Pacific: Projected to witness the highest growth rate, driven by increasing disposable incomes, urbanization, and a shift towards skincare routines.

Competitive Landscape

Key players in the facial cleanser market include:

Procter & Gamble Co. (Olay): Offers a range of facial cleansers catering to various skin types and concerns.

Unilever (Dove): Known for its gentle and moisturizing facial cleansers.

L'Oréal S.A. (Garnier): Provides a diverse portfolio of facial cleansers targeting different skin needs.

Johnson & Johnson (Neutrogena): Offers dermatologist-recommended facial cleansers.

Beiersdorf AG (NIVEA): Known for its mild and skin-friendly facial cleansing products.

Conclusion

The facial cleanser market is poised for substantial growth, driven by increasing consumer awareness, preference for natural ingredients, and the expansion of online retail channels. Companies focusing on product innovation, catering to diverse skin types, and enhancing consumer trust through quality and transparency are well-positioned to capitalize on the emerging opportunities in this dynamic market.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com

Watermelon Seed Market to be Driven by increasing population in the Forecast Period of 2025-2032

By Rushistellar, 2025-10-16

Watermelon Seed Market – Growth, Trends, and Strategic Outlook

Request Free Sample Report: https://www.stellarmr.com/report/req_sample/Watermelon-Seed-Market/1815

Market Overview

The global watermelon seed market was valued at USD 2.31 billion in 2024 and is projected to reach USD 5.13 billion by 2032 , growing at a compound annual growth rate (CAGR) of 10.45% during the forecast period from 2025 to 2032.

Market Dynamics

Drivers:

Health Benefits: Watermelon seeds are rich in essential fatty acids, magnesium, zinc, and copper, making them a popular choice among health-conscious consumers seeking nutritious snacks.

Rising Demand for Vegan and Gluten-Free Products: As consumer preferences shift towards plant-based and gluten-free diets, watermelon seeds are gaining popularity due to their high protein content and digestibility

Technological Advancements in Cultivation: The development of hybrid and climate-resilient watermelon seed varieties is enhancing yield and quality, driving market growth.

Restraints:

Regulatory Challenges: In certain regions, the sale and use of watermelon seeds are subject to strict regulations, which may hinder market expansion.

Supply Chain Disruptions: Global events and geopolitical tensions can lead to supply chain uncertainties, affecting product availability and pricing.

Market Segmentation

By Seed Type:

Hybrid Diploid Seeds: Held 58% of the market share in 2024.

Hybrid Triploid Seeds: Projected to grow at a CAGR of 12.1% through 2030.

By Treatment:

Untreated Seeds: Accounted for 56% of the market share in 2024.

Film-Coated/Pelleted Seeds: Expanding at a CAGR of 10.2%.

By End User:

Open-Field Cultivation: Owned 72% of the revenue share in 2024.

Protected Cultivation: Represents the fastest growth at a CAGR of 10.7%.

Competitive Landscape

Key players in the watermelon seed market include:

Syngenta Group

BASF SE (Nunhems)

Bayer Crop Science (Seminis)

UPL Limited (Advanta Seeds Limited)

Sakata Seed Corporation

Conclusion

The watermelon seed market is experiencing significant growth, driven by increasing health awareness, demand for plant-based products, and advancements in seed technology. However, challenges such as regulatory constraints and supply chain disruptions need to be addressed to ensure sustainable market expansion. Companies focusing on product innovation, compliance with regulations, and consumer education are well-positioned to capitalize on emerging opportunities in this dynamic sector.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com

เมื่อพูดถึงการเลี้ยง เต่าบก สิ่งหนึ่งที่เจ้าของมือใหม่มักสงสัยมากที่สุดคือ “เต่าบกกินอะไรได้บ้าง?” เพราะอาหารคือปัจจัยสำคัญที่ส่งผลโดยตรงต่อสุขภาพ อายุ และพัฒนาการของเต่า หลายคนอาจคิดว่าเต่าบกกินอะไรก็ได้ แต่จริง ๆ แล้ว เต่าบกมีระบบย่อยอาหารที่ละเอียดอ่อนและต้องการอาหารเฉพาะที่มีไฟเบอร์สูง แคลเซียมมาก และโปรตีนต่ำ บทความนี้จะพาคุณไปรู้จักกับ 9 เมนูอาหารเพื่อสุขภาพของเต่าบก ที่ทั้งปลอดภัยและช่วยให้เต่าของคุณแข็งแรง มีชีวิตชีวา

1. ผักใบเขียวสด – แหล่งไฟเบอร์และแคลเซียมชั้นดี

ผักใบเขียวคืออาหารหลักของ เต่าบก เพราะอุดมไปด้วยวิตามินและแร่ธาตุสำคัญที่ช่วยบำรุงกระดองและกระดูก เช่น ผักคะน้า ผักกาดหอม ผักบุ้ง ผักสลัด และใบตำลึง ควรให้ผักสดที่ล้างสะอาดและไม่มีสารเคมีตกค้าง ควรหลีกเลี่ยงผักที่มีกรดออกซาลิกสูง เช่น ผักโขมหรือผักปวยเล้ง เพราะอาจรบกวนการดูดซึมแคลเซียมของเต่าได้

2. ดอกไม้กินได้ – เพิ่มสีสันและสารอาหาร

เต่าบก หลายสายพันธุ์ชอบกินดอกไม้ โดยเฉพาะเต่าดาวหรือเต่ากรีก ดอกไม้กินได้อย่างเช่น ดอกชบา ดอกกุหลาบ (ที่ไม่พ่นยา) ดอกดาวเรือง และดอกโสน นอกจากจะมีสีสันน่ากินแล้วยังอุดมด้วยสารต้านอนุมูลอิสระ ช่วยเสริมภูมิคุ้มกันและเพิ่มความอยากอาหารให้เต่าด้วย

3. หญ้าและพืชคลุมดิน – อาหารธรรมชาติที่ดีที่สุด

ในธรรมชาติ เต่าบก ส่วนใหญ่ใช้เวลาทั้งวันเดินกินหญ้าและพืชคลุมดิน การให้หญ้า เช่น หญ้าขน หญ้าแพงโกล่า หรือหญ้าเนเปียร์ ถือเป็นทางเลือกที่ดีมาก เพราะช่วยระบบขับถ่ายและรักษาระดับไฟเบอร์ในร่างกาย หากมีพื้นที่กว้าง ควรปลูกหญ้าไว้ให้เต่าได้แทะเองตามธรรมชาติ จะช่วยให้เต่าแข็งแรงและไม่อ้วนเกินไป

4. ผลไม้ – ของว่างที่ให้ได้แต่อย่ามากเกิน

แม้ว่า เต่าบก จะกินผลไม้ได้ แต่ควรให้ในปริมาณน้อย เพราะน้ำตาลในผลไม้มากเกินไปอาจทำให้ย่อยยาก ตัวอย่างผลไม้ที่เหมาะสม ได้แก่ มะละกอสุก แอปเปิล ฝรั่ง แตงโม และกล้วย ให้สัปดาห์ละ 1–2 ครั้งพอเพื่อเสริมวิตามินและช่วยให้เต่ารู้สึกสดชื่น

5. แคลเซียมเสริม – ป้องกันกระดองนิ่มและกระดูกผิดรูป

เต่าบก ต้องการแคลเซียมสูงเพื่อพัฒนากระดองและกระดูก ควรเสริมแคลเซียมในรูปแบบผงโรยบนอาหาร 2–3 ครั้งต่อสัปดาห์ โดยเฉพาะในเต่าที่เลี้ยงในร่มหรือไม่ได้รับแสงแดดเพียงพอ เพราะรังสี UVB จากแสงแดดจำเป็นต่อการดูดซึมแคลเซียม หากขาดอาจทำให้กระดองนิ่มหรือผิดรูปได้

6. ผักสมุนไพร – ตัวช่วยย่อยอาหารและขับลม

ผักสมุนไพรอย่างผักชี ใบสะระแหน่ หรือโหระพาเป็นอาหารที่ดีต่อระบบย่อยของ เต่าบก เพราะช่วยลดแก๊สในลำไส้และเพิ่มภูมิคุ้มกันตามธรรมชาติ ควรให้ในปริมาณน้อยแต่สม่ำเสมอ เพราะกลิ่นหอมของสมุนไพรยังช่วยกระตุ้นความอยากอาหารของเต่าด้วย

7. กระบองเพชรและใบอโลเวรา – อาหารโปรดของเต่าในเขตร้อน

ในแหล่งอาศัยตามธรรมชาติ เต่าบก หลายสายพันธุ์ เช่น Sulcata และ Leopard Tortoise จะกินกระบองเพชรหรือใบอโลเวราเป็นอาหาร เนื่องจากให้ความชุ่มชื้นและมีไฟเบอร์สูง หากจะให้เต่ากินควรปอกหนามออกและล้างให้สะอาดก่อนเสมอ ถือเป็นอาหารที่ช่วยป้องกันภาวะขาดน้ำในเต่าบกได้ดีมาก

8. พืชป่าธรรมชาติ – เสริมความหลากหลายทางโภชนาการ

หากคุณมีพื้นที่ธรรมชาติหรือสวนหลังบ้าน ลองหาพืชป่าที่ปลอดสารพิษ เช่น ใบหญ้าน้ำพุ ใบมันสำปะหลังอ่อน หรือใบตำแย ซึ่งเป็นอาหารที่ เต่าบก ในธรรมชาติชอบกินมาก การให้เต่ากินพืชหลายชนิดจะช่วยให้ได้รับสารอาหารครบถ้วนและไม่เบื่ออาหาร

9. น้ำสะอาด – สิ่งที่เต่าห้ามขาด

แม้ว่า เต่าบก จะไม่ใช่สัตว์น้ำ แต่ “น้ำ” ก็เป็นสิ่งจำเป็นอย่างยิ่ง เต่าบกควรมีภาชนะน้ำที่แช่ตัวได้ตลอดเวลา เพื่อให้เต่าสามารถดื่มและรักษาความชุ่มชื้นของผิวหนัง การแช่น้ำอุ่นสัปดาห์ละ 2–3 ครั้งยังช่วยระบบขับถ่ายและป้องกันอาการท้องผูก ซึ่งเป็นปัญหาพบบ่อยในเต่าบกที่กินผักแห้งหรืออาหารไม่สด

เคล็ดลับการให้อาหาร เต่าบก อย่างถูกวิธี

ให้ผักสดใหม่ทุกวันในช่วงเช้า เต่าน้ำ เย็น

หลีกเลี่ยงอาหารที่มีแป้งหรือโปรตีนสูง เช่น ข้าว ถั่ว หรือเนื้อสัตว์

อย่าให้อาหารซ้ำชนิดเดียวทุกวัน ควรหมุนเวียนเพื่อความหลากหลาย

ใช้จานตื้นหรือแผ่นหินรองอาหาร เพื่อป้องกันการกลืนทรายหรือดินเข้าไป

สังเกตพฤติกรรมการกินของเต่าบก หากกินน้อยลงหรือไม่ถ่าย ควรปรึกษาสัตวแพทย์ทันที

สรุป

อาหารที่เหมาะสมคือหัวใจของการเลี้ยง เต่าบก ให้แข็งแรงและอายุยืน เต่าบกควรได้รับอาหารที่มีไฟเบอร์สูง แคลเซียมเพียงพอ และโปรตีนต่ำ โดยเน้นผักใบเขียว หญ้า และดอกไม้เป็นหลัก เสริมผลไม้บ้างเล็กน้อยและจัดให้มีน้ำสะอาดตลอดเวลา หากเจ้าของใส่ใจในเรื่องโภชนาการ เต่าบกของคุณจะไม่เพียงมีสุขภาพดีเท่านั้น แต่ยังมีสีสันสดใส เคลื่อนไหวกระฉับกระเฉง และเป็นเพื่อนคู่ใจไปอีกหลายสิบปี

Market Overview

The Global Nuts Market , valued at USD 63.64 billion in 2024 , is projected to reach USD 97.66 billion by 2032 , growing at a CAGR of 5.5% during the forecast period.

The market is primarily driven by the rising demand for healthy snacks , increasing awareness of nutritional benefits , and the growing adoption of plant-based and vegan diets worldwide. Nuts are versatile ingredients used across multiple applications—from snacks to confectionery, dairy alternatives, and functional foods—making them one of the most dynamic categories in the global food industry.

In recent years, nut-based products such as nut butters, plant-based milk, and protein bars have witnessed significant adoption. Food brands are actively marketing nuts as “natural energy boosters” and “heart-healthy snacks,” strengthening their position in both developed and emerging markets.

Gain Valuable Insights – Request Your Complimentary Sample Now @ https://www.maximizemarketresearch.com/request-sample/187767/

Market Size and Growth Projections

The growth is attributed to:

Expansion in nut-based value-added products .

Increased export potential from emerging economies due to advanced agroecological farming practices .

Strong consumer preference for natural protein-rich and fiber-dense foods .

The food processing and packaging sectors are also playing a crucial role by innovating products that enhance shelf life, flavor diversity, and on-the-go convenience.

Key Market Drivers

Health and Wellness Trends: Rising consumer focus on fitness and heart health drives demand for almonds, walnuts, pistachios, and cashews.

Plant-Based and Vegan Diets: Nuts serve as a key protein substitute in vegan and flexitarian diets.

Functional and Convenience Foods: Nuts are increasingly used in bakery, confectionery, and ready-to-eat snacks.

Nutritional Awareness: Growing understanding of nuts’ benefits, including omega-3 fatty acids, antioxidants, vitamins, and minerals.

E-commerce Growth: Online retail channels have broadened accessibility for organic and premium nut varieties.

Market Restraints

High Production Costs: Exotic and imported nuts face supply chain issues, inconsistent yields, and high processing expenses.

Allergy Concerns: Peanut and tree nut allergies restrict consumption among certain consumers, necessitating strict labeling compliance.

Price Volatility: Dependence on seasonal yields and climatic conditions impacts global pricing trends.

Feel free to request a complimentary sample copy or view a summary of the report: https://www.maximizemarketresearch.com/request-sample/187767/

Market Opportunities

Plant-Based Dairy and Meat Alternatives: Expanding markets for almond milk, cashew cheese, and nut-based yogurt.

Product Diversification: Innovative flavors (roasted, salted, spiced) and convenient packaging formats attract a wider demographic.

Organic and Sustainable Farming: Rising preference for ethically sourced and eco-friendly nut products.

Emerging Markets: Asia-Pacific and Middle East regions offer strong potential due to health awareness and rising disposable incomes.

Market Challenges

Supply Chain Complexity: Multiple intermediaries in sourcing and distribution affect product quality and traceability.

Food Safety Risks: Contamination by aflatoxins or pathogens like Salmonella poses health and regulatory risks.

Quality Control: Maintaining consistent moisture content and size across global markets is a continuous challenge.

Market Segmentation

By End Use

Foodservice Industry: Largest segment (CAGR 5.8%)—nuts are widely used in restaurants, cafes, and catering.

Household: Increasing home consumption due to the rise in healthy snacking and baking trends.

By Product

Almonds: Dominant segment; rising use in skincare and health foods.

Peanuts: Widely consumed in confectionery and sauces; supports weight management.

Cashews: Popular globally; major export crop for Asia and Africa.

Walnuts: High omega-3 content; used in bakery and sauces.

Hazelnuts: Integral to the chocolate industry; growing demand in premium confectionery.

Pistachios: Popular among diabetic consumers; high antioxidant content.

By Form

Whole (Plain, Roasted, Salted): Major share due to convenience and portability.

Powdered Nuts: Growing application in gluten-free and high-protein foods.

Dive deeper into the market dynamics and future outlook: https://www.maximizemarketresearch.com/request-sample/187767/

Regional Insights

North America:

Leads the global market with a CAGR of 5.6%. The U.S. and Canada are key contributors, driven by health-conscious consumers and organic farming adoption.

Europe:

Steady growth driven by healthy snacking and sugar reduction trends. Germany, the U.K., and France are major consumption hubs.

Asia Pacific:

Fastest-growing region due to rising awareness of nut-based health benefits and increasing vegan population in India, Japan, and China.

Middle East & Africa:

Expanding consumption owing to WHO recommendations for incorporating nuts into daily diets. Strong growth in GCC nations.

South America:

Brazil and Argentina lead production, particularly of cashews and Brazil nuts, with rising export opportunities.

Key players in the Nuts market

1. Borges Agricultural & Industrial Nuts.

2. Diamond Foods, Inc.

3. John B. Sanfilippo & Son.

4. Ludlow Nut Co Ltd.

5. Hines Nut Company.

6. Mariani Nut Company.

7. Germack Pistachio Company.

8. Hampton Farms, Inc.

9. Star Snacks Co. LLC.

10. Grower Direct Nut Co. Ltd.

11. Wildly Organic.

12. TIERRA FARM

13. Big Tree Organic Farms

14. Food to Live.

15. Truefarm Foods

16. Forest Whole Foods Ltd

17. prana organic

18. Wholefood Earth

19. South Valley Farms

20. Blue Diamond Growers

Conclusion

The global nuts market is on a steady upward trajectory, supported by health-driven consumption patterns, product innovation, and rising demand for plant-based nutrition. While challenges such as allergy concerns and cost fluctuations persist, opportunities in functional foods, sustainable sourcing, and premium snacking will sustain long-term growth.

Companies investing in product differentiation, traceability, and sustainable production are best positioned to capitalize on the expanding global demand for nuts.

More Related Reports

Global Yeast Market https://www.maximizemarketresearch.com/market-report/yeast-market/617/

Global Vinegar market https://www.maximizemarketresearch.com/market-report/global-vinegar-market/26017/

Liquid Feed Market https://www.maximizemarketresearch.com/market-report/liquid-feed-market/146056/

About Us

The global linerless labels market share is set to gain momentum from their rising demand from the packaging & labeling industry. It is mainly occurring as the concerns regarding liner waste are upsurging. This information is published by Fortune Business Insights™ The report further mentions that the linerless labels market size was USD 2.33 billion in 2019 and is projected to reach USD 3.43 billion by 2027, exhibiting a CAGR of 5.0% during the forecast period.

Fortune Business Insights™ lists out the names of all the companies present in the global market. They are as follows:

Gipako UAB, Hub Labels, Cenveo Corporation, Reflex Labels Ltd., Skanem AS, NAStar Inc., 3M, Coveris, Avery Dennison Corporation, Ravenwood Packaging, Innovia Films, Constantia Flexibles, Lexit Group AS, RR Donnelley & Sons Company, Optimum Group, SATO Europe GmbH, Tereoka Seiko Co., Ltd., L&N Label Company, Preprint Group, DuraFast Label Company, Bizerba Australia, Bostik, Dykam A.C.A. Ltd., Weber Packaging Solutions

Get a Free Sample PDF :-

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/linerless-labels-market-102778

Drivers & Restraints-

Rising Usage of Attractive & Food-safe Labels to Spur Growth

Brand recognition plays a vital role when it comes to the sales of food products worldwide. Labeling is a significant part of branding. The utilization of food-safe and attractive labels helps the food and beverage industry to grow. In the Latin American and Asian countries, namely, Brazil, Japan, and Southeast Asia, food products, such as fruits, bacon, and ham are packed with liner-free labels. Also, several ruling bodies have put forward strict norms and regulations regarding the information that is to be printed on the labels of food products.

Unlike conventional labels, linerless labels are capable of including 30% more print. In addition to this, manufacturers won’t have to change the dimensions of linerless labels and thus, they can be easily used instead of the traditional ones. They are also cost-effective and hence, are very popular in the food and beverage sector. The expansion of the food and beverage industry across the globe is likely to contribute to the growth of the backless labels market growth in the coming years. However, the regular shapes of linerless labels may not fulfill the requirements for a novel trademark. It may hamper growth.

Segment-

Food & Beverage Segment to Hold Largest Share Backed by the High Demand for Linerless Labels

Based on application, the market is segregated into logistics, retail, pharmaceutical & personal care, food & beverage, and others. Amongst these, the retail segment held 16.9% liner-free labels market share in 2019. The food & beverage segment is expected to procure the largest share throughout the forthcoming period as it is necessary for prominent companies to differentiate their products from the competitors. Therefore, they need a wide variety of labels to showcase authentic information regarding the contents of the product.

Competitive Landscape-

Key Players Focus on R&D Activities to Develop New Products

The market is semi-consolidated. Most of the top players are investing hefty amounts of money in research and development activities to introduce innovative linerless labels and their components. Below are two of the latest key industry developments:

- January 2020 : Bostik unveiled its new linerless label adhesive. It is mainly designed to improve efficiencies of the production line and deliver sustainable packaging, especially for quick service restaurant applications.

- May 2019 : R.R. Donnelley & Sons Company (RRD) announced the broadening of its label manufacturing platform. It added a 26” linerless press for this expansion. The press was developed by ETI Converting Equipment.

Regional Analysis-

Growth of E-commerce to Drive Market in Asia Pacific

Geographically, the market is categorized into the Middle East and Africa, Latin America, Asia Pacific, Europe, and North America. Out of these, Asia Pacific generated USD 892.5 million in revenue in 2019. This growth is attributable to the expansion of e-commerce in this region. North America is anticipated to grow considerably backed by the presence of a well-established retail sector in the U.S. Also, the demand for retail and personal care goods would upsurge because of the outbreak of the Covid-19 pandemic. For gaining the confidence of customers, companies are demanding eye-catching labels for their products. In Europe, the market is set to grow steadily owing to the high demand from the pharmaceutical industry.

Key Players Assessment in this Research:

- The report offers a detailed analysis of leading companies in the market across the globe.

- It provides details of the major vendors involved in this market

- A comprehensive overview of each company including the company profile generated revenue, pricing of goods, and the manufactured products is incorporated in the report.

- The facts and figures about market competitors along with standpoints of leading market players are presented in the report.

Inquire Before Buying This Report:

https://www.fortunebusinessinsights.com/enquiry/queries/linerless-labels-market-102778

About Us:

Fortune Business Insights™ offers expert corporate analysis and accurate data, helping organizations of all sizes make timely decisions. We tailor innovative solutions for our clients, assisting them to address challenges distinct to their businesses. Our goal is to empower our clients with holistic market intelligence, giving a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights™ Pvt. Ltd.

9th Floor, Icon Tower, Baner-Mahalunge Road,

Baner, Pune-411045, Maharashtra, India.

Phone:

US: +1 424 253 0390

UK: +44 2071 939123

APAC: +91 744 740 1245

Email: sales@fortunebusinessinsights.com