Blogs

Infants & Toddlers Toy Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2032

By Intel Market Research, 2025-10-06

According to a new report from Intel Market Research , the g lobal Infants & Toddlers Toy market was valued at USD 831 million in 2024 and is projected to reach USD 1,811 million by 2032 , growing at a robust CAGR of 11.9% during the forecast period (2025–2032). This significant growth is driven by increasing parental focus on early childhood development, rising disposable incomes in emerging markets, and the proliferation of innovative educational toys that combine play with learning.

What are Infants & Toddlers Toys?

Infants & Toddlers Toys are specialized play and learning tools designed for children aged 0-6 years, created to stimulate curiosity, imagination, and creativity during critical developmental stages. These toys range from basic building blocks, puzzles, and art supplies to sophisticated electronic learning devices and role-playing sets. Beyond entertainment, they serve important educational functions by helping develop language skills, enhance cognitive and analytical abilities, improve hand-eye coordination, and foster imagination and critical thinking.

Given that infants and toddlers are in crucial growth phases, these toys must adhere to stringent safety standards during design and manufacturing to prevent any potential harm. The market offers remarkable diversity in materials, pricing, shapes, structures, colors, and functionalities to meet the varying needs and interests of different age groups within this demographic.

Download Sample Report : Infants & Toddlers Toy Market - View in Detailed Research Report

Key Market Drivers

1. Growing Emphasis on Early Childhood Development and Education

The increasing recognition of early childhood as a critical period for cognitive and emotional development has become a primary market driver. Modern parents and educators increasingly seek toys that offer educational value alongside entertainment , fueling demand for products that promote STEM learning, language acquisition, and social skills. Research from child development experts confirms that appropriately designed toys can significantly enhance neural connections during these formative years, making educational toys a priority for conscious parenting.

2. Rising Disposable Income and Demographic Shifts

Growing middle-class populations in emerging economies, particularly in the Asia-Pacific region , have substantially increased spending power dedicated to children's products. The ongoing urbanization trend and the increasing number of dual-income households have further amplified this effect. Additionally, demographic patterns showing sustained birth rates in developing regions versus declining but more premium-focused markets in developed economies create a diverse but consistently growing global demand pattern.

3. Digital Transformation and E-commerce Expansion

The rapid growth of online retail channels has dramatically improved accessibility to a wide variety of toys across geographic regions. E-commerce platforms offer parents extensive product information, reviews, and competitive pricing, while also enabling niche and specialty toy manufacturers to reach global audiences without traditional brick-and-mortar limitations. The convenience of online shopping, coupled with enhanced digital marketing strategies targeting parents, has significantly expanded market reach and consumer awareness.

Market Challenges

- Stringent Safety Regulations and Compliance Costs : Manufacturers face increasing regulatory requirements across different regions, particularly concerning material safety, choking hazards, and chemical composition, leading to higher production and compliance costs.

- Counterfeit Products and Brand Protection : The market faces significant challenges from counterfeit products that not only impact brand reputation but also pose serious safety risks to children, requiring substantial investment in anti-counterfeiting measures.

- Price Sensitivity in Emerging Markets : While demand is growing in developing regions, price sensitivity remains a considerable challenge, balancing quality and safety standards with affordability constraints.

- Rapidly Changing Consumer Preferences : The toy industry must continuously innovate to keep pace with evolving educational trends, technological advancements, and changing play patterns, requiring significant R&D investment.

Opportunities Ahead

The global shift toward sustainable and eco-friendly products presents substantial growth opportunities. Environmentally conscious parents are increasingly seeking toys made from renewable materials, with non-toxic finishes, and sustainable manufacturing processes. This trend aligns with the broader movement toward responsible consumption and offers premium positioning opportunities for manufacturers.

Additionally, the integration of smart technology and interactive features continues to create new market segments. Augmented reality toys, coding kits for young children, and interactive learning systems represent the frontier of toy innovation, blending physical play with digital enhancements to create engaging educational experiences.

Emerging markets, particularly in Southeast Asia, Latin America, and Africa , present significant untapped potential. As disposable incomes rise and educational awareness grows, these regions are expected to contribute substantially to market growth through:

- Localized product development catering to regional preferences and cultural contexts

- Expanded distribution networks reaching rural and underserved areas

- Public-private partnerships promoting early childhood development initiatives

Download Sample PDF : Infants & Toddlers Toy Market - View in Detailed Research Report

Regional Market Insights

- North America : Dominates the premium segment with high safety standards and strong demand for educational toys. The region benefits from well-established retail networks and high consumer awareness about child development products.

- Europe : Characterized by stringent safety regulations and growing demand for sustainable toys. Western European markets show particular strength in wooden and eco-friendly toy segments, with Germany and Scandinavia leading innovation in educational toys.

- Asia-Pacific : The fastest-growing region, driven by rising middle-class populations, increasing disposable incomes, and growing emphasis on early education. China represents both a manufacturing hub and the largest consumer market, while Southeast Asian countries show remarkable growth potential.

- Latin America : Emerging markets with growing retail infrastructure and increasing parental investment in educational toys. Brazil and Mexico lead regional growth with improving economic conditions.

- Middle East & Africa : Developing markets with growing awareness about early childhood development. Gulf Cooperation Council countries show premium market characteristics, while African markets present long-term growth opportunities as economic conditions improve.

Market Segmentation

By Type

- Intellectual Games

- Creative Games

- Ball Games

- Other

By Application

- Family

- Kindergarten

- Early Childhood Education Center

- Nursery

- Other

By Distribution Channel

- Specialty Stores

- Department Stores

- Online Retail

- Other Retail Formats

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Get Full Report : Infants & Toddlers Toy Market - View in Detailed Research Report

Competitive Landscape

The global Infants & Toddlers Toy market features a diverse competitive landscape with established multinational corporations, specialized educational toy manufacturers, and innovative startups. The market is characterized by continuous product innovation, brand building, and strategic partnerships with educational institutions.

The report provides in-depth competitive profiling of key players, including:

- Melissa & Doug

- Hape

- Green Toys

- Plan Toys

- Manhattan Toy

- Janod

- VTech

- Skip Hop

- Lamaze

- Tiny Love

- Infantino

- HABA

- Djeco

- B. Toys

- Fat Brain Toys

- Cuddle + Kind

- Tegu

- Smart Noggin

- Manhattan Toy Company

- Kiddieland

Report Deliverables

- Global and regional market forecasts from 2025 to 2032

- Strategic insights into product innovations, market trends, and consumer preferences

- Market share analysis and competitive SWOT assessments

- Pricing analysis and distribution channel dynamics

- Comprehensive segmentation by product type, application, distribution channel, and geography

- Analysis of regulatory environment and safety standards across regions

- Impact assessment of digital transformation and e-commerce growth

Get Full Report Here : Infants & Toddlers Toy Market - View in Detailed Research Report

Download Sample PDF : Infants & Toddlers Toy Market - View in Detailed Research Report

Browse More Reports:

https://www.intelmarketresearch.com/food-liability-insurance-market-3419

https://www.intelmarketresearch.com/global-india-battery-modulepack-equipment-forecast-market-10322

https://www.intelmarketresearch.com/global-india-color-resists-forecast-market-10325

https://www.intelmarketresearch.com/veterinary-antibacterial-prescription-drugs-market-2817

https://www.intelmarketresearch.com/d-laser-vision-positioning-system-market-2872

https://www.intelmarketresearch.com/beverage-microbiological-testing-equipment-market-2828

https://www.intelmarketresearch.com/global-india-herbal-medicine-forecast-market-10362

https://www.intelmarketresearch.com/united-states-yogurt-powders-market-10711

https://www.intelmarketresearch.com/cough-lozenges-market-2824

https://www.intelmarketresearch.com/electronic-radiator-thermostats-market-3206

https://www.intelmarketresearch.com/united-states-bindersscaffolders-for-meatmeat-substitutes-market-10528

https://www.intelmarketresearch.com/united-states-ready-to-drink-cold-brew-coffee-market-10666

https://www.intelmarketresearch.com/x-ray-digital-subtraction-angiography-machine-market-2999

https://www.intelmarketresearch.com/paintless-grade-pmmaasa-market-2891

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in financial services , insurance , and risk management . Our research capabilities include:

- Real-time industry benchmarking

- Regulatory impact analysis

- Over 500+ annual sector reports

Trusted by Fortune 500 companies, our insights empower decision-makers to navigate complex markets with confidence.

Website : https://www.intelmarketresearch.com

Contact : +1 (332) 2424 294

The caps & closures market size was valued at USD 73.49 billion in 2023 and is projected to grow from USD 77.45 billion in 2024 to USD 125.10 billion by 2032, exhibiting a CAGR of 6.18% during the forecast period. There is an enormous range in the shapes and sizes of caps and closures. Depending on the specifications and intended application, they can be made of cork, metal, plastic rubber, or other materials. The growing demand for convenient and environmentally friendly packaging alternatives is driving the global market. Fortune Business Insights presents this information in their report titled "Global Caps & Closures Market, 2025–2032."

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/102542

Segmentation Analysis:

Several Features Offered by Plastic Propels Demand

Based on the material, the market is segmented into plastic, metal, and others. Due to plastics’ chemical stability and cost-effectiveness, it dominates the market.

Screw Caps Leads the Market due to Safety Features

Based on the product type, the market is segmented into tethered caps, push/pull caps, screw caps, and others. High sealing capability, child-resistant, and convenience primarily drive the screw caps market.

Brand Recognition due to Attractive Packaging Drives Segmental Growth

Based on the end-use industry, the market is segmented into food & beverages, pharmaceutical, consumer goods, personal care & cosmetics, and others. The food & beverages segment dominates the market as caps and closures create brand awareness among consumers.

Geographically, the market is studied across North America, South America, Europe, Asia Pacific, and the Middle East and Africa.

Drivers & Restraints:

Safety and Convenience Offered by Caps & Closures to Increase Demand

The urban population tends to consume food and beverages available in packaged form as they keep the product fresh, are convenient, and offer an air-tight seal to keep the food items safe from bacteria. Therefore, during the projected period the caps & closures market share is anticipated to increase. On the contrary, alternative packaging options like blisters, pouches, and others that are cost-effective may stifle the caps & closures market.

Regional Insights

High Income Changing Lifestyle Boosts Market in Europe

Europe is one of the dominating regions of the caps & closures market as changing lifestyles and increased disposable incomes have led to a huge demand for alcoholic beverages, carbonated drinks, and other items. Increased demand from the cosmetics industry also drives the market. North America also has a large share due to rising innovations, key manufacturers, and the processed food and healthcare sector.

Competitive Landscape

Companies Focus on Producing Creative Packaging Solutions to Foster Growth

Much fragmentation and competition exist in the caps & closures global market. Due to their creative packaging offerings in the packaging sector, a select few significant businesses control a considerable market share. The market's leading companies concentrate on innovation, grow the market's revenue, and diversify their client base across the geographies.

List of Key Companies Profiled:

- BERICAP Holding GmbH (Germany)

- Guala Closures S.p.A (Italy)

- Closure Systems International, Inc. (U.S.)

- Amcor Plc (Australia)

- Silgan Holdings Inc. (U.S.)

- Aptar Group (U.S.)

- UNITED CAPS (Luxembourg)

- Nippon Closures Co., Ltd. (Japan)

- Mold-Rite Plastics, LLC (U.S.)

- O.Berk Company, LLC (U.S.)

- Pelliconi & C. Spa. (Italy)

- Weener Plastics (Netherlands)

- Blackhawk Molding Co. Inc. (U.S.)

- C. L. Smith Company (U.S.)

- Elmoris, Jsc (U.S.)

Key Industry Development:

- July 2022 - Guala Closures, a global leading producer of closures for spirits, wines, beverages and oil bottles acquired Labrenta. The acquisition took place to strengthen Guala Closure's presence in the luxury segment.

- January 2023 - Aptar Pharma, part of AptarGroup, Inc., launched APF Futurity™, its first metal-free and highly recyclable, multidose nasal spray pump developed to deliver nasal saline and other comparable over-the-counter (OTC) formulations.

Get Your Customization Research Report:

https://www.fortunebusinessinsights.com/enquiry/customization/102542

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower,

Baner - Mahalunge Road, Baner,

Pune-411045, Maharashtra, India.

Phone:

US: +18339092966

UK: +448085020280

APAC: +91 744 740 1245

Email: sales@fortunebusinessinsights.com

Food Liability Insurance Market Size, Share, Trends, Growth, Strategies, Opportunities, Top Companies, Regional Analysis and Forecast 2025-2032

By Market research desk, 2025-10-06

According to a new report from Intel Market Research , the global Food Liability Insurance market was valued at USD 887 million in 2024 and is projected to reach USD 1,300 million by 2032 , growing at a steady CAGR of 5.6% during the forecast period (2024–2032). This growth is driven by increasing regulatory scrutiny in the food industry, rising consumer awareness about food safety, and the growing number of foodborne illness lawsuits.

What is Food Liability Insurance?

Food Liability Insurance is a specialized liability coverage protecting food manufacturers, distributors, and retailers against financial losses arising from claims of foodborne illnesses, contamination, mislabeling, or allergic reactions. This insurance covers legal defense costs, settlements, and medical expenses when consumers suffer harm from consuming insured products. It's increasingly becoming non-negotiable in an era where a single contamination incident can lead to multi-million dollar lawsuits and reputational damage.

Leading insurers now offer tailored policies covering everything from product recalls to third-party liability claims . The evolving risk landscape—including emerging food safety regulations and litigious consumer behavior—makes this insurance essential for businesses of all sizes in the food value chain.

Download Sample Report :

Food Liability Insurance Market - View in Detailed Research Report

Key Market Drivers

1. Stringent Food Safety Regulations

Governments worldwide are tightening food safety standards. The FDA's Food Safety Modernization Act (FSMA) in the U.S. and the EU's General Food Law Regulation now impose stricter accountability measures. Non-compliance penalties coupled with mandatory recall protocols have forced food businesses to prioritize liability coverage. Regulatory complexities differ by region, but the common thread is clear: stringent oversight equals greater insurance demand.

2. Rising Foodborne Illness Litigation

High-profile cases—like the $25 million Chipotle E. coli settlement—demonstrate growing legal risks. Data shows food illness lawsuits increased by 32% from 2015–2023 , with average settlement values climbing. Restaurants, processed food brands, and agricultural producers face particular exposure. Insurance has become a financial lifeline when facing claims involving allergen mislabeling, pathogen contamination, or ingredient toxicity.

Market Segmentation

By Insurance Type

- Product Liability Insurance : Covers claims from product-related injuries/illnesses

- Public Liability Insurance : Protects against third-party property damage/bodily injury

- Recall Insurance : Specific to product withdrawal expenses

By End User

- Food Manufacturers

- Restaurants & Food Service

- Agricultural Producers

- Distributors & Retailers

Regional Market Insights

- North America : Dominates with 42% market share due to high litigation rates and strict FDA oversight

- Europe : Strong growth in Germany/France from allergen labeling laws

- Asia-Pacific : Fastest-growing region with expanding food safety regulations

Competitive Landscape

Major players like Chubb, AIG, and Zurich lead the market, while insurtech firms like Next Insurance are disrupting traditional underwriting with AI-driven solutions. The report analyzes 12+ key providers on coverage options, pricing strategies, and regional strengths.

Get Full Report :

Food Liability Insurance Market - View in Detailed Research Report

Browse more related report

https://www.intelmarketresearch.com/veterinary-antibacterial-prescription-drugs-market-2817

https://www.intelmarketresearch.com/d-laser-vision-positioning-system-market-2872

https://www.intelmarketresearch.com/global-india-battery-modulepack-equipment-forecast-market-10322

https://www.intelmarketresearch.com/global-india-color-resists-forecast-market-10325

https://www.intelmarketresearch.com/global-india-herbal-medicine-forecast-market-10362

https://www.intelmarketresearch.com/united-states-bindersscaffolders-for-meatmeat-substitutes-market-10528

https://www.intelmarketresearch.com/united-states-ready-to-drink-cold-brew-coffee-market-10666

https://www.intelmarketresearch.com/x-ray-digital-subtraction-angiography-machine-market-2999

https://www.intelmarketresearch.com/paintless-grade-pmmaasa-market-2891

https://www.intelmarketresearch.com/cough-lozenges-market-2824

https://www.intelmarketresearch.com/electronic-radiator-thermostats-market-3206

https://www.intelmarketresearch.com/united-states-yogurt-powders-market-10711

https://www.intelmarketresearch.com/beverage-microbiological-testing-equipment-market-2828

https://www.intelmarketresearch.com/infants-toddlers-toy-market-2805

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in financial services , insurance , and risk management . Our research capabilities include:

- Real-time industry benchmarking

- Regulatory impact analysis

- Over 500+ annual sector reports

Trusted by Fortune 500 companies, our insights empower decision-makers to navigate complex markets with confidence.

Website : https://www.intelmarketresearch.com

Contact : +1 (332) 2424 294

Global Pro Video Equipment Market Research Report 2025(Status and Outlook)

By SiliconSage, 2025-10-06

The global Pro Video Equipment Market , valued at US$ 8,470 million in 2024, is poised for substantial growth, projected to reach US$ 13,240 million by 2032. This expansion, representing a compound annual growth rate (CAGR) of 6.5%, is detailed in a comprehensive new report published by Semiconductor Insight. The study underscores the pivotal role of professional video equipment in enabling high-quality content creation across broadcast, film, live events, and digital media sectors.

Professional video equipment, encompassing cameras, audio gear, lighting, and accessories, has become indispensable for delivering the visual fidelity and production quality demanded by today's audiences. The shift towards 4K/8K resolution, HDR imaging, and immersive audio formats is driving continuous innovation and investment in production technology. These tools are fundamental to minimizing production bottlenecks and optimizing creative workflows, making them the backbone of modern media production.

Streaming Content Expansion: The Primary Growth Engine

The report identifies the explosive growth of streaming media platforms as the paramount driver for pro video equipment demand. With the streaming segment accounting for approximately 40% of total professional video equipment application, the correlation is direct and substantial. The global streaming market itself is projected to exceed $250 billion annually, fueling demand for production equipment across all levels.

"The massive concentration of content production facilities and streaming platform investments in North America and Europe, which together consume about 65% of global pro video equipment, is a key factor in the market's dynamism," the report states. With global investments in streaming content production exceeding $300 billion through 2030, the demand for high-quality production equipment is set to intensify, especially with the transition to 8K resolution and virtual production requiring advanced technical capabilities.

Read Full Report: https://semiconductorinsight.com/report/global-pro-video-equipment-market/

Market Segmentation: Camera Systems and Broadcast Applications Dominate

The report provides a detailed segmentation analysis, offering a clear view of the market structure and key growth segments:

Segment Analysis:

By Equipment Type

- Camera Systems

- Audio Equipment

- Lighting Equipment

- Accessories and Support Gear

By Application

- Broadcast Television

- Film Production

- Live Events and Sports

- Corporate Video Production

- Streaming Content Creation

- Education and Training

- Aviation and Defense

- Others

By Technology

- HD (1080p)

- 4K UHD

- 8K UHD

- HDR and High Frame Rate

- Virtual Production Technologies

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=95987

Competitive Landscape: Key Players and Strategic Focus

The report profiles key industry players, including:

-

Sony Corporation (Japan)

-

Panasonic Corporation (Japan)

-

Blackmagic Design (Australia)

-

Canon Inc. (Japan)

-

ARRI (Germany)

-

Red Digital Cinema (U.S.)

-

AJA Video Systems (U.S.)

-

Ross Video (Canada)

-

Evertz Microsystems (Canada)

-

Shure Incorporated (U.S.)

-

Sennheiser Electronic GmbH (Germany)

-

Yamaha Corporation (Japan)

-

Roland Corporation (Japan)

These companies are focusing on technological advancements, such as integrating AI for automated production workflows, and geographic expansion into high-growth regions like Asia-Pacific to capitalize on emerging opportunities.

Emerging Opportunities in Virtual Production and Remote Workflows

Beyond traditional drivers, the report outlines significant emerging opportunities. The rapid adoption of virtual production techniques and remote collaboration tools presents new growth avenues, requiring advanced camera tracking, real-time rendering, and network infrastructure. Furthermore, the integration of cloud-based production ecosystems is a major trend. Smart production equipment with IoT-enabled monitoring can reduce production setup time by up to 50% and improve workflow efficiency significantly.

Report Scope and Availability

The market research report offers a comprehensive analysis of the global and regional Pro Video Equipment markets from 2025–2032. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trends, and an evaluation of key market dynamics.

For a detailed analysis of market drivers, restraints, opportunities, and the competitive strategies of key players, access the complete report.

Download FREE Sample Report: Global Pro Video Equipment Market - View in Detailed Research Report

Get Full Report Here: Global Pro Video Equipment Market Research Report 2025(Status and Outlook) - View in Detailed Research Report

Related Reports:

https://semiconductorinsight.com/report/global-pro-video-equipment-market/

https://semiconductorinsight.com/report/global-semiconductor-euv-photomask-inspection-equipment-market/

https://semiconductorinsight.com/report/global-gauge-pressure-sensor-ics-market/

https://semiconductorinsight.com/report/4d-radar-chip-market/

https://semiconductorinsight.com/report/airbag-chip-market/

https://semiconductorinsight.com/report/lighting-control-dimming-panel-market/

https://semiconductorinsight.com/report/industrial-led-lighting-market/

https://semiconductorinsight.com/report/global-touch-control-chip-market/

https://semiconductorinsight.com/report/global-automotive-interface-bridge-integrated-circuits-market/

https://semiconductorinsight.com/report/global-semiconductor-alcohol-sensors-market-size/

https://semiconductorinsight.com/report/multi-loop-pid-temperature-regulators-market/

https://semiconductorinsight.com/report/global-desktop-usb-port-chargers-market/

https://semiconductorinsight.com/report/mobile-document-reader-market/

https://semiconductorinsight.com/report/global-microprojector-market/

https://semiconductorinsight.com/report/fbg-strain-sensor-market/

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

Website : https://semiconductorinsight.com/

International : +91 8087 99 2013

LinkedIn : Follow Us

Minimally Invasive Fascial Suture Device Market Regional Analysis, Demand Analysis and Competitive Outlook 2025-2032

By lifesciencesid, 2025-10-06

Date – 06-10-2025

[ Pune , India ]

Minimally invasive fascial suture devices are advanced surgical tools used for suturing the fascia during laparoscopic or minimally invasive procedures. These devices enable precise closure of small incisions with minimal tissue trauma, helping reduce complications such as bleeding and incisional hernias. Designed to enhance procedural efficiency and patient safety, these devices are increasingly adopted in hospitals and surgical centers globally. They are available in single-use and reusable configurations and play a critical role in the growing adoption of minimally invasive surgical techniques.

"Comprehensive Insights: Download Our Latest Industry Report"

Market Size

The Global Minimally Invasive Fascial Suture Device Market was valued at USD 71.1 million in 2024 and is projected to reach USD 108 million by 2031 , growing at a CAGR of 6.3% during the forecast period (2025–2032).

This robust growth is driven by the increasing preference for minimally invasive procedures , a rise in laparoscopic surgeries , and the healthcare industry’s emphasis on infection control and faster patient recovery . Additionally, advancements in medical device design and integration with robotic-assisted systems further contribute to market expansion.

Market Dynamics

Drivers

- Rising Demand for Minimally Invasive Surgeries:

Surgeons increasingly favor minimally invasive approaches due to shorter hospital stays, reduced pain, and quicker recovery. These factors are boosting demand for precision closure tools such as fascial suture devices. - Technological Advancements:

Innovations in device ergonomics, suture anchoring systems, and compatibility with laparoscopic instruments are driving product adoption. - Enhanced Infection Control Standards:

The growing emphasis on sterile, disposable surgical devices aligns with the rising use of single-use fascial closure devices , especially in high-volume hospitals.

Restraints

- High Cost of Advanced Devices:

Despite their benefits, minimally invasive fascial suture devices are relatively expensive, limiting access in cost-sensitive healthcare systems. - Sterilization Challenges for Reusable Devices:

Reusable devices require rigorous reprocessing to ensure sterility, adding operational burdens and potential risks of contamination.

Opportunities

- Expansion into Emerging Markets:

Developing countries in Asia-Pacific, Latin America, and the Middle East are rapidly investing in healthcare infrastructure, creating growth opportunities for device manufacturers. - Integration with Robotic Surgery Systems:

The growing use of surgical robots opens avenues for specialized fascial suture tools designed for robotic-assisted applications.

Challenges

- Stringent Regulatory Approvals:

Medical device manufacturers must navigate complex regulatory pathways across regions, which can delay product launches. - Training and Skill Requirements:

Surgeons need adequate training to utilize these advanced devices effectively, posing a barrier to adoption in low-resource settings.

Regional Analysis

North America

North America dominates the global market, driven by advanced healthcare infrastructure, high surgical volumes, and the presence of key players like Medtronic and Teleflex . The United States, in particular, exhibits strong demand for disposable fascial closure devices , supported by stringent infection control protocols.

Europe

Europe holds a substantial market share due to government-supported healthcare reforms and high awareness of minimally invasive procedures. Countries such as Germany, France, and the U.K. are at the forefront of adopting advanced surgical technologies.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, fueled by a surge in laparoscopic surgeries, rising healthcare expenditure, and expanding hospital networks in China, India, and Japan . Local manufacturers such as Shandong Bainus Medical Instrument and Weipu Medical are enhancing regional competitiveness.

Latin America

Latin America is experiencing steady growth due to increased adoption of cost-effective surgical solutions in countries like Brazil and Mexico , alongside government investments in healthcare modernization.

Middle East & Africa

The region shows promising potential as healthcare infrastructure continues to develop. Growing partnerships between international and regional manufacturers are expected to boost access to advanced suture devices.

"Comprehensive Insights: Download Our Latest Industry Report"

Competitor Analysis

The Minimally Invasive Fascial Suture Device Market is moderately competitive, featuring both established multinational corporations and emerging regional manufacturers. Key players focus on innovation, regulatory compliance, and strategic distribution networks to strengthen their global presence.

Major Companies Include:

- Teleflex

- Medtronic

- CooperSurgical

- Shandong Bainus Medical Instrument

- Golden Stapler Surgical

- Suture Ease

- EndoSystem

- Weipu Medical

- Longmed

- Aofo

- Double Medical Technology

- Dongfeng Yihe

- WODELIPAI

- Portoria Medical

- Anrei Sinolinrs

- Shenghua Medical

These players prioritize R&D investments to enhance device precision, ergonomics, and integration with advanced laparoscopic and robotic platforms.

Market Segmentation (By Type)

Single Use Fascial Closure Device

The single-use segment dominates the market due to its superior hygiene standards and ability to reduce the risk of cross-contamination. These devices are highly preferred in hospitals with large surgical volumes and are compliant with infection prevention guidelines.

Reusable Fascial Closure Device

Reusable devices, while cost-effective over time, require strict sterilization protocols. Their adoption is higher in facilities with lower surgical turnover and access to advanced sterilization systems.

Market Segmentation (By Application)

Hospital

Hospitals represent the largest application segment , driven by the high frequency of complex laparoscopic and abdominal surgeries. The increasing integration of minimally invasive surgery suites further strengthens hospital demand.

Clinic

Clinics use fascial suture devices for outpatient laparoscopic interventions , offering patients faster recovery and lower procedural costs.

Others

This category includes ambulatory surgical centers and specialized surgical facilities , which contribute to overall market growth through broader accessibility and streamlined care pathways.

Key Company Strategies

Market leaders are focusing on:

- Launching ergonomically advanced , easy-to-handle devices.

- Expanding distribution partnerships to penetrate emerging markets.

- Collaborating with surgical training centers to promote device adoption.

- Securing regulatory approvals to broaden product portfolios globally.

Geographic Segmentation

|

Region |

Market Share (2024) |

Key Growth Drivers |

|

North America |

35% |

High surgical volume, strong regulatory compliance |

|

Europe |

28% |

Advanced healthcare systems, growing laparoscopic procedures |

|

Asia-Pacific |

25% |

Rising healthcare investment, expanding hospital networks |

|

Latin America |

7% |

Increasing adoption of cost-effective medical devices |

|

Middle East & Africa |

5% |

Growing healthcare infrastructure and partnerships |

"Comprehensive Insights: Download Our Latest Industry Report"

About 24lifesciences

Founded in 2017, 24LifeScience has emerged as a trusted research and analytics partner for organizations operating within the global life sciences and chemical industries. Our core mission is to provide intelligent, future-ready insights that help clients stay ahead in an increasingly complex and innovation-driven market

International: +1(332) 2424 294 | Asia: +91 9425150513 (Asia)

Website: http://www.24lifesciences.com

Follow us on LinkedIn: http://www.linkedin.com/company/lifesciences24

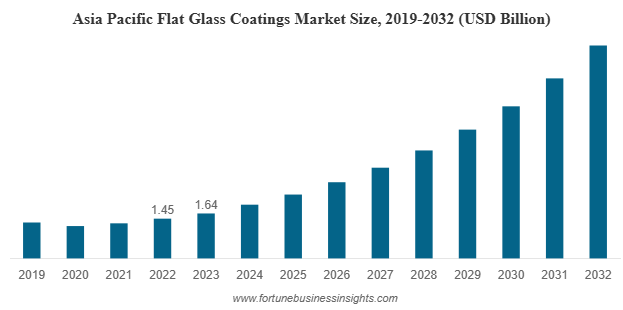

The global flat glass coatings market was valued at USD 2.50 billion in 2023 and is projected to expand from USD 2.98 billion in 2024 to USD 11.50 billion by 2032, registering an impressive CAGR of 18.0% during the forecast period. Asia Pacific emerged as the leading region, accounting for 65.6% of the global market share in 2023.

List Of Key Companies Profiled:

- Arkema S.A. (France)

- The Sherwin-Williams Company (U.S.)

- Nippon Sheet Glass Co., Ltd (Japan)

- Guardian Glass (U.S.)

- Ferro Corporation (U.S.)

- Fenzi Group (Italy)

- Corning Inc. (U.S.)

- Vitro Architectural Glass (Mexico)

- Hesse GmbH & Co. KG (Germany)

- Viracon (U.S.)

Market Overview

Flat glass coatings market have evolved from being just a protective layer to a core enabler of performance, energy efficiency, and sustainability across industries. From architectural façades to solar panels and automotive glazing, coated glass is redefining how modern infrastructure interacts with light, heat, and the environment. As technology advances and green building initiatives expand, the global flat glass coatings market is witnessing remarkable growth and innovation.

The market’s transformation is also linked to technological advancements in nanocoatings, water-based solutions, and multifunctional protective layers that enhance glass performance in various environmental conditions.

Key Growth Drivers

Rising Demand for Solar Energy Applications

One of the strongest forces driving the flat glass coatings market is the rapid growth of the solar energy industry. Solar panels rely on coated glass to improve energy absorption and minimize light reflection. Anti-reflective and hydrophobic coatings play a crucial role in increasing efficiency and reducing maintenance costs for photovoltaic systems. As renewable energy adoption accelerates worldwide, the need for high-performance coatings in solar panels is expected to multiply.

Sustainable Construction and Energy Efficiency Trends

The construction industry is undergoing a major sustainability transformation. Governments and private developers are investing in green buildings that reduce energy consumption and improve occupant comfort. Coated flat glass helps achieve these goals by controlling heat transfer, blocking harmful UV rays, and allowing optimal daylight transmission. Low-emissivity (Low-E) coatings, for instance, have become essential in modern architecture for maintaining thermal balance and reducing energy costs.

Technological Advancements in Coating Materials

Innovation is another cornerstone of this market’s expansion. The industry is moving toward water-based coatings and nano-coatings that deliver better performance while complying with environmental regulations. Water-based coatings produce lower volatile organic compound (VOC) emissions, aligning with sustainability standards. Meanwhile, nano-coatings provide additional benefits such as self-cleaning, anti-bacterial, anti-fog, and scratch-resistant properties. These advancements not only improve durability but also open up new applications in automotive, electronics, and decorative sectors.

Market Challenges

While the outlook is highly positive, certain challenges persist.

- Environmental Regulations: Traditional solvent-based coatings often contain high levels of VOCs, which can be harmful to both the environment and human health. Stringent environmental rules across Europe and North America have limited their usage, pushing manufacturers to invest in cleaner alternatives.

- Raw Material Volatility: Price fluctuations in raw materials, including resins and solvents, can affect production costs and profit margins.

- Supply Chain Disruptions: The pandemic underscored vulnerabilities in global supply chains, highlighting the importance of local sourcing and diversification strategies.

Market Segmentation Insights

- By Resin Type

Acrylic resins dominate the flat glass coatings market, valued for their exceptional weather resistance, clarity, and cost-effectiveness. Polyurethane and epoxy resins follow closely, providing enhanced durability and chemical resistance for demanding environments.

- By Technology

Water-based coatings hold the largest market share due to their eco-friendly characteristics and regulatory compliance. However, nano-coating technology is emerging as the fastest-growing segment, driven by its superior optical clarity, resistance, and multifunctionality.

- By Application

The mirror application segment currently leads the market, particularly in interior design and automotive sectors. Architectural applications are growing rapidly as smart cities and energy-efficient infrastructure projects increase worldwide. Solar, decorative, and automotive applications are also witnessing robust growth, supported by aesthetic preferences and functional requirements.

Read More : https://www.fortunebusinessinsights.com/flat-glass-coatings-market-102910

Regional Analysis

- Asia Pacific

Asia Pacific remains the dominant regional market, accounting for approximately 65.6% of the global share in 2023. The growth is largely attributed to massive infrastructure development, rapid urbanization, and expanding solar energy capacity in countries such as China, India, and Japan. The region’s booming construction and automotive industries further amplify demand for advanced glass coatings.

- North America and Europe

Both North America and Europe are expected to post steady growth through 2032. Stringent energy-efficiency regulations, coupled with strong adoption of solar technologies and green building standards, are major contributing factors. Europe, in particular, is witnessing significant demand for low-E and anti-reflective coatings in both residential and commercial buildings.

- Rest of the World

Regions such as the Middle East, Africa, and Latin America are gradually embracing flat glass coatings, driven by the expansion of construction and renewable energy projects. Increasing awareness about sustainable materials and technological modernization is expected to create new growth avenues across these markets.

Key Industry Developments:

- September 2021: Guardian Glass started to produce 130” x 240” or superjumbo, SunGuard coatings on clear or Guardian UltraClear float glass at its Carleton, Michigan facility. The flat glass manufacturer has responded to the demand from architects who have pushed design boundaries with buildings that maximize views and natural light for occupants in forward-thinking facades while also reaching energy performance codes and standards.

- April 2021: Ferro Corporation, a leading global supplier of technology-based functional coatings and color solutions, announced that Prince International Corporation (Prince) has completed the previously announced acquisition of Ferro.

Competitive Landscape

The flat glass coatings industry is characterized by intense competition and continuous innovation. Leading companies are focusing on R&D initiatives, strategic partnerships, and geographic expansion to strengthen their global presence. Manufacturers are also investing in advanced coating technologies that enhance energy efficiency, optical quality, and longevity while minimizing environmental impact.

Future Outlook

Looking ahead, the flat glass coatings market is poised for transformative growth. The integration of nanotechnology, eco-friendly water-based solutions, and smart coatings will redefine performance standards in the glass industry. Moreover, the growing emphasis on sustainability and energy conservation will continue to boost adoption across multiple sectors.

In the next decade, the industry’s trajectory will be shaped by innovations that merge functionality with environmental responsibility. Companies that prioritize R&D investment, align with evolving regulations, and cater to high-growth applications—particularly in solar energy and green construction—will be best positioned to lead this dynamic market.

According to a new report from Intel Market Research , the India Color Resists Market was valued at US$ 134 million in 2024 and is projected to reach US$ 206 million by 2032 , growing at a CAGR of 7.4% during the forecast period (2024–2032). This steady expansion is driven by increasing display production capabilities within India, rising consumer demand for high-resolution and wide color gamut displays, and significant advancements in nanomaterial-based color resist technologies.

What are Color Resists?

Color resists are photosensitive polymer materials used to create precise color filters in display manufacturing processes. These critical components are applied to glass substrates through photolithography to form red, green, and blue subpixels that enable vibrant color reproduction in electronic displays. The technology represents a sophisticated intersection of chemistry, materials science, and precision engineering, requiring exceptional purity, thermal stability, and photochemical properties.

These specialized materials serve as the foundation for color reproduction in both LCD (Liquid Crystal Display) and OLED (Organic Light-Emitting Diode) technologies, with formulations varying significantly between display types. The Indian market has seen particular growth in color resists optimized for mobile displays and automotive applications, where color accuracy and durability are paramount.

Download Sample Report : India Color Resists Market - View in Detailed Research Report

Key Market Drivers

1. Expanding Display Manufacturing Ecosystem

India's display manufacturing capabilities have experienced remarkable growth, particularly with the government's Production Linked Incentive (PLI) scheme for large-scale electronics manufacturing. This initiative has attracted significant investments from global display panel manufacturers, creating substantial demand for upstream materials including color resists. The establishment of new panel fabrication facilities across states like Maharashtra, Uttar Pradesh, and Tamil Nadu has created a robust ecosystem that supports domestic color resist consumption.

The push toward Atmanirbhar Bharat (Self-Reliant India) has further accelerated domestic manufacturing across the electronics value chain. While color resist production requires sophisticated chemical engineering capabilities, several Indian companies have developed indigenous formulations that compete with international standards, particularly for entry-level and mid-range display applications.

2. Growing Demand for High-Resolution Displays

The Indian consumer electronics market has demonstrated increasing sophistication, with demand shifting toward higher resolution displays featuring wider color gamuts and enhanced brightness. This trend is particularly evident in the smartphone sector, where Full HD+ and Quad HD+ resolutions have become standard even in mid-range devices. The automotive display sector has similarly evolved, with digital instrument clusters and infotainment systems requiring advanced color resist technologies.

This consumer-driven demand for superior visual experiences necessitates color resists with higher pigment concentrations, improved thermal stability, and enhanced color purity. Manufacturers are responding by developing formulations that support narrower pixel pitches and higher aperture ratios, enabling the vibrant, high-contrast displays that modern consumers expect.

3. Technological Advancements in Nanomaterial-Based Formulations

The development of nanomaterial-based color resists represents a significant technological frontier in display materials. These advanced formulations utilize nano-sized pigment particles that offer superior optical properties, including higher transparency, improved color strength, and reduced light scattering. Indian research institutions and chemical companies have made notable progress in developing indigenous nano-pigment technologies that reduce dependence on imported materials.

Recent innovations include quantum dot-enhanced color resists that enable wider color gamuts exceeding 100% of the NTSC standard , meeting the demanding requirements of premium displays. Additionally, environmentally friendly formulations with reduced solvent content and improved development characteristics are gaining traction as manufacturers seek to minimize environmental impact while maintaining performance standards.

Market Challenges

- Raw material dependency : India remains heavily dependent on imported specialty chemicals and pigments for color resist production, creating supply chain vulnerabilities and cost pressures.

- Technical expertise gap : The highly specialized nature of color resist formulation and manufacturing requires sophisticated technical knowledge that remains concentrated among a limited number of experienced chemists and engineers.

- Capital intensity : Establishing color resist manufacturing facilities requires significant investment in cleanroom infrastructure, precision coating equipment, and quality control instrumentation, creating barriers to entry.

- Global competition : Indian manufacturers face intense competition from established international players who benefit from economies of scale and decades of research and development experience.

Opportunities Ahead

The Indian color resists market presents numerous growth opportunities driven by technological evolution and policy support. The government's focus on electronics manufacturing and chemical industry development creates a favorable environment for domestic production of advanced display materials.

Emerging application areas including flexible displays , transparent displays , and micro-LED technology require specialized color resist formulations that represent new market segments. Indian companies that develop expertise in these advanced areas can capture significant value as these technologies transition from laboratory to mass production.

Notably, several leading Indian chemical companies have announced expansion plans and research initiatives focused on display materials:

- Development of color resists for next-generation display technologies including foldable OLED and micro-LED

- Investment in research and development facilities specifically dedicated to electronic chemicals and display materials

- Strategic partnerships with display panel manufacturers to develop customized formulations for specific applications

- Exploration of export opportunities to other emerging markets seeking alternatives to traditional supply sources

Download Sample PDF : India Color Resists Market - View in Detailed Research Report

Regional Market Insights

- Western India : Leads market share owing to established chemical manufacturing clusters in Maharashtra and Gujarat, proximity to major ports for raw material imports, and concentration of display panel assembly facilities.

- Southern India : Emerging as a significant hub with growing electronics manufacturing in Karnataka and Tamil Nadu, supported by strong academic institutions and research centers focused on materials science.

- Northern India : Showing rapid growth due to new electronics manufacturing corridors in Uttar Pradesh and infrastructure development supporting industrial expansion.

- Eastern India : Currently developing manufacturing capabilities with several new industrial parks and special economic zones announced for electronics production.

Market Segmentation

By Type

- Color Resist Materials for LCD

- Color Resist Materials for OLED

By Application

- TVs

- Monitors

- Notebook and Tablet

- Mobile Phones

- Automotive Displays

- Wearable Devices

- Others

By End User

- Display Panel Manufacturers

- Electronics Assembly Services

- Automotive Electronics Suppliers

- Consumer Electronics Brands

By Technology

- Conventional Color Resists

- Advanced Nanomaterial-Based Resists

- Environment-Friendly Formulations

Get Full Report : India Color Resists Market - View in Detailed Research Report

Competitive Landscape

The India Color Resists Market features a mix of domestic chemical companies and multinational corporations serving the display industry. While the market remains relatively concentrated, several Indian manufacturers have developed competitive capabilities in specific segments and applications.

The report provides in-depth competitive profiling of key players, including:

- Atul Ltd

- Pidilite Industries

- BASF India Ltd

- Asian Paints

- Kansai Nerolac Paints Ltd

- Berger Paints India Ltd

- Akzo Nobel India Ltd

- Jotun India Pvt. Ltd

- Aarti Industries Ltd

- DIC India Ltd

These companies are pursuing strategies including technological innovation, capacity expansion, strategic partnerships with display manufacturers, and development of specialized formulations for emerging applications.

Report Deliverables

- Comprehensive market size and forecast data from 2024 to 2032

- Detailed analysis of market drivers, restraints, and opportunities

- Competitive landscape assessment with market share analysis

- Technical analysis of color resist formulations and manufacturing processes

- Supply chain analysis and raw material sourcing assessment

- Regulatory environment and policy impact analysis

- Strategic recommendations for market participants

Get Full Report : India Color Resists Market - View in Detailed Research Report

Download Sample PDF : India Color Resists Market - View in Detailed Research Report

Browse more related report

https://www.intelmarketresearch.com/veterinary-antibacterial-prescription-drugs-market-2817

https://www.intelmarketresearch.com/d-laser-vision-positioning-system-market-2872

https://www.intelmarketresearch.com/global-india-battery-modulepack-equipment-forecast-market-10322

https://www.intelmarketresearch.com/food-liability-insurance-market-3419

https://www.intelmarketresearch.com/global-india-herbal-medicine-forecast-market-10362

https://www.intelmarketresearch.com/united-states-bindersscaffolders-for-meatmeat-substitutes-market-10528

https://www.intelmarketresearch.com/united-states-ready-to-drink-cold-brew-coffee-market-10666

https://www.intelmarketresearch.com/x-ray-digital-subtraction-angiography-machine-market-2999

https://www.intelmarketresearch.com/paintless-grade-pmmaasa-market-2891

https://www.intelmarketresearch.com/cough-lozenges-market-2824

https://www.intelmarketresearch.com/electronic-radiator-thermostats-market-3206

https://www.intelmarketresearch.com/united-states-yogurt-powders-market-10711

https://www.intelmarketresearch.com/beverage-microbiological-testing-equipment-market-2828

https://www.intelmarketresearch.com/infants-toddlers-toy-market-2805

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in advanced materials , chemicals , and electronics manufacturing . Our research capabilities include:

- Real-time competitive benchmarking

- Global supply chain and technology monitoring

- Country-specific regulatory and industry analysis

- Over 500+ specialized industry reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website : https://www.intelmarketresearch.com

International : +1 (332) 2424 294

Asia-Pacific : +91 9169164321

LinkedIn : Follow Us

Hot Sauce Market Size, Share, Report Insights: Growth Forecast Through 2032

By Deven3042, 2025-10-06

The global hot sauce market was valued at USD 3.30 billion in 2024 and is projected to rise to USD 3.54 billion in 2025. By 2032, the market is anticipated to reach approximately USD 5.98 billion, expanding at a CAGR of 7.78% during the forecast period (2025–2032). North America dominated the global landscape in 2024 with a 44.24% share. Within the region, the U.S. market is set for remarkable growth, estimated to reach around USD 1.94 billion by 2032, driven by the increasing demand for Mexican and Asian cuisines and the introduction of innovative product formulations by major brands.

The ongoing globalization of culinary trends continues to propel the use of condiments, seasonings, and sauces across international markets. Hot sauce, known for its intense umami flavor and adaptability, has become a popular choice for a wide range of dishes—from savory meat products to sweet and salty snacks. Additionally, expanding international distribution networks and branding efforts by leading manufacturers are expected to strengthen the industry’s growth trajectory.

Information Source: https://www.fortunebusinessinsights.com/industry-reports/hot-sauce-market-100495

Market Segmentation

The hot sauce market is categorized based on type into Tabasco pepper sauce, Habanero pepper sauce, Jalapeño sauce, sweet and spicy sauce, and other varieties.

Among these, Tabasco pepper sauce held approximately 23% of the global share in 2022, supported by growing consumer interest in bold and complex flavor experiences. Meanwhile, the sweet and spicy sauce segment is experiencing rapid growth due to its balanced taste and health-oriented appeal. Rising flavor experimentation and interest in ethnic condiments further boost its adoption.

By distribution channel, supermarkets and hypermarkets remain the leading retail platforms, accounting for the largest market share in 2021, as they continue to be the preferred outlets for chili sauce purchases. However, online retail is expanding quickly owing to digital transformation, convenience, and wider product access—especially across emerging economies.

Report Coverage

The report provides a detailed analysis of:

- Key market drivers, restraints, and challenges

- Emerging opportunities and industry trends

- Regional market performance and consumption analysis

- Profiles of major market participants

- Strategic developments such as product launches, collaborations, and mergers & acquisitions

Growth Drivers and Challenges

Rising Popularity of Ethnic Flavors to Drive Market Expansion

The increasing global fascination with Latin American and Asian cuisines has been a central factor fueling hot sauce demand. Markets such as India and China are witnessing heightened exposure to Mexican-style flavors, influencing taste preferences and creating opportunities for cayenne and chili-based sauces.

Furthermore, growing immigration to Western nations from Asia-Pacific and South America is diversifying culinary offerings and expanding the availability of hot sauces in mainstream retail. The surging interest in gourmet and adventurous food experiences among younger consumers is another key factor supporting market growth.

Volatility in Raw Material Prices May Restrict Growth

Despite strong growth prospects, the market faces challenges from fluctuating prices of essential ingredients, including tomatoes, chili peppers, and jalapeños. Supply chain interruptions, particularly those seen during the COVID-19 pandemic, significantly impacted both production volumes and raw material costs, affecting profitability across the value chain.

Regional Insights

North America Retains Market Leadership

In 2022, the North American hot sauce market was valued at USD 1.28 billion. High consumer spending power and evolving taste preferences have transformed hot sauce from a niche ethnic product into a mainstream household condiment across the U.S. and Canada. Both countries are among the world’s top importers of chili-based sauces, reinforcing their dominance in the global market.

Competitive Landscape

Innovation and Collaboration as Key Competitive Strategies

The global hot sauce market is moderately consolidated, with several leading international companies competing through flavor innovation, marketing collaborations, and strategic partnerships. Continuous product diversification and brand positioning efforts are helping companies strengthen their market presence. Many players are experimenting with new heat levels, exotic flavors, and regional blends to attract diverse consumer groups.

Major Companies Profiled:

- The Kraft Heinz Company (U.S.)

- McCormick & Company, Inc. (U.S.)

- Campbell Soup Company (U.S.)

- Unilever PLC (U.K.)

- Conagra Brands, Inc. (U.S.)

- McIlhenny Company (U.S.)

- Southeastern Mills, Inc. (U.S.)

- Hormel Foods Corporation (U.S.)

- Baumer Foods, Inc. (U.S.)

- T.W. Garner Food Company (U.S.)

Get Sample PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/hot-sauce-market-100495

Recent Industry Development:

- November 2020 – Mountain Dew (PepsiCo) collaborated with NBA star Joel Embiid to introduce the brand’s first-ever hot sauce, merging beverage branding with bold flavor innovation.

Global Semiconductor EUV Photomask Inspection Equipment Market Research Report 2025(Status and Outlook)

By SiliconSage, 2025-10-06

The global Semiconductor EUV Photomask Inspection Equipment Market , valued at US$ 1.15 billion in 2024, is poised for substantial growth, projected to reach US$ 2.28 billion by 2032. This expansion, representing a compound annual growth rate (CAGR) of 9.14% during the forecast period 2025-2032, is detailed in a comprehensive new report published by Semiconductor Insight. The study underscores the indispensable role of these advanced inspection systems in enabling next-generation semiconductor manufacturing, particularly for nodes below 7nm where EUV lithography has become essential.

EUV photomask inspection equipment represents the critical quality control layer in semiconductor fabrication, ensuring defect-free patterns are transferred onto silicon wafers with nanometer precision. These systems have become increasingly vital as chipmakers push the boundaries of Moore's Law, where even sub-nanometer defects can render entire wafers unusable. The technology's evolution has been remarkable, transitioning from optical inspection methods to sophisticated actinic (EUV wavelength) systems that can detect phase defects and other anomalies invisible to traditional inspection methods.

Semiconductor Miniaturization Drive: The Core Growth Catalyst

The report identifies the relentless pursuit of semiconductor miniaturization as the primary driver for EUV photomask inspection equipment demand. With the semiconductor industry segment accounting for approximately 92% of the total market application, the correlation is direct and powerful. The global semiconductor equipment market itself is projected to exceed $120 billion annually, creating substantial demand for complementary inspection and metrology solutions.

"The massive concentration of advanced semiconductor manufacturing in the Asia-Pacific region, which consumes about 76% of global EUV photomask inspection systems, is a fundamental factor shaping market dynamics," the report states. With worldwide investments in new semiconductor fabrication facilities surpassing $600 billion through 2030, the requirement for ultra-precise inspection solutions continues to intensify, particularly for 3nm and below node production where defect tolerances approach atomic scales.

Read Full Report: https://semiconductorinsight.com/report/global-semiconductor-euv-photomask-inspection-equipment-market/

Market Segmentation: Die-to-Die Inspection and IC Manufacturing Dominate

The report provides detailed segmentation analysis, offering clear visibility into market structure and high-growth segments:

Segment Analysis:

By Type

- Die-to-Die (DD) Inspection

- Die-to-Database (DB) Inspection

- Hybrid Inspection Systems

- Other Specialized Inspection Methods

By Application

- IC Manufacturers

- Mask Shops

- Foundries

- Research and Development Institutions

- Semiconductor Equipment Manufacturers

- Academic Research Facilities

By Technology

- Optical Inspection Systems

- E-Beam Inspection Systems

- Multi-Beam Inspection Technology

- Actinic EUV Inspection Systems

- Hybrid Inspection Solutions

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=95950

Competitive Landscape: Technology Leaders and Strategic Positioning

The report profiles key industry players, including:

-

KLA Corporation (U.S.)

-

ASML Holding NV (Netherlands)

-

Lasertec Corporation (Japan)

-

Carl Zeiss AG (Germany)

-

Applied Materials, Inc. (U.S.)

-

Vision Technology Inc. (South Korea)

-

NuFlare Technology (Japan)

-

Holon Corporation (Japan)

-

SUSS MicroTec (Germany)

-

Advantest Corporation (Japan)

These companies are focusing on technological breakthroughs, particularly in artificial intelligence-enhanced defect detection and multi-beam inspection technologies, while expanding their presence in high-growth regions like Asia-Pacific to capture emerging opportunities.

Emerging Opportunities in Advanced Packaging and Heterogeneous Integration

Beyond traditional semiconductor manufacturing drivers, the report highlights significant emerging opportunities in advanced packaging and heterogeneous integration. The rapid growth of chiplet-based designs and 3D packaging technologies creates new requirements for inspection solutions that can verify interconnects and through-silicon vias. Furthermore, the integration of machine learning and computational metrology represents a major trend, with AI-powered inspection systems reducing false detection rates by up to 40% while improving throughput significantly.

Report Scope and Availability

The market research report offers a comprehensive analysis of the global and regional Semiconductor EUV Photomask Inspection Equipment markets from 2025-2032. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trend analysis, and evaluation of key market dynamics.

For detailed analysis of market drivers, restraints, opportunities, and competitive strategies of key players, access the complete report.

Read Full Report: https://semiconductorinsight.com/report/global-semiconductor-euv-photomask-inspection-equipment-market/

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=95950

Related Reports:

https://semiconductorinsight.com/report/global-semiconductor-euv-photomask-inspection-equipment-market/

https://semiconductorinsight.com/report/global-gauge-pressure-sensor-ics-market/

https://semiconductorinsight.com/report/4d-radar-chip-market/

https://semiconductorinsight.com/report/airbag-chip-market/

https://semiconductorinsight.com/report/lighting-control-dimming-panel-market/

https://semiconductorinsight.com/report/industrial-led-lighting-market/

https://semiconductorinsight.com/report/global-touch-control-chip-market/

https://semiconductorinsight.com/report/global-pro-video-equipment-market/

https://semiconductorinsight.com/report/global-automotive-interface-bridge-integrated-circuits-market/

https://semiconductorinsight.com/report/global-semiconductor-alcohol-sensors-market-size/

https://semiconductorinsight.com/report/multi-loop-pid-temperature-regulators-market/

https://semiconductorinsight.com/report/global-desktop-usb-port-chargers-market/

https://semiconductorinsight.com/report/mobile-document-reader-market/

https://semiconductorinsight.com/report/global-microprojector-market/

https://semiconductorinsight.com/report/fbg-strain-sensor-market/

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high-technology industries. Our in-depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high-quality, data-driven research to our clients worldwide.

Website : https://semiconductorinsight.com/

International : +91 8087 99 2013

LinkedIn : Follow Us

Automatic Door Market Expanding Modern Infrastructure with Intelligent, Energy-Efficient, and Automated Entry Solutions

By saloni dutta, 2025-10-06

The Automatic Door Market is experiencing strong growth due to rising demand for automated, energy-saving, and user-friendly entry systems. Airports, hospitals, retail complexes, corporate offices, and residential buildings are increasingly adopting automatic doors to improve operational efficiency, accessibility, and hygiene. Integration with smart sensors, AI-based controls, and IoT technology ensures responsive operation, predictive maintenance, and energy conservation. These systems have become vital components of intelligent, sustainable, and modern infrastructure worldwide, supporting both environmental goals and user convenience in contemporary architecture.

Smart Integration Enhancing Building Efficiency

Automation is a key driver of the Automatic Door Market. Motion sensors, infrared detectors, and AI-based control systems enable doors to operate efficiently, minimizing unnecessary openings and conserving energy. Integration with building management systems provides centralized monitoring, predictive maintenance, and optimized operational performance, enhancing overall building functionality.

Automatic doors also promote accessibility for differently-abled individuals and meet international building standards. Remote-controlled and voice-activated systems offer convenience in high-traffic commercial areas and smart residential projects, ensuring modern infrastructure requirements are met.

Energy Efficiency and Sustainability

Energy efficiency is a major factor supporting market growth. Advanced sealing mechanisms, low-power motors, and smart sensor systems maintain indoor climate control, reduce HVAC energy consumption, and lower operational costs. Some doors include renewable energy features, such as solar-powered sensors, further reducing environmental impact.

Green construction projects, including LEED-certified buildings, increasingly prioritize energy-efficient automatic doors. By combining automation with sustainability, these doors contribute to environmentally responsible and cost-effective infrastructure.

Technological Innovations

Technological advancement continues to shape the market. Modern automatic doors incorporate IoT connectivity, AI-driven predictive controls, and cloud-based monitoring, improving efficiency, reliability, and user experience. Modular and lightweight designs simplify installation and retrofitting, making doors suitable for both new constructions and existing buildings.

Touchless sensors and antimicrobial coatings have gained prominence, particularly in healthcare, hospitality, and food-processing sectors. These features enhance hygiene, improve safety, and reflect global trends in health-conscious infrastructure design.

Applications Across Sectors

Automatic doors are utilized across healthcare, transportation, retail, industrial, and residential sectors. Hospitals use touchless doors to prevent contamination and ensure smooth movement of staff and patients. Airports and transit hubs enhance passenger flow and security through automated entry systems. Retail environments benefit from improved customer experience, operational efficiency, and energy management. Industrial facilities maintain controlled environments, streamline workflow, and protect workers with automated doors.

Residential applications, including automated garage doors and smart entryways, are also expanding, offering convenience, security, and modern design appeal.

Regional Market Dynamics

Asia-Pacific leads growth due to rapid urbanization, infrastructure development, and smart city initiatives in China, India, and Japan. Europe and North America maintain steady adoption driven by modernization projects, regulatory compliance, and energy efficiency standards. The Middle East is witnessing growing deployment of automatic doors in luxury commercial developments and hospitality projects.

Challenges and Opportunities

Challenges include high installation costs, technical complexity, and integrating doors into existing structures. Retrofitting older buildings can be complicated, requiring specialized labor and planning. These challenges drive innovation in modular, plug-and-play solutions that simplify installation and reduce operational issues.

Opportunities exist in expanding applications, adopting AI and IoT technologies, and addressing global needs for sustainability, hygiene, and accessibility. Emerging trends in energy-efficient, adaptive, and intelligent systems are expected to further propel market growth.

Future Outlook

The Automatic Door Market is projected to continue growing as smart building integration, energy efficiency, and advanced automation become essential. AI and IoT-enabled doors will enable adaptive operation, predictive maintenance, and optimized energy use. Biometric access and cloud monitoring will enhance security and user convenience. With ongoing trends in automation and sustainability, automatic doors will remain critical for intelligent, eco-friendly, and user-centric infrastructure globally.

Conclusion

The Automatic Door Market is redefining modern architecture through automation, sustainability, and intelligent design. By improving convenience, safety, energy efficiency, and accessibility, automatic doors are integral to smart, functional, and environmentally responsible buildings worldwide.

Learn More - https://www.pristinemarketinsights.com/automatic-door-market-report