Blogs

Fiber Reinforced Polymer (FRP) Rebars Market to Reach US$ 421.02 Million by 2028, Growing at 10.2% CAGR

By ashu1411, 2025-10-03

United States of America – October 3, 2025 – The Insight Partners is proud to announce its newest market report, " Fiber Reinforced Polymer (FRP) Rebars Market : An In-depth Analysis". The report provides a holistic view of the FRP Rebars Market and describes the current scenario as well as growth estimates of FRP Rebars during the forecast period.

Download Sample PDF Copy https://www.theinsightpartners.com/sample/TIPRE00003768/

Overview of FRP Rebars Market

The Fiber Reinforced Polymer (FRP) Rebars Market is witnessing significant growth driven by the increasing demand for durable, lightweight, and corrosion-resistant construction materials. The market is expected to grow from US$ 215.88 million in 2021 to US$ 421.02 million by 2028 , expanding at a CAGR of 10.2% from 2022 to 2028 . Factors such as the rising adoption of FRP rebars in infrastructure projects, advancements in composite materials, and the shift toward sustainable construction practices are fueling market expansion.

Key Findings and Insights

Market Size and Growth

- Historical Data : The FRP Rebars Market was valued at US$ 215.88 million in 2021.

- Forecast : It is projected to reach US$ 421.02 million by 2028, growing at a CAGR of 10.2%.

- Key Drivers :

- Increased investment in infrastructure projects.

- Rising demand for materials with superior strength-to-weight ratio.

- Government focus on sustainable and corrosion-resistant construction solutions.

Market Segmentation

The FRP Rebars Market has been segmented as follows:

- By Resin Type

- Vinyl Ester

- Polyester

- Epoxy

- By Fiber Type

- Glass Fiber Composites

- Carbon Fiber Composites

- Basalt Fiber Composites

- By Application

- Highway Bridge and Construction

- Marine Structures and Waterfronts

- Water Treatment Plants

Spotting Emerging Trends

- Technological Advancements : Development of hybrid composites and improved resin systems is enhancing the performance and durability of FRP rebars.

- Changing Consumer Preferences : There is a growing preference for FRP rebars over traditional steel due to their non-corrosive nature, lightweight properties, and longer service life.

- Regulatory Changes : Governments are encouraging the use of sustainable construction materials, which is expected to boost FRP rebar adoption across infrastructure projects globally.

Growth Opportunities

The FRP Rebars Market presents vast opportunities, including:

- Expanding use in marine structures and water treatment plants , where resistance to chemical corrosion is critical.

- Growing application in bridge construction and rehabilitation projects due to their durability.

- Rising investments in smart infrastructure and green building projects .

- Emerging economies in Asia-Pacific and the Middle East are becoming key growth regions for FRP rebar adoption.

Market Leaders and Key Company Profiles

Prominent players in the FRP Rebars Market include:

- Owens Corning

- KODIAC Fiberglass Rebar

- MARSHALL COMPOSITE TECHNOLOGIES, LLC.

- TUF-BAR

- Armastek USA

- Pultron Composites

- FiRep Inc.

- PULTRALL, Inc.

- Schock Bauteile GmbH

Conclusion

The Fiber Reinforced Polymer (FRP) Rebars Market: Global Industry Trends, Share, Size, Growth, Opportunity, and Forecast 2023–2031 report provides much-needed insight for companies aiming to establish or expand their presence in the FRP Rebars Market. By offering an in-depth analysis of competitive dynamics, market drivers, and growth prospects, this report enables stakeholders to make fact-based decisions and unlock business opportunities in this rapidly growing sector.

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients get solutions to their research requirements through our syndicated and consulting research services. We specialize in semiconductor and electronics, aerospace and defense, automotive and transportation, biotechnology, healthcare IT, manufacturing and construction, medical devices, technology, media and telecommunications, and chemicals and materials.

Contact Us

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

Also Available in: 日本 | 한국어 | Français | لعربية | 中文 | Italiano | Español | Deutsch

Dual-pass Opacity Monitor Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2032

By Market research desk, 2025-10-03

According to a new report from Intel Market Research , the global dual-pass opacity monitor market was valued at USD 596 million in 2024 and is projected to reach USD 946 million by 2032 , growing at a CAGR of 6.9% during the forecast period (2025–2032). This growth is propelled by increasingly stringent environmental regulations worldwide, rapid industrialization in emerging economies, and technological advancements in optical measurement systems.

What is a Dual-pass Opacity Monitor?

Dual-pass opacity monitors are precision instruments designed to measure particulate matter concentrations in gases or liquids using advanced optical principles. These devices employ either light scattering or light absorption techniques, with the dual-pass technology significantly enhancing measurement accuracy by performing two optical path detections. This makes these instruments indispensable for environmental compliance and industrial process control applications where precise particulate measurement is critical.

These monitoring systems are primarily used for industrial emission monitoring , ambient air quality assessment , and scientific research applications . Major manufacturers like SICK AG, AMETEK Land, and Durag Group are actively expanding their product portfolios to address evolving regulatory requirements and industry needs across global markets.

Download Sample Report : Dual-pass Opacity Monitor Market - View in Detailed Research Report

Key Market Drivers

1. Stringent Environmental Regulations Accelerate Adoption

The global push for cleaner industrial emissions is driving unprecedented demand for advanced monitoring technologies. Over 120 countries have implemented strict particulate matter (PM) regulations, with the European Union's Industrial Emissions Directive (IED) requiring continuous opacity monitoring for all major industrial plants. This regulatory pressure has created a $280 million annual market for emission monitoring systems in Europe alone. The dual-pass design's superior accuracy in measuring low concentration particulates (as low as 0.1 mg/m³) makes it particularly valuable for compliance reporting.

2. Industrial Automation and IoT Integration

The fourth industrial revolution is transforming environmental monitoring through advanced connectivity solutions. Modern dual-pass opacity monitors now seamlessly integrate with distributed control systems (DCS) and cloud platforms, enabling real-time data analysis across multiple facilities. The industrial IoT market, projected to reach $1.1 trillion by 2030, has spurred development of smart monitoring devices with predictive maintenance capabilities. Leading manufacturers have reported 30% higher adoption rates for networked opacity monitors compared to standalone units, as they reduce manual inspection costs by approximately 45%.

Market Challenges

- High initial investment costs : Complete monitoring station installations typically range between $25,000-$75,000, with annual maintenance adding 15-20% to the total cost of ownership, making adoption challenging for smaller operators.

- Technical complexities in harsh environments : Extreme industrial conditions with temperatures exceeding 500°C and dust loads reaching 50g/m³ present significant challenges for optical measurement systems.

- Lack of standardized calibration protocols : Discrepancies in calibration methods between regions create compliance challenges for multinational operators.

Opportunities Ahead

The rapid industrialization of Southeast Asia and Africa is creating new demand centers for environmental monitoring. Countries like Vietnam and Nigeria have announced $3.2 billion in combined investments to modernize their emissions control infrastructure by 2030. These markets currently have less than 30% penetration of continuous monitoring systems, representing significant expansion opportunities.

Additionally, the global carbon capture utilization and storage (CCUS) market, projected to grow at 19% CAGR through 2035, requires precise particulate monitoring to ensure system efficiency. Dual-pass technology's ability to measure both opacity and particle size distribution makes it ideal for these applications.

Download Sample PDF : Dual-pass Opacity Monitor Market - View in Detailed Research Report

Regional Market Insights

- Asia-Pacific : Dominates the global market with over 50% regional demand driven by China's "Blue Sky" initiative and rapid industrialization across India, Japan, and South Korea.

- North America : Represents a mature yet steadily growing market characterized by stringent regulatory enforcement under the EPA's Clean Air Act requirements.

- Europe : Maintains a sophisticated market with preference for integrated monitoring solutions that combine opacity measurement with other gas analyzers.

- Latin America, Middle East & Africa : Emerging markets showing gradual growth through increasing environmental awareness and international investment.

Market Segmentation

By Type

- Light Scattering Method

- Light Absorption Method

By Application

- Industrial Emission Monitoring

- Ambient Air Quality Monitoring

- Transportation and Energy

- Others

By End User

- Manufacturing Industries

- Environmental Agencies

- Research Institutions

- Energy Sector

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Get Full Report : Dual-pass Opacity Monitor Market - View in Detailed Research Report

Competitive Landscape

The global dual-pass opacity monitor market features a dynamic competitive landscape with a mix of established multinational corporations and emerging regional players. Acoem and SICK AG dominate with extensive portfolios and global distribution networks, particularly in Europe and North America.

The report provides in-depth competitive profiling of key players, including:

- Acoem (France)

- SICK AG (Germany)

- Durag Group (Germany)

- AMETEK Land (UK)

- CODEL International (UK)

- LISUN Electronics (China)

- Shanghai Shouli Industry (China)

- Other prominent manufacturers and technology providers

Report Deliverables

- Global and regional market forecasts from 2025 to 2032

- Strategic insights into technological developments and regulatory approvals

- Market share analysis and SWOT assessments

- Pricing trends and industry dynamics

- Comprehensive segmentation by type, application, end user, and geography

Get Full Report : Dual-pass Opacity Monitor Market - View in Detailed Research Report

Download Sample PDF : Dual-pass Opacity Monitor Market - View in Detailed Research Report

Browse more related report

https://www.intelmarketresearch.com/pilocarpine-hydrochloride-ophthalmic-solution-market-3002

https://www.intelmarketresearch.com/tablet-cutter-market-2929

https://www.intelmarketresearch.com/aluminum-nitride-rod-market-2917

https://www.intelmarketresearch.com/pressurized-phase-change-boiler-market-3515

https://www.intelmarketresearch.com/aaviation-coatings-market-3051

https://www.intelmarketresearch.com/intelligent-flexible-conveyor-system-market-3345

https://www.intelmarketresearch.com/electronic-low-temperature-drop-weight-testing-machine-market-2946

https://www.intelmarketresearch.com/plasma-arc-welding-machine-market-6443

https://www.intelmarketresearch.com/custom-card-game-printing-service-market-2971

https://www.intelmarketresearch.com/human-macrophage-colony-stimulating-factor-reagent-market-2850

https://www.intelmarketresearch.com/renewable-food-grade-lubricants-market-3450

https://www.intelmarketresearch.com/united-states-cake-concentrates-market-10698

https://www.intelmarketresearch.com/hydrogen-peroxide-vaporization-disinfection-machine-market-3509

https://www.intelmarketresearch.com/ai-smart-headphones-market-2810

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in environmental technology , industrial instrumentation , and compliance solutions . Our research capabilities include:

- Real-time competitive benchmarking

- Global regulatory and standards monitoring

- Country-specific compliance and market analysis

- Over 500+ industrial and environmental reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website : https://www.intelmarketresearch.com

International : +1 (332) 2424 294

Asia-Pacific : +91 9169164321

LinkedIn : Follow Us

When it comes to building reliable, durable, and cost-effective structures, the choice of materials is one of the most critical decisions any builder, architect, or project manager can make. Steel has long been recognized as one of the strongest and most versatile materials in the construction industry. Among the many steel providers around the world, Mackay Steel stands out as a trusted name that has consistently delivered high-quality steel products designed to meet the demands of modern construction. Understanding how Mackay Steel can help you build stronger structures begins with exploring its quality standards, product range, technical expertise, and the value it provides to the construction industry.

The Importance of Steel in Modern Construction

Steel has become the backbone of modern infrastructure. From skyscrapers and bridges to warehouses and residential developments, steel provides the strength, flexibility, and reliability that other materials often cannot match. Unlike wood or concrete, steel is resistant to pests, fire, and severe weather conditions. Its high strength-to-weight ratio allows engineers to design bold and innovative structures without compromising safety. Mackay Steel, with its commitment to superior quality, ensures that every product meets these demanding expectations. This is why the company has become synonymous with strength and dependability.

Mackay Steel’s Commitment to Quality

One of the main reasons Mackay Steel plays such an important role in building stronger structures is its commitment to maintaining the highest quality standards. Every batch of steel is carefully manufactured, tested, and certified to ensure it meets strict industry requirements. This attention to quality control means that contractors and engineers can confidently use Mackay Steel in projects of any size, knowing that the material will perform as expected under heavy loads and challenging conditions. Consistency in quality is not just a promise but a standard that Mackay Steel delivers with every product.

Wide Range of Steel Products

Another factor that makes Mackay Steel a preferred choice is the diversity of its product range. Construction projects often require various types of steel to serve different purposes. Structural beams, reinforcement bars, steel plates, and specialized steel sections all play a unique role in building design. Mackay Steel offers an extensive portfolio of products designed to meet these varying requirements. By providing a one-stop solution for different steel needs, the company saves contractors and suppliers time and resources. Instead of sourcing from multiple vendors, they can rely on Mackay Steel for a comprehensive selection of materials that guarantee strength and durability.

Technical Expertise and Innovation

Steel is not just about strength; it is also about innovation. The construction industry is constantly evolving, with new building methods and design requirements emerging every year. Mackay Steel invests in research and development to stay ahead of industry trends. By combining technical expertise with innovative manufacturing techniques, the company produces steel that is lighter, stronger, and more sustainable. This innovation allows engineers and builders to push the boundaries of design while ensuring that safety and stability are never compromised. Mackay Steel’s ability to balance tradition with innovation makes it an indispensable partner in the modern construction landscape.

Durability and Long-Term Performance

For any structure to stand the test of time, it must be built with materials that can endure decades of use and exposure to the elements. Mackay Steel provides materials that offer long-term durability, resisting corrosion, rust, and other forms of degradation. This durability reduces maintenance costs and extends the life of buildings and infrastructure. Whether it is a residential high-rise, an industrial warehouse, or a transportation bridge, structures built with Mackay Steel demonstrate superior resilience compared to those built with lower-quality alternatives. This long-term performance is one of the key reasons why Mackay Steel is trusted by engineers and builders alike.

Sustainable Building Solutions

In today’s world, sustainability has become a top priority in construction. Builders are under increasing pressure to reduce their environmental footprint while still delivering safe and reliable projects. Mackay Steel supports this goal by producing steel that is recyclable, energy-efficient, and environmentally responsible. Unlike many other building materials, steel can be recycled multiple times without losing its strength or quality. By using Mackay Steel, builders contribute to a more sustainable construction industry that benefits both the environment and future generations. This commitment to green building practices further enhances the value that Mackay Steel brings to the table.

Enhancing Safety and Structural Integrity

Safety is at the heart of every construction project. A structure that is not safe puts lives at risk and undermines trust in the industry. Mackay Steel helps builders achieve the highest levels of safety by providing materials that exceed safety standards and regulatory requirements. The steel’s ability to withstand high stress, extreme temperatures, and natural disasters makes it an essential component in structures where safety cannot be compromised. By choosing Mackay Steel, builders ensure that the foundations of their projects are strong, reliable, and built to last.

Supporting Large-Scale Infrastructure Projects

Large-scale infrastructure projects such as highways, bridges, airports, and railways demand materials that can handle immense stress and constant usage. Mackay Steel has proven its reliability in such projects, delivering the steel products required to ensure both structural integrity and longevity. These projects often serve as the backbone of a nation’s economy, and using Mackay Steel ensures that the investments made in infrastructure are secure and sustainable. The ability to contribute to projects of this scale demonstrates not only the strength of the steel but also the credibility and reputation of Mackay Steel as a partner in national development.

Competitive Advantage in Construction

Every construction company is looking for ways to gain a competitive edge. Using high-quality steel from a trusted provider like Mackay Steel gives companies that advantage. Reliable materials mean fewer delays, lower maintenance costs, and a stronger final product. In highly competitive markets, these factors can make the difference between winning and losing major contracts. Mackay Steel empowers construction companies by giving them confidence in their materials, enabling them to focus on delivering projects that exceed client expectations. This competitive advantage is a vital part of why Mackay Steel continues to be a leader in the industry.

Mammography X-ray Devices Market Regional Analysis, Demand Analysis and Competitive Outlook 2025-2032

By lifesciencesid, 2025-10-03

[Pune, India]

MARKET INSIGHTS

Global Mammography X-ray Devices market was valued at USD 1329 million in 2024 and is projected to reach USD 1801 million by 2031, at a CAGR of 4.5% during the forecast period.

A mammography unit is a box with a tube that produces x-rays. The unit is used exclusively for breast x-ray exams and features special accessories to limit x-ray exposure to only the breast.

"Comprehensive Insights: Download Our Latest Industry Report"

The mammography X-ray devices market is driven by the increasing incidence of breast cancer and the growing awareness of early detection through screening programs. Mammography X-ray devices are essential medical imaging tools used for breast cancer screening and diagnosis. While the rise in breast cancer cases underscores the need for effective and timely detection contributing to market growth as mammography plays a crucial role in improving patient outcomes and reducing mortality rates advancements in technology, such as digital mammography and 3D tomosynthesis, have enhanced the accuracy and efficiency of breast imaging. However, the market also faces challenges, including concerns about radiation exposure and the need for improved accessibility to mammography services in underserved regions. Furthermore, addressing the cost of mammography equipment and ensuring compliance with regulatory standards can pose obstacles for manufacturers. To succeed, companies must focus on research and development to offer innovative and cost-effective solutions. Key players like Hologic, GE Healthcare, Siemens, and FUJIFILM dominate the landscape with robust portfolios, driving further innovation and market expansion.

Mammography X-ray Devices Market

MARKET DYNAMICS

MARKET DRIVERS

Increasing Incidence of Breast Cancer to Drive Demand for Mammography X-ray Devices

Breast cancer remains one of the most prevalent cancers worldwide, with approximately 2.3 million new cases diagnosed annually among women. This rising incidence, particularly in developed and developing regions alike, underscores the critical need for effective screening tools. Mammography X-ray devices play a pivotal role in early detection, allowing for interventions that significantly improve survival rates early-stage detection can boost five-year survival to over 90 percent. As populations age and lifestyle factors contribute to higher risks, healthcare systems are prioritizing routine screenings, fueling demand for advanced imaging equipment. The global mammography X-ray devices market, valued at $1,329 million in 2024, is projected to reach $1,801 million by 2031, growing at a compound annual growth rate (CAGR) of 4.5 percent. This expansion is largely propelled by the urgent push to address breast cancer through widespread screening programs, which rely heavily on reliable mammography technology to identify abnormalities before symptoms appear.

Furthermore, government-backed initiatives and public health campaigns are amplifying awareness, encouraging more women to participate in regular mammograms. In regions like North America and Europe, where screening coverage exceeds 70 percent in many countries, the integration of mammography into national health policies has led to substantial investments in diagnostic infrastructure. However, even in these areas, the sheer volume of cases necessitates upgrades to existing devices and the adoption of newer models to handle increased throughput. Manufacturers are responding by enhancing device portability and efficiency, ensuring that mammography X-ray systems can support high-volume screening without compromising image quality. Such developments not only meet current demands but also pave the way for broader accessibility, ultimately driving sustained market growth as the battle against breast cancer intensifies.

Advancements in Digital and 3D Imaging Technologies to Boost Market Expansion

Technological innovations in mammography, particularly the shift toward digital solutions and 3D tomosynthesis, are transforming breast imaging by offering superior accuracy and reduced false positives. Full Field Digital Mammography (FFDM) now dominates the market, accounting for over 60 percent of installations due to its ability to produce high-resolution images with lower radiation doses compared to traditional film-based systems. Digital Breast Tomosynthesis (DBT), which provides layered views of breast tissue, has seen adoption rates climb by 15 percent annually in recent years, enabling better detection of cancers hidden in dense breast tissue. These advancements address longstanding limitations in conventional mammography, making screening more effective and patient-friendly. As a result, healthcare providers are increasingly investing in hybrid systems that combine 2D and 3D capabilities, further propelling the market forward.

The integration of artificial intelligence (AI) into mammography devices enhances diagnostic precision, with AI algorithms assisting radiologists in identifying subtle anomalies that might otherwise be overlooked. Recent launches, such as upgraded DBT systems in 2023, have incorporated AI-driven software to streamline workflows and improve outcomes in clinical settings. Hospitals and medical centers, which represent more than 80 percent of the market's application segments, are leading this adoption to cope with growing patient loads. Moreover, these technological strides are lowering operational costs over time through efficient data management and remote diagnostics, encouraging even resource-constrained facilities to upgrade. Consequently, the emphasis on innovation continues to be a key driver, supporting the market's projected CAGR of 4.5 percent through 2031.

➤ For instance, regulatory approvals for AI-enhanced mammography tools have accelerated their deployment, ensuring that patients benefit from faster and more accurate diagnoses in routine screenings.

Additionally, the trend toward minimally invasive diagnostics aligns with patient preferences for less discomfort during procedures, fostering greater compliance with screening guidelines. While challenges like initial implementation costs persist, the long-term benefits in terms of reduced healthcare expenditures from early interventions outweigh them, solidifying technology as a cornerstone of market growth.

Growing Awareness and Screening Programs to Enhance Market Penetration

Heightened public and professional awareness about the importance of early breast cancer detection has led to expanded screening programs globally, directly boosting the utilization of mammography X-ray devices. Organizations worldwide recommend annual or biennial mammograms for women over 40, and compliance rates have risen to around 65 percent in high-income countries, up from 50 percent a decade ago. This surge in screenings translates to increased demand for devices capable of handling diverse patient populations, including those with dense breasts where traditional methods fall short. The market benefits as healthcare budgets allocate more funds to preventive care, recognizing that mammography reduces mortality by up to 30 percent when performed regularly.

In emerging markets like Asia and Latin America, awareness campaigns supported by international health bodies are bridging gaps, with screening participation growing by 20 percent in the past five years. This creates opportunities for manufacturers to introduce affordable, user-friendly devices tailored to these regions' needs. Furthermore, partnerships between device makers and screening networks ensure steady equipment supply, enhancing reliability and trust in the technology.

Rising Investments in Healthcare Infrastructure to Support Market Growth

Substantial investments in healthcare infrastructure, especially in hospitals and medical centers, are fueling the procurement of advanced mammography X-ray devices. With hospitals accounting for nearly 70 percent of the market's application share, expansions in diagnostic capabilities are essential to meet rising patient demands. Governments and private sectors are pouring resources into modernizing facilities, particularly in North America and Europe, where infrastructure upgrades have driven a 10 percent increase in installed mammography units over the last two years.

Moreover, the focus on integrated healthcare systems promotes the adoption of multi-modal imaging solutions, where mammography complements other diagnostics for comprehensive care. These investments not only expand capacity but also emphasize quality assurance, ensuring devices meet stringent safety standards. As a result, the market is poised for robust growth, aligned with broader healthcare advancements.

MARKET CHALLENGES

Concerns Over Radiation Exposure to Hinder Widespread Adoption

The mammography X-ray devices market, while advancing rapidly, grapples with persistent concerns regarding radiation exposure, which can deter both patients and providers from routine use. Although modern devices deliver doses as low as 3-7 milligrays per exam significantly less than earlier models the cumulative risk from repeated screenings remains a topic of debate, especially for younger women or those at low risk. This apprehension leads to lower screening rates in some demographics, with studies indicating that up to 20 percent of eligible women avoid mammograms due to radiation fears. Balancing diagnostic benefits with safety is crucial, yet it poses a challenge for manufacturers seeking to promote broader acceptance.

Efforts to mitigate these concerns include ongoing refinements in dose-reduction technologies, but public perception often lags behind scientific evidence. In regions with high awareness of radiation risks, such as parts of Europe, alternative imaging modalities like ultrasound or MRI are gaining traction for supplemental screening, potentially fragmenting the market. However, addressing these issues through education and innovation is essential to maintain mammography's position as the gold standard for breast cancer detection.

Other Challenges

Accessibility Issues in Underserved Regions

Limited access to mammography services in rural and low-income areas continues to challenge market penetration. In many developing countries, fewer than 30 percent of facilities are equipped with digital mammography units, exacerbating disparities in early detection. Infrastructure barriers, including unreliable power supplies and transportation logistics, further complicate deployment, making it difficult for manufacturers to reach these markets effectively.

Regulatory Compliance Burdens

Navigating diverse regulatory landscapes across countries demands rigorous testing and certification, often delaying product launches by 12-18 months. Stringent standards from bodies like the FDA in the U.S. ensure safety but increase development costs, straining smaller players and slowing overall innovation pace in the industry.

"Comprehensive Insights: Download Our Latest Industry Report"

MARKET RESTRAINTS

High Costs of Equipment and Maintenance to Restrain Market Growth

Mammography X-ray devices offer vital tools for breast cancer screening, yet their high acquisition and operational costs pose significant restraints on market expansion. A single advanced unit can cost between $200,000 and $500,000, with annual maintenance adding another 10-15 percent of that value. These expenses are particularly burdensome for smaller clinics and facilities in emerging economies, where budget constraints limit upgrades to digital or 3D systems. As a result, many institutions rely on outdated analog equipment, which not only hampers efficiency but also affects image quality and patient throughput.

Additionally, the need for specialized training and quality control programs further escalates long-term costs, deterring investments in underserved areas. While financing options and leasing models are emerging, they often come with high interest rates, perpetuating a cycle of financial strain. These cost-related barriers collectively slow the adoption of cutting-edge technologies, capping the market's potential despite growing demand.

Segment Analysis

By Type

Full Field Digital Mammography (FFDM) Segment Dominates the Market Due to its Widespread Adoption in Routine Screening and Superior Image Quality

The market is segmented based on type into:

· Full Field Digital Mammography (FFDM)

· Digital Breast Tomosynthesis (DBT)

· Breast CT

By Application

Hospital Segment Leads Due to High Volume of Breast Cancer Screenings and Diagnostic Procedures

The market is segmented based on application into:

· Hospital

· Medical Center

· Other

Competitive Landscape

The competitive environment in the Mammography X-ray Devices market is characterized by innovation, strategic partnerships, and a focus on expanding market share through technological superiority. Leading players invest heavily in R&D to introduce next-generation devices that offer lower radiation doses and faster imaging times. Mergers and acquisitions are common, enabling companies to enhance their product portfolios and global reach. Key challenges include maintaining compliance with evolving regulations and competing on pricing in price-sensitive markets.

Recent developments include the launch of AI-integrated systems and portable mammography units to improve accessibility. Industry experts highlight the importance of sustainable manufacturing practices and robust distribution networks to navigate supply chain volatilities. The following are prominent companies in the market:

· Hologic

· GE Healthcare

· Siemens

· FUJIFILM

· Philips Healthcare

· Canon Medical

· IMS Giotto

· Planmed

· Carestream Health

· Metaltronica

· MEDI-FUTURE

· Wandong Medical

· ANKE

· Sino MDT

· Angell

Market Drivers and Challenges

Key drivers include the escalating global breast cancer burden, with millions of new cases diagnosed annually, underscoring the need for effective screening tools. Awareness initiatives by organizations like the World Health Organization promote regular mammograms, boosting device demand. Technological innovations, such as 3D imaging capabilities in DBT systems, reduce recall rates and enhance detection of dense breast tissues.

Challenges encompass concerns over ionizing radiation exposure, prompting the development of low-dose alternatives. Accessibility remains a barrier in developing regions, where infrastructure limitations hinder deployment. High initial costs and maintenance requirements also deter smaller facilities, though reimbursement policies in many countries mitigate these issues to some extent.

Conclusion

The Mammography X-ray Devices market is poised for steady growth, driven by healthcare advancements and preventive strategies. Stakeholders should prioritize innovation and equitable distribution to capitalize on emerging opportunities while addressing persistent barriers. This comprehensive analysis equips businesses with insights to formulate strategies that align with market trends and regulatory landscapes.

Mammography X-ray Devices Market Trends

Advancements in Digital Imaging Technologies to Emerge as a Trend in the Market

The mammography X-ray devices market is experiencing significant transformation driven by rapid advancements in digital imaging technologies. Full Field Digital Mammography (FFDM) and Digital Breast Tomosynthesis (DBT) have become cornerstones, offering superior image quality and reduced radiation exposure compared to traditional film-based systems. These innovations allow for earlier and more accurate detection of breast abnormalities, which is crucial in improving patient outcomes. For instance, DBT provides three-dimensional views of breast tissue, minimizing overlapping structures that can obscure lesions in standard 2D mammograms. As healthcare providers increasingly adopt these technologies, the market sees heightened demand, particularly in developed regions where screening programs emphasize precision diagnostics. Furthermore, the integration of artificial intelligence algorithms into mammography systems enhances lesion detection rates, with studies indicating improvements in sensitivity by up to 10-15%. This trend not only boosts efficiency for radiologists but also addresses longstanding challenges in breast cancer screening, paving the way for broader accessibility and cost-effectiveness in the long term.

Other Trends

Increasing Incidence of Breast Cancer and Early Detection Initiatives

The rising global incidence of breast cancer continues to propel the mammography X-ray devices market forward, as early detection remains the most effective strategy for reducing mortality rates. With breast cancer accounting for approximately 25% of all cancer cases among women worldwide, governments and health organizations are ramping up screening efforts through national and regional programs. These initiatives encourage regular mammograms, leading to a surge in device installations in hospitals and diagnostic centers. However, while urban areas benefit from advanced setups, rural and underserved regions often struggle with limited access, highlighting the need for portable and affordable mammography solutions. Technological progress, such as contrast-enhanced mammography, further refines diagnostic accuracy for dense breast tissue, a common issue affecting up to 50% of women. As awareness grows, particularly through campaigns targeting younger demographics, the market is poised for sustained expansion, though challenges like overdiagnosis and false positives necessitate ongoing refinements in imaging protocols.

"Comprehensive Insights: Download Our Latest Industry Report"

https://sites.google.com/view/24lifesciencessid/home/rosuvastatin-calcium-market

https://sites.google.com/view/24lifesciencessid/home/vegetarian-softgel-capsules-market?authuser=1

https://sites.google.com/view/24lifesciencessid/home/vegetarian-softgel-capsules-market?authuser=1

About 24lifesciences

Founded in 2017, 24LifeScience has emerged as a trusted research and analytics partner for organizations operating within the global life sciences and chemical industries. Our core mission is to provide intelligent, future-ready insights that help clients stay ahead in an increasingly complex and innovation-driven market

International: +1(332) 2424 294 | Asia: +91 9425150513 (Asia)

Website: http://www.24lifesciences.com

Follow us on LinkedIn: http://www.linkedin.com/company/lifesciences24

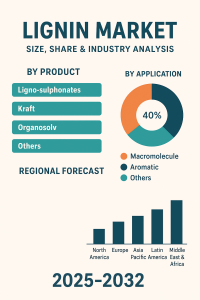

According to Fortune Business Insights, The lignin market is gaining traction as industries worldwide are shifting toward sustainable and bio-based solutions. Lignin, a natural polymer derived from plant cell walls and a by-product of the pulp and paper industry, has emerged as a versatile material with applications in chemicals, construction, agriculture, animal feed, and energy production. Its eco-friendly nature, coupled with rising demand for renewable resources, is driving market growth.

Lignin is a group of organic polymers that serve as a key structural component in the supporting tissues of vascular plants and algae. It plays a crucial role in the development of cell walls, particularly in wood and bark. From a chemical perspective, lignins are cross-linked phenolic polymers with a molecular mass exceeding 10,000 unified amu. They are hydrophobic in nature and characterized by a high content of aromatic subunits.

In the lignin market, manufacturers are steadily working to recover from previous setbacks. Encouragingly, the rising production and demand for concrete additives, along with the expanding application of lignin as an organic additive, are driving growth. With the growing influence of the Internet and e-commerce platforms, the market outlook appears highly promising.

Request PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/lignin-market-104547

Key Players Covered:

The global Lignin market consists of global & regional players operating. Some of the key players in the market include-

- Borregaard LignoTech

- Domtar Corporation

- Aditya Birla Group

- Liquid Lignin Company LLC

- Nippon Paper Industries Co., Ltd

- Metsa Group

- Others

Market Overview

Lignin is primarily obtained as kraft lignin, lignosulfonates, and organosolv lignin. It is widely used as a dispersant, binder, adhesive, and additive in various end-use industries. Increasing demand for green chemicals and the growing emphasis on reducing carbon footprints are fueling investments in lignin-based products. The market is also witnessing innovation in lignin-derived carbon fibers, resins, and bio-based polymers , which hold strong potential for replacing petroleum-based alternatives.

Key Growth Drivers

Sustainability and Bio-based Economy – Growing awareness about environmental concerns and the shift toward circular economies are driving lignin adoption.

Applications in Construction and Agriculture – Lignin-based binders and dispersants are widely used in concrete admixtures, fertilizers, and soil conditioners.

Rising Demand for Renewable Energy – Lignin’s potential as a feedstock for biofuels and bioplastics is opening new avenues for market players.

Cost-effectiveness – As a by-product of paper and pulp mills, lignin offers an abundant and low-cost raw material source.

Market Challenges

Despite its potential, the lignin market faces challenges such as:

Limited awareness and commercialization of lignin-based advanced products.

Technical difficulties in consistent large-scale production.

Competition from synthetic substitutes with established supply chains.

Regional Insights

Europe dominates the market, driven by strong government support for bio-based products, stringent sustainability regulations, and advanced R&D activities.

North America is witnessing growth due to the expansion of bio-refineries and increasing investment in lignin-based energy solutions.

Asia-Pacific is expected to be the fastest-growing region, fueled by rapid industrialization, a large paper & pulp industry base, and rising infrastructure development.

Future Outlook

The lignin market is projected to expand steadily as industries continue to transition toward eco-friendly materials. With technological advancements in lignin valorization and the rising demand for bio-based chemicals, carbon fibers, and green composites , the market is set to witness significant innovation. Strategic collaborations between paper mills, chemical companies, and research institutions will play a vital role in scaling up lignin applications.

The lignin market stands at the intersection of sustainability and innovation. Its versatility and eco-friendly properties make it a crucial component of the bio-based economy. As industries push toward decarbonization and resource efficiency, lignin is poised to evolve from a by-product to a valuable raw material across multiple sectors.

Information Source: https://www.fortunebusinessinsights.com/lignin-market-104547

Lignin Industry Developments

- In June 2020, Metsa and Fortum joined forces to develop a exceptional R&D program from renewable and sustainable sources. The main objective of the joint venture is to provide high value end-products made from components like straw, lignin and hemicellulose.

Animal Orthopedic Diseases Stem Cell Therapy Market - Latest Study with Future Growth, COVID-19 Analysis

By vaishnavi , 2025-10-03

According to a new report from Intel Market Research , the global Animal Orthopedic Diseases Stem Cell Therapy market was valued at USD 247 million in 2024 and is projected to reach USD 720 million by 2032 , growing at an impressive CAGR of 16.7% during the forecast period (2025–2032). This rapid growth is driven by increasing pet ownership, advancements in veterinary regenerative medicine, and the rising adoption of stem cell therapies for treating osteoarthritis and other musculoskeletal conditions in animals.

What is Animal Orthopedic Diseases Stem Cell Therapy?

Animal orthopedic diseases stem cell therapy is a regenerative medicine approach that harnesses the unique properties of stem cells to repair damaged bones, cartilage, tendons, and muscles in animals. The therapy primarily utilizes mesenchymal stem cells (MSCs) derived from adipose tissue, bone marrow, or umbilical cord blood. These cells demonstrate exceptional differentiation potential, low immunogenicity, and strong tissue regeneration capabilities.

The treatment is particularly effective for conditions like osteoarthritis, hip dysplasia , and cartilage defects , offering a promising alternative to traditional surgical interventions. Veterinary clinics worldwide are increasingly adopting these therapies due to their minimally invasive nature and potential to restore mobility in companion animals.

Download Sample Report :

Animal Orthopedic Diseases Stem Cell Therapy Market - View in Detailed Research Report

Key Market Drivers

1. Booming Pet Economy and Humanization of Pets

The global pet care industry has witnessed exponential growth, with spending on veterinary care increasing by 8-10% annually in developed markets. Pet owners now view their companions as family members, leading to greater willingness to invest in advanced treatments. Studies show 65% of pet owners would consider regenerative therapies if recommended by their veterinarian.

2. Clinical Efficacy in Orthopedic Conditions

Clinical trials have demonstrated remarkable success rates, particularly for canine osteoarthritis cases:

- 85% of dogs showed significant pain reduction within 8 weeks of treatment

- 70% improvement in mobility scores sustained over 12 months

- Cartilage regeneration observed in 60% of treated joints

3. Technological Advancements in Stem Cell Processing

The market is benefiting from innovations such as:

- Automated stem cell isolation systems reducing processing time by 40%

- Cryopreservation techniques extending cell viability to 5+ years

- Novel 3D bioprinting applications for customized cartilage repair

Market Challenges

Despite the promising outlook, several barriers persist:

-

Regulatory heterogeneity : While the FDA has established guidelines, regulatory frameworks vary significantly across countries, creating market access challenges

-

High treatment costs : Average therapy costs range between $2,000-$5,000 per procedure, limiting accessibility

-

Limited veterinary awareness : Only 35% of general practice veterinarians actively recommend stem cell therapies

-

Ethical concerns : Ongoing debates about embryonic stem cell use continue in some regions

Emerging Opportunities

The market presents several promising growth avenues:

-

Expansion into livestock applications : Potential to treat racehorses and high-value breeding animals

-

Development of allogeneic (off-the-shelf) stem cell products : Reducing treatment costs by 30-40%

-

Combination therapies : Integrating stem cells with platelet-rich plasma (PRP) for enhanced outcomes

-

Telemedicine integration : Remote consulting for post-treatment monitoring

Notably, industry leaders like VetStem and MediVet Biologics have announced expansion plans for 2024-2025, focusing on:

- New clinical trials for feline arthritis applications

- International market expansion in Asia and Latin America

- Development of next-generation cellular matrices

Get Full Report :

Animal Orthopedic Diseases Stem Cell Therapy Market - View in Detailed Research Report

Regional Market Insights

-

North America : Dominates with 45% market share , driven by advanced veterinary infrastructure and high pet care expenditure

-

Europe : Growing at 18% CAGR , with Germany and UK leading adoption due to favorable reimbursement policies

-

Asia-Pacific : Emerging as the fastest-growing region ( 21% CAGR ), particularly in China and Japan where pet ownership is rising rapidly

-

Latin America : Brazil and Mexico showing strong potential with increasing veterinary specialization

Market Segmentation

By Cell Type

- Totipotent Stem Cells

- Pluripotent Stem Cells

- Unipotent Stem Cells

By Application

- Osteoarthritis

- Cartilage Injury

- Fracture Repair

- Femoral Head Necrosis

- Spinal Degenerative Diseases

- Others

By Animal Type

- Companion Animals (Dogs, Cats, Horses)

- Livestock

- Other Animals

By End User

- Veterinary Hospitals

- Veterinary Clinics

- Research Institutes

Download Sample Report :

Animal Orthopedic Diseases Stem Cell Therapy Market - View in Detailed Research Report

Competitive Landscape

The market features a mix of established players and innovative startups:

- MediVet Biologics

- VetStem Biopharma

- Regeneus Ltd.

- Aratana Therapeutics

- Boehringer Ingelheim

- Tianjin BION Biotechnology

- Vetcell Therapeutics

- Others developing advanced cellular therapies

Report Coverage

- Market size estimation for 2024-2032

- Detailed competitive analysis of 15+ companies

- Clinical trial landscape and pipeline assessment

- Regulatory scenario analysis across key markets

- Pricing and reimbursement trends

- Emerging technology evaluation

Get Full Report :

Animal Orthopedic Diseases Stem Cell Therapy Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology , pharmaceuticals , and healthcare infrastructure . Our research capabilities include:

-

Real-time competitive benchmarking

-

Global clinical trial pipeline monitoring

-

Country-specific regulatory and pricing analysis

-

Over 500+ healthcare reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website : https://www.intelmarketresearch.com

International : +1 (332) 2424 294

Asia-Pacific : +91 9169164321

LinkedIn : Follow Us

Pill Crushers & Splitters Market : Industry Size, Growth, Demand, Opportunities and Forecast

By vaishnavi , 2025-10-03

According to Intel Market Research , the global Pill Crushers & Splitters market was valued at USD 22.3 million in 2024 and is projected to reach USD 30.7 million by 2032 , growing at a steady CAGR of 4.8% during the forecast period (2025–2032). This growth is driven by rising geriatric populations requiring medication assistance and increasing awareness about precise dosage administration.

What are Pill Crushers & Splitters?

Pill Crushers & Splitters are medical devices designed to either crush tablets into fine powder for easy swallowing or accurately split them into smaller doses. These tools play a critical role in medication management, particularly for elderly patients, children, and individuals with swallowing difficulties (dysphagia). The devices enhance medication adherence while ensuring dose precision – a crucial factor in treatments requiring careful titration.

Modern variants feature ergonomic designs , anti-slip mechanisms , and storage compartments , with materials ranging from medical-grade plastics to stainless steel for durability. Unlike traditional methods (mortar-pestle or knife cutting), these FDA-cleared devices prevent contamination and dosage inaccuracies.

Download Free Sample Report :

Pill Crushers & Splitters Market - Detailed Research Report

Key Market Drivers

1. Growing Geriatric Population and Chronic Disease Burden

With 1 in 6 people worldwide projected to be aged 60+ by 2030 (WHO), the demand for medication assistance devices escalates. Conditions like Parkinson's, arthritis, and stroke often impair patients' ability to swallow whole pills, making crushers/splitters indispensable. Furthermore, 60% of adults over 65 take ≥3 daily medications (CDC), necessitating precise dosage tools.

2. Technological Advancements in Design

Innovations are addressing longstanding user pain points:

- Electric pill crushers reducing physical strain for caregivers

- Integrated measuring systems ensuring dose accuracy

- Travel-friendly models with spill-proof designs

- Children's versions featuring colorful, non-threatening designs

Market Challenges

Despite strong demand, several factors constrain market expansion:

- Price sensitivity : Basic plastic models dominate developing markets despite inferior durability

- Regulatory variations : Differing medical device classifications across regions delay product launches

- Alternative methods : Some healthcare providers still prefer liquid medications or crushed preparations

Opportunities Ahead

The market presents multiple growth avenues:

- Smart connected devices integrating with medication reminder apps

- Hospital-at-home programs driving demand for professional-grade home devices

- Emerging markets in Asia-Pacific witnessing healthcare infrastructure upgrades

Notably, industry leaders like Health Care Logistics and Medline are expanding their geriatric care portfolios, while pharmacies increasingly bundle crushers with complex medication regimens.

Regional Market Insights

- North America : Dominates market share (42%) due to advanced elderly care infrastructure

- Europe : Strong growth via NHS and private healthcare initiatives

- Asia-Pacific : Fastest-growing region with Japan's super-aged society and India's expanding middle class

Market Segmentation

By Product Type

- Pill Crushers

- Pill Splitters

- Combination Devices

By Material

- Plastic

- Metal

- Others

By End User

- Hospitals

- Clinics

- Home Care

- Long-term Facilities

Get Full Report Here :

Pill Crushers & Splitters Market - Detailed Research Report

Competitive Landscape

The market features both specialized manufacturers and diversified medical suppliers:

- Health Care Logistics

- Medline Industries

- McKesson

- Apothecary Products

- Ocelco

Recent developments include Walgreens launching store-brand crushers and Suzhou Sunmed exporting cost-effective models to emerging markets.

Report Coverage

- Market size forecasts to 2032

- Material innovation trends

- Regulatory landscape analysis

- Strategic recommendations

Download Free Sample :

Pill Crushers & Splitters Market Sample

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in medical devices , healthcare infrastructure , and aging population solutions . Our research capabilities include:

- Real-time competitive benchmarking

- Emerging technology analysis

- Regulatory pathway mapping

- Over 500+ healthcare reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website : https://www.intelmarketresearch.com

International : +1 (332) 2424 294

Asia-Pacific : +91 9169164321

LinkedIn : Follow Us

Disposable Medical Ice Packs Market Regional Analysis, Demand Analysis and Competitive Outlook 2025-2032

By lifesciencesid, 2025-10-03

[Pune, India]

The global Disposable Medical Ice Packs Market was valued at USD 854 million in 2024 and is projected to grow from USD 883 million in 2025 to USD 1,010 million by 2031 , exhibiting a CAGR of 2.5% during the forecast period (2025–2032). As single-use cryotherapy solutions , disposable medical ice packs play a vital role in pain management, inflammation reduction, trauma care, and post-operative recovery across hospitals, clinics, and homecare settings.

"Comprehensive Insights: Download Our Latest Industry Report"

The market’s growth is fueled by rising surgical volumes, increasing sports-related injuries, and the expansion of ambulatory care centers . While competition from reusable alternatives remains a challenge, innovations in eco-friendly and biodegradable materials are opening new opportunities, supported by healthcare’s growing emphasis on sustainability.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Cryotherapy in Post-Surgical Care to Propel Market Expansion

Disposable medical ice packs play a vital role in cryotherapy, offering immediate relief from pain, swelling, and inflammation following surgical procedures, injuries, or dental interventions. As healthcare providers increasingly adopt non-invasive methods to enhance patient recovery, the need for reliable, single-use cooling solutions has surged. These packs, designed for one-time application, ensure hygiene and reduce the risk of cross-contamination in clinical settings. With the global medical devices market valued at approximately US$603 billion in 2023 and projected to grow at a compound annual growth rate (CAGR) of 5% over the next six years, disposable ice packs benefit from this broader expansion. The integration of these products into standard post-operative protocols is driven by evidence showing faster healing times and improved patient comfort, particularly in high-volume environments like hospitals where efficiency is paramount. Furthermore, advancements in gel formulations have made these packs more effective at maintaining consistent temperatures, encouraging wider adoption across various medical applications.

In recent years, the emphasis on infection control has amplified the preference for disposable options over reusable ones. For example, during the heightened awareness of hygiene post the global health challenges of the early 2020s, healthcare facilities reported a 20-30% increase in procurement of single-use medical supplies, including ice packs. This shift not only supports regulatory compliance but also streamlines workflows in busy clinics and hospitals. As the aging population grows expected to reach 1.5 billion people aged 65 and older by 2050 the incidence of conditions requiring cryotherapy, such as arthritis and sports injuries, will likely rise, further boosting demand. While traditional ice methods persist in some regions, the convenience and safety of disposable packs are winning over providers, positioning this market for steady growth at a CAGR of 2.5% from 2024 to 2031.

Expansion of Healthcare Infrastructure in Emerging Markets Fuels Adoption

The proliferation of healthcare facilities in developing regions is a key catalyst for the disposable medical ice packs market. As countries in Asia and South America invest heavily in building more clinics and hospitals to meet rising health needs, the demand for essential supplies like these packs intensifies. Global healthcare spending, which accounts for about 10% of the world's GDP, continues to climb due to factors such as chronic disease prevalence and an expanding geriatric demographic. In particular, the Asia-Pacific region, with its rapid urbanization and increasing access to medical services, is seeing a notable uptick in the use of disposable cryotherapy products. Hospitals and clinics in these areas prioritize cost-effective, easy-to-store items that align with growing patient volumes, estimated to increase by 15% annually in some emerging economies.

Moreover, government initiatives aimed at improving public health infrastructure are accelerating this trend. For instance, programs in countries like India and Brazil have led to the construction of thousands of new primary care centers, each requiring stockpiles of disposable medical aids. This not only enhances local treatment capabilities for trauma and post-procedural care but also opens avenues for international suppliers to penetrate these markets. The segment for hospitals, which holds the largest share at over 50% of the market in 2024, stands to gain the most from this infrastructure boom. However, while opportunities abound, ensuring supply chain reliability remains crucial to capitalize on this driver effectively.

MARKET OPPORTUNITIES

Innovations in Eco-Friendly Materials to Open New Avenues for Sustainable Growth

The push toward sustainability presents a compelling opportunity for the disposable medical ice packs market, as manufacturers explore biodegradable and recyclable alternatives to traditional plastics. With environmental regulations tightening such as the EU's single-use plastics directive aiming to reduce waste by 50% by 2030 developing green variants could differentiate products and attract eco-conscious buyers. The surgical sterilization grade segment, comprising 40% of the market in 2024, stands to benefit most, as hospitals seek compliant supplies that align with corporate social responsibility goals. Rising consumer demand for sustainable healthcare products, evidenced by a 25% increase in green certifications for medical devices over the past five years, underscores this potential.

Key players are already investing in R&D for plant-based gels that maintain cooling efficacy while degrading naturally, potentially expanding market share in North America and Europe, where regulatory incentives favor such innovations. This not only addresses waste concerns but also taps into premium pricing for advanced, earth-friendly options.

Additionally, collaborations with environmental organizations could accelerate adoption, turning a challenge into a competitive edge for future expansion.

Strategic Partnerships and Expansion into Emerging Markets to Drive Revenue Growth

Strategic alliances among manufacturers, distributors, and healthcare providers offer lucrative prospects for scaling operations in high-growth regions. With Asia expected to account for 35% of global market share by 2031, partnerships can facilitate entry into underserved areas like India and Southeast Asia, where clinic networks are expanding rapidly. Companies like those in the top five, holding 40% of revenues in 2024, are pursuing mergers to enhance supply chains and localize production, reducing costs by up to 15% and improving delivery times.

Moreover, initiatives by international health bodies to bolster emergency response kits in developing countries create demand spikes for disposable ice packs in trauma care. By leveraging these, firms can achieve diversified revenue streams, particularly in the clinic application segment growing at 3% annually.

Furthermore, e-commerce platforms for medical supplies are enabling direct-to-consumer sales, broadening reach beyond institutions and fostering innovation in packaging for home delivery.

Market Highlights

Segmentation by Type

- Surgical Sterilization Grade – The dominant segment , driven by stringent hygiene requirements in surgical and hospital environments. This segment accounted for nearly 40% of the market in 2024 and benefits from sterilization compliance standards.

- Ordinary Sterilization Grade – Preferred in less critical care settings, offering cost-effective options for routine treatments and outpatient care.

Segmentation by Application

- Hospitals – Lead the market due to extensive use in post-operative recovery, emergency departments, and trauma care .

- Clinics – Gaining traction as outpatient procedures and diagnostic applications increase.

- Others – Includes homecare and sports medicine , expanding access to portable cryotherapy solutions.

Key Market Drivers

- Rising global surgical volumes and emphasis on infection control .

- Growing incidence of chronic conditions like arthritis and musculoskeletal disorders.

- Expanding sports medicine sector , with athletes relying on fast recovery solutions.

- Healthcare expenditure growth , accounting for 10% of global GDP in 2023.

- Innovation in gel formulations for prolonged cooling and biocompatibility.

Emerging Trends Shaping the Healthcare Market

The Disposable Medical Ice Packs Market is evolving alongside broader healthcare and life sciences innovations:

- Eco-Friendly Materials: Manufacturers are investing in biodegradable and recyclable materials to reduce waste, aligning with regulatory initiatives like the EU’s single-use plastics directive .

- Advanced Gel Technology: New plant-based gels maintain cooling efficacy while offering natural degradation properties.

- Sterile Packaging: Growing adoption in surgical settings to ensure hygienic, single-use cryotherapy solutions .

- Integration with Digital Health: Portable cryotherapy packs are increasingly being paired with connected medical kits for emergency and home use.

- Sustainability Certifications: A 25% rise in green certifications for medical devices in the past five years highlights growing demand for sustainable healthcare solutions.

Regional Analysis

- North America – The largest market in 2024, supported by high surgical volumes, advanced hospital infrastructure, and growing sports medicine applications . Strong focus on infection control and post-operative care continues to drive demand.

- Europe – Significant adoption, particularly in Germany, France, and the U.K., where regulatory incentives for sustainable medical devices are accelerating eco-friendly product launches.

- Asia-Pacific – The fastest-growing region , projected to account for 35% of global market share by 2031 . Expansion of clinic networks, rising healthcare investments, and growing awareness of patient safety standards fuel growth in India, China, and Southeast Asia.

- Latin America & Middle East – Emerging markets with expanding hospital networks and increasing government focus on affordable healthcare solutions.

Key Players & Competitive Landscape

The market is moderately fragmented , with leading players accounting for approximately 40% of total revenues in 2024 . Competition centers on eco-friendly innovations, sterilization compliance, and partnerships for global distribution .

Major Companies Include:

- Reuseit (U.S.)

- Dispotech

- King Healthcare

- Techniice

- Lloyds Pharmacy

- Gel Frost Packs

- The Coldest

- Magic Gel

- Ice Wraps

- FlexiKold

- Decathlon

- LFCare

- Hai Shi Hai Nuo

- Intco Medical

Companies are pursuing strategic partnerships, M&A activity, and local production facilities to reduce costs and enhance regional presence. For example, top-tier manufacturers are expanding into Asia-Pacific markets through collaborations with healthcare providers and distributors to meet rising demand.

Future Outlook

The global Disposable Medical Ice Packs Market is set to reach USD 1,010 million by 2031 , reflecting steady growth amid evolving healthcare priorities. Sustainability innovations , coupled with growing adoption in surgical and sports medicine applications , will play a critical role in shaping market dynamics.

While competition from reusable alternatives and regulatory disparities may slow expansion, manufacturers that invest in biodegradable solutions, localized supply chains, and sterilization compliance are expected to gain a competitive edge.

"Comprehensive Insights: Download Our Latest Industry Report"

https://sites.google.com/view/24lifesciencessid/home/rosuvastatin-calcium-market

https://sites.google.com/view/24lifesciencessid/home/vegetarian-softgel-capsules-market?authuser=1

https://sites.google.com/view/24lifesciencessid/home/vegetarian-softgel-capsules-market?authuser=1

Small Nucleic Acid Drugs for Hepatitis B market : Analysis by Product Types, Application, Region and Country, Trends and Forecast

By vaishnavi , 2025-10-03

According to a new report from Intel Market Research , the global Small Nucleic Acid Drugs for Hepatitis B market was valued at USD 783 million in 2024 and is projected to reach USD 1,148 million by 2032 , growing at a steady CAGR of 6.1% during the forecast period (2025–2032). This expansion reflects the growing scientific and commercial interest in advanced RNA-based therapies targeting chronic hepatitis B virus (HBV) infections—a disease affecting over 296 million people worldwide according to WHO estimates.

What Are Small Nucleic Acid Drugs for Hepatitis B?

Small nucleic acid drugs represent a breakthrough class of therapeutics leveraging RNA interference (RNAi) or antisense oligonucleotide (ASO) technology to combat HBV infections. These precision medicines work by selectively silencing viral gene expression, effectively reducing key markers like hepatitis B surface antigen (HBsAg) and core protein levels. Unlike conventional antivirals that merely suppress viral replication, these drugs demonstrate potential for achieving functional cure —defined as sustained HBsAg loss after treatment cessation.

The treatment landscape is evolving rapidly, with candidates like Arbutus Biopharma's AB-729 and GSK's bepirovirsen showing promising Phase II results, including extended dosing intervals of 8-12 weeks. Currently, over 15 clinical-stage programs globally are evaluating these modalities as monotherapies or in combination with existing nucleos(t)ide analogs.

Download Sample Report :

Small Nucleic Acid Drugs for Hepatitis B Market - View in Detailed Research Report

Key Market Drivers

1. Unmet Need in Chronic HBV Treatment

Despite available therapies, only 10-15% of patients achieve functional cure with current regimens. This glaring treatment gap has spurred intense R&D, particularly after studies demonstrated that reducing HBsAg levels below 100 IU/mL significantly improves chances of functional cure. Small nucleic acid drugs directly address this by achieving 1-2 log10 reductions in HBsAg in clinical trials—a feat conventional therapies rarely accomplish.

2. Technological Advancements in Delivery Systems

Recent breakthroughs in N-Acetylgalactosamine (GalNAc) conjugation technology have revolutionized siRNA delivery to hepatocytes, enhancing potency while reducing systemic exposure. Meanwhile, next-gen ASO chemistries (e.g., cEt and LNA modifications) are improving target affinity and stability. These innovations are creating drugs with:

-

Longer dosing intervals (some extending to quarterly administration)

-

Reduced injection-site reactions versus earlier generations

-

Improved safety profiles with lower risk of immune stimulation

Market Challenges

The pathway to commercialization faces several hurdles:

-

Regulatory complexity: No clear FDA/EMA guidelines yet on endpoints for functional cure approvals, requiring sponsors to negotiate unique development paths

-

Pricing pressures: Potential therapy costs exceeding $50,000 annually may face resistance in key markets like China where HBV prevalence is highest

-

Treatment sequencing: Uncertainty persists about optimal combination approaches with existing antivirals or emerging immune modulators

Emerging Opportunities

The field is entering an exciting phase with multiple catalysts:

-

Combinatorial approaches: Trials like Janssen's REEF-1 (combining siRNA JNJ-3989 with capsid inhibitor JNJ-6379) may redefine treatment paradigms

-

Geographic expansion: Asia-Pacific markets—home to 68% of global HBV cases —are establishing specialized reimbursement pathways for advanced therapies

-

Pipeline diversification: Next-wave candidates targeting HBV cccDNA (the viral reservoir) using CRISPR or ASO technologies are entering preclinical development

Regional Market Insights

-

North America: Leads in R&D investment with 42% of ongoing clinical trials , driven by strong biotech funding and expedited FDA review pathways

-

Europe: EMA's PRIME designation for multiple candidates is accelerating development, particularly for therapies addressing treatment-experienced patients

-

Asia-Pacific: China's NMPA has prioritized HBV curative therapies, with domestic players like Ascletis and Suzhou Ribo advancing competitive candidates

-

Latin America/Middle East: Emerging as key clinical trial hubs due to high HBV prevalence and improving research infrastructure

Market Segmentation

By Type

-

Antisense Oligonucleotide (ASO) Drugs

-

siRNA Drugs

By Application

-

Hospital

-

Clinic

-

Others

By Region

-

North America

-

Europe

-

Asia-Pacific

-

Latin America

-

Middle East & Africa

Competitive Landscape

The market features a dynamic mix of pharma giants and specialist biotechs , with Arbutus Biopharma and GSK currently leading clinical development. Recent activities include:

-

Arbutus/GSK collaboration: Co-developing AB-729 with bepirovirsen in Phase II trials

-

Janssen's multipronged approach: Advancing siRNA (JNJ-3989) alongside other direct-acting agents

-

Asian innovators: Ascletis' ASC22 and Brii Biosciences' BRII-835 showing competitive efficacy profiles

Report Highlights

-

Market size projections through 2032 with COVID-19 impact analysis

-

Technology deep-dives: Comparing GalNAc-siRNA vs. LNA-ASO platforms

-

Pipeline analysis of 15+ clinical-stage candidates

-

Pricing and reimbursement scenario across key markets

-

Emerging competitive threats from gene editing approaches

Get Full Report :

Small Nucleic Acid Drugs for Hepatitis B Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology , pharmaceuticals , and healthcare infrastructure . Our research capabilities include:

-

Real-time competitive benchmarking

-

Global clinical trial pipeline monitoring

-

Country-specific regulatory and pricing analysis

-

Over 500+ healthcare reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website : https://www.intelmarketresearch.com

International : +1 (332) 2424 294

Asia-Pacific : +91 9169164321

LinkedIn : Follow Us

Urinary Guide Wire Market Regional Analysis, Demand Analysis and Competitive Outlook 2025-2032

By lifesciencesid, 2025-10-03

[Pune, India]

The global Urinary Guide Wire Market was valued at USD 525 million in 2024 and is projected to grow from USD 560 million in 2025 to USD 808 million by 2031 , expanding at a CAGR of 6.5% during the forecast period (2025–2032). This growth underscores the increasing significance of minimally invasive urological procedures in modern healthcare, driven by rising prevalence of urinary tract disorders, technological innovation in device manufacturing, and growing demand from hospitals and clinics worldwide.

"Comprehensive Insights: Download Our Latest Industry Report"

Urinary guide wires are thin, flexible medical devices essential in urology for facilitating catheter placement, dilation, and drainage. With variations in diameter—such as 0.028-inch, 0.032-inch, 0.035-inch, and 0.038-inch —these devices provide structural support and precise navigation under endoscopic visualization. Their ability to enhance procedural safety and efficiency makes them a critical component in diagnostic and therapeutic interventions across global urology practices.

URINARY GUIDE WIRE MARKET DYNAMICS

MARKET DRIVERS

Rising Prevalence of Urological Disorders Accelerates Market Growth

The global urinary guide wire market is experiencing significant growth due to the increasing prevalence of urological conditions such as kidney stones, benign prostatic hyperplasia (BPH), and urinary tract obstructions. Recent epidemiological data indicates that over 12% of the global population will develop kidney stones during their lifetime, with recurrence rates exceeding 50% within 5-10 years. This growing patient pool requires frequent urological interventions where guide wires play a critical role in catheter placement, stent insertion, and other minimally invasive procedures. The market is further boosted by aging demographics, as individuals over 65 years are three times more likely to develop urological conditions requiring interventional treatments.

Technological Advancements in Minimally Invasive Procedures Fuel Demand

The shift toward minimally invasive urological procedures is transforming the urinary guide wire market. Modern guide wires now incorporate advanced features such as hydrophilic coatings, enhanced torque control, and improved radiopacity, enabling more precise navigation through complex urinary tract anatomies. The global minimally invasive surgical devices market, valued at over $25 billion in 2023, continues to expand at approximately 7% annually, creating parallel growth opportunities for complementary devices like urinary guide wires. Recent product launches featuring hybrid designs combining stiffness gradients with ultra-smooth distal tips demonstrate how innovation is driving procedure success rates above 95% for complex urological interventions.

MARKET RESTRAINTS

High Cost of Advanced Guide Wire Technologies Limits Market Penetration