Blogs

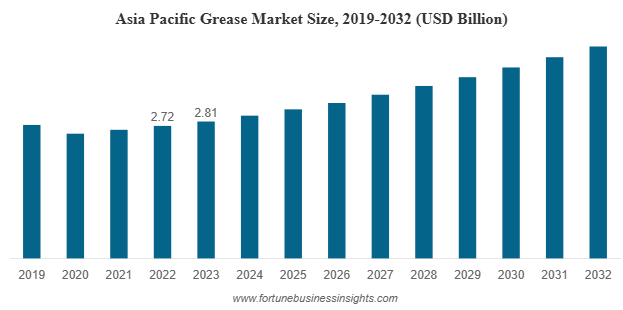

The global grease market was valued at USD 6.60 billion in 2023 and is expected to expand from USD 6.85 billion in 2025 to USD 9.49 billion by 2032, registering a CAGR of 4.60% during the forecast period. Asia Pacific led the market in 2023, accounting for a 44.18% share of the global revenue.

List of Top Grease Companies:

- Exxon Mobil Corporation (U.S.)

- Total Energies (France)

- Shell PLC (U.K.)

- Chevron Corporation (U.S.)

- P. PLC (U.K.)

- FUCHS (Germany)

- Sinopec (China)

- PETRONAS (Malaysia)

Rising Demand from Automotive and Manufacturing Sectors

The automotive sector remains the cornerstone of the grease market, with applications spanning wheel bearings, steering joints, suspension systems, and electric motors. As global vehicle production rises, demand for specialized greases with enhanced temperature resistance, wear protection, and longer service life continues to surge.

A major trend shaping the industry is the transition toward electric vehicles (EVs). EVs demand customized lubricants for high-speed motors, battery systems, and transmission components that operate under unique temperature and torque conditions. Manufacturers are responding with formulations tailored for electric drivetrains, supporting smoother performance and improved energy efficiency.

Beyond automobiles, industrial expansion across construction, mining, power generation, and manufacturing is also driving demand. Grease ensures the reliability of heavy machinery, cranes, turbines, and industrial bearings, making it indispensable in high-load and high-temperature environments.

Shift Toward Sustainable and Bio-Based Greases

Sustainability has become a defining factor in the lubricant industry. Increasing regulatory pressure and customer preference for eco-friendly products are pushing companies to invest in bio-based and biodegradable greases. These greases, derived from renewable base oils such as vegetable oils and synthetic esters, reduce environmental impact while maintaining comparable or superior performance to conventional mineral-based greases.

Bio-based greases are gaining particular attention in environmentally sensitive applications such as marine transport, food processing, and forestry operations. These formulations not only help meet environmental regulations but also align with global efforts toward carbon neutrality and circular manufacturing.

Challenges: Raw Material Volatility and Regulatory Hurdles

While the grease market offers attractive growth potential, it faces challenges stemming from volatile raw material prices and stringent environmental regulations. The cost of base oils, especially mineral and synthetic variants, is highly sensitive to fluctuations in crude oil markets. This volatility affects overall production costs and supply stability.

Additionally, compliance with evolving regulatory standards concerning chemical safety and emissions requires extensive R&D investments. Manufacturers must continually reformulate products to meet performance benchmarks while minimizing environmental impact, which adds to production complexity and cost pressures.

Read More : https://www.fortunebusinessinsights.com/grease-market-110042

Market Segmentation Overview

By Base Oil:

Mineral oil-based greases continue to dominate the global market due to their cost-effectiveness and wide availability. However, synthetic greases are expected to witness faster growth in the coming years, driven by their superior performance under extreme conditions, better oxidation stability, and extended service intervals. Bio-based greases are gradually emerging as the next growth frontier, fueled by environmental awareness and corporate sustainability initiatives.

By Application:

The automotive industry holds the largest market share, accounting for a major portion of global consumption. Power generation, construction, agriculture, and food & beverage sectors also represent substantial demand segments. In the food industry, non-toxic and odorless greases designed to meet strict hygiene standards are increasingly used in machinery that comes into indirect contact with food products.

Regional Insights

Asia Pacific remains the leading regional market, accounting for approximately 44.18% of the global share in 2023. Rapid industrialization, infrastructure investments, and vehicle production in China, India, Japan, and Southeast Asia have positioned the region as a hub for grease consumption. China and India, in particular, are witnessing strong growth due to increased automotive manufacturing and heavy industry expansion.

In North America and Europe, demand is being driven by advanced manufacturing, energy generation, and automation sectors. Stricter environmental regulations in these regions are also fostering the shift toward high-performance synthetic and bio-based greases. Meanwhile, Latin America and the Middle East & Africa are emerging as promising markets owing to large-scale infrastructure projects, mining operations, and oil & gas industry activities.

Key Industry Developments:

- November 2023: B.Grimm Technologies and PETRONAS Lubricants International teamed up to work together and utilize their business expertise to enhance the lubricants market in Thailand. This partnership signified the beginning of future collaborations between B.Grimm and the PETRONAS Group, which would explore new energy solutions in Thailand and the Southeast Asian market.

- March 2023: ExxonMobil announced its plan to invest approximately USD 110 million in constructing a lubricant manufacturing facility in Maharashtra. The new plant would have the capability to produce 159,000 kiloliters of finished lubricants per year, serving the increasing demand of Indian industrial sectors such as steel, manufacturing, mining, power, and construction. The plant is projected to commence operations by the end of 2025.

Future Outlook and Opportunities

The grease market’s future is defined by innovation, sustainability, and regional diversification. As industries move toward automation, precision engineering, and electrification, the need for advanced lubricants will only intensify. Companies that prioritize R&D to develop high-performance, long-life, and eco-friendly greases are likely to capture significant market share.

Moreover, emerging markets offer strong potential for expansion. Strategic partnerships, joint ventures, and localized manufacturing can help global players tap into demand from fast-growing economies. Certifications such as food-grade, biodegradable, and high-performance ratings will also serve as differentiators in this competitive landscape.

In summary, the global grease market is on a growth trajectory fueled by industrial modernization, the rise of electric mobility, and increasing awareness of sustainable lubrication solutions. With strong demand from both traditional and emerging industries, the market is poised for steady and resilient expansion through 2032.

Market Overview

The global honey market growth is poised for significant expansion, with its value projected to rise from USD 9.40 billion in 2024 to USD 15.59 billion by 2032. The market, valued at USD 8.94 billion in 2023, is expected to exhibit a strong CAGR of 6.52% during this forecast period. In the U.S., growth is also projected to be substantial, with the market reaching an estimated value of USD 1.89 billion by 2032, driven by an increasing number of beekeepers and rising demand for natural sweeteners. Regionally, Asia Pacific held the largest market share in 2023.

List of Key Companies Profiled in the Report:

- Bee Maid Honey Limited (Canada)

- Comvita Limited (New Zealand)

- Capilano Honey Ltd. (Australia)

- Dabur India Ltd. (India)

- Billy Bee Honey Products (Canada)

- New Zealand Honey Co. (New Zealand)

- Barkman Honey LLC (U.S.)

- Yamada Bee Company (Japan)

- Dutch Gold Honey Inc. (U.S.)

- Golden Acres Honey (Canada)

Industry Trends:

Honey is experiencing a modern renaissance, driven by a powerful consumer shift towards natural wellness. In the wake of the pandemic, shoppers are increasingly aware of honey's immune-boosting properties, leading to a surge in its popularity. This trend is especially pronounced in developed nations, where the demand for organic and clean-label products is at an all-time high.

Capitalizing on this momentum, the industry is innovating beyond the jar. New health-focused products, from supplements to functional beverages like Singapore’s "Honey Exir," are expanding honey's reach. Behind the scenes, technological advancements in automation are streamlining the supply chain, ensuring that a higher-quality product reaches a more health-conscious consumer.

Segments

Buckwheat Segment to Dominate Attributable to High Nutritional Value

By type, the market is segmented into alfalfa, buckwheat, wildflower, clover, acacia, and others. The buckwheat segment is expected to dominate due to its high nutritional value.

Food & Beverage Segment to Dominate Attributable to its Increasing Applications

Based on application, the market is classified into food & beverages, personal care & cosmetics, pharmaceuticals, and others. The food & beverage segment is expected to dominate due to its increasing applications.

Bottle Segment to Lead Owing to Easy Transportation

By packaging, the market is categorized into glass jar, bottle, tub, tube, and others. The bottle segment is expected to lead the market due to its easy transportation.

Regionally, the market is clubbed into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Report Coverage

The report gives an in-depth view of the leading segments and the latest trends in the market. It looks at what is driving market growth and what is hindering it, including the impact of COVID-19. It also discusses developments in various regions and the strategies used by major companies in the market.

Source: https://www.fortunebusinessinsights.com/industry-reports/honey-market-100551

Market Growth

The global honey market is steadily growing, driven by increasing consumer awareness of honey’s health-promoting properties, such as its antioxidant, anti-inflammatory, and antibacterial effects. As a natural alternative to refined sugars and artificial sweeteners, honey is gaining popularity, especially in the food and beverage sector. Its therapeutic qualities are also boosting demand in the cosmetics and pharmaceutical industries. Premium varieties like manuka and organic honey are seeing a surge in popularity, often fetching higher prices. Furthermore, the rise of e-commerce and global trade is helping to fuel the market’s continued expansion.

Drivers and Restraints

Rising Adoption of the Product for Natural Sweeteners Production to Foster Market Growth

Honey is widely regarded as a healthier alternative to sugar, valued for its healing properties like soothing sore throats and supporting immune health. With a growing number of consumers choosing honey as a natural sweetener, demand is projected to increase. Health-conscious lifestyles, rising incomes, and a shift toward organic products are all contributing to its growing popularity. Additionally, honey’s applications in medicine are expected to boost sales further.

However, potential changes or adulteration of the product could present challenges to sustained market growth.

Regional Insights

Rising Production of Nectar to Propel Market Growth in Asia Pacific

Asia Pacific is expected to lead the honey market due to its high production levels. In 2021, the market in this region was valued at USD 2.86 billion and is projected to capture a large share of the global market in the coming years. Government investments in beekeeping are also likely to boost market growth. For instance, in May 2020, the Indian government allocated nearly USD 68 million for beekeeping under the Atma Nirbhar Bharat initiative.

In Europe, increasing awareness of honey's health benefits is expected to drive its adoption. Changing consumer preferences and a rise in the consumption of organic products may further promote market growth.

In North America, the growing number of beekeepers in Canada and the U.S. is expected to increase product demand. Additionally, strong demand for organic products is enhancing industry growth.

Competitive Landscape

Companies Devise Novel Product Launches to Elevate Brand Image

Top companies are releasing new products to boost their brand image and increase sales. For instance, in January 2022, Tayima Foods launched I'M HONEY, an organic and raw honey in various flavors with significant medicinal benefits. This product is sold on online platforms like Amazon and is anticipated to increase Tayima's sales and expand their global reach. Moreover, companies are also focusing on mergers, partnerships, expansions, and research and development to fuel market growth.

Honey Market Outlook

- Growing demand: Global demand for honey is on the rise. Consumers are increasingly aware of the health benefits and natural muscle tone.

- Health notes: Honey is often considered a healthy alternative to refined sugar. This trend is leading more people to choose honey in their diet.

- Sustainability focus: More focus on sustainable and organic products. Beekeeping, which supports environmental health, is on the rise.

- Product innovation: New products such as fermented foods and beverages are emerging. This diversity of brands creates widespread appeal and increases sales.

KEY INDUSTRY DEVELOPMENTS:

January 2024: Apis India launched organic honey, which is made of honey sourced from organic-certified lands in India.

March 2023: Bagrrys India, a leading honey manufacturer, launched Bagrry’s Organic Wild Honey. The product is available in glass jars across all retail outlets in the country.

Application Security Market Price, Trends, Growth, Analysis, Key Players, Outlook, Report, Forecast 2025-2032

By Rushistellar, 2025-10-13

Application Security Market – Growth, Trends, and Strategic Outlook

Request Free Sample Report: https://www.stellarmr.com/report/req_sample/Application-Security-Market/2166

Market Estimation & Definition

The global application security market is experiencing significant growth:

Fortune Business Insights estimates the market was valued at USD 8.86 billion in 2022 and is projected to grow from USD 9.95 billion in 2023 to USD 25.30 billion by 2030 , at a compound annual growth rate (CAGR) of 14.3% during the forecast period.

Mordor Intelligence forecasts the market size will grow from USD 13.64 billion in 2025 to USD 30.41 billion by 2030 , advancing at a 17.39% CAGR .

Research and Markets projects the market size will increase from USD 38.93 billion in 2025 to USD 68.84 billion by 2030 , growing at a 12.08% CAGR .

Research Nester reports the market surpassed USD 14.12 billion in 2025 and is projected to grow at a 11.8% CAGR , reaching USD 43.08 billion by 2035 .

Straits Research estimates the market size was USD 11.89 billion in 2024 and is expected to grow from USD 13.87 billion in 2025 to USD 47.38 billion by 2033 , growing at a 16.6% CAGR .

Application security encompasses measures and tools designed to protect applications from threats throughout their lifecycle, including development, deployment, and maintenance.

Market Growth Drivers & Opportunities

Several factors are contributing to the growth of the application security market:

Increasing Cybersecurity Threats : The rise in cyberattacks and data breaches is driving organizations to invest in robust application security solutions.

Regulatory Compliance : Stringent regulations and compliance requirements are compelling businesses to adopt comprehensive application security measures.

Digital Transformation : The shift towards digital platforms and cloud services is expanding the attack surface, necessitating enhanced application security.

Emerging Trends Shaping the Future

The application security market is witnessing several emerging trends:

Integration of AI and Machine Learning : Leveraging AI and ML for predictive threat detection and automated response is becoming increasingly prevalent.

DevSecOps Adoption : Integrating security into the DevOps pipeline (DevSecOps) is gaining traction to ensure continuous security throughout the development process.

Zero Trust Architecture : Implementing Zero Trust models to minimize trust assumptions and enhance security posture is on the rise.

Segmentation Analysis

The application security market can be segmented based on component, deployment mode, application, end-user industry, and region:

Component : Includes solutions such as web application firewalls, identity and access management, encryption, and security testing tools.

Deployment Mode : Comprises cloud-based and on-premises deployment models.

Application : Encompasses mobile applications, web applications, and desktop applications.

End-User Industry : Spans across BFSI, healthcare, IT and telecom, retail, and government sectors.

Region : North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. North America is expected to hold the largest market share due to the presence of key market players and high adoption rates of advanced security solutions.

Competitive Landscape

Key players in the application security market include:

IBM Corporation : Offers a comprehensive suite of application security solutions, including static and dynamic analysis tools.

Micro Focus : Provides a range of application security products, such as Fortify, to help organizations secure their applications.

Checkmarx : Specializes in static application security testing (SAST) and software composition analysis (SCA) solutions.

Veracode : Offers cloud-based application security testing services to identify and remediate vulnerabilities.

Synopsys : Provides a comprehensive set of application security testing tools, including SAST, DAST, and software composition analysis.

Press Release Conclusion

The application security market is poised for substantial growth, driven by increasing cybersecurity threats, regulatory compliance requirements, and digital transformation initiatives. Organizations across various industries are prioritizing application security to safeguard their digital assets and maintain customer trust. Companies that focus on innovation, integration of advanced technologies, and comprehensive security solutions will be well-positioned to capitalize on the expanding global demand for application security.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com

Medical Laminates Market by Companies, Applications, Industry Growth, Competitors Analysis, New Technology and Forecast

By vaishnavi , 2025-10-13

According to a new report from Intel Market Research , the global Medical Laminates market was valued at USD 2,238 million in 2024 and is projected to reach USD 3,253 million by 2032 , growing at a steady CAGR of 6.1% during the forecast period (2025–2032). This sustained expansion is driven by increasing global healthcare infrastructure development, stringent hygiene and safety regulations in medical environments, and the growing demand for durable, easy-to-clean surfaces in hospitals and clinics.

What are Medical Laminates?

Medical laminates are high-performance composite materials engineered specifically for demanding medical environments. They are manufactured by combining multiple layers of resin—such as epoxy, phenolic, or melamine —with reinforcing materials like glass fiber or carbon fiber under high temperature and pressure. These materials are distinguished by their antibacterial coatings (compliant with ISO 22196 standards), exceptional resistance to harsh chemical disinfectants, high mechanical strength, and proven biocompatibility (certified by USP Class VI). They are extensively used in operating tables, instrument trays, medical equipment housings, and other critical healthcare applications where durability and infection control are paramount.

These specialized laminates represent a significant advancement over traditional materials, offering healthcare facilities a combination of longevity, safety, and compliance that is essential in modern medical practice.

Download Sample Report : Medical Laminates Market - View in Detailed Research Report

Key Market Drivers

1. Rising Global Healthcare Standards and Infection Control Protocols

The increasing global emphasis on hospital-acquired infection (HAI) prevention is a primary growth driver. With organizations like the WHO and CDC enforcing stricter surface hygiene protocols, medical laminates have become the material of choice for high-touch surfaces. Their non-porous surfaces prevent bacterial colonization, and their resistance to potent disinfectants like sodium hypochlorite and hydrogen peroxide solutions ensures long-term functionality without degradation, directly supporting patient safety initiatives worldwide.

2. Expansion of Healthcare Infrastructure and Medical Tourism

Massive investments in healthcare infrastructure across emerging economies, particularly in the Asia-Pacific and Middle East regions , are creating substantial demand. Countries like China, India, and those in the GCC are constructing new hospitals and specialty clinics at an unprecedented rate, all requiring surfaces that meet international medical standards. Furthermore, the global medical tourism industry, valued in the hundreds of billions, pushes facilities to compete on quality, directly fueling the adoption of premium materials like medical-grade laminates to attract international patients.

3. Technological Advancements in Material Science

Innovation is a constant in this market. Manufacturers are developing next-generation laminates with enhanced properties, such as:

- Anti-microbial copper-infused surfaces for continuous pathogen reduction

- Advanced flame-retardant properties for improved safety in critical care settings

- Lightweight, high-strength composites for use in portable medical devices and mobile carts

- Customizable aesthetics that merge infection control with healing-centered design principles

These innovations are expanding the applications of medical laminates beyond traditional surfaces into new medical devices and architectural elements.

Market Challenges

- High raw material and manufacturing costs : The complex production process involving high-pressure lamination and specialized resins results in a premium product cost, which can be a barrier for budget-constrained healthcare facilities, especially in developing regions.

- Competition from alternative materials : Solid surface materials, advanced polymers, and coated metals continue to evolve, offering competitive properties for specific applications and challenging laminate dominance.

- Stringent and evolving certification processes : Achieving and maintaining certifications like USP Class VI and ISO 22196 requires significant investment in testing and compliance, slowing down time-to-market for new products.

- Supply chain vulnerabilities : The industry relies on a complex global supply chain for specialty resins and reinforcing fibers, which can be disrupted by geopolitical events and trade policies, leading to price volatility and availability issues.

Opportunities Ahead

The future of the medical laminates market is bright, fueled by several converging trends. The post-pandemic world has permanently elevated the importance of infection prevention , making investment in high-performance surfaces a long-term priority for healthcare administrators.

Significant opportunities lie in the untapped potential of emerging markets , where healthcare modernization is accelerating. Furthermore, the trend towards outpatient and ambulatory surgical centers is creating new demand for medical-grade surfaces outside traditional hospital settings. These facilities require the same high standards of care and infection control, presenting a substantial growth vector for laminate manufacturers.

Notably, leading manufacturers are pursuing aggressive expansion strategies, focusing on:

- Developing sustainable and recyclable laminate solutions to meet growing environmental regulations

- Creating specialized laminates for niche applications like MRI suites and radiation therapy rooms

- Forming strategic partnerships with medical equipment OEMs to integrate laminates directly into product design

- Expanding production capacity in key growth regions to better serve local markets and reduce logistical costs

Download Sample PDF : Medical Laminates Market - View in Detailed Research Report

Regional Market Insights

- North America : Dominates the global market, driven by strict FDA and CDC regulations, high healthcare expenditure, and rapid adoption of advanced medical technologies. The U.S. represents the largest single-country market, with a well-established network of manufacturers and suppliers.

- Europe : A mature market characterized by stringent EU-wide medical device and material regulations (MDR). Growth is steady, supported by refurbishment projects in existing healthcare facilities and a strong focus on cross-contamination prevention.

- Asia-Pacific : The fastest-growing region, fueled by massive healthcare infrastructure development in China, India, and Southeast Asian nations. Rising medical tourism, growing disposable incomes, and increasing government health spending are key catalysts here.

- Latin America, Middle East & Africa : These are emerging regions with high growth potential. The GCC countries, in particular, are investing heavily in world-class healthcare cities and hospitals, driving demand for premium medical construction materials, including laminates.

Market Segmentation

By Type

- Epoxy Laminate

- Phenolic Laminate

- Melamine Laminate

By Application

- Medical Equipment Manufacturing

- Medical Packaging

- Medical Decoration

By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Research & Academic Institutes

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Get Full Report Here : Medical Laminates Market - View in Detailed Research Report

Competitive Landscape

The global medical laminates market is moderately fragmented, featuring a mix of large multinational material science corporations and specialized manufacturers. Competition is based on product quality, compliance certifications, technological innovation, and the ability to provide customized solutions.

The report provides an in-depth competitive analysis of over 15 key players, including:

- Amcor

- Trioworld

- Delstar

- Formica

- Polyzen

- UFP MedTech

- Magnetix

- 3M

- Eurocast

- Westfield Medical

- Priontex

- Isola

- Shawmut

- ACE Srl

- Neks

These companies are actively engaged in strategies such as new product launches, capacity expansions, and strategic mergers and acquisitions to strengthen their market position.

Report Deliverables

- Global and regional market size forecasts from 2025 to 2032 in value (USD Million) and volume (K Units)

- Detailed analysis of market drivers, restraints, opportunities, and challenges

- Comprehensive segmentation by Type, Application, End User, and Region with deep-dive analysis

- Market share analysis and competitive benchmarking of key players

- SWOT and Porter's Five Forces analysis

- Insights into regulatory landscapes, supply chain analysis, and pricing trends

Get Full Report Here : Medical Laminates Market - View in Detailed Research Report

Download Sample PDF : Medical Laminates Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology , pharmaceuticals , and healthcare infrastructure . Our research capabilities include:

- Real-time competitive benchmarking

- Global clinical trial pipeline monitoring

- Country-specific regulatory and pricing analysis

- Over 500+ healthcare reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website : https://www.intelmarketresearch.com

International : +1 (332) 2424 294

Asia-Pacific : +91 9169164321

LinkedIn : Follow Us

Automatic Textile Screen Print Machines Market Analysis, Size, Share, Growth, Trends, Opportunities and Forecast

By vaishnavi , 2025-10-13

According to a new report from Intel Market Research , the global Automatic Textile Screen Print Machines market was valued at USD 200 million in 2024 and is projected to reach USD 305 million by 2031 , growing at a CAGR of 6.4% during the forecast period (2025–2031). This growth is fueled by rising demand for customized apparel, technological advancements in printing automation, and the expansion of textile manufacturing in emerging economies.

Download Sample Report :

Automatic Textile Screen Print Machines Market - View in Detailed Research Report

What Are Automatic Textile Screen Print Machines?

Automatic textile screen print machines are advanced manufacturing systems that apply designs to fabrics using a stencil-based process. Unlike manual printing methods, these automated systems use precision-engineered components to transfer ink through mesh screens onto textiles with exact registration and consistent quality. The technology excels at producing vibrant, durable prints across various fabric types - from cotton T-shirts to synthetic performance wear.

Modern variants like carousel printers (holding multiple screens in circular configurations) and linear systems (for sequential color application) dominate industrial-scale textile production. Leading manufacturers such as M&R and ROQ International continue refining these systems with features like automatic screen alignment and IoT-enabled production monitoring.

Key Market Drivers

1. Explosion of Custom Apparel Demand

The global personalized apparel market's 9% annual growth directly fuels screen printing equipment sales. Today's consumers want unique designs - from limited-edition band merchandise to corporate-branded uniforms. Automatic machines enable print shops to fulfill these orders efficiently, producing up to 1,200 impressions per hour with multi-color precision. The sports apparel sector particularly relies on these systems for complex designs requiring specialized inks and fabric treatments.

2. Technological Leap in Printing Automation

Recent advances have transformed screen printing from a labor-intensive craft to a high-tech manufacturing process. The latest generation machines feature:

- Servo-driven precision registration systems with micron-level accuracy

- Integrated drying tunnels that cure prints 25% faster

- Cloud-connected monitoring for real-time production analytics

These innovations reduce setup times by 70% compared to older systems while minimizing material waste - critical advantages in today's fast-paced fashion industry.

3. Sustainability Push in Textile Manufacturing

Environmental regulations and consumer preferences are driving adoption of eco-friendly printing solutions. Modern automatic printers now accommodate:

- Water-based inks (42% of new installations globally)

- Closed-loop ink circulation systems that reduce waste by 40%

- Energy-efficient curing systems with 30% lower power consumption

These features help manufacturers meet stringent environmental standards while maintaining production quality, particularly in export-focused markets like Bangladesh and Vietnam.

Market Challenges

Despite strong growth potential, several factors restrain market expansion:

1. High Capital Investment Requirements

Entry-level industrial systems cost $50,000-$150,000, with advanced models exceeding $500,000. For small print shops, this represents a significant financial barrier compounded by:

- Operator training expenses (25-40% of initial cost)

- Maintenance contracts and spare parts inventory

- Potential facility upgrades for larger equipment

2. Technical Complexity and Skilled Labor Shortage

Operating modern screen printers requires expertise in:

- Screen tension calibration

- Ink viscosity management

- Precision registration adjustments

The scarcity of trained technicians, especially in developing markets, slows adoption rates despite equipment availability.

3. Competition from Digital Printing Alternatives

Direct-to-garment (DTG) and digital textile printing technologies are gaining ground with advantages like:

- Simpler workflow for complex, full-color designs

- Lower minimum order quantities

- Reduced setup times between jobs

While screen printing remains superior for bulk production, the 15% annual growth of digital alternatives pressures equipment manufacturers to enhance their offerings.

Emerging Opportunities

1. Asia-Pacific Manufacturing Expansion

Textile producers in Southeast Asia present substantial growth potential as they:

- Upgrade from manual to automated systems

- Expand capacity to meet Western brand demands

- Benefit from government modernization incentives

China alone accounts for 60% of regional market revenue, with India and Bangladesh showing accelerating adoption rates.

2. Industry 4.0 Integration

Forward-thinking manufacturers are developing smart printing systems with:

- AI-powered quality control that detects defects in real-time

- Predictive maintenance algorithms that reduce downtime

- Automated workflow integration from design to production

Early adopters report 20-35% productivity gains - a compelling value proposition for large-scale operations.

3. Technical Textile Applications

The 6.8% CAGR in technical textiles for automotive, medical, and industrial uses creates demand for specialized printing capabilities like:

- Conductive ink deposition for smart fabrics

- Precision application of functional coatings

- High-durability prints on synthetic substrates

This represents a high-margin segment for equipment manufacturers to target.

Regional Market Insights

| Region | Market Characteristics |

|---|---|

| Asia-Pacific | Dominates with 45% market share, driven by textile manufacturing hubs in China, India, and Bangladesh. Focused on high-volume production efficiency. |

| North America | Prioritizes quick-changeover systems for custom apparel and special effects. The U.S. leads in premium printing technologies. |

| Europe | Emphasizes sustainable printing solutions. Germany serves as innovation center with advanced technical textile applications. |

| Latin America | Gradual transition from manual to semi-automatic systems. Brazil dominates regional demand amid economic challenges. |

| Middle East & Africa | Emerging market with growth in Turkey and Egypt. Increasing adoption among exporters meeting international standards. |

Competitive Landscape

The market features intense competition between established Western manufacturers and emerging Asian suppliers:

- M&R (U.S.) leads with 18% global share through advanced carousel systems like the Gauntlet III series

- ROQ International (Spain) specializes in energy-efficient designs for sustainable printing

- MHM screenprinting (Austria) excels in precision engineering for technical textiles

- Yantai YouCheng (China) provides cost-effective solutions for budget-conscious manufacturers

The industry sees increasing mergers and acquisitions as companies seek to broaden technological capabilities and geographic reach.

Future Outlook

The automatic textile screen printing equipment market will evolve through:

- Continued automation replacing manual processes in developing markets

- Tighter integration with digital design workflows

- Expansion into adjacent applications like smart textiles

- Stronger focus on sustainability across the print production chain

Equipment manufacturers that address these trends while lowering cost barriers can capitalize on the market's steady growth trajectory.

Get Full Report :

Automatic Textile Screen Print Machines Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in industrial equipment , manufacturing technologies , and global supply chains . Our research capabilities include:

-

Real-time competitive benchmarking

-

Emerging technology trend analysis

-

Country-specific manufacturing sector assessments

-

Over 500+ industrial reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website : https://www.intelmarketresearch.com International : +1 (332) 2424 294

Asia-Pacific : +91 9169164321

LinkedIn : Follow Us

Water Turbidity Meters Market Analysis, Size, Regional Outlook, Competitive Strategies and Forecast

By vaishnavi , 2025-10-13

According to a new report from Intel Market Research , the global Water Turbidity Meters market was valued at USD 522 million in 2024 and is projected to reach USD 737 million by 2031 , growing at a steady CAGR of 5.2% during the forecast period (2025–2031). This growth is driven by increasingly stringent water quality regulations worldwide, rising industrial applications, and technological advancements in precision monitoring instruments.

What are Water Turbidity Meters?

Water turbidity meters are precision instruments designed to measure the cloudiness or haziness of a fluid caused by suspended particles. These devices utilize optical principles, typically nephelometric or attenuation methods, to quantify light scattering and absorption properties. Turbidity measurements are expressed in Nephelometric Turbidity Units (NTU) or Formazin Turbidity Units (FTU), providing critical data for water quality assessment across multiple sectors.

These instruments play a vital role in ensuring compliance with water safety standards, environmental monitoring protocols, and industrial process control. From municipal water treatment plants to pharmaceutical manufacturing facilities, turbidity meters serve as essential tools for maintaining water purity and operational efficiency. Modern turbidity meters range from portable field devices to sophisticated inline monitoring systems, offering varying levels of precision depending on application requirements.

Download Sample Report : Water Turbidity Meters Market - View in Detailed Research Report

Key Market Drivers

1. Stringent Regulatory Requirements for Water Quality Monitoring

The increasing global emphasis on water safety and environmental protection has led to tighter regulatory standards across multiple jurisdictions. Regulatory bodies including the US Environmental Protection Agency (EPA) and European Union water directives have established rigorous turbidity limits for drinking water and wastewater discharge. For instance, the EPA's Surface Water Treatment Rule mandates turbidity levels not exceeding 0.3 NTU in treated drinking water, creating mandatory compliance requirements for water utilities.

These regulatory frameworks are continuously evolving, with many regions adopting even stricter standards. The implementation of real-time monitoring requirements and digital reporting has further accelerated the adoption of advanced turbidity measurement systems. Municipalities and industrial operators are investing in reliable monitoring solutions to avoid regulatory penalties and ensure public health protection.

2. Expanding Industrial Applications Beyond Traditional Water Treatment

While water treatment remains the dominant application, turbidity meters are finding new applications across diverse industries. The food and beverage sector increasingly relies on turbidity monitoring for quality control in products like beer, wine, and bottled beverages where clarity affects consumer acceptance. Pharmaceutical manufacturers implement ultra-precise turbidity measurement to ensure water purity meets pharmacopeia standards for injection and manufacturing processes.

Other growing applications include environmental monitoring of rivers and lakes, aquaculture operations maintaining optimal water conditions, and industrial processes where water clarity affects manufacturing outcomes. This diversification creates multiple growth vectors for turbidity meter manufacturers, allowing them to develop specialized products for niche applications while maintaining their core water treatment business.

3. Technological Advancements Enhancing Measurement Capabilities

Recent technological innovations have significantly improved turbidity measurement accuracy, reliability, and usability. Modern instruments now incorporate features like automated calibration, temperature compensation, and anti-fouling mechanisms that maintain accuracy in challenging environments. The integration of digital interfaces enables real-time data logging, remote monitoring, and seamless integration with plant control systems.

Portable turbidity meters have particularly benefited from technological advancements, with many now offering laboratory-grade accuracy in field-deployable packages. These devices typically include features like rechargeable batteries, data storage capabilities, and ruggedized construction suitable for environmental monitoring applications. The development of smart sensors with IoT connectivity represents the next frontier, enabling predictive maintenance and centralized water quality management.

Market Challenges

- High equipment and maintenance costs : Advanced turbidity measurement systems require significant capital investment, while ongoing calibration and maintenance add to operational expenses, particularly challenging for small-scale operators

- Measurement interference and accuracy issues : Variability in water composition, presence of colored compounds, and air bubbles can affect measurement accuracy, requiring sophisticated compensation techniques

- Technical expertise requirements : Proper operation and maintenance of advanced turbidity meters demands trained personnel, creating staffing challenges in some regions

- Standardization complexities : Different regulatory standards and measurement methodologies across regions complicate product development and validation processes

Opportunities Ahead

The global push toward water conservation and reuse presents significant growth opportunities for turbidity meter manufacturers. Water-stressed regions are implementing large-scale recycling projects that require precise turbidity monitoring at multiple process stages. These projects often incorporate sophisticated monitoring networks with numerous measurement points, generating substantial demand for both portable and inline turbidity measurement solutions.

Emerging markets represent another significant opportunity, particularly as developing economies invest in water infrastructure and tighten environmental regulations. While price sensitivity remains a challenge in these markets, manufacturers are developing cost-optimized solutions that maintain adequate accuracy while reducing ownership costs. Innovative business models including equipment leasing and monitoring-as-a-service offerings are improving accessibility in price-sensitive markets.

The integration of turbidity measurement with other water quality parameters creates opportunities for multi-parameter monitoring systems. These integrated solutions offer operational efficiencies and comprehensive water quality assessment, particularly appealing to municipal water utilities and large industrial facilities managing complex water systems.

Download Sample PDF : Water Turbidity Meters Market - View in Detailed Research Report

Regional Market Insights

- North America : Leads the global market with advanced regulatory frameworks and significant investments in water infrastructure, particularly in the United States where EPA regulations drive continuous monitoring adoption

- Europe : Follows stringent EU water directives with strong emphasis on environmental monitoring and wastewater treatment compliance, particularly in Germany, France, and Scandinavian countries

- Asia-Pacific : Shows the fastest growth rate driven by rapid industrialization, urbanization, and increasing investments in water treatment infrastructure, particularly in China and India

- Latin America : Emerging market with growing focus on water quality management, particularly in industrial applications and municipal water systems in Brazil and Mexico

- Middle East & Africa : Developing market with opportunities in desalination projects and basic water infrastructure, though adoption rates vary significantly across the region

Market Segmentation

By Product Type

- Portable Turbidity Meters

- Benchtop Turbidity Meters

- Inline Process Turbidity Meters

By Application

- Drinking Water Treatment

- Wastewater Treatment

- Industrial Process Water

- Environmental Monitoring

- Food & Beverage Production

- Pharmaceutical Manufacturing

- Other Applications

By End User

- Municipal Water Authorities

- Industrial Facilities

- Environmental Agencies

- Research and Testing Laboratories

- Other End Users

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Get Full Report : Water Turbidity Meters Market - View in Detailed Research Report

Competitive Landscape

The global water turbidity meters market features several established players competing through technological innovation, product quality, and geographic coverage. Leading companies are focusing on developing integrated water quality monitoring solutions that combine turbidity measurement with other parameters like pH, conductivity, and dissolved oxygen. The competitive environment remains dynamic with companies balancing between meeting sophisticated industrial requirements and addressing cost-sensitive municipal applications.

The report provides comprehensive competitive analysis of key market participants, including:

- Thermo Fisher Scientific Inc.

- Hanna Instruments, Inc.

- Hach Company (Danaher Corporation)

- Xylem Inc.

- Merck KGaA

- DKK-TOA Corporation

- INESA Scientific Instrument Co., Ltd.

- Other prominent manufacturers and regional players

Report Deliverables

- Global and regional market size forecasts from 2025 to 2031

- Detailed segmentation analysis by product type, application, end user, and geography

- Competitive landscape with market share analysis and company profiles

- Technology trends and innovation assessment

- Regulatory framework analysis across key regions

- Strategic recommendations for market participants

Get Full Report : Water Turbidity Meters Market - View in Detailed Research Report

Download Sample PDF : Water Turbidity Meters Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in environmental technology , industrial instrumentation , and water infrastructure . Our research capabilities include:

- Real-time competitive benchmarking

- Global regulatory and standards monitoring

- Technology adoption trend analysis

- Over 500+ industrial and environmental reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website : https://www.intelmarketresearch.com

International : +1 (332) 2424 294

Asia-Pacific : +91 9169164321

LinkedIn : Follow Us

The Insight Partners is proud to announce its latest market research report titled, “Bio-based PET Market: An In-depth Analysis of the Bio-based PET Market.” The report provides a comprehensive overview of the Bio-based PET Market , examining current market dynamics, key trends, and projected growth patterns during the forecast period.

Overview of the Bio-based PET Market

The Bio-based PET Market has gained significant traction in recent years as industries shift toward sustainable and environmentally responsible materials. PET (Polyethylene Terephthalate) is widely used in packaging, textiles, and automotive applications. However, growing environmental concerns and the increasing demand for renewable materials have accelerated the adoption of bio-based PET, which is derived from biomass instead of petroleum feedstock.

The Bio-based PET Market is expected to register a CAGR of 15% from 2025 to 2031, driven by global sustainability initiatives, technological innovations, and rising consumer awareness regarding eco-friendly packaging. This growth is further supported by commitments from global brands and governments to reduce carbon emissions and dependency on fossil fuels.

Key Findings and Insights

Market Size and Growth

The global Bio-based PET Market is projected to witness robust expansion during the forecast period. Companies are increasingly investing in research and development to enhance production efficiency, reduce costs, and improve product quality. The shift from conventional plastics to bio-based alternatives in the food and beverage packaging sector remains one of the strongest growth drivers.

Key Factors Affecting the Bio-based PET Market

Rising demand for sustainable packaging: The food, beverage, and personal care industries are leading adopters of bio-based PET bottles and containers.

Government initiatives and regulations: Many countries have implemented environmental policies to encourage the use of renewable materials and reduce plastic waste.

Corporate sustainability goals: Major brands such as Coca-Cola, PepsiCo, and Nestlé have pledged to use recyclable or bio-based materials in their packaging, boosting market growth.

Technological innovation: Advances in bio-refinery processes and the development of cost-effective feedstocks are improving the commercial viability of bio-based PET.

Consumer preference for green products: Growing environmental awareness among consumers is shifting demand toward sustainable materials.

Spotting Emerging Trends

Technological Advancements

The industry is witnessing continuous innovation in biopolymer synthesis, catalytic conversion, and bio-refining technologies, which enhance yield and scalability. Research into alternative biomass sources such as agricultural residues and sugarcane molasses is helping reduce raw material costs and improve sustainability.

Changing Consumer Preferences

Consumers are showing strong interest in eco-conscious brands that prioritize sustainable packaging. The trend toward circular economy practices, including recycling and reuse, is pushing manufacturers to integrate bio-based PET with closed-loop production systems.

Regulatory Changes

Governments worldwide are implementing stricter regulations on single-use plastics and offering incentives for green materials. These policies are creating a favorable environment for bio-based PET adoption, particularly in Europe, North America, and parts of Asia-Pacific.

Growth Opportunities

The Bio-based PET Market offers several growth avenues across end-use sectors:

Packaging Industry: Increasing use in beverage bottles, food containers, and personal care packaging.

Automotive Sector: Demand for lightweight and durable bio-based materials for interiors and components.

Textile Industry: Expansion in bio-based PET fibers used in clothing and upholstery.

Emerging Economies: Rapid industrialization and sustainability initiatives in Asia-Pacific and Latin America create new opportunities for manufacturers.

Collaborations between biotechnology firms and packaging giants are expected to accelerate market penetration. Moreover, as production costs decline with technological advancements, bio-based PET will become increasingly competitive with petroleum-based PET.

Conclusion

The Bio-based PET Market: Global Industry Trends, Share, Size, Growth, Opportunity, and Forecast 2023–2031 report provides valuable insights for companies seeking to capitalize on the global transition toward sustainable materials. With increasing investments in R&D, supportive government regulations, and rising environmental awareness, the bio-based PET industry is poised for rapid growth. Companies that embrace innovation and sustainability will play a vital role in shaping the future of this eco-friendly market.

Also Available in: Korean German Japanese French Arabic Chinese Italian Spanish

Global Condensed Milk Market to See Steady Growth Through 2031 | The Insight Partners

By AdarshS, 2025-10-13

The Insight Partners is proud to announce its newest market report, “Condensed Milk Market: An In-depth Analysis of the Condensed Milk Market.” The report provides a comprehensive overview of the Condensed Milk Market , describing the current landscape as well as growth projections during the forecast period.

Overview of the Condensed Milk Market

The Condensed Milk Market has undergone notable changes in recent years, driven by evolving consumer preferences, product innovation, and expanding applications in the food and beverage industry. This report highlights the primary factors shaping the market’s dynamics — from advancements in packaging and processing technologies to the growing demand for convenient and shelf-stable dairy alternatives.

The increasing popularity of ready-to-eat and on-the-go food products, coupled with the rise in home baking trends, has significantly contributed to the growth of condensed milk consumption globally. Moreover, the industry continues to see growth opportunities across emerging markets, where condensed milk is an essential household ingredient for confectionery, coffee, and desserts.

Key Findings and Insights

Market Size and Growth

The Condensed Milk Market is expected to grow steadily between 2025 and 2031, driven by robust demand across multiple food processing segments. The market benefits from condensed milk’s long shelf life, versatility, and ability to enhance flavor and texture in numerous culinary applications.

Key Factors Affecting the Condensed Milk Market

Rising demand in the bakery and confectionery industry: Condensed milk’s rich texture and sweetness make it a key ingredient in desserts, cakes, and chocolates.

Growth in coffee culture: The expanding café and instant coffee sector worldwide boosts the use of sweetened condensed milk as a creamer.

Increasing preference for dairy-based convenience foods: Consumers in urban areas seek products that combine taste, nutrition, and convenience.

Innovation in packaging and shelf stability: Extended shelf life and eco-friendly packaging options enhance market adoption.

Emergence of lactose-free and vegan alternatives: Producers are expanding portfolios with plant-based condensed milk options, targeting health-conscious and lactose-intolerant consumers.

Spotting Emerging Trends

Technological Advancements

The industry is witnessing innovations in evaporation, pasteurization, and homogenization technologies that improve product consistency and nutrient retention. Manufacturers are also investing in automation and digital quality control systems to enhance production efficiency and reduce costs.

Changing Consumer Preferences

Consumers are increasingly drawn to clean-label, organic, and low-sugar condensed milk products. The demand for ethically sourced and traceable dairy ingredients continues to rise, prompting producers to align with sustainable sourcing and processing practices.

Regulatory Changes

Stringent food safety and labeling regulations are shaping the global condensed milk industry. Compliance with international dairy standards, such as those established by Codex Alimentarius, ensures product quality and safety, particularly for export markets. Governments are also encouraging the reduction of added sugars in processed foods, influencing product formulations.

Growth Opportunities

The Condensed Milk Market offers numerous growth opportunities in the years ahead:

Expansion into emerging economies: Rising disposable incomes and changing eating habits in Asia-Pacific, Latin America, and Africa will boost consumption.

Product diversification: Launches of flavored, organic, and plant-based condensed milk open new revenue streams.

E-commerce and retail penetration: Growing online grocery platforms provide manufacturers with broader market reach.

Strategic partnerships: Collaborations between dairy producers and food manufacturers will drive product innovation and branding.

Conclusion

The Condensed Milk Market: Global Industry Trends, Share, Size, Growth, Opportunity, and Forecast 2023–2031 report offers vital insights for companies seeking to strengthen their presence in this rapidly evolving segment. The combination of changing consumer lifestyles, continuous innovation, and expanding distribution channels positions the market for steady growth in the coming years. Businesses investing in sustainable practices, product diversification, and regional expansion are likely to gain a competitive edge in the global condensed milk industry.

Also Available in: Korean German Japanese French Arabic Chinese Italian Spanish

Vacuum Coaters for Wood Market by Size, Business Strategies, Deployment Model, Trends, Applications and Forecast

By vaishnavi , 2025-10-13

According to a new report from Intel Market Research , the global vacuum coaters for wood market was valued at USD 85.7 million in 2024 and is projected to reach USD 134 million by 2031 , growing at a steady CAGR of 6.7% during the forecast period (2025–2031). This growth is propelled by increasing demand for sustainable wood finishing solutions, advancements in vacuum coating technologies, and expanding applications across furniture and architectural sectors.

What are Vacuum Coaters for Wood?

Vacuum coaters for wood are advanced industrial systems that utilize vacuum deposition techniques to apply thin, uniform protective or decorative layers on wood surfaces. These machines significantly enhance wood durability, aesthetics, and resistance to environmental factors while enabling precise control over coating thickness. Major types include vacuum evaporation coating machines, vacuum sputtering coating machines, and chemical vapor deposition (CVD) coating machines, each offering distinct advantages for different wood finishing applications.

These systems represent a technological leap from traditional coating methods, providing superior finish quality while reducing volatile organic compound (VOC) emissions and material waste. The technology is particularly valued for its ability to preserve wood's natural aesthetic while providing enhanced protection against scratches, UV radiation, and moisture damage.

Download Sample Report : Vacuum Coaters for Wood Market - View in Detailed Research Report

Key Market Drivers

1. Growing Demand for Eco-Friendly Wood Finishes

The global push towards sustainable construction and interior design is significantly driving the adoption of vacuum coaters for wood applications. With increasing environmental regulations prohibiting volatile organic compounds (VOCs) in wood finishes, manufacturers are rapidly transitioning to vacuum coating technologies that offer superior environmental benefits. The wood coating market has seen a notable shift towards vacuum deposition methods as they eliminate liquid waste and reduce material consumption compared to conventional finishing processes.

This transition is particularly evident in the European Union, where stringent environmental policies have accelerated technology adoption. Manufacturers are increasingly recognizing that vacuum coating not only meets regulatory requirements but also provides competitive advantages through improved product quality and reduced environmental impact.

2. Advancements in Vacuum Coating Technologies

Recent technological breakthroughs in vacuum coating systems are revolutionizing wood finishing processes. Modern vacuum coaters now incorporate advanced plasma-enhanced chemical vapor deposition (PECVD) and magnetron sputtering technologies that enable ultra-thin, highly durable coatings with exceptional optical clarity. These advancements allow wood products to maintain their natural aesthetic while gaining enhanced protection against environmental factors.

The furniture industry, which accounts for a significant portion of global vacuum coater applications, has been particularly quick to adopt these advanced systems. Major manufacturers are investing in automated vacuum coating lines that dramatically improve production efficiency while maintaining consistent quality standards across large production volumes.

3. Rising Preference for Premium Wood Finishes

The architectural sector's growing demand for high-end wood finishes is creating substantial opportunities for vacuum coating solutions. Luxury residential and commercial projects increasingly specify vacuum-coated wood for interior paneling, flooring, and decorative elements due to their superior aesthetics and durability. This trend is particularly strong in markets where construction activity remains robust, with certain regions accounting for significant portions of regional demand.

The ability of vacuum coaters to apply metallic, colored, and specialty finishes while preserving wood grain patterns has made them indispensable for high-value architectural woodwork. This capability allows designers and architects to create unique visual effects while maintaining the natural beauty and warmth of wood materials.

Market Challenges

- High initial investment costs : Complete vacuum coating systems for wood applications require substantial capital expenditure, placing them beyond the reach of many small and medium-sized wood product manufacturers.

- Technical complexity : Maintaining consistent vacuum levels, managing plasma parameters, and ensuring uniform coating deposition across large wood substrates require specialized technical expertise.

- Material limitations : The technology works best with flat or gently curved surfaces, making it difficult to coat complex three-dimensional wood components evenly.

- Rapid technological evolution : The fast pace of innovation in vacuum coating technologies presents challenges regarding equipment obsolescence and the need for continuous technical training.

Opportunities Ahead

The global shift toward sustainable manufacturing practices and premium quality requirements presents a favorable outlook for vacuum coating technologies. Regions across the globe are witnessing growing momentum through revised environmental policies, expanded manufacturing infrastructure, and strategic partnerships between equipment manufacturers and wood product producers.

Notably, industry leaders are focusing on several strategic initiatives including the development of hybrid coating systems that combine vacuum deposition with traditional methods, expansion into new application areas such as automotive wood trim, and continuous improvement of coating efficiency and environmental performance.

Download Sample PDF : Vacuum Coaters for Wood Market - View in Detailed Research Report

Regional Market Insights

- Europe : Leads the global market owing to stringent environmental regulations and strong emphasis on sustainable wood finishing solutions. The EU's focus on reducing VOC emissions has accelerated technology adoption, with certain countries demonstrating particularly strong market presence.

- North America : Shows strong demand in architectural woodwork and high-end furniture sectors, with the market being more consolidated than Europe's. The region benefits from well-established manufacturing infrastructure and high awareness of premium finishing technologies.

- Asia-Pacific : Presents the fastest growth potential, primarily fueled by expanding furniture export industries and precision woodworking sectors. While adoption rates vary across countries, increasing environmental awareness is gradually shifting preferences toward advanced coating solutions.

- Latin America and Middle East & Africa : Emerging markets with growing opportunities in specialized applications and luxury interior markets, though infrastructure limitations and economic factors currently restrain broader market penetration.

Market Segmentation

By Type

- Vacuum Evaporation Coating Machine

- Vacuum Sputtering Coating Machine

- Chemical Vapor Deposition (CVD) Coating Machine

- Others

By Application

- Furniture

- Architecture

- Rail and Transportation

- Crafts and Musical Instruments

- Others

By End User

- Wood Product Manufacturers

- Furniture Makers

- Contractors and Builders

- Automotive and Aerospace Industries

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Get Full Report : Vacuum Coaters for Wood Market - View in Detailed Research Report

Competitive Landscape

The global vacuum coaters for wood market showcases a moderately fragmented competitive landscape, characterized by a mix of established players and emerging regional competitors. Key industry participants are focusing on technological innovation, regional expansion, and strategic collaborations to strengthen their market positions.

The report provides in-depth competitive profiling of key players, including:

- Cefla Finishing (Italy)

- Dubois (Switzerland)

- Teknos (Finland)

- Schiele Maschinenbau (Germany)

- Palmer Primer (U.S.)

- Y&J Industries (Taiwan)

- Other prominent regional and specialized manufacturers

Report Deliverables

- Global and regional market forecasts from 2025 to 2031

- Strategic insights into technological developments and market trends

- Market share analysis and competitive assessments

- Comprehensive segmentation by type, application, end user, and geography

- Analysis of regulatory impacts and sustainability trends

Get Full Report : Vacuum Coaters for Wood Market - View in Detailed Research Report

Download Sample PDF : Vacuum Coaters for Wood Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in industrial machinery , manufacturing technologies , and advanced materials processing . Our research capabilities include:

- Real-time competitive benchmarking

- Global technology adoption monitoring

- Country-specific regulatory and market analysis

- Over 500+ industrial reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website : https://www.intelmarketresearch.com

International : +1 (332) 2424 294

Asia-Pacific : +91 9169164321

LinkedIn : Follow Us

Spasticity Treatment Market Growth World Technology, Development, Trends and Opportunities Market Research

By poojammr, 2025-10-13

The Spasticity Treatment Market size was valued at USD 1.47 Billion in 2024 and the total Spasticity Treatment revenue is expected to grow at a CAGR of 11% from 2025 to 2032, reaching nearly USD 3.40 Billion.

Spasticity Treatment Market Report Overview

The study includes ever-changing trends, the industry environment, and all of the Clinical Nutrition Market's leading elements. The research approach was used to investigate the Spasticity Treatment Marketindustry, and the results have been logically presented in the report.

Download a Free Sample Report Today : https://www.maximizemarketresearch.com/request-sample/81891/

Market Scope:

The research examines the pivotal trends within the Clinical Nutrition Market and assesses their potential impacts on new business ventures and overall industry development. Market trends influence aspects like new technology adoption, international market entry, regulatory changes, governmental investments, novel applications, and other industry dynamics. This study entails an exhaustive trend analysis to empower informed decision-making in the Clinical Nutrition Market.

The Spasticity Treatment MarketResearch Report offers exclusive essential statistics, facts, insights, trends, and a competitive landscape overview within this specific field. It dissects the present state of the Clinical Nutrition Market and provides forecasts extending until 2029. The study is expected to encompass company profiles, encompassing key details like capacity, production, pricing, costs, revenue, and contact information for global leading Spasticity Treatment Marketmanufacturers.

Spasticity Treatment MarketRegional Insights

Geographically, the report is segmented into several key countries, with Clinical Nutrition Market size, growth rate, import and export of Clinical Nutrition Market in these countries, which cover North America, U.S., Canada, Mexico, Europe, UK, Germany, France, Spain, Italy, Rest of Europe, Asia Pacific, China, India, Japan, Australia, South Korea, ASEAN Countries, Rest of APAC, South America, Brazil, and the Middle East and Africa.

Spasticity Treatment Market Segmentation

by Drug Class

Benzodiazepines

Alpha2-adrenergic Agonists

Botulinum Toxins

Others

by Indication

Multiple Sclerosis (MS)

Cerebral Palsy (CP)

Traumatic Brain Injury (TBI)

Others

Spasticity Treatment MarketKey Players include:

1. F. Hoffmann-La Roche Ltd

2. GlaxoSmithKline plc

3. Medtronic

4. ALLERGAN

5. Pfizer Inc

6. Ipsen Pharma

7. UCB Pharma Ltd

8. Sanofi

9. INMED PHARMACEUTICALS INC

10. Orient Pharma

11. Taj Pharmaceuticals Limited

12. Johnson & Johnson Services, Inc.

13. MediciNova, Inc.

14. Sun Pharmaceutical Industries Ltd

15. Novartis AG

To Gain More Insights into the Market Analysis, Browse Summary of the Research Report: https://www.maximizemarketresearch.com/request-sample/81891/

Key Questions answered in the Spasticity Treatment MarketReport are:

- What is the expected Clinical Nutrition Market size by 2030?

- What are the Clinical Nutrition Market segments?

- Which region holds the largest share in the Clinical Nutrition Market?

- What is the expected CAGR of the Clinical Nutrition Market during the forecast period?

- Which application segment emerged as the leading segment in the Clinical Nutrition Market?

- What key trends are expected to emerge in the Clinical Nutrition Market in the coming years?

- Which factor is contributing to the final price of the Clinical Nutrition Market ?

- What is the expected Clinical Nutrition Market size by 2024?

- Who are the Spasticity Treatment Marketkey players in the industry?

- Which company held the largest share in the Clinical Nutrition Market?

Key Offerings:

- Market Overview

- Market Share

- Market Size

- Forecast by Revenue | 2024−2030

- Market Dynamics – Growth Drivers, Restraints, Investment Opportunities, and Key Trends

- Market Segmentation – A detailed analysis by segments, sub-segments and region

- Competitive Landscape – Top Key Vendors and Other Prominent Vendors

About Maximize Market Research:

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research:

3rd Floor, Navale IT Park, Phase 2

Pune Banglore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656