Blogs

Nanodisc MSP Protein Market Regional Analysis, Demand Analysis and Competitive Outlook 2025-2032

By lifesciencesid, 2025-10-27

Membrane Scaffold Proteins (MSPs) are engineered proteins that form lipid nanodiscs, creating a stable and soluble lipid bilayer environment for studying membrane proteins. These nanodiscs mimic the natural cell membrane, allowing researchers to analyze challenging targets such as G-protein-coupled receptors (GPCRs) , ion channels, and transporters.

By stabilizing membrane proteins in their native conformation, MSP-based nanodiscs are essential for structural biology, drug discovery, and biophysical characterization . This technology bridges the gap between traditional detergent-based solubilization and native membrane analysis, offering improved stability, homogeneity, and functional integrity.

Get free sample of this report at : https://www.24lifesciences.com/download-sample/2737/nanodisc-msp-protein-market-market

Market Size

The global Nanodisc MSP Protein market was valued at USD 202 million in 2024 and is projected to reach USD 303 million by 2031 , growing at a CAGR of 6.1% during the forecast period (2025–2032).

This growth is primarily driven by the expanding use of nanodiscs in membrane protein research , drug target validation , and high-resolution structural studies using techniques such as cryo-electron microscopy (Cryo-EM) and nuclear magnetic resonance (NMR).

Recent Development

The Nanodisc MSP Protein industry has witnessed significant progress in recent years through both technological advancements and strategic collaborations :

-

Integration with Cryo-EM and AI Modeling: Researchers now combine nanodisc technology with AI-assisted protein modeling to enhance visualization of dynamic membrane complexes.

-

Expansion of Custom MSP Libraries: Companies like Cube Biotech and Merck KGaA have introduced tailored MSP variants to accommodate diverse membrane proteins.

-

Fluorescent and Isotope Labeling Innovations: Development of labeled MSPs has boosted imaging and spectroscopic analysis in real-time protein dynamics studies.

-

Collaborative Structural Biology Projects: Increasing partnerships between academic institutes and biotech firms are accelerating the use of nanodiscs in therapeutic discovery.

Market Dynamics

Drivers

-

Growing Investment in Structural Biology: Rising R&D funding in academia and pharma for GPCR and ion channel research drives market demand.

-

Advancements in Drug Discovery: Nanodisc MSPs enhance reproducibility and accuracy in screening membrane protein–drug interactions.

-

Shift Toward Biologics and Targeted Therapies: With biologics projected to exceed USD 690 billion by 2031, the demand for accurate protein characterization tools continues to grow.

Restraints

-

Standardization Challenges: Variability in nanodisc formulations can affect reproducibility across protein classes.

-

High Production Costs: The preparation of high-purity MSP proteins requires sophisticated purification and expression systems.

Opportunities

-

Emerging Nanodisc Applications: Expanding use in vaccine development , biosensor technology , and drug delivery systems .

-

Automation and High-Throughput Platforms: Integration of automated nanodisc assembly systems is improving experimental scalability.

Regional Analysis

North America

North America leads the global market, supported by strong investments in biopharmaceutical R&D , advanced protein analysis infrastructure , and the presence of major players such as Cube Biotech and ACROBiosystems . The U.S. dominates regional growth with its leadership in Cryo-EM facilities and academic research centers.

Europe

Europe follows closely, with countries like Germany, the U.K., and France driving progress through collaborative programs in membrane protein structural studies. The region benefits from robust funding mechanisms like the Horizon Europe Framework for life sciences research.

Asia-Pacific

The Asia-Pacific market is witnessing rapid expansion, propelled by increasing investments in biotechnology , academic collaborations , and drug discovery research in countries such as China, Japan, and South Korea . Growing adoption of nanodisc technology in pharmaceutical development is accelerating regional demand.

Latin America and Middle East & Africa

These emerging markets are at a nascent stage but hold future potential as biotechnology infrastructure develops and international collaborations expand.

Competitor Analysis

The Nanodisc MSP Protein Market is characterized by innovation-focused companies developing specialized proteins and custom lipid systems. The competition is primarily based on product quality , customization capabilities , and strategic partnerships with pharmaceutical and academic institutions.

Leading Companies Include:

-

Cube Biotech – A pioneer in MSP protein technology and nanodisc reagents tailored for GPCR and membrane protein research.

-

Creative Biostructure – Offers a wide range of nanodisc preparation services and MSP variants for structural and functional studies.

-

Merck KGaA – Provides high-quality lipids and recombinant proteins supporting large-scale nanodisc assembly.

-

ACROBiosystems – Focuses on biopharmaceutical-grade MSP proteins and custom labeling solutions for imaging and binding analysis.

These companies are investing heavily in automation , AI-based protein analysis , and collaborative research projects , which are reshaping the competitive landscape.

Market Segmentation (by Application)

Drug Development and Discovery

This segment dominates the market, driven by widespread adoption in target identification , binding affinity studies , and therapeutic screening . Nanodisc MSP proteins provide an ideal platform for membrane protein stabilization , essential for drug design.

Cancer

Nanodiscs play a vital role in understanding oncogenic receptor mechanisms , aiding in the development of precision cancer therapies and antibody targeting.

Neurodegenerative Diseases

MSP-based nanodiscs are increasingly used to study membrane-associated proteins such as amyloid-beta and synuclein, offering valuable insights into diseases like Alzheimer’s and Parkinson’s.

Infectious Diseases

Researchers employ nanodiscs to investigate viral entry proteins and immune receptor interactions, contributing to vaccine design and antiviral drug development .

Others

This includes applications in biomarker discovery , biosensing , and nanomedicine for studying diverse biological systems.

Market Segmentation (by Type)

Labeled

The labeled MSP protein segment leads the market, accounting for the largest share due to its high utility in spectroscopic , fluorescent , and imaging-based studies . These labeled nanodiscs facilitate visualization of membrane protein interactions at molecular resolution.

Unlabeled

The unlabeled MSP segment caters to structural studies requiring unmodified systems, widely used in Cryo-EM and biochemical characterization workflows.

Key Company

-

Cube Biotech

-

Creative Biostructure

-

Merck KGaA

-

ACROBiosystems

These key players are driving market innovation through high-quality MSP products, efficient nanodisc assembly solutions, and collaborative research initiatives focused on precision drug discovery and advanced structural biology.

Geographic Segmentation

| Region | 2024 Market Share | Forecast CAGR (2025–2032) | Key Highlights |

|---|---|---|---|

| North America | 39% | 6.0% | Dominant research ecosystem and high R&D spending |

| Europe | 27% | 5.8% | Advanced protein research and academic-industry collaborations |

| Asia-Pacific | 25% | 7.4% | Rapid biotech expansion and increased drug discovery programs |

| Latin America & MEA | 9% | 5.3% | Growing adoption of biotechnology research tools |

Future Outlook

The future of the Nanodisc MSP Protein Market looks promising, with expanding applications in precision medicine , AI-driven structural biology , and membrane protein therapeutics . As pharmaceutical and academic institutions increasingly integrate nanodisc technology into their R&D pipelines, market growth will accelerate.

Advancements in automated nanodisc assembly , label-free detection methods , and integration with computational protein modeling will further enhance accuracy, scalability, and accessibility.

Key Innovation

-

AI-Assisted Nanodisc Simulation Models for predicting lipid–protein interactions.

-

Dual-Labeled MSP Systems for advanced fluorescence resonance energy transfer (FRET) analysis.

-

Hybrid Nanodisc Platforms combining lipids with polymers for enhanced stability.

-

Cryo-EM Integration Pipelines for high-throughput membrane protein visualization.

-

Automated MSP Production Systems enabling scalable manufacturing for industrial research.

Get free sample of this report at : https://www.24lifesciences.com/download-sample/2737/nanodisc-msp-protein-market-market

About 24lifesciences

Founded in 2017, 24LifeScience has emerged as a trusted research and analytics partner for organizations operating within the global life sciences and chemical industries. Our core mission is to provide intelligent, future-ready insights that help clients stay ahead in an increasingly complex and innovation-driven market

International: +1(332) 2424 294 | Asia: +91 9425150513 (Asia)

Website: http://www.24lifesciences.com

Follow us on LinkedIn: http://www.linkedin.com/company/lifesciences24

Advanced Therapy Based on Gene Market Regional Analysis, Demand Analysis and Competitive Outlook 2025-2032

By lifesciencesid, 2025-10-27

Advanced Therapy Based on Gene refers to the cutting-edge field of biotechnology that focuses on using genetic material to treat, prevent, or potentially cure diseases at their root cause. Unlike conventional treatments that alleviate symptoms, gene-based therapies target the underlying genetic defects by introducing, replacing, or silencing specific genes.

Get free sample of this report at : https://www.24lifesciences.com/download-sample/2816/advanced-therapy-based-on-gene-market-market

These therapies encompass a range of advanced techniques, including gene therapy, gene editing (CRISPR-Cas9, TALENs, ZFNs), and cell-based gene transfer , enabling targeted correction of faulty genetic instructions. This transformative approach is reshaping the future of personalized medicine, regenerative healthcare, and rare disease treatment.

Market Size

The global Advanced Therapy Based on Gene market was valued at USD 12,500 million in 2024 and is projected to reach USD 48,250 million by 2031 , growing at a robust CAGR of 21.8% during the forecast period (2025–2032).

This exponential growth is fueled by technological breakthroughs in genetic engineering, a growing pipeline of clinical trials, and the increasing success rate of gene therapies gaining regulatory approvals worldwide. The expanding application of gene-based treatments in oncology, neurology, and rare diseases underscores the market’s transformative potential.

Recent Development

In recent years, the gene therapy landscape has witnessed remarkable progress through innovation and regulatory milestones:

FDA and EMA Approvals: Notable approvals include Zolgensma (Novartis) for spinal muscular atrophy and Luxturna (Spark Therapeutics) for inherited retinal disease.

CRISPR-Based Clinical Trials: Trials using CRISPR-Cas9 technology for beta-thalassemia and sickle cell anemia have shown encouraging long-term efficacy and safety outcomes.

Manufacturing Expansion: Companies like Biogen and Gilead Sciences are scaling up their viral vector production to meet increasing global demand.

Strategic Collaborations: Partnerships between pharma and biotech firms, such as Sarepta Therapeutics with Roche , are accelerating therapy commercialization.

Next-Gen Delivery Systems: Emerging non-viral vector technologies promise safer and more efficient gene delivery with reduced immune response risk.

Market Dynamics

Drivers

Growing Burden of Genetic Disorders: Over 400 million people globally suffer from rare genetic diseases, fueling the need for curative gene-based interventions.

Advancements in Genetic Engineering: CRISPR-Cas9 and other gene-editing platforms have revolutionized precision medicine and therapeutic accuracy.

Rising R&D Investments: Governments and private investors are increasingly funding gene therapy startups and clinical programs.

Regulatory Support: Streamlined approval pathways such as FDA’s Regenerative Medicine Advanced Therapy (RMAT) designation are expediting market entry.

Restraints

High Therapy Costs: Gene therapies can exceed USD 1 million per treatment, posing affordability challenges.

Manufacturing Complexity: Producing viral vectors and ensuring product consistency remain major technical hurdles.

Safety and Ethical Concerns: Risks associated with off-target gene editing and immune reactions may slow adoption.

Opportunities

Emergence of Non-Viral Vectors: Advances in lipid nanoparticles and mRNA-based delivery systems promise lower risk and higher scalability.

Expanding Therapeutic Applications: Beyond genetic disorders, gene-based therapies are being explored for oncology, cardiovascular, and infectious diseases.

Global Market Penetration: Growing adoption in Asia-Pacific and Middle Eastern markets presents vast untapped potential.

Regional Analysis

North America

North America dominates the global market, accounting for the largest share due to its strong biotechnology ecosystem, high R&D funding, and a large concentration of gene therapy companies. The U.S. leads in clinical trials, FDA-approved therapies, and investment in next-generation gene editing platforms.

Europe

Europe holds a significant market position supported by the European Medicines Agency’s (EMA) favorable regulatory frameworks and public-private research partnerships. The U.K., Germany, and France are key contributors, with growing focus on rare disease therapies.

Asia-Pacific

The Asia-Pacific region is expected to witness the fastest growth during 2025–2032, driven by expanding biopharmaceutical industries in China, Japan, and South Korea , along with government initiatives supporting genomics and regenerative medicine.

Latin America and Middle East & Africa

These regions are emerging markets with increasing awareness and access to advanced therapies. Governments are beginning to invest in healthcare modernization, setting the stage for future growth as costs decline and infrastructure improves.

Competitor Analysis

The Advanced Therapy Based on Gene market features a dynamic competitive landscape marked by strategic alliances, acquisitions, and technological innovation.

Major players are focusing on expanding their gene therapy pipelines, improving delivery mechanisms, and securing regulatory approvals for breakthrough products.

Key Companies:

Biogen – Pioneering neurological gene therapies and CNS-focused R&D programs.

Novartis – Leader in commercialized gene therapies such as Zolgensma .

Gilead Sciences – Through its Kite Pharma division, it develops cutting-edge CAR-T and gene-modified therapies.

Sarepta Therapeutics – Specializes in gene therapy for muscular dystrophies and neuromuscular disorders.

Alnylam Pharmaceuticals – A frontrunner in RNA interference (RNAi)-based therapies.

Amgen , Spark Therapeutics , Akcea Therapeutics , Sunway Biotech , SIBIONO , AnGes , Orchard Therapeutics , and Human Stem Cells Institute also contribute significantly to the global gene therapy ecosystem.

These companies collectively drive innovation through advanced delivery platforms, large-scale production facilities, and collaborative research networks.

Market Segmentation (by Application)

Cancer

The cancer segment holds the dominant share due to the high global cancer burden and significant advancements in gene-targeted immunotherapies such as CAR-T cell therapy. Gene modification techniques enable precise targeting of tumor antigens, offering improved survival rates and reduced side effects.

Neurological Diseases

Gene therapies for neurological disorders, including Parkinson’s, Huntington’s, and spinal muscular atrophy, are gaining traction with clinical successes like Zolgensma and experimental CRISPR-based trials.

Other Applications

This includes cardiovascular diseases, rare metabolic disorders, and inherited immunodeficiencies, where gene therapies are showing increasing promise.

Market Segmentation (by Type)

Viral

The viral vector segment dominates the market due to its established safety profile, high transfection efficiency, and widespread clinical adoption. Adeno-associated viruses (AAV) and lentiviruses are the most common platforms used for gene delivery.

Non-Viral

The non-viral segment is rapidly emerging, driven by advancements in lipid nanoparticles, electroporation, and polymer-based delivery systems that minimize immune responses and manufacturing costs.

Key Company

Biogen, Novartis, Gilead Sciences, Sarepta Therapeutics, Alnylam Pharmaceuticals, Amgen, Spark Therapeutics, Akcea Therapeutics, Sunway Biotech, SIBIONO, AnGes, Orchard Therapeutics, and Human Stem Cells Institute are the major contributors to innovation, production, and commercialization of advanced gene-based therapies. Their collaborations and research initiatives are propelling the market forward.

Geographic Segmentation

| Region | 2024 Market Share | CAGR (2025–2032) | Key Highlights |

|---|---|---|---|

| North America | 40% | 20.5% | Strong biotech base, FDA approvals, and R&D intensity |

| Europe | 28% | 19.8% | Favorable EMA regulations and public-private partnerships |

| Asia-Pacific | 24% | 25.1% | Rapid growth in China and Japan, expanding research infrastructure |

| Latin America & MEA | 8% | 17.5% | Gradual adoption and increasing healthcare investment |

Future Outlook

The future of gene-based advanced therapies is highly promising, with transformative potential across various therapeutic areas.

By 2032, the market is expected to evolve into a mainstream treatment segment as manufacturing costs decline, regulatory pathways mature, and global accessibility improves. Integration of AI-driven genomics , personalized treatment platforms , and next-generation gene editing tools will revolutionize healthcare delivery and disease management.

Key Innovation

-

CRISPR and Base Editing Platforms for precise gene correction

-

RNA-based and Epigenetic Therapies offering reversible genetic modulation

-

Automated Viral Vector Manufacturing Systems improving scalability

-

AI and Bioinformatics in Gene Target Identification

-

Personalized Gene Therapy Models enabling patient-specific customization

About 24lifesciences

Founded in 2017, 24LifeScience has emerged as a trusted research and analytics partner for organizations operating within the global life sciences and chemical industries. Our core mission is to provide intelligent, future-ready insights that help clients stay ahead in an increasingly complex and innovation-driven market

International: +1(332) 2424 294 | Asia: +91 9425150513 (Asia)

Website: http://www.24lifesciences.com

Follow us on LinkedIn: http://www.linkedin.com/company/lifesciences24

Ultra-thin Glass Market Emerging Innovations Reshaping Consumer Electronics and Automotive Applications Globally

By Apeksha More, 2025-10-27

The global Ultra-thin Glass Market is witnessing a remarkable transformation, driven by groundbreaking innovations across consumer electronics and automotive sectors. As industries demand lighter, more flexible, and durable materials, ultra-thin glass (UTG) has become a critical enabler of modern product design and performance. With its combination of superior optical clarity, mechanical strength, and reduced thickness, ultra-thin glass is redefining the capabilities of next-generation devices and vehicles. From foldable smartphones and augmented reality (AR) interfaces to advanced automotive displays, the market is poised for sustained expansion in the coming years.

Rising Integration Across Consumer Electronics

Consumer electronics manufacturers are rapidly adopting ultra-thin glass to meet the growing demand for sleek, portable, and innovative device designs. Modern smartphones, tablets, and laptops rely heavily on display surfaces that combine flexibility with strength. Ultra-thin glass provides the perfect balance — being thinner than human hair yet offering enhanced durability and scratch resistance. As foldable and rollable displays become more mainstream, manufacturers are prioritizing UTG for its superior bending performance compared to conventional materials such as plastic or thicker glass.

Furthermore, wearable technology manufacturers are embracing ultra-thin glass for devices such as smartwatches, augmented reality headsets, and smartbands. Its excellent transparency ensures bright and crisp displays, while its lightweight form supports user comfort. The rapid evolution of display technologies such as OLED and micro-LED has further boosted the material’s relevance. As display resolutions and brightness levels continue to advance, the need for optically precise, durable cover materials grows stronger — positioning ultra-thin glass as a central component in the future of consumer electronics.

Technological Innovations Enhancing Product Performance

Recent innovations in ultra-thin glass manufacturing are reshaping market dynamics globally. Cutting-edge processes such as chemical tempering, roll-to-roll production, and ion-exchange strengthening are enabling mass production at lower costs while improving product consistency. These technological advancements have enhanced the glass’s resistance to bending, cracking, and scratching — critical properties for consumer and automotive applications.

Notably, developments in nano-coating and surface treatment technologies are improving anti-reflective, fingerprint-resistant, and hydrophobic properties. Such coatings are especially beneficial for touchscreen and in-vehicle display applications, where visibility and cleanliness are key. Additionally, manufacturers are introducing hybrid materials that combine ultra-thin glass with flexible polymers, offering improved resilience without compromising flexibility. These hybrid composites are emerging as promising solutions for next-generation foldable and wearable devices.

Expanding Role in Automotive Displays and Interiors

The automotive industry is undergoing a digital revolution, with display technologies playing a central role in vehicle design and functionality. Ultra-thin glass is now being integrated into digital instrument clusters, infotainment panels, and head-up displays (HUDs), offering unmatched visual clarity and durability. As vehicles transition toward electric and autonomous systems, the demand for advanced display solutions continues to surge.

Automakers are increasingly using ultra-thin glass for its lightweight and form-fitting properties, which allow seamless integration into curved or edge-to-edge dashboard displays. In high-end vehicles, UTG is also being employed in touch-control panels, smart mirrors, and interior lighting interfaces. Beyond aesthetics, ultra-thin glass improves safety and performance by providing anti-glare and shatter-resistant features. Its thermal stability makes it well-suited for high-temperature automotive environments, where conventional plastics often fail to perform consistently.

Moreover, as connected vehicles become more prevalent, the need for durable and responsive display interfaces grows. Ultra-thin glass enables precise touch sensitivity and long-term optical quality, making it indispensable in modern automotive design. Industry players are also exploring UTG applications in solar roofs, navigation panels, and adaptive smart windows — extending its potential far beyond traditional display use.

Sustainability and Manufacturing Efficiency

Sustainability has emerged as a key driver in ultra-thin glass market innovation. Manufacturers are increasingly adopting environmentally conscious production methods, focusing on energy efficiency, material recyclability, and waste reduction. Advanced float glass and fusion draw processes enable the creation of thinner sheets with minimal energy input, significantly reducing carbon emissions during manufacturing.

Furthermore, research initiatives are directed toward developing eco-friendly coatings and chemical treatments that avoid hazardous substances. The integration of automation and smart manufacturing systems in production facilities has also improved consistency, yield rates, and scalability. As demand for high-performance materials continues to rise, such advancements will play a vital role in ensuring the sustainable expansion of the ultra-thin glass market worldwide.

Regional Developments and Competitive Landscape

Asia-Pacific remains the dominant hub for ultra-thin glass production, driven by the presence of leading manufacturers in China, Japan, and South Korea. These countries have established strong supply chains catering to global electronics and automotive industries. China, in particular, has become a powerhouse in ultra-thin glass fabrication, supported by government initiatives promoting high-tech material development. Meanwhile, South Korean and Japanese manufacturers continue to lead in innovation, especially in precision coating and glass strengthening technologies.

In North America and Europe, rising investments in electric vehicle production, renewable technologies, and smart consumer devices are driving additional market growth. Companies in these regions are focusing on strategic collaborations and R&D partnerships to enhance material performance and expand application scope. Competitive strategies among key players include product diversification, partnerships with OEMs, and technological integration to strengthen market presence.

Major industry participants such as Corning Incorporated, SCHOTT AG, AGC Inc., Nippon Electric Glass, and Asahi Glass are continuously investing in next-generation ultra-thin glass solutions. Their focus on combining performance, flexibility, and sustainability positions them to capitalize on emerging market opportunities across multiple verticals.

Future Outlook

The future of the Ultra-thin Glass Market appears exceptionally promising as technological innovations and end-user demand align toward more flexible, durable, and sustainable material solutions. With ongoing miniaturization in electronics and increased digitalization in automotive systems, the material’s versatility ensures long-term relevance. Its integration into future applications such as smart windows, solar panels, and transparent displays will further diversify its role across industries.

As global manufacturers invest in research, automation, and eco-friendly production methods, ultra-thin glass will continue to set new standards in product performance and design. The convergence of innovation, energy efficiency, and evolving consumer expectations guarantees that ultra-thin glass remains at the forefront of the world’s technological transformation.

Lipidic Cubic Phase Crystallization Service Market Regional Analysis, Demand Analysis and Competitive Outlook 2025-2032

By lifesciencesid, 2025-10-27

Lipidic Cubic Phase (LCP) crystallization is an advanced structural biology technique widely used to study membrane proteins, particularly G-protein coupled receptors (GPCRs). This method involves the formation of a stable lipid bilayer matrix that mimics the natural membrane environment, enabling high-resolution crystallization where traditional vapor diffusion or microbatch techniques often fail.

The LCP approach combines aqueous and lipid components to form a three-dimensional network of bilayers and water channels, providing an ideal environment for membrane protein stability and crystallization.

Get free sample of this report at : https://www.24lifesciences.com/download-sample/2744/lipidic-cubic-phase-crystallization-service-market-market

Market Size

The global lipidic cubic phase crystallization service market was valued at USD 293 million in 2024 and is projected to grow from USD 315 million in 2025 to USD 463 million by 2031 , registering a CAGR of 6.9% during the forecast period (2025–2032).

This growth is driven by the expanding demand for structural biology research, particularly for understanding GPCRs and other complex membrane proteins crucial for modern drug discovery.

Recent Development

Recent advancements in automation and high-throughput screening have transformed the LCP crystallization workflow. Innovations include:

- Automated LCP Robots – Enhancing reproducibility and reducing manual labor in crystal setup (e.g., Formulatrix and Cube Biotech systems).

- Next-generation Lipid Matrices – Improved monoolein derivatives offering superior stability and broader pH compatibility.

- Integration with Cryo-EM and X-ray Diffraction – Hybrid analytical workflows now enable atomic-level insights into protein structures, improving pharmaceutical design efficiency.

- Collaborations in Structural Biology – Academic and pharmaceutical alliances are expanding global access to crystallization services and data-sharing networks.

Market Dynamics

Drivers

- Rising Focus on GPCR and Membrane Protein Research: Over 30% of FDA-approved drugs target GPCRs, driving demand for high-quality crystallization services.

- Growth in Pharmaceutical R&D Spending: Increased investments in biopharmaceutical research enhance the use of LCP crystallization in drug discovery.

- Technological Advancements: Automation and AI-driven image analysis tools improve crystal detection accuracy and yield.

Restraints

- High Cost and Technical Complexity: The specialized nature of LCP crystallization demands skilled personnel and high-end infrastructure, limiting its adoption among smaller institutions.

- Limited Availability of Expertise: A shortage of trained crystallographers slows large-scale adoption in developing regions.

Opportunities

- Emerging Structural Genomics Programs: Government and institutional funding for protein structure projects in Asia-Pacific offer growth prospects.

- Expansion of Contract Research Organizations (CROs): Increasing outsourcing of crystallization services boosts market accessibility.

Regional Analysis

North America

North America dominates the global market, attributed to strong biopharmaceutical R&D investments, presence of leading CROs, and well-established structural biology centers in the U.S. and Canada. The region benefits from collaborations between academia and industry for GPCR-based drug design.

Europe

Europe represents a mature market with high adoption in academic research and drug discovery projects, particularly in Germany, the U.K., and Switzerland. Research consortia such as Instruct-ERIC support advanced crystallization initiatives across the EU.

Asia-Pacific

The Asia-Pacific region is projected to record the highest CAGR during 2025–2032. Expanding research infrastructure, increased government funding in countries like China, Japan, and India, and a growing number of biopharmaceutical startups are fueling market expansion.

Latin America & Middle East

These regions are gradually adopting LCP crystallization services through academic collaborations and technology transfers. Although market penetration remains low, increasing investments in life sciences are expected to create future growth opportunities.

Competitor Analysis

Leading players in the Lipidic Cubic Phase Crystallization Service Market are investing in automation, lipid chemistry innovation, and service expansion. Key strategies include partnerships with research institutions and the development of proprietary crystallization platforms.

Major Companies:

- Cube Biotech – Offers specialized LCP reagents and protein purification solutions.

- Creative Biostructure – Provides comprehensive crystallization and structural biology services.

- Formulatrix – Known for automated imaging and crystallization systems.

- Anatrace – Supplies detergents and lipids tailored for membrane protein studies.

- Jena Bioscience GmbH – Offers advanced lipid matrices and LCP-related consumables.

These firms collectively strengthen the market through innovation, collaboration, and the introduction of new lipidic formulations.

Market Segmentation (by Application)

Pharmaceutical Companies

This segment dominates the market, driven by intensive drug discovery programs targeting GPCRs and ion channels. LCP crystallization enables accurate protein modeling, accelerating lead optimization and validation.

Academic Research Institutes

Academic institutions utilize LCP crystallization for structural genomics and functional protein analysis, supported by public research grants and collaborative networks.

Others

Includes biotechnology startups and CROs offering contract-based crystallization services to pharmaceutical firms and research laboratories.

Market Segmentation (by Type)

Monoolein

The monoolein segment leads the market due to its superior biocompatibility, stability, and proven efficacy in membrane protein crystallization. Its versatility across temperature and pH ranges makes it the lipid of choice for LCP studies.

Monopalmitolein

Used for proteins sensitive to specific lipid environments, monopalmitolein supports alternative crystallization conditions, expanding the applicability of LCP techniques.

Others

Includes novel synthetic lipids and mixtures tailored to complex protein structures, offering flexibility for unique crystallization requirements.

Key Companies

- Cube Biotech

- Creative Biostructure

- Formulatrix

- Anatrace

- Jena Bioscience GmbH

Each of these companies contributes to advancing LCP crystallization by offering cutting-edge lipid products, customized crystallization setups, and AI-enabled image analysis systems.

Geographic Segmentation

| Region | 2024 Market Share | Forecast Growth (CAGR 2025–2032) | Key Insights |

|---|---|---|---|

| North America | 38% | 6.5% | Dominance due to pharma R&D investment and GPCR focus |

| Europe | 27% | 6.2% | Strong academic collaborations and research grants |

| Asia-Pacific | 25% | 8.1% | Rapidly emerging with new structural biology centers |

| Latin America & MEA | 10% | 5.4% | Growing adoption via technology partnerships |

Future Outlook

The future of the Lipidic Cubic Phase Crystallization Service Market looks promising, with increasing integration of AI, robotics, and cryo-electron microscopy (cryo-EM) expanding its application scope. As pharmaceutical companies pursue precision drug design, demand for membrane protein crystallography will continue to rise. Emerging economies are expected to witness significant adoption as local biotech ecosystems mature and funding support strengthens.

Key Innovation

- AI-Driven Crystal Imaging and Classification Systems

- Microfluidic LCP Platforms for Miniaturized Experiments

- Hybrid Crystallography-CryoEM Pipelines

- Customized Synthetic Lipid Libraries for Complex Proteins

- Collaborative Cloud Databases for Protein Structure Sharing

Get free sample of this report at : https://www.24lifesciences.com/download-sample/2744/lipidic-cubic-phase-crystallization-service-market-market

About 24lifesciences

Founded in 2017, 24LifeScience has emerged as a trusted research and analytics partner for organizations operating within the global life sciences and chemical industries. Our core mission is to provide intelligent, future-ready insights that help clients stay ahead in an increasingly complex and innovation-driven market

International: +1(332) 2424 294 | Asia: +91 9425150513 (Asia)

Website: http://www.24lifesciences.com

Follow us on LinkedIn: http://www.linkedin.com/company/lifesciences24

Artificial Intelligence in Transportation Market Investment Opportunities, Future Trends, Business Demand and Growth Forecast 2032

By ashpak, 2025-10-27

Market Overview:

Artificial Intelligence in Transportation Market size was valued at USD 3.72 Bn in 2024 and the total Artificial Intelligence in Transportation Market revenue is expected to grow at 17.85% through 2025 to 2032, reaching nearly USD 13.84 Bn, with Autonomous Trucks serving as powerful engine fuelling this transformative surge.

A detailed analysis of the Global Artificial Intelligence in Transportation Market is presented, offering crucial Market intelligence, demand and pricing assessments, and a thorough competitive landscape review. This report provides a current Market overview and projects trends through 2030.

To delve deeper into this research, kindly explore the following link: https://www.maximizemarketresearch.com/request-sample/24592/

Research Scope and Methodology:

This Global Artificial Intelligence in Transportation Market report offers a global perspective, examining key factors influencing Market dynamics, including trends, challenges, and opportunities. Segmentation is provided by end-user industry, service type, company size, and geographic region. Major Market players are profiled, with a focus on their strategies, product portfolios, revenue, and Market positioning. Macroeconomic influences, regulatory frameworks, and technological advancements are also analyzed to provide a holistic Market view.

Our research methodology blends primary and secondary research. Primary research involves direct engagement with industry stakeholders, including key Market participants, experts, and end-users, through interviews, surveys, and direct communication. Secondary research complements this by leveraging existing data from published reports, company information, trade publications, government databases, and reputable online sources. This rigorous approach ensures the accuracy, reliability, and validity of the insights presented, empowering stakeholders to make informed decisions and capitalize on emerging opportunities.

Regional Market Dynamics:

Understanding regional nuances is crucial for navigating the Global Artificial Intelligence in Transportation Market. The report segments the Market into North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa. For each region, we analyze key influencing factors, Market size, growth rate, and import/export dynamics. This section provides a snapshot of the current Market status within each covered country.

Eager to discover what's within? Secure your sample copy of the report today: https://www.maximizemarketresearch.com/request-sample/24592/

Market Segmentation:

by Machine Learning

Deep Learning

Computer Vision

Context Awareness

Natural Language Processing

by Offering

Hardware

• Neuromorphic

• Von Nuemann

Software

• Platforms

• Solutions

by Process

Signal Recognition

Object Recognition

Data Mining & Analytics

by Application

Autonomous Trucks

HMI

Semi-Autonomous Trucks

Others

To explore further details about this research, please go to: https://www.maximizemarketresearch.com/request-sample/24592/

Key Market Participants:

1. Continental (Hanover, Germany)

2. Volvo

3. ZF

4. Zonar

5. Tier-I Suppliers

6. Daimler (Stuttgart, Germany)

7. Scania

8. Microsoft

9. Paccar

10. Man

11. Bosch

12. NVIDIA

13. Valeo

14. Peloton

15. Xevo

16. Software Suppliers

17. Start-Up’s Bosch

18. Intel

19. Alphabet

20. Magna

21. Nauto

22. IBM Corporation

Key Questions Addressed:

What is Global Artificial Intelligence in Transportation?

What was the Global Artificial Intelligence in Transportation Market size in 2024?

Who are the major players and what are their offerings in the Global Artificial Intelligence in Transportation Market?

What growth strategies are key players employing to expand their Market share?

What are the emerging applications and future trends in the Global Artificial Intelligence in Transportation Market?

What factors are driving Market growth?

What current industry trends can be leveraged for revenue generation in the Global Artificial Intelligence in Transportation Market?

What are the various Market segments?

What is the projected CAGR for the Global Artificial Intelligence in Transportation Market?

What is the Market's growth trajectory?

What specific segments are covered in the report?

What are the key challenges and opportunities facing the Market?

Which application segment holds the most significant potential?

Who are the key players in the Global Artificial Intelligence in Transportation Market?

Want a comprehensive Market analysis? Check out the summary of the research report: https://www.maximizemarketresearch.com/market-report/global-artificial-intelligence-ai-in-transportation-market/24592/

Key Deliverables:

Historical Market Size and Competitive Landscape (2019-2024)

Historical Pricing Data and Regional Price Trends (2019-2024)

Market Size, Share, and Forecast by Segment (2025-2032)

Market Drivers, Restraints, Opportunities, and Key Trends by Region

Granular Market Segmentation Analysis by Segment and Sub-segment, with Regional Breakdown

In-depth Competitive Landscape Analysis, including Strategic Profiles of Key Players by Region:

Market Leaders

Market Followers

Regional Players

Competitive Benchmarking by Region

PESTLE Analysis

Porter's Five Forces Analysis

Value Chain and Supply Chain Analysis

Regional Legal and Regulatory Considerations

SWOT Analysis of Lucrative Business Opportunities

Strategic Recommendations

Catch Up with Trending Topics:

Lancets Market

https://www.maximizemarketresearch.com/market-report/global-lancets-market/31935/

Parenteral Nutrition Market

https://www.maximizemarketresearch.com/market-report/parenteral-nutrition-market/38008/

About Us:

Maximize Market Research is one of the fastest-growing Market research and business consulting firms serving clients globally. Our revenue impact and focused growth-driven research initiatives make us a proud partner of majority of the Fortune 500 companies. We have a diversified portfolio and serve a variety of industries such as IT & telecom, chemical, food & beverage, aerospace & defense, healthcare and others.

Contact Us:

MAXIMIZE Market RESEARCH PVT. LTD.

3rd Floor, Navale IT park Phase 2,

Pune Banglore Highway, Narhe

Pune, Maharashtra 411041, India.

+91 9607365656

sales@maximizeMarketresearch.com

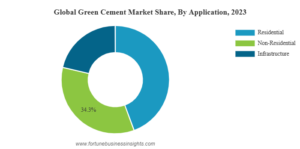

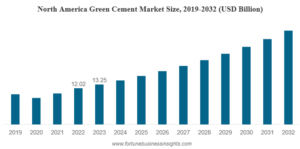

According to Fortune Business Insights, The global green cement market was valued at USD 35.65 billion in 2023 and is expected to grow from USD 39.32 billion in 2024 to USD 83.28 billion by 2032, registering a CAGR of 9.9% during the forecast period. North America led the global market with a 37.17% share in 2023. In the U.S., the green cement market is anticipated to witness substantial growth, reaching approximately USD 28.89 billion by 2032, fueled by the increasing adoption of sustainable cement alternatives in both residential and non-residential construction projects.

Green cement is an eco-friendly alternative to conventional cement, primarily produced using industrial by-products such as blast furnace slag and fly ash. Its production process is highly energy-efficient, as leading manufacturers employ advanced technologies to minimize carbon emissions. As per JK Lakshmi Cement Ltd., the use of green cement in construction can help reduce carbon footprints by up to 40%, making it a crucial component of sustainable building practices.

The global green cement market is witnessing strong growth as the construction industry increasingly adopts sustainable materials to reduce carbon emissions. Green cement, an eco-friendly alternative to traditional Portland cement, is produced using industrial waste such as fly ash, slag, and recycled aggregates. This shift supports global efforts toward carbon neutrality and sustainable infrastructure development.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/green-cement-market-107251

Market Overview

The green cement market is projected to experience substantial expansion from 2024 to 2032. Rising environmental awareness, stringent government regulations on carbon emissions, and growing investment in green infrastructure projects are key drivers fueling market growth. Increasing urbanization and demand for energy-efficient buildings further accelerate adoption across residential, commercial, and industrial sectors.

Key Market Drivers

1. Growing Focus on Sustainability and Carbon Reduction

The construction sector is one of the largest contributors to global CO₂ emissions. Green cement reduces carbon output by up to 30–40% compared to conventional cement, aligning with global sustainability goals such as the Paris Agreement. Governments and corporations are actively promoting low-carbon materials to meet green building certification standards such as LEED and BREEAM.

2. Rising Demand in Infrastructure Development

Massive infrastructure projects in emerging economies—such as smart cities, transportation networks, and renewable energy plants—are propelling demand for sustainable building materials. Green cement’s durability and low environmental impact make it an ideal choice for large-scale construction.

3. Technological Innovations and Product Advancements

Continuous R&D has led to innovative formulations of green cement incorporating materials like geopolymers, rice husk ash, and silica fume. These advancements enhance product performance while minimizing clinker usage, further lowering emissions and energy consumption during production.

Market Segmentation

By Type:

Fly Ash-Based Cement

Slag-Based Cement

Recycled Aggregate Cement

Others (Geopolymer Cement, Limestone Calcined Clay Cement, etc.)

By Application:

Residential

Non-Residential (Commercial, Industrial)

Infrastructure (Roads, Bridges, Dams, etc.)

By Region:

North America: Driven by strict environmental policies and green building initiatives.

Europe: Leading in eco-friendly construction standards and carbon-neutral targets.

Asia Pacific: Expected to dominate the market, fueled by rapid urbanization in China, India, and Southeast Asia.

Latin America and Middle East & Africa: Emerging markets showing growing awareness and adoption of sustainable materials.

Regional Insights

Asia Pacific holds the largest market share owing to robust construction activities and government-led sustainability programs. India and China are heavily investing in green infrastructure, supported by public-private partnerships.

Europe continues to be a pioneer in adopting sustainable construction materials, backed by stringent EU environmental regulations.

North America is seeing increased adoption due to corporate ESG commitments and government incentives for green buildings.

Key Industry Players

Leading companies in the global green cement market are focusing on strategic mergers, partnerships, and sustainable manufacturing technologies to strengthen their positions. Major players include:

LafargeHolcim Ltd.

HeidelbergCement AG

CEMEX S.A.B. de C.V.

CRH plc

UltraTech Cement Ltd.

Calera Corporation

Anhui Conch Cement Co., Ltd.

These players are actively investing in carbon capture technologies, alternative fuel use, and waste material integration to meet sustainability targets.

The future of the green cement market looks promising as governments, corporations, and consumers increasingly prioritize sustainability. The demand for carbon-neutral buildings, coupled with the growing use of recycled materials in cement production, will continue to propel market growth through 2032.

The green cement market is set to redefine the global construction industry by offering sustainable, durable, and cost-effective alternatives to traditional cement. As eco-conscious construction practices become the norm, innovations in green cement manufacturing will play a pivotal role in achieving a low-carbon future.

Information Source: https://www.fortunebusinessinsights.com/green-cement-market-107251

KEY INDUSTRY DEVELOPMENTS:

- November 2023: Heidelberg Cement launched the low-carbon cement brand to reduce greenhouse gas emissions during the cement manufacturing and mixing process.

- October 2022 : JSW Cement planned to invest USD 390 million to begin an integrated green cement production facility in Madhya Pradesh and a split grinding unit in Uttar Pradesh. The proposed investment includes a 2.5 MTPA grinding capacity, 15 MW Waste heat recovery system, and 2.5 MTPA clinker capacity.

According to Fortune Business Insights™, the global Inertial Navigation System Market is anticipated to record significant growth in the coming years, reaching an estimated value of USD 24.28 billion. The market is forecast to expand at a compound annual growth rate (CAGR) of 8.6% over the period 2025–2032.

The report on the Inertial Navigation System Market provides an in-depth assessment of the current industry landscape as well as future opportunities. It examines crucial aspects including market size, emerging trends, growth drivers, restraints, and potential opportunities. Furthermore, the study evaluates consumer behavior, regional developments, demand dynamics, and technological advancements. These insights are designed to support businesses, investors, and stakeholders in identifying profitable opportunities, formulating strategic decisions, and effectively addressing market challenges.

Latest Trends in the Inertial Navigation System Market

The global Inertial Navigation System Market is undergoing significant transformation, fueled by rapid technological advancements, evolving customer expectations, and shifting global dynamics. A key development is the accelerated adoption of digital technologies and automation, which enable organizations to streamline operations, improve efficiency, and lower operational costs.

Sustainability has emerged as a central focus, with leading companies investing in eco-friendly solutions such as energy-efficient systems, green manufacturing practices, and sustainable supply chains. At the same time, the integration of artificial intelligence (AI), machine learning (ML), and advanced analytics is revolutionizing decision-making, enhancing productivity, and enabling data-driven solutions across the industry.

The market is also seeing rising demand for product customization and enhanced user experiences, prompting businesses to innovate in design and deliver tailored offerings. In addition, the rapid expansion of e-commerce and digital platforms is reshaping customer engagement strategies, allowing deeper market penetration and opening new avenues for growth and differentiation in the Inertial Navigation System Market.

Key Companies

The global Inertial Navigation System Market is characterized by the presence of several leading companies that significantly influence the competitive landscape. These players focus on continuous product innovation, strategic collaborations, mergers and acquisitions, and international expansion to reinforce their market positions.

Some of the prominent companies operating in the market include:

- Bharat Electronic Limited (BEL) (India)

- Gladiator Technologies (U.S)

- Honeywell International Inc. (U.S.)

- iXblue SAS (France)

- Northrop Grumman Corporation (U.S.)

- Parker Hannifin Corporation (U.S.)

- RTX Corporation (U.S.)

- Safran S.A. (France)

- Teledyne Technologies Incorporated (U.S.)

- Thales Group (France)

- Trimble Inc. (U.S.)

- VectroNav Technologies LLC. (U.S.)

These key players are expected to remain instrumental in shaping the industry’s future by advancing technologies, setting new benchmarks, and driving the overall growth and transformation of the Inertial Navigation System Market in the years ahead.

Information Source:

https://www.fortunebusinessinsights.com/inertial-navigation-system-ins-market-102849

Report Scope

This report offers a comprehensive analysis of the Inertial Navigation System Market, delivering actionable insights for businesses, investors, policymakers, and other stakeholders. It provides an in-depth evaluation of market size, growth trajectories, key drivers, challenges, and emerging opportunities that are shaping the industry’s future.

The study encompasses detailed market segmentation by product type, application, end-user, and region, enabling a granular perspective on different market segments. Additionally, it examines the competitive landscape by profiling leading companies, analyzing their strategies, and highlighting recent innovations, mergers, acquisitions, and partnerships.

With its broad coverage, the report equips stakeholders with a clear understanding of market dynamics, supporting informed decision-making, effective strategic planning, and sustainable long-term growth initiatives.

Driving Factors

The growth of the Inertial Navigation System Market is being fueled by a combination of influential factors that are driving demand and fostering innovation. Key drivers include rapid technological advancements, shifting consumer preferences, and the increasing adoption of products and solutions across multiple industries.

Rising investments, supportive government initiatives, and growing disposable incomes are further accelerating market expansion. At the same time, evolving lifestyle trends and heightened awareness of sustainability are pushing companies to prioritize eco-friendly innovations, energy-efficient systems, and smarter product designs.

In addition, organizations are ramping up research and development (R&D) efforts to deliver advanced solutions, improve performance, and enhance user experiences—further strengthening market competitiveness. Collectively, these factors are expected to sustain growth momentum and open up new opportunities within the Inertial Navigation System Market over the forecast period.

Market Segmentation

The Inertial Navigation System Market is segmented to provide a detailed understanding of the industry landscape, based on key parameters such as product type, application, end-user, and region. This structured segmentation enables the identification of emerging trends, growth opportunities, and challenges within each category, supporting more informed strategic decisions for stakeholders.

By Service (Voice and Data), By Frequency (L-Band, S-Band, and Others), By End User (Aviation, Maritime, Government and Military, and Others), and Regional Forecast, 2023-2030

Regional Insights

Regional segmentation highlights how the market performs across different geographies, analyzing consumer behavior, investment patterns, and regulatory environments that shape market growth. The key regions covered include:

North America – Comprising the United States and Canada, this region leads with strong innovation, advanced technology adoption, and significant R&D investments.

Europe – Including Germany, the U.K., France, and other major economies, the region emphasizes industrial modernization, sustainability initiatives, and stringent regulatory frameworks.

Asia Pacific – Covering high-growth economies such as China, India, Japan, South Korea, and Southeast Asia, the region benefits from a vast consumer base, expanding digital infrastructure, and robust manufacturing capacity.

Latin America – Encompassing markets such as Brazil, Mexico, and Argentina, where infrastructure development, industrial expansion, and rising economic growth are driving demand.

Middle East & Africa – Featuring markets like GCC countries and South Africa, with increasing investments in energy, defense, construction, and smart technologies fueling market expansion.

Marine Parallel Hybrid Propulsion Market Share, Analysis, and Outlook 2023–2030

By Rishika19, 2025-10-27

According to Fortune Business Insights™, the global Marine Parallel Hybrid Propulsion Market is anticipated to record significant growth in the coming years, reaching an estimated value of USD 2.25 billion. The market is forecast to expand at a compound annual growth rate (CAGR) of 11.9% over the period 2023-2030.

The report on the Marine Parallel Hybrid Propulsion Market provides an in-depth assessment of the current industry landscape as well as future opportunities. It examines crucial aspects including market size, emerging trends, growth drivers, restraints, and potential opportunities. Furthermore, the study evaluates consumer behavior, regional developments, demand dynamics, and technological advancements. These insights are designed to support businesses, investors, and stakeholders in identifying profitable opportunities, formulating strategic decisions, and effectively addressing market challenges.

Latest Trends in the Marine Parallel Hybrid Propulsion Market

The global Marine Parallel Hybrid Propulsion Market is undergoing significant transformation, fueled by rapid technological advancements, evolving customer expectations, and shifting global dynamics. A key development is the accelerated adoption of digital technologies and automation, which enable organizations to streamline operations, improve efficiency, and lower operational costs.

Sustainability has emerged as a central focus, with leading companies investing in eco-friendly solutions such as energy-efficient systems, green manufacturing practices, and sustainable supply chains. At the same time, the integration of artificial intelligence (AI), machine learning (ML), and advanced analytics is revolutionizing decision-making, enhancing productivity, and enabling data-driven solutions across the industry.

The market is also seeing rising demand for product customization and enhanced user experiences, prompting businesses to innovate in design and deliver tailored offerings. In addition, the rapid expansion of e-commerce and digital platforms is reshaping customer engagement strategies, allowing deeper market penetration and opening new avenues for growth and differentiation in the Marine Parallel Hybrid Propulsion Market.

Key Companies

The global Marine Parallel Hybrid Propulsion Market is characterized by the presence of several leading companies that significantly influence the competitive landscape. These players focus on continuous product innovation, strategic collaborations, mergers and acquisitions, and international expansion to reinforce their market positions.

Some of the prominent companies operating in the market include:

- ABB Ltd. (Switzerland)

- Rolls-Royce Holdings plc (U.K.)

- Caterpillar Inc. (U.S.)

- General Electric Company (U.S.)

- Nidec Industrial Solutions (Italy)

- MAN Energy Solutions (Germany)

- Siemens AG (Germany)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Wärtsilä Oyj Abp (Finland)

- Cummins Inc. (U.S.)

These key players are expected to remain instrumental in shaping the industry’s future by advancing technologies, setting new benchmarks, and driving the overall growth and transformation of the Marine Parallel Hybrid Propulsion Market in the years ahead.

Information Source:

https://www.fortunebusinessinsights.com/marine-parallel-hybrid-propulsion-market-108735

Report Scope

This report offers a comprehensive analysis of the Marine Parallel Hybrid Propulsion Market, delivering actionable insights for businesses, investors, policymakers, and other stakeholders. It provides an in-depth evaluation of market size, growth trajectories, key drivers, challenges, and emerging opportunities that are shaping the industry’s future.

The study encompasses detailed market segmentation by product type, application, end-user, and region, enabling a granular perspective on different market segments. Additionally, it examines the competitive landscape by profiling leading companies, analyzing their strategies, and highlighting recent innovations, mergers, acquisitions, and partnerships.

With its broad coverage, the report equips stakeholders with a clear understanding of market dynamics, supporting informed decision-making, effective strategic planning, and sustainable long-term growth initiatives.

Driving Factors

The growth of the Marine Parallel Hybrid Propulsion Market is being fueled by a combination of influential factors that are driving demand and fostering innovation. Key drivers include rapid technological advancements, shifting consumer preferences, and the increasing adoption of products and solutions across multiple industries.

Rising investments, supportive government initiatives, and growing disposable incomes are further accelerating market expansion. At the same time, evolving lifestyle trends and heightened awareness of sustainability are pushing companies to prioritize eco-friendly innovations, energy-efficient systems, and smarter product designs.

In addition, organizations are ramping up research and development (R&D) efforts to deliver advanced solutions, improve performance, and enhance user experiences—further strengthening market competitiveness. Collectively, these factors are expected to sustain growth momentum and open up new opportunities within the Marine Parallel Hybrid Propulsion Market over the forecast period.

Market Segmentation

The Marine Parallel Hybrid Propulsion Market is segmented to provide a detailed understanding of the industry landscape, based on key parameters such as product type, application, end-user, and region. This structured segmentation enables the identification of emerging trends, growth opportunities, and challenges within each category, supporting more informed strategic decisions for stakeholders.

By Ship Type (Tugs & Barge, Offshore Vessel, Fishing Vessel, Research and Survey Vessel, Search & Rescue Vessel, Patrol Boats, Passenger Ship, Recreational Boats, & Landing Crafts), By Engine Power Rating (Upto 150 HP, 150 to 500 HP, 500 HP to 1,000 HP, and 1,000 HP to 3,000 HP), By Component (IC Engine, Generator, Power Management System, Battery, Gearbox), By Installment (Line Fit & Retro Fit), By Motor Capacity (Upto 50 KW, 50 KW to 200 KW, and 200 KW to 400 KW), and Regional Forecast, 2023-2030

Regional Insights

Regional segmentation highlights how the market performs across different geographies, analyzing consumer behavior, investment patterns, and regulatory environments that shape market growth. The key regions covered include:

North America – Comprising the United States and Canada, this region leads with strong innovation, advanced technology adoption, and significant R&D investments.

Europe – Including Germany, the U.K., France, and other major economies, the region emphasizes industrial modernization, sustainability initiatives, and stringent regulatory frameworks.

Asia Pacific – Covering high-growth economies such as China, India, Japan, South Korea, and Southeast Asia, the region benefits from a vast consumer base, expanding digital infrastructure, and robust manufacturing capacity.

Latin America – Encompassing markets such as Brazil, Mexico, and Argentina, where infrastructure development, industrial expansion, and rising economic growth are driving demand.

Middle East & Africa – Featuring markets like GCC countries and South Africa, with increasing investments in energy, defense, construction, and smart technologies fueling market expansion.

According to Fortune Business Insights™, the global Handgun Market is anticipated to record significant growth in the coming years, reaching an estimated value of USD 5.35 billion by 2030. The market is forecast to expand at a compound annual growth rate (CAGR) of 6.6% over the period 2023-2030.

The report on the Handgun Market provides an in-depth assessment of the current industry landscape as well as future opportunities. It examines crucial aspects including market size, emerging trends, growth drivers, restraints, and potential opportunities. Furthermore, the study evaluates consumer behavior, regional developments, demand dynamics, and technological advancements. These insights are designed to support businesses, investors, and stakeholders in identifying profitable opportunities, formulating strategic decisions, and effectively addressing market challenges.

Latest Trends in the Handgun Market

The global Handgun Market is undergoing significant transformation, fueled by rapid technological advancements, evolving customer expectations, and shifting global dynamics. A key development is the accelerated adoption of digital technologies and automation, which enable organizations to streamline operations, improve efficiency, and lower operational costs.

Sustainability has emerged as a central focus, with leading companies investing in eco-friendly solutions such as energy-efficient systems, green manufacturing practices, and sustainable supply chains. At the same time, the integration of artificial intelligence (AI), machine learning (ML), and advanced analytics is revolutionizing decision-making, enhancing productivity, and enabling data-driven solutions across the industry.

The market is also seeing rising demand for product customization and enhanced user experiences, prompting businesses to innovate in design and deliver tailored offerings. In addition, the rapid expansion of e-commerce and digital platforms is reshaping customer engagement strategies, allowing deeper market penetration and opening new avenues for growth and differentiation in the Handgun Market.

Key Companies

The global Handgun Market is characterized by the presence of several leading companies that significantly influence the competitive landscape. These players focus on continuous product innovation, strategic collaborations, mergers and acquisitions, and international expansion to reinforce their market positions.

Some of the prominent companies operating in the market include:

- Glock gmbh (Austria)

- SIG SAUER (U.S.)

- Sturm, Ruger & Co., Inc. (U.S.)

- FN HERSTAL (Belgium)

- Ceska zbrojovka a.s. (Czech Republic)

- Israel Weapon Industries (Israel)

- Colt's Manufacturing (U.S.)

- Beretta (Italy)

- Smith & Wesson (U.S.)

- Kalashnikov Group (Russia)

These key players are expected to remain instrumental in shaping the industry’s future by advancing technologies, setting new benchmarks, and driving the overall growth and transformation of the Handgun Market in the years ahead.

Information Source:

https://www.fortunebusinessinsights.com/handgun-market-108876

Report Scope

This report offers a comprehensive analysis of the Handgun Market, delivering actionable insights for businesses, investors, policymakers, and other stakeholders. It provides an in-depth evaluation of market size, growth trajectories, key drivers, challenges, and emerging opportunities that are shaping the industry’s future.

The study encompasses detailed market segmentation by product type, application, end-user, and region, enabling a granular perspective on different market segments. Additionally, it examines the competitive landscape by profiling leading companies, analyzing their strategies, and highlighting recent innovations, mergers, acquisitions, and partnerships.

With its broad coverage, the report equips stakeholders with a clear understanding of market dynamics, supporting informed decision-making, effective strategic planning, and sustainable long-term growth initiatives.

Driving Factors

The growth of the Handgun Market is being fueled by a combination of influential factors that are driving demand and fostering innovation. Key drivers include rapid technological advancements, shifting consumer preferences, and the increasing adoption of products and solutions across multiple industries.

Rising investments, supportive government initiatives, and growing disposable incomes are further accelerating market expansion. At the same time, evolving lifestyle trends and heightened awareness of sustainability are pushing companies to prioritize eco-friendly innovations, energy-efficient systems, and smarter product designs.

In addition, organizations are ramping up research and development (R&D) efforts to deliver advanced solutions, improve performance, and enhance user experiences—further strengthening market competitiveness. Collectively, these factors are expected to sustain growth momentum and open up new opportunities within the Handgun Market over the forecast period.

Market Segmentation

The Handgun Market is segmented to provide a detailed understanding of the industry landscape, based on key parameters such as product type, application, end-user, and region. This structured segmentation enables the identification of emerging trends, growth opportunities, and challenges within each category, supporting more informed strategic decisions for stakeholders.

By Type (Single-Shot Handguns (Muzzleloaders), Revolvers, and Semi-Automatic Pistols), By Operation (Automatic, Semi-Automatic, and Manual), By End-user (Defense & Homeland Security, Self-Defense, Sports, Hunting, and Law Enforcement), and Regional Forecast, 2023-2030

Regional Insights

Regional segmentation highlights how the market performs across different geographies, analyzing consumer behavior, investment patterns, and regulatory environments that shape market growth. The key regions covered include:

North America – Comprising the United States and Canada, this region leads with strong innovation, advanced technology adoption, and significant R&D investments.

Europe – Including Germany, the U.K., France, and other major economies, the region emphasizes industrial modernization, sustainability initiatives, and stringent regulatory frameworks.

Asia Pacific – Covering high-growth economies such as China, India, Japan, South Korea, and Southeast Asia, the region benefits from a vast consumer base, expanding digital infrastructure, and robust manufacturing capacity.

Latin America – Encompassing markets such as Brazil, Mexico, and Argentina, where infrastructure development, industrial expansion, and rising economic growth are driving demand.

Middle East & Africa – Featuring markets like GCC countries and South Africa, with increasing investments in energy, defense, construction, and smart technologies fueling market expansion.

According to Fortune Business Insights™, the global Mobile Satellite Services Market is anticipated to record significant growth in the coming years, reaching an estimated value of USD 8.63 billion. The market is forecast to expand at a compound annual growth rate (CAGR) of 6.5% over the period 2023-2030.

The report on the Mobile Satellite Services Market provides an in-depth assessment of the current industry landscape as well as future opportunities. It examines crucial aspects including market size, emerging trends, growth drivers, restraints, and potential opportunities. Furthermore, the study evaluates consumer behavior, regional developments, demand dynamics, and technological advancements. These insights are designed to support businesses, investors, and stakeholders in identifying profitable opportunities, formulating strategic decisions, and effectively addressing market challenges.

Latest Trends in the Mobile Satellite Services Market

The global Mobile Satellite Services Market is undergoing significant transformation, fueled by rapid technological advancements, evolving customer expectations, and shifting global dynamics. A key development is the accelerated adoption of digital technologies and automation, which enable organizations to streamline operations, improve efficiency, and lower operational costs.

Sustainability has emerged as a central focus, with leading companies investing in eco-friendly solutions such as energy-efficient systems, green manufacturing practices, and sustainable supply chains. At the same time, the integration of artificial intelligence (AI), machine learning (ML), and advanced analytics is revolutionizing decision-making, enhancing productivity, and enabling data-driven solutions across the industry.

The market is also seeing rising demand for product customization and enhanced user experiences, prompting businesses to innovate in design and deliver tailored offerings. In addition, the rapid expansion of e-commerce and digital platforms is reshaping customer engagement strategies, allowing deeper market penetration and opening new avenues for growth and differentiation in the Mobile Satellite Services Market.

Key Companies

The global Mobile Satellite Services Market is characterized by the presence of several leading companies that significantly influence the competitive landscape. These players focus on continuous product innovation, strategic collaborations, mergers and acquisitions, and international expansion to reinforce their market positions.

Some of the prominent companies operating in the market include:

- Inmarsat Plc (U.K.)

- Viasat, Inc. (U.S.)

- Globalstar, Inc. (U.S.)

- Iridium Communications Inc. (U.S.)

- Al Yah Satellite Communications Company P.J.S.C. (UAE)

- Intelsat S.A. (Luxembourg)

- EchoStar Corporation (U.S.)

- Eutelsat S.A. (France)

- Telesat Corporation (Canada)

- SES S.A. (Luxembourg)

- Telefonaktiebolaget LM Ericsson (Sweden)

- ORBCOMM Inc. (U.S.)

These key players are expected to remain instrumental in shaping the industry’s future by advancing technologies, setting new benchmarks, and driving the overall growth and transformation of the Mobile Satellite Services Market in the years ahead.

Information Source:

https://www.fortunebusinessinsights.com/mobile-satellite-services-mss-market-103743

Report Scope

This report offers a comprehensive analysis of the Mobile Satellite Services Market, delivering actionable insights for businesses, investors, policymakers, and other stakeholders. It provides an in-depth evaluation of market size, growth trajectories, key drivers, challenges, and emerging opportunities that are shaping the industry’s future.

The study encompasses detailed market segmentation by product type, application, end-user, and region, enabling a granular perspective on different market segments. Additionally, it examines the competitive landscape by profiling leading companies, analyzing their strategies, and highlighting recent innovations, mergers, acquisitions, and partnerships.

With its broad coverage, the report equips stakeholders with a clear understanding of market dynamics, supporting informed decision-making, effective strategic planning, and sustainable long-term growth initiatives.

Driving Factors

The growth of the Mobile Satellite Services Market is being fueled by a combination of influential factors that are driving demand and fostering innovation. Key drivers include rapid technological advancements, shifting consumer preferences, and the increasing adoption of products and solutions across multiple industries.

Rising investments, supportive government initiatives, and growing disposable incomes are further accelerating market expansion. At the same time, evolving lifestyle trends and heightened awareness of sustainability are pushing companies to prioritize eco-friendly innovations, energy-efficient systems, and smarter product designs.

In addition, organizations are ramping up research and development (R&D) efforts to deliver advanced solutions, improve performance, and enhance user experiences—further strengthening market competitiveness. Collectively, these factors are expected to sustain growth momentum and open up new opportunities within the Mobile Satellite Services Market over the forecast period.

Market Segmentation

The Mobile Satellite Services Market is segmented to provide a detailed understanding of the industry landscape, based on key parameters such as product type, application, end-user, and region. This structured segmentation enables the identification of emerging trends, growth opportunities, and challenges within each category, supporting more informed strategic decisions for stakeholders.

By Service (Voice and Data), By Frequency (L-Band, S-Band, and Others), By End User (Aviation, Maritime, Government and Military, and Others), and Regional Forecast, 2023-2030

Regional Insights

Regional segmentation highlights how the market performs across different geographies, analyzing consumer behavior, investment patterns, and regulatory environments that shape market growth. The key regions covered include:

North America – Comprising the United States and Canada, this region leads with strong innovation, advanced technology adoption, and significant R&D investments.

Europe – Including Germany, the U.K., France, and other major economies, the region emphasizes industrial modernization, sustainability initiatives, and stringent regulatory frameworks.