Category: Business

According to Fortune Business Insights , the global teeth whitening market size was valued at USD 8.52 billion in 2024 and is projected to grow from USD 8.93 billion in 2025 to USD 12.77 billion by 2032, registering a CAGR of 5.24% during the forecast period. Asia Pacific dominated the teeth whitening market with a market share of 33.80% in 2024.

- Asia Pacific witnessed teeth whitening market growth from USD 2.76 Billion in 2023 to USD 2.88 Billion in 2024.

The U.S. teeth whitening market is expected to reach USD 2.62 billion by 2032, driven by the rising adoption of at-home whitening kits and increasing consumer spending on self-care. Asia Pacific dominated the global market in 2024, accounting for 33.80% of the market share, supported by urbanization, Western beauty trends, and government-backed oral health initiatives.

Teeth whitening refers to cosmetic dental procedures and products that lighten the shade of teeth and enhance appearance. Popular products include whitening toothpaste , strips, gels, and rinses, widely available in pharmacies, supermarkets, and online channels. Growing influence from social media, celebrities, and lifestyle influencers is further fueling market demand.

Request Free Sample PDF Copy of Teeth Whitening Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/teeth-whitening-market-110349

Market Impact of COVID-19

The COVID-19 pandemic created a mixed scenario for the market. While many dental clinics faced closures during lockdowns, leading to reduced professional whitening treatments, consumer interest in at-home whitening kits surged significantly. According to the British Dental Association’s 2020 report, sales of at-home dental kits in the U.K. increased by 87%, reflecting a clear consumer shift toward self-care solutions.

Teeth Whitening Market Trends

- Rising Popularity of Cosmetic Dentistry

The growing availability of cosmetic dentistry services has encouraged consumers to adopt professional whitening treatments, driving market growth. According to the American Dental Association (2022), the U.S. had 214,700 dental hygienists and 363,880 dental assistants, highlighting the scale of cosmetic dentistry adoption.

- Growing Focus on Oral Hygiene

Consumers are increasingly incorporating oral hygiene into their lifestyle routines, boosting demand for teeth whitening products. In 2024, Dr. Dento launched natural ingredient-based oral care products, reflecting the shift toward healthier formulations.

- Technological Advancements in Whitening Solutions

The launch of LED light-activated gels, laser whitening treatments, and advanced at-home kits has enhanced effectiveness and convenience. In February 2024, Philips Oral Healthcare launched its Sonicare Tooth Whitening Kits , strengthening its product portfolio.

Market Restraints

Despite growth opportunities, sensitivity and gum irritation caused by whitening products limit consumer adoption. Concerns over side effects often push consumers toward alternative dental care solutions, restraining overall market expansion.

Teeth Whitening Market Segmentation

By Product:

- Whitening Toothpaste (55.4% share in 2024): Affordable, accessible, and suitable for daily use.

- Whitening Gels & Strips: Offer faster and more visible whitening effects due to higher concentrations of peroxide.

- Light-Based Whitening Devices: Gaining traction for professional-grade results at home.

By Distribution Channel:

- Supermarkets/Hypermarkets: Widely accessible and convenient for bulk purchases.

- Pharmacy Stores: Expected to dominate due to expert-backed product recommendations.

- Online Retail: Rapidly growing with rising e-commerce adoption and influencer-driven promotions.

Read Full Summary of Teeth Whitening Market: https://www.fortunebusinessinsights.com/teeth-whitening-market-110349

Regional Analysis

- Asia Pacific (USD 2.88 billion in 2024): Leading region with strong demand influenced by Western beauty standards and government oral health initiatives.

- North America: High adoption of laser and LED whitening treatments; strong post-COVID growth in at-home kits.

- Europe: Developed dental infrastructure and high disposable incomes fuel cosmetic dentistry demand.

- South America & Middle East & Africa: Market supported by growing dental tourism and demand for affordable whitening products.

Key Industry Players

Major players are focusing on digital marketing campaigns, influencer collaborations, and product innovations to expand consumer reach. For instance, Superdrug Stores plc in the U.K. launched the Healthy Smile Campaign with a 20% price reduction on ProCare products to boost adoption.

Leading Companies:

- Colgate-Palmolive Company (U.S.)

- Glaxo Smithkline (U.K)

- The Procter & Gamble Company (U.S.)

- Johnson & Johnson Consumer Inc. (U.S.)

- Philips Oral Healthcare, Inc. (U.S.)

- Henry Schein, Inc. (U.S.)

- Unilever (U.K.)

- KöR Whitening (U.S.)

- Opalescence (U.S.)

- Beyond Dental & Health (U.S.)

- Supersmile (U.S.)

- WhiteWash Laboratories (U.K.)

- Dentsply Sirona (U.S.)

- Beaming White (U.S.)

- Dabur (India)

Key Industry Developments:

- January 2024 – Whites Beaconsfield, a U.K.-based provider of oral care products, launched its innovative whitening toothpaste to cater to the demand of customers with veneers.

- April 2024 – Spotlight Oral Care, a U.K.-based oral care company, introduced ‘Ultra Tooth Whitening Strips,’ made with active ingredients and clinically proven to whiten teeth without any type of sensitivity.

The global teeth whitening market is set for strong growth, driven by cosmetic dentistry adoption, oral hygiene awareness, and advanced whitening technologies. With Asia Pacific at the forefront and North America leading in innovation, the industry is poised to expand significantly through 2032.

According to Fortune Business Insights , the global cricket bat market size was valued at USD 200.96 million in 2024 and is projected to grow to USD 346.20 million by 2032, registering a robust CAGR of 7.13% during the forecast period. This market growth is fueled by the rising global popularity of cricket, increasing demand for premium-quality equipment, and the strong expansion of professional and amateur cricket leagues worldwide. In 2024, Asia Pacific dominated the market with a 35.1% market share, supported by a rapidly growing player base, thriving local manufacturing hubs, and the sport’s massive following in cricket-loving nations such as India, Pakistan, and Australia.

Request FREE Sample Copy of Cricket Bat Market Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/cricket-bat-market-113141

Market Trends

Design Innovation & Sustainability

The market is witnessing a shift towards eco-friendly, recycled materials and advanced design features. Lightweight designs, better grip, and customizable features attract the younger generation and align with modern performance expectations.

Key Players

- Kookaburra Sport Pty Ltd (Australia)

- Grays International (U.K.)

- Sommers (Australia)

- KIPPAX WILLOW LIMITED COMPANY (U.K.)

- Bradbury (Australia)

- Blue Tongue Sports (Australia)

- Adidas AG (Germany)

- Stag Cricket (U.K.)

- Salix Cricket Bat Co. Ltd. (U.K.)

- Sareen Sports Industries (India)

Market Dynamics

Market Drivers

- Rise of Domestic & International Cricket Leagues:

The global expansion of cricket leagues such as the Indian Premier League (IPL), Big Bash League (BBL), and The Hundred is boosting the demand for high-quality bats. The emergence of Major League Cricket in the USA further diversifies the consumer base.

- Increased Investment in Sports Gear:

Consumers are investing more in customized, high-performance cricket equipment, with online platforms making these products more accessible. The influence of professional endorsements and player-specific bat models further drives premium bat sales.

- Grassroots Participation Growth:

With growing cricket academies, school tournaments, and recreational play, demand is surging across both professional and amateur segments.

Market Restraints

- High Cost of Premium Raw Materials:

English willow bats, known for their superior performance, are expensive due to limited availability and rising logistics costs. Kashmir willow alternatives do not always meet professional performance standards, limiting their adoption.

Market Opportunities

Smart Cricket Bats with Sensor Technology:

Tech-integrated cricket bats that track swing speed, impact force, and bat angle present a major opportunity. These innovations, coupled with partnerships with academies and leagues, can enhance training outcomes and appeal to tech-savvy athletes.

Segmentation Analysis

By Type

- Wooden Bats (English & Kashmir Willow) dominate due to their performance and historical preference.

- EVA Bats are gaining popularity for being lightweight, durable, and cost-effective, especially among beginners.

By End-user

- Professional Players account for the highest revenue share due to demand for high-performance bats.

- Amateur Players seek mid-to-premium range bats offering value and durability.

- Recreational Players prefer budget-friendly options for casual play.

By Price Range

- Mid-Range Bats led the market in 2024, appealing to a broad customer base.

- Premium Bats are expected to grow fastest due to rising disposable income and preference for branded, endorsed equipment.

- Budget Bats cater to beginners and recreational players in emerging markets.

Regional Insights

Asia Pacific

Leading the global cricket bat market, the region benefits from:

- Strong cricket culture and grassroots support

- Local manufacturing dominance (India produces 80% of protective gear globally)

- Export networks to over 40 countries, including Europe and the Middle East

North America

Rapidly growing due to:

- Technological innovation in bat manufacturing

- Expanding cricket fan base and league formation (e.g., USA’s Major League Cricket)

- Online sales channels and top-tier brand penetration

Europe

Europe, especially Germany and the U.K., is showing promising growth. Germany has expanded from 30 to over 400 cricket teams since 1988. Female participation and youth programs are also on the rise.

South America & Middle East & Africa

Growth is fueled by:

- Increased women’s cricket in Brazil

- Expansion of domestic tournaments and youth development programs

Read More Info: https://www.fortunebusinessinsights.com/cricket-bat-market-113141

Competitive Landscape

Continuous Development and Innovation resulted in the Dominating Position of the Key Players in the Market

The global cricket bat industry is concentrated with key players such as Adidas AG, Kookaburra Sport Pty Ltd, Grays International, Bradbury, and KIPPAX WILLOW LIMITED COMPANY, which account for a significant market share.

Strategic Developments

- June 2024: Kookaburra Sport Pty Ltd, a Melbourne based sports equipment and apparel company, launched 2024/25 cricket gear range, a collection that is set to transform the cricketing world. This collection includes variety of cricket bats

- April 2024: GR8 Sports India Pvt Ltd, a producer of Kashmir Willow cricket bats, launched a bat made of Kashmir willow for Women’s International Cricket.

- October 2023: Gray Nicolls, the well-known cricket brand and a manufacturer of rackets and cricket bats, unveiled a brand new cricket range for season 2022/23, which includes a couple of modern-day classics: the Predator and a modern twist of the bat.

The cricket bat market is set for steady growth through 2025 to 2032, backed by increasing cricket adoption across demographics, tech-integrated products, and rising sports investment globally. Companies focusing on sustainability, innovation, and partnerships are well-positioned to dominate this evolving landscape.

According to Fortune Business Insights , the global mobile gaming market , valued at USD 106.53 billion in 2024, is set to reach USD 232.58 billion by 2032, registering a CAGR of 9.78% between 2025 and 2032. The surge in smartphone adoption, coupled with the rollout of 5G networks, has transformed mobile gaming into one of the most profitable segments of the entertainment industry. Advanced technologies such as augmented reality (AR) and virtual reality (VR) are enhancing gameplay experiences, while the booming e-sports sector continues to attract both players and spectators worldwide.

In 2024, Asia Pacific dominated the market with a 47.04% market share, fueled by its vast youth demographic, high mobile penetration, and a thriving esports ecosystem. Countries like China, Japan, and South Korea remain key hubs for innovation and consumer spending in mobile gaming. This regional strength, combined with ongoing technological advancements and evolving consumer preferences, is expected to keep the sector on a high-growth trajectory over the coming years.

Request FREE Sample Copy of Mobile Gaming Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/mobile-gaming-market-113099

List of Key Mobile Gaming Companies Profiled:

- Electronic Arts (U.S.)

- Nintendo Co., Ltd. (Japan)

- NetEase, Inc. (China)

- Gameloft SE (France)

- Tencent (China)

- Microsoft Corporation (U.S.)

- Niantic, Inc. (U.S.)

- Supercell Oy (Finland)

- Zynga Inc. (U.S.)

- Epic Games (U.S.)

MARKET DYNAMICS

Market Drivers

- Proliferation of Smartphones and 5G Connectivity

The global spread of affordable smartphones has expanded access to mobile games, especially in emerging markets. Coupled with the global rollout of 5G, which enables faster and more stable gameplay, this has significantly improved user experience. According to 5G Americas, global 5G connections reached 2 billion in Q1 2024, projected to rise to 7.7 billion by 2028, ensuring a strong infrastructure foundation for the mobile gaming boom. - Rise of E-Sports and Competitive Gaming

The gamification of competitive events has elevated mobile gaming into a spectator sport. Game developers such as Electronic Arts, Nintendo, NetEase, and Gameloft SE are sponsoring high-profile tournaments, integrating advanced tech such as AR/VR for more immersive and social gaming experiences.

Market Restraints

- Growing Data Privacy Concerns

Increasingly stringent regulations, such as the Digital Markets Act, are compelling developers to balance monetization with user privacy. Failure to do so can reduce ARPU, hinder innovation, and affect user retention as players grow more cautious of privacy breaches.

Market Opportunities

- AR, VR, and AI Innovations

Emerging technologies are opening new avenues in mobile gaming. AR/VR features offer immersive gameplay, while AI personalizes user experiences, increasing engagement and retention. For instance, Nextech3D.ai introduced AR-based games in 2023 to boost event engagement—a model with widespread applicability across verticals.

SEGMENT ANALYSIS

By Game Type

- Shooter games lead the market, driven by multiplayer features and strong community engagement, making them central to esports events.

- Others (casual games like Candy Crush) are growing at the fastest rate due to their accessibility and wide demographic appeal.

By Platform

- Android dominates due to affordability and broader user base, especially in developing regions.

- iOS, while smaller in volume, records higher user spending, making it the fastest-growing platform.

By Business Model

- In-app purchases are the leading revenue model, offering a steady stream through virtual items and subscriptions.

- Paid games, though a smaller share, are gaining traction due to demand for premium, ad-free content.

By End-user

- Male users currently dominate due to the competitive nature of mobile gaming.

- Female gamers are the fastest-growing segment, driven by casual and puzzle game formats and increasing gaming frequency.

REGIONAL INSIGHTS

Asia Pacific – USD 50.11 Billion in 2024

The region’s youth-heavy demographics, growing digital infrastructure, and widespread smartphone adoption make it the largest and fastest-expanding market. India’s 808 million youth and China’s mobile-first population are key growth engines.

North America

Home to leading developers like Activision Blizzard and Electronic Arts, the region benefits from technological innovation and a robust esports ecosystem. The expansion of platforms like MPL into the U.S. market further drives growth.

Europe

Europe's expanding esports culture and adoption of AR/VR have boosted engagement. Events such as Games.com Cologne and moves like OG Esports’ 2025 mobile expansion enhance the region’s competitive presence.

South America & Middle East & Africa

Growth is fueled by improving digital infrastructure and local developer ecosystems. Countries like Brazil and Argentina are investing in broadband and game development, while UAE and Saudi Arabia lead in 5G rollout and youth engagement in gaming.

To get to know more about mobile gaming market; please visit: https://www.fortunebusinessinsights.com/mobile-gaming-market-113099

COMPETITIVE LANDSCAPE

The mobile gaming industry is highly fragmented yet fiercely competitive. Companies are actively diversifying genres and monetization models to attract various gamer demographics and sustain revenue streams. Notable moves include LinkedIn’s 2024 launch of puzzle games—an unconventional but strategic push to boost engagement through casual gaming among professionals.

Leading players such as Tencent, NetEase, Activision Blizzard, Zynga, Nintendo, and Supercell continue to dominate by blending immersive storytelling, high-quality graphics, and monetization through in-app purchases and subscriptions. These companies are leveraging user data, AI, and social connectivity to retain players and extend lifetime value.

KEY INDUSTRY DEVELOPMENTS

- November 2024 - Words with Friends, an online gaming platform, introduced a new suite of game modes to enhance player engagement and provide more diverse gameplay options. These new modes cater to both solo players and competitive participants, offering a range of puzzle-based challenges.

- May 2024 – NetEase, Inc., a Chinese internet and online game services provider, unveiled an exciting lineup of over 40 game franchises and products during its annual product launch event. The event highlighted new game plans and content updates for titles such as Where Winds Meet, NARAKA: BLADEPOINT Mobile, Once Human, Ashfall, and Lost Light.

The global mobile gaming market is in the midst of a transformation, driven by technological innovation, changing consumer behaviors, and competitive dynamics. As 5G expands and AR/VR technologies mature, the market will continue to diversify in terms of users, platforms, and monetization strategies. With Asia Pacific at the forefront and untapped potential in Latin America and the Middle East, mobile gaming is poised for long-term, global growth.

According to Fortune Business Insights , the global movie theater market size valued at USD 62.86 billion in 2024, is expected to rise to USD 68.37 billion in 2025 and reach USD 95.66 billion by 2032, registering a CAGR of 4.92%. North America dominated the market in 2024 with a 33.33% market share, supported by advanced cinema infrastructure and strong demand for premium viewing experiences.

Movie theaters continue to hold a pivotal role in the entertainment industry, fueled by blockbuster releases, cutting-edge audiovisual technologies, and the growing appeal of immersive, social viewing. To counter competition from streaming services, theaters are elevating the customer experience through luxury seating, gourmet dining, and advanced formats such as IMAX and 4DX.

Request FREE Sample Copy of Movie Theater Market Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/movie-theater-market-113097

Key Market Trends

- Premiumization and Diversified Offerings

To differentiate from home entertainment, theaters are leaning into luxury formats, dine-in services, and themed screenings. The shift toward event-based cinema, including concerts and e-sports, reflects evolving consumer expectations.

- Pandemic Impact and Post-Recovery Initiatives

COVID-19 drastically reduced in-person attendance, accelerating a shift to streaming. However, post-pandemic recovery efforts have seen a rise in event cinema , safety-focused venue enhancements, and hybrid releases that combine streaming with theatrical runs.

Competitive Landscape

Key market players are focusing on loyalty programs , social media marketing , cross-promotions , and tech innovation to engage consumers. Major companies include:

- AMC Entertainment Holdings Inc. (U.S.)

- Cineworld Group Plc (U.K.)

- Cinemark Holdings, Inc (U.S.)

- IMAX Corporation (Canada)

- Regal Cinemas (U.S.)

- PVR INOX (India)

- Wanda Cinema (China)

- CJ CGV (South Korea)

- Cineplex Inc. (Canada)

- Vue International (U.K.)

Market Dynamics

Market Drivers

- Rising Demand for Immersive Cinema Experiences

Consumers are increasingly drawn to premium formats such as IMAX , Dolby Atmos , and 4DX , which offer large-format screens, surround sound, and motion-enhanced seating. These features offer a cinematic experience that is difficult to replicate at home, making them a primary driver for theater attendance—especially during major film releases and franchise premieres.

- Diverse Content and Regional Localization

The inclusion of regional films, international releases, and niche genres has expanded theater audiences. Cinemas are increasingly programming local-language films and special events like concerts and sports broadcasts, attracting a wider demographic and supporting consistent footfall across markets.

Market Restraints

- Rising Competition from Streaming Services

Streaming giants like Netflix , Disney+ , and Amazon Prime Video offer affordable, on-demand entertainment, significantly affecting theater attendance. With exclusive content and the convenience of home viewing, these platforms continue to challenge the traditional movie theater business model.

Market Opportunities

- Advanced Audiovisual Technology and Luxury Amenities

The future of cinema lies in premiumization . The adoption of advanced projection systems, immersive soundscapes, recliner seating, and gourmet concessions is redefining the movie-going experience. 3D , panoramic screens , and AR/VR integrations are drawing tech-savvy audiences back into theaters.

- Urban Expansion and Experiential Entertainment

Emerging markets, especially in Asia Pacific and South America , are witnessing rising urbanization and disposable incomes, creating untapped opportunities for theater chains. Integration of non-traditional content such as gaming , live sports , and concert films is enhancing consumer engagement.

Market Challenges

- Operational Costs and Infrastructure Investments

Running a modern movie theater involves substantial costs—from real estate and utilities to staffing and equipment upgrades. Meeting evolving audience expectations while keeping ticket prices reasonable poses a significant challenge for profitability.

Segmentation Analysis

By Theater Type

- Multiplexes dominate the market with a 72.94% share in 2024 , providing multiple screens, convenience, and diverse offerings under one roof.

- IMAX is projected to grow at the fastest CAGR , thanks to its superior storytelling capabilities, premium image and sound technology, and expanding global footprint.

By Screen Format

- 2D screens remain dominant due to affordability and wide availability across genres and locations.

- 3D screens are expected to grow rapidly, driven by immersive viewing preferences for animated and action-packed films.

- 4DX is gaining niche popularity for delivering sensory experiences beyond visual and auditory engagement.

Regional Insights

North America (USD 20.95 Billion in 2024)

Despite rising streaming competition, North America remains a stronghold for cinema, with high demand for premium formats and franchise blockbusters. The rise of concert films like Taylor Swift’s Eras Tour, shown in collaboration with AMC, marks a growing trend in event-based cinema.

Europe

With a mature movie market, Europe is witnessing growth in arthouse cinemas, localized content, and technology upgrades. Nations such as the U.K., Germany, and France dominate the region’s box office landscape.

Asia Pacific

Expected to grow at the fastest CAGR, the region benefits from a large population, growing middle class, and expanding entertainment infrastructure. Countries like India, China, and South Korea are witnessing rapid growth in urban multiplex chains and technology-forward theaters.

South America & Middle East & Africa

These regions show promising potential, led by strong cultural ties to cinema in Brazil and Argentina, and luxury theater investments in GCC countries. Africa, while nascent, is growing through domestic industries like Nollywood.

Read More Info: https://www.fortunebusinessinsights.com/movie-theater-market-113097

Recent Strategic Developments

- June 2024: Wanda Film, China's largest exhibitor, and IMAX Corporation collaborated to form a strategic partnership agreement spanning content and technology. Under this partnership, Wanda Film is all set to upgrade 61 of its top-performing locations to state-of-the-art IMAX with Laser technology. Moreover, Wanda Film is also renewing up to 37 of its existing IMAX locations for another five years.

- May 2024: IMAX Corporation and French exhibition company MEGARAMA announced an agreement for three new state-of-the-art IMAX with laser system installations across France. Under this deal, one system will be added in the main urban area north of France, set to open in 2025 and two other locations in the suburbs of the country scheduled to open in 2026.

The global movie theater market is undergoing a renaissance fueled by consumer demand for memorable, immersive experiences. While challenges such as streaming competition and operational costs persist, the industry's pivot toward premiumization, regional content diversification, and technological innovation is expected to sustain long-term growth. Emerging markets, strategic partnerships, and experiential content will be key to unlocking the full potential of this dynamic sector.

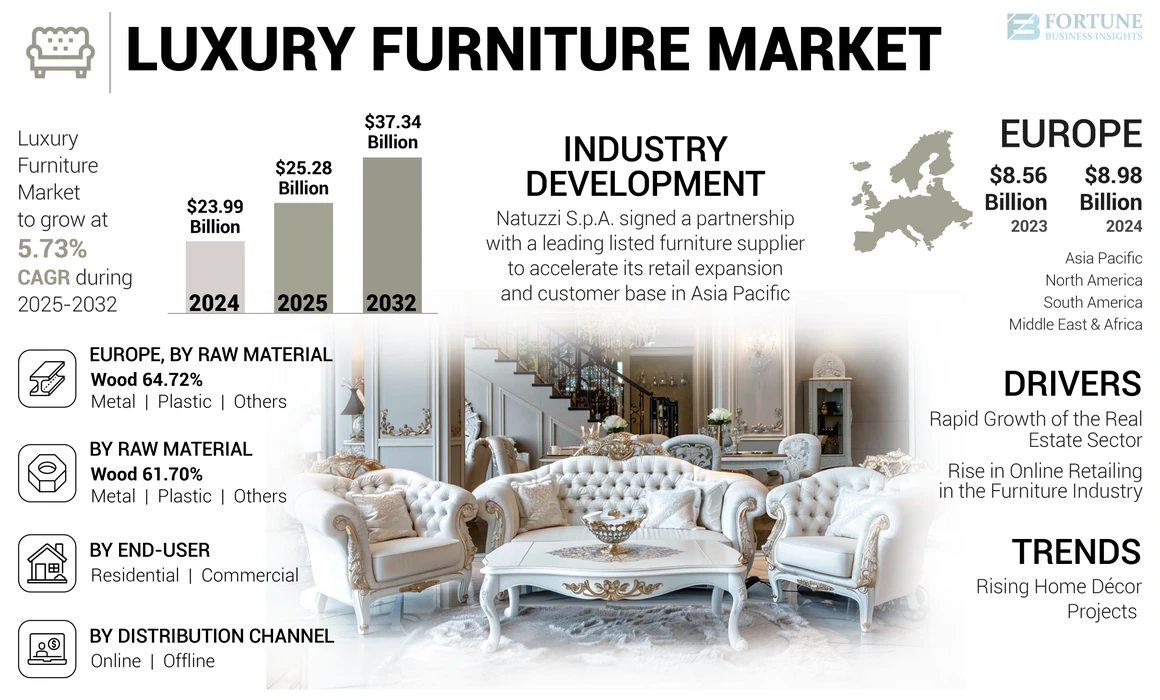

According to Fortune Business Insights , the global luxury furniture market size was valued at USD 23.99 billion in 2024 and is expected to reach USD 25.28 billion in 2025. It is projected to grow significantly, hitting USD 37.34 billion by 2032, at a compound annual growth rate (CAGR) of 5.73% during the forecast period. In 2024, Europe led the luxury furniture market, accounting for a dominant 37.43% market share.

The industry outlook is being positively influenced by growing consumer spending and various other factors such as household debt levels, per-capita income, and consumer expectations. Other aspects, such as ever-increasing disposable income, improvement in sliving standards, growing demand for furniture, and robust popularity of home renovation and decoration projects, will also fuel the market growth.

Request FREE Sample PDF Copy of Luxury Furniture Market Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/luxury-furniture-market-107326

PROMINENT COMPANIES PROFILED IN THE REPORT

- SCAVOLINI S.P.A. (Italy)

- Cassina S.p.A (Italy)

- Kimball International, Inc. (U.S.)

- Brown Jordan International (U.S.)

- Herman Miller, Inc. (Knoll Inc) (U.S.)

- Vivono (India)

- Boca do Lobo (U.K.)

- DURESTA (U.K.)

- Haworth, Inc. (Italy)

- MUEBLES PICO SA (Spain)

Market Trend

The luxury furniture market is experiencing robust growth, driven by rising demand for aesthetically appealing and eco-friendly décor solutions across homes, offices, hotels , and restaurants. Urbanization, growing disposable incomes, and heightened awareness of global design trends—especially in developing economies—are encouraging consumers to invest in premium furniture. Leading players such as Kimball International, Herman Miller (Knoll Inc), DURESTA, and Cassina S.p.A. are responding to evolving consumer preferences, particularly among younger buyers, by innovating in design, materials, and functionality. The rising popularity of multifunctional furniture, coupled with aggressive social media marketing on platforms like Instagram, Facebook, and YouTube, is further expanding market reach and fueling industry expansion.

Segments

Aesthetic Design and High Durability Offered by Wooden Furniture to Support Market Expansion

Based on raw material, the market is divided into wood, metal, plastic, and others. The wood segment is expected to hold a dominant market share, owing to its adaptability and high-quality finishing. Wood is the most popular material due to its high aesthetic value and durability. These features will boost the sales of luxurious wooden furniture.

Rise in Home Décor Projects to Fuel Market Growth

Based on end-user, the market is divided into residential and commercial. The residential segment is predicted to hold a significant market share owing to the large-scale manufacturing of home décor and furnishing products.

Growing Demand for Personalized Shopping Experience to Boost Sales of Offline Distribution Channels

In terms of distribution channel, the market is divided into online and offline. The offline segment is predicted to capture a sizeable industry share as it offers customers a personalized experience and allows them to check a product’s quality through physical inspection.

Report Coverage:

The research report analyzes the industry in detail and highlights several crucial aspects such as prominent companies, competitive landscape, raw materials, end users, and distribution channels. Apart from this, the report also offers insights into the industry trends and underlines many important developments in the market.

Drivers and Restraints:

Rapid Growth of Real Estate Sector to Contribute to the Luxury Furniture Industry Growth

The real estate sector has recently shown substantial expansion due to increased demand for office and residential spaces. The growing construction of residential and commercial buildings will drive the market progress.

The wide availability of counterfeit products might hinder the market development. Counterfeiting also involves placing the logo or trademark of a famous brand on a product, but the product is not manufactured or authorized by that brand.

Regional Insights:

In terms of region, the market is studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa (MEA). The Europe region is anticipated to capture a sizeable luxury furniture market share during the forecast period as many companies across the region are involved in in-depth research & development. They are also constantly upgrading technologies used in the production of luxury furniture, thereby spurring the product sales across the region.

The North America region is also predicted to hold a major market share as there is a notable presence of reputed luxury furniture manufacturers. Also, the construction of residential and commercial buildings will spur the adoption of luxurious furnishing products.

To get to know more about this market, please visit: https://www.fortunebusinessinsights.com/luxury-furniture-market-107326

Competitive Landscape:

Acquisitions and Partnerships by Leading Companies to Boost Market Growth

Reputed organizations, such as Scavolini S.P.A., Cassina S.p.A., Kimball International, Inc., Brown Jordan International, and many others, are developing a wide range of growth strategies to fortify their presence in the global market. For example, in October 2022, Linly Designs acquired Marge Carson, a luxury furniture brand, which manufactures high-end residential furniture. The deal is expected to enhance operational efficiencies and product offerings.

Key Industry Development:

- In December 2022 , Kogan.com took over the management of Brosa, one of Australia's largest online retailers of luxury furniture. The deal is anticipated to revive the operations of the popular furniture brand, with the support of the Kogan Group.

- In October 2022 , Linly Designs acquired the luxury furniture brand Marge Carson, which manufactures high-end residential furniture. The acquisition is expected to enhance operational efficiencies and product offerings.

Global Knitwear Market: Size, Share, Scope, and Future Forecast 2025–2032

By Market News, 2025-07-30

According to Fortune Business Insights , the global knitwear market is undergoing a significant transformation, driven by evolving fashion trends, sustainability innovations, and rising demand for comfort-centric apparel. Knitwear refers to garments made from wool, cotton, or synthetic yarns, intricately knitted to create flexible, breathable fabrics. These are widely used in outerwear, innerwear, athletic wear, and seasonal clothing. The rise in demand for stylish, functional clothing and innovations in textile production have elevated knitwear from basic apparel to a fashion staple for men, women, and children globally.

The market is also witnessing a surge in the adoption of eco-friendly materials such as organic cotton, recycled fibbers’, and low-impact dyes, aligning with the global shift toward sustainable fashion. For instance, in September 2023, Scotland-based Woolkind launched a made-to-order scarf collection featuring sustainable materials and personalized designs—indicating a consumer shift toward conscious and customized knitwear products.

Request FREE Sample Copy of Knitwear Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/knitwear-market-109875

Key Players Covered

- Adidas AG

- Puma SE

- Ralph Lauren

- Victoria’s Secret

- Gildan Activewear

- Loro Piana S.p.A.

- The Nautical Company Ltd.

- The Gap, Inc.

- Ecowool

IMPACT OF COVID-19 ON THE KNITWEAR MARKET

The COVID-19 pandemic disrupted global apparel supply chains and significantly affected knitwear production and retail. Lockdowns and logistical challenges resulted in inventory shortages and reduced consumer spending. According to Mastercard SpendingPulse, clothing and accessory sales dropped by 15% in August 2021 and 25% in August 2020 year-over-year. However, the pandemic also triggered a shift toward casual, comfortable clothing—boosting demand for knit loungewear, athleisure, and homewear. This trend led to a revival in the knitwear sector post-pandemic, as brands adapted their offerings to meet evolving consumer preferences.

MARKET SEGMENTATION

By Material Type

- Natural Fibers (Cotton, Wool)

- Synthetic Fibers

- Blended Materials

- Others

The natural material segment dominates due to its comfort, breathability, and environmental benefits. Wool and cotton are particularly popular for their softness and adaptability across seasons.

By Application

- Outerwear

- Innerwear

Innerwear leads the segment owing to its essential role in daily use. Knit fabrics used in this category are valued for their stretchability, softness, and breathability. The blend of fashion and functionality in this segment ensures continued consumer interest.

By End-User

- Men

- Women

- Kids

The men’s segment holds the largest market share, driven by rising demand for casual clothing like sweaters, cardigans, and hoodies. The trend of casualization in workplaces and leisure settings has broadened the appeal of knitwear in men’s fashion.

By Distribution Channel

- Online

- Offline

The offline segment is expected to maintain a larger market share, as many consumers prefer the tactile experience of physically assessing knitwear fabrics before purchase. However, the online segment is gaining momentum due to convenience, broader selections, and ease of access.

Read Full Summary: https://www.fortunebusinessinsights.com/knitwear-market-109875

REGIONAL ANALYSIS

Asia Pacific

Asia Pacific dominates the knitwear market, supported by a strong manufacturing base in China, India, and Bangladesh. The region also benefits from rising consumer spending and increasing exposure to global fashion trends. According to UN Comtrade, ASEAN nations accounted for nearly 50% of global textile and apparel exports in 2022.

Europe

Europe is a key market with a strong inclination toward sustainable and premium knitwear. Countries such as Germany, France, and the U.K. are trendsetters in ethical fashion, supporting demand for organic and recycled materials.

North America

North America, particularly the U.S., is witnessing growing adoption of sustainable knitwear and high demand for athleisure and loungewear. The region also benefits from strong online retail infrastructure and brand-driven consumption.

South America and Middle East & Africa

These regions are emerging markets for knitwear, fueled by rising fashion awareness and urbanization. Countries like Brazil, UAE, and South Africa are investing in retail expansion and fashion infrastructure.

KEY INDUSTRY DEVELOPMENTS

- July 2023 : Tokyo-based YOKE launched winter garments using Brewed Protein fiber, emphasizing biodegradable innovation.

- February 2022 : Mr Porter released 36 knitwear items made from surplus yarns, recycled, and organic materials, reaffirming commitment to circular fashion.

The global knitwear market is positioned for strong growth, underpinned by sustainability trends, fashion innovation, and rising demand for comfort-focused apparel. As consumer awareness about eco-conscious products increases, and as fashion brands push the boundaries of design and material use, knitwear is evolving into a high-value category within the global apparel market.

Global Vacation Rentals Market: Size, Share, Scope, and Future Forecast 2025–2032

By Market News, 2025-07-30

According to Fortune Business Insights , the global vacation rentals market was valued at USD 174.84 billion in 2024 and is projected to reach USD 396.93 billion by 2032, expanding at a CAGR of 10.65% during 2025–2032. In 2025 alone, the market is expected to reach USD 195.45 billion. Growth is driven by the global rise in travel, changing consumer accommodation preferences, and the rise of digital platforms like Airbnb, Vrbo, Booking.com, and Tripadvisor.

Vacation rentals have become a preferred alternative to traditional hotels, offering travelers personalized, cost-effective, and flexible lodging. The rise of remote work and lifestyle travel further strengthens the demand for vacation homes, villas, and short-term rentals. With increasing user penetration and digital convenience, vacation rentals are quickly becoming mainstream for global travelers.

Request FREE Sample Copy of Vacation Rentals Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/vacation-rentals-market-113271

KEY MARKET TRENDS

- Experiential & Themed Stays on the Rise: Travelers increasingly seek accommodations that offer more than just a place to sleep. Properties that deliver unique experiences—such as heritage homes, nature retreats, and locally curated activities—are gaining traction.

- Luxury Rentals Surge Post-Pandemic: High-income travelers are gravitating toward private, amenity-rich spaces that offer exclusivity and wellness-focused experiences.

LIST OF KEY VACATION RENTALS COMPANIES PROFILED

- Airbnb (U.S.)

- Vrbo (U.S.)

- Booking.com (Netherlands)

- Tripadvisor (U.S.)

- TUI Group (Germany)

- Sonder Holdings Inc. (U.S.)

- Vacasa, Inc. (U.S.)

- Blueground (U.S.)

- Plum Guide (U.K.)

- OYO Vacation Homes (Switzerland)

MARKET DYNAMICS

Market Drivers

- Remote Work & Digital Nomadism: With more professionals working remotely, extended stays in vacation homes have surged, especially in scenic and culturally rich destinations.

- Tech-Driven Convenience: Platforms now offer dynamic pricing, digital check-ins, and property management tools, making vacation rentals more competitive with hotels.

- Traveler Preferences: Increasing demand for privacy, larger spaces, and immersive local experiences drive market momentum, particularly among millennial and Gen Z travelers.

Market Restraints

- Competition from Traditional Hotels: Hotels offer standardized services, loyalty programs, and central locations, which still appeal to many business and luxury travelers.

- Quality and Regulation Issues: Variation in property standards and inconsistent regulations across countries can hinder consumer trust and limit growth in certain markets.

Market Opportunities

- Government Tourism Campaigns: Initiatives promoting local tourism and supporting small property owners open up new opportunities, especially in emerging economies.

- Themed and Experiential Stays: Growth in demand for cultural, eco-friendly, and themed accommodations (treehouses, farm stays, etc.) provides differentiation and premium pricing options.

SEGMENTATION ANALYSIS

By Accommodation Type

- Home/Villa Rentals dominated the market in 2024, offering privacy, space, and affordability, especially for families and groups.

- Resorts/Condominiums are projected to grow at a CAGR of 11.32%, driven by demand for upscale amenities paired with home-like comfort.

By Booking Channel

- Online Booking platforms lead growth, with travelers preferring platforms like Airbnb and Vrbo for their convenience, global reach, and user-friendly interfaces.

- Offline Channels still contribute significantly, particularly among baby boomers and Gen X travelers booking via traditional travel agencies.

By Price Point

- Mid-Range Rentals were the most popular in 2024 due to their balance between affordability and comfort. This segment caters to budget-conscious families and middle-income travelers.

- Luxury Rentals are expected to grow fastest as affluent travelers seek premium, curated experiences with amenities like private pools, chefs, and concierge services.

REGIONAL OUTLOOK

Europe

- Dominated the global market with an 89.47% share in 2024.

- The region’s growth is supported by a preference for localized and authentic stays, especially among younger travelers embracing “bleisure” (business + leisure) travel.

- Countries like Germany, France, and the U.K. are key contributors.

North America

- The U.S. leads regional growth with high platform usage, digital integration, and a surge in work-from-anywhere culture.

- Tech-enabled property management and flexible stay models strengthen market performance.

Asia Pacific

- Expected to register the fastest CAGR from 2025–2032.

- Growth is fueled by rising disposable incomes, domestic travel trends, and increased adoption of digital booking in countries like India, China, and Southeast Asia.

- Coastal areas and nature-centric destinations are driving up revenue during peak travel seasons.

South America and Middle East & Africa

- Emerging growth regions benefiting from cultural tourism, eco-tourism, and increasing government investment in travel infrastructure.

- Countries like Brazil and South Africa are attracting tourists through unique natural and cultural experiences, while UAE and Saudi Arabia support luxury vacation rental growth.

Read Full Summary of the Report: https://www.fortunebusinessinsights.com/vacation-rentals-market-113271

COMPETITIVE LANDSCAPE

Leading players such as Airbnb, Vrbo, Booking.com, and Tripadvisor dominate the vacation rentals market. Key strategies include:

- Strengthening brand visibility through SEO, social media, and influencer marketing.

- Partnering with local hosts and businesses to enhance guest experiences.

- Offering curated, themed stays to stand out in a competitive landscape.

- Launching proprietary platforms (e.g., Hyatt’s Homes & Hideaways) to reduce reliance on third-party sites and control guest experience.

KEY INDUSTRY DEVELOPMENTS

- December 2024: Casago, a premier holiday rental property management company, announced that it entered into a definitive agreement with Vacasa, Inc., a leading rental vacation home management platform in North America. Both companies strive to offer unmatched rental vacation property management platforms by offering best-in-class home care and revenue for homeowners and providing superior hospitality for guests.

- September 2024: co, the leading platform for curated luxury holiday rental homes, acquired Experientials, a pioneer in brand activation and product integration. This acquisition aims at revolutionizing customer experience, blending premium products with high-end properties from the leading brands across the globe to create unique stays.

The global vacation rentals market is undergoing rapid transformation, driven by changing traveler behavior, technology advancements, and growing demand for authentic and flexible accommodation experiences. With remote work becoming a norm and travelers seeking more personalized options, vacation rentals are positioned to rival traditional hotel offerings, offering immense growth potential across both mature and emerging markets.

Global Smart Faucets Market: Size, Share, Scope, and Future Forecast 2025–2032

By Market News, 2025-07-30

According to Fortune Business Insights , the global smart faucets market size was valued at USD 2.32 billion in 2024 and is projected to reach USD 3.67 billion by 2032, expanding at a CAGR of 5.97% during the forecast period (2025–2032). In 2025, the market is expected to register USD 2.44 billion in value. North America dominated the market in 2024 with an overwhelming 95.4% market share, driven by high smart home adoption and robust integration of IoT-enabled technologies.

Smart faucets, equipped with motion sensors, infrared detection, and smart connectivity (via Wi-Fi, Bluetooth, or voice assistants like Alexa and Google Assistant), are increasingly being used across residential and commercial applications. These advanced fixtures promote water conservation, offer hygienic benefits, and support growing sustainability goals. Key manufacturers such as Kohler Co., Lixil Group, Moen Incorporated, Delta Faucet Company, and Hansgrohe SE are leading innovation in this space, focusing on features such as touchless operation, custom temperature control, and voice activation.

Request FREE Sample Copy of Smart Faucets Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/smart-faucets-market-113432

SMART FAUCETS MARKET TRENDS

Rising Focus on Eco-Friendly and Water-Saving Innovations Driving Market Evolution

A key trend shaping the smart faucets market is the increasing emphasis on sustainability and advanced water conservation technologies. Manufacturers are introducing smart faucets equipped with features such as real-time water usage monitoring, adjustable flow rates, and automatic shutoff systems to significantly reduce water wastage. These eco-conscious innovations appeal to a growing segment of environmentally aware consumers and align with tightening global regulations on water conservation. As demand for green, energy-efficient home solutions rises, smart faucets are emerging as a preferred choice—combining intelligent functionality with environmental responsibility in modern residential and commercial spaces.

MARKET SEGMENTATION

By Type

- Touchless Faucets held the largest market share in 2024 due to post-pandemic hygiene concerns and growing adoption in bathrooms and kitchens.

- Touch-Activated Faucets are projected to grow at the fastest CAGR, appealing to tech-savvy consumers for their ease-of-use and contemporary design.

- Voice-Activated Faucets are gaining popularity as integration with smart home assistants becomes more mainstream.

By Application

- Bathroom Faucets led in 2024, fueled by the need for hands-free hygiene and consistent temperature control.

- Kitchen Faucets are forecasted to grow fastest during 2025–2032, as they reduce cross-contamination during food preparation and offer added convenience in high-usage areas.

By End-User

- Residential Segment dominated in 2024, driven by rising smart home trends and consumer preference for modern, hygienic living spaces.

- Commercial Segment is anticipated to grow rapidly, supported by rising demand in hospitality, healthcare, and office sectors for water-saving and touchless features.

By Distribution Channel

- Retail Outlets/Offline led the market in 2024 due to the advantage of live product demonstrations and in-person customer support.

- E-commerce/Online segment is expected to witness the highest CAGR, driven by digital convenience, broader product selections, and the influence of online reviews and social media marketing.

REGIONAL INSIGHTS

North America

- Accounted for USD 0.87 billion in 2024.

- Dominated the global market due to widespread adoption of smart homes, tech-savvy consumers, and commercial deployment in hospitals and corporate spaces.

- The U.S. remains the largest contributor, fueled by strong commercial infrastructure and high IoT integration.

Europe

- Ranked second in market share and is projected to grow steadily due to urban property upgrades, strong sustainability mandates, and rising consumer interest in premium smart fixtures.

- Countries like Germany and the U.K. show high demand due to disposable income and eco-conscious behavior.

Asia Pacific

- Forecasted to register the fastest CAGR from 2025 to 2032, led by rapid urbanization and infrastructure projects in India, China, and Southeast Asia.

- Rising middle-class population, increasing living standards, and water conservation policies are key growth factors.

South America and Middle East & Africa

- Projected to grow significantly, driven by water scarcity concerns and luxury property developments.

- UAE, Israel, and Saudi Arabia are major adopters due to severe water stress and growing tourism infrastructure.

MARKET DYNAMICS

Drivers

- Surging Hygiene Awareness Post-COVID-19: Contactless faucets reduce cross-contamination risks and are increasingly favored in homes, restaurants, and public facilities.

- Integration with Smart Homes: Advanced features such as water usage tracking, temperature control, and voice commands support the growth of smart home ecosystems.

Restraints

- High Cost of Installation and Maintenance: Advanced sensors and smart tech raise upfront and long-term costs, deterring budget-conscious users.

- Complex Retrofitting in Commercial Settings: Integrating smart systems into existing infrastructures is expensive and often technically challenging.

Opportunities

- Growing Demand in Commercial & Hospitality Sectors: Touchless, water-efficient faucets appeal to hotels, malls, airports, and office spaces prioritizing hygiene and eco-friendly operations.

Challenges

- Cybersecurity & Data Privacy Risks: Connectivity to home networks raises concerns about hacking and unauthorized access, potentially impacting consumer trust.

Read Full Summary: https://www.fortunebusinessinsights.com/smart-faucets-market-113432

COMPETITIVE LANDSCAPE

The market is competitive with innovation as the primary differentiator. Leading players focus on:

- Collaborations with smart home ecosystems.

- Launching customizable and premium design products.

- Investing in sustainable R&D and expanding to emerging markets.

- Utilizing both digital and physical channels to boost brand visibility.

List of Key Smart Faucets Companies Profiled In the Report

- Kohler Co. (U.S.)

- Moen Incorporated (U.S.)

- LIXIL Group (Japan)

- Delta Faucet Company (U.S.)

- Hansgrohe SE (Germany)

- Roca Sanitario, S.A. (Spain)

- Jaquar Group (India)

- TOTO Ltd. (Japan)

- CERA Sanitaryware Ltd. (India)

- Pfister (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2024: Studio McGee and Kohler together created six collection of kitchen and bathroom outfitting, including faucets, vanities, and light fixtures for a wide range of interior design styles. The Edalyn Kitchen Faucet Collection features four kitchen faucet varieties and a wall-mounted pot filler. Another range, Castia Bathroom Faucet Collection, offers sleek yet aesthetic and classic bath fixtures in multiple finishes.

- May 2024: S.-based, Delta Faucet Company, announced the launch of Touch2O with Touchless Technology. The contactless technology makes multi-tasking even easier and mess-free by offering three ways to control the water flow: placing a hand near the faucet to activate the motion sensor, using the standard handle for manual control, or tapping anywhere on the faucet surface.

The global smart faucets market is poised for steady growth, driven by rising hygiene awareness, sustainability focus, and smart home integration. Although high costs and cybersecurity concerns present challenges, strong demand across residential and commercial sectors, especially in North America and Asia Pacific, presents lucrative opportunities for stakeholders.

According to Fortune Business Insights , the global tobacco products market is projected to grow steadily, from USD 1,058.20 billion in 2025 to USD 1,260.59 billion by 2032, exhibiting a CAGR of 2.53% during the forecast period. In 2024, the market was valued at USD 1,018.57 billion, with Asia Pacific leading the industry by holding 48.87% of the global share, fueled by high cigarette consumption and expanding retail presence in countries like China, India, and Southeast Asia.

List of Key Tobacco Product Companies Profiled

- Philip Morris Products S.A. (U.S.)

- Altria Group, Inc. (U.S.)

- British American Tobacco plc. (U.K.)

- Japan Tobacco Inc. (Japan)

- Imperial Brands plc. (U.K.)

- ITC Limited (India)

- PT Hanjaya Mandala Sampoerna Tbk (Indonesia)

- PT Perusahaan Rokok Tjap Gudang Garam Tbk (Indonesia)

- KT&G Corporation (South Korea)

- China National Tobacco Corporation (China)

Request FREE Sample PDF Copy of Tobacco Product Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/tobacco-products-market-112987

Opportunities and Trends

- - Rising Popularity of Flavored Tobacco Products

- The demand for flavored nicotine products continues to grow, particularly among young adults. From mint and chocolate to menthol and fruit-infused options, these products appeal to modern users seeking variety. Companies like Japan Tobacco Inc. have capitalized on this trend with products like the “with 2” device, utilizing infused vapor technology for a smooth smoking experience.

- - Digital Marketing and Social Media Campaigns

- The increasing use of platforms like TikTok, Instagram, and Facebook for brand promotions is enhancing consumer reach. For example, ZYN nicotine pouches by Philip Morris amassed over 700 million followers through targeted digital marketing campaigns.

Key Market Drivers

- Growing Disposable Income Among Women

The rising disposable income and changing cultural norms among women, particularly in developed regions like the U.K. and U.S., are contributing to the market expansion. A report by Cancer Research U.K. showed a notable increase in smoking rates among women aged 18–45, which climbed from 12% to 15% between 2013 and 2023. This demographic shift, alongside growing autonomy and lifestyle changes, has significantly impacted product demand.

- Increased Usage of Nicotine Products Among Youth

The exposure of young consumers to nicotine product advertising—especially via social media and influencers—has accelerated demand. In the U.S., nearly 24.8% of 12th-grade students used nicotine products in 2022, reflecting a broader trend of increased adoption of vaping, nicotine pouches, and heated tobacco.

- Product Innovation and Next-Generation Products (NGPs)

Tobacco companies are heavily investing in reduced-risk products such as e-cigarettes, heated tobacco, and nicotine pouches. These items offer customizable flavors and safer alternatives to traditional cigarettes. For example, Philip Morris International launched "BONDS by IQOS," a heat-not-burn device that aligns with the global shift toward smoke-free alternatives.

Market Restraints

Despite the growth, strict government regulations are impeding market potential. Countries like India, Brazil, and Egypt have imposed bans on e-cigarette sales, limiting market access and stifling innovation in certain regions. Additionally, increasing health concerns around nicotine addiction, coupled with higher taxes and advertising restrictions, pose serious challenges to global market players.

Segment Analysis

- By Product Type

The market is segmented into traditional tobacco products and next-generation products (NGPs).

- Traditional Products: Cigarettes remain dominant due to their accessibility and strong consumer base. Cigar and roll-your-own (RYO) tobacco are also gaining traction, especially among middle and lower-income groups due to affordability.

- NGPs: The fastest-growing segment, including e-cigarettes, heated tobacco products, nicotine pouches, and snus. The heated tobacco segment is expected to witness the highest CAGR due to its positioning as a safer smoking alternative.

Regional Outlook

Asia Pacific

Asia Pacific remains the largest and fastest-growing region, driven by high smoking rates in China (over 291 million smokers) and rising consumer interest in flavored and slim e-cigarettes.

North America

Strong adoption of reduced-risk products in the U.S. and Canada is bolstering growth. Increasing female cigar and pipe tobacco use and youth e-cigarette adoption also support the upward trend.

Europe

The region is witnessing high growth in NGPs, with countries like the U.K., Sweden, and Switzerland leading the adoption of nicotine pouches and smokeless alternatives. Innovative launches, such as TACJA’s 30-minute nicotine pouch, are drawing consumer attention.

South America & Middle East & Africa

Market development here is shaped by regulatory changes, high taxes, and rising awareness of smoking hazards. Consumers are increasingly switching to heat-not-burn and herbal alternatives in countries like Brazil, Egypt, and South Africa.

Read More Info: https://www.fortunebusinessinsights.com/tobacco-products-market-112987

Competitive Landscape

The global tobacco products market is highly fragmented, with the top five companies accounting for only 13.60% of the total share.

These companies are focusing on R&D, flavored product launches, and emerging market penetration. For instance, PMI invested USD 800 million in a nicotine pouch factory in Colorado, and British American Tobacco launched a “Smokeless World” initiative to promote its Omni™ platform for tobacco harm reduction.

KEY INDUSTRY DEVELOPMENTS

- December 2024- Philip Morris International (PMI) announced the development of affordable next-generation products (NGPs) aimed at the African market. This initiative is driven by the recognition that the smoke-free market in Africa is still in its early stages, and there is a significant demand for cost-effective alternatives among price-sensitive consumers.

- September 2024- British American Tobacco (BAT) launched a significant global initiative aimed at creating a "Smokeless World." This initiative, unveiled during the company's first Transformation Forum in London, features the Omni™ platform, which serves as an evidence-based resource to facilitate discussions around Tobacco Harm Reduction (THR).

The global tobacco products market is undergoing a significant transformation, fueled by innovation, shifting consumer preferences, and changing demographics. While traditional products still dominate, next-generation tobacco alternatives are paving the way for future growth. Companies that adapt quickly to regulatory environments, invest in product development, and embrace digital marketing will be best positioned to lead in this evolving landscape.

According to Fortune Business Insights , the global furniture and home furnishing market is witnessing steady expansion, driven by increasing urbanization, rising consumer income, homeownership growth, and the rising appeal of aesthetic living spaces. Valued at USD 120.66 billion in 2024 , the market is expected to reach USD 130.79 billion in 2025 and climb to USD 191.40 billion by 2032 , growing at a CAGR of 5.59% during the forecast period.

Key Market Insights

Furniture includes movable items like beds, chairs, and tables used for seating, sleeping, and storage, while home furnishing comprises decorative and functional accessories that enhance the home’s ambiance. Growing investments in residential real estate, consumer interest in interior design, and increasing renovation activities are significantly driving global demand for these products.

In 2024, Asia Pacific held a dominant 91.6% market share , owing to rapid real estate development and expanding middle-class populations in India, China, and Southeast Asia.

Market Trends

- Work-from-Home Driving Demand for Functional Furniture : Remote work has fueled demand for multi-functional desks, chairs, and convertible furniture that blend with home décor while serving professional needs.

- Smart Furniture Adoption : Tech-integrated furniture featuring wireless charging, LED lighting, and smart home connectivity is gaining traction, especially in Europe and North America.

Request FREE Sample PDF Copy of Furniture and Home Furnishing Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/furniture-and-home-furnishing-market-113434

Competitive Landscape

Key players are enhancing their global footprint through collaborations, product innovation, and regional expansion. Partnerships with designers and global retail networks have allowed companies to strengthen brand equity and cater to evolving consumer demands.

LIST OF KEY FURNITURE AND HOME FURNISHING COMPANIES PROFILED

- Cassina S.p.A. (Italy)

- Kimball International, Inc. (U.S.)

- Nilkamal Furniture (India)

- BROWN JORDAN (U.S.)

- Steelcase (U.S.)

- Herman Miller, Inc. (Knoll Inc) (U.S.)

- Vivono Designs (India)

- American Signature, Inc. (U.S.)

- DURESTA (U.K.)

- Haworth, Inc. (Italy)

Market Dynamics

Drivers: Rising Consumer Spending on Home Décor

Consumers are spending more on home décor to enhance comfort, aesthetics, and personal expression. Factors such as growing disposable incomes, urban migration, and global design exposure (via social media and international brands) contribute significantly to this trend. Emerging markets like India, Vietnam, and Brazil are witnessing a rise in home remodeling and furniture purchases due to increased lifestyle aspirations.

Restraints: Volatile Raw Material Prices

Frequent fluctuations in raw material prices due to geopolitical instability, tariffs, and currency volatility pose a significant challenge. For example, the U.S. imposed a 125% tariff on Chinese imports in April 2025 , increasing manufacturing costs and limiting profit margins for furniture producers worldwide.

Opportunities: Surge in Eco-Friendly Furniture Demand

Sustainable living trends are creating lucrative opportunities. Consumers are increasingly opting for eco-friendly furniture made from bamboo, reclaimed wood, recycled metals, and organic fabrics . Manufacturers are responding by launching green product lines that combine design, durability, and sustainability.

Segmentation Analysis

By Product Type

- Living Room & Lounge Furniture dominates due to the growing preference for stylish, modular seating that enhances both comfort and interior appeal.

- Bedroom Furniture is anticipated to grow rapidly with increasing interest in smart beds and compact furniture optimized for urban homes.

By Material

- Wood leads in material preference due to its natural aesthetics and longevity.

- Metal furniture is growing in demand for its affordability, low maintenance, and increasing popularity in modern minimalist interiors.

By Distribution Channel

- Offline/Retail Outlets currently hold the largest share, favored for personalized service and product inspection.

- E-commerce is the fastest-growing segment, driven by rising internet access, ease of price comparison, and platforms like Amazon, Flipkart, and Wayfair offering convenient shopping experiences.

Regional Outlook

Asia Pacific (USD 56.41 Billion in 2024)

The region leads the market, supported by robust urban development, high property sales, and a growing preference for modern interiors. According to the India Brand Equity Foundation , India saw residential sales peak at USD 42 billion in FY 2023 , while Trade Promotion Council of India ranks it as the fourth-largest furniture consumer globally.

North America

North America is seeing increased investment in sustainable furniture. Home sales in the U.S. reached 6.12 million units in 2021 , and Canada saw a 3.7% increase in sales between Dec 2023 and Jan 2024. Manufacturers like Cabinetworks Group are expanding production facilities to meet rising demand for kitchen and home furniture.

Europe

Demand in Europe is fueled by urban growth, tech-savvy furniture buyers, and a shift towards compact, smart homes. Countries like Germany, the U.K., and France are driving demand for multi-functional and tech-enabled furniture with features like USB ports and voice control.

South America and Middle East & Africa

These regions are experiencing rapid growth, backed by digital marketing efforts and rising consumer interest in affordable and stylish home décor. Social platforms like TikTok and Instagram are helping brands influence buying behavior.

Read More Info: https://www.fortunebusinessinsights.com/furniture-and-home-furnishing-market-113434

Recent Developments:

- February 2025 - IKEA Systems B.V., a Netherlands-based manufacturer, announced opening eight new U.S. stores in 2025. The launch would help the company to enhance its customer reach and operation revenue.

- May 2024 - IKEA Systems B.V., a home furnishing retailer, partnered with Rhenus, a warehouse facility company, to build its online home furnishing products’ reach across Delhi NCR, India.

- May 2024 – Remax Furniture, an India-based manufacturer of home furniture products, introduced its flagship furniture store in New Delhi, India. The newly launched store would provide home furnishing and décor products to make home interiors more appealing and aesthetic.

The global furniture and home furnishing market is set for steady growth through 2032, driven by rising urban housing, eco-conscious consumers, and the boom in digital retail. With increasing demand for smart, modular, and sustainable furniture, key players are well-positioned to capture new opportunities through product innovation and global expansion.