Category: Business

According to Fortune Business Insights, the global magnetometer market was valued at USD 3.64 billion in 2024 and is projected to grow to USD 7.75 billion by 2032, exhibiting a CAGR of 10.2% during the forecast period.

The market is expected to reach USD 3.94 billion in 2025, driven by increasing adoption across industries such as aerospace, defense, automotive, and consumer electronics. North America dominated the market in 2024 with a 38.74% share, supported by strong defense investments and advancements in magnetic sensing technologies.

Magnetometers are critical tools used to measure magnetic fields and are widely deployed in navigation systems, geophysical exploration, space missions, and industrial applications. The rising demand for precision navigation in drones, smartphones, and autonomous vehicles is significantly contributing to market growth. Additionally, ongoing innovation, sensor miniaturization, and growing integration of magnetometers in IoT devices are expected to further drive global market expansion.

List of key magnetometer companies profiled:

- Honeywell International Inc. (U.S.)

- Geometrics, Inc. (U.S.)

- Billingsley Aerospace & Defense (U.S.)

- AlphaLab, Inc. (U.S.)

- Applied Physics Systems (U.S.)

- Metrolab Technology SA (Switzerland)

- Bartington Instruments Ltd. (U.K.)

- FOERSTER Holding GmbH (Germany)

- Lake Shore Cryotronics, Inc. (U.S.)

- Marine Magnetics Corp. (Canada)

Information Source:

https://www.fortunebusinessinsights.com/magnetometer-market-112875

Segmentation: Magnetometer Market

Space Segment to Grow Steadily with Satellite-Based Deployments in LEO and Scientific Missions

By platform , the market is segmented into airborne , ground , maritime , and space . The space segment is expected to witness the fastest growth due to increasing launches of LEO (Low Earth Orbit) satellites, which rely on compact and high-precision magnetometers for navigation and attitude control systems.

Aerospace & Defense to Emerge as Dominant End-User Amid Rising Investments in Geospatial Intelligence

By end-user , the magnetometer market is categorized into aerospace & defense , consumer electronics , marine/naval , automotive , and others . The aerospace & defense segment held the largest share in 2024 due to extensive use in military aircraft, submarines, drones, and satellite missions requiring precise magnetic field detection.

North America Leads Global Adoption, Backed by High Investments in Space and Defense Programs

Regionally, the market is analyzed across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa . North America held the largest share in 2024, bolstered by advanced infrastructure, key magnetometer manufacturers, and robust demand from defense and space agencies such as NASA and the U.S. Department of Defense.

MARKET DYNAMICS

Market Drivers

Rising Integration of Magnetometers in UAVs and Autonomous Systems to Drive Market Growth

The increasing deployment of UAVs and autonomous systems across defense and commercial sectors is significantly fueling the demand for magnetometers. These sensors play a vital role in navigation by detecting Earth’s magnetic field, especially in GPS-denied or challenging environments. Their expanding use in aerospace applications—such as satellite positioning—and in defense for magnetic anomaly detection is further propelling market growth.

Market Restraints

Interference and Calibration Issues May Impede Market Expansion

Magnetometers are susceptible to magnetic interference from surrounding metallic objects and electronic equipment, which can compromise their accuracy and reliability. Moreover, these sensors often require frequent calibration and ongoing maintenance to ensure optimal performance. These technical challenges can increase operational complexity and costs, potentially limiting broader adoption in high-stakes sectors like aerospace and defense.

Key Industry Developments:

December 2024 — MDA Space selected Honeywell to supply Attitude Control Systems and Magnetometer Unit components, including Reaction Wheel Assemblies and 3-axis Space Rate Sensors, for the MDA AURORA satellite line. These systems will support Telesat’s LEO constellation by maintaining orientation and enhancing signal reliability and solar energy absorption.

Gallium Nitride Device Market Competitive Landscape: Key Players and Strategies 2032

By Miyasingh, 2025-08-08

The global gallium nitride device market was valued at approximately USD 20.56 billion in 2019 and is expected to expand to around USD 39.74 billion by 2032, reflecting a compound annual growth rate (CAGR) of 5.20% from 2020 to 2032. In 2019, North America held a significant portion of the market, accounting for 35.89% of the total share. This growth trajectory indicates a strong demand for GaN devices across various applications in the coming years.

The gallium nitride (GaN) device market is experiencing significant growth, driven by increasing demand across various applications. This expansion reflects advancements in technology and the rising adoption of GaN devices in sectors such as telecommunications, automotive, and consumer electronics. North America is a key player in this market, showcasing a substantial share. Overall, the outlook for the GaN device market remains positive, with expectations for continued innovation and development in the coming years.

A list of all the prominent Gallium Nitride Device Market Key Players:

- Infineon Technologies AG (Germany)

- Efficient Power Conversion Corporation. (The U.S.)

- EPISTAR Corporation (Taiwan)

- GaN Systems (Canada)

- MACOM (The U.S.)

- Microsemi (The U.S.)

- Mitsubishi Electric Corporation (Japan)

- NICHIA CORPORATION (Japan)

- Northrop Grumman Corporation (The U.S.)

- NXP Semiconductors. (Netherland)

- Qorvo, Inc (The U.S.)

- Texas Instruments Incorporated. (The U.S.)

- Toshiba Corporation (Japan)

Information Source:

https://www.fortunebusinessinsights.com/gallium-nitride-gan-devices-market-103367

Segmentation:

The gallium nitride (GaN) device market is segmented by various factors, including device type, wafer size, component, application, end user, and geography. Device types encompass opto-semiconductor, power semiconductor, and RF semiconductor devices. Wafer sizes range from 2-inch to 6-inch and above. Key components include transistors, diodes, rectifiers, and power integrated circuits (ICs). Applications for GaN devices span light detection and ranging, wireless and electric vehicle charging, as well as radar and satellite radio frequencies. End users include sectors such as aerospace, defense, healthcare, renewables, and information and communication technology. Geographically, the market is divided into regions such as North America, Europe, Asia-Pacific, the Middle East, and the rest of the world, with specific countries like the U.S., Canada, China, and Germany highlighted for their device type contributions.

Drivers & Restraints

Expansion of the Telecommunications Sector to Boost Growth

The increasing demand for energy-efficient gallium nitride (GaN) devices is being driven by the rapid expansion of the telecommunications sector. Many internet service providers are now prioritizing lower latency through optical fiber connections, along with enhancing connectivity and network capacity. Additionally, the growing adoption of GaN devices in 5G infrastructure is expected to further accelerate gallium nitride device market growth in the coming years. However, the high costs associated with the maintenance and development of gallium nitride devices may pose a challenge to this growth.

Segmentation- Gallium Nitride Device Market

Opto-semiconductor Device Segment to Grow Rapidly Backed by Increasing Usage in Lasers

Based on device type, the opto-semiconductor device segment procured the highest gallium nitride device market share in 2019. This growth is attributable to their increasing usage in various aerospace applications, such as Light Detection and Ranging (LiDAR) and pulsed lasers. Besides, they are used in optoelectronics, LEDs, lasers, photodiodes, and solar cells.

Regional Insights- Gallium Nitride Device Market

High Demand for Wireless Devices to Favor Growth in Europe

Geographically, North America generated USD 7.38 billion in 2019 because of the presence of numerous prominent manufacturers, such as MACOM, Cree, Inc., Northrop Grumman Corporation, Efficient Power Conversion Corporation, Microsemi, and others in this region.

Europe, on the other hand, is anticipated to grow significantly on account of the rising demand for wireless devices in Germany, France, and the U.K. In Asia Pacific, the rising demand for gallium nitride devices from emerging nations, such as India and China would aid growth.

Key Industry Developments:

January 2025 - Wolfspeed launched its Gen 4 MOSFET technology platform, delivering breakthrough performance for high-power applications, enhancing efficiency and reliability in real-world conditions.

November 2024 - Infineon introduced the world's first 300mm power gallium nitride (GaN) wafer technology at electronica 2024, marking a significant advancement in power electronics manufacturing.

The global LEO satellite market was valued at USD 7.71 billion in 2024 and is projected to grow to USD 11.53 billion by 2032, rising from USD 7.93 billion in 2025, at a CAGR of 5.5% during the forecast period. North America dominated the market in 2024, holding a significant 38.91% share.

Market expansion is being driven by rising demand for high-speed communication, Earth observation, and seamless global connectivity. LEO satellites, positioned closer to Earth than traditional satellites, offer key advantages such as reduced latency and faster data transmission. These capabilities make them well-suited for a range of applications, including broadband internet, disaster response, navigation, and defense-related missions.

GLOBAL LEO SATELLITE MARKET OVERVIEW

- Market Size & Forecast

2024 Market Size: USD 7.71 billion

2025 Market Size: USD 7.93 billion

2032 Forecast Market Size: USD 11.53 billion

CAGR: 5.5% from 2025–2032 - Market Share

North America dominated the LEO satellite market with a 38.91% share in 2024, supported by substantial investments in satellite infrastructure, defense applications, and broadband expansion through large-scale satellite constellations like Starlink and Project Kuiper.

By type, the small satellite segment accounted for the largest share, owing to its lower launch costs, shorter development cycles, and increasing demand for compact, cost-effective systems.

By application, the communication segment led the market, driven by the rising need for global broadband and mobile connectivity, particularly in remote and underserved regions.

By end-use, the commercial segment held the dominant position, backed by rapid growth in IoT networks, satellite imaging, and navigation services across various industries. - Key Country Highlights

United States: Leads the global LEO satellite market with strong involvement from major players such as SpaceX, Amazon (Project Kuiper), and Lockheed Martin, supported by high levels of investment in both defense and commercial satellite capabilities.

Information Source:

https://www.fortunebusinessinsights.com/leo-satellite-market-112113

List of Key Players Mentioned in the Report:

- SpaceX (U.S.)

- Airbus Defense and Space (Germany)

- Lockheed Martin (U.S.)

- OneWeb (U.K.)

- Boeing (U.S.)

- Planet Labs Inc. (U.S.)

- Spire Global Inc. (U.S.)

- Iridium Communications Inc. (U.S.)

- Swarm Technologies (U.S.)

- GomSpace (Denmark)

Segmentation:

The global LEO satellite market is segmented by type, application, end use, and region. By type, the market is categorized into small, medium, and large satellites. In terms of application, it includes communication, Earth observation, navigation, scientific research, and others. By end use, the market is divided into government and military, and commercial sectors. Regionally, the market is analyzed across North America (U.S. and Canada), Europe (U.K., Germany, France, Russia, and the Rest of Europe), Asia Pacific (China, India, Japan, South Korea, and the Rest of Asia Pacific), and the Rest of the World, which includes Latin America and the Middle East & Africa. Each regional segment is further assessed by type, application, and end use to provide comprehensive market insights.

Report Coverage:

The global LEO satellite market report offers an in-depth analysis of market size, forecasts, and segmentation by application, end use, and type. It explores market trends, competition, product pricing, and key developments that have influenced the global market growth.

Drivers and Restraints: LEO Satellite Market

Rise of Small Satellites Constellations and Incorporation of Advanced Technologies to Bolster Market Growth

The launch of 2,402 small satellites in 2022 highlights the growing trend of adopting cost-effective and interconnected satellites. These systems enable extensive constellations that enhance global coverage and connectivity, meeting rising data and connectivity demands. Moreover, LEO satellite systems are becoming increasingly sophisticated, utilizing AI and machine learning to improve operational efficiency, lower costs, and provide low-latency solutions, further accelerating product adoption.

However, stringent regulations for satellite coordination and management can drive up operational costs and add complexity to satellite deployment, deterring LEO satellite market growth.

Regional Insights:

North America to Dominate the Market Owing to Strong Investment in Satellite Systems

North America leads the LEO satellite market with significant investments aimed at improving border surveillance, missile tracking capabilities, and national security. Leading companies such as Amazon, SpaceX, and Boeing are rapidly advancing satellite production and deployment, including Amazon’s Project Kuiper, which aims to produce over 3,000 satellites for enhanced global connectivity in July 2024.

The Asia Pacific region is benefitting from ongoing progress in spaceflight technology and launch systems, which supports the growth of the market. In August 2024, China’s plans to launch LEO satellites for its megaconstellation backed to a significant contract with the NRO, are set to enhance satellite infrastructure and global connectivity.

Competitive Landscape-

Key Players Focus on Mergers and Acquisitions to Sustain their Market Growth

Market leaders are focusing on advancing their product offerings by investing in R&D and developing diverse solutions. They are leveraging mergers, acquisitions, and new product launches to sustain their growth. Additionally, heavy investments in satellite networks are driving the push for global connectivity.

Key Industry Development:

May 2024 - The Ministry of Science and ICT in South Korea announced a USD 234.4 million project to launch two LEO satellites by 2030, leveraging 6G communication technology for advanced satellite-based connectivity.

The global aircraft component MRO market was valued at USD 18.13 billion in 2023 and is projected to grow from USD 19.20 billion in 2024 to USD 36.93 billion by 2032, registering a CAGR of 8.52% during the forecast period. North America led the market in 2023, accounting for a dominant share of 30.5%, driven by a strong presence of major MRO service providers, a large commercial aircraft fleet, and increasing investments in maintenance infrastructure.

Fortune Business Insights™ mentioned this in a report titled " Aircraft Component MRO Market Size, Share, Forecast and 2025-2032 ."

List of Key Players Present in the Report :

- Lufthansa Technik (Germany)

- AAR Corp. (U.S.)

- SIA Engineering Company (Singapore)

- ST Aerospace (Singapore)

- ST Engineering (Singapore)

- BOEING Company (U.S.)

- SR Technics (Switzerland)

- GE Aviation (U.S.)

- HAECO (Hong Kong)

- Bombardier Inc. (Canada)

Information Source:

https://www.fortunebusinessinsights.com/aircraft-component-mro-market-104871

Segmentation-

Commercial Aircraft Segment to Dominate due to Growing Demand for Aircraft Component MRO Services

By type, the market is segmented into commercial aircraft, business jets, general aviation aircraft, and helicopters. The commercial aircraft segment had the highest aircraft component MRO market share in 2022. The segment is also estimated to witness the highest growth rate due to increasing demand for aircraft component MRO services during the forecast period.

Flight Control Segment to Dominate due to Cost of the Component's MRO

By component, the market is segmented into wheel and brakes, landing gear, avionics, fuel system, hydraulic system, cockpit systems, flight control, electrical systems, thrust reversers, and others. The flight control segment will dominate the market during the forecast period due to the control’s complexity and cost associated with the component's maintenance, repair, and overhaul.

Process Ensuring Aircraft Performance to Lead to Overhaul Segment’s Dominance

By maintenance service, the market is segmented into inspection, overhaul, repairs, and others. The overhaul segment had the highest market share in 2022. The segment's dominance is attributed to the process ensuring the aircraft performance and tolerance set by its manufacturer.

Geographically, the market is studied across North America, Europe, Asia Pacific, the Middle East & Africa, and Rest of the World.

Report Coverage-

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- The latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints-

Increased Air Fleet Expansion and Aircraft Deliveries to Drive Market Growth

The demand for MRO services will increase due to continuous growth in fleet sizes and aircraft deliveries worldwide. A continuous rise in air travel in developing nations, such as China and India, will increase new aircraft demand in some major countries. There are choices available between independent MROs, aircraft traffic, and components due to increased experiences by the passenger-growth trend.

The high consultancy fees charged by the OEMs have made it difficult for the MRO services providers to expand and diversify their services worldwide, affecting the market growth.

Regional Insights-

Growing Demand for Aircraft Component MRO to Drive Market in North America.

The North America market was valued at USD 5.04 billion in 2022. North America is expected to dominate due to the growing MRO services market and increasing presence of top key players during the forecast period. In February 2022, IBS Software and Lynx Air partnered to implement the iFlight digital platform to manage flight and crew operations.

Asia Pacific is expected to grow at the highest CAGR over 2023-2030 owing to increasing demand for aircraft component MRO services from the commercial airlines of Singapore.

Competitive Landscape-

Rising Focus of Key Players on Providing a Variety of Services to Aid Market Growth

The upcoming trends in the market are technologically advanced aviation MRO software systems, cloud deployment, and new enhancements. Key companies, such as Aar Corp. (U.S.) and Lufthansa Technik, adopting collaboration strategies are driving the aircraft component MRO market growth during the forecast period. The rising investment by key players in the research and development of new technologies will also boost the market during the forecast period.

Key Industry Development

September 2023 – ST Engineering announced that it had secured a multi-year contract to provide Japan Airlines with component Maintenance-By-the-Hour (MBHTM) solutions. The contract stated that ST Engineering will continue to provide Japan Airlines’ Boeing 737-800s with a full suite of component solutions, including component pooling, component modification, repair & overhaul, component predictive health monitoring, and logistics services.

The global air defense systems market was valued at USD 87.63 billion in 2024. It is expected to grow from USD 95.73 billion in 2025 to USD 154.81 billion by 2032, registering a compound annual growth rate (CAGR) of 7.11% during the forecast period. In 2024, North America led the market, accounting for a dominant share of 34.58%.

The air defense systems market is experiencing steady growth, driven by increasing global defense spending, rising geopolitical tensions, and the need for advanced technologies to counter evolving aerial threats. These systems play a crucial role in national security by detecting, tracking, and neutralizing incoming missiles, aircraft, and unmanned aerial vehicles (UAVs). Ongoing technological advancements, such as the integration of radar, missile interceptors, and command and control systems, are further enhancing system capabilities. With a growing focus on modernizing military infrastructure, countries worldwide are investing heavily in air defense solutions to strengthen their defense preparedness.

List of Key Players Profiled in the Report:

- BAE Systems Plc. (U.K.)

- Elbit Systems Ltd. (Israel)

- General Dynamics Corp. (U.S.)

- Hanwha Aerospace Co., Ltd. (South Korea)

- Israel Aerospace Industries Ltd. (Israel)

- Kongsberg Gruppen ASA (Norway)

- L3Harris Technologies Inc. (U.S.)

- Leonardo S.P.A. (Italy)

- Lockheed Martin Corp. (U.S.)

- Northrop Grumman Corp. (U.S.)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Raytheon Technologies Corp. (U.S.)

- Rheinmetall AG (Germany)

Browse In-depth Summary of This Research Insight:

https://www.fortunebusinessinsights.com/air-defense-systems-market-113430

Segmentation Highlights

Weapon Systems Segment Leads the Market Due to Strategic Defense Focus

By component, the air defense systems market is segmented into command & control systems, weapon systems, fire control systems, radar systems, and support equipment. Weapon systems dominate due to increasing investments in interceptors, missile launchers, and kinetic/directed energy weapons.

Threat Detection Systems Segment Expected to See Rapid Growth

Based on system type, the market is bifurcated into threat detection systems and countermeasure systems. Threat detection systems are expected to register the highest growth due to the escalating need for early-warning and tracking technologies.

Land-Based Segment Holds Largest Share

By platform, the land-based segment leads, attributed to the deployment of mobile and stationary units in conflict-prone regions for border and civilian infrastructure protection.

Short-Range Segment Driven by Rise in Drone and Cruise Missile Threats

On the basis of range, the air defense systems market is divided into short (below 10 km), medium (10–100 km), and long-range (above 100 km) systems. The short-range segment is growing rapidly due to the proliferation of small UAV threats.

Radar & Tracking Dominates Technology Segment

The radar & tracking category leads due to constant advancements in surveillance, tracking, and data fusion systems necessary for intercepting modern aerial threats.

Fixed Installations Remain Critical for Strategic Locations

By deployment mode, fixed installations are projected to maintain a significant share as they are essential for safeguarding key military bases, industrial sites, and cities.

Market Dynamics

Drivers:

- Rising Geopolitical Tensions Fuel Demand for Air Defense

Nations are accelerating procurement of integrated defense systems due to evolving threats from both state and non-state actors. Increased defense budgets are particularly evident in Europe, the Middle East, and Asia Pacific. - Advancements in Directed Energy and Radar Technologies Boost Growth

Technological progress in radar detection, AI-enabled tracking, and laser-based countermeasures enhance air defense efficiency, making these systems more reliable and responsive.

Restraints:

- High Development and Maintenance Costs May Hamper Adoption

Advanced air defense systems require substantial investment, which may challenge adoption in countries with limited defense budgets.

Regional Insights

North America Dominates Global Market Share with Strong Defense Infrastructure

North America accounted for a significant share in 2024, supported by large-scale procurement programs by the U.S. Department of Defense and the presence of major players like Raytheon, Lockheed Martin, and Northrop Grumman.

Europe and Asia-Pacific Emerging as Strategic Markets

Europe’s growth is driven by rising regional tensions and collaborative NATO defense efforts. Asia Pacific, led by China, India, and South Korea, is investing in indigenous air defense capabilities and multi-domain deterrence.

Competitive Landscape

Collaborations and Product Innovation Key to Competitive Edge

Leading defense contractors are forming joint ventures and upgrading their air defense portfolios with new launches. Strategic contracts with governments continue to shape market growth.

Key Industry Development

November 2024 – Anduril received a USD 200 million, five-year Indefinite Delivery/Indefinite Quantity (IDIQ) contract from the U.S. Marine Corps to develop and deliver a Counter Unmanned Aerial System (CUAS) Engagement System (CES) for the Marine Air Defense Integrated System (MADIS). The MADIS CES is designed to offer rapid deployment and effective threat mitigation for expeditionary operations.

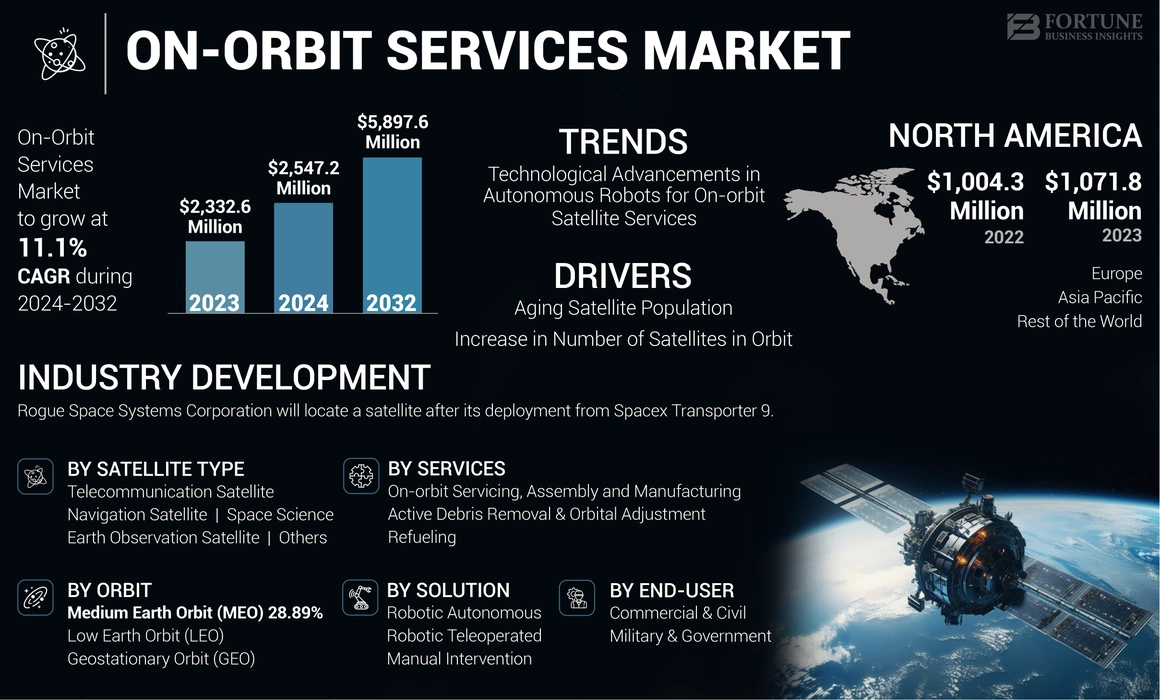

On-Orbit Services Market Growth Opportunities, Trends, and Forecast to 2032

By Miyasingh, 2025-08-06

The global on-orbit services market was valued at USD 2,332.6 million in 2023 and is projected to grow from USD 2,547.2 million in 2024 to USD 5,897.6 million by 2032, exhibiting a CAGR of 11.1% during the forecast period. North America led the market in 2023 with a dominant share of 45.95%.

The on-orbit services market is rapidly expanding, driven by the increasing need for satellite life extension, debris removal, refueling, and in-space manufacturing. As the number of satellites in orbit continues to grow, the demand for sustainable space operations and infrastructure maintenance is becoming more critical. Emerging technologies and partnerships between public and private space agencies are further accelerating innovation in on-orbit servicing capabilities. North America remains at the forefront, supported by strong government funding, a mature aerospace sector, and active participation from key players focused on extending satellite functionality and enhancing space situational awareness.

Key On-Orbit Services Market Players

Several companies are actively shaping the on-orbit services landscape. Leading organizations include:

- Airbus S.A.S (Netherlands)

- Thales Alenia Space (France)

- Lockheed Martin Corporation (U.S.)

- Orbit Fab (U.S.)

- Astroscale (Japan)

- ClearSpace SA (Switzerland)

- Obruta Space Solutions Corp. (Canada)

- D-Orbit SpA (Italy)

- Maxar Technologies (U.S.)

- Eta Space (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/on-orbit-services-market-108399

Market Segmentation

The on-orbit services market is segmented by end-user, orbit, satellite type, service, and solution. Among end-users, the military & government segment is growing rapidly due to investments from agencies like NASA and ESA, while the commercial & civil segment dominated in 2023. By orbit, Low Earth Orbit (LEO) held the largest share owing to increased small satellite deployments, whereas Geostationary Orbit (GEO) is expected to grow at the fastest pace as aging satellites require servicing. In terms of satellite type, Earth observation satellites led the market, while the space science segment is projected to grow fastest due to the critical nature of scientific missions. By service, refueling dominated and is anticipated to continue its strong growth, supported by cost-saving benefits and extended satellite lifespan. Lastly, robotic teleoperated solutions led in 2023 due to precision handling, while robotic autonomous systems are set to expand quickly with advancements in AI and visual perception technologies.

Regional Insights

North America

North America led the on-orbit services market in 2023, holding a dominant market share of 45.95%. The presence of major space companies, robust government funding, and increasing private sector participation have propelled growth in this region.

Europe

Europe is witnessing steady growth due to advancements in satellite servicing technologies and collaborations between government agencies and private firms.

Asia-Pacific

Countries like Japan and China are investing heavily in space missions, driving demand for on-orbit services in this region.

Rest of the World

Other regions, including the Middle East and Africa, are slowly entering the market, focusing on satellite-based communication and Earth observation initiatives.

Industry Developments:

December 2024 – Thales Alenia Space, a joint venture between Thales and Leonardo, signed a first-phase contract valued at €25 million (USD 26.09 million) with the European Space Agency (ESA) to develop and demonstrate a complete cargo delivery service to and from space stations in low-Earth orbit (LEO) by 2028. The company will co-lead the development of this innovative LEO Cargo Return Service, marking a key step toward commercial space logistics.

December 2023 – Rogue Space Systems Corporation, a provider of space situational awareness and satellite servicing solutions, announced its upcoming mission to locate and communicate with a customer’s satellite following its deployment from SpaceX's Transporter-9 mission. The operation will involve establishing contact and initiating in-orbit servicing tasks, supporting the customer’s satellite functionality and mission objectives.

Future Outlook

The on-orbit services market is poised for rapid expansion due to technological innovations, increasing satellite deployments, and the growing need for sustainable space operations. Companies are focusing on automation, AI-powered diagnostics, and in-orbit manufacturing to revolutionize the industry. As demand for satellite servicing rises, the sector is expected to witness increased investments, partnerships, and policy developments, shaping the future of space sustainability.

Software Defined Radio Market Growth Opportunities, Trends, and Forecast to 2032

By Miyasingh, 2025-08-06

The global software defined radio market was valued at USD 14.19 billion in 2023 and is projected to grow from USD 14.94 billion in 2024 to USD 21.97 billion by 2032, exhibiting a CAGR of 4.9% during the forecast period. North America led the market in 2023, accounting for a 32.84% share.

The software defined radio market is gaining momentum globally, driven by increasing demand for flexible and interoperable communication systems across defense, commercial, and public safety sectors. SDR technology allows radios to be reprogrammed and updated via software, enabling seamless adaptation to different frequencies and protocols without changing hardware. This flexibility is particularly valuable in military operations, disaster response, and emerging 5G networks. Growing investments in defense modernization, along with the rising need for secure, high-speed communication, are fueling market growth. Additionally, technological advancements in cognitive radio and the integration of artificial intelligence are expected to create new growth opportunities in the SDR market.

Browse In-depth Summary of This Research Insight:

https://www.fortunebusinessinsights.com/software-defined-radios-market-102524

List of the Companies Operating in the Market:

- BAE Systems PLC (The U.K.)

- Northrop Grumman Corporation (The U.S.)

- Raytheon Technologies Corporation (The U.S.)

- Elbit Systems Ltd. (Israel)

- Thales Group S.A. (France)

- L3Harris Technologies, Inc. (The U.S.)

- General Dynamics Corporation (The U.S.)

- Viasat, Inc. (The U.S.)

- Leonardo S.p.A. (Italy)

- Rohde & Schwarz GmbH & Co. KG (Germany)

Report Coverage:

The Software Defined Radios (SDR) market is projected to grow at a CAGR of 5.3% during the forecast period of 2023 to 2028, reaching an estimated value of USD 16.20 billion by 2028, up from USD 11.60 billion in 2021. The report, spanning 200 pages, provides in-depth analysis covering revenue forecasts, company profiles, the competitive landscape, key growth factors, and the latest market trends. It offers segmentation by type, component, frequency band, platform, and application, along with regional insights across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Key drivers fueling the growth of the SDR market include the increasing adoption of software defined radios for military applications, which offer enhanced interoperability and flexibility, and the growing shift from conventional communication systems to modern, software-driven communication technologies across both defense and commercial sectors.

Market Segmentation:

Based on the type, the market is classified into general-purpose radio, joint tactical radio system (JTRS), cognitive/intelligent radio, and terrestrial trunked radio (TETRA). Based on the component, the market is bifurcated into hardware and software. Moreover, On the basis of frequency band, the market is categorized into MF/HF (Medium/high frequency), VHF (very high frequency), UHF (ultra-high frequency), and other bands. Based on the platform, the market is segregated into airborne, naval, land, and space. On the basis of application, the market is divided into commercial and military & defense. Lastly, based on the region, the market is segregated into North America, Asia-Pacific, Europe, and Rest of the World.

Report Coverage:

The global market report includes qualitative and quantitative analysis of several factors such as the key drivers and restraints that will impact growth. Additionally, the report provides insights into the regional analysis that covers different regions, which are contributing to the growth of the market. It includes the competitive landscape that involves the leading companies and the adoption of strategies by them to announce partnerships, introduce new products, and collaboration that will further contribute to the growth of the market between 2021 and 2028. Moreover, the research analyst has adopted several research methodologies such as SWOT and PESTEL analysis to extract information about the current trends and industry developments that will drive the market growth during the forecast period.

Driving Factors:

Increasing Adoption of the Product across Several Military Applications to Promote Growth

In February 2021, the Indian Army announced its plans to focus on the revamping of its military communication systems by procuring VHF/UHF Manpack software defined radios under the Make-II class. Like India, several countries are focusing on adopting advanced radio communication systems for tactical applications for their militaries. Moreover, the growing adoption of advanced modern radio communication systems across commercial and military applications is expected to surge the adoption of the product. These modern systems provide efficient transmitting and receiving of several modulation methods by adopting a common set of hardware whole enhancing functionality through software modulation. Therefore, such initiatives are anticipated to boost the global software defined radio market growth during the forecast period.

Further Report Findings:

- North America is expected to hold the largest global market growth during the forecast period. This is due to the high military spending and the rapid-paced adoption of advanced communication technologies in countries such as the United States. North America stood at USD 4.9 billion in 2020.

- The market in Asia-Pacific is anticipated to experience exponential growth backed by the high development of the telecommunication sector and supportive government space programs that will boost the demand for advanced software defined radio systems between 2023 and 2028.

- Based on platform, the land segment is expected to hold the largest market share in terms of revenue in the forthcoming years. This is owing to the growing adoption of advanced software defined radio across several cellular base stations. Moreover, the rising installations of these systems on military vehicles is anticipated to lead to the segmental growth during the forecast period.

COMPETITIVE LANDSCAPE:

Product Innovation by Eminent Companies to Amplify Their Market Positions

The global market is experiencing significant competition from the players operating in the market. These players are focusing on developing advanced software defined radio systems to cater to the growing demand from the defense and healthcare sector globally. Additionally, adoption of strategies such as merger and acquisition, collaboration, and facility expansion by other companies to maintain their stronghold is expected to favor the market growth in the forthcoming years.

Industry Development:

-

March 2024 – Elta Systems , a subsidiary of Israel Aerospace Industries (IAI) , announced the launch of its latest software-defined radio (SDR). The new SDR is equipped with a modern architecture and supports operations across very high frequency (VHF), ultra high frequency (UHF), and L-band ranges, enhancing its versatility and performance across various mission-critical applicatio

The global magnetometer market was valued at USD 3.64 billion in 2024 and is projected to grow from USD 3.94 billion in 2025 to USD 7.75 billion by 2032, registering a CAGR of 10.2% during the forecast period. North America led the market in 2024, accounting for a 38.74% share.

The global magnetometer market is experiencing steady growth, driven by increasing demand across various sectors such as aerospace, defense, consumer electronics, automotive, and industrial applications. Magnetometers, which measure magnetic field strength and direction, are essential for navigation systems, geological surveys, and emerging technologies like autonomous vehicles and wearable devices. Advancements in miniaturization, sensor accuracy, and integration with IoT and GPS technologies are further boosting market adoption. As industries continue to prioritize precision, safety, and automation, the role of magnetometers is expected to expand significantly, especially in high-growth regions like North America and Asia Pacific.

List of key magnetometer companies profiled:

- Honeywell International Inc. (U.S.)

- Geometrics, Inc. (U.S.)

- Billingsley Aerospace & Defense (U.S.)

- AlphaLab, Inc. (U.S.)

- Applied Physics Systems (U.S.)

- Metrolab Technology SA (Switzerland)

- Bartington Instruments Ltd. (U.K.)

- FOERSTER Holding GmbH (Germany)

- Lake Shore Cryotronics, Inc. (U.S.)

- Marine Magnetics Corp. (Canada)

Information Source:

https://www.fortunebusinessinsights.com/magnetometer-market-112875

Segmentation: Magnetometer Market

Space Segment to Grow Steadily with Satellite-Based Deployments in LEO and Scientific Missions

By platform , the market is segmented into airborne , ground , maritime , and space . The space segment is expected to witness the fastest growth due to increasing launches of LEO (Low Earth Orbit) satellites, which rely on compact and high-precision magnetometers for navigation and attitude control systems.

Aerospace & Defense to Emerge as Dominant End-User Amid Rising Investments in Geospatial Intelligence

By end-user , the magnetometer market is categorized into aerospace & defense , consumer electronics , marine/naval , automotive , and others . The aerospace & defense segment held the largest share in 2024 due to extensive use in military aircraft, submarines, drones, and satellite missions requiring precise magnetic field detection.

North America Leads Global Adoption, Backed by High Investments in Space and Defense Programs

Regionally, the market is analyzed across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa . North America held the largest share in 2024, bolstered by advanced infrastructure, key magnetometer manufacturers, and robust demand from defense and space agencies such as NASA and the U.S. Department of Defense.

MARKET DYNAMICS

Market Drivers

Growing Use of Magnetometers in UAVs and Autonomous Systems to Boost Market Growth

The rising adoption of UAVs and drones in defense and commercial sectors is driving demand for magnetometers. These devices are essential for navigation, especially in GPS-denied environments, by measuring Earth’s magnetic field. Their use in aerospace for satellite positioning and in defense for detecting magnetic anomalies is further accelerating market growth.

Market Restraints

Interference and Calibration Challenges to Hinder Market Growth

Magnetometer performance can be affected by interference from nearby metals or electronic devices, leading to reduced accuracy. Additionally, they require regular calibration and maintenance, increasing operational complexity and costs. These issues may limit wider adoption, particularly in critical aerospace and defense applications.

December 2024 — MDA Space selected Honeywell to supply Attitude Control Systems and Magnetometer Unit components, including Reaction Wheel Assemblies and 3-axis Space Rate Sensors, for the MDA AURORA satellite line. These systems will support Telesat’s LEO constellation by maintaining orientation and enhancing signal reliability and solar energy absorption.

Aerospace Superalloy Fasteners Market Growth Opportunities, Trends, and Forecast to 2031

By Miyasingh, 2025-08-06

The global aerospace superalloy fasteners market was valued at USD 1,128.4 million in 2024 and is projected to grow from USD 1,268.0 million in 2025 to USD 2,716.8 million by 2031, at a CAGR of 13.5%. North America led the market in 2024 with a 41.61% share.

Aerospace superalloy fasteners are high-performance components designed for the demanding environments of the aviation and space industries. Manufactured from materials such as Inconel 718, Waspaloy, MP35N, A286, and titanium alloys, these fasteners exhibit outstanding strength, resistance to corrosion and oxidation, and superior durability at elevated temperatures. They are widely used in engines, turbines, landing gears, and structural assemblies across commercial, military, and space platforms.

The market is witnessing a strong revival post-COVID-19 disruptions, fueled by resurgent aircraft production, modernization programs, and technological advancements. The ongoing Russia-Ukraine conflict is also reshaping global supply chains and creating opportunities for domestic production in key aerospace nations.

Fortune Business Insights™ displays this information in a report titled, "Aerospace Superalloy Fasteners Market, 2025–2031."

LIST OF KEY COMPANIES PROFILED IN THE REPORT

- LISI Aerospace SAS (France)

- Precision Castparts Corp. (U.S.)

- Howmet Aerospace Inc. (U.S.)

- TriMas (U.S.)

- Arconic Corporation (U.S.)

- National Aerospace Fasteners Corporation (Taiwan)

- SPS Technologies Ltd. (U.K.)

- TFI Aerospace Corporation (Canada)

- B&B Specialties, Inc. (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/aerospace-superalloy-fasteners-market-113525

Segmentation: Aerospace Superalloy Fasteners Market

Rivets Dominated Market Owing to Their Robust Design

By product, the market is segmented into rivets, screws, nuts & bolts, and others. The rivets segment held the largest market share in 2024 due to their durability and essential role in aircraft structural integrity. The screws segment is expected to grow rapidly due to increasing demand for easy maintenance and modular aircraft parts.

Fixed-Wing Aircraft Represented Largest Market Share

Based on platform, the market is bifurcated into fixed-wing and rotary-wing aircraft. The fixed-wing segment dominated in 2024, fueled by rising aircraft production by major OEMs like Boeing and Airbus. The expansion of global commercial fleets is a major contributing factor.

Airframe Segment Led Due to Fleet Modernization

By application, the market is categorized into airframe, engine, interior, and others. The airframe segment led the market due to the ongoing replacement of aging aircraft and increased MRO (Maintenance, Repair, and Overhaul) activities. The engine segment is set to grow significantly due to the increasing use of fasteners that can withstand high heat and stress environments.

Drivers and Restraints

Increased Adoption for Advanced Aircraft Engines to Boost Product Demand

The rising adoption of next-gen aircraft engines requiring high-temperature, high-strength fasteners is a major driver. Alloys like MP35N and AEREX 350 are gaining traction due to their exceptional performance under extreme stress and temperatures.

Stringent Aerospace Certification Standards Hampering Market Entry

Strict regulatory and quality standards such as AS9100, MIL-SPEC, and NAS create high barriers to entry and extend product development cycles, impacting smaller players and startups.

Opportunities & Trends

Growing Demand for Lightweight, High-Strength Materials in Modern Aircraft

Aircraft manufacturers are prioritizing fuel efficiency and sustainability, increasing the demand for high-performance materials like superalloy fasteners.

Adoption of Additive Manufacturing and AI-Powered QC

The integration of 3D printing and AI-based quality control systems enables rapid prototyping, lower production waste, and highly customizable fastener designs. These innovations support real-time adaptation to evolving aircraft design requirements.

Regional Insights

North America Dominated Global Market

North America led the market in 2024 with a market size of USD 469.56 million. The presence of aerospace giants such as Boeing, Lockheed Martin, and Precision Castparts Corp., along with advanced manufacturing infrastructure and FAA regulatory support, gives the region a significant edge.

Europe’s Growth Fueled by Airbus and Defense Investments

Europe holds a significant market share, led by France, the U.K., and Germany. Airbus's expanding aircraft production and R&D activities across platforms like the A350 and A330neo are major contributors to regional demand.

Asia Pacific to be Fastest Growing Region

China and India are experiencing a boom in commercial and defense aviation. Growing fleet sizes, new airport developments, and local manufacturing expansion are expected to drive rapid growth in the region.

Rest of the World Shows Steady Growth

The Middle East & Africa are investing in airport infrastructure and fleet expansion, especially in Gulf nations. Latin America is gaining traction due to increased aircraft deliveries and test programs in high-altitude regions like Mexico and Bolivia.

Competitive Landscape

Ongoing Technological Advancements Sustain Market Leadership

Key market players are investing in next-gen materials, including nickel-cobalt-chromium alloys and proprietary compositions for superior performance. Sustainability is also becoming a key differentiator, with leading firms adopting eco-friendly production techniques.

Notable Industry Development

February 2025 – TriMas announced a multi-year global contract with Airbus, expanding the role of its aerospace brands (Monogram, Allfast, and Mac Fasteners) across Airbus's supply chain. This contract enhances TriMas Aerospace's footprint in commercial aircraft fastener solutions.

The global military drone market was valued at USD 14.14 billion in 2023 and is expected to expand from USD 16.07 billion in 2024 to USD 47.16 billion by 2032, registering a robust CAGR of 13.15% during the forecast period. In 2023, North America led the market, accounting for a 36.1% share. The U.S. military drone market, in particular, is projected to witness substantial growth, reaching approximately USD 10.71 billion by 2030, fueled by rising R&D investments from key players including Sikorsky, Boeing, and other prominent regional manufacturers.

The U.S. continues to spearhead global military drone developments, awarding significant contracts such as the USD 389 million deal with General Atomics for MQ-1C Gray Eagle drones. Meanwhile, drones are playing a pivotal role in modern warfare, as seen in Ukraine’s use of over 700 kamikaze drones and Russia’s deployment of Shahed-136 drones in high-conflict zones. China and Israel remain dominant exporters, supplying advanced UAVs to allied nations, while the UK boosts tactical drone investments to strengthen ISR capabilities under its military modernization agenda.

This information is provided by Fortune Business Insights™ in its research report, titled “Military Drone Market Size, Share, Forecast and 2024-2032”.

List of Key Players Mentioned in the Report:

- General Atomics Aeronautical Systems, Inc. (U.S.)

- Northrop Grumman Corporation (U.S.)

- Elbit Systems Ltd. (Israel)

- Israel Aerospace Industries Ltd. (Israel)

- AeroVironment, Inc. (U.S.)

- Lockheed Martin Corporation (U.S.)

- Thales Group (France)

- Boeing (U.S.)

- BAE Systems (U.K.)

- SAAB Group (Sweden)

- Textron Systems (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/military-drone-market-102181

Segmentation:

Fixed Wing Segment to Register Substantial Demand Impelled by Rising Use for Long Distance Operations

Based on product type, the market is segmented into hybrid wing, fixed wing, and rotary wing. Of these, the fixed wing segment is set to dominate the product type segment over the study period. The growth is on account of rising deployment of the product for long-distance missions such as mapping, surveillance, and defense.

EVLOS Segment to have Fastest CAGR Driven by Escalating Adoption in Electronic Warfare

By range, the market is subdivided into Beyond Line of Sight (BLOS), Visual Line of Sight (VLOS), and Extended Visual Line of Sight (EVLOS). The EVLOS segment is expected to register fastest CAGR over the forecast period. The rise is propelled by the soaring product adoption in long-range missions, electronic warfare, and proper battle management.

Remotely Operated UAVs Segment to Record Appreciable Expansion Driven by Surging Adoption

Based on technology, the market is subdivided into semi-autonomous drones, remotely operated drones, and autonomous drones. The remotely operated drones segment is estimated to depict an appreciable surge over the estimated period. The expansion is on account of stringent government requirements for autonomous flying over long distances.

A irframe Segment to Dominate due to Increasing Adoption of UAVs by the Armed Forces

By system, the market is classified into payload, avionics, airframe, propulsion, software, and others. The airframe segment held the highest market share. The growth is impelled by the growing UAV adoption for a range of operations such as monitoring, surveillance, reconnaissance, and others.

ISRT Segment to Emerge as a Leading Segment Considering Growing Awareness for Strengthening the Defense System

Based on application, the market is segmented into logistics & transportation, Intelligence, Surveillance, Reconnaissance, and Targeting (ISRT), battle damage management, combat operations, and others. The surge is propelled by the growing role of UAVs in the defense sector.

Based on geography, the market is fragmented into Asia Pacific, Europe, North America, and the rest of the world.

Report Coverage:

The report gives a comprehensive coverage of the major trends augmenting the market share over the forecast period. It further offers an insight into the key factors boosting the global business landscape over the ensuing years. Other aspects in the market comprise an account of merger agreements, acquisitions, and additional initiatives adopted by leading industry participants for strengthening their business positions.

Drivers and Restraints:

Rising Military Expenditure to Propel Industry Expansion

One of the key factors propelling the military drone market growth is the escalation in military expenditure. The industry expansion is further propelled by the surging procurement of next-generation military drones.

However, the industry expansion could be affected by the high cost of modern systems.

Regional Insights:

North America to Emerge as Dominant Region Owing to the Presence of OEMs

The North America military drone market share is slated to dominate the global market over the forecast period. The surge is on account of the presence of several OEMs in the region.

The Europe market is poised to exhibit considerable expansion throughout the forecast period. The rise is due to the growing awareness associated with the improvement of military, navy, and air force capabilities.

Competitive Landscape:

Major Companies Ink Partnership Agreements to Strengthen Market Foothold

Leading market players are focused on adopting a series of strategic initiatives for strengthening their industry positions. These include merger agreements, collaborations, and the formation of alliances. Additional aspects comprise an increase in research activities and the development of new products.

Key Industry Development:

February 2023 – The Indian Army announced plans to procure 850 indigenous nano drones to support special military operations. These drones will be used primarily for surveillance and counter-terrorism missions.

February 2023 – The U.S. Air Force completed the development of facial recognition technology integrated into UAVs. These autonomous drones are capable of identifying and engaging targets independently. They are intended for use by special operations forces to gather intelligence and support mission-critical activities.