Category: Business

The global small arms market was valued at USD 9.07 billion in 2023 and is expected to rise from USD 9.46 billion in 2024 to USD 12.32 billion by 2032, reflecting a steady CAGR of 3.35% during the forecast period. In 2023, North America led the market with a 43.33% share, driven by strong defense spending, civilian firearm ownership, and the presence of leading manufacturers.

In 2023, North America dominated the small arms market with a 43.33% share, supported by high civilian firearm ownership, significant defense spending, and strong procurement from law enforcement and homeland security agencies. By type, handguns accounted for the largest share, driven by rising demand for personal protection, sports shooting, and concealed carry across the U.S., Canada, and Germany. The United States led globally, with over 400 million privately held firearms, robust defense modernization programs, and major contracts awarded to FN America and Heckler & Koch. Canada advanced with Colt Canada’s C20 rifle contract for the Department of National Defence, while Germany, home to Heckler & Koch, strengthened its position through NATO-aligned investments. France benefited from the contributions of Thales and Beretta in defense programs and exports, whereas India boosted domestic manufacturing and exports through procurement of 7.62mm rifles and joint ventures like PLR Systems. In China, more than 49 million civilian-owned firearms and state-backed modernization efforts bolstered growth, while Russia, led by Kalashnikov Group, continued exports to Africa, Asia, and Latin America despite sanctions.

Information Source:

https://www.fortunebusinessinsights.com/small-arms-market-103173

List of companies profiled in the report:

- American Outdoor Brands Corporation (The U.S.)

- Fabbrica d'Armi Pietro Beretta S.p.A. (Italy)

- FN HERSTAL (Belgium)

- General Dynamics Corporation (The U.S.)

- Heckler & Koch GmbH (Germany)

- Lockheed Martin Corporation (The U.S.)

- Northrop Grumman Corporation (The U.S.)

- Sturm, Ruger & Co., Inc. (The U.S.)

- Taurus International Manufacturing, Inc. (Brazil)

- Thales Group (France)

Increasing Number of Company Mergers will Bode Well for Market Growth

The report encompasses several factors that have contributed to the growth of the overall market in recent years. Among all factors, the increasing number of company mergers and acquisitions has made the highest impact on market growth. Due to constant demand for small arms, companies are tying-up with manufacturers for supply of these products for a long duration. In January 2019, the United States Army announced that it has signed a contract with Sig Sauer for long-term supply and development of the company’s popular P320 handgun. The contract is said to worth USD 580 million and will last for 8 years. This will be a significant step in the progress and expansion of the company. The collaboration

with US Army will also make it more popular in the global market. Sig Sauer’s collaboration with the United States Army will not just help the company grow, but will play a huge part in the growth of the overall small arms market in the foreseeable future.

North America Holds the Highest Market Share; High Defense Budget is a Primary Factor Behind Market Growth

The report analyses the latest market trends across five major regions, including North America, Rest of the Word, Europe, Asia Pacific, and the Middle East and Africa. Among all regions, the market in North America is expected to emerge dominant in the coming years. The high defense budgets in countries such as the United States has not just led to a wider product adoption, but has also yielded technologically advanced products. The increasing terror attacks and tense cross-border relations have also contributed to the growth of the small arms market in this region. As of 2019, the market in North America was worth USD 1.56 billion and this value is projected to increase at a considerable pace in the coming years.

Industry Developments:

- November 2023 – Belgium approved a long-term strategic partnership between Belgian Defence and FN Herstal to ensure small-caliber ammunition supply and maintain the army’s small arms fleet for 20 years. The initiative, part of EU and NATO strategic autonomy goals, is also open to other European nations.

- May 2023 – Israel Weapon Industries (IWI) signed a technology transfer agreement with FAME to set up an ARAD assault rifle production line in Peru, covering assembly, quality assurance, and maintenance, with potential expansion to other weapons and optical sights.

Hydrogen Aircraft Market Size, Top Key Players and Competitive Landscape 2024-2032

By Miyasingh, 2025-08-29

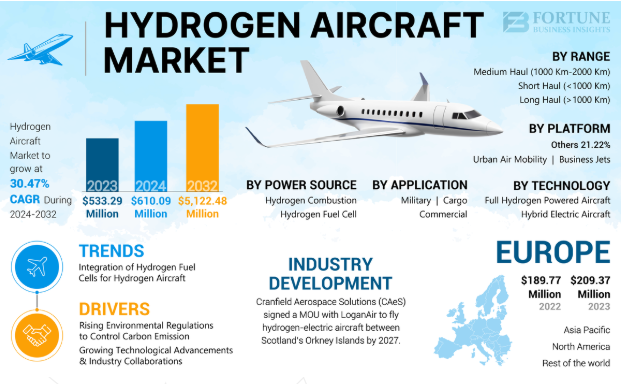

The global hydrogen aircraft market size was valued at USD 533.29 million in 2023 and is expected to expand from USD 610.09 million in 2024 to USD 5,122.48 million by 2032, registering a remarkable CAGR of 30.47% during the forecast period. In 2023, Europe led the market with a 39.26% share, driven by strong government support, R&D investments, and initiatives to accelerate sustainable aviation technologies.

At the country level, France stands out with Airbus spearheading hydrogen aircraft development under the ZEROe program and EU-backed sustainability projects. Germany benefits from robust public-private partnerships and institutional research support from DLR, whereas the UK is advancing hydrogen propulsion and storage through investments from GKN Aerospace and Rolls-Royce. In the United States, initiatives from NASA and the FAA, coupled with efforts by Boeing and ZeroAvia, accelerate hydrogen’s commercial adoption. Meanwhile, Japan fosters hydrogen integration through JAXA-led projects and private sector investment, China channels significant funding into hydrogen infrastructure to support aviation adoption, and the UAE positions itself as an emerging hub through hydrogen-focused diversification strategies.

Major Players Profiled in the Hydrogen Aircraft Market:

- Rolls Royce (U.K.)

- Safran SA (France)

- PIPISTREL (Slovenia)

- Hydrogen Energy Systems LLC (U.S.)

- GKN Aerospace (U.K.)

- Airbus (Netherlands)

- Boeing (U.S.)

- Urban Aeronautics Ltd. (Israel)

- Embraer (Brazil)

- Honeywell International Inc. (U.S.)

- Bell Textron Inc. (U.S.)

- ZeroAvia, Inc. (U.S.)

Get a Free Sample Research PDF:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/hydrogen-aircraft-market-108161

Segmentation:

- By platform, the hydrogen aircraft market is classified into air taxis, business jets, unmanned aerial vehicles, and others.

- On the basis of power source, the market is divided into hydrogen combustion and hydrogen fuel cell.

- Based on the passenger capacity, the market is segregated into less than 100, 100-200, and above 200.

- By range, the market is segregated into short haul (less than 1000km), medium haul (1000km - 2000km), and long haul (above 2000km).

- From the regional ground, the market is segmented into North America, Europe, Asia Pacific, and Rest of the World.

Report Coverage

The comprehensive hydrogen aircraft market research report delves into crucial elements, including the competitive landscape, material, product type, and application. The document provides valuable insights into prevailing market trends and significant industry advancements. It also encompasses a wide range of variables that have contributed to the recent expansion of the market. With a thorough examination of these factors, the report offers a holistic view of the market's current state and future potential.

Drivers & Restraints: Hydrogen Aircraft Market

Governments Globally Are Implementing Policies for the Promotion Of Sustainable Solutions To Offer Market Development Scope

Governments globally are implementing policies for the promotion of sustainable solutions in the aviation which is driving the hydrogen aircraft market growth. Hydrogen is considered to be one of the alternatives to the traditional fossil fuels in the aviation industry. Incentives, subsidies, and tax benefits for the development and employment of hydrogen aircrafts. These aircrafts provide sustainable solutions as they produce zero emissions at the time of operations, resulting in clean air.

One of the major restraints in the hydrogen aircraft market growth is issues with long-haul flights which require new designs of aircrafts. Integration of hydrogen fuel cell can get challenging and it gets heater repeatedly which requires cooling effect leading to more weight on the aircraft.

Information Source:

https://www.fortunebusinessinsights.com/hydrogen-aircraft-market-108161

Regional Insights

North America Leads the Market Share Due Presence Of Key Market Players

North America holds the largest part in global hydrogen aircraft market share as the region owing to high rate of innovation and technological advancements. Presence of key market players in the market for the production is also one of the reasons for the market growth.

Competitive Landscape

Various Business Initiatives Adopted By The Key Market Players To Drive Market Competition

The hydrogen aircraft market size has various key market players engaging into partnerships, collaborations, and getting certification for their new products. These strategies are set to enhance the market positions of the key market players.

Key Industry Development

- March 2023: Worcester Polytechnic Institute (WPI) and Honeywell Aerospace partnered for the examination of hydrogen cells which can help in the powering of new generation of aircrafts.

The global aircraft gearbox market size was valued at USD 3,381.5 million in 2024 and is anticipated to expand from USD 3,653.7 million in 2025 to USD 6,094.1 million by 2032, registering a CAGR of 7.58% during the forecast period. In 2024, North America led the market, accounting for 45.71% of the global share.

North America led the market with a 45.71% share in 2024, supported by the presence of major OEMs such as Boeing, GE, and Pratt & Whitney, along with strong defense spending and R&D investments. By component, the gear segment dominated due to its essential role in power transmission, torque control, and engine efficiency, while by platform, commercial aviation held the largest share, fueled by rising passenger traffic and global fleet expansion. In terms of gearbox type, accessory gearboxes led the market on account of increasing fleet size and demand for auxiliary system support, whereas OEMs accounted for the highest end-user share due to advanced technology integration and long-term supply chain partnerships with aircraft manufacturers. Regionally, the United States market is driven by military modernization and a large commercial fleet, with the Department of the Air Force requesting USD 217.5 billion for FY2025, including USD 66.7 billion for procurement and R&D. Canada benefits from a strong MRO ecosystem and suppliers like Safran and Liebherr, while Germany advances through aerospace investments and gearbox innovation led by Liebherr-Aerospace. The UK, with Rolls-Royce, continues to develop high-performance gearboxes, whereas France’s Safran focuses on lightweight, efficient designs for geared turbofans. In Asia, China and India drive growth with rapid fleet expansion, indigenous programs such as COMAC C919 and HAL Tejas, and growing MRO demand. The Middle East market expands with aircraft deliveries, airport development, and rising MRO needs in the UAE and Saudi Arabia, while Brazil and Mexico see steady growth through civil aviation recovery and MRO investments across Latin America.

Information Source:

https://www.fortunebusinessinsights.com/aircraft-gearbox-market-105541

List of Key Players Mentioned in the Report:

- Safran (France)

- Liebherr (Switzerland)

- United Technologies Corporation (UTC) (U.S.)

- Rexnord Aerospace (U.S.)

- Triumph Group (U.S.)

- Aero Gear (U.S.)

- CEF Industries Inc. (U.S.)

- The Timken Company (U.S.)

- AAR Corp (U.S.)

- Rolls-Royce plc (U.K.)

- Regal Rexnord (U.S.)

Segmentation:

Gear Segment Dominated Owing to its Crucial Role in Power Transmission and Engine Optimization

By component, the market is segmented into gear, housing, bearing, and others. The gear segment dominated the market in 2024 due to its essential function in transmitting power from the engine to various aircraft systems. Lightweight, high-precision gears support improved fuel efficiency and engine performance.

The housing segment is also anticipated to witness notable growth, driven by advances in lightweight materials that contribute to overall aircraft weight reduction and increased component durability.

Commercial Segment Led the Market Amid Rising Air Travel Demand

Based on platform, the market is segmented into commercial, civil, and military. The commercial segment held the dominant share in 2024, fueled by increasing airline fleet sizes and global passenger traffic. With 850 million passengers in the U.S. alone in 2023, demand for commercial aircraft—and their gearboxes—continues to rise.

Meanwhile, the military segment is expected to grow significantly, as heightened geopolitical tensions spur defense modernization efforts and procurement of advanced aircraft with robust gearbox requirements.

Accessory Gearbox Segment Dominated Due to Fleet Expansion

By gearbox type, the market is categorized into accessory gearboxes, reduction gearboxes, actuation gearboxes, tail rotor gearboxes, APU gearboxes, and others. The accessory gearbox segment led the market in 2024 due to expanding airline fleets and growing demand for more efficient aircraft systems.

The reduction gearbox segment is expected to grow steadily as it enables efficient engine-propeller coordination, supported by innovations in materials and designs that enhance reliability and longevity.

OEM Segment Led Market Due to Advanced Integration Capabilities

By end-user, the market is segmented into OEM, MRO, and others. The OEM segment dominated in 2024, owing to established supply chain networks and technical integration capabilities. OEMs play a vital role in incorporating new gearbox technologies into next-generation aircraft.

The MRO segment is projected to expand rapidly during the forecast period, driven by the aging global fleet and rising demand for maintenance, repair, and overhaul services.

Drivers and Restraints: Aircraft Gearbox Market

Rising Demand for Lightweight Aircraft Components to Boost Market Growth

With airlines and aircraft manufacturers focusing on efficiency, the demand for lightweight components, including gearboxes, is increasing. Lighter components not only enhance fuel efficiency but also improve performance, reduce emissions, and extend component lifespan. Manufacturers are leveraging advanced materials and design techniques to create high-performance, lightweight gear systems.

Stringent Regulations Pose Challenges to Market Expansion

However, the aircraft gearbox market faces challenges from stringent aerospace regulations. The high costs associated with design, development, and certification of gearboxes can hinder new entrants and slow innovation. Regulatory compliance and safety testing add to the complexity and cost of market participation, acting as a restraint on growth.

Regional Insights:

North America to Maintain Dominance Owing to Aerospace Leadership and Military Investment

North America led the global aircraft gearbox market in 2024, with a market value of USD 1,545.82 million. The region benefits from the presence of key players such as Boeing and GE, as well as strong R&D capabilities and government defense programs. The U.S. Department of the Air Force’s FY2025 budget of USD 217.5 billion—featuring USD 29 billion for procurement and USD 37.7 billion for R&D—underscores the scale of investment supporting the gearbox market.

Europe Benefiting from Technological Advancements and Green Aviation Initiatives

Europe holds a significant market share, supported by investments from leading aerospace firms focused on reducing emissions and improving aircraft efficiency. Collaborations between governments and industry players have been key to driving innovation in the region.

Asia Pacific Set to Grow at Fastest Pace Due to Civil Aviation Boom

The Asia Pacific region is projected to witness the highest CAGR due to increasing demand for civil aviation and regional fleet expansions in countries like China and India. Infrastructure development and rising disposable incomes are contributing to a flourishing aviation market and growing demand for reliable gearboxes.

Other Regions See Gradual Growth

The Middle East & Africa are experiencing modest growth through fleet expansion and investments in aviation infrastructure. Latin America, led by Brazil and Mexico, is seeing steady market recovery through a focus on MRO capabilities and aviation development.

Competitive Landscape:

Key Players Focus on Innovation, Contracts, and Partnerships to Strengthen Market Position

The aircraft gearbox market is competitive, with leading players investing heavily in R&D and strategic partnerships to meet evolving industry needs. Companies are also expanding product lines and entering long-term agreements to maintain market leadership.

Key Industry Developments:

- February 2025 – Bell Boeing received a USD 46 million contract for the integration and supply of V-22 Gearbox Vibration Monitoring/Osprey Drive System Safety and Health Information (ODSSHI) kits.

- August 2023 – Leonardo announced partnerships to support its AW09 helicopter at Heli-Expo 2023.

Sustainable Aviation Fuel Market Size, Growth Drivers and Opportunities 2025–2032

By Miyasingh, 2025-08-28

The global sustainable aviation fuel market size was valued at USD 1,845.2 million in 2024 and is projected to expand from USD 2,723.8 million in 2025 to USD 28,636.36 million by 2032, registering an impressive CAGR of 39.9% during the forecast period. North America led the market in 2024 with a 46% share, driven by strong policy support, airline commitments to net-zero targets, and significant investments in SAF production capacity.

Key Players:

- Neste (Finland)

- World Energy (U.S.)

- Gevo, Inc. (U.S.)

- Alder Fuels (U.S.)

- SkyNRG (Netherlands)

- Air BP (U.K.)

- Shell Aviation (Netherlands)

- TotalEnergies (France)

- Vitol Aviation (Switzerland)

- LanzaTech (U.S.)

- Fulcrum Bioenergy (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/sustainable-aviation-fuel-saf-market-111563

Segmentation: Sustainable Aviation Fuel Market

The sustainable aviation fuel market is segmented by type, technology, blending capacity, end use, application, and region. By type, the market is classified into biofuel and synthetic fuel. Based on technology, it includes HEFA-SPK (Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene), FT-SPK (Fischer-Tropsch Synthetic Paraffinic Kerosene), ATJ-SPK (Alcohol-to-Jet Synthetic Paraffinic Kerosene), and others. By blending capacity, the market is divided into 5–30%, 30–50%, and above 50%. In terms of end use, SAF is applied in commercial aviation, military aviation, and others, while by application it is used in fixed-wing and rotary-wing aircraft. Regionally, the market is segmented into North America (U.S. and Canada), Europe (UK, Germany, France, Russia, and Rest of Europe), Asia Pacific (China, Japan, India, South Korea, and Rest of Asia Pacific), and Rest of the World, which further includes Latin America and the Middle East & Africa.

Global Sustainable Aviation Fuel Market Key Takeaways:

- Market Size & Forecast

The global sustainable aviation fuel (SAF) market was valued at USD 1,845.2 million in 2024 and is projected to grow from USD 2,723.8 million in 2025 to USD 28,636.36 million by 2032 , at a robust CAGR of 9% during 2025–2032. - Market Share

In 2024, North America dominated the market with a 46% share , supported by strong policy frameworks, tax incentives, and initiatives such as the U.S. SAF Grand Challenge. By type, biofuel led the market due to its compatibility with current aircraft engines and fueling infrastructure. By technology, HEFA-SPK remained the leading pathway thanks to its maturity and flexibility in feedstock usage. By blending capacity, the 30–50% blend segment led in 2024 as airlines moved toward higher SAF utilization to meet sustainability targets. By end use, commercial aviation accounted for the largest share , driven by airline commitments to net-zero emissions. By application, fixed-wing aircraft dominated , supported by OEM adoption initiatives and favorable government subsidies. - Key Country Highlights

United States: Expansion supported by tax credits, ethanol-based SAF subsidies, and the SAF Grand Challenge targeting 3 billion gallons annually by 2030.

Canada: Air Canada signed a 60,000-ton SAF supply deal with Neste in 2024 to meet its 1% SAF blending goal by 2025.

United Kingdom: Announced a 2% SAF blending mandate from 2025 under its decarbonization roadmap.

Germany: Deutsche Aircraft successfully tested a 100% Fischer-Tropsch synthetic fuel flight , advancing certification efforts.

France: TotalEnergies secured a 5 million ton SAF supply agreement with Air France-KLM through 2035.

China: Completed its first 40% SAF blend helicopter flight in 2023 , underscoring Asia’s growing adoption.

Brazil: Enacted the “Fuel of the Future” law in 2024 to promote SAF use and strengthen its role in aviation decarbonization.

South Africa: IATA identified potential production capacity of 3.2–4.5 billion liters annually from biomass and sugarcane residues.

Report Coverage:

The report has conducted a detailed study of the market and highlighted several critical areas, such as leading types, technologies, applications, and prominent market players. It has also focused on the latest market trends and the key industry developments. Apart from the aforementioned factors, the report has given information on many other factors that have helped the market grow.

Drivers and Restraints:

Increasing Demand for Alternative Fuels to Boost Product Adoption

Industries across the world, including aviation, are becoming aware of the harmful effects of using fossil fuels on the environment, such as global warming and climate change. This factor has prompted them to take various measures to reduce their greenhouse gas emissions and make their business operations eco-friendlier. This is expected to fuel the adoption of Sustainable Aviation Fuel (SAF) in the aviation sector as this fuel has the potential to decrease emissions by nearly 80%, depending on the production technique and type of feedstock used. This can make the aviation industry more sustainable in its operations.

However, high cost and limited availability of feedstock can hinder the Sustainable Aviation Fuel (SAF) market growth.

Regional Insights:

North America Dominated Global Market Owing to Implementation of Strict Environmental Regulations

North America held the biggest sustainable aviation fuel market share in 2024 and might retain its dominance during the forecast period as well as governments across the region have imposed several stringent environmental regulations to reduce their carbon emissions. They have also formulated various policies to support the adoption of cleaner fuels in various industries.

Europe is also increasing its reliance on Sustainable Aviation Fuel (SAF) owing to the strict regulations imposed by the governments to decrease the carbon emissions of its industries, including aviation.

Competitive Landscape:

Market Players to Focus On Launch of Innovative Fuels to Cater to Wider Audience

Some of the top companies driving the global Sustainable Aviation Fuel (SAF) market growth are focusing on developing and launching a wide range of eco-friendly fuels for different industries. They are increasing their investments in research & development programs to find out about the latest technologies and use them to manufacture SAF.

Notable Industry Development:

September 2024- TotalEnergies signed an agreement with Air France-KLM to help the former deliver around 1.5 million tons of Sustainable Aviation Fuel (SAF) over a period of 10 years until 2035. This deal was one of the biggest SAF purchase agreements for Air France-KLM to date. It strengthened the airline’s dominance in the use of SAF, accounting for 17% and 16% of the global SAF production in 2022 and 2023, respectively.

The global on-orbit services market was valued at USD 2,332.6 million in 2023 and is expected to grow from USD 2,547.2 million in 2024 to USD 5,897.6 million by 2032, registering a CAGR of 11.1% during the forecast period.

North America led the market in 2023 with a 45.95% share, supported by the presence of major commercial players, advanced servicing infrastructure, and strong government backing. By service type, the life extension segment accounted for the largest share in 2023, driven by rising demand for cost-effective satellite mission prolongation. Country-wise, the United States dominates with leading companies like Northrop Grumman and Orbit Fab supported by government and defense contracts, while China is advancing rapidly in satellite servicing technology with both commercial and military ambitions. Russia continues investment in satellite servicing despite sanctions, focused on defense and national security. India is expanding capabilities through ISRO’s initiatives and private sector participation, while Japan invests heavily in debris removal and refueling technologies. In Europe, France is driving collaborations under ESA to enhance life extension and de-orbiting systems, and the UK strengthens its position through investments in startups such as Astroscale for debris mitigation and satellite repair.

On-Orbit Services Market Key Players

Several companies are actively shaping the on-orbit services landscape. Leading organizations include:

- Airbus S.A.S (Netherlands)

- Thales Alenia Space (France)

- Lockheed Martin Corporation (U.S.)

- Orbit Fab (U.S.)

- Astroscale (Japan)

- ClearSpace SA (Switzerland)

- Obruta Space Solutions Corp. (Canada)

- D-Orbit SpA (Italy)

- Maxar Technologies (U.S.)

- Eta Space (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/on-orbit-services-market-108399

Market Segmentation

The on-orbit services market is segmented by end-user, orbit, satellite type, service, and solution. Among end-users, the military & government segment is growing rapidly due to investments from agencies like NASA and ESA, while the commercial & civil segment dominated in 2023. By orbit, Low Earth Orbit (LEO) held the largest share owing to increased small satellite deployments, whereas Geostationary Orbit (GEO) is expected to grow at the fastest pace as aging satellites require servicing. In terms of satellite type, Earth observation satellites led the market, while the space science segment is projected to grow fastest due to the critical nature of scientific missions. By service, refueling dominated and is anticipated to continue its strong growth, supported by cost-saving benefits and extended satellite lifespan. Lastly, robotic teleoperated solutions led in 2023 due to precision handling, while robotic autonomous systems are set to expand quickly with advancements in AI and visual perception technologies.

Regional Insights

North America

North America led the on-orbit services market in 2023, holding a dominant market share of 45.95%. The presence of major space companies, robust government funding, and increasing private sector participation have propelled growth in this region.

Europe

Europe is witnessing steady growth due to advancements in satellite servicing technologies and collaborations between government agencies and private firms.

Asia-Pacific

Countries like Japan and China are investing heavily in space missions, driving demand for on-orbit services in this region.

Rest of the World

Other regions, including the Middle East and Africa, are slowly entering the market, focusing on satellite-based communication and Earth observation initiatives.

Industry Developments:

December 2024 – Thales Alenia Space, a joint venture between Thales and Leonardo, signed a first-phase contract valued at €25 million (USD 26.09 million) with the European Space Agency (ESA) to develop and demonstrate a complete cargo delivery service to and from space stations in low-Earth orbit (LEO) by 2028. The company will co-lead the development of this innovative LEO Cargo Return Service, marking a key step toward commercial space logistics.

December 2023 – Rogue Space Systems Corporation, a provider of space situational awareness and satellite servicing solutions, announced its upcoming mission to locate and communicate with a customer’s satellite following its deployment from SpaceX's Transporter-9 mission. The operation will involve establishing contact and initiating in-orbit servicing tasks, supporting the customer’s satellite functionality and mission objectives.

Future Outlook

The on-orbit services market is poised for rapid expansion due to technological innovations, increasing satellite deployments, and the growing need for sustainable space operations. Companies are focusing on automation, AI-powered diagnostics, and in-orbit manufacturing to revolutionize the industry. As demand for satellite servicing rises, the sector is expected to witness increased investments, partnerships, and policy developments, shaping the future of space sustainability.

The global small satellite market size was valued at USD 11.41 billion in 2024 and is expected to increase from USD 14.21 billion in 2025 to USD 19.67 billion by 2032, registering a CAGR of 4.8% during the forecast period. North America dominated the market in 2024 with a 49.17% revenue share, supported by substantial investments and the strong presence of leading industry players in the region.

North America dominated with a 49.17% share in 2024, supported by broadband initiatives, government funding, and private sector contributions from SpaceX, OneWeb, and Amazon’s Kuiper. By application, communication is expected to be the fastest-growing segment, driven by rising demand for high-speed internet in underserved areas and the rollout of large LEO constellations. The United States leads global deployment, with investments from programs like Starlink and NASA’s satellite contracts, while India is emerging as a key manufacturing and launch hub, with companies such as Azista BST ramping up production. The United Kingdom is spearheading European growth through ESA-backed initiatives like Open Cosmos, and China is expanding rapidly in communication, Earth observation, and defense applications under government-led space programs. Meanwhile, the UAE is strengthening its role with satellite investments focused on civil and defense uses in collaboration with international partners.

Leading Players Featured in the Research Report:

- Airbus S.A.S. (Netherlands)

- The Boeing Company (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Sierra Nevada Corporation (U.S.)

- ST Engineering (Singapore)

- Thales Group (France)

- SpaceX (U.S.)

- L3Harries Technologies (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/industry-reports/small-satellite-market-101917

Segmentation:

The global small satellite market is segmented by application into communication, navigation, Earth observation, and others; by component into telemetry, tracking and command (TT&C), power systems (solar panels and battery backup), propulsion systems, command & data handling (C&DH), and others; and by type into minisatellites, microsatellites, nanosatellites, and picosatellites. Based on end-use, the market is categorized into civil, military, and commercial sectors. Regionally, the market covers North America (by component, weight, application, and end-use) with detailed analysis of the U.S. and Canada by application; Europe (by component, weight, application, and end-use) with insights on the U.K., Germany, France, Russia, and the rest of Europe by application; Asia Pacific (by component, weight, application, and end-use) including China, India, Japan, and the rest of Asia Pacific by application; and the Rest of the World (by component, weight, application, and end-use) comprising the Middle East & Africa and Latin America by application.

Report Coverage:

The report provides an analysis of the prominent trends driving the global industry landscape. It further gives an account of the key steps and initiatives undertaken by leading market participants for strengthening their industry position. Some of these steps include merger agreements, acquisitions, and the launch of new products.

Drivers and Restraints:

Rise in Market Value Owing to Surging Development of Launch Vehicles

One of the key factors propelling the small satellite market growth is the increasing development of small launch vehicles. The industry expansion is propelled by the lower cost of SLVs and shorter production time.

However, the industry expansion is likely to be hindered on account of short lifespan and the limitations of weight and size.

Regional Insights:

North America to Depict Substantial Growth Driven by Various Upcoming and Ongoing Projects

The North America small satellite market share is poised to grow at a commendable pace over the projected period. The rise is driven by an increase in the range of upcoming and ongoing projects.

The Europe market is expected to depict moderate growth throughout the study period. The surge is impelled by a range of smallsats for earth observation and military applications.

Competitive Landscape:

Leading Companies Form Joint Ventures to Secure Competitive Edge

Major small satellite industry players are formulating and implementing a range of strategic initiatives for the consolidation of their position in the market. Some of these initiatives include acquisitions, merger agreements, joint ventures, and the rollout of new products. Additional steps include an increase in research activities.

Key Industry Development:

November 2022 – The Indian Space Research Organization launched an earth observation satellite in addition to 8 nanosatellites. The purpose of these nanosatellites was technology demonstration and optical imaging.

The global LEO satellite market size was valued at USD 7.71 billion in 2024 and is projected to reach USD 11.53 billion by 2032, growing from USD 7.93 billion in 2025 at a CAGR of 5.5% during the forecast period. North America led the market in 2024 with a 38.91% share.

Market growth is primarily fueled by the increasing demand for high-speed communication, Earth observation, and global connectivity. Positioned closer to Earth than traditional satellites, LEO satellites provide significant advantages, including lower latency and faster data transmission. These features make them highly suitable for applications such as broadband internet, disaster management, navigation, and defense operations.

GLOBAL LEO SATELLITE MARKET OVERVIEW

North America dominated with a 38.91% share in 2024, supported by significant investments in satellite infrastructure, defense applications, and large-scale constellations such as Starlink and Project Kuiper. By type, small satellites led the market due to lower launch costs and shorter development cycles, while by application, communication emerged as the largest segment, fueled by growing broadband and mobile connectivity needs in remote regions. On an end-use basis, the commercial sector held the leading share, supported by expanding IoT networks, satellite imaging, and navigation services. The United States remains the global leader, with strong participation from major players like SpaceX, Amazon, and Lockheed Martin, alongside substantial defense and commercial satellite investments.

Information Source:

https://www.fortunebusinessinsights.com/leo-satellite-market-112113

List of Key Players Mentioned in the Report:

- SpaceX (U.S.)

- Airbus Defense and Space (Germany)

- Lockheed Martin (U.S.)

- OneWeb (U.K.)

- Boeing (U.S.)

- Planet Labs Inc. (U.S.)

- Spire Global Inc. (U.S.)

- Iridium Communications Inc. (U.S.)

- Swarm Technologies (U.S.)

- GomSpace (Denmark)

Segmentation:

The global LEO satellite market is segmented by type, application, end use, and region. By type, the market is categorized into small, medium, and large satellites. In terms of application, it includes communication, Earth observation, navigation, scientific research, and others. By end use, the market is divided into government and military, and commercial sectors. Regionally, the market is analyzed across North America (U.S. and Canada), Europe (U.K., Germany, France, Russia, and the Rest of Europe), Asia Pacific (China, India, Japan, South Korea, and the Rest of Asia Pacific), and the Rest of the World, which includes Latin America and the Middle East & Africa. Each regional segment is further assessed by type, application, and end use to provide comprehensive market insights.

Report Coverage:

The global LEO satellite market report offers an in-depth analysis of market size, forecasts, and segmentation by application, end use, and type. It explores market trends, competition, product pricing, and key developments that have influenced the global market growth.

Drivers and Restraints: LEO Satellite Market

Rise of Small Satellites Constellations and Incorporation of Advanced Technologies to Bolster Market Growth

The launch of 2,402 small satellites in 2022 highlights the growing trend of adopting cost-effective and interconnected satellites. These systems enable extensive constellations that enhance global coverage and connectivity, meeting rising data and connectivity demands. Moreover, LEO satellite systems are becoming increasingly sophisticated, utilizing AI and machine learning to improve operational efficiency, lower costs, and provide low-latency solutions, further accelerating product adoption.

However, stringent regulations for satellite coordination and management can drive up operational costs and add complexity to satellite deployment, deterring LEO satellite market growth.

Regional Insights: LEO Satellite Market Size

North America to Dominate the Market Owing to Strong Investment in Satellite Systems

North America leads the LEO satellite market size with significant investments aimed at improving border surveillance, missile tracking capabilities, and national security. Leading companies such as Amazon, SpaceX, and Boeing are rapidly advancing satellite production and deployment, including Amazon’s Project Kuiper, which aims to produce over 3,000 satellites for enhanced global connectivity in July 2024.

The Asia Pacific region is benefitting from ongoing progress in spaceflight technology and launch systems, which supports the growth of the market. In August 2024, China’s plans to launch LEO satellites for its megaconstellation backed to a significant contract with the NRO, are set to enhance satellite infrastructure and global connectivity.

Competitive Landscape-

Key Players Focus on Mergers and Acquisitions to Sustain their Market Growth

Market leaders are focusing on advancing their product offerings by investing in R&D and developing diverse solutions. They are leveraging mergers, acquisitions, and new product launches to sustain their growth. Additionally, heavy investments in satellite networks are driving the push for global connectivity.

Key Industry Development:

May 2024 - The Ministry of Science and ICT in South Korea announced a USD 234.4 million project to launch two LEO satellites by 2030, leveraging 6G communication technology for advanced satellite-based connectivity.

The global cargo drone market size was valued at USD 1.15 billion in 2024 and is projected to grow from USD 1.82 billion in 2025 to USD 33.79 billion by 2032, registering a CAGR of 51.8% during the forecast period. In 2024, North America led the market, accounting for a 42.61% share.

North America led the market with a 42.61% share in 2024, driven by strong regulatory support, technological innovation, and investments in drone logistics. Rotary wing drones are expected to retain the largest share in 2025 due to their simplicity, affordability, and adaptability for urban deliveries. Key countries include the U.S., benefiting from FAA regulations, defense spending, and manufacturer partnerships; India, with growing demand supported by drones like CargoMax 20KHC; Germany, leading European innovation through companies like Volocopter and government-funded advanced air mobility projects; UAE, establishing air corridors and regulations for autonomous cargo operations; and the U.K., where firms like Dronamics are pioneering cross-border drone logistics.

List of Key Companies Profiled

- DJI (China)

- Parrot SA (France)

- Natilus (U.S.)

- Dronamics (U.K.)

- Silent Arrow (U.S.)

- Sabrewing Aircraft Company (U.S.)

- Elroy Air (U.S.)

- Volocopter GmbH (Germany)

- Dufour Aerospace (Switzerland)

- H3 Dynamics (Singapore)

- Bell Textron Inc. (U.S.)

- Kaman Corporation (U.S.)

- Airbus (Netherlands)

- Elbit Systems (Israel)

- Israel Aerospace Industries (IAI) (Israel)

Information Source:

https://www.fortunebusinessinsights.com/cargo-drones-market-108151

Cargo Drones Market Drivers and Opportunities

Growth of E-Commerce and On-Demand Delivery Services

The boom in global e-commerce and expectations of faster delivery are fueling the adoption of cargo drones. Major retailers and logistics firms are exploring drone-based delivery systems to enhance operational efficiency and reduce reliance on ground transport in congested areas.

Technological Advancements and Automation

Advancements in VTOL design, battery technology, AI-powered navigation, and lightweight materials are making drones more capable and cost-efficient. Semi and fully autonomous systems are becoming viable for cargo missions over varying distances and terrains.

Regulatory Support and Infrastructure Development

Governments are increasingly supportive of drone logistics, developing regulatory frameworks, test corridors, and UAS traffic management systems. Strategic partnerships with logistics companies, tech firms, and municipal bodies are enabling pilot programs and ecosystem building.

Segmentation Analysis

The drone logistics and transportation market is segmented by several key categories. By type, it includes fixed-wing, hybrid, and rotary-wing drones. Based on automation level, it is classified into fully autonomous, semi-autonomous, and remotely controlled systems. By range, drones are segmented into very short, short, medium, and long range. Payload capacity ranges from featherweight and lightweight to middleweight and heavy-lift categories. By component, the market includes cameras, sensors, equipment, and delivery packages. Applications are primarily divided into commercial cargo and military cargo. End-user industries span across e-commerce, construction, government and defense organizations, healthcare, and offshore & energy sectors.

Regional Insights

North America: Leading the market in 2024, driven by strong government funding, defense logistics integration, and FAA-backed commercial drone programs.

Europe: Focused on eco-friendly and humanitarian drone use, with players like Dronamics and Airbus developing heavy-lift cargo solutions.

Regional Insights

North America : Leading the market in 2024, driven by strong government funding, defense logistics integration, and FAA-backed commercial drone programs.

Europe : Focused on eco-friendly and humanitarian drone use, with players like Dronamics and Airbus developing heavy-lift cargo solutions.

Asia Pacific : Rapid growth fueled by urbanization, booming e-commerce, and smart city initiatives in China, India, and Southeast Asia.

Rapid growth fueled by urbanization, booming e-commerce, and smart city initiatives in China, India, and Southeast Asia.Competitive Landscape

Innovation and Strategic Alliances Drive Market Dynamics

Leading cargo drone manufacturers are prioritizing R&D, prototype testing, and regulatory approvals. Collaborations with logistics providers, technology developers, and defense agencies are enabling scalable deployments. M&A activity is on the rise as companies race to develop versatile, payload-optimized platforms.

Report Coverage

The global cargo drone market report offers a deep dive into industry dynamics, including market size, segmentation by platform type, range, payload, automation, and end-user industry. It features key trends, pricing and cost analysis, competitive benchmarking, innovation pipelines, and regulatory landscapes. Regional and country-level forecasts, as well as insights into R&D investments and emerging opportunities, are comprehensively covered.

Key Industry Developments

- April 2025 – Piasecki Aircraft acquired Kaman Air Vehicles’ Kargo UAV to expand its portfolio and accelerate the commercialization of autonomous aerial logistics. The production-ready model is expected by 2026.

AI in Aviation Market Size, Growth Opportunities, and Global Forecast 2025–2032

By Miyasingh, 2025-08-26

The global AI in aviation market size was valued at USD 6,200.0 million in 2024 and is expected to grow from USD 7,449.3 million in 2025 to USD 26,997.6 million by 2032, registering a CAGR of 20.20% during the forecast period. In 2024, North America led the market, accounting for a 46.19% share.

North America led the market with a 46.19% share in 2024, supported by strong technology infrastructure, early adoption by airlines and airports, and collaborations with tech companies. Flight operations emerged as the leading application segment, driven by AI-enabled predictive maintenance, real-time aircraft health monitoring, and fuel optimization. Country-wise, the U.S. is advancing with predictive maintenance, biometric check-ins, and AI-based route optimization; China is expanding rapidly through smart airport initiatives, tech partnerships, and government investment in AI-powered systems; India is integrating AI through DigiYatra and other modernization programs in passenger management, logistics, and energy optimization; while Germany is adopting AI under the European Green Deal to reduce emissions, optimize flight paths, and enhance digital air traffic management in line with EU regulations.

List of Key Players Mentioned in the Report:

- Intel Corporation (U.S.)

- IBM Corporation (U.S.)

- Airbus S.A.S. (Netherlands)

- Thales Group (France)

- Lockheed Martin Corporation (U.S.)

- General Electric Company (U.S.)

- The Boeing Company (U.S.)

- Garmin Ltd. (U.S.)

- Northrop Grumman Corporation (U.S.)

- Honeywell International Inc. (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/ai-in-aviation-market-113289

Segmentation Highlights:

The global AI in aviation market is segmented by application, offering, technology, end user, and region. By application, the market is categorized into flight operations, maintenance, air traffic management, and others. In terms of offering, it includes software, hardware, and service. Based on technology, the segmentation covers machine learning, computer vision, data analytics, and others. By end user, the market comprises airlines, airports, OEMs, and MROs. Regionally, the market is analyzed across North America (U.S. and Canada), Europe (U.K., Germany, France, Russia, and Rest of Europe), Asia Pacific (China, Japan, India, South Korea, and Rest of Asia Pacific), and the Rest of the World, which includes Latin America and the Middle East & Africa. Each region is further examined based on application, offering, technology, and end user.

Market Dynamics:

Drivers:

Operational Efficiency and Automation to Bolster Market Growth

AI’s growing role in optimizing air traffic management and flight route planning is a key driver. AI algorithms and machine learning systems are improving decision-making and enabling real-time adjustments in response to changing weather, airspace congestion, and fuel efficiency demands.

For example, in April 2025 , Alaska Airlines reported saving 480,000 gallons of jet fuel in six months by using an AI-powered flight route optimizer, showcasing AI’s ability to enhance sustainability and operational savings.

Post-Pandemic Digital Acceleration and Passenger Experience Enhancements

Post-COVID digital transformation has fast-tracked AI implementation across passenger-facing services, including biometric boarding, baggage tracking, and chatbots for customer engagement. Airports and airlines alike are prioritizing seamless, contactless experiences that AI can deliver.

Restraints:

Data Security and Privacy Concerns May Restrict Market Expansion

The integration of AI in aviation raises concerns around data privacy, cybersecurity, and compliance with international data regulations , especially with AI systems processing sensitive operational and passenger data. These challenges may hinder adoption, particularly in regions with stringent privacy laws.

Regional Insights:

North America to Maintain Dominance

North America is expected to lead the global AI in aviation market throughout the forecast period. The region benefits from early adoption of AI technologies, the presence of leading aerospace companies, and high investments in AI-enabled aviation platforms. Strategic collaborations between AI firms and aviation authorities further bolster growth.

Asia Pacific to Register the Fastest Growth

Asia Pacific is anticipated to witness the highest CAGR over the forecast period, driven by rising air passenger traffic , rapid airport modernization , and the growing presence of budget airlines. Countries like China , India , and Singapore are at the forefront of integrating AI into smart airport operations and traffic control systems.

Competitive Landscape:

Companies Focusing on AI Innovation and Aviation-Specific Solutions

Market leaders are investing heavily in developing tailored AI solutions for aviation. Strategies include partnerships with aviation regulatory bodies, collaborations with AI startups, and deployment of cloud-based analytics platforms for predictive and prescriptive intelligence.

Key Industry Developments:

-

March 2025 – The Federal Aviation Administration (FAA) awarded an $80,000 contract titled “ Azure OpenAI CDO ” to develop AI-driven aviation solutions leveraging OpenAI’s models via Microsoft Azure , signaling growing government interest in AI adoption.

-

October 2024 – Thales Group partnered with SITA to enhance air traffic management through real-time AI analytics, focusing on flight delay reduction and improved situational awareness.

Agriculture Drone Market Size, Emerging Trends & Investment Opportunities 2024–2032

By Miyasingh, 2025-08-26

The global agriculture drone market size was valued at USD 4.98 billion in 2023 and is expected to rise from USD 6.10 billion in 2024 to USD 23.78 billion by 2032, registering a CAGR of 18.5% during the forecast period. In 2023, Europe led the market, accounting for a 30.52% share.

Global Agriculture Drone Market Overview

The global agriculture drone market was valued at USD 4.98 billion in 2023 and is projected to grow from USD 6.10 billion in 2024 to USD 23.78 billion by 2032, registering a CAGR of 18.5% during the forecast period. Europe dominated the market with a 30.52% share in 2023, driven by strong R&D capabilities, funding support, and the rise of agri-tech startups such as Delair and Gamaya. By offering, hardware leads the market due to its ability to collect and process vast agricultural data, while by payload capacity, medium-weight drones (10–25 kg) dominate, supporting crop monitoring, spraying, and sowing applications. Monitoring and mapping remain the largest application segment, enabling farmers to detect crop stress and field variability with advanced imaging. Country-wise, the U.S. market benefits from USDA and FAA support and regulatory relaxations under Part 107, while China remains a leading innovator and exporter with companies like DJI launching advanced models such as Agras T50 and T25. France fosters UAV innovation in precision farming through R&D incentives and startups like Parrot and Delair, whereas the UAE leads the Middle East in drone adoption for food security and environmental monitoring initiatives.

Information Source:

https://www.fortunebusinessinsights.com/agriculture-drones-market-102589

List of Key Players Mentioned in the Report:

- Drone Deploy (U.S.)

- DJI (China)

- Precision Hawk Inc (U.S.)

- AeroVironment Inc. (U.S.)

- Trimble Navigation Ltd. (U.S.)

- 3D Robotics (U.S.)

- Ag Eagle (U.S.)

- Parrot Drone (France)

- Sintera LLC (U.S.)

- Delair Tech SAS (France)

Segmentation: Agriculture Drone Market Size

Rotary Drone Segment to Dominate Due to Improved Structural Benefits

Based on type, the market is split into fixed wing, rotary wing, and hybrid. Among these, the rotary wing segment captured the largest agriculture drone market share in 2022. Rotary wing drones are available in a variety of designs and sizes. The enhanced structural benefits of the segment are aiding growth of this segment.

Hardware Segment to Lead Stoked by the Improved Ability to Collect and Process Data

As per component, the agriculture drone market is bifurcated into hardware and software. The hardware segment held majority of the global market share in 2022 owing to the improved capability of hardware components to collect and process the data and enable farmers to make informed decisions.

Frames Segment to Hold Major Share Due to Surging Demand for Robust Frame Structures

According to hardware, the market is divided into frames, control systems, propulsion systems, navigation systems, payload, avionics and others. Among these, the frame segment captured a significant market share in 2022 backed by the rising need for robust frames to support the drone’s hardware components, Moreover, industry leaders are focused on producing non-breakable frames, further aiding segment growth.

Imaging Software Segment to Capture Largest Share Due to its Ability to Help in Quick Problem Solving

The market by software is arrayed into imaging software, data management software, data analytics software, and others. Imaging software segment held the largest market share in 2022 as it enables the operator to detect and respond to the potential problems early, thus decreasing the risk of crop loss and improving yields.

Field Mapping & Monitoring Segment to Lead Due to Availability of Better Equipment

By application, the agriculture drone market size is segregated into field mapping & monitoring, crop spraying, crop scouting, variable rate application, livestock monitoring, and others. The field mapping & monitoring segment dominated the market in 2022 owing to the availability of better high-tech camera equipment to monitor crops.

Geographically, the market is segregated North America, Europe, Asia Pacific, and the Rest of the World.

Report Coverage:

The report includes:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major agriculture drone industry players.

- Key strategies adopted by the agriculture drone market

- Recent industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers and Restraints:

Rising Support by Various Governments for Agriculture Drones to Propel Market Expansion

Governments across the world are announcing several policies and initiatives to support agriculture drone adoption. This includes R&D grants, tax incentives, subsides, regulatory frameworks, training and education, and others. For instance, in April 2022, the U.S. Department of Agriculture received a grant for USD 1 million for innovations in digital agriculture. By providing regulatory and financial support, governments are helping to make UAVs more accessible to farmers while also ensuring that they are used in a safe and responsible way.

On the other hand, concerns regarding data overload and inaccuracies in collected data due to hardware or software issues and environmental factors will pose as challenges for businesses operating in this domain.

Regional Insights:

Europe to Hold Largest Share Backed by Strong Research and Development Facilities

Europe captured a significant global agriculture drone market share in 2022 owing to the surging demand for the drones, rising funding, and strong research and development capabilities of the region. Moreover, the growing number of startups such as Gamaya, Delair, Accelerated Dynamics, and others will further aid regional market expansion.

Meanwhile, Asia Pacific is projected to record the highest growth rate in the forecast timeframe due to presence of large agricultural countries such as India, Indonesia, China, and others. The rising demand for UAVs from these countries and growing focus of market players on developing advanced products will further facilitate regional market expansion.

Competitive Landscape:

Innovative Product Launches by Leading Companies to Drive Market Expansion

Industry leaders usually make tactical moves such as collaborations, partnerships, mergers and acquisitions, and product launches to hold a dominant share in the global market. For example, in November 2021, XAG announced its plans to launch its P40 and V40 agricultural drones worldwide, thus bringing digital agriculture to rural areas with geriatric populations and poor infrastructure. The XAG V40 and P40 are fully autonomous drones capable of mapping, spraying, and farm broadcasting.

Key Industry Development:

March 2023 – Avikus and Korea Shipbuilding & Offshore Engineering, a subsidiary of Hyundai, entered into an agreement to carry out an experiment on fuel efficiency by implementing self-governing navigation systems. The venture incorporates five firms, Pan Ocean, POS SM, Korea Shipbuilding & Offshore Engineering, Avikus, and Korean Register of Shipping.