According to Fortune Business Insights™, the global marine vessel market size was valued at USD 152.38 billion in 2023 and is projected to grow from USD 160.56 billion in 2024 to USD 247.96 billion by 2032, exhibiting a CAGR of 5.6% during the forecast period. Asia Pacific dominated the market in 2023, accounting for 52.46% of the global share.

Market Overview

Marine vessels are essential for global trade and transportation, serving as the backbone for cargo and passenger movement across international waters. The sector is experiencing growth driven by increasing seaborne trade, technological advancements, and strong government support for domestic shipbuilding industries. Although the COVID-19 pandemic caused a temporary decline in shipping activities, long-term demand remains strong due to globalization and industrialization.

Shipbuilding, an industry with high capital intensity, plays a critical role in the market. Governments worldwide are investing in indigenous shipbuilding programs, ensuring political and economic stability in the sector.

Growth Factors

1. Rising International Maritime Trade

Maritime transport plays a critical role in sustaining global supply chains, as nearly 90% of world trade volume moves by sea. It remains the most cost-effective and environmentally friendly mode of transporting large quantities of goods across borders, producing significantly lower carbon emissions than road or air freight. According to UNCTAD, over 11 billion tons of goods were shipped in 2019, highlighting the immense scale of seaborne trade. Even during economic slowdowns, demand for crude oil, ores, coal, steel, agricultural produce, and finished goods such as motor vehicles continues to push marine transportation forward. This growing trade volume directly increases the demand for tankers, cargo ships, bulk carriers, and specialized vessels, which in turn fuels the global shipbuilding sector. Shipyards across Asia, particularly in China, Japan, and South Korea, have been witnessing record-breaking orders for new vessels, supported by both commercial operators and government-backed initiatives to modernize fleets.

2. Expansion of Trade-related Agreements

The increasing number of trade-related agreements between developed and developing economies has become another major driver for the marine vessel market. Free Trade Agreements (FTAs) and regional trade blocs help reduce or eliminate customs duties, streamline border checks, and simplify compliance procedures, which makes waterborne trade more attractive and efficient. This shift has encouraged suppliers and exporters to rely more on containerized cargo and bulk shipping routes, stimulating demand for larger and technologically advanced vessels. Moreover, the post-pandemic recovery has accelerated global trade flows, particularly in energy, raw materials, and consumer goods, driving up marine cargo movements. A key example is India’s participation in multilateral trade negotiations in September 2022, aimed at expanding export markets and improving access to critical imports like natural resources and intermediate goods. Similar initiatives across Asia-Pacific, Europe, and Latin America are creating favorable conditions for shipbuilding, as cargo operators seek to upgrade fleets with better fuel efficiency, digitalized operations, and compliance with stricter environmental regulations.

Restraining Factors

1. High Costs of Development and Maintenance

The construction of modern marine vessels demands substantial capital investment, as they are equipped with advanced propulsion systems, navigation technologies, communication modules, and integrated control systems. These components, while enhancing efficiency and compliance with global maritime regulations, significantly increase the initial cost of vessel development. Furthermore, the maintenance of these ships adds to the financial burden on operators. For older vessels, maintenance costs can account for 25% to 30% of total operational expenses, compared to around 10% for newer fleets. Rising costs are linked to unforeseen repairs, unavailability of spare parts, and the need for skilled technicians. This makes it difficult for smaller operators to remain competitive. Without proper maintenance planning and lifecycle cost management, expenses escalate quickly, limiting profitability and deterring new ship investments.

2. Rapid Technological Changes

The fast-paced evolution of marine technologies poses another major challenge for shipowners. The industry is under constant pressure to adopt innovations in propulsion, navigation, and environmental compliance systems, such as hybrid engines, LNG-powered systems, and digitalized monitoring platforms. While these upgrades improve operational efficiency and reduce emissions, they also result in frequent system overhauls, retrofits, and training requirements for crew members. This leads to higher operational costs and shorter technology cycles, forcing owners to spend more on modernization than anticipated. For example, new regulations such as the IMO 2023 GHG emission standards require ships to integrate energy efficiency and carbon reduction technologies, which demand heavy investments. Such rapid technological shifts place a financial strain on operators and shipbuilders, particularly in emerging markets.

Information Source:

https://www.fortunebusinessinsights.com/marine-vessel-market-102699

Market Trends

Digital Transformation in Shipbuilding

-

Adoption of IoT, robotics, 3D printing, smart ship solutions, and hybrid propulsion systems is reshaping ship design and construction.

-

Example: In July 2022, French LNG containment specialist GTT signed a contract to equip more than 30 LNG vessels with its GTT Digital smart shipping solution to optimize energy efficiency and environmental performance.

Segmentation Analysis

By Ship Type

In 2023, container ships accounted for the largest market share and are projected to remain the fastest-growing segment during the forecast period. The expansion of global e-commerce, rising seaborne trade, and increasing demand for efficient cargo handling systems are driving this growth. Container vessels are also adopting digitalized tracking systems and eco-friendly propulsion to meet stringent IMO environmental standards. For instance, in April 2023, China State Shipbuilding Corporation (CSSC) and CMA CGM signed a USD 3.06 billion contract to build 16 advanced container ships, reflecting industry confidence in containerized trade. Bulk carriers represented the second-fastest growing segment, driven by demand for transporting grains, coal, and ores. Industrial expansion and energy requirements in Asia-Pacific are further boosting demand for bulk shipping. In June 2023, Mitsui O.S.K. Lines announced a dual-fuel bulk carrier project equipped with LNG propulsion capabilities, showcasing the industry’s shift toward sustainable solutions.

By Dead Weight (DWT)

Ships ranging between 25,000 GT and 59,999 GT are expected to grow at the fastest pace, supported by increasing demand for chemical tankers and medium-sized container ships. These vessels provide flexibility in transporting specialized cargo, making them highly suitable for niche shipping requirements. Meanwhile, vessels above 60,000 GT dominated the market in 2023, largely due to their extensive use as bulk carriers and liquefied gas carriers. Global LNG and LPG transportation continues to rise, particularly across Asia and Europe, which is expected to sustain the dominance of this category.

By System

The propulsion system segment held the largest share in 2023 and is projected to grow at the fastest pace, primarily due to decarbonization initiatives such as the Carbon Intensity Indicator (CII) and IMO 2050 carbon-neutral goals. Shipowners are increasingly investing in dual-fuel engines, LNG-powered propulsion, and hybrid-electric solutions to reduce emissions and optimize fuel consumption. On the other hand, the deck machinery segment emerged as the second-fastest growing category, supported by the integration of automated mooring systems, advanced winches, and hybrid vessel applications that improve efficiency and reduce crew workload.

By Solution

Line-fit solutions dominated the market in 2023 and are anticipated to expand at the highest rate throughout the forecast period, driven by rising indigenous shipbuilding programs and large-scale contracts for new vessel construction. For example, in April 2023, CMA CGM and CSSC signed a USD 3.06 billion deal to build 21 container ships, underscoring the momentum in line-fit demand. Retrofit solutions are also gaining traction, supported by modernization efforts to extend the service life of vessels while meeting new regulatory standards. IMO 2023 greenhouse gas (GHG) emission regulations are compelling shipowners to retrofit older fleets with scrubbers, LNG propulsion, and hybrid systems.

Regional Insights

Asia Pacific

Asia Pacific emerged as the largest market in 2023, valued at USD 79.94 billion. The region’s dominance is reinforced by countries such as China, Japan, and South Korea, which together account for nearly 94% of global shipbuilding output (UNCTAD, 2021). Strong domestic demand, extensive shipbuilding infrastructure, and government-backed innovation in green shipping technologies continue to drive the region’s leadership.

Europe

Europe is the second-fastest growing market, supported by rising investments in LNG carriers and advanced ship designs. European shipbuilders are at the forefront of sustainable maritime solutions, focusing on low-emission propulsion systems and automation technologies that align with the region’s strict environmental regulations.

North America

North America is projected to record significant growth, largely driven by U.S. federal investments in next-generation naval and commercial vessels. The focus on modernizing naval fleets and developing eco-efficient ships is expected to strengthen the region’s position in the global marine vessel market.

Latin America

Latin America’s growth is primarily supported by hybrid vessel upgrades and modernization of offshore fleets. A notable example is the 2020 partnership between Wärtsilä and CBO, which involved retrofitting offshore support vessels with hybrid propulsion systems, reducing emissions while improving operational efficiency.

Middle East & Africa

The Middle East & Africa is witnessing market expansion through fleet acquisitions and maritime infrastructure investments. In 2023, for example, AD Ports Group enhanced its shipping capabilities by acquiring five bulk carriers, signaling the region’s growing focus on strengthening trade and logistics capacity.

Key Industry Players

The market is fragmented, with major players focusing on M&A, partnerships, and advanced technologies.

- BAE Systems (U.K.)

- Mazagon Dock Shipbuilders Limited (India)

- Garden Reach Shipbuilders and Engineers (GRSE) (India)

- Hyundai Heavy Industries Co. Ltd (HHI) (South Korea)

- Hyundai Mipo Dockyard (South Korea)

- General Dynamics Corp NASSCO (U.S.)

- Larsen & Toubro Ltd. (India)

- Navantia (Spain)

- ThyssenKrupp Marine Systems (Germany)

- Damen Shipyards Group (Netherlands)

Recent Developments:

-

July 2023 : Hyundai Mipo Dockyard announced plans to develop a hybrid electric propulsion system for CSOVs.

-

June 2023 : Acta Marine signed a contract with Tersan Shipyard for the construction of two new CSOVs, expanding its green fleet.

Future Outlook of Military Robots Market: Size, Growth, Trends, Share, and Forecast, 2020–2027

By Rishika19, 2025-09-04

According to Fortune Business Insights™, the global military robots market size was valued at USD 13.87 billion in 2019 and is projected to grow from USD 13.03 billion in 2020 to USD 64.13 billion by 2032, exhibiting a CAGR of 12.5% during the forecast period. Europe dominated the market in 2019, accounting for 33.74% of the global share, driven by technological superiority and the presence of established robotics manufacturing firms.

The increasing adoption of advanced aerial, land, and naval robots for tactical military operations—including surveillance, combat support, and search and rescue—is significantly accelerating market growth. Major global powers such as the U.S., China, and Russia are prioritizing AI-enabled unmanned systems to enhance battlefield decision-making and reduce human risk.

Technological advancements in modern warfare are driving the demand for autonomous machines to minimize personnel risk and optimize operational efficiency. Leading defense companies are leveraging strategies such as mergers & acquisitions, product launches, and collaborations to expand globally. For instance, in February 2019, FLIR Systems, Inc. acquired Endeavor Robotics for approximately USD 382 million, strengthening its position in ground-based and aerial robotics platforms.

Key Market Drivers

Integration of Advanced Technologies : The incorporation of artificial intelligence (AI), real-time data monitoring, and the Internet of Things (IoT) in military robots has revolutionized modern warfare. AI-integrated robots can track, monitor, and perform counter-attacks on targets remotely, supporting intelligence, surveillance, and reconnaissance (ISR) missions. Small robots capable of transmitting real-time images and video enable battlefield decision-making, significantly enhancing operational efficiency.

Restraining Factors

High Initial Costs and Technological Limitations: Military robots involve substantial procurement, programming, and maintenance costs, which may limit adoption by smaller defense organizations. Additionally, pre-programmed patterns can make some robots predictable and vulnerable to enemy countermeasures, posing challenges to sustained operational efficiency.

Information Source:

https://www.fortunebusinessinsights.com/military-robots-market-104663

Market Segmentation

By Platform : The market is divided into airborne, land, and naval robots. The land segment is expected to grow substantially due to higher adoption across countries, increased R&D, and rising border security concerns in Asia. Airborne and naval robots are also expected to expand due to modernization programs and government investments. In 2019, the airborne segment held 26.3% of the market.

By Mode of Operation : The market is classified into autonomous and semi-autonomous (human-operated) robots. The autonomous segment is expected to see significant growth due to advanced aerial robots equipped with reconnaissance capabilities and weapons, leveraging technologies like LiDAR, fiber optics, and 3D imaging. The semi-autonomous segment is growing due to government initiatives in conventional military robotics and border surveillance.

By Mode of Propulsion : Segmentation includes manual, electric, and hybrid propulsion. Manual robots, widely used for ground-based operations, accounted for the largest market share in 2019. The electric propulsion segment is projected to grow at the highest CAGR due to aerial and naval applications powered by batteries and electric motors. Hybrid robots combine manual and electric propulsion, sometimes incorporating solar panels for extended operations.

By Application : Military robots are deployed across intelligence, surveillance, and reconnaissance (ISR), search and rescue, combat support, transportation, and other applications. ISR is the largest segment in 2019 and is expected to grow the fastest, driven by UAVs, UGVs, USVs, AUVs, and ROVs used for monitoring enemy movements. Transportation robots support the movement of weapons, ammunition, and personnel, while combat support and search and rescue applications enhance real-time situational awareness and operational safety.

Regional Insights

Europe led the market in 2019 with USD 4.68 billion, driven by over 300 service robot manufacturers excelling in navigation, haptics, and motion planning technologies.

Asia-Pacific is projected to grow rapidly due to investments by China and India in defense modernization programs and autonomous systems.

North America is expected to witness strong growth, supported by government-backed R&D, robust supplier networks, and advanced robotics technologies.

Middle East & Africa and Latin America are anticipated to grow steadily, fueled by defense modernization and adoption of unmanned systems.

Key Industry Players

Leading manufacturers are focusing on technologically advanced military robots and integrating AI, IoT, and big data to enhance capabilities. The top players include:

Northrop Grumman Corporation (U.S.)

Thales Group (France)

FLIR Systems, Inc. (U.S.)

Clearpath Robotics Inc. (Canada)

Cobham Limited (U.K.)

QinetiQ (U.K.)

AeroVironment, Inc. (U.S.)

BAE Systems (U.K.)

Elbit Systems Ltd. (Israel)

Raytheon Technologies (U.S.)

Recent Industry Developments

November 2020 – Tyndall Air Force Base, USA, deployed semi-autonomous robotic dogs for patrolling, enhancing situational awareness and reducing manpower risk.

September 2020 – AeroVironment, Inc. partnered with Robotic Skies to provide maintenance and repair support for military robots, improving after-sales performance and reliability.

Push-to-Talk (PTT) Market Trends, Size, Growth, Analysis, Insights, Forecast, 2020–2032

By Rishika19, 2025-09-04

According to Fortune Business Insights™, the global push-to-talk (PTT) market was valued at USD 12.00 billion in 2019 and is projected to reach USD 46.75 billion by 2032, exhibiting a robust CAGR of 12.0% during the forecast period. North America dominated the market with a 37.42% share in 2019, driven by the strong presence of leading telecom players and the early adoption of advanced communication technologies.

Market Growth Overview

The growth of the push-to-talk market is fueled by the adoption of cloud-based Push-to-Talk over Cellular (PoC) solutions, which provide secure, real-time, and scalable communication. These platforms integrate multimedia sharing, GPS tracking, and two-way voice services, making them attractive across industries such as public safety, logistics, utilities, and construction.

Large enterprises are leveraging PoC to reduce communication costs, streamline workflows, and enhance safety. At the same time, advancements in LTE and 5G networks are enabling mission-critical communication with low latency and higher bandwidth.

Emerging technologies such as AI, IoT, natural language processing (NLP), and mobile apps are creating fresh opportunities for market players. Strategic moves such as mergers and acquisitions are reshaping the competitive landscape. For instance, in March 2019, Motorola Solutions acquired Avtec, Inc., strengthening its end-to-end PTT platform for public safety customers.

Key Industry Players

Leading companies in the push-to-talk (PTT) market are focusing on expanding their product portfolios and enhancing technological capabilities to strengthen their global market presence. AT&T Intellectual Property, a U.S.-based communications holding company, is one of the key players driving this growth. The company operates through four major segments—WarnerMedia, Xandr, Communications, and Latin America—with its Communications segment providing wireline and wireless video, broadband, and telecom services. Within its mobility business unit, AT&T offers the Enhanced EPTT service, which delivers highly secure messaging, instant voice communication, and location-sharing capabilities across 3G, 4G, 4G LTE, and Wi-Fi networks. Based on 3GPP Mission Critical standards, the service employs VoIP technology to ensure fast call setup and reliable performance over AT&T’s Wi-Fi infrastructure. AT&T continues to invest in expanding these services worldwide, reinforcing its position as a leader in the PTT market.

List of top Push-To-Talk companies:

- Motorola Solutions Inc. (US)

- Zebra Technologies Corporation (US)

- AT&T Intellectual Property (US)

- Verizon Wireless (US)

- Qualcomm Technologies, Inc. (US)

- Harris Corporation (US)

- ICOM Inc. (Japan)

- Kyocera

- Siyata Mobile (Canada)

- ECOM Instruments GmbH (US)

- RugGear (US)

- Telefonaktiebolaget LM Ericsson (Sweden)

- Sonim Technologies (US)

- Simoco (India)

- Airbus DS Communications (US)

Information Source:

https://www.fortunebusinessinsights.com/industry-reports/push-to-talk-market-100079

Growth Drivers

The growth of the push-to-talk market is strongly supported by several key drivers. One of the most prominent factors is the rising adoption of wireless PTT devices across defense, enterprise, and commercial sectors, where these systems play a crucial role in enhancing operational efficiency and ensuring reliable communication. Another major contributor is the increasing demand for smartphone-based PTT software, which enables seamless group communication and boosts overall market penetration. Additionally, the expansion of accessories and rugged PTT-enabled devices, including wireless microphones, multimedia-supported radios, and durable handsets, is fueling adoption among enterprises and public safety organizations. Moreover, the rapid rollout of LTE and 5G infrastructure is significantly strengthening the market by providing high-speed, low-latency, and scalable communication platforms tailored for mission-critical applications.

Restraining Factors

Despite strong growth potential, the push-to-talk market faces several challenges that could hinder its expansion. Latency issues in regions with weak or limited network coverage remain a significant barrier, particularly where reliable communication is mission-critical. In addition, the high infrastructure costs associated with deploying advanced PTT systems pose difficulties for small and medium-sized enterprises with limited budgets. Another important restraint is the lack of awareness and infrastructure readiness in emerging markets, which slows the adoption of PTT solutions in countries where technological ecosystems are still developing. These challenges collectively act as hurdles to widespread market adoption, though ongoing network advancements are expected to ease their impact over time.

Market Trends

The push-to-talk market is undergoing notable transformation, largely driven by technological advancements and evolving enterprise needs. One of the most significant trends is the shift from Land Mobile Radio (LMR) to LTE-based PTT solutions, as LTE networks enable enhanced functionalities such as push-to-alert, push-to-message, and push-to-locate services. Enterprises are increasingly adopting LTE-powered solutions to improve workflow efficiency and reduce hardware costs, thereby streamlining communication processes across dispersed operations. Furthermore, strategic partnerships and collaborations are playing a vital role in driving innovation within the market. A key example is the 2020 partnership between Siyata Mobile and Verizon, which led to the launch of the Uniden UV350, an LTE-based in-vehicle IoT communication device that expanded advanced PTT capabilities for enterprise customers.

Segmentation Overview

By Component

Devices (Largest Share): Adoption of rugged, multimedia-enabled, long-battery PTT devices.

Software & Services: Growing demand for cloud-based software such as Honeywell’s Smart Talk launched in 2020.

By Network Type

Land Mobile Radio (LMR): Strong presence in defense, law enforcement, and emergency services.

Push-to-Talk over Cellular (PoC): Fastest growth due to cost-efficiency, broad coverage, and flexibility. Example: Hytera PNC370 PoC radio launched in 2019.

By Enterprise Size

Large Enterprises (Leading Share): High adoption of cloud-based PTT for dispersed operations.

SMEs: Favor PoC for affordability and ease of deployment.

By Sector

Public Safety & Security (21.2% share in 2019): Heavy adoption of ultra-rugged devices and mission-critical communications.

Government & Defense: Boosted by border security and national defense initiatives.

Transportation & Logistics, Energy & Utilities, Travel & Hospitality: Growing adoption of cost-efficient, cloud-based communication.

Regional Insights

North America is expected to lead the market, driven by advanced telecom infrastructure, strong presence of vendors like Motorola Solutions and AT&T, and high adoption in public safety, defense, and healthcare.

Asia-Pacific will grow at the highest CAGR, supported by rapid IT infrastructure development and investments from China and India in public safety. Product launches, such as Kyocera’s rugged LTE smartphone, are further fueling growth.

Europe holds a notable share due to players like iPTT and Azetti Networks, with new product launches such as iPTT’s P500 PoC radio expanding adoption across industries.

The Middle East & Africa and Latin America are projected to grow moderately, driven by rising internet penetration, cloud adoption, and increasing demand for public safety communication. Countries like Brazil and Mexico present strong opportunities, supported by new cloud-based offerings from players such as Motorola Solutions.

Recent Industry Developments

October 2019 – T-Mobile launched its broadband PTT service integrated with ESChat technology, targeting government and enterprise customers across the U.S.

March 2019 – Motorola Solutions acquired Avtec, Inc. , expanding its portfolio of public safety and enterprise dispatch communication solutions.

Aircraft Turbocharger Industry Market Insights, Growth and Forecast, 2024–2032

By Rishika19, 2025-08-29

According to Fortune Business Insights™, the global aircraft turbocharger industry was valued at USD 790.3 million in 2023 and is projected to grow from USD 834.7 million in 2024 to USD 1,318.2 million by 2032, at a CAGR of 5.9% during the forecast period. Asia Pacific accounted for the largest share (29.68%) in 2023, underscoring the region’s strong aviation presence and investment in aerospace technologies.

What is an Aircraft Turbocharger?

An aircraft turbocharger, commonly known as a “turbo,” is a forced induction device used in internal combustion engines (ICEs). It captures energy from exhaust gases to compress intake air, ensuring a greater volume enters the combustion chamber. This process enhances engine power output without increasing engine size, thereby improving performance and fuel efficiency.

In aviation, turbochargers are particularly valuable for piston engines at high altitudes, where lower air pressure can reduce performance. By compressing thinner air, they enable engines to maintain near sea-level efficiency up to their “critical altitude.” Above this limit, effectiveness gradually decreases, but turbochargers still extend performance considerably—making them vital for both commercial and military aircraft.

Market Growth Drivers

1. Rising Adoption of Fuel-Efficient Aircraft

The aviation industry is undergoing rapid modernization, with airlines seeking cost-effective and fuel-efficient aircraft. This shift is boosting demand for electric aircraft, advanced propulsion systems, and ultralight models. The push for efficiency reflects not only cost pressures but also regulatory and environmental demands, as consumers and governments prioritize sustainable aviation.

2. Innovations in Turbocharger Technology

The market is being reshaped by advancements such as intercooled turbochargers and electric turbochargers (E-Turbos).

E-Turbos use electric motors to eliminate turbo lag and directly power the compressor at low speeds, enabling larger, more efficient designs.

They improve fuel efficiency by 2–4% and can cut emissions—particularly NOx—by up to 20% in diesel applications.

Companies like Garrett Motion are leading with award-winning E-Turbo systems that recover energy during deceleration, further enhancing efficiency and environmental compliance.

Information Source:

https://www.fortunebusinessinsights.com/aircraft-turbocharger-market-111198

Market Restraints

Long Engine Lifespan: Aircraft engines are designed for extended life cycles, limiting the need for frequent replacements. New turbocharger demand often arises only with new aircraft production.

Aircraft Manufacturing Backlogs: Supply chain constraints and reduced aircraft output have further slowed the turbocharger market’s momentum.

Key Market Trends

Shift Toward Micro Turbines

Micro turbines are increasingly preferred over electric motors and propellers for propulsion. Compared to electric propellers, micro turbines provide:

Higher thrust and speed, essential for advanced aircraft.

Fuel efficiency advantages, as diesel fuel stores nearly 40 times more energy per pound than lithium batteries.

Faster refueling, taking only minutes versus hours for electric recharging.

Notably, FusionFlight (U.S.) unveiled its AB6 JetQuad in 2021, a quadcopter powered by four micro turbines using kerosene, gasoline, or jet A fuel. Producing 700 newtons of thrust, it demonstrates how turbine-based propulsion can support surveillance, emergency response, and logistics applications.

Segmentation Analysis

By Platform , the heavyweight aircraft segment remains the largest contributor to the aviation turbocharger market. This growth is strongly tied to the continuous increase in global air travel, where airlines are investing in large, fuel-efficient aircraft to accommodate passenger demand. Furthermore, defense modernization programs are boosting the adoption of advanced turbocharging systems in heavy military aircraft. In contrast, the lightweight aircraft segment is experiencing strong momentum, supported by the rising popularity of general aviation, regional transport, and unmanned aerial vehicles (UAVs). Here, compact turbocharger systems are particularly valued, as they enhance thrust and altitude performance without significantly increasing weight—an essential factor in UAV and light aircraft operations.

By Turbocharger Type , butterfly valve turbochargers are projected to dominate due to their advantages such as simplicity of design, lightweight structure, low maintenance needs, and high reliability in diverse operating conditions. These features make them highly suitable for both civil and defense aviation platforms. At the same time, poppet valve turbochargers are registering steady adoption. Their design supports advanced performance optimization and aligns with the industry’s shift toward more eco-friendly propulsion systems, reducing emissions and enhancing fuel efficiency—critical considerations for next-generation aircraft programs.

By Component , turbines stand out as both the largest and the fastest-growing segment. Their expansion is directly linked to rising air travel demand, growing defense budgets, and strict regulatory standards aimed at reducing fuel consumption and emissions. Turbines are essential in driving efficient airflow and improving thrust-to-weight ratios in modern aircraft engines. Meanwhile, compressors accounted for 31.55% of the market share in 2023 and are expected to grow steadily due to their critical role in air compression and performance enhancement. Finally, waste gates continue to play a supportive yet vital function in controlling airflow, preventing over-boost conditions, and ensuring overall engine efficiency, making them indispensable in turbocharger systems.

Regional Insights

Asia Pacific (USD 234.6 Million in 2023): Largest market, driven by China, Japan, India, and South Korea, all investing heavily in aviation capacity and aircraft manufacturing.

North America: Poised for robust growth due to technological innovations, commercial aviation expansion, and strict environmental regulations.

Europe: Holds a significant share, with strong demand fueled by air passenger growth and emission compliance measures.

Rest of the World: Latin America and the Middle East show strong growth potential, while Africa remains in the early adoption stage.

Key Industry Players

Leading companies are focusing on advanced turbocharger technologies, hybrid propulsion integration, and lightweight designs.

Top Players Include:

ABB Ltd. (Switzerland)

Airmark Overhaul, Inc. (U.S.)

BorgWarner Inc. (U.S.)

General Electric Company (U.S.)

Hartzell Engine Technologies LLC (U.S.)

Honeywell International Inc. (U.S.)

Kawasaki Heavy Industries, Ltd. (Japan)

PBS Group, A.S. (Czech Republic)

Rajay Parts LLC (U.S.)

Victor Aviation Service, Inc. (U.S.)

Recent Industry Development

March 2024: India’s Ministry of Defense signed an agreement with Hindustan Aeronautics Limited (HAL) worth USD 5.25 billion to procure MiG-29 aircraft engines. The program emphasizes localization of key engine components, supporting domestic aerospace manufacturing capabilities.

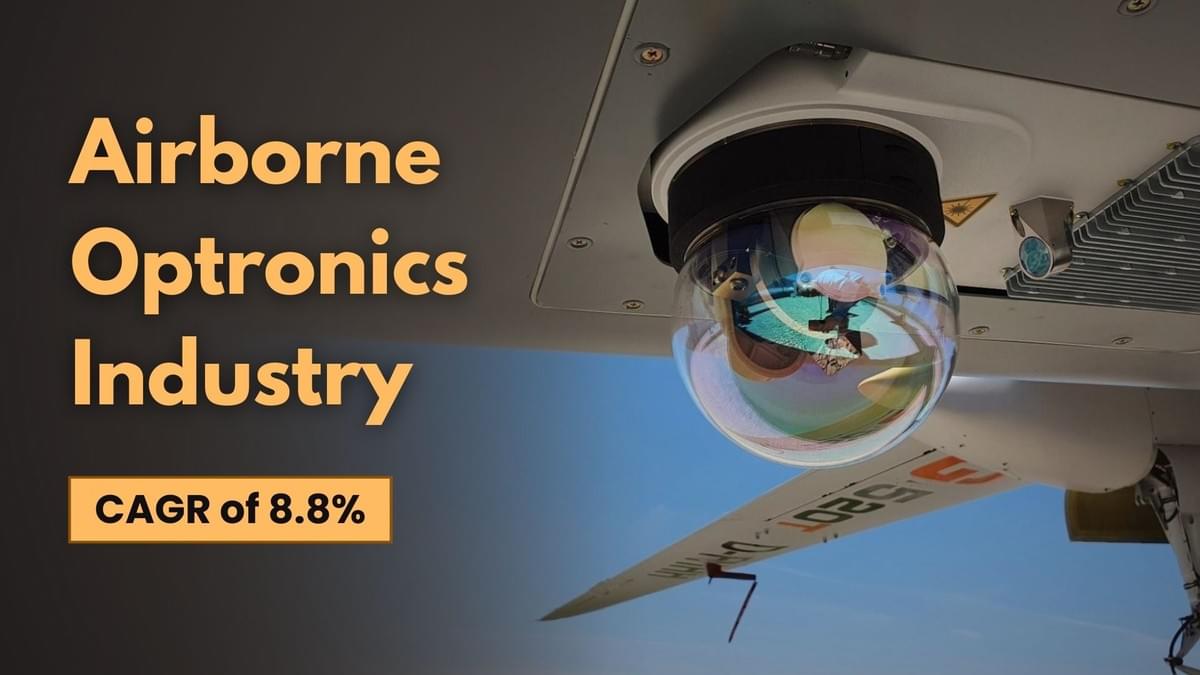

Airborne Optronics Industry Analysis, Forecast, Share and Trends, 2024–2032

By Rishika19, 2025-08-29

According to Fortune Business Insights™, the global airborne optronics industry size was valued at USD 2.03 billion in 2023 and is projected to grow from USD 2.53 billion in 2024 to USD 4.96 billion by 2032, registering a CAGR of 8.8% during the forecast period.

Growth is fueled by rising defense investments, increasing adoption of UAVs (unmanned aerial vehicles), and growing emphasis on ISR (intelligence, surveillance, and reconnaissance) missions. In 2023, North America led the market with a 34.98% share, supported by high military spending and the presence of major aerospace and defense companies.

What is Airborne Optronics?

Airborne optronics refers to the integration of optical and electronic technologies into aerial platforms—both manned and unmanned—for missions such as surveillance, targeting, navigation, and reconnaissance.

These systems employ infrared sensors, electro-optical modules, laser rangefinders, and AI-enabled processors to deliver high-resolution, real-time data. The result is improved situational awareness, mission accuracy, and platform survivability, making airborne optronics critical for both military modernization and commercial aviation safety.

Market Dynamics

Growth Drivers

1. Rising Adoption of UAVs

The proliferation of drones in both commercial and defense sectors is a major driver of market growth. UAVs require advanced optronics—such as infrared cameras, electro-optical targeting systems, and laser rangefinders—to conduct missions involving surveillance, target acquisition, and reconnaissance.

2. Increasing Focus on ISR Operations

The growing demand for intelligence, surveillance, and reconnaissance is reshaping defense strategies worldwide. Optronic systems equipped with EO/IR sensors and real-time data processing are essential for counterterrorism, homeland security, and border surveillance.

Restraints

Complex Installation and Maintenance

Integrating airborne optronics into platforms such as UAVs, fighter jets, and satellites is technically demanding, requiring custom designs, advanced testing, and specialized expertise. Moreover, these systems must endure harsh conditions like electromagnetic interference, extreme temperatures, and vibrations, which drive up maintenance costs.

Regular software upgrades, calibration, and spare parts replacement further escalate lifecycle expenses, presenting a key challenge for both manufacturers and end-users.

Market Trends

Integration of AI and Machine Learning

Artificial intelligence (AI) and machine learning (ML) are transforming airborne optronics by enhancing object detection, automatic target classification, and decision-making speed.

AI-enhanced systems are also being applied to targeting and guidance, enabling faster and more precise engagements in combat scenarios.

Information Source:

https://www.fortunebusinessinsights.com/airborne-optronics-market-108108

Market Segmentation

By Aircraft Type

Fixed-wing aircraft dominated the market in 2023, accounting for nearly 44% of the share, owing to their extensive use in surveillance, targeting, and intelligence collection missions. Rotary-wing platforms are expected to record the fastest growth between 2024 and 2032, supported by their rising adoption in reconnaissance, search-and-rescue, and military operations. Unmanned Aerial Vehicles (UAVs) are also expanding rapidly, driven by the growing global adoption of drones across defense and commercial applications. Meanwhile, Urban Air Mobility (UAM) represents an emerging segment, benefiting from increasing investments in smart mobility and advanced aerial platforms.

By Application

The military sector remained the largest application segment in 2023, bolstered by modernization programs, intelligence, surveillance, and reconnaissance (ISR) missions, as well as border security initiatives. The commercial sector, however, is projected to grow at the fastest pace during the forecast period, fueled by rising demand for urban air mobility solutions, aviation safety systems, and monitoring applications. Space-based applications are also gaining traction, as satellites increasingly integrate advanced imaging technologies for ISR and Earth observation purposes.

By Technology

Multispectral technology held the largest share in 2023, valued for its broad spectral coverage, ability to support data fusion, and cost-effectiveness. Hyperspectral technology is anticipated to register the fastest growth through 2032, as it enables highly detailed spectral imaging that is critical for advanced reconnaissance, surveillance, and precise target identification.

By System

Reconnaissance systems accounted for the largest share and are expected to grow at the fastest pace, driven by the rising demand for ISR operations worldwide. Other key system categories include targeting systems, search & track systems, surveillance systems, warning & detection systems, countermeasure systems, navigation & guidance systems, and special mission systems, each supporting specialized defense and commercial applications.

By End-User

Original Equipment Manufacturers (OEMs) represented the largest end-user segment in 2023, as new aircraft production continues to incorporate advanced optronics solutions. The aftermarket segment is also witnessing robust growth, propelled by increasing requirements for maintenance, system upgrades, and retrofitting of existing platforms to enhance operational capabilities.

Regional Insights

North America – Largest market, valued at USD 0.71 billion in 2023, driven by U.S. defense spending and aerospace giants like Lockheed Martin, Northrop Grumman, and L3Harris.

Europe – Strong market presence with companies such as Thales, Safran, and Leonardo advancing ISR and defense modernization.

Asia Pacific – Fastest-growing, with China and India boosting defense budgets and focusing on indigenous UAV and ISR programs.

Middle East & Africa – Growth led by military modernization in Saudi Arabia, Israel, and UAE.

Latin America – Emerging demand in Brazil and Mexico for border surveillance and counter-narcotics operations.

Key Industry Players

Major companies shaping the airborne optronics industry include:

L3Harris Technologies (U.S.)

Safran (France)

Elbit Systems (Israel)

Hensoldt AG (Germany)

Northrop Grumman (U.S.)

Lockheed Martin (U.S.)

Collins Aerospace (U.S.)

FLIR Systems (U.S.)

Thales (France)

Leonardo S.p.A. (Italy)

These players are investing in AI integration, multispectral/hyperspectral imaging, lightweight designs, and strategic collaborations to expand their portfolios.

Recent Developments

May 2024 – The U.S. Air Force awarded SNC a multibillion-dollar contract to modernize the E-4B “Nightwatch” aircraft, also known as the "Doomsday Plane," enhancing command-and-control capabilities for national security leadership.

Military Communication Industry Growth, Dynamics, Forecast and Analysis, 2024–2032

By Rishika19, 2025-08-29

According to Fortune Business Insights™, the global military communication industry size was valued at USD 33.12 billion in 2023 and is projected to grow from USD 34.74 billion in 2024 to USD 60.40 billion by 2032, exhibiting a CAGR of 7.2% during the forecast period.

Market growth is driven by the rising demand for secure, real-time, and multi-domain communication systems, the integration of wireless tactical networks, and the growing adoption of SATCOM (Satellite Communication) to enhance battlefield situational awareness.

North America Leads with 31.49% Market Share

In 2023, North America accounted for 31.49% of the global share, supported by high defense budgets, advanced technological infrastructure, and the presence of leading contractors such as Lockheed Martin, Northrop Grumman, and L3Harris Technologies.

The U.S. military continues to prioritize SATCOM-based systems, encrypted tactical radios, and secure communication protocols to ensure seamless coordination between commanders, deployed forces, and allied partners. Furthermore, programs like Joint All-Domain Command and Control (JADC2) and Warfighter Information Network-Tactical (WIN-T) are reinforcing wireless, real-time communication capabilities across all domains.

Market Dynamics

Growth Factors

1. Increasing Procurement of Advanced Communication Systems

The defense sector places a premium on confidential and accurate communication, critical for surveillance, command, and control. Rising geopolitical disputes are driving defense investments in advanced communication systems with enhanced security and privacy features to safeguard sensitive information.

2. Adoption of Wireless Communication Technologies

Evolving wireless technologies such as SATCOM, VHF/UHF communication, and 5G-enabled networks are replacing traditional wired systems. The U.S. military’s JADC2 program, which unifies sensors across the Army, Navy, Air Force, Marine Corps, and Space Force, highlights the growing adoption of next-generation wireless tactical communication.

3. IoT and Next-Gen Technologies

The integration of IoT-based communication, Ka-band technology, and 5G is enhancing interoperability, situational awareness, and network resilience, creating multiple growth opportunities for the market.

Restraining Factor

High Development and Infrastructure Costs

Developing advanced communication satellites requires investments of around USD 1 billion, while launch costs range from USD 55 million to USD 90 million per satellite. The high cost of infrastructure, installation, and maintenance remains a key challenge for market expansion.

Market Trends

Growing Adoption of SATCOM Systems

As modern battlefields become increasingly network-centric, military satellite communication systems (Military SATCOM) are emerging as a cornerstone of defense infrastructure. These systems provide secure, global, and high-bandwidth connectivity, ensuring reliable information sharing across air, ground, naval, and space domains.

Naval forces, in particular, rely heavily on SATCOM for network-centric warfare, enabling seamless connectivity between sensors, platforms, and weapons systems.

Information Source:

https://www.fortunebusinessinsights.com/military-communications-market-102696

Segmentation Overview

By Component

Hardware – Dominated the market in 2023 and is expected to grow fastest, driven by rising adoption of tactical radios, handheld and man-portable systems, antennas, and transceivers.

Software – Expected to witness significant growth due to rising adoption of software-defined radios (SDRs).

By Hardware

Antennas – Accounted for the largest share in 2023, fueled by applications in surveillance, SATCOM, electronic warfare, and navigation.

Receivers – Ranked second, supported by next-gen upgrades such as advanced multiband GPS-enabled radios supplied under contracts by L3Harris and others.

By Technology

SATCOM – Dominated the market in 2023 due to its role in ISR and combat operations.

VHF/UHF/L-Band – Accounted for 26.08% share in 2023.

Data Link – Expected to expand significantly, supported by programs like Link 16 for real-time tactical data exchange.

By Platform

Ground – Held the largest share in 2023 due to extensive use of ground antennas and secure communication systems.

Airborne – Expected to record notable growth with next-generation avionics integration in fighter aircraft, including SATCOM systems by Viasat.

Naval and Space – Anticipated to witness steady demand, supported by network-centric warfare applications.

Regional Insights

North America – Largest market in 2023, supported by U.S. defense spending and leading OEMs.

Europe – Fastest-growing region, driven by increased defense modernization amid the Russia-Ukraine conflict.

Asia Pacific – Second-largest market, led by rising military budgets in China and India.

Middle East & Africa – Moderate growth fueled by defense investments in Saudi Arabia, Israel, and the UAE.

Latin America – Gradual growth driven by Brazil and Mexico’s defense upgrades.

Competitive Landscape

The market is highly competitive, with leading players focusing on R&D investments, strategic acquisitions, and long-term defense contracts to expand their portfolios.

Top Companies in the Military Communication Market:

ASELSAN A.S. (Turkiye)

General Dynamics Corporation (U.S.)

L3Harris Technologies, Inc. (U.S.)

Viasat Inc. (U.S.)

Cobham PLC (U.K.)

BAE Systems PLC (U.K.)

Elbit Systems Ltd. (Israel)

Lockheed Martin Corporation (U.S.)

Northrop Grumman Corporation (U.S.)

RTX Corporation (U.S.)

Recent Developments

March 2024 – The U.S. Space Force awarded Boeing a USD 439.6 million contract to develop the WGS-12 military communications satellite, part of the Wideband Global SATCOM constellation.

Aircraft Communication System Industry Analysis, Forecast and Share, 2024–2032

By Rishika19, 2025-08-28

According to Fortune Business Insights™, the global aircraft communication system industry was valued at USD 17.12 billion in 2024 and is projected to reach USD 33.52 billion by 2032, registering a CAGR of 8.8% during the forecast period. The market growth is primarily driven by the increasing need for secure, efficient, and real-time communication between aircraft and ground control, along with rapid advancements in satellite-based communication, software-defined radios (SDR), and high-speed data link technologies.

Market Overview

Aircraft communication systems (ACARS) integrate audio systems, communication radios, tuning units, cockpit voice recorders (CVRs), antennas, and static dischargers to facilitate seamless air-to-ground and in-flight communication. The growing air traffic, stringent safety requirements, and rising adoption of satellite-based navigation and wireless communication systems are boosting demand across both commercial and defense aviation.

The increasing commercialization of Unmanned Aerial Vehicles (UAVs) presents additional opportunities. For instance, in April 2019, Honeywell International Inc. extended a contract with OJets to provide in-flight connectivity services for business aircraft, highlighting the rising demand in the UAV segment.

Impact of Geopolitical Tensions

The Russia-Ukraine war has notably influenced the aircraft communication system industry, increasing the emphasis on secure and resilient communication technologies. The conflict disrupted global supply chains, causing delays and higher costs for aviation components, including communication systems. Heightened security requirements have spurred demand for tamper-proof and reliable communication solutions, while restricted airspaces and altered flight routes have necessitated more robust and adaptable infrastructures.

Key Growth Drivers

Increase in Aircraft Deliveries

The rising number of aircraft deliveries is fueling market growth. For example, Airbus planned to deliver 863 commercial jets by 2019, driving procurement of audio integrating systems, antennas, cockpit voice recorders, and static dischargers. In commercial aircraft such as the Airbus A320 and Boeing 767, multiple antennas are deployed for in-flight broadband communication, enabling reliable connectivity at altitudes up to 50,000 ft.

The growing demand for military helicopters, commercial aviation, and regional jets is also expected to propel the military aircraft communication system market during the forecast period.

Software Defined Radio (SDR) Adoption

SDR technology is transforming aircraft communication systems by providing a software-enabled digital infrastructure. SDR decodes incoming radio signals and enhances the accuracy and efficiency of radio communication, helping pilots receive real-time operational data. The increasing adoption of SDR across commercial and military aviation is a key factor driving market growth.

Restraining Factors

The high development cost of aircraft communication systems is a major challenge. Advanced systems include expensive antennas, communication radios, and audio integration components. Rapid technological changes in aircraft antennas and limited availability of radio spectrum from regulatory authorities may also constrain market growth.

Information Source:

https://www.fortunebusinessinsights.com/aircraft-communication-system-market-102541

Market Segmentation

By Component: The antennas segment dominates the aircraft communication system market, driven by the rising need for reliable wireless communication systems in both commercial and defense aviation. Modern antennas, such as the AV-17 RAMI and AV-529 RAMI, support air-to-ground communication as well as in-flight broadband connectivity, enabling seamless data transmission for navigation, weather monitoring, and passenger connectivity. These antennas are designed to withstand high-altitude and high-speed conditions, ensuring uninterrupted communication across long distances. The transponder segment is also expected to grow significantly, particularly ADS-B-enabled transponders, which provide real-time aircraft position data, enhancing safety and air traffic management. Products like uAvionix’s tailBeaconX integrate with EFIS (Electronic Flight Instrument Systems) to deliver enhanced situational awareness and ensure compliance with global aviation regulations. Other components, including receivers, transmitters, SDR units, and radio tuning systems, complement the core communication infrastructure, further supporting growth in this segment.

By System: The radio communication system holds the largest market share, accounting for 29.5% in 2023, driven by its widespread adoption across commercial, military, and business aircraft. Radio communication systems, encompassing VHF, HF, and UHF transceivers, facilitate long-range voice communication, essential for air traffic coordination and operational safety. The cockpit voice recorder (CVR) segment is projected to grow rapidly, driven by regulatory mandates from authorities such as the FAA and ICAO. The FAA, for instance, proposed extending CVR recording duration to 25 hours for newly manufactured aircraft, necessitating upgrades to existing systems and boosting market demand for advanced CVRs with longer recording capacity and improved durability.

By Connectivity: Satellite communication (SATCOM) is anticipated to witness the fastest growth, fueled by increasing adoption of satellite-based voice and data services in both commercial and military aviation. SATCOM enables aircraft to maintain continuous global connectivity, even over remote or oceanic regions where conventional radio communication is limited. Additionally, VHF, UHF, and L-Band antennas are projected to see strong adoption, supporting in-flight entertainment, data streaming, and line-of-sight communication applications. The integration of Software Defined Radio (SDR) further enhances connectivity by allowing flexible frequency management, modulation, and data rate adjustment in real time.

By Fit Type: The line fit segment dominates due to increasing incorporation of advanced communication systems in newly delivered UAVs, commercial jets, and military aircraft. Line fit installations offer optimal system integration, ensuring maximum performance, reliability, and compliance with aircraft certification standards. The retrofit segment is also witnessing significant growth as airlines and defense operators upgrade legacy systems to next-generation antennas, including 5G-ready and SATCOM-enabled solutions, to meet evolving operational requirements and passenger expectations.

By Platform: Within aircraft platforms, the fixed-wing segment is expected to witness the fastest growth, supported by the rising number of commercial aircraft deliveries globally, including aircraft like the Boeing 787, Airbus A320, and Airbus A380, which employ multiple antennas and radio communication systems for both passenger and operational connectivity. The rotary-wing segment, including military and commercial helicopters, is also expected to grow due to increased deployment of GPS, HF, and VHF antennas for surveillance, reconnaissance, navigation, and communication applications. Enhanced communication capabilities are particularly critical for mission-critical operations in military, search and rescue (SAR), and oil & gas sectors, driving demand for robust, high-performance communication systems.

Regional Insights

North America is expected to hold the largest market share, driven by high air passenger traffic, UAV adoption, and the presence of key industry players such as Lockheed Martin and Northrop Grumman.

Asia Pacific is projected to see significant growth due to the rising utilization of UAVs and 3D-printed aircraft antennas, particularly in China. Airbus forecasts over 7,000 passenger aircraft will be required in the region by 2037.

Europe is estimated to grow rapidly due to increased investments in military UAVs and GPS-enabled helicopters for search and rescue operations.

Middle East & Africa and Latin America are also expected to register steady growth, driven by helicopter usage for oil, gas, and commercial applications.

Key Players

Leading companies in the aircraft communication system market include:

- Cobham Plc (U.K.)

- General Dynamics Corporation (U.S.)

- Thales Group (France)

- Harris Corporation (U.S.)

- United Technologies Company (U.S.)

- Honeywell International Inc. (U.S.)

- Iridium Communications Inc. (U.S.)

- l3harris technologies (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Systems Corporation (U.S.)

- Raytheon Company (U.S.)

- Rohde & Schwarz GmbH & Co KG (Germany)

- Viasat, Inc. (U.S.)

Cobham Plc, for example, offers a broad portfolio of SATCOM, VHF, and datalink antennas to support reliable communication across helicopters, regional jets, business jets, and wide-body aircraft.

Recent Industry Developments

April 2024: BAE Systems secured a USD 459 million contract from the U.S. Department of Defense for the supply of hardware, repair services, and technical support for the AN/ARC-231/A Multi-mode Aviation Radio Suite, highlighting ongoing demand for advanced communication solutions in defense aviation.

According to Fortune Business Insights™, the global smart weapons industry was valued at USD 18.99 billion in 2023 and is projected to expand from USD 20.20 billion in 2024 to USD 45.24 billion by 2032, registering a CAGR of 10.61% during the forecast period. Growth is driven by rising global defense budgets, increasing military modernization programs, and the growing demand for precision strike capabilities in modern combat environments.

Market Overview

The global defense landscape is rapidly evolving, shaped by geopolitical tensions, cross-border disputes, and asymmetric warfare. Militaries are prioritizing precision, flexibility, and reduced collateral damage, which has accelerated the adoption of smart weapons systems worldwide.

Smart weapons—including guided bombs, cruise missiles, directed-energy weapons, and satellite/laser-guided systems—provide superior accuracy, extended operational range, and improved mission success rates compared to conventional arms.

In 2023, North America led the market with a 33.86% share, supported by high U.S. defense spending and the presence of leading contractors such as Lockheed Martin, Northrop Grumman, and Raytheon Technologies.

Growth Factors

Increasing Need for Precision Weapons

Rising warfare activities and cross-border disputes are boosting the demand for highly accurate and cost-effective weapons. Precision-guided systems offer enhanced range, minimal training requirements, and higher mission efficiency.

Surging Defense Budgets

Defense spending continues to rise globally. For example, the U.S. allocated USD 732 billion in 2020, while China, India, Russia, and Saudi Arabia collectively invested hundreds of billions more. These budgets directly support procurement of advanced smart weapons.

Modernization Programs

Ongoing replenishment and modernization initiatives are driving contracts for advanced systems. In March 2020, Raytheon Technologies signed a USD 110 million contract with the U.S. Navy to upgrade radar-guided gun systems.

Information Source:

https://www.fortunebusinessinsights.com/smart-weapons-market-104058

Restraining Factors

Stringent Regulations

Strict firearm and weapons regulations in countries such as India, New Zealand, Australia, and the U.K. hinder market growth. For instance, New Zealand banned semi-automatic weapons in 2019 after the Christchurch attacks.

Market Segmentation

By Product:

The missiles segment is projected to dominate the guided weapons market, driven by increasing defense budgets and the strategic need for advanced long-range precision strike capabilities. These systems are crucial for modern military operations, providing accuracy, speed, and lethality. Munitions are expected to record the highest growth rate, as militaries worldwide increasingly adopt precision-guided bombs and artillery shells to minimize collateral damage during counter-terrorism operations and cross-border conflicts. Additionally, segments such as guided projectiles, guided rockets, and directed energy weapons are experiencing steady adoption due to technological advancements, operational versatility, and integration into modern combat platforms.

By Platform:

The land segment is anticipated to be the fastest-growing, fueled by growing army procurements and modernization programs. Ground forces are investing in next-generation guided missiles, rockets, and munitions to enhance battlefield effectiveness and mobility. Air platforms are also experiencing significant growth, supported by air force modernization initiatives and the deployment of precision air-to-ground weapons that improve strike accuracy and operational efficiency. The naval segment, while holding a moderate share of 23.33% in 2023, is seeing rising interest in directed energy weapons and missile systems to enhance maritime defense capabilities against modern threats, including unmanned surface vessels and incoming missile attacks.

By Technology:

Laser guidance technology is forecasted to witness the highest growth due to its ability to provide highly accurate targeting in real-time, even against moving targets. Satellite guidance systems are also expected to see strong demand as GPS-based technologies enable precision strikes in all weather conditions and challenging terrains, enhancing operational reliability. Infrared and radar guidance continue to be widely adopted, offering versatile tracking and targeting solutions across multiple platforms. These technologies allow military forces to engage targets effectively in diverse scenarios, from close-range skirmishes to long-range strategic operations.

Regional Insights

North America (USD 6.43 billion, 2023)

The largest market, benefiting from high defense budgets and advanced modernization programs. U.S. procurement of over 6,000 munitions in 2019 highlights strong demand.

Asia-Pacific

Expected to showcase the fastest growth, driven by defense investments in China, India, Japan, and South Korea amid rising regional conflicts and terrorism.

Europe

Significant growth projected due to defense expansions in the U.K., France, and Russia, alongside contributions from players such as BAE Systems, Thales Group, and Rheinmetall AG.

Rest of the World

Middle Eastern countries like the UAE and Saudi Arabia are investing heavily in precision weapons. In 2019, EDGE (UAE) signed a USD 1 billion contract to deliver Desert Sting-16 precision weapons.

Key Players

- BAE Systems (The U.K)

- Boeing (The U.S.)

- General Dynamics Corporation (The U.S.)

- Lockheed Martin Corporation (The U.S.)

- MBDA (France)

- Northrop Grumman Corporation (The U.S.)

- Raytheon Company, a Raytheon Technologies company (The U.S.)

- Rheinmetall AG (Germany)

- Textron Inc. (The U.S.)

- Thales Group (France)

Leading players focus on business expansion, contracts, and acquisitions. For example, in February 2021, Lockheed Martin secured a USD 414 million contract with the U.S. Navy and Air Force for LRASM (Long-Range Anti-Ship Missile) systems.

Key Industry Developments

February 2021 – Lockheed Martin signed a USD 414 million contract with the U.S. Navy and Air Force for LRASM delivery.

January 2021 – India’s DRDO successfully tested the Smart Anti-Airfield Weapon (SAAW) on HAL’s Hawk-I jet.

2019–2020 – Multiple modernization contracts signed, including Elbit Systems’ USD 30 million supply of precision-guided mortar munitions to an Asia-Pacific nation.