Category: Metallic Materials

SF6 Gas Load Break Switches Market: Competitive Strategies and Growth Projections 2025-2032

By SemiconductorinsightPrerana, 2025-07-30

SF6 Gas Load Break Switches Market , Trends, Business Strategies 2025-2032

MARKET INSIGHTS

The global SF6 Gas Load Break Switches Market size was valued at US$ 1.67 billion in 2024 and is projected to reach US$ 2.89 billion by 2032, at a CAGR of 8.3% during the forecast period 2025-2032 .

SF6 gas load break switches are arc extinguishing devices that utilize sulfur hexafluoride gas for superior insulation and switching performance. These components consist of two primary circuits – the main circuit and ground circuit – enclosed in epoxy-insulated shells for enhanced safety and reliability. Their compact design makes them ideal for medium voltage applications ranging from 12kV to 40.5kV.

The market growth is driven by increasing electrification projects worldwide and the rising demand for reliable power distribution infrastructure. While environmental concerns about SF6 gas persist, its excellent dielectric properties continue to make it the preferred choice for medium voltage applications. The outdoor segment currently dominates with over 65% market share due to widespread use in utility-scale projects. Key players like Honeywell and Ensto Building Systems are investing in R&D to improve switch efficiency and explore eco-friendly alternatives.

List of Key SF6 Gas Load Break Switch Manufacturers

- Honeywell International Inc . (U.S.)

- Ensto Building Systems (Finland)

- Allis Electric Co., Ltd. (Taiwan)

- ENTEC ELECTRIC & ELECTRONIC CO.,LTD (South Korea)

- Katko Oy (Finland)

- Chirag Techno Electricals (India)

- Spark Engineering (India)

- Power-Grid Switchgears (India)

- P. C. Industries (India)

- Safvolt Switchgears (India)

- Aswich Electrical (China)

- Zhejiang Farady Powertech (China)

- Wenzhou Vacem Technology (China)

- Ningbo Tianan (Group) (China)

- Ningbo Yinzhou Huayuan Electric (China)

Segment Analysis:

By Type

Outdoor Segment Dominates Due to Higher Demand in Utility and Industrial Applications

The SF6 Gas Load Break Switches market is segmented based on type into:

- Outdoor

- Subtypes: Pole-mounted, Pad-mounted, and others

- Indoor

By Application

Utilities Segment Leads Owing to Widespread Grid Modernization Initiatives

The market is segmented based on application into:

- Utilities

- Industrial

- Commercial

By Voltage Level

Medium Voltage Segment Holds Significant Share Due to Common Distribution Network Use

The market is segmented based on voltage level into:

- Low Voltage

- Medium Voltage

- High Voltage

By Operation Mechanism

Motorized Operation Gains Traction for Remote Control Capabilities

The market is segmented based on operation mechanism into:

- Manual

- Motorized

Regional Analysis: SF6 Gas Load Break Switches Market

North America

The North American SF6 gas load break switches market is driven by aging power infrastructure replacement initiatives and strict environmental regulations. The U.S. dominates the regional market, with an estimated $XX million market size in 2024, supported by grid modernization projects and the growing need for reliable power distribution systems. While SF6 remains widely used due to its excellent arc-quenching properties, increasing environmental concerns are prompting utilities to explore alternatives. Major manufacturers are investing in R&D to develop hybrid solutions that reduce SF6 usage while maintaining performance.

Europe

Europe presents a complex landscape for SF6 switches, with strong demand from energy utilities counterbalanced by the F-gas Regulation (EU) No 517/2014, which phases down SF6 usage. Germany and France lead in adopting SF6 alternatives, while Eastern European countries continue conventional deployments. The market is transitioning toward vacuum and solid insulation technologies for medium-voltage applications. Recent developments include increased collaboration between switchgear manufacturers and research institutions to develop next-generation eco-friendly solutions that meet the region’s stringent emission standards.

Asia-Pacific

Asia-Pacific dominates global SF6 switch consumption, accounting for over 40% of the market share, with China leading demand. Rapid urbanization, industrialization, and massive power infrastructure projects drive market growth. While environmental concerns exist, cost-effectiveness and proven reliability maintain SF6’s dominance in the region. India’s market is expanding significantly, supported by government initiatives like the Revamped Distribution Sector Scheme (RDSS) with a $40 billion investment in grid modernization. Japan and South Korea are at the forefront of developing SF6-free alternatives, reflecting the region’s diverse market dynamics.

South America

The South American market shows moderate growth potential, with Brazil and Argentina being key markets. Investments in renewable energy integration and distribution network upgrades create opportunities for SF6 switch deployment. However, economic volatility and limited regulatory pressure on SF6 emissions slow the adoption of alternative technologies. The market remains price-sensitive, favoring cost-effective SF6 solutions over newer, more expensive alternatives. Infrastructure development projects in mining and industrial sectors present growth avenues, though political and economic instability pose challenges for long-term planning.

Middle East & Africa

This emerging market is characterized by growing electricity demand and grid expansion projects, particularly in GCC countries and South Africa. The SF6 switch market benefits from large-scale power projects and industrialization, though adoption varies widely across the region. While environmental regulations remain limited, some countries are beginning to consider SF6 alternatives in line with global trends. The market faces challenges including limited local manufacturing, reliance on imports, and volatile energy prices, but presents long-term growth potential as electrification rates improve across Africa.

MARKET DYNAMICS

The electrical industry faces a pivotal transition as environmental pressures accelerate development of SF6-free alternatives. Vacuum and clean air insulation technologies are gaining traction, with several major manufacturers launching competing solutions. This technological shift creates a challenging environment for SF6 switch producers, who must balance continued R&D in traditional products with investments in emerging alternatives. The situation is further complicated by inconsistent global regulations – while some regions aggressively pursue SF6 phase-outs, others maintain fewer restrictions, creating a fragmented market landscape.

Supply Chain Vulnerabilities

Specialized components for SF6 switches, including high-grade epoxy insulators and precision gas handling valves, often come from limited supplier bases. Recent disruptions have caused lead times to extend beyond 6 months in some cases, challenging manufacturers’ ability to meet project timelines.

End-of-Life Management

Responsible SF6 gas recovery and recycling requires specialized equipment that many regional utilities lack. The absence of comprehensive recycling infrastructure in developing markets raises concerns about potential environmental impacts as equipment reaches end-of-life.

Emerging SF6 gas blends with reduced environmental impact present significant growth opportunities for manufacturers. These next-generation mixtures maintain excellent dielectric properties while cutting global warming potential by over 90%. Utilities testing these solutions report comparable performance to pure SF6 in medium voltage applications, with several European TSOs approving their use. Successful commercialization of these alternatives could extend the technology’s viability despite environmental concerns, potentially unlocking new market segments sensitive to sustainability considerations.

Power utilities worldwide are prioritizing replacement of obsolete switchgear, with an estimated 45% of installed base in North America and Europe exceeding 30 years of service. This refurbishment cycle represents a substantial opportunity, particularly for SF6 solutions offering compact retrofits for space-constrained substations. The U.S. infrastructure bill alone has allocated over $65 billion for grid modernization, with medium voltage switchgear upgrades comprising a significant portion of planned expenditures. Manufacturers offering turnkey replacement solutions are particularly well positioned to capitalize on this trend.

The rapid growth of distributed renewable generation requires specialized switching solutions capable of handling bidirectional power flows and frequent operational cycling. SF6 load break switches adapted for solar and wind applications feature enhanced mechanical endurance and advanced monitoring capabilities. With global renewable capacity projected to grow by over 2,400 GW through 2030, these niche applications represent one of the most dynamic segments for technology providers. Several manufacturers have already developed product lines specifically optimized for renewable integration, featuring reduced maintenance requirements and remote monitoring interfaces.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=108123

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global SF6 Gas Load Break Switches Market?

Which key companies operate in Global SF6 Gas Load Break Switches Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/07/harmonic-absorbing-filters-market.html

https://semiconductorblogs21.blogspot.com/2025/07/portable-frequency-jammers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/low-frequency-choke-market-revenue.html

https://semiconductorblogs21.blogspot.com/2025/07/power-timing-controllers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/magnetic-lighting-drivers-market-key.html

https://semiconductorblogs21.blogspot.com/2025/07/radio-frequency-rf-coaxial-isolator.html

https://semiconductorblogs21.blogspot.com/2025/07/rocker-potentiometers-market-regional.html

https://semiconductorblogs21.blogspot.com/2025/07/high-frequency-chokes-market-trends.html

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Gas Scrubbers for Semiconductor Market: Investment Opportunities and Emerging Segments 2025-2032

By SemiconductorinsightPrerana, 2025-07-29

Gas Scrubbers for Semiconductor Market Size, Share, Trends, Market Growth, and Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=3318

Gas Scrubbers for Semiconductor Market Overview

Market Growth

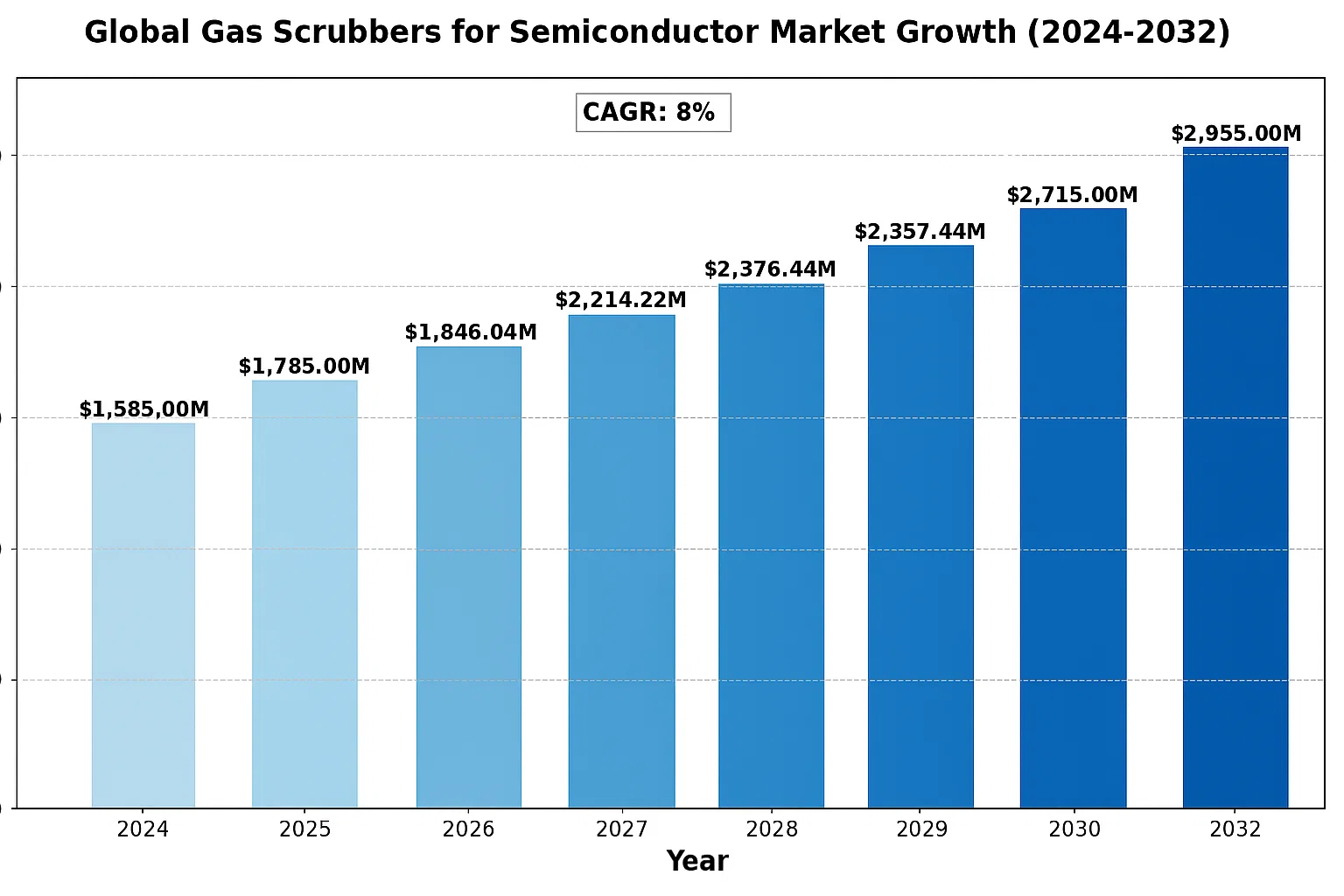

The global market for Gas Scrubbers for Semiconductor was valued at US$ 1585 million in the year 2024 and is projected to reach a revised size of US$ 2955 million by 2032, growing at a CAGR of 8% during the forecast period.

Burn Wet Type is a system that maximizes CO and Nox treatment efficiency through multi-stage combustion by passing the gas generated after use in the semiconductor process directly through the flame. Plasma Wet Type is a system that treats generated gas at a high temperature of 2000 °C or higher using DC Arc Jet Plasma in semiconductor, LCD, LED, OLED, and SOLAR processes. Wet Type is a system that treats water-soluble gas and dust through a high-pressure water pump and fine spray of water. Dry type is a system that treats harmful gases below TLV through physical and chemical adsorption as harmful gases pass through the adsorbent filling tank.

Burn Wet Type is a system that maximizes CO and Nox treatment efficiency through multi-stage combustion by passing the gas generated after use in the semiconductor process directly through the flame. Plasma Wet Type is a system that treats generated gas at a high temperature of 2000 °C or higher using DC Arc Jet Plasma in semiconductor, LCD, LED, OLED, and SOLAR processes. Wet Type is a system that treats water-soluble gas and dust through a high-pressure water pump and fine spray of water. Dry type is a system that treats harmful gases below TLV through physical and chemical adsorption as harmful gases pass through the adsorbent filling tank.

Gas scrubbers, also known as gas abatement systems or gas treatment systems, are commonly used in the to remove hazardous or unwanted gases from the exhaust streams of semiconductor manufacturing processes. These scrubbers help to ensure compliance with environmental regulations and protect the health and safety of workers.

Semiconductor manufacturing involves various processes that generate hazardous gases, such as volatile organic compounds (VOCs), toxic gases, and corrosive gases. These gases can be emitted during deposition, etching, cleaning, and other fabrication steps. Gas scrubbers are designed to capture and neutralize or remove these gases before they are released into the environment.

This report aims to provide a comprehensive presentation of the global market for Gas Scrubbers for Semiconductor, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding Gas Scrubbers for Semiconductor.

This report contains market size and forecasts of Gas Scrubbers for Semiconductor in global, including the following market information:

Global main manufacturers of gas scrubbers for semiconductor include Ebara, Global Standard Technology and Unisem, etc. The top three players hold a share about 51%. South Korea is the largest producer, holds a share around 47%, followed by Japan and Europe, with share 37% and 5%, separately. The largest market is Asia-Pacific, holds a share about 80%, followed by Americas and Europe, with around 10% and 6% market share respectively.

MARKET DYNAMICS

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=3318

FREQUENTLY ASKED QUESTIONS:

Q. What is a scrubber in the semiconductor industry?

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/07/harmonic-absorbing-filters-market.html

https://semiconductorblogs21.blogspot.com/2025/07/portable-frequency-jammers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/low-frequency-choke-market-revenue.html

https://semiconductorblogs21.blogspot.com/2025/07/power-timing-controllers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/magnetic-lighting-drivers-market-key.html

https://semiconductorblogs21.blogspot.com/2025/07/radio-frequency-rf-coaxial-isolator.html

https://semiconductorblogs21.blogspot.com/2025/07/rocker-potentiometers-market-regional.html

https://semiconductorblogs21.blogspot.com/2025/07/high-frequency-chokes-market-trends.html

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Sensor for Aircraft Market: Technology Advancements and Demand Outlook 2025-2032

By SemiconductorinsightPrerana, 2025-07-29

Sensor for Aircraft Market , Trends, Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=108111

MARKET INSIGHTS

The global Sensor for Aircraft Market size was valued at US$ 5.67 billion in 2024 and is projected to reach US$ 12.34 billion by 2032, at a CAGR of 12.0% during the forecast period 2025-2032 . The U.S. market accounted for 35% of global revenue in 2024, while China’s market is expected to grow at a faster pace due to increasing aircraft production.

Aircraft sensors are critical components that monitor various operational parameters to ensure flight safety and efficiency. These devices measure and transmit data related to pressure, temperature, position, vibration, and other variables across different aircraft systems. Key sensor types include pressure sensors (accounting for 28% market share), position sensors, temperature sensors (projected to grow at 7.2% CAGR), and radar sensors used in navigation and collision avoidance systems.

The market growth is driven by increasing aircraft deliveries (with Boeing and Airbus forecasting demand for over 40,000 new aircraft through 2040), stringent safety regulations, and the adoption of advanced avionics. Recent developments include Honeywell’s 2024 launch of next-gen MEMS-based pressure sensors with 30% improved accuracy, while TE Connectivity introduced a compact temperature sensor with 50% faster response time for engine monitoring applications. Other major players like Safran and UTC Aerospace Systems are investing heavily in IoT-enabled predictive maintenance solutions incorporating advanced sensor technologies.

Modern aircraft generate over 10 terabytes of sensor data per flight, overwhelming existing data processing architectures. Airlines report that less than 30% of collected sensor data is currently analyzed due to bandwidth limitations and computational constraints. The rapid proliferation of IIoT-enabled sensors compounds this challenge, requiring carriers to invest in expensive edge computing infrastructure capable of processing real-time data streams during flight operations.

List of Key Sensor for Aircraft Companies Profiled

- Honeywell International (U.S.)

- TE Connectivity Corporation (Switzerland)

- UTC Aerospace Systems (U.S.)

- Zodiac Aerospace (France)

- Ametek (U.S.)

- Safran Electronics & Defense (France)

- Curtiss-Wright Corporation (U.S.)

- Thales Group (France)

- Raytheon Company (U.S.)

- General Electric (U.S.)

Segment Analysis:

By Type

Pressure Sensor Segment Leads Due to Critical Role in Aircraft Performance Monitoring

The market is segmented based on type into:

- Pressure Sensor

- Position Sensor

- Force Sensor

- Temperature Sensor

- Vibration Sensor

- Radar Sensor

- Others

By Application

Flight Controls Segment Dominates Due to Increasing Demand for Enhanced Aviation Safety

The market is segmented based on application into:

- Air Pressure Level Detection

- Doors and Slides Locking

- Flight Controls

- Landing Gears

- Cabin and Cargo Environment Controls

- Others

Regional Analysis: Sensor for Aircraft Market

North America

The North American aircraft sensor market is driven by advanced aerospace technology adoption and a strong emphasis on safety and operational efficiency . The U.S., as the largest market contributor, benefits from heavy defense budgets and commercial airline investments, with sensor demand fueled by NextGen air traffic modernization initiatives. Regulatory bodies like the FAA mandate precision sensors for flight control, engine monitoring, and environmental systems , pushing innovations in IoT-enabled and AI-integrated sensor solutions. Key players such as Honeywell International and UTC Aerospace Systems dominate due to long-term contracts with OEMs and aftermarket service providers. While Canada and Mexico have smaller markets, increasing MRO (Maintenance, Repair, Overhaul) activities and rising passenger traffic offer growth opportunities.

Europe

Europe’s aircraft sensor market thrives on stringent aviation safety regulations and sustainability goals under EASA (European Union Aviation Safety Agency). Countries like Germany and France lead in composite-material-based sensor integration , reducing aircraft weight and emissions. The A350 and A320neo programs heavily utilize advanced pressure and temperature sensors, with suppliers like Safran Electronics & Defense and Thales Group expanding production capacities. Stringent noise and emission norms further propel innovations in vibration and radar sensors for predictive maintenance. However, geopolitical tensions and supply-chain disruptions pose challenges for sensor procurement, particularly due to reliance on specialized semiconductor components.

Asia-Pacific

As the fastest-growing region , Asia-Pacific benefits from booming air travel demand and fleet expansions, particularly in China and India. China’s COMAC C919 program and India’s UDAN scheme drive demand for localized sensor manufacturing . While Japan and South Korea focus on high-precision MEMS sensors for avionics, Southeast Asian markets prioritize cost-effective solutions favoring suppliers like TE Connectivity . The surge in low-cost carriers and airport expansions necessitates sensors for cabin monitoring and landing gear systems , though quality standardization and aftermarket service gaps remain hurdles. China’s dominance in rare-earth materials also influences pricing dynamics for sensor components.

South America

Market growth in South America is moderate , constrained by economic instability but supported by regional airline expansions in Brazil and Argentina. Sensor adoption is primarily retrofit-driven, with older fleets requiring upgrades for fuel efficiency and emissions compliance . Brazil’s Embraer collaborations with global sensor suppliers create pockets of innovation, yet currency volatility limits large-scale investments. Infrastructure bottlenecks and uneven regulatory enforcement slow OEM adoption of cutting-edge sensor technologies, with price sensitivity favoring mid-tier suppliers.

Middle East & Africa

The Gulf region, led by the UAE and Saudi Arabia, is a high-potential market due to luxury airline growth and aviation hub strategies. The demand for real-time engine health monitoring sensors is rising, supported by fleets like Emirates and Qatar Airways. Africa’s market remains nascent, with limited penetration due to underdeveloped MRO networks and budget constraints. However, air traffic growth in Nigeria and Ethiopia signals long-term opportunities. Middle Eastern governments’ investments in smart airports and drone technologies could accelerate sensor adoption, contingent on technology transfer partnerships with global leaders.

Other Challenges

Cybersecurity Vulnerabilities

The increasing connectivity of aircraft sensor networks has expanded the attack surface for malicious actors. Recent vulnerability assessments revealed that over 40% of aviation sensor networks lack adequate encryption for data transmission between components. The FAA has issued multiple security bulletins mandating enhanced protections for sensor data buses following demonstrated spoofing attacks on position sensor networks.

Technological Obsolescence

The rapid pace of sensor innovation creates maintenance challenges for operators maintaining mixed-generation fleets. Many current sensor models face component obsolescence within 7-10 years as manufacturers transition to newer technologies, forcing costly retrofits or maintaining dual supply chains for legacy systems. This issue particularly impacts regional airlines operating aircraft beyond typical 20-year service lives.

MARKET OPPORTUNITIES

AI-Enabled Predictive Analytics Creates New Sensor Value Proposition

Integration of artificial intelligence with sensor networks enables truly predictive maintenance capabilities, with potential to reduce unplanned maintenance events by up to 45%. Airlines implementing AI-driven sensor analytics report 30% improvements in component lifespan predictions. This technological convergence is driving development of self-diagnosing sensor systems capable of predicting their own maintenance needs before failure, creating significant value for operators.

Urban Air Mobility Sector Emerging as High-Growth Sensor Market

The emerging eVTOL sector represents a $25 billion opportunity for specialized sensor solutions by 2030. These aircraft require novel sensor arrays for vertiport navigation, obstacle detection, and distributed electric propulsion monitoring. Major sensor manufacturers are collaborating with eVTOL developers to create ultra-compact, lightweight sensing packages meeting the stringent size-weight-power constraints of urban air vehicles while maintaining aviation-grade reliability.

MARKET DYNAMICS

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=108111

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Sensor for Aircraft Market?

Which key companies operate in this market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/07/harmonic-absorbing-filters-market.html

https://semiconductorblogs21.blogspot.com/2025/07/portable-frequency-jammers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/low-frequency-choke-market-revenue.html

https://semiconductorblogs21.blogspot.com/2025/07/power-timing-controllers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/magnetic-lighting-drivers-market-key.html

https://semiconductorblogs21.blogspot.com/2025/07/radio-frequency-rf-coaxial-isolator.html

https://semiconductorblogs21.blogspot.com/2025/07/rocker-potentiometers-market-regional.html

https://semiconductorblogs21.blogspot.com/2025/07/high-frequency-chokes-market-trends.html

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Human Motion Sensor Market: Key Players, Regional Analysis, and Projections 2025-2032

By SemiconductorinsightPrerana, 2025-07-29

Human Motion Sensor Market , Trends, Business Strategies 2025-2032

MARKET INSIGHTS

The global Human Motion Sensor Market size was valued at US$ 4.45 billion in 2024 and is projected to reach US$ 9.78 billion by 2032, at a CAGR of 12.1% during the forecast period 2025-2032 . The U.S. market accounted for 35% of global revenue share in 2024, while China is expected to witness the fastest growth at 10.2% CAGR through 2032.

Human motion sensors are electronic devices that detect physical movement through various technologies including infrared, ultrasonic, microwave, and dual-technology systems. These sensors play a critical role in security systems, smart home automation, industrial applications, and healthcare monitoring by converting motion into measurable signals. Key product categories include passive infrared (PIR), microwave, ultrasonic, and dual-technology sensors, each serving distinct applications based on sensitivity and environmental requirements.

The market expansion is driven by increasing adoption in security systems, where motion detectors accounted for over 40% of the market share in 2024. Rising smart home penetration, with global adoption reaching 15% of households in 2023, further accelerates demand. Technological advancements such as AI-powered motion analytics and IoT integration are creating new growth opportunities. Major players including Honeywell International, Robert Bosch GmbH, and Panasonic continue to dominate the competitive landscape, collectively holding 55% market share through continuous innovation in sensor accuracy and energy efficiency.

List of Key Human Motion Sensor Companies Profiled

- Honeywell International (U.S.)

- Panasonic Corporation (Japan)

- Robert Bosch GmbH (Germany)

- Murata Manufacturing (Japan)

- Cypress Semiconductor (U.S.)

- Elmos Semiconductor (Germany)

- Epson Toyocom (Japan)

- Atmel (U.S.)

Segment Analysis:

By Type

Heat Detector Segment Dominates the Market Due to Widespread Adoption in Smart Security Systems

The market is segmented based on type into:

- Heat detectors

- Subtypes: Fixed temperature, rate-of-rise, and combination

- Smoke detectors

- Subtypes: Ionization, photoelectric, and dual-sensor

- Infrared sensors

- Ultrasonic sensors

- Microwave sensors

- Others

By Application

Security Application Segment Leads Due to Increasing Demand for Surveillance Systems

The market is segmented based on application into:

- Security

- Commercial

- Smart homes

- Military and defense

- Industrial automation

By Technology

Passive Infrared (PIR) Technology Segment Dominates Due to Energy Efficiency

The market is segmented based on technology into:

- Passive Infrared (PIR)

- Active ultrasonic

- Microwave

- Tomographic

By Installation Type

Wireless Installation Segment Shows Strong Growth Due to Ease of Deployment

The market is segmented based on installation type into:

- Wired

- Wireless

Regional Analysis: Human Motion Sensor Market

North America

The North American human motion sensor market is driven by strong demand in security applications , smart home automation, and commercial establishments. The U.S., as the largest contributor, accounts for over 65% of the regional market share , fueled by technological advancements and high adoption rates of IoT devices. Strict regulatory frameworks, such as those enforced by the Federal Communications Commission (FCC) , ensure product reliability and safety. Additionally, investments in smart city initiatives and rising concerns over energy efficiency further propel market growth. Canada and Mexico also show steady expansion, particularly in retail and healthcare applications, though adoption lags slightly behind due to infrastructure constraints.

Europe

Europe’s human motion sensor market thrives on strict privacy and data protection laws , such as the General Data Protection Regulation (GDPR) , which influence sensor deployment in security and smart home sectors. Germany and the U.K. lead regional adoption with high consumer awareness and industrial automation initiatives . The European Commission’s push for energy-efficient building solutions under the Energy Performance of Buildings Directive (EPBD) further accelerates demand. While Western Europe dominates, Eastern Europe is emerging as a lucrative market with manufacturing hubs in Poland and Hungary integrating motion sensors for industrial automation. However, price sensitivity and economic uncertainties in some regions slightly hinder growth.

Asia-Pacific

As the fastest-growing region , the Asia-Pacific market is fueled by rapid urbanization, industrialization, and smart city projects , particularly in China, Japan, and India. China alone captures over 40% of the regional market , driven by government-backed smart infrastructure projects. Japan focuses on advanced robotics and healthcare applications , while India sees growing demand in security and commercial sectors . Cost-effective sensor technologies dominate the market, although a shift toward higher-end solutions is emerging. Challenges include lack of standardization and fragmented regulatory policies across countries, but long-term growth prospects remain strong due to increasing disposable incomes and IoT adoption .

South America

The human motion sensor market in South America remains nascent but promising , with Brazil and Argentina spearheading adoption in commercial and residential sectors. Brazil’s demand is largely security-driven , particularly in urban areas facing rising theft concerns. Argentina, though smaller in scale, is witnessing growth in retail and industrial automation . However, broader market expansion is constrained by economic instability, limited investment in R&D, and lack of robust infrastructure . Despite these challenges, increasing digitization and smart home trends , coupled with government efforts toward modernization, offer potential for future market growth.

Middle East & Africa

This region presents a mixed adoption landscape —while Gulf Cooperation Council (GCC) countries like the UAE and Saudi Arabia invest heavily in smart city initiatives and security infrastructure , sub-Saharan Africa lags due to limited technological penetration. The UAE leads with projects like Smart Dubai , integrating motion sensors in public and private sectors. Saudi Arabia follows closely, focusing on mega-projects such as NEOM . However, high costs, geopolitical instability, and uneven regulatory frameworks slow broader regional adoption. Nonetheless, long-term investments in urbanization and digitization projects indicate gradual market potential.

MARKET DYNAMICS

The human motion sensor market faces persistent challenges related to reliability and false alarms, which undermine customer confidence and satisfaction. Industry studies indicate that false trigger rates for conventional PIR sensors can exceed 15% in certain environments, leading to user frustration and increased operational costs. These reliability issues stem from various factors including pet movements, shifting sunlight patterns, and ventilation system disturbances that can inadvertently activate sensors. The challenge intensifies in complex environments where multiple detection zones overlap or in applications requiring precise movement differentiation.

Integration Complexities

The proliferation of smart home platforms and protocols creates compatibility issues, with many consumers facing difficulties integrating motion sensors from different manufacturers into cohesive systems.

Power Consumption

Battery-powered sensor nodes in wireless systems face limitations in energy efficiency, often requiring frequent maintenance and replacement that increases total cost of ownership.

The human motion sensor market stands to benefit significantly from emerging applications in healthcare monitoring and smart retail environments. In healthcare settings, advanced motion detection systems enable remote patient monitoring and fall detection for elderly care, with the global market for such applications projected to grow at 12% CAGR through 2030. Retailers are increasingly adopting people counting sensors and gesture recognition systems to optimize store layouts and create interactive shopping experiences. These novel applications demonstrate the versatility of motion sensing technology beyond traditional security uses.

Additionally, the integration of motion sensors with augmented reality systems presents exciting opportunities for gaming, training simulations, and industrial applications. The development of miniaturized, low-power sensors compatible with wearable devices is opening new avenues in fitness tracking and sports analytics. As technology continues to evolve, these innovative applications will drive the next phase of growth in the human motion sensor market.

Strategic partnerships between sensor manufacturers and software developers are accelerating innovation in this space, with collaborations focused on creating more intelligent, context-aware motion detection systems. The convergence of edge computing with motion sensor networks promises to unlock new capabilities in real-time analytics and predictive maintenance applications across various industries.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=108110

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Human Motion Sensor Market?

Which key companies operate in Global Human Motion Sensor Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/07/harmonic-absorbing-filters-market.html

https://semiconductorblogs21.blogspot.com/2025/07/portable-frequency-jammers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/low-frequency-choke-market-revenue.html

https://semiconductorblogs21.blogspot.com/2025/07/power-timing-controllers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/magnetic-lighting-drivers-market-key.html

https://semiconductorblogs21.blogspot.com/2025/07/radio-frequency-rf-coaxial-isolator.html

https://semiconductorblogs21.blogspot.com/2025/07/rocker-potentiometers-market-regional.html

https://semiconductorblogs21.blogspot.com/2025/07/high-frequency-chokes-market-trends.html

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Inductive Voltage Dividers Market: Regional Trends, Opportunities, and Risks 2025-2032

By SemiconductorinsightPrerana, 2025-07-29

Inductive Voltage Dividers Market, Trends, Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=108152

MARKET INSIGHTS

The global Inductive Voltage Dividers Market size was valued at US$ 198 million in 2024 and is projected to reach US$ 334 million by 2032, at a CAGR of 7.7% during the forecast period 2025-2032 . While North America currently dominates the market share, the Asia-Pacific region is expected to witness the fastest growth due to expanding industrial automation.

An inductive voltage divider is a precision electrical instrument composed of interconnected multi-tap iron core coils that provide an output voltage proportional to a selected ratio of input voltage. These devices serve critical functions in measurement and calibration systems across industries, offering advantages like high accuracy (typically ±0.001% or better), excellent stability, and minimal phase shift compared to resistive dividers.

The market growth is primarily driven by increasing demand from the aerospace and defense sectors, where precision voltage measurement is critical for avionics and radar systems. Furthermore, advancements in power electronics and the renewable energy sector are creating new opportunities, particularly for AC/DC voltage divider variants. Key players like Ross Engineering Corporation and TT Electronics are expanding their product portfolios to cater to these emerging applications.

List of Key Inductive Voltage Divider Manufacturers

- Ross Engineering Corporation (U.S.)

- erivolt (U.S.)

- Ludlum Measurements Inc. (ET Enterprises Limited) (U.K.)

- TT Electronics (U.K.)

- Schniewindt (Germany)

- SRT Resistor Technology GmbH

- V (Germany)

- Xianyang Yongtai Power Electronic Technology (China)

- Wuhan Huayi Electric Power Technology (China)

- Wuhan Guoshi Electric Equipment Co., LTD (China)

- Wuhan Nanrui Electric (China)

- Shanghai Laiyang Electric Technology (China)

Segment Analysis:

By Type

AC and DC Voltage Divider Segment Dominates Due to Widespread Applications in Power Distribution Systems

The market is segmented based on type into:

- AC and DC Voltage Divider

- Subtypes: Precision, High-frequency, and Multi-range

- Pulse Voltage Divider

- Others

By Application

Industrial Segment Holds Major Share Owing to Increased Automation and Energy Management Requirements

The market is segmented based on application into:

- Defence

- Aerospace

- Industrial

- Others

By End User

Power Generation Sector Leads Market Adoption Due to Critical Voltage Regulation Needs

The market is segmented based on end user into:

- Power Generation Companies

- Manufacturing Units

- Research Laboratories

- Military and Defense Establishments

Regional Analysis: Inductive Voltage Dividers Market

North America

The North American market for inductive voltage dividers is driven by advanced technological adoption, particularly in the defense and aerospace sectors , where high-precision voltage measurement is critical. The U.S. holds the dominant share, backed by substantial investments in electrical infrastructure modernization and research & development. The region’s stringent regulatory standards for safety and performance in industrial automation further fuel demand. Additionally, growing emphasis on renewable energy integration into power grids creates opportunities for advanced voltage measurement solutions , including inductive voltage dividers. Leading manufacturers like Ross Engineering Corporation and Verivolt have a strong presence, leveraging innovation to maintain competitiveness.

Europe

Europe demonstrates steady growth in the inductive voltage divider market, supported by strict industrial safety regulations and expanding applications in aerospace and renewable energy projects . Countries like Germany and the UK lead in adoption, owing to their well-established electronics and precision engineering sectors . The EU’s push for grid modernization and smart energy solutions is driving demand for high-accuracy voltage measurement tools , boosting the market. Challenges include rising costs due to supply chain complexities , but European manufacturers like SRT Resistor Technology GmbH and TT Electronics continue to innovate with low-loss, high-efficiency designs.

Asia-Pacific

This region is the fastest-growing market, with China and Japan at the forefront due to large-scale industrialization and infrastructure expansion . The increasing demand for power electronics in manufacturing processes , coupled with rising automation in India and Southeast Asia , boosts the adoption of inductive voltage dividers. China’s dominance is reinforced by local manufacturers such as Xianyang Yongtai Power Electronic Technology , catering to both domestic and export markets. While cost-effective solutions prevail due to competitive pricing pressures, there is a gradual shift toward high-performance, durable solutions as industries prioritize efficiency and reliability.

South America

The market in South America is emerging, with Brazil and Argentina showing moderate growth due to expanding industrialization and energy infrastructure projects . However, limited investment in R&D and economic volatility hinder rapid market penetration for advanced inductive voltage divider solutions. Some niche applications in mining and oil & gas industries drive demand, but manufacturers face challenges in scaling production due to inconsistent regulatory frameworks and reliance on imported components. Nonetheless, gradual investments in renewable energy integration present long-term opportunities.

Middle East & Africa

This region exhibits nascent but promising growth , primarily fueled by infrastructure development in GCC countries and expanding industrial automation in South Africa . The demand for high-precision voltage measurement tools remains relatively low compared to other regions, focusing mostly on oil & gas and utility sectors . Key barriers include limited local manufacturing capabilities and dependency on imports . However, rising awareness of smart grid technologies and foreign investments in energy projects offer future potential for market expansion, particularly in UAE and Saudi Arabia .

MARKET DYNAMICS

The aerospace and defense sectors are experiencing significant growth in demand for high-precision electronic components, with inductive voltage dividers playing a crucial role in accurate voltage measurement applications. These sectors require robust solutions for avionics, radar systems, and electronic warfare equipment where measurement accuracy directly impacts system performance. The global defense budget has consistently increased, with many nations allocating over 2% of their GDP to military expenditures, creating a favorable environment for specialized electronic components. Furthermore, the transition to next-generation aircraft with advanced electronic systems is driving adoption of high-precision voltage measurement solutions across commercial and military aviation sectors.

The rapid advancement of Industry 4.0 technologies has significantly increased the need for precise voltage measurement and control systems in industrial environments. Inductive voltage dividers provide accurate and stable performance in harsh industrial conditions, making them ideal for factory automation, robotics, and process control applications. Recent developments in smart manufacturing have accelerated adoption rates, with industrial automation investments growing at approximately 8% annually. The ability of inductive voltage dividers to maintain accuracy across wide temperature ranges and in electromagnetic interference-heavy environments makes them particularly valuable for modern automated production facilities.

The global shift toward renewable energy sources is creating significant opportunities for inductive voltage divider applications in power conversion and distribution systems. Solar and wind energy installations require precise voltage measurement for efficient power conditioning and grid integration. With renewable energy capacity projected to grow substantially over the next decade, the demand for reliable voltage division solutions in this sector is expected to increase correspondingly. Notably, inductive voltage dividers offer advantages in high-voltage applications common in renewable energy systems, including better noise immunity and temperature stability compared to alternative solutions.

MARKET CHALLENGES

The production of high-performance inductive voltage dividers involves sophisticated manufacturing processes and specialized materials, resulting in substantial production costs. The need for precision-wound coils and high-quality magnetic core materials contributes significantly to the component cost structure. This economic barrier makes it challenging for smaller manufacturers to compete in the market and potentially limits adoption in price-sensitive applications. Furthermore, the specialized nature of production creates longer lead times compared to more conventional voltage division solutions, potentially affecting supply chain dynamics.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=108152

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Inductive Voltage Dividers Market?

Which key companies operate in Global Inductive Voltage Dividers Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/07/harmonic-absorbing-filters-market.html

https://semiconductorblogs21.blogspot.com/2025/07/portable-frequency-jammers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/low-frequency-choke-market-revenue.html

https://semiconductorblogs21.blogspot.com/2025/07/power-timing-controllers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/magnetic-lighting-drivers-market-key.html

https://semiconductorblogs21.blogspot.com/2025/07/radio-frequency-rf-coaxial-isolator.html

https://semiconductorblogs21.blogspot.com/2025/07/rocker-potentiometers-market-regional.html

https://semiconductorblogs21.blogspot.com/2025/07/high-frequency-chokes-market-trends.html

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Multi-Phase Static Inverters Market: Trends, Growth Opportunities, and Forecast 2025-2032

By SemiconductorinsightPrerana, 2025-07-29

Multi-Phase Static Inverters Market, Trends, Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=108151

MARKET INSIGHTS

The global Multi-Phase Static Inverters Market size was valued at US$ 2.89 billion in 2024 and is projected to reach US$ 6.45 billion by 2032, at a CAGR of 12.3% during the forecast period 2025-2032 . The U.S. market alone accounted for 25% of global revenue in 2024, while China is expected to witness the fastest growth with an estimated 9.1% CAGR through 2032.

Multi-phase static inverters are critical power conversion devices that transform DC electricity into stable AC power with precise frequency and voltage regulation. These systems consist of three key components: an inverter bridge for power conversion, control logic for operational management, and filter circuits to ensure clean output. The technology finds extensive applications across transport infrastructure, telecommunications, and industrial sectors where reliable power conversion is essential.

Market expansion is primarily driven by increasing electrification in transportation and growing renewable energy integration. The high power inverter segment, which represented 68% of total sales in 2024, is anticipated to maintain dominance due to industrial demand. Key players like Hitachi America Ltd. and Exide Industries continue to innovate, with recent developments focusing on higher efficiency models exceeding 98% conversion rates. While grid modernization initiatives boost demand, supply chain constraints for power semiconductors present ongoing challenges for manufacturers.

List of Key Multi-Phase Static Inverters Companies Profiled

- Microtek (India)

- UTL Solar (India)

- Exide Industries (India)

- Polycab (India)

- EAPRO Global Ltd. (China)

- Growatt New Energy (China)

- Applied Power Systems (U.S.)

- Hitachi America Ltd. (U.S.)

- Power Machines (Russia)

- Protonix Fortuner India Private Limited (India)

- Tanishq Engineering (India)

- Jiangsu Watson Electrical Equipment (China)

- Ruian An Chuan Electronics (China)

- Vesige Electric (Shan Dong) (China)

- Jinan Xinyuhua Energy Technology (China)

- JIANGSU CHANGRONG ELECTRICAL APPLIANCE (China)

- Hunan Vicruns Electric Technology (China)

Segment Analysis:

By Type

High Power Inverter Segment Holds Significant Market Share Due to Industrial and Commercial Applications

The market is segmented based on type into:

- High Power Inverter

- Low Power Inverter

By Application

Transportation Segment Leads Market Owing to Growing Electric Vehicle Infrastructure

The market is segmented based on application into:

- Transport

- Communication

- Others

By End User

Industrial Sector Dominates Market Share Due to High-Voltage Power Conversion Needs

The market is segmented based on end user into:

- Industrial

- Commercial

- Residential

Regional Analysis: Multi-Phase Static Inverters Market

North America

The North American market for multi-phase static inverters is driven by robust demand from transport and communication sectors , supported by significant infrastructure investments. The U.S. accounts for the largest share, with government initiatives like the Infrastructure Investment and Jobs Act fueling modernization efforts. High-power inverters dominate applications in rail and aerospace, where energy efficiency and reliability are critical. Additionally, stringent regulatory standards on power quality and emissions push manufacturers toward advanced, high-performance inverters . However, the high cost of installation and maintenance poses a challenge for widespread adoption in smaller industrial applications.

Europe

Europe’s market thrives on strict energy efficiency directives , particularly those under the EU Green Deal , which emphasize renewable integration and grid stability. Germany leads in adoption due to its industrial automation and renewable energy transitions. The transport sector , especially railways, relies heavily on multi-phase static inverters for stable power conversion. Meanwhile, technological collaboration between manufacturers and research institutions accelerates developments in low-power, high-efficiency inverters . Despite steady growth, market expansion faces constraints from fluctuating raw material costs and competition from regional Asian players offering more cost-effective solutions.

Asia-Pacific

As the fastest-growing region , Asia-Pacific is propelled by large-scale infrastructure projects and industrialization in China and India. The region benefits from local manufacturing hubs , reducing production costs and boosting adoption in communication and transport applications. China’s push for electric vehicle (EV) charging infrastructure and high-speed rail networks significantly drives demand. Meanwhile, Southeast Asian nations are gradually increasing investments in smart grid technologies , though market penetration remains uneven due to price-sensitive end-users . The dominance of local players, such as Growatt New Energy and Hitachi , intensifies competition but fosters affordability.

South America

The South American market shows moderate growth , largely influenced by Brazil and Argentina’s fledgling industrial and transport sectors . Demand is rising for low-power inverters in telecommunication towers and microgrid applications , particularly in remote areas. However, economic instability and underdeveloped electrical infrastructure hinder large-scale projects, delaying the adoption of high-power solutions. Government initiatives to upgrade public transport systems present future opportunities, but reliance on imported inverters keeps costs prohibitive for many small-to-medium enterprises.

Middle East & Africa

This region represents an emerging market , with growth concentrated in GCC countries and South Africa. Investments in oil & gas, renewable energy , and urban transport fuel the need for reliable power conversion solutions. High-power inverters are increasingly deployed in desalination plants and metro rail projects , driven by government funding. However, limited local manufacturing and dependence on imports slow market expansion. Long-term potential lies in solar energy integration , where inverters play a critical role, but affordability remains a barrier across most African nations.

MARKET DYNAMICS

While multi-phase static inverters offer significant technical advantages, their adoption faces challenges related to upfront costs and installation complexity. Industrial-grade systems require substantial capital investment, often deterring small and medium enterprises. The sophisticated control systems and power electronics involved contribute significantly to the overall system cost.

Thermal Management Issues

Managing heat dissipation in high-power inverter systems remains an engineering challenge that impacts reliability and lifespan. Proper cooling systems add to both installation complexity and ongoing maintenance requirements.

Grid Compliance Complexity

Meeting stringent grid interconnection standards across different regions requires continuous design adaptations, increasing development costs and time-to-market for manufacturers.

The multi-phase static inverter market faces constraints from ongoing supply chain challenges affecting critical components. Power semiconductors, particularly IGBTs and silicon carbide devices, have experienced periodic shortages, delaying production timelines. These components often have long lead times and come from concentrated supply bases, creating vulnerabilities in the value chain.

Additionally, the specialized workforce required for inverter system design and commissioning remains in short supply. The combination of electrical engineering and power electronics expertise needed is rare, slowing deployment schedules for large projects.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=108151

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Multi-Phase Static Inverters Market?

Which key companies operate in this market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/07/harmonic-absorbing-filters-market.html

https://semiconductorblogs21.blogspot.com/2025/07/portable-frequency-jammers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/low-frequency-choke-market-revenue.html

https://semiconductorblogs21.blogspot.com/2025/07/power-timing-controllers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/magnetic-lighting-drivers-market-key.html

https://semiconductorblogs21.blogspot.com/2025/07/radio-frequency-rf-coaxial-isolator.html

https://semiconductorblogs21.blogspot.com/2025/07/rocker-potentiometers-market-regional.html

https://semiconductorblogs21.blogspot.com/2025/07/high-frequency-chokes-market-trends.html

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Safety Circuit Breaker Market: Competitive Strategies and Growth Projections 2025-2032

By SemiconductorinsightPrerana, 2025-07-29

Safety Circuit Breaker Market , Trends, Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=108150

MARKET INSIGHTS

The global Safety Circuit Breaker Market size was valued at US$ 4.23 billion in 2024 and is projected to reach US$ 7.89 billion by 2032, at a CAGR of 9.4% during the forecast period 2025-2032.

Safety circuit breakers are critical protective devices designed to automatically interrupt electrical current flow when faults such as short circuits or overloads are detected. These devices safeguard electrical systems from damage by immediately disconnecting the circuit during abnormal conditions. The market offers various types including high-voltage circuit-breakers (rated above 1kV) and low-voltage circuit-breakers (below 1kV), with applications spanning residential, commercial, and industrial sectors.

The market growth is driven by increasing electrification projects, stringent safety regulations, and rising infrastructure development worldwide. North America currently dominates with 32% market share, while Asia-Pacific shows the fastest growth due to rapid urbanization. Key players like Schneider Electric, Siemens, and ABB are investing in smart circuit breaker technologies with IoT capabilities, further propelling market expansion. The high-voltage segment is expected to grow at 7.1% CAGR through 2032, driven by renewable energy integration projects.

List of Key Safety Circuit Breaker Manufacturers

- Schneider Electric SA (France)

- SIEMENS AG (Germany)

- SMC Corporation (Japan)

- Circuit Breaker Analyzer (Group CBS) (UK)

- Scope T & M (India)

- Crest Test Systems (UK)

- Huatian Electric (China)

- General Electric (U.S.)

- ABB (Switzerland)

- Westinghouse Electric Corporation (U.S.)

- PACS Industries (U.S.)

- HV Hipot Electric Co., Ltd. (China)

- Shijiazhuang Handy Technology (China)

- Wuhan Huaying Power (China)

Segment Analysis:

By Type

Low-Voltage Segment Leads Due to Widespread Use in Residential and Commercial Applications

The market is segmented based on type into:

- High-Voltage Circuit-Breaker

- Subtypes: Air-blast, Oil, Vacuum, SF6, and others

- Low-Voltage Circuit-Breaker

- Subtypes: Miniature, Molded Case, and others

By Application

Industrial Segment Dominates Owing to Critical Need for Electrical Safety in Manufacturing

The market is segmented based on application into:

- Residential

- Commercial

- Industrial

- Utility

- Others

By Voltage Range

Below 1 kV Segment Accounts for Largest Share Due to Consumer Electronics Demand

The market is segmented based on voltage range into:

- Below 1 kV

- 1-15 kV

- 15-38 kV

- Above 38 kV

By End-Use Industry

Construction Sector Shows Strong Growth Potential with Rising Infrastructure Development

The market is segmented based on end-use industry into:

- Construction

- Manufacturing

- Energy & Power

- Oil & Gas

- Others

Regional Analysis: Safety Circuit Breaker Market

North America

The North American safety circuit breaker market is characterized by strong regulatory frameworks and a mature electrical infrastructure, driving demand for high-performance safety solutions. The U.S. leads the region, with increasing emphasis on grid modernization and renewable energy integration. Stringent safety standards set by organizations such as UL (Underwriters Laboratories) and the National Electrical Code (NEC) ensure that circuit breakers meet rigorous safety and reliability criteria. Investments in smart grid technologies and industrial automation further fuel the adoption of advanced circuit breakers with IoT-enabled monitoring capabilities. However, market growth faces challenges due to high product costs and competition from refurbished equipment in certain segments.

Europe

Europe’s safety circuit breaker market benefits from stringent EU directives on electrical safety and energy efficiency, including the Low Voltage Directive (LVD) and Ecodesign regulations. Countries such as Germany, France, and the U.K. prioritize smart energy solutions, supporting demand for modular and digital circuit breakers. The region’s focus on Industry 4.0 and renewable energy expansion, particularly in wind and solar applications, drives the need for safety-compliant electrical protection devices. Additionally, the phase-out of older circuit breakers in favor of modern, eco-friendly alternatives contributes to steady market growth. Nevertheless, pricing pressures from Asian manufacturers and prolonged supply chain disruptions remain key challenges.

Asia-Pacific

The Asia-Pacific region dominates the global safety circuit breaker market in terms of volume, driven by rapid urbanization, industrialization, and infrastructure expansion. China and India are the primary growth engines, with large-scale investments in power distribution networks and manufacturing hubs. While cost-sensitive markets favor low-voltage circuit breakers for residential and commercial applications, increasing industrial automation is boosting demand for high-voltage variants. Government initiatives like India’s Smart Cities Mission and China’s infrastructure development plans create substantial opportunities. However, inconsistent regulatory enforcement and the prevalence of counterfeit products pose risks to quality and safety standards in some areas.

South America

The safety circuit breaker market in South America is growing steadily, supported by gradual electrical infrastructure upgrades and industrial sector development. Brazil and Argentina lead demand, with investments in energy distribution and expanding commercial construction projects. Despite potential, economic instability and limited access to advanced technology slow market penetration. Manufacturers must navigate fluctuating import regulations and price sensitivity among local buyers. Nevertheless, rising awareness of electrical safety and gradual regulatory improvements signal longer-term market expansion.

Middle East & Africa

This region presents a developing but promising market for safety circuit breakers. GCC countries, especially the UAE and Saudi Arabia, are investing heavily in smart infrastructure and renewable energy projects, increasing the need for reliable circuit protection. In Africa, electrification initiatives in countries like South Africa and Nigeria drive demand, though political and economic uncertainties restrict faster adoption. While affordability remains a concern, the market is expected to grow as industrialization and urbanization accelerate in key regions.

MARKET DYNAMICS

The safety circuit breaker market is characterized by intense competition among established players and emerging manufacturers, particularly from Asia. This competitive landscape has led to significant price pressures, forcing companies to balance quality with cost competitiveness. While major brands maintain premium pricing for high-end products, regional players often undercut prices with more economical alternatives. This dynamic creates challenges in maintaining profitability while investing in research and development for next-generation products.

Technological Obsolescence

The rapid pace of technological advancement in electrical systems means that circuit breaker designs must constantly evolve. Manufacturers face the challenge of keeping their product lines current while managing existing inventory and production processes.

Supply Chain Disruptions

Global supply chain volatility continues to impact the availability of key components such as specialized contacts and trip mechanisms. These disruptions can lead to production delays and increased costs that are difficult to pass on to customers in a competitive market.

The integration of IoT capabilities and smart monitoring features in circuit breakers represents a significant market opportunity. Smart circuit breakers that provide real-time performance data, remote control functionality, and predictive maintenance alerts are gaining traction. These advanced systems help prevent electrical failures before they occur, reducing downtime and maintenance costs. The industrial IoT sector’s expansion is expected to drive a compound annual growth rate of over 15% for smart circuit breakers through the forecast period.

Furthermore, the renewable energy sector’s rapid expansion presents substantial opportunities for specialized safety circuit breakers. Solar and wind power systems require circuit protection solutions capable of handling variable loads and harsh environmental conditions. Manufacturers developing products specifically for these applications stand to benefit from the global shift toward clean energy.

The increasing focus on building automation and smart cities is another area creating demand for innovative safety circuit breaker solutions. As urban infrastructure becomes more connected and energy-efficient, the need for reliable, intelligent circuit protection will continue to grow across commercial and municipal applications.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=108150

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Safety Circuit Breaker Market?

Which key companies operate in Global Safety Circuit Breaker Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/07/harmonic-absorbing-filters-market.html

https://semiconductorblogs21.blogspot.com/2025/07/portable-frequency-jammers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/low-frequency-choke-market-revenue.html

https://semiconductorblogs21.blogspot.com/2025/07/power-timing-controllers-market.html

https://semiconductorblogs21.blogspot.com/2025/07/magnetic-lighting-drivers-market-key.html

https://semiconductorblogs21.blogspot.com/2025/07/radio-frequency-rf-coaxial-isolator.html

https://semiconductorblogs21.blogspot.com/2025/07/rocker-potentiometers-market-regional.html

https://semiconductorblogs21.blogspot.com/2025/07/high-frequency-chokes-market-trends.html

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

AC Phase Angle Transducers Market: Innovations, Trends, and Market Size Forecast 2025-2032

By SemiconductorinsightPrerana, 2025-07-29

AC Phase Angle Transducers Market , Trends, Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=108149

MARKET INSIGHTS

The global AC Phase Angle Transducers Market size was valued at US$ 123 million in 2024 and is projected to reach US$ 189 million by 2032, at a CAGR of 6.3% during the forecast period 2025-2032 .

AC Phase Angle Transducers are critical control devices in AC power conversion systems that generate reference signals synchronized with input voltage phases. These components play a vital role in power electronics by enabling precise phase control in applications ranging from industrial automation to renewable energy systems. The market comprises two primary product types: Step-down Transducers and Boost Transducers , each serving distinct voltage regulation needs.

The market growth is driven by increasing demand for energy-efficient power management solutions and expanding industrial automation. While the U.S. currently dominates with 35% market share, China is emerging as the fastest-growing region due to rapid industrialization. The Step-down Transducers segment, currently holding 62% market share, continues to lead due to widespread application in voltage reduction scenarios. Key players like Ohio Semitronics and Weschler Instruments are investing in smart transducer technologies to capitalize on Industry 4.0 adoption.

List of Prominent AC Phase Angle Transducer Manufacturers

- Ohio Semitronics (U.S.)

- Eltime Controls (U.K.)

- Weschler Instruments (U.S.)

- Ziegler (Germany)

- Moore Industries-International, Inc. (U.S.)

- Rawet s.r.o. (Czech Republic)

- ADTEK Electronics (Taiwan)

- Crompton Instruments (U.K.)

While the market remains competitive, differentiation through application-specific designs and enhanced measurement accuracy has become crucial. Larger corporations are investing heavily in R&D to develop transducers compatible with IoT-enabled systems, whereas mid-sized players focus on cost-optimized solutions for emerging markets.

Segment Analysis:

By Type

Step-down Transducers Dominate Due to Widespread Use in Power Regulation Applications

The market is segmented based on type into:

- Step-down Transducers

- Boost Transducers

- Linear Transducers

- Non-linear Transducers

- Others

By Application

Industrial Automation Segment Leads Owing to Increasing Adoption in Process Control Systems

The market is segmented based on application into:

- Industrial Automation

- Power Generation & Distribution

- Renewable Energy Systems

- Test & Measurement Equipment

- Others

By End User

Manufacturing Sector Accounts for Significant Share Due to High Equipment Integration

The market is segmented based on end user into:

- Manufacturing Industries

- Energy & Utilities

- Telecommunications

- Research Institutions

- Others

By Technology

Digital Transducers Gain Traction for Enhanced Accuracy and Communication Capabilities

The market is segmented based on technology into:

- Analog Transducers

- Digital Transducers

- Hybrid Transducers

- Smart Transducers

- Others

Regional Analysis: AC Phase Angle Transducers Market

North America

The North American AC Phase Angle Transducers market is characterized by strong demand from industrial automation, energy-efficient power systems, and smart grid modernization initiatives. The U.S. leads due to widespread adoption in manufacturing, renewable energy sectors, and advancements in smart infrastructure projects. Key applications include voltage regulation in data centers and power distribution networks. Major suppliers like Ohio Semitronics and Eltime Controls dominate the region with technologically advanced solutions. Regulatory compliance (e.g., IEEE standards) and the push for energy efficiency are fundamental drivers, though high production costs could limit smaller enterprises. The U.S. is projected to maintain its market leadership, supported by steady investments in power infrastructure and automation.

Europe

Europe’s market is shaped by strict energy efficiency directives and the transition toward sustainable power solutions. Germany and France are key contributors, with demand stemming from industrial automation, automotive manufacturing, and renewable energy applications. The EU’s focus on minimizing energy wastage in power conversion processes has increased reliance on precision phase angle transducers. Local manufacturers, including Ziegler and Moore Industries-International, Inc. , emphasize innovation to meet evolving industry needs. While demand remains robust, competition from Asian manufacturers offering cost-effective alternatives presents a challenge. Europe’s shift toward green energy and Industry 4.0 will continue to propel market expansion.

Asia-Pacific

As the fastest-growing region, Asia-Pacific is driven by industrial expansion, urbanization, and rapid electrification. China leads with its vast manufacturing base and infrastructure development, followed by India and Japan. The proliferation of consumer electronics, automotive electrification, and telecom infrastructure fuels demand for AC phase angle transducers. While local manufacturers leverage cost advantages, quality inconsistencies and intellectual property concerns persist. Companies like ADTEK Electronics and Crompton Instruments are expanding their footprint through strategic partnerships. With rising investments in smart grids and renewable energy, the region is expected to dominate volume growth, albeit with price-sensitive dynamics.

South America

South America’s market is emerging, with Brazil and Argentina spearheading demand due to industrialization and gradual grid modernization. The automotive sector, particularly electric vehicle production, and growing telecom infrastructure are key application areas. However, economic instability and inadequate infrastructure stifle large-scale adoption. Local manufacturers struggle with import dependencies for advanced components, limiting production scalability. Despite these challenges, government initiatives to improve power distribution efficiency create long-term opportunities, though growth will remain moderate compared to other regions.

Middle East & Africa

The Middle East and Africa exhibit niche demand, primarily driven by energy projects, oil & gas operations, and urban electrification in GCC countries. South Africa and Saudi Arabia are the primary markets, with investments in power infrastructure boosting transducer applications. However, budget constraints and reliance on imports hinder rapid market penetration. Local manufacturing capabilities are underdeveloped, creating opportunities for international suppliers. As renewable energy projects gain traction, the demand for efficient power control solutions is expected to rise steadily, albeit from a smaller base.

Report Scope

MARKET DYNAMICS

The lack of global standardization for power measurement protocols creates substantial challenges for AC phase angle transducer manufacturers and users alike. Different regions and industries employ varying voltage levels, frequency ranges, and communication protocols, requiring customized transducer configurations. This variability increases development costs and inventory complexity for manufacturers while creating integration challenges for end-users upgrading or expanding their systems.

Moreover, the rapid evolution of industrial communication standards frequently renders existing transducers obsolete. Many facilities face the dilemma of either replacing perfectly functional transducers to maintain compatibility with new monitoring systems or maintaining outdated communications infrastructure. This dynamic creates uncertainty in purchasing decisions and can delay modernization projects that would otherwise drive market growth.

The proliferation of Industrial Internet of Things (IIoT) solutions presents significant growth opportunities for AC phase angle transducer manufacturers. Modern transducers with built-in digital communication capabilities can seamlessly integrate with predictive maintenance systems and energy management platforms. This integration enables real-time monitoring and analytics, allowing facilities to optimize energy usage and prevent equipment failures.