Category: Metallic Materials

Sequential Linker Market: Economic Impact and Global Forecast 2025–2032

By SemiconductorinsightPrerana, 2025-07-14

Sequential Linker Market , Trends, Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=103473

MARKET INSIGHTS

The global Sequential Linker Market size was valued at US$ 67.8 million in 2024 and is projected to reach US$ 96.4 million by 2032, at a CAGR of 4.5% during the forecast period 2025-2032.

A sequential linker is an industrial component that ensures step-by-step execution of manufacturing processes without conditional requirements. These linkers automatically trigger subsequent operations immediately upon completion of prerequisite steps, providing reliable workflow automation in production environments. Unlike conditional connectors, sequential linkers operate independently of process outcomes, making them essential for deterministic manufacturing systems.

The market growth is primarily driven by increasing automation across industries such as automotive (accounting for XX% market share), aerospace, and medical technology. While standard sequential linkers dominate with XX% market share, demand for bespoke solutions is growing at XX% CAGR due to specialized industrial requirements. Key players including WESOBA Werkzeug- und Sondermaschinenbau GmbH and Lochanstalt Aherhammer collectively held approximately XX% market share in 2024, with recent expansions in Asia-Pacific regions contributing to market expansion.

List of Key Sequential Linker Manufacturers

- WESOBA Werkzeug- und Sondermaschinenbau GmbH (Germany)

- Lochanstalt Aherhammer Stahlschmidt & Flender GmbH (Austria)

- EasyMold Software & Training GmbH (Germany)

- Ammer, Quick & Partner GmbH (Germany)

- Buschhoff Stanztechnik GmbH & Co KG (Germany)

- Paul Beier GmbH (Germany)

- Wanzke AG (Switzerland)

- A+N/POTT GmbH (Germany)

- Ahlberg Metalltechnik GmbH (Germany)

- Albert Hillringhaus Werkzeugbau KG (Germany)

- Primaform AG (Japan)

- technical works (Italy)

- Veith AG (Germany)

Sequential Linker Market: Segment Analysis

By Type

Regular Segment Holds Major Share Due to Standardization in Industrial Applications

The Sequential Linker market is segmented by type into:

- Regular

- Subtypes: Standardized connectors for mass production

- Bespoke

- Subtypes: Custom-designed connectors for specialized applications

By Application

Automotive Industry Leads Demand Owing to Increased Automation in Manufacturing

The market segmentation by application includes:

- Mechanical Engineering

- Automotive Industry

- Aerospace

- Oil and Gas

- Chemical Industry

- Medical Technology

- Electrical Industry

By Technology

Electro-Mechanical Systems Dominate Due to Reliability in Sequential Operations

- Electro-Mechanical Systems

- Pneumatic Systems

- Hydraulic Systems

By Operation

Fully Automated Systems Gain Traction in High-Volume Manufacturing

- Manual Linkers

- Semi-Automated Linkers

- Fully Automated Linkers

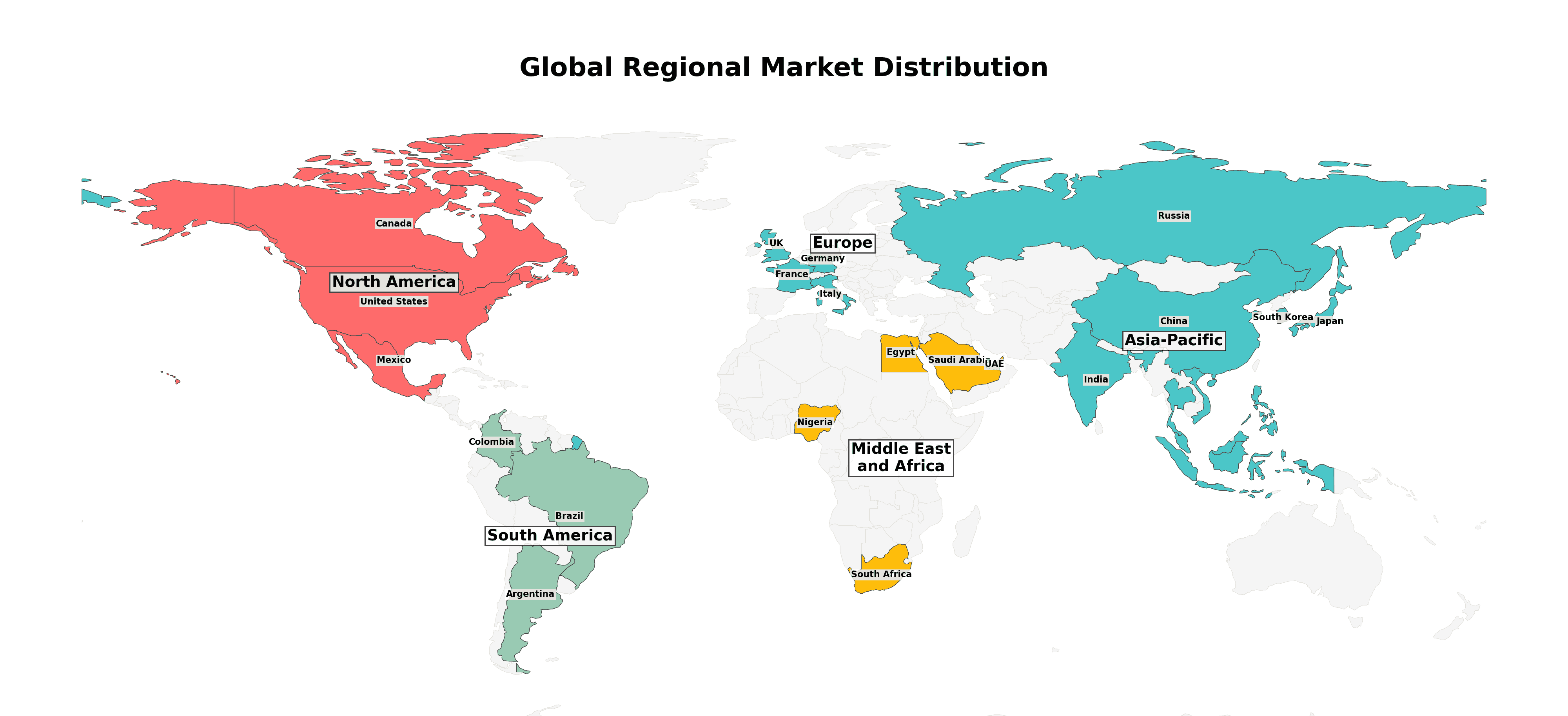

Regional Analysis: Sequential Linker Market

North America

The North American market for sequential linkers is characterized by strong demand from advanced manufacturing sectors, particularly automotive, aerospace, and medical technology industries. The U.S. accounts for approximately 65% of the regional market share, driven by its well-established industrial base and adoption of automation technologies. Regulatory standards for process control and manufacturing consistency further support the need for precision linking solutions. While the regular segment dominates due to standardization benefits, bespoke sequential linkers are gaining traction in specialized applications such as semiconductor manufacturing and precision medical device assembly. Key players like Ammer, Quick & Partner GmbH have expanded their North American operations to better serve this high-value market.

Europe

Europe maintains a robust sequential linker market, particularly in Germany and Italy where industrial automation penetration exceeds 70% in key manufacturing sectors. The region’s strong emphasis on Industry 4.0 initiatives and lean manufacturing practices has accelerated demand for reliable process linking solutions. EU manufacturing directives that emphasize production traceability and quality control have made sequential linkers integral to compliance strategies. While price sensitivity exists among medium-sized enterprises, premium German engineering continues to command market leadership through companies like WESOBA Werkzeug- und Sondermaschinenbau GmbH. Recent supply chain realignments post-pandemic have also driven increased investment in domestic linking solutions.

Asia-Pacific

As the fastest-growing regional market, Asia-Pacific demonstrates diverse adoption patterns for sequential linkers. China accounts for over 50% of regional demand, propelled by massive investments in automotive and electronics manufacturing infrastructure. India shows accelerating growth as its Make in India initiative boosts domestic production capabilities. While cost-conscious manufacturers initially favored basic linking solutions, rising labor costs and quality expectations are driving uptake of more sophisticated systems. Japanese and South Korean manufacturers lead in adopting high-precision linkers for robotics and semiconductor applications. The sheer scale of manufacturing activity across the region ensures Asia-Pacific will remain the volume leader, though the proliferation of local suppliers creates pricing pressures for international brands.

South America

The South American market for sequential linkers remains constrained by economic volatility but shows pockets of opportunity in Brazil’s automotive sector and Argentina’s agricultural equipment manufacturing. Infrastructure limitations and import dependencies create challenges for sophisticated linking solutions, leading many manufacturers to rely on basic mechanical linking methods. However, growing foreign direct investment in Mexico’s manufacturing sector presents a bright spot, with sequential linker adoption increasing in automotive tier suppliers serving North American OEMs. The market favors cost-effective regular linkers over bespoke solutions, though established industrial clusters around São Paulo show willingness to invest in advanced linking technologies for export-oriented production.

Middle East & Africa

This emerging market demonstrates selective demand concentrated in oil & gas and construction equipment manufacturing. While overall penetration remains low compared to other regions, strategic investments in industrial diversification (particularly in UAE and Saudi Arabia) are creating new opportunities. Turkey represents the most developed market in the region, with a growing base of automotive and appliance manufacturers adopting sequential linking solutions. Infrastructure development across Africa creates potential for future growth in construction machinery manufacturing, though the current market remains constrained by limited industrialization. Regional players are gradually recognizing how sequential linkers can improve process reliability in harsh operating environments common in Middle Eastern industries.

MARKET DYNAMICS

Manufacturers operating aging production equipment face substantial difficulties when attempting to incorporate sequential linking technology. Many legacy machines lack the digital interfaces required for seamless sequential control integration, necessitating costly retrofits or complete replacements. Industry analyses suggest that over 60% of industrial equipment currently in use was manufactured before modern sequential control standards were established, creating a significant installed base challenge.

Additionally, the scarcity of engineers skilled in both traditional manufacturing systems and modern sequential control technology complicates upgrade projects. Workforce surveys reveal that nearly three-quarters of industrial firms report difficulty finding personnel with the interdisciplinary expertise needed to successfully implement these solutions, leading to extended project timelines and implementation risks.

The expanding medical technology sector presents compelling opportunities for sequential linker adoption as device manufacturers seek to enhance production precision. Regulatory requirements for medical devices mandate strict process controls and documentation – an area where sequential linking technology provides distinct advantages. The global medical device market, projected to exceed $600 billion by 2028, is driving increased investment in manufacturing systems capable of executing error-proof production sequences.

Recent technological advances are also creating opportunities in micro-manufacturing applications. The development of compact sequential linkers with sub-millisecond timing resolution enables their use in delicate assembly processes for electronics and micro-mechanical components. Industry leaders are actively developing specialized sequential control solutions tailored to these high-precision applications, with several major product launches anticipated in the coming year.

Furthermore, the growing emphasis on sustainable manufacturing is prompting development of energy-efficient sequential linking systems that minimize power consumption during production cycles. Environmental regulations and corporate sustainability initiatives are expected to accelerate adoption of these next-generation solutions across multiple industries.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=103473

FREQUENTLY ASKED QUESTIONS:

- What is the current market size of Global Sequential Linker Market?

- Which key companies operate in Global Sequential Linker Market?

- What are the key growth drivers?

- Which region dominates the market?

- What are the emerging trends?

Related Reports:

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Lever Actuator Market: SWOT Analysis and Strategic Forecast 2025–2032

By SemiconductorinsightPrerana, 2025-07-14

Lever Actuator Market , Trends, Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=103443

MARKET INSIGHTS

The global Lever Actuator Market was valued at 613 million in 2024 and is projected to reach US$ 892 million by 2032, at a CAGR of 5.6% during the forecast period.

Lever actuators are mechanical devices designed to convert rotary motion into linear displacement through a pivoting lever mechanism. These components feature compact designs with strokes typically limited to 1mm, optimized for precise control in space-constrained applications. The actuator types include manual, automatic, and semi-automatic variants, serving diverse industrial requirements.

The market growth stems from increasing automation across manufacturing sectors and demand for precision motion control solutions. Key applications span mechanical engineering (32% market share), automotive systems (21%), and aerospace (18%) as per 2024 data. Recent material innovations have enhanced durability, with manufacturers like SMC Corporation and Parker Hannifin introducing corrosion-resistant aluminum alloys for harsh environments. The Asia-Pacific region dominates demand (42% market share), driven by China’s expanding industrial automation sector which grew 8.3% year-over-year in Q1 2024.

List of Key Lever Actuator Companies Profiled

- SMC Corporation (Japan)

- Parker Hannifin (U.S.)

- Festo (Germany)

- Rotork (U.K.)

- Johnson Electric (Hong Kong)

- Thomson Industries (U.S.)

- SCHUNK (Germany)

- Linak (Denmark)

- Tolomatic (U.S.)

- General Electric Company (U.S.)

- DEZURIK (U.S.)

- Assured Automation (U.S.)

Segment Analysis:

By Type

Automatic Lever Actuators Drive Market Growth Due to High Efficiency and Precision Control

The market is segmented based on type into:

- Manual

- Automatic

- Semi-Automatic

By Application

Mechanical Engineering Leads Due to Widespread Use in Industrial Automation

The market is segmented based on application into:

- Mechanical Engineering

- Automotive Industry

- Aerospace

- Oil and Gas

- Medical Technology

By End User

Manufacturing Sector Dominates Due to High Demand in Production Lines

The market is segmented based on end user into:

- Manufacturing

- Construction

- Healthcare

- Energy

Regional Analysis: Lever Actuator Market

North America

The lever actuator market in North America is characterized by high adoption rates in advanced manufacturing, automotive, and aerospace sectors. The U.S. remains the dominant player, contributing over 65% of the regional market share, driven by strong industrial automation trends and R&D investments. Stringent efficiency and safety standards push manufacturers toward precision-engineered lever actuators, notably in robotics and medical device applications. However, supply chain disruptions and fluctuating raw material costs pose challenges. Key companies like Parker Hannifin and Thomson Industries are driving innovations in compact, high-torque lever actuators tailored for specialized applications.

Europe

Europe’s lever actuator market thrives on technological advancements and regulatory compliance, particularly in Germany and France. The region holds approximately 25% of the global market, with growing demand from renewable energy and smart manufacturing sectors. EU machinery directives mandate enhanced actuator precision, fostering adoption of automated and semi-automatic lever actuators. Local players like Festo and SCHUNK lead in energy-efficient designs. While labor costs and economic uncertainties in Southern Europe slightly hinder growth, Northern Europe’s strong R&D ecosystem ensures sustained innovation in smart actuator solutions.

Asia-Pacific

Asia-Pacific dominates the global lever actuator market, accounting for nearly 40% of worldwide demand. China’s manufacturing expansion and India’s “Make in India” initiative fuel growth, particularly in automotive and construction applications. Japan and South Korea remain innovation hubs for compact actuator designs. Though price sensitivity favors manual lever actuators in developing nations, rising labor costs are accelerating automation adoption. Supply chain localization by global players like SMC Corporation and increasing OEM partnerships signal strong future growth potential across the region.

South America

The South American lever actuator market shows moderate growth, primarily led by Brazil’s agricultural machinery and oil & gas sectors. Infrastructure constraints and economic instability have slowed adoption compared to other regions. Most demand comes from replacement rather than new installations. However, mining sector modernizations in Chile and Peru present emerging opportunities. Local manufacturers focus on cost-effective manual actuators, while imported automated solutions gain traction in multinational industrial facilities. The market remains price-driven with limited technological penetration beyond urban industrial centers.

Middle East & Africa

This region represents the smallest but fastest-growing lever actuator market (<5% global share). Oil & gas applications in GCC countries drive demand for rugged actuators, while infrastructure projects in Turkey and South Africa boost construction-related usage. The lack of local manufacturing makes the market import-dependent. Though adoption lags behind global averages, increasing industrial automation and smart city initiatives in the UAE and Saudi Arabia signal future potential. Market education about actuator benefits remains crucial to overcoming traditional mechanical system preferences.

MARKET DYNAMICS

Device manufacturers across industries continue demanding smaller form factors without sacrificing performance. This creates engineering challenges as actuator designers balance shrinking footprints against force output and cycle life requirements. The medical technology sector exemplifies this trend, where new surgical tools require sub-10mm actuators capable of sustaining 50,000+ operational cycles. Meeting these specifications while maintaining cost competitiveness has forced manufacturers to invest heavily in advanced materials and precision manufacturing techniques, with R&D budgets increasing an average of 22% annually across leading firms.

As demand grows, the industry faces a shortage of qualified personnel across engineering and production roles. Specialized positions in precision mechatronics and motion control design remain particularly difficult to fill, with over 35% of manufacturers reporting extended vacancies for these critical roles. This skills shortage comes at a crucial time, as companies attempt to scale production to meet booming demand from automation projects. Many firms are now partnering with technical schools to develop specialized training programs, but these initiatives typically require 2-3 years before yielding results.

The integration of IoT capabilities presents a significant growth avenue for lever actuator manufacturers. Smart actuators incorporating sensors and connectivity allow predictive maintenance and real-time performance monitoring, reducing downtime in industrial applications. A recent survey of manufacturing plants showed facilities using smart actuators achieved 30% fewer unplanned maintenance events compared to conventional models. As Industry 4.0 adoption accelerates, the premium pricing potential of these intelligent systems – typically 25-40% above standard models – creates attractive margin opportunities for forward-thinking manufacturers.

With millions of lever actuators installed across industries, manufacturers are developing lucrative service offerings. Preventive maintenance programs, repair services, and retrofit kits for legacy systems now contribute over 15% of revenue for some leading suppliers. The automotive sector particularly demonstrates this potential, where actuator replacement cycles typically occur every 5-7 years in heavy-use applications. One European manufacturer recently grew its aftermarket business by 40% by offering customized service plans aligned with customer maintenance schedules, demonstrating the untapped potential in this segment.

Advances in composite materials and surface treatments are expanding performance boundaries for lever actuators. New ceramic-coated bearings and graphene-enhanced components now allow operation in extreme environments previously inaccessible to conventional designs. The aerospace sector has been an early adopter, with next-generation actuator designs achieving weight reductions of 30% while maintaining strength characteristics. These material innovations also benefit renewable energy applications, where corrosion-resistant variants now withstand coastal environments that previously limited offshore wind turbine deployments.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=103443

- What is the current market size of Global Lever Actuator Market?

- Which key companies operate in Global Lever Actuator Market?

- What are the key growth drivers?

- Which region dominates the market?

- What are the emerging trends?

Related Reports:

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Probe Station Micropositioners Market: Growth Projections and Industry Overview 2025–2032

By SemiconductorinsightPrerana, 2025-07-14

Probe Station Micropositioners Market , Trends, Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=103503

MARKET INSIGHTS

The global Probe Station Micropositioners Market size was valued at US$ 187.3 million in 2024 and is projected to reach US$ 276.4 million by 2032, at a CAGR of 5.1% during the forecast period 2025-2032

Probe station micropositioners, also known as micromanipulators or probe heads, are precision instruments that position probe arms and tips for semiconductor device testing. These critical components enable nanoscale positioning in three dimensions (X, Y, and Z axes), with some advanced models offering roll adjustment for specialized radio frequency (RF) or optical measurements. Mounting options include magnetic, vacuum, or mechanical fixation depending on application requirements.

The market growth is primarily driven by semiconductor industry expansion , which increased 8.4% year-over-year in 2023 according to industry reports. Key applications include integrated circuit validation, wafer-level testing, and failure analysis – particularly for advanced packaging solutions like 3D ICs and fan-out wafer-level packaging (FOWLP). Recent technological advancements in micro-electromechanical systems (MEMS) and the proliferation of 5G/IoT devices are creating new demand vectors. Leading manufacturers are responding with innovative solutions, such as FormFactor’s 2023 launch of temperature-controlled micropositioners for extreme environment testing.

List of Key Probe Station Micropositioner Companies

- MPI Corporation (Taiwan)

- FormFactor Inc. (U.S.)

- Signatone (U.S.)

- Wentworth Laboratories (U.K.)

- ESDEMC Technology (U.S.)

- SemiProbe (U.S.)

- Micromanipulator (U.S.)

- MicroXact (Italy)

- Ecopia (South Korea)

- Everbeing Int’l (Taiwan)

- KeyFactor Systems (Germany)

- KeithLink Technology (Taiwan)

- Semishare (China)

- Shenzhen Cindbest Technology (China)

Segment Analysis:

By Type

Electric Micropositioners Dominate Market Share Due to Precision and Automation Advantages

The market is segmented based on type into:

- Manual Micropositioners

- Subtypes: Standard Manual, High-Precision Manual

- Electric Micropositioners

- Subtypes: Stepper Motor, Piezoelectric, Servo Motor

By Application

Semiconductor Testing Leads Market Share for Quality Control in IC Manufacturing

The market is segmented based on application into:

- Semiconductor Testing

- MEMS/NEMS Device Testing

- Photonics Testing

- Academic Research

- Failure Analysis

By End User

Semiconductor Foundries Lead Demand for Wafer-Level Testing Applications

The market is segmented based on end user into:

- Semiconductor Foundries

- IDMs (Integrated Device Manufacturers)

- Research Laboratories

- Testing Service Providers

By Movement Range

Standard Range Solutions Dominate Mainstream Testing Requirements

The market is segmented based on movement range into:

- Standard Range

- High Precision (<1μm)

- Ultra-High Precision (Nanoscale)

Regional Analysis: Probe Station Micropositioners Market

North America

North America remains a critical hub for probe station micropositioner adoption due to its robust semiconductor manufacturing and R&D ecosystem. The U.S. accounts for over 35% of global demand , driven by major semiconductor firms and nanotechnology research institutions. Strict quality standards in industries like automotive electronics and 5G infrastructure necessitate high-precision testing equipment, creating steady demand. However, supply chain disruptions and export restrictions on advanced semiconductor technologies pose challenges to market expansion. Key players like FormFactor and MPI dominate the region, offering automated micropositioners for wafer-level testing to meet the needs of fabless chip designers and foundries.

Europe

Europe’s market thrives on specialized applications in MEMS, photonics, and automotive semiconductor testing. Germany and France lead in high-end electric micropositioner adoption , particularly for industrial and academic research. The EU’s €43 billion Chips Act aims to bolster semiconductor sovereignty, indirectly benefiting equipment suppliers. Nevertheless, slower growth in consumer electronics manufacturing compared to Asia limits volume demand. Local suppliers like Micromanipulator focus on customized solutions for niche applications, while compliance with ISO 9001 and IEC standards remains a key purchasing criterion for buyers.

Asia-Pacific

As the largest and fastest-growing regional market , Asia-Pacific captures over 50% of global sales , with China, Japan, and South Korea as primary contributors. The region’s semiconductor foundries and OSAT providers drive bulk purchases of manual and semi-automated micropositioners for cost-sensitive high-volume testing. While TSMC and Samsung’s advanced packaging initiatives create demand for precision models, price competition among local manufacturers like Shenzhen Cindbest Technology pressures profit margins. India’s emerging semiconductor policy could unlock new growth avenues, though infrastructural gaps currently limit adoption rates outside major tech hubs.

South America

The market here remains nascent, with Brazil and Argentina showing pockets of demand in university research labs and niche electronics manufacturing. Economic instability and limited local semiconductor production constrain large-scale adoption, though imports of basic manual micropositioners continue for repair/maintenance applications. Some growth potential exists in mining equipment electronics testing , but the lack of regional distributors forces buyers to rely on international suppliers with extended lead times.

Middle East & Africa

This emerging region presents a long-term opportunity tied to technology transfer initiatives in Israel, Saudi Arabia, and the UAE. Israel’s mature semiconductor design ecosystem supports demand for advanced probe systems, while GCC nations are investing in local electronics manufacturing capabilities. However, low local expertise in precision measurement technologies and dependence on imported equipment slow market development. Partnerships between global players like Wentworth Laboratories and regional universities aim to build testing infrastructure for future growth.

MARKET DYNAMICS

The semiconductor industry’s cyclical nature makes capital expenditures for testing equipment highly sensitive to market conditions. A complete probe station with micropositioners represents a significant investment, with prices ranging from $50,000 to over $500,000 depending on specifications. During market downturns, testing capacity expansions often get deferred, directly impacting micropositioner sales. Additionally, the long service life of these systems (typically 7-10 years) extends replacement cycles, creating periods of reduced demand between upgrade cycles.

The cost factor becomes especially restrictive in emerging semiconductor markets where budget constraints limit access to advanced probing solutions. Without more affordable options, these regions may continue relying on older testing methods, potentially slowing their adoption of cutting-edge semiconductor technologies.

The semiconductor industry currently faces a shortage of skilled technicians capable of operating and maintaining advanced probe stations, with estimates suggesting a 30% gap between demand and available talent. Micropositioners require specialized knowledge for proper calibration and troubleshooting, with improper handling potentially reducing measurement accuracy by up to 40%. This skills gap becomes more pronounced with each technological advancement, as newer systems incorporate increasingly sophisticated features like automated multi-probe alignment and AI-assisted positioning.

Educational institutions struggle to keep pace with the rapid evolution of semiconductor testing technologies, leaving many new technicians unprepared for the complexities of modern probe station operations. Without significant investment in workforce development, this constraint may continue limiting market growth in the medium term.

The rapid development of compound semiconductors (GaN, SiC) for power electronics and 5G applications creates substantial opportunities for probe station micropositioner manufacturers. These materials require different probing approaches than traditional silicon, with testing parameters that often demand specialized positioning solutions. The compound semiconductor market expects to grow at over 12% CAGR through 2030, requiring corresponding investment in testing infrastructure. Micropositioner providers that can offer solutions optimized for these materials stand to capture significant market share in this high-growth segment.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=103503

FREQUENTLY ASKED QUESTIONS:

- What is the current market size of Global Probe Station Micropositioners Market?

- Which key companies operate in Global Probe Station Micropositioners Market?

- What are the key growth drivers?

- Which region dominates the market?

- What are the emerging trends?

Related Reports:

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Gesture Recognition Sensors Market: Innovation Trends and Application Outlook 2025–2032

By SemiconductorinsightPrerana, 2025-07-14

Gesture Recognition Sensors Market , Trends, Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=103504

MARKET INSIGHTS

The global Gesture Recognition Sensors Market size was valued at US$ 892.4 million in 2024 and is projected to reach US$ 1.78 billion by 2032, at a CAGR of 9.0% during the forecast period 2025-2032.

Gesture recognition sensors are advanced input devices that detect and interpret human gestures as commands through technologies like infrared (IR), time-of-flight (TOF), and computer vision. These sensors enable touchless interaction across applications including automotive infotainment systems, medical equipment control, and smart home automation.

The market growth is driven by rising demand for hygienic touchless interfaces post-pandemic and increased adoption in consumer electronics. While North America currently holds the largest market share (38.2% in 2024), Asia-Pacific is emerging as the fastest-growing region due to expanding automotive and electronics manufacturing. Key technological segments include TOF-based sensors (holding 47% market share) and IR-based sensors (31% share), with the automotive sector accounting for 34% of total applications. Major players like STMicroelectronics and Infineon Technologies are investing heavily in AI-enhanced gesture recognition, with STMicroelectronics launching new FlightSense TOF sensors in Q1 2024 for improved accuracy in low-light conditions.

List of Key Gesture Recognition Sensor Companies Profiled

- STMicroelectronics (Switzerland)

- Infineon Technologies (Germany)

- Microchip Technology (U.S.)

- ams-OSRAM (Austria)

- Bosch Sensortec (Germany)

- Vishay Intertechnology (U.S.)

- Texas Instruments (U.S.)

- Sharp Corporation (Japan)

- PixArt Imaging (Taiwan)

- Broadcom (U.S.)

- KODENSHI (Japan)

- Analog Devices (U.S.)

The market remains dynamic as these companies compete through product innovation, strategic partnerships, and geographic expansion. Recent developments suggest an increasing focus on developing solutions that combine gesture recognition with other sensing modalities, creating more versatile human-machine interfaces. Smaller players are finding niche opportunities in specialized applications like medical device controls and industrial automation, where precision requirements create differentiation opportunities.

Segment Analysis:

By Type

TOF-Based Gesture Sensor Segment Leads Due to High Precision in 3D Motion Tracking

The market is segmented based on type into:

- TOF-Based Gesture Sensor

- IR-Based Gesture Sensor

- Others

- Subtypes: Capacitive proximity sensors, Ultrasonic sensors, and others

By Application

Automotive Segment Dominates with Rising Demand for Touchless Controls

The market is segmented based on application into:

- Automotive

- Medical

- Home Automation

- Others

- Subtypes: Gaming consoles, Industrial automation, Retail kiosks

By Technology

2D Gesture Recognition Holds Major Share Due to Cost-Effectiveness

The market is segmented based on technology into:

- 2D Gesture Recognition

- 3D Gesture Recognition

By End-User Industry

Consumer Electronics Leads with Growing Adoption in Smart Devices

The market is segmented based on end-user industry into:

- Consumer Electronics

- Subtypes: Smartphones, Tablets, Wearables, Smart TVs

- Healthcare

- Automotive

- Industrial

Regional Analysis: Gesture Recognition Sensors Market

North America

North America represents one of the most advanced markets for gesture recognition sensors, primarily driven by technological innovation and high adoption rates in consumer electronics, automotive, and healthcare. The U.S., in particular, accounts for a significant share of the market due to the presence of leading tech companies and substantial investments in R&D. The region benefits from strong demand for touchless interfaces, especially in the post-pandemic era, where hygiene concerns have accelerated the deployment of gesture-controlled public kiosks and medical equipment. Additionally, the automotive sector continues to integrate gesture recognition in infotainment systems to enhance driver safety and convenience. However, high costs of implementation remain a challenge for broader market penetration.

Europe

The European gesture recognition sensors market is primarily propelled by stringent regulatory standards and the growing adoption of automation in industrial and healthcare sectors. Countries like Germany and the UK lead in automotive applications, leveraging gesture-based controls in premium vehicle models. The EU’s emphasis on accessibility and inclusivity has further fueled the use of gesture sensors for assistive technologies. Industrial automation also presents a key growth area, particularly in Germany and France, where manufacturers are increasingly adopting hands-free operating solutions for efficiency and workplace safety. Despite steady growth, the market faces constraints due to high development costs and competition from established user interfaces.

Asia-Pacific

The Asia-Pacific region is witnessing the fastest growth in gesture recognition adoption, driven by expanding consumer electronics markets in China, Japan, and South Korea. China, as the largest manufacturing hub, leads in the production and integration of infrared (IR) and time-of-flight (ToF) sensors in smartphones, gaming devices, and smart home appliances. India and Southeast Asian nations are also emerging as key markets, with increasing urbanization and digitalization efforts supporting demand for intuitive interfaces. Gaming and entertainment applications, particularly in Japan, are fostering innovation in immersive gesture-based controls. However, budget constraints in price-sensitive markets still slow the transition from traditional touch-based systems to gesture recognition technologies.

South America

The South American market is in the nascent stage , with growth primarily concentrated in Brazil and Argentina. Automotive and home automation sectors show promising adoption, supported by economic recovery and increasing tech awareness. However, infrastructure limitations and inconsistent regulatory frameworks hinder rapid deployment. Economic volatility and currency fluctuations further impact investment in advanced gesture technologies, resulting in slower adoption compared to other regions. Nonetheless, Brazil’s expanding middle class and demand for smart devices present long-term opportunities, particularly in infotainment and IoT applications.

Middle East & Africa

The MEA region demonstrates gradual uptake of gesture recognition sensors, largely in luxury automotive and smart building applications. Countries like the UAE and Saudi Arabia exhibit higher adoption driven by smart city initiatives and infrastructure modernization. Healthcare applications, particularly in surgical settings, are also gaining traction. However, market growth remains uneven due to limited technological infrastructure in certain areas and reliance on imports for sensor components. South Africa shows moderate potential with increasing local tech startups exploring gesture-based solutions for retail and public service applications, though low consumer awareness remains a challenge.

MARKET DYNAMICS

Operating rooms and medical facilities represent high-value opportunities for advanced gesture recognition systems. Surgeons navigating sterile fields can benefit enormously from touchless control of imaging systems, reducing contamination risks during procedures. Early implementations demonstrate 30-50% time savings in image manipulation compared to verbal commands or foot controls. Emerging applications extend to rehabilitation therapies, where motion tracking enables quantitative assessment of patient mobility and coordination. The healthcare vertical is particularly receptive to premium-precision solutions given the critical nature of medical applications, creating favorable conditions for sensor manufacturers to develop specialized medical-grade products.

Smart factories are adopting gesture recognition as part of Industry 4.0 initiatives to create more intuitive human-machine interfaces on factory floors. Workers operating in environments requiring protective equipment or handling materials benefit from hands-free control of dashboards and documentation systems. Combining gesture input with AR visualization enables technicians to access schematics and technical data while keeping tools in hand. The industrial sector’s emphasis on reliability and safety drives demand for ruggedized sensor solutions that withstand harsh conditions while maintaining millimeter-level precision. These applications command higher price points and longer product lifecycles than consumer markets.

Continuous gesture recognition remains impractical for many battery-powered devices due to the significant power draw of active sensing technologies. While time-of-flight sensors can consume as little as 10mW when optimized, this still impacts the operating life of compact wearable devices. Manufacturers must balance responsiveness with energy efficiency, often implementing wake-on-gesture architectures that delay initial detection. These compromises degrade the seamless experience expected from modern interfaces. Breakthroughs in event-based vision sensors and ultra-low-power radar technologies show promise for overcoming these limitations, but widespread implementation remains several development cycles away.

The absence of universal gesture vocabularies forces users to relearn interaction patterns across different devices and platforms. While some common gestures like swipe and pinch have achieved broad adoption, many proprietary implementations create unnecessary complexity. This fragmentation extends to development frameworks, requiring engineers to master multiple APIs and toolchains. Industry groups have attempted to address this through standards like the IEEE P2874 working group on gesture interfaces, but competing commercial interests have slowed convergence. The resulting inconsistency presents a significant barrier to creating truly intuitive cross-platform experiences expected by modern users.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=103504

FREQUENTLY ASKED QUESTIONS:

- What is the current market size of Global Gesture Recognition Sensors Market?

- Which key companies operate in Global Gesture Recognition Sensors Market?

- What are the key growth drivers?

- Which region dominates the market?

- What are the emerging trends?

Related Reports:

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Multi Channel Piezo Driver Market: Demand Analysis and Future Potential 2025–2032

By SemiconductorinsightPrerana, 2025-07-14

Multi Channel Piezo Driver Marke t, Trends, Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=103470

MARKET INSIGHTS

The global Multi Channel Piezo Driver Market size was valued at US$ 178.9 million in 2024 and is projected to reach US$ 267.4 million by 2032, at a CAGR of 5.2% during the forecast period 2025-2032. The U.S. market accounted for approximately 32% of global revenue in 2024, while China is expected to witness the fastest growth with an estimated 8.2% CAGR through 2032.

Multi Channel Piezo Drivers are precision electronic devices that control piezoelectric actuators in multiple axes simultaneously. These drivers provide low-noise, high-accuracy voltage outputs (typically -10V to +10V) for precise motion control in applications requiring nanometer-level positioning. The technology enables synchronized operation of multiple piezoelectric elements through analog control signals with gain values up to 25, making them essential for advanced motion systems.

The market growth is driven by increasing demand from semiconductor manufacturing equipment, where piezo drivers enable sub-micron precision in wafer inspection and lithography systems. Furthermore, the medical technology sector, particularly in surgical robotics and microscopy applications, is adopting multi-channel solutions for their compact form factor and precise motion control capabilities. Recent developments include PI’s launch of the E-517 multi-axis controller in 2023, featuring enhanced dynamic response for high-speed nanopositioning applications.

List of Key Multi Channel Piezo Driver Manufacturers

- PI (Physik Instrumente) (Germany)

- piezosystem jena GmbH (Germany)

- PiezoDrive (Australia)

- Piezo Direct (U.S.)

- DEWALT (U.S.)

- TEM Messtechnik GmbH (Germany)

- Analog Technologies, Inc (U.S.)

- CoreMorrow (China)

- Thorlabs, Inc. (U.S.)

- General Photonics Corporation (U.S.)

- Boréas Technologies (Canada)

- PIEZOTECHNICS GmbH (Germany)

- Omega Piezo Technologies (U.S.)

- ORLIN Technologies Ltd. (Israel)

- Texas Instrument (U.S.)

- Queensgate Instruments (UK)

- Newport Corporation (U.S.)

Segment Analysis:

By Type

Rigid Displacement Segment Leads the Market Due to High Precision in Static Applications

The market is segmented based on type into:

- Rigid Displacement

- Subtypes: High-voltage, Low-voltage, and others

- Resonant Displacement

- Subtypes: Single-channel, Dual-channel, and others

By Application

Medical Technology Segment Dominates Owing to Growing Demand in Ultrasound and Micropositioning Systems

The market is segmented based on application into:

- Mechanical Engineering

- Automotive Industry

- Aerospace

- Medical Technology

- Electrical Industry

By Voltage Range

0-100V Segment Holds Major Share for Low-power Piezo Actuator Applications

The market is segmented based on voltage range into:

- 0-100V

- 100-200V

- Above 200V

By Channel Configuration

Dual-channel Configuration Most Popular for Basic Positioning Systems

The market is segmented based on channel configuration into:

- Single-channel

- Dual-channel

- Multi-channel (3+)

Regional Analysis: Multi Channel Piezo Driver Market

North America

The North American market for Multi Channel Piezo Drivers is driven by strong demand from industries such as aerospace, medical technology, and automotive engineering . The region benefits from substantial R&D investments, particularly in the U.S., where companies like Thorlabs and Newport Corporation are leading innovation. The U.S. accounted for approximately 38% of the regional market share in 2024, supported by advancements in precision instrumentation and automation. Canada and Mexico are also witnessing steady growth, albeit at a slower pace due to smaller industrial bases. Regulatory standards for precision and safety in manufacturing further boost adoption in this region.

Europe

Europe remains a key market for Multi Channel Piezo Drivers, with Germany and France at the forefront due to their strong mechanical engineering and medical device sectors . The EU’s emphasis on high-precision manufacturing and energy efficiency aligns well with the capabilities of piezoelectric actuators, particularly in applications like industrial automation and optical systems. Companies such as PI (Physik Instrumente) and piezosystem jena GmbH dominate the competitive landscape. However, market growth faces challenges due to high production costs and stringent environmental regulations, which influence supply chain decisions.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market, led by China, Japan, and South Korea. China alone contributes over 45% of the regional demand , fueled by expanding electronics manufacturing and automation in sectors such as consumer robotics and semiconductor fabrication. Japan’s expertise in precision engineering reinforces its position as a key player, with companies like TEM Messtechnik GmbH driving innovation. Meanwhile, India and Southeast Asia are emerging markets, though adoption is constrained by limited awareness and access to high-end piezoelectric solutions compared to more established regions.

South America

South America’s market remains nascent but shows potential, particularly in Brazil and Argentina, where industries such as oil & gas and medical technology are slowly integrating piezo-driven automation. The lack of local manufacturing capabilities means most demand is met through imports, which raises costs and limits accessibility. Economic instability further complicates sustained investment, though partnerships with international suppliers are gradually improving technology transfer.

Middle East & Africa

The Middle East & Africa region is developing, with limited but growing applications in oilfield instrumentation and defense technology . The UAE and Saudi Arabia lead in adoption due to infrastructure modernization efforts, while Africa’s market remains constrained by underdeveloped industrial sectors. Despite challenges, increasing foreign investments in automation and smart manufacturing hint at future opportunities for Multi Channel Piezo Driver suppliers.

MARKET DYNAMICS

The sophisticated nature of multi-channel piezo systems presents significant implementation challenges across industries. Proper configuration requires deep expertise in both piezoelectric physics and control theory – a skillset combination that remains scarce in the industrial automation workforce. Many organizations report 6-12 month learning curves for engineering teams adopting these technologies, delaying ROI realization. The challenge is compounded by rapid technology evolution, as new driver architectures and control algorithms emerge faster than workforce training programs can adapt. This skills gap affects system performance optimization, with improperly tuned installations often operating at 60-70% of their theoretical capability.

Piezo drivers face growing competition from emerging motion technologies including voice coil actuators and magnetic levitation systems that offer comparable precision with potentially simpler integration. While piezoelectric solutions maintain advantages in stiffness and response speed, alternative technologies are closing the performance gap while offering lower voltage requirements and reduced system complexity. In medical device applications particularly, electromagnetic actuators have gained market share by eliminating high-voltage safety concerns. This competitive pressure is driving piezo system manufacturers to accelerate innovation cycles while simultaneously reducing solution footprints and power requirements.

The rapid evolution of photonic and quantum technologies is creating unprecedented demand for ultra-precision motion control solutions that multi-channel piezo drivers are uniquely positioned to address. In quantum computing applications, piezo-based positioning systems enable the sub-nanometer alignment required for superconducting qubit arrays and photonic interconnects. The global quantum technology market, projected to exceed $100 billion by 2030, represents a significant growth vector for specialized piezo solutions. Similarly, advancements in silicon photonics manufacturing demand precise wafer-level alignment capabilities that multi-axis piezo systems can provide with nanometer repeatability. Industry analysts estimate the photonics alignment sector alone could represent a $400-600 million addressable market for high-performance piezo drivers by 2027.

Leading manufacturers are increasingly collaborating with academic and government research institutions to develop next-generation piezo solutions, creating symbiotic relationships that accelerate technology transfer. These partnerships enable access to cutting-edge materials science research while providing researchers with industrial-grade test platforms for novel concepts. Recent initiatives have yielded breakthroughs in low-voltage piezo ceramics and adaptive control algorithms that promise to reduce system power consumption by 30-40% while maintaining performance. Such collaborations also serve as talent pipelines, helping address the industry’s critical skills shortage by providing practical training for engineering graduates in advanced motion control applications.

The development of modular, scalable piezo driver architectures is dramatically lowering adoption barriers for mid-tier manufacturers. New plug-and-play solutions reduce integration complexity by 50-70% compared to traditional systems while maintaining performance specifications suitable for most industrial applications. This architectural shift aligns with growing demand for flexible manufacturing systems that can be easily reconfigured for different production requirements. Market response has been positive, with early adopters reporting 30-45% reductions in total cost of ownership through decreased commissioning time and simplified maintenance requirements. As these modular platforms continue maturing, they are expected to capture significant market share in general industrial automation applications previously dominated by conventional motion technologies.

The global multi-channel piezo driver market is experiencing robust growth due to increasing demand for high-precision motion control in various industries. The ability of these drivers to achieve nanometer-level accuracy in positioning applications has made them indispensable in sectors such as semiconductor manufacturing, medical technology, and aerospace. Piezo drivers with multiple channels, typically ranging from 2 to 8 in commercial offerings, enable complex motion control for advanced piezo stages and actuators. Market data indicates that the rigid displacement segment currently dominates the landscape with over 60% market share, while resonant displacement applications are growing at a faster CAGR of approximately 8% annually.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=103470

FREQUENTLY ASKED QUESTIONS:

- What is the current market size of Global Multi Channel Piezo Driver Market?

- Which key companies operate in Global Multi Channel Piezo Driver Market?

- What are the key growth drivers?

- Which region dominates the market?

- What are the emerging trends?

Related Reports:

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Video Sync Separator Market: Market Segmentation and Regional Insights 2025–2032

By SemiconductorinsightPrerana, 2025-07-14

Video Sync Separator Market , Emerging Trends, Technological Advancements, and Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=97771

MARKET INSIGHTS

The global Video Sync Separator Market size was valued at US$ 234 million in 2024 and is projected to reach US$ 312 million by 2032, at a CAGR of 4.1% during the forecast period 2025-2032

Video sync separators are semiconductor devices designed to extract synchronization signals (horizontal and vertical timing information) from composite video inputs. These components are critical in processing video signals across multiple standards, including NTSC, PAL, SECAM, SDTV, and HDTV. By isolating sync pulses, they enable stable video display and synchronization in applications such as broadcasting, imaging, and consumer electronics.

The market is expanding due to rising demand for high-definition video processing, particularly in surveillance systems and digital displays. While the U.S. dominates with an estimated market size of USD 12.4 million in 2024, China is expected to witness accelerated growth, driven by increasing electronics manufacturing. Key players like Texas Instruments, Renesas, and ROHM collectively hold over 60% of the global market share, with innovations in low-power and multi-standard compatibility shaping competition.

List of Key Video Sync Separator Companies Profiled

- Renesas Electronics Corporation (Japan)

- Texas Instruments (U.S.)

- National Semiconductor Corporation (U.S.)

- NTE Electronics (U.S.)

- ROHM Semiconductor (Japan)

- Maxim Integrated (U.S.)

- GENNUM Corporation (Canada)

- Intersil Corporation (U.S.)

Segment Analysis:

By Type

Composite Segment Leads the Market Due to Widespread Use in Standard Video Processing

The market is segmented based on type into:

- Composite

- Subtypes: PAL, NTSC, SECAM

- Horizontal

- Vertical

- Others

By Application

Consumer Electronics Segment Dominates Due to High Demand from Display Manufacturers

The market is segmented based on application into:

- Imaging

- Consumer electronics

- Broadcast equipment

- Medical imaging devices

- Others

By Protocol

HDTV Segment Growing Rapidly Due to Shift Towards High Definition Content

The market is segmented based on protocol compatibility into:

- SDTV

- HDTV

- NTSC

- PAL

- SECAM

By End User

Original Equipment Manufacturers (OEMs) Hold Major Market Share

The market is segmented based on end users into:

- Original Equipment Manufacturers (OEMs)

- Consumer electronics repair services

- Broadcast equipment manufacturers

- Medical device manufacturers

- Others

Regional Analysis: Video Sync Separator Market

North America

The North American market remains a dominant player in the video sync separator industry, driven by strong demand from the consumer electronics and imaging sectors. The U.S. alone holds a significant market share, accounting for nearly 40% of global demand in 2024. This is largely due to the proliferation of high-definition broadcasting standards and investments in 4K and 8K display technologies. Major semiconductor manufacturers, including Texas Instruments and Maxim Integrated, are headquartered in the region, accelerating innovation in sync separator ICs. However, market maturity and saturation in core segments pose challenges for aggressive growth. Stringent FCC compliance standards continue to influence product development, pushing the adoption of advanced sync solutions.

Europe

Europe’s market benefits from robust demand in automotive infotainment and medical imaging, where precise video synchronization is critical. Germany and the U.K. are leading contributors, aided by a thriving industrial electronics ecosystem. The region is witnessing increased adoption of AI-powered video processing, which relies on high-performance sync separators for latency-sensitive applications. EU regulations on electromagnetic compatibility (EMC) indirectly shape product specifications, creating a preference for compliant chipsets from suppliers like Renesas and NXP. While the market exhibits steady growth, pricing pressures from Asian manufacturers and slow adoption of legacy analog systems restrain expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing market, spearheaded by China, Japan, and South Korea, where consumer electronics manufacturing dominates demand. China alone contributes over 30% of global shipments, with local players expanding their footprint in IC design. The rise of smart TVs, surveillance systems, and gaming consoles directly fuels demand for sync separators. Japan remains a hub for high-precision imaging equipment, while India’s burgeoning digital infrastructure projects offer untapped potential. However, intense competition from domestic suppliers and price volatility in the semiconductor supply chain create margin pressures for international players. The region’s shift toward IP-based video transmission could redefine long-term demand for traditional sync solutions.

South America

South America presents nascent opportunities, primarily in Brazil and Argentina, where broadcast infrastructure modernization is underway. Local production remains limited, forcing reliance on imports from North American and Asian suppliers. Economic instability and currency fluctuations deter large-scale investments, though niche applications in security systems and educational AV equipment sustain moderate demand. The absence of stringent technical standards results in a fragmented market where both high-end and low-cost solutions coexist. Potential growth hinges on increased digitization of media and telecommunications networks.

Middle East & Africa

This region shows gradual growth, led by the UAE and Saudi Arabia, where smart city initiatives and expanding broadcast networks drive procurement of video processing components. The market is highly import-dependent, with suppliers like ROHM and Intersil leveraging distribution partnerships to serve the region. Inconsistent regulatory frameworks and budgetary constraints delay the adoption of cutting-edge technologies, though demand for basic sync separators in surveillance and signage applications remains steady. Long-term prospects hinge on infrastructure development and increased localization of semiconductor assembly.

MARKET DYNAMICS

driven by the increasing adoption of advanced driver assistance systems (ADAS) and in-vehicle infotainment solutions. Modern vehicles incorporate multiple high-resolution displays for navigation, entertainment, and vehicle diagnostics, all requiring precise video synchronization. The automotive display market is projected to grow at nearly 8% annually through 2030, creating substantial demand for specialized video processing components.

Additionally, the development of augmented reality head-up displays (AR HUDs) in premium vehicles requires advanced synchronization capabilities to ensure seamless integration of digital information with the real-world view. This emerging technology segment is expected to drive innovation in video sync separator solutions.

MARKET CHALLENGES

Rapid Technological Evolution Requires Continuous R&D Investment

The video processing industry faces constant technological disruption, requiring manufacturers to maintain significant research and development expenditures. Developing solutions that support emerging video standards while maintaining backward compatibility with legacy systems presents both technical and financial challenges. Smaller players in particular may struggle to keep pace with the innovation required to remain competitive.

Other Challenges

Supply Chain Vulnerabilities

The global semiconductor shortage highlighted the fragility of electronics supply chains. Video sync separator manufacturers must navigate component availability issues and price fluctuations that can impact production schedules and profitability.

Standardization Gaps

The lack of unified standards for emerging video interfaces creates compatibility challenges. Developing solutions that work seamlessly across different manufacturers’ implementations requires extensive testing and adaptation efforts.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=97771

Frequently Asked Questions:

- What is the current market size of Global Video Sync Separator Market?

- Which key companies operate in Global Video Sync Separator Market?

- What are the key growth drivers?

- Which region dominates the market?

Related Reports:

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

TV Tuner IC Market: Investment Analysis and Strategic Outlook 2025–2032

By SemiconductorinsightPrerana, 2025-07-14

TV Tuner IC Market , Emerging Trends, Technological Advancements, and Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=97552

MARKET INSIGHTS

The global TV Tuner IC Market size was valued at US$ 3,780 million in 2024 and is projected to reach US$ 5,890 million by 2032, at a CAGR of 6.59% during the forecast period 2025-2032 .

TV Tuner ICs are semiconductor devices that convert radio frequency television signals into audio and video outputs for display. These integrated circuits form the core component of television receivers, supporting both analog (NTSC, PAL, SECAM) and digital (ATSC, DVB-T, ISDB-T) broadcasting standards. Key product categories include 5th Generation Silicon Tuner ICs, 6th Generation Silicon Tuner ICs, and hybrid solutions combining both technologies.

Market growth is driven by the ongoing transition to digital broadcasting worldwide, increasing demand for smart TVs, and the integration of tuner functionality in set-top boxes. However, the rising popularity of streaming services poses challenges to traditional broadcast tuner markets. Major players like Skyworks, STMicroelectronics, and NXP Semiconductors are innovating with low-power, multi-standard tuner ICs to address evolving consumer needs. For instance, in 2023, MaxLinear launched its newest silicon tuner supporting global digital TV standards while reducing power consumption by 30% compared to previous generations.

The convergence of broadcast and broadband delivery creates significant opportunities for innovative tuner IC designs. Hybrid receivers that combine terrestrial TV reception with IP connectivity enable seamless content blending, addressing evolving consumer preferences. Major manufacturers are investing in solutions that incorporate AI-based interference mitigation and adaptive signal processing to optimize performance across diverse reception conditions. These advanced capabilities command premium pricing and enhance product differentiation.

Developing regions offer substantial growth opportunities as digital transition initiatives gain momentum. Governments across Asia-Pacific, Africa, and Latin America are implementing policies to expand digital broadcasting infrastructure. These initiatives drive demand for cost-effective tuner solutions tailored to local market requirements. Furthermore, rising disposable incomes and expanding middle-class populations in these regions are accelerating TV ownership rates, creating favorable market conditions.

List of Key TV Tuner IC Manufacturers Profiled

- Skyworks Solutions, Inc. (U.S.)

- STMicroelectronics (Switzerland)

- MaxLinear, Inc. (U.S.)

- NXP Semiconductors (Netherlands)

- Infineon Technologies (Germany)

- Silicon Laboratories (U.S.)

- Analog Devices, Inc. (U.S.)

- AltoBeam (China)

Segment Analysis:

By Type

5th Generation Silicon Tuner ICs Segment Dominates Due to Superior Performance in High-Definition Broadcasting

The market is segmented based on type into:

- 5th Generation Silicon Tuner ICs

- Subtypes: Single-tuner, multi-tuner, and hybrid variants

- 6th Generation Silicon Tuner ICs

- Subtypes: Low-power, high-integration, and automotive-grade variants

- Other Advanced Tuner ICs

By Application

Digital Tuners Segment Leads Driven by Global Transition to Digital Television

The market is segmented based on application into:

- Analog Tuners

- Digital Tuners

- Subtypes: DVB-T, DVB-T2, DVB-S, ATSC, and ISDB variants

By End-User Industry

Consumer Electronics Remains Key Market Driver with Expanding Smart TV Adoption

The market is segmented based on end-user industry into:

- Consumer Electronics

- Subtypes: Smart TVs, set-top boxes, and media players

- Automotive

- Broadcasting Equipment

- Others

By Integration Level

Integrated Solutions Gaining Traction in Compact Device Designs

The market is segmented based on integration level into:

- Discrete Tuner ICs

- Integrated System-on-Chip (SoC) Solutions

Regional Analysis: TV Tuner IC Market

North America

The North American TV Tuner IC market is driven by high demand for advanced broadcasting technologies , particularly in the U.S., where content providers and consumers prioritize seamless digital signal reception. The region is witnessing a shift toward 6th Generation Silicon Tuner ICs due to their superior performance in handling 4K and 8K Ultra HD broadcasts. Major players like Skyworks and MaxLinear dominate the market, leveraging their expertise in semiconductor design. However, the gradual decline in cable TV subscriptions poses a challenge, with demand shifting toward internet-based streaming solutions. Despite this, the market remains robust due to innovations in ATSC 3.0-compatible tuner ICs and hybrid broadcast-broadband TV models.

Europe

Europe’s TV Tuner IC market benefits from standardized digital broadcasting regulations such as DVB-T2 and stringent energy efficiency requirements under EU directives. Countries like Germany and the U.K. lead in adoption, driven by the need for high-performance tuners in smart TVs and set-top boxes. Local manufacturers, including NXP and Infineon , maintain a strong foothold, though competition from Asian suppliers is intensifying. The region is also witnessing growing demand for automotive TV tuner ICs, as in-vehicle entertainment systems become more sophisticated. Despite economic fluctuations, Europe’s focus on digital infrastructure modernization ensures steady market growth.

Asia-Pacific

As the largest and fastest-growing market for TV Tuner ICs, the Asia-Pacific region is propelled by massive electronics manufacturing hubs in China, South Korea, and Japan . China alone accounts for a significant share of global production, with local players like AltoBeam gaining traction alongside multinational giants. The region’s cost-sensitive consumer base drives demand for mid-range 5th Generation Silicon Tuner ICs, though premium markets are gradually transitioning to 6th Generation solutions. Rapid urbanization, increasing disposable income, and government initiatives for digital terrestrial television (DTT) expansion further boost the market. Nevertheless, supply chain dependencies and trade tensions present potential risks.

South America

The South American market is characterized by moderate growth , with Brazil and Argentina being key contributors. Limited investment in broadcast infrastructure has slowed adoption of advanced TV tuner ICs, though digital TV migration projects in some countries offer growth opportunities. Local demand is primarily for analog and basic digital tuner ICs due to budget constraints, with price sensitivity outweighing performance considerations. The presence of global suppliers remains limited, and the market relies heavily on imports. However, gradual economic stabilization and rising middle-class populations could unlock long-term potential.

Middle East & Africa

This region presents a mixed landscape for TV Tuner IC adoption. While Gulf Cooperation Council (GCC) countries, particularly the UAE and Saudi Arabia, show strong demand for high-end tuner ICs in smart TVs and hospitality sectors, other areas struggle with low digital penetration. Infrastructure development is uneven, with urban centers driving most of the demand. The lack of local semiconductor manufacturing forces reliance on imports, often resulting in higher costs. Despite these challenges, the market holds promise as governments invest in digital broadcasting upgrades and satellite TV services gain traction in rural areas.

MARKET DYNAMICS

Developing cutting-edge TV tuner ICs has become increasingly challenging due to escalating performance requirements. Modern designs must support multiple frequency bands, advanced modulation schemes, and stringent EMI specifications while minimizing power consumption. These competing demands require substantial engineering expertise and extended development cycles. Industry benchmarks indicate that developing a new generation tuner IC now typically necessitates 18-24 months from concept to mass production.

The semiconductor industry continues facing supply chain volatility affecting tuner IC production. Critical components including specialized substrates and high-performance RF components frequently experience allocation challenges. These disruptions complicate production planning and may lead to extended lead times. Recent market analysis suggests that component shortages could potentially constrain industry growth by 10-15% annually until supply-demand equilibrium is restored.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=97552

FREQUENTLY ASKED QUESTIONS:

- What is the current market size of Global TV Tuner IC Market?

- Which key companies operate in Global TV Tuner IC Market?

- What are the key growth drivers?

- Which region dominates the market?

- What are the emerging trends?

Related Reports:

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Single Channel Video Encoder Market: Emerging Trends and Business Opportunities 2025–2032

By SemiconductorinsightPrerana, 2025-07-14

Single Channel Video Encoder Marke t, Emerging Trends, Technological Advancements, and Business Strategies 2025-2032

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=97601

MARKET INSIGHTS

The global Single Channel Video Encoder Market size was valued at US$ 289 million in 2024 and is projected to reach US$ 423 million by 2032, at a CAGR of 5.5% during the forecast period 2025-2032. While North America currently dominates with 35% market share, Asia-Pacific is expected to witness the fastest growth due to increasing digitization initiatives.

https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-300x200.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-1024x683.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-768x512.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-90x60.webp 90w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-135x90.webp 135w" alt="" width="1536" height="1024" data-lazyloaded="1" data-src="https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market.webp" data-warning="Missing alt text" data-srcset="https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market.webp 1536w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-300x200.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-1024x683.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-768x512.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-90x60.webp 90w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-135x90.webp 135w" data-sizes="(max-width: 1536px) 100vw, 1536px" data-ll-status="loaded">

https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-300x200.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-1024x683.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-768x512.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-90x60.webp 90w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-135x90.webp 135w" alt="" width="1536" height="1024" data-lazyloaded="1" data-src="https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market.webp" data-warning="Missing alt text" data-srcset="https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market.webp 1536w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-300x200.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-1024x683.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-768x512.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-90x60.webp 90w, https://semiconductorinsight.com/wp-content/uploads/2025/06/Single-Channel-Video-Encoder-Market-135x90.webp 135w" data-sizes="(max-width: 1536px) 100vw, 1536px" data-ll-status="loaded"> A single channel video encoder is a crucial component in digital video systems that compresses or decompresses video streams for efficient transmission and storage. These devices typically incorporate audio/video codec chips (supporting standards like H.264, H.265, and MPEG-4), network interfaces, and control protocols to enable high-quality video processing. The technology plays a vital role in applications ranging from broadcast television to security surveillance systems.

List of Key Single Channel Video Encoder Companies Profiled

- Hikvision (China)

- VITEC (France)

- Harmonic (U.S.)

- Motorola Solutions (U.S.)

- Cisco (U.S.)

- CommScope (U.S.)

- HaiVision (Canada)

- Axis Communications (Sweden)

- Dahua Technology (China)

- Panasonic (Japan)

- Niagara Video Corporation (U.S.)

- Datavideo (Taiwan)

- Cathexis (South Africa)

Recent market developments highlight intensifying competition, with companies increasingly focusing on AI-powered encoding solutions and cloud-based deployment models. The emergence of new compression standards like VVC (Versatile Video Coding) is prompting accelerated R&D investments across the industry. Smaller innovators such as Datavideo are gaining traction by addressing specific niche requirements in educational and house of worship applications, proving that specialized solutions can compete against broader offerings from market leaders.