Side-mounted float level switch is based on the principle of liquid buoyancy and is a level sensor consisting of a magnetic spring switch and a float for detecting the position of the liquid level.

This report provides a deep insight into the global Side-Mounted Float Level Switch market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Side-Mounted Float Level Switch Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Side-Mounted Float Level Switch market in any manner.

Side-Mounted Float Level Switch Market Analysis:

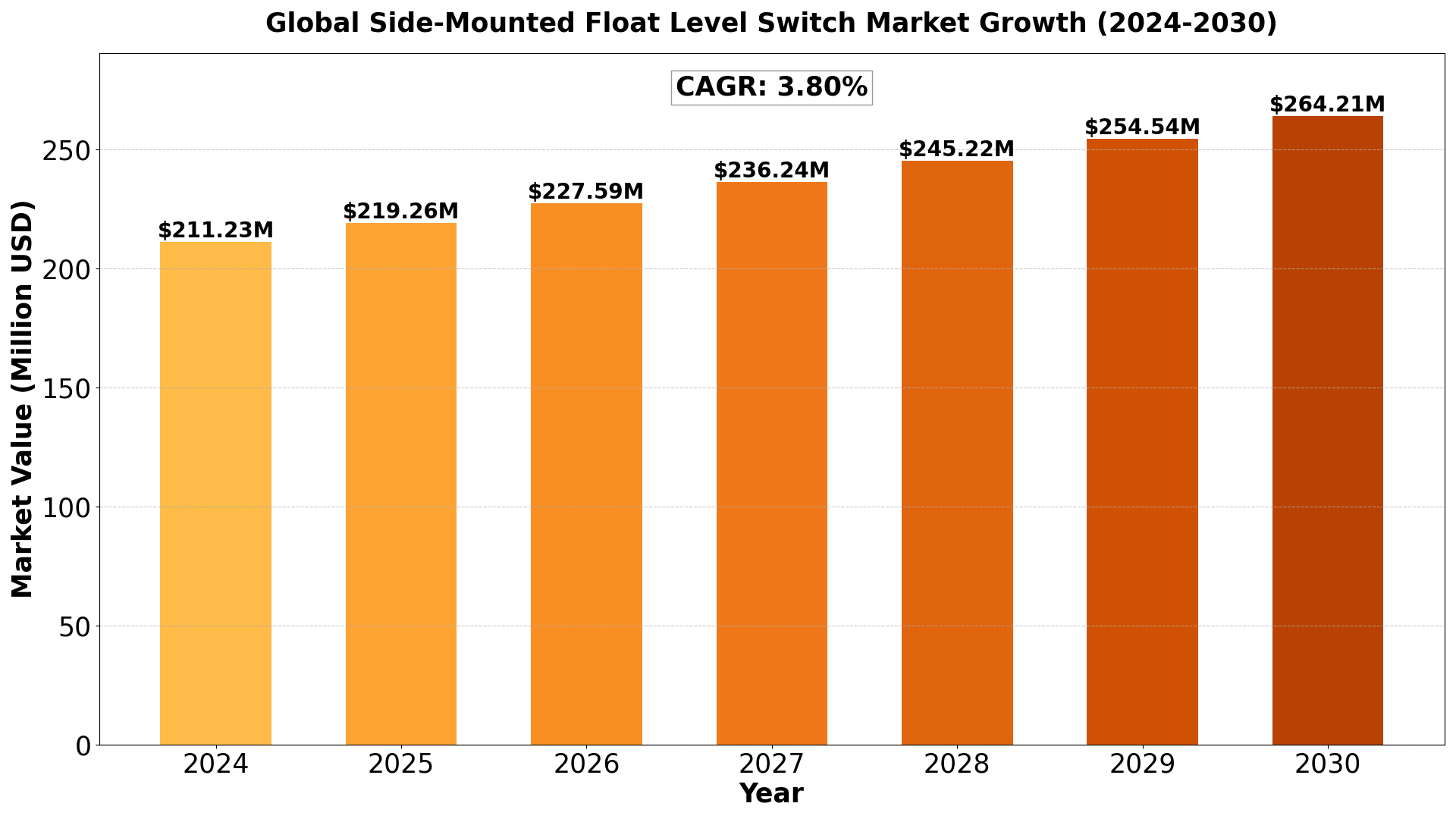

The Global Side-Mounted Float Level Switch Market size was estimated at USD 203.50 million in 2023 and is projected to reach USD 264.21 million by 2030, exhibiting a CAGR of 3.80% during the forecast period.

North America Side-Mounted Float Level Switch market size was USD 53.03 million in 2023, at a CAGR of 3.26% during the forecast period of 2024 through 2030.

https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-300x169.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-1024x576.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-768x432.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-1536x864.webp 1536w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-107x60.webp 107w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-160x90.webp 160w" alt="" width="1920" height="1080" data-lazyloaded="1" data-src="https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0.webp" data-warning="Missing alt text" data-srcset="https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0.webp 1920w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-300x169.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-1024x576.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-768x432.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-1536x864.webp 1536w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-107x60.webp 107w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-160x90.webp 160w" data-sizes="(max-width: 1920px) 100vw, 1920px" data-ll-status="loaded">

https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-300x169.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-1024x576.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-768x432.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-1536x864.webp 1536w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-107x60.webp 107w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-160x90.webp 160w" alt="" width="1920" height="1080" data-lazyloaded="1" data-src="https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0.webp" data-warning="Missing alt text" data-srcset="https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0.webp 1920w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-300x169.webp 300w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-1024x576.webp 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-768x432.webp 768w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-1536x864.webp 1536w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-107x60.webp 107w, https://semiconductorinsight.com/wp-content/uploads/2025/01/global-side-mounted-float-level-switch-market-679b446c3edd0-160x90.webp 160w" data-sizes="(max-width: 1920px) 100vw, 1920px" data-ll-status="loaded"> Side-Mounted Float Level Switch Key Market Trends :

- Increased Demand in Industrial Automation: Side-mounted float level switches are widely used in automation systems for monitoring liquid levels in tanks, driving growth in manufacturing, chemical, and water treatment industries.

- Growth in Oil & Gas Industry: The oil and gas sector uses float level switches for monitoring liquid levels in pipelines, storage tanks, and separators, fueling demand for these devices.

- Rising Focus on Safety and Process Control: With industries prioritizing safety and precision in process control, side-mounted float level switches are preferred for their reliability in critical liquid level detection.

- Technological Advancements: Innovations in material design, wireless integration, and durability are expanding the range of applications for side-mounted float level switches.

- Expansion in Emerging Markets: As industrial sectors grow in emerging economies, the adoption of float level switches in sectors like water treatment, food processing, and chemicals is on the rise.

Shortwave Infrared (SWIR) Market Regional Analysis :

-

North America:

Strong demand driven by EVs, 5G infrastructure, and renewable energy, with the U.S. leading the market.

-

Europe:

Growth fueled by automotive electrification, renewable energy, and strong regulatory support, with Germany as a key player.

-

Asia-Pacific:

Dominates the market due to large-scale manufacturing in China and Japan, with growing demand from EVs, 5G, and semiconductors.

-

South America:

Emerging market, driven by renewable energy and EV adoption, with Brazil leading growth.

-

Middle East & Africa:

Gradual growth, mainly due to investments in renewable energy and EV infrastructure, with Saudi Arabia and UAE as key contributors.

Shortwave Infrared (SWIR) Market Segmentation :

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

- WIKA Group

- Emerson

- Dwyer

- Magnetrol

- RIKO Float

- Kobold

- Nivelco

- Baumer

- Towa Seiden

- Madison

- SMD Fluid Controls

- Besta

- Hy Control

- Emco Control

- Zhejiang KRIPAL

- Feejoy Technology (ShangHai) Co.

- Ltd.

Market Segmentation (by Type)

- Stainless Steel

- Plastic

Market Segmentation (by Application)

- Water Treatment

- Petrochemicals

- Shipbuilding

- Other

Drivers:

- Increasing Industrial Automation: Growing adoption of automation in industries like chemicals, oil & gas, and water treatment is boosting demand for reliable level measurement solutions like side-mounted float level switches.

- Need for Accurate Measurement in Harsh Environments: Side-mounted float level switches offer precise level control in harsh environments, driving their demand in industries like chemicals, petrochemicals, and water treatment.

- Rising Demand for Smart Sensors: Integration of smart technology and IoT for real-time monitoring and predictive maintenance is enhancing the demand for side-mounted float level switches in modern industrial setups.

- Environmental Regulations: Stricter environmental regulations for waste management and resource conservation are driving the need for precise level monitoring systems.

- Energy Efficiency Focus: Increased focus on energy-efficient systems in industries encourages the adoption of float level switches to reduce operational costs.

Opportunities:

- Growth in Emerging Markets: Expanding industrial activities in developing regions like Asia-Pacific create opportunities for market growth.

- Technological Advancements: Integration with IoT, wireless communication, and enhanced sensors offers growth potential in various industries, improving accuracy and efficiency.

- Adoption in Renewable Energy Sectors: Increasing use in renewable energy applications like solar and wind power for monitoring storage systems and fluid levels.

- Integration with Smart Manufacturing: Side-mounted float level switches can be integrated into smart manufacturing systems for better process control and monitoring.

Challenges:

- Compatibility Issues: Side-mounted float level switches may face compatibility issues with existing equipment and infrastructure in older plants.

- Maintenance and Calibration Needs: Regular maintenance and calibration are essential for accuracy, which can be resource-intensive for companies with limited technical expertise.

- Market Competition: Increasing competition from alternative level sensing technologies like capacitance, ultrasonic, and radar sensors poses a challenge to market growth.

Key Benefits of This Market Research:

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the Side-Mounted Float Level Switch Market

- Overview of the regional outlook of the Side-Mounted Float Level Switch Market:

Download Free Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=64061

FAQs

Q1: What are the key driving factors and opportunities in the Side-Mounted Float Level Switch Market?

Q2: Which region is projected to have the largest market share?

Q3: Who are the top players in the Side-Mounted Float Level Switch Market?

Q4: What are the latest technological advancements in the industry?

Q5: What is the current size of the Side-Mounted Float Level Switch Market?

Related Reports:

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/display-driver-ic-ddic-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/industrial-igbt-power-device-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/industrial-automatic-door-sensors-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/rf-transceiver-ics-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/photomasks-for-pcb-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/machine-vision-image-acquisition-lens-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/5g-base-station-rf-chip-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/gas-scrubbers-for-semiconductor-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/global-lithium-battery-separator-market

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

https://semiconductorinsight.com/wp-content/uploads/2023/04/Ceramic-Packages-Market-2_11zon-300x169.png 300w,

https://semiconductorinsight.com/wp-content/uploads/2023/04/Ceramic-Packages-Market-2_11zon-300x169.png 300w,

https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-300x175.webp 300w,

https://semiconductorinsight.com/wp-content/uploads/2025/03/global-smart-roads-anemometers-market-67d15849239d9-1-300x175.webp 300w,

https://semiconductorinsight.com/wp-content/uploads/2025/03/global-single-ended-triode-set-amplifiers-market-67d14e177f808-300x175.webp 300w,

https://semiconductorinsight.com/wp-content/uploads/2025/03/global-single-ended-triode-set-amplifiers-market-67d14e177f808-300x175.webp 300w,