Radar Signal Generators Market: Opportunities, Industry Developments, and Market Share Insights 2025–2032

By SemiconductorinsightPrerana, 2025-09-16

Radar Signal Generators Market , Trends, Business Strategies 2025-2032

MARKET INSIGHTS

The global Radar Signal Generators Market size was valued at US$ 315 million in 2024 and is projected to reach US$ 567 million by 2032, at a CAGR of 7.2% during the forecast period 2025-2032.

Radar signal generators are electronic devices used to simulate radar signals for testing and calibration purposes. These instruments generate precise RF (radio frequency) and microwave signals that mimic real-world radar scenarios, enabling the evaluation of radar receivers, transmitters, and other critical components. The market includes both fixed and portable signal generators, catering to diverse applications in military and civil sectors.

The market growth is primarily driven by increasing defense spending worldwide and the modernization of radar systems. However, supply chain disruptions and high development costs pose challenges. Key players like L3Harris Technologies and Keysight are investing in advanced signal generation technologies, such as software-defined radar test solutions, to meet evolving industry demands. The military segment currently dominates the market, accounting for over 65% of total revenue in 2024.

MARKET DYNAMICS

The growing intersection between electronic warfare and cyber warfare is creating unprecedented challenges for signal generator developers. Modern radar systems increasingly incorporate network connectivity for data fusion, making them vulnerable to cyber-physical attacks that blend RF and digital intrusions. Testing these hybrid threats requires signal generators that can simultaneously output RF waveforms while simulating protocol-level attacks—a capability few commercial units currently offer. Security certification processes (such as NSA Type 1) for such multifunction test equipment can extend beyond 36 months, delaying critical defense programs. The lack of standardized test methodologies for cyber-RF convergence is forcing manufacturers to develop proprietary solutions, fragmenting the market and increasing development risks.

Other Challenges

Workforce Shortages in RF Engineering

The industry faces a critical shortage of engineers skilled in both analog RF design and digital signal processing—a rare combination needed for next-gen signal generator development. Educational institutions produce fewer than 300 qualified RF engineering graduates annually in the U.S., while experienced professionals are being aggressively recruited by aerospace and semiconductor firms. This talent gap is particularly acute for millimeter-wave design expertise, with some companies reporting 12-month vacancy periods for key positions.

Obsolescence Management in Long-Lifecycle Systems

Military radar test equipment often remains in service for 20+ years, creating complex obsolescence management challenges. The rapid evolution of commercial semiconductor technologies frequently outpaces defense procurement cycles, forcing expensive redesigns when critical components become unavailable. One study found that 70% of fielded military test systems require component substitution within 10 years, with requalification costs averaging $500,000 per system.

MARKET OPPORTUNITIES

Emerging Quantum Radar Technologies to Drive Next Wave of Innovation

The development of quantum radar systems—currently in advanced research stages—presents a transformative opportunity for signal generator manufacturers. These systems require ultra-stable frequency references with stability exceeding 1e-15, driving demand for atomic clock-referenced signal sources. Early prototype quantum radars are already demonstrating 30 dB improvement in signal-to-noise ratios compared to conventional systems, suggesting massive future testing requirements. Forward-looking companies are investing in cryogenic signal generation technologies capable of operating at 4K temperatures to support superconducting quantum radar development. The quantum radar market is projected to transition from research labs to limited deployment within 5-7 years, creating a premium segment for specialized test equipment.

Adoption of AI/ML Techniques for Radar Testing Automation

Artificial intelligence is revolutionizing radar test methodologies, creating opportunities for smart signal generator platforms. Machine learning algorithms can optimize test sequences in real-time, reducing characterization time for complex radar systems by 40-60%. Some manufacturers are integrating neural network processors directly into signal generators to enable adaptive waveform generation—automatically adjusting parameters based on device-under-test responses. This convergence of AI and RF test equipment is particularly valuable for 6G research, where beamforming algorithms require testing across thousands of spatial configurations. The AI-enabled test equipment segment is forecast to grow at 28% CAGR through 2030, with radar applications representing the largest vertical.

Expansion of Over-the-Air Testing Facilities for Phased Array Systems

The proliferation of phased array antennas—both in defense and telecom applications—is driving massive investments in over-the-air (OTA) test facilities. These installations require coordinated multi-channel signal generation systems capable of simulating dynamic electromagnetic environments. Recent advancements in phase-coherent multi-unit synchronization now allow testing of arrays with 100+ elements, a capability previously limited to government labs. Commercial 5G infrastructure providers are establishing OTA chambers exceeding 10,000 square feet, each requiring $5-10 million in signal generation equipment. This trend is creating sustained demand for modular, scalable signal generation platforms with precise phase alignment capabilities across dozens of channels.

List of Key Radar Signal Generator Manufacturers

- L3Harris Technologies (U.S.)

- Textron Systems (U.S.)

- Exelis (U.S.)

- Keysight Technologies (U.S.)

- NCSIST (Taiwan)

- AWT Global (U.K.)

- Adacel Technologies (Australia)

- ARI Simulation (U.S.)

- Mercury Systems (U.S.)

- Rockwell Collins (U.S.)

Segment Analysis:

By Type

Fixed Radar Signal Generators Dominate the Market Due to Their High Precision and Stability in Defense Applications

The market is segmented based on type into:

- Fixed

- Subtypes: Bench-top, Rack-mounted, and others

- Portable

- Subtypes: Handheld, Compact, and others

By Application

Military Segment Leads Due to Extensive Use in Radar Testing and Electronic Warfare

The market is segmented based on application into:

- Military

- Subtypes: Radar testing, Electronic countermeasures, Training simulators

- Civil

- Subtypes: Weather monitoring, Air traffic control, Automotive radar testing

By Frequency Range

X-Band Segment Gains Prominence for its Versatility in Defense and Commercial Applications

The market is segmented based on frequency range into:

- L-Band

- S-Band

- C-Band

- X-Band

- Ku/K/Ka-Band

- Others

By End-User

Defense Organizations Hold Major Share Due to Continuous Modernization Programs

The market is segmented based on end-user into:

- Defense organizations

- Research institutions

- Commercial aviation

- Automotive manufacturers

- Others

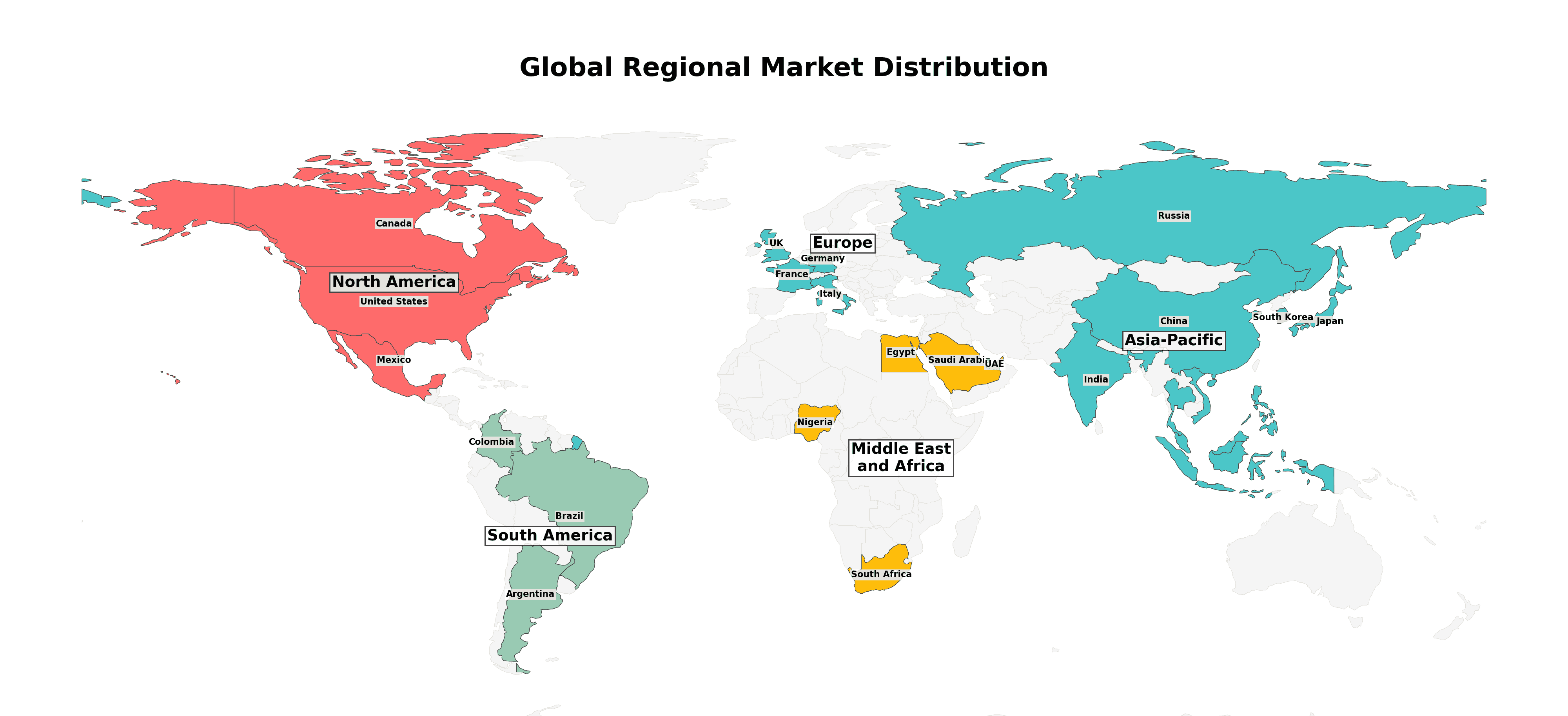

Regional Analysis: Radar Signal Generators Market

North America

The North American radar signal generators market is propelled by defense modernization programs and commercial aviation upgrades , with the U.S. accounting for over 80% of regional demand. The Pentagon’s FY2024 budget allocates $842 billion for defense, including radar system advancements requiring precise signal generation for testing. Civil applications are growing due to FAA-mandated upgrades to Air Traffic Control radars. However, stringent ITAR regulations create barriers for international manufacturers. Key players like L3Harris and Keysight dominate through innovation in multi-band signal synthesis for 5G and aerospace applications. A shift toward software-defined solutions is evident, with portable models gaining traction for field testing.

Europe

European demand stems from military modernization projects like the Eurofighter upgrades and ESA satellite radar programs. Stringent EU electromagnetic compatibility (EMC) directives drive adoption of advanced vector signal generators for compliance testing. The region shows particular strength in automotive radar testing, with Germany’s automotive sector accounting for 35% of regional demand. Collaborative defense projects among NATO members foster standardization, benefiting manufacturers offering interoperable solutions. Challenges include Brexit-related supply chain disruptions and high R&D costs. Water-cooled high-power radar signal generators see rising adoption for naval applications across Mediterranean countries.

Asia-Pacific

This fastest-growing region benefits from China’s military-civil fusion strategy and India’s $130 billion defense modernization plan. Commercial applications dominate in Japan and South Korea, where 77% of demand comes from automotive and telecom sectors. The proliferation of dual-use technologies blurs military-civil boundaries, with Chinese manufacturers like NCSIST gaining market share through cost-competitive solutions. While portable models lead in field maintenance applications, concerns persist about technology transfers and IP protection. Emerging applications in weather radar systems and drone detection present new growth avenues, though export controls on high-end models constrain some markets.

South America

Market growth remains constrained by budget limitations despite Brazil’s SISFRON border surveillance system and Argentina’s radar network upgrades. Over 60% of regional demand comes from fixed installations at airports and military bases. Dependence on imported technology persists due to limited local manufacturing capabilities. Economic instability delays procurement cycles, favoring refurbished equipment markets. Recent investments in coastal surveillance systems create niche opportunities for marine radar signal generators. Regulatory harmonization efforts across MERCOSUR countries could stimulate cross-border trade if implemented effectively.

Middle East & Africa

The market shows polarized growth , with GCC nations driving 68% of demand through megaprojects like Saudi Arabia’s NEOM smart city radar infrastructure. Counter-drone applications see rapid adoption following Houthi missile threats. Sub-Saharan Africa relies heavily on donor-funded systems, creating a preference for entry-level portable generators. Geopolitical tensions accelerate military procurements, though technology embargoes limit options in some markets. Localized maintenance requirements favor suppliers with regional service centers. Long-term potential exists in mineral exploration radars as mining investments increase across the continent.

Download Sample Report https://semiconductorinsight.com/download-sample-report/?product_id=107591

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Market?

Which key companies operate in Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/wi-fi-6-chip-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/grating-scale-displacement-sensor-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/golf-gps-tracker-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/sports-wearable-tracking-system-marke

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/refrigerator-camera-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/hologram-mesh-screen-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/custom-capacitor-assemblies-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/active-optical-module-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/remote-control-rf-modules-market

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Silicon Carbide Diffusion Tube Market: Trends, Revenue Forecast, and Regional Analysis 2025–2032

By SemiconductorinsightPrerana, 2025-09-16

Silicon Carbide Diffusion Tube Market , Trends, Business Strategies 2025-2032

MARKET INSIGHTS

The global Silicon Carbide Diffusion Tube Market size was valued at US$ 185 million in 2024 and is projected to reach US$ 398 million by 2032, at a CAGR of 9.5% during the forecast period 2025-2032.

Download Sample Report https://semiconductorinsight.com/download-sample-report/?product_id=107590

Silicon Carbide Diffusion Tubes are high-performance ceramic components widely used in semiconductor manufacturing, solar energy, and LED production. These tubes offer exceptional thermal stability, corrosion resistance, and mechanical strength, making them ideal for high-temperature diffusion processes. They come in various sizes, including below 150 mm, 150-350 mm, and above 350 mm, to meet diverse industrial requirements.

The market is driven by the growing semiconductor industry, advancements in renewable energy technologies, and increasing demand for energy-efficient lighting solutions. Key players such as Ferrotec Material Technologies Corporation , Coorstek , and Worldex Industry dominate the market, collectively holding a significant revenue share. Recent expansions in semiconductor fabrication facilities, particularly in Asia-Pacific, are expected to further propel market growth in the coming years.

MARKET DYNAMICS

The silicon carbide diffusion tube market faces growing competition from advanced quartz and ceramic composite materials that offer comparable performance at lower price points. Recent developments in quartz doping technologies have produced variants capable of withstanding temperatures up to 1300°C – sufficient for many mid-range semiconductor processes. These alternatives currently capture about 35% of the diffusion tube market for processes below 1200°C, creating pricing pressure on silicon carbide solutions.

Technology Transition Risks

The semiconductor industry’s transition to larger wafer sizes presents both opportunities and challenges for silicon carbide tube manufacturers. While the shift to 300mm and 450mm wafers drives demand for larger diameter tubes, it also requires complete retooling of production lines. Industry estimates suggest the transition to next-generation wafer sizes could require capital investments exceeding $50 million per production line, potentially slowing adoption rates as manufacturers evaluate return on investment.

Quality Consistency Concerns

Maintaining material purity and dimensional tolerances across large-scale production runs remains an ongoing challenge. Even minor variations in silicon carbide composition or tube wall thickness can significantly impact diffusion process uniformity. Recent quality control data reveals that approximately 12% of tubes fail to meet the stringent specifications required for advanced semiconductor nodes below 10nm, creating bottlenecks for manufacturers serving this high-value segment.

Emerging Applications in Wide Bandgap Semiconductor Production to Open New Revenue Streams

The rapid adoption of silicon carbide and gallium nitride semiconductors for electric vehicles and power electronics presents substantial growth opportunities for diffusion tube manufacturers. These next-generation semiconductors require even higher processing temperatures (up to 1800°C) where silicon carbide becomes the only viable containment material. With the wide bandgap semiconductor market projected to grow at over 30% CAGR through 2030, specialized diffusion tubes tailored for these applications could represent a $500 million addressable market within five years.

Aftermarket Services Expansion

The installed base of silicon carbide diffusion tubes has grown significantly in recent years, creating opportunities for maintenance, refurbishment, and recycling services. Analysis suggests the aftermarket for silicon carbide components could grow to represent 25% of total industry revenue by 2028 as manufacturers develop proprietary recoating and repair processes that extend tube lifespan by up to 40%. Several leading players have recently launched dedicated service divisions to capitalize on this recurring revenue opportunity.

Regional Manufacturing Expansion

Government incentives for semiconductor equipment localization in North America and Europe are prompting strategic investments in regional production. The market could see 5-7 new silicon carbide component manufacturing facilities established outside traditional Asian production hubs within the next three years, reducing lead times and improving supply chain resilience for end-users in these regions.

The silicon carbide diffusion tube market faces growing competition from advanced quartz and ceramic composite materials that offer comparable performance at lower price points. Recent developments in quartz doping technologies have produced variants capable of withstanding temperatures up to 1300°C – sufficient for many mid-range semiconductor processes. These alternatives currently capture about 35% of the diffusion tube market for processes below 1200°C, creating pricing pressure on silicon carbide solutions.

Technology Transition Risks

The semiconductor industry’s transition to larger wafer sizes presents both opportunities and challenges for silicon carbide tube manufacturers. While the shift to 300mm and 450mm wafers drives demand for larger diameter tubes, it also requires complete retooling of production lines. Industry estimates suggest the transition to next-generation wafer sizes could require capital investments exceeding $50 million per production line, potentially slowing adoption rates as manufacturers evaluate return on investment.

Quality Consistency Concerns

Maintaining material purity and dimensional tolerances across large-scale production runs remains an ongoing challenge. Even minor variations in silicon carbide composition or tube wall thickness can significantly impact diffusion process uniformity. Recent quality control data reveals that approximately 12% of tubes fail to meet the stringent specifications required for advanced semiconductor nodes below 10nm, creating bottlenecks for manufacturers serving this high-value segment..

List of Key Silicon Carbide Diffusion Tube Manufacturers

- Ferrotec Material Technologies Corporation (Japan)

- Coorstek (U.S.)

- Worldex Industry (China)

- CE-MAT (Germany)

- Kallex Company (China)

- Shandong Huamei (China)

- Xian Zhongwei (China)

- Tangshan FCT (China)

- Ningbo VET Energy Technology (China)

Segment Analysis:

By Type

Below 150 mm Segment Leads the Market Due to Widespread Adoption in Semiconductor Fabrication

The Silicon Carbide Diffusion Tube market is segmented based on type into:

- Below 150 mm

- 150-350 mm

- Above 350 mm

By Application

Semiconductor Segment Dominates Owing to High Demand for High-Temperature Processing Solutions

The market is segmented based on application into:

- Semiconductor

- Solar Energy

- LED

By Material Grade

High-Purity Silicon Carbide Gains Importance for Critical Semiconductor Applications

The market is segmented based on material grade into:

- Standard Grade

- High Purity Grade

Regional Analysis: Silicon Carbide Diffusion Tube Market

North America

The Silicon Carbide Diffusion Tube market in North America is driven by its advanced semiconductor and solar energy industries , particularly in the U.S., where demand is bolstered by substantial R&D investments and strict quality standards. The region benefits from a well-established supply chain and collaborations between manufacturers like Coorstek and Ferrotec. Government initiatives supporting next-generation electronics and renewable energy further stimulate growth. However, high production costs and competition from Asian suppliers pose challenges. The market is expected to rise steadily, leveraging technological advancements in SiC-based power electronics and LED applications.

Europe

Europe’s market thrives on stringent regulatory frameworks that emphasize eco-friendly production and energy-efficient semiconductor manufacturing . Countries like Germany and France lead in adopting SiC diffusion tubes for automotive and industrial applications , thanks to strong collaborations between research institutions and manufacturers. Despite being a mature market, Europe faces constraints from high raw material costs and reliance on imports. The shift toward sustainable energy solutions , including solar and power electronics, continues to drive demand. Emerging innovations in wide-bandgap semiconductors present long-term opportunities for market expansion.

Asia-Pacific

The Asia-Pacific region dominates the global Silicon Carbide Diffusion Tube market, accounting for the highest consumption volume . China, Japan, and South Korea lead due to their thriving semiconductor and LED industries , supported by aggressive government policies and local manufacturing hubs. The cost-competitive production ecosystem attracts global players, though quality disparities persist in some markets. Countries like India are gradually increasing their adoption of SiC technology , fueled by rising renewable energy projects. The region’s market is expected to maintain rapid growth, driven by expanding 5G infrastructure and electric vehicle manufacturing , though supply chain disruptions occasionally hinder progress.

South America

South America’s market remains nascent but promising , with Brazil showing gradual uptake in semiconductor and solar panel production . Limited local manufacturing capabilities and economic instability slow widespread adoption, forcing reliance on imports. However, increasing investments in renewable energy infrastructure and partnerships with global suppliers offer growth potential. Manufacturers must navigate trade barriers and logistical challenges to capitalize on this emerging demand. The market’s trajectory largely depends on policy reforms and technological advancements in material sciences.

Middle East & Africa

This region presents long-term potential , particularly in Gulf countries like Saudi Arabia and the UAE, where diversification efforts are boosting semiconductor and solar energy projects. However, the market is constrained by limited industrial infrastructure and a lack of local expertise. Africa’s growth is slower due to funding gaps and fragmented supply chains, though South Africa shows modest demand for LED and energy applications . Partnerships with global manufacturers and technology transfers could accelerate market development, provided geopolitical and economic hurdles are addressed.

Download Sample Report https://semiconductorinsight.com/download-sample-report/?product_id=107590

What is the current market size of Market?

Which key companies operate in Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/wi-fi-6-chip-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/grating-scale-displacement-sensor-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/golf-gps-tracker-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/sports-wearable-tracking-system-marke

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/refrigerator-camera-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/hologram-mesh-screen-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/custom-capacitor-assemblies-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/active-optical-module-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/remote-control-rf-modules-market

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

SiC Susceptor Market: Dynamics, Challenges, and Innovation Strategies 2025–2032

By SemiconductorinsightPrerana, 2025-09-16

SiC Susceptor Market , Trends, Business Strategies 2025-2032

MARKET INSIGHTS

The global SiC Susceptor Market size was valued at US$ 220 million in 2024 and is projected to reach US$ 456 million by 2032, at a CAGR of 8.9% during the forecast period 2025-2032. While North America leads in adoption, Asia-Pacific shows the highest growth potential with China accounting for over 30% of regional demand.

Download Sample Report https://semiconductorinsight.com/download-sample-report/?product_id=107589

Silicon carbide (SiC) susceptors are critical components in semiconductor manufacturing, particularly in epitaxial growth processes for power electronics and LED production. These high-purity graphite components coated with SiC facilitate uniform heat distribution in chemical vapor deposition (CVD) and metal-organic chemical vapor deposition (MOCVD) systems. The pancake-type segment dominates with 62% market share due to its compatibility with single-wafer processing, though barrel-type susceptors are gaining traction for batch processing efficiency.

Market expansion is driven by surging demand for wide-bandgap semiconductors in electric vehicles and renewable energy systems, where SiC devices enable higher efficiency. However, supply chain constraints for high-purity graphite and complex coating processes present challenges. Key players like Toyo Tanso and SGL Carbon are investing in capacity expansions, with Tokai Carbon recently commissioning a new production facility in 2023 to meet growing 200mm wafer demand.

MARKET DYNAMICS

SiC susceptors gradually degrade during high-temperature semiconductor manufacturing processes, developing surface defects that eventually require replacement. This ongoing replacement cycle creates operational challenges for semiconductor manufacturers who require uninterrupted production schedules. The average lifespan of a high-quality SiC susceptor in continuous operation is approximately 6-12 months, depending on process conditions, resulting in significant recurring costs for fabrication facilities.

Standardization Issues

The lack of globally standardized specifications for SiC susceptors complicates procurement and quality assurance processes. Manufacturers often need to customize susceptors for specific equipment configurations, hindering economies of scale and increasing lead times.

Technical Support Requirements

The integration of advanced susceptor designs requires substantial technical support and training. As semiconductor fabrication processes become more sophisticated, the knowledge gap between susceptor manufacturers and end-users continues to present implementation challenges.

Emerging Applications in Power Electronics to Create New Growth Avenues

The expansion of 5G infrastructure and renewable energy systems is creating substantial opportunities for SiC susceptor manufacturers. These high-frequency applications demand power electronic components with superior thermal performance that can only be produced using advanced susceptor technology. The renewable energy sector alone is expected to drive significant demand growth as solar inverters and wind power converters increasingly adopt SiC-based solutions.

Innovations in Coating Technologies to Enhance Market Potential

Recent advancements in protective coatings present promising opportunities to extend susceptor lifespans and improve performance. New coating formulations that reduce surface degradation and contamination in high-temperature environments could significantly enhance the value proposition of premium SiC susceptors. These innovations are particularly relevant for next-generation semiconductor nodes where even minor contamination can impact yields.

Additionally, the development of hybrid susceptor designs combining SiC with other advanced materials may open new application areas while potentially reducing overall system costs through performance optimization.

List of Key SiC Susceptor Manufacturers

- Toyo Tanso Co., Ltd. (Japan)

- Top Seiko Co., Ltd. (Japan)

- SGL Carbon (Germany)

- Tokai Carbon Co., Ltd. (Japan)

- Mersen (France)

- CoorsTek, Inc. (U.S.)

- Schunk Xycarb Technology (Netherlands)

Segment Analysis:

By Type

Pancake SiC Susceptors Lead the Market Due to High Thermal Stability in Semiconductor Manufacturing

The market is segmented based on type into:

- Pancake

- Barrel

- Cylindrical

- Custom configurations

- Others

By Application

Semiconductor Segment Dominates Owing to Increased Demand for Wafer Processing Applications

The market is segmented based on application into:

- Semiconductor

- Power electronics

- LED manufacturing

- Wireless communication devices

- Others

By Material Grade

High-Purity SiC Segment Holds Major Share for Critical Semiconductor Applications

The market is segmented based on material grade into:

- High-purity SiC

- Industrial grade SiC

- Coated SiC

- Others

By End-User

Foundries Lead Consumption Due to Large-Scale Semiconductor Production Requirements

The market is segmented based on end-user into:

- Semiconductor foundries

- IDMs (Integrated Device Manufacturers)

- Research institutions

- Wafer manufacturers

- Others

Regional Analysis: SiC Susceptor Market

North America

The North American SiC susceptor market is driven by robust semiconductor manufacturing and research investments, particularly in the U.S. With the CHIPS and Science Act injecting $52.7 billion into domestic semiconductor production, demand for high-purity SiC susceptors used in epitaxial growth processes is accelerating. Leading manufacturers like CoorsTek and Mersen dominate the regional supply chain, specializing in large-diameter pancake susceptors for 5G and electric vehicle (EV) power electronics . However, stringent export controls on advanced semiconductor technologies have created supply chain complexities, pushing local players to develop vertically integrated production capabilities.

Europe

Europe’s market prioritizes sustainability, with SGL Carbon and Tokai Carbon leading the adoption of recyclable SiC susceptor solutions. The EU’s €43 billion Chips Act is fueling demand for susceptors in compound semiconductor fabs, particularly in Germany and France. A notable trend is the shift from graphite-coated to pure SiC susceptors , driven by stricter contamination control requirements in silicon carbide wafer production. While innovation is strong, dependence on Asian raw material suppliers and energy-intensive manufacturing processes present cost challenges. Collaborative R&D initiatives between universities and corporations aim to improve susceptor lifespans beyond 1,500 deposition cycles .

Asia-Pacific

Accounting for over 60% of global SiC susceptor consumption , the APAC region is powered by China’s booming third-generation semiconductor industry. Local players like Toyo Tanso and Top Seiko aggressively compete on price, offering susceptors 20-30% cheaper than Western counterparts. Japan leads in technical sophistication, with susceptors tailored for ultrahigh-temperature (up to 2,000°C) MOCVD applications . India is emerging as a growth hotspot, with new SiC wafer plants driving 15% YoY demand increases . The region’s main challenge is quality consistency, as rapid production scaling sometimes compromises dimensional tolerances critical for uniform thermal distribution.

South America

The South American market remains niche but shows potential, with Brazil investing in local assembly of power electronics modules . Most susceptors are imported from China or the U.S., creating 6-8 week lead times that hinder just-in-time manufacturing. Argentina’s developing rare earth mining sector could enable future raw material localization, though current susceptor adoption focuses mainly on research institutions rather than volume production. Currency volatility and 35-40% import duties on advanced ceramics significantly inflate end-user costs, limiting market expansion.

Middle East & Africa

This region is in the early adoption phase, with Saudi Arabia and UAE leading demand through investments in semiconductor test and packaging facilities. The lack of local manufacturing means nearly 90% of susceptors are imported , primarily from Europe. High-growth potential exists in RF device production for telecommunications infrastructure projects, though market education about SiC susceptor benefits versus traditional graphite remains a barrier. Political instability in some areas creates supply chain uncertainties, while desert environmental conditions require specialized coatings to prevent particulate contamination during susceptor use.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Market?

Which key companies operate in Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/wi-fi-6-chip-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/grating-scale-displacement-sensor-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/golf-gps-tracker-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/sports-wearable-tracking-system-marke

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/refrigerator-camera-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/hologram-mesh-screen-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/custom-capacitor-assemblies-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/active-optical-module-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/remote-control-rf-modules-market

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Organic Type Temperature Fuse Market: Size, Technological Advancements, and Future Prospects 2025–2032

By SemiconductorinsightPrerana, 2025-09-16

Organic Type Temperature Fuse Market , Trends, Business Strategies 2025-2032

Download Sample Report https://semiconductorinsight.com/download-sample-report/?product_id=103093

MARKET INSIGHTS

The global Organic Type Temperature Fuse Market size was valued at US$ 345 million in 2024 and is projected to reach US$ 434 million by 2032, at a CAGR of 2.9% during the forecast period 2025-2032.

Organic type temperature fuses are critical safety components designed to protect electrical circuits from overheating. These devices operate on a thermal cutoff principle: when ambient temperature exceeds the fuse’s rating, an organic temperature-sensitive material melts, triggering a spring mechanism that permanently breaks the circuit. This fail-safe mechanism makes them indispensable in applications where temperature regulation is crucial.

The market growth is driven by increasing adoption in consumer electronics, automotive systems, and industrial equipment where overheating protection is mandatory. Asia-Pacific dominates the market with 42% share in 2024, fueled by China’s electronics manufacturing boom. Key players including Littelfuse and Schott are expanding their production capacities to meet the growing demand, particularly for low-voltage variants which accounted for 68% of 2024 sales. Recent regulatory mandates for enhanced electrical safety across multiple industries are further accelerating market expansion.

MARKET DYNAMICS

Rapid Growth in Consumer Electronics to Fuel Organic Type Temperature Fuse Demand

The global surge in smart home appliances and connected devices is creating strong demand for reliable circuit protection components like organic type temperature fuses. With the smart home market projected to grow at over 14% CAGR , manufacturers are increasingly adopting these fuses for applications ranging from washing machines to air conditioners. The unique thermal triggering mechanism of organic fuses makes them particularly suitable for temperature-sensitive applications where precise circuit interruption is critical. Major electronics manufacturers are now standardizing on these components for their superior reliability compared to mechanical alternatives.

Stringent Safety Regulations Driving Adoption Across Industries

Increasingly strict international safety standards are compelling manufacturers across multiple sectors to upgrade their overcurrent protection systems. The organic type temperature fuse market benefits significantly from these regulatory changes because its fail-safe mechanism meets the most rigorous safety requirements. Industries including automotive (where electric vehicle adoption is accelerating), industrial automation, and telecommunications infrastructure are all transitioning to these solutions. The ability of organic fuses to provide permanent circuit disconnection at precise temperature thresholds makes them indispensable for compliance with modern safety certifications.

Expansion of 5G Infrastructure Creating New Applications

The global rollout of 5G networks presents a significant growth opportunity for organic type temperature fuses. Telecom equipment requires advanced thermal protection due to higher power densities and smaller form factors. Major infrastructure providers are increasingly specifying organic fuses for base stations and network equipment, with some regions showing 20% year-over-year growth in these applications. The market is further buoyed by the integration of these components in power supply units for 5G small cells, where space constraints make traditional circuit breakers impractical.

Price Pressure from Alternative Technologies Constrains Market Expansion

While organic type temperature fuses offer superior performance characteristics, the market faces challenges from lower-cost alternatives like resettable thermal switches. Price-sensitive applications in emerging markets often opt for these alternatives despite their limitations in precision and reliability. The competitive landscape has intensified as some manufacturers achieve 15-20% cost reductions through alternative fuse technologies. However, industry experts note that this cost advantage often comes at the expense of product lifespan and safety margins.

Other Trends

Technological Advancements in Fuse Design

Innovations in materials science are enhancing the performance of organic type temperature fuses, making them more responsive and durable. For instance, manufacturers are focusing on improving the thermal sensitivity of the organic sensing block to enable faster response times. Additionally, the development of low-voltage fuses , which accounted for over 60% of the market share in 2024, is meeting the needs of compact electronic devices such as smartphones and wearables. These advancements are critical in reducing failure rates and enhancing energy efficiency in modern circuits.

Expansion of Automotive and Renewable Energy Applications

The automotive sector is emerging as a key driver for organic type temperature fuses, particularly in electric vehicles (EVs) and battery management systems. With global EV sales exceeding 10 million units annually , the need for thermal protection in high-energy-density batteries is accelerating demand. Similarly, renewable energy systems, such as solar inverters and wind turbines, are adopting these fuses to mitigate risks associated with overheating. The reliability of organic temperature fuses in extreme conditions makes them indispensable for sustainable energy infrastructure, further boosting market potential.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovation and Expansion Define the Organic Type Temperature Fuse Market

The global organic type temperature fuse market showcases a moderately competitive landscape, characterized by the presence of both established multinational corporations and emerging regional players. Schott AG and Littelfuse Inc. currently dominate the market, collectively accounting for approximately 35% of global revenue share in 2024, primarily due to their extensive product portfolios spanning low and high voltage applications across industrial and consumer segments.

Bel Fuse Inc. and Emerson Electric Co. maintain strong positions in the market through continuous technological advancements in thermal protection solutions. These companies have particularly strengthened their foothold in the automotive sector, where demand for organic temperature fuses is growing at nearly 8% annually, driven by increasing electrification of vehicles.

The competitive scenario is further intensified by Japanese players like Uchihashi Estec Co., Ltd. and Sungwoo Industrial , who are making significant strides in miniaturization technologies. Their ultra-compact temperature fuse solutions are gaining traction in consumer electronics, especially in smartphone and wearable device applications where space constraints are critical.

Meanwhile, European manufacturers such as Limitor GmbH are focusing on high-temperature applications, developing fuses capable of operating in extreme environments up to 150°C. This specialization allows them to maintain premium pricing power in niche industrial segments like renewable energy systems and heavy machinery.

List of Key Organic Type Temperature Fuse Manufacturers

- Schott AG (Germany)

- Littelfuse, Inc. (U.S.)

- Bel Fuse Inc. (U.S.)

- Emerson Electric Co. (U.S.)

- Uchihashi Estec Co., Ltd. (Japan)

- Elmwood Sensors (U.S.)

- Betterfuse (China)

- SETsafe (Germany)

- Sinolec Electronics (China)

- Lanson Electronics (Taiwan)

- Cantherm (Canada)

- Sungwoo Industrial (South Korea)

- Limitor GmbH (Germany)

- AUPO (Taiwan)

Segment Analysis:

By Type

Low Voltage Fuse Segment Dominates Due to Widespread Use in Consumer Electronics and Home Appliances

The market is segmented based on type into:

- Low Voltage Fuse

- High Voltage Fuse

By Application

Home Appliance Segment Leads Owing to Rising Demand for Safety Components in Consumer Electronics

The market is segmented based on application into:

- Home Appliance

- Communication

- Automotive

- Others

By End User

Electronics Manufacturers Hold Largest Share Due to Growing Production of Smart Devices

The market is segmented based on end user into:

- Electronics Manufacturers

- Automotive Industry

- Industrial Sector

- Telecommunication Providers

By Material Composition

Organic Compound-Based Fuses Lead Market Due to Superior Thermal Sensitivity

The market is segmented based on material composition into:

- Paraffin-Based

- Rosin-Based

- Wax-Based

- Other Organic Compounds

Regional Analysis: Organic Type Temperature Fuse Market

North America

The North American market for organic type temperature fuses is characterized by stringent safety regulations and high adoption in critical applications such as automotive and home appliances. The U.S. dominates the region, driven by robust demand from manufacturers of HVAC systems, electric vehicles, and industrial equipment. Recent legislation emphasizing equipment safety and energy efficiency has further bolstered market growth. Major manufacturers like Littelfuse and Bel maintain a strong presence here, leveraging advanced manufacturing capabilities and R&D investments. However, price sensitivity among mid-tier OEMs continues to challenge wider adoption of high-performance fuses in cost-competitive segments.

Europe

Europe’s organic temperature fuse market benefits from strict EU directives on electronic safety (e.g., RoHS, EN 60691) and the growing electrification of industries. Germany leads in industrial applications, while France and Italy show high demand in the home appliance sector. The region’s focus on sustainability has accelerated the shift toward lead-free and recyclable fuse materials. European manufacturers like Schott and Emerson emphasize precision engineering and compliance with evolving standards. However, the market faces margin pressures due to rising raw material costs and the need for frequent product recertification under updated regulations.

Asia-Pacific

As the largest regional market, Asia-Pacific contributes over 45% of global demand, propelled by China’s electronics manufacturing boom and India’s expanding automotive sector. Chinese producers like Sinolec dominate the low-voltage fuse segment, catering to price-sensitive buyers across emerging markets. Japan and South Korea prioritize high-reliability fuses for automotive electronics, driven by stringent OEM specifications. While the region shows strong volume growth, intellectual property concerns and inconsistent quality standards among local suppliers remain key challenges for international brands seeking market expansion.

South America

This emerging market demonstrates steady growth, primarily in Brazil’s industrial and appliance manufacturing sectors. The lack of domestic production capabilities creates import dependence, with U.S. and European brands commanding premium positioning. Infrastructure limitations in thermal management systems hinder adoption in high-temperature industrial applications. Recent economic stabilization policies and trade agreements are gradually improving market access, though currency volatility continues to impact pricing strategies for international suppliers.

Middle East & Africa

The region presents niche opportunities in oil/gas equipment and construction-related electrical systems. Gulf Cooperation Council countries lead in adopting imported high-temperature fuses for harsh environment applications. African markets remain underpenetrated but show potential in renewable energy projects requiring thermal protection components. Market growth is constrained by limited technical expertise in fuse selection and installation, creating opportunities for supplier-led education initiatives alongside product distribution.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Organic Type Temperature Fuse markets , covering the forecast period 2025–2032 . It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast : Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Organic Type Temperature Fuse market was valued at US$ 345 million in 2024 and is projected to reach US$ 434 million by 2032.

- Segmentation Analysis : Detailed breakdown by product type (Low Voltage Fuse, High Voltage Fuse) and application (Home Appliance, Communication, Automotive, Others) to identify high-growth segments.

- Regional Outlook : Insights into market performance across North America (USD 85.2 million in 2024), Europe, Asia-Pacific (China estimated at USD 102.4 million by 2032), Latin America, and the Middle East & Africa.

- Competitive Landscape : Profiles of leading market participants including Schott, Littelfuse, Bel, Emerson, and Uchihashi, which collectively held approximately 58% market share in 2024.

- Technology Trends & Innovation : Assessment of fuse safety standards, miniaturization trends, and material science advancements in organic thermal sensing components.

- Market Drivers & Restraints : Evaluation of factors including growing electronics demand, safety regulations, and challenges from alternative protection technologies.

- Stakeholder Analysis : Insights for component manufacturers, OEMs, system integrators, and investors regarding the evolving ecosystem.

Download Sample Report https://semiconductorinsight.com/download-sample-report/?product_id=107588

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Market?

Which key companies operate in Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/wi-fi-6-chip-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/grating-scale-displacement-sensor-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/golf-gps-tracker-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/sports-wearable-tracking-system-marke

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/refrigerator-camera-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/hologram-mesh-screen-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/custom-capacitor-assemblies-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/active-optical-module-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/remote-control-rf-modules-market

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Zirconium Dioxide Oxygen Sensors Market: Demand, Competitive Landscape, and Investment Outlook 2025–2032

By SemiconductorinsightPrerana, 2025-09-16

Zirconium Dioxide Oxygen Sensors Market , Global Outlook and Forecast 2025-2031

Zirconium Dioxide Oxygen Sensors Market Analysis:

The global Zirconium Dioxide Oxygen Sensors Market was valued at 6704 million in 2024 and is projected to reach US$ 7874 million by 2031, at a CAGR of 2.4% during the forecast period.

Zirconium Dioxide Oxygen Sensors Market Overview

Zirconia oxygen sensors are comprised of a zirconium-dioxide-based solid electrolyte. Zirconia oxygen sensors have unique characteristics, such as fast operational readiness, temperature resistance, not sensitive to hydraulic shock, etc. It is used extensively to monitor the air-to-fuel ratio of internal combustion engines.

Global Zirconia Oxygen Sensors key players include Bosch, NGK-NTK, Denso, Delphia, Hyundai KEFICO, etc. Global top five manufacturers hold a share over 60%. Europe is the largest market, with a share over 25%, followed by USA and Japan, both have a share over 40%. In terms of product, Planar is the largest segment, with a share over 70%. And in terms of application, the largest application is Automotive, followed by Motorcycle, Industrial, etc.

We have surveyed the Zirconium Dioxide Oxygen Sensors manufacturers, suppliers, distributors, and industry experts on this industry, involving the sales, revenue, demand, price change, product type, recent development and plan, industry trends, drivers, challenges, obstacles, and potential risks

This report aims to provide a comprehensive presentation of the global market for Zirconium Dioxide Oxygen Sensors, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding Zirconium Dioxide Oxygen Sensors. This report contains market size and forecasts of Zirconium Dioxide Oxygen Sensors in global, including the following market information:

- Global Zirconium Dioxide Oxygen Sensors market revenue, 2020-2025, 2026-2031, ($ millions)

- Global Zirconium Dioxide Oxygen Sensors market sales, 2020-2025, 2026-2031, (K Units)

- Global top five Zirconium Dioxide Oxygen Sensors companies in 2024 (%)

Zirconium Dioxide Oxygen Sensors Key Market Trends :

Growing Demand in Automotive Industry

The increasing adoption of zirconium dioxide oxygen sensors in modern vehicles for fuel efficiency and emissions control is driving market growth.

Technological Advancements

Continuous improvements in sensor design, such as miniaturization and enhanced durability, are boosting the adoption of advanced zirconia oxygen sensors.

Stringent Emission Regulations

Governments worldwide are implementing strict emission standards, increasing the demand for high-performance oxygen sensors in vehicles and industrial applications.

Rising Industrial Applications

The industrial sector is increasingly using these sensors for combustion efficiency monitoring and environmental safety applications.

Growth in Electric and Hybrid Vehicles

Although EVs do not require oxygen sensors, hybrid vehicles still depend on them, ensuring steady market demand.

Zirconium Dioxide Oxygen Sensors Market Regional Analysis :

https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-300x137.png 300w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-1024x468.png 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-768x351.png 768w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-1536x702.png 1536w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-2048x935.png 2048w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-131x60.png 131w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-197x90.png 197w" alt="semi insight" width="4000" height="1827" data-lazyloaded="1" data-src="https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1.png" data-srcset="https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1.png 4000w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-300x137.png 300w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-1024x468.png 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-768x351.png 768w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-1536x702.png 1536w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-2048x935.png 2048w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-131x60.png 131w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-197x90.png 197w" data-sizes="(max-width: 4000px) 100vw, 4000px" data-ll-status="loaded">

https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-300x137.png 300w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-1024x468.png 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-768x351.png 768w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-1536x702.png 1536w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-2048x935.png 2048w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-131x60.png 131w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-197x90.png 197w" alt="semi insight" width="4000" height="1827" data-lazyloaded="1" data-src="https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1.png" data-srcset="https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1.png 4000w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-300x137.png 300w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-1024x468.png 1024w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-768x351.png 768w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-1536x702.png 1536w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-2048x935.png 2048w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-131x60.png 131w, https://semiconductorinsight.com/wp-content/uploads/2025/01/download-34_11zon-1-197x90.png 197w" data-sizes="(max-width: 4000px) 100vw, 4000px" data-ll-status="loaded">

-

North America:

Strong demand driven by EVs, 5G infrastructure, and renewable energy, with the U.S. leading the market.

-

Europe:

Growth fueled by automotive electrification, renewable energy, and strong regulatory support, with Germany as a key player.

-

Asia-Pacific:

Dominates the market due to large-scale manufacturing in China and Japan, with growing demand from EVs, 5G, and semiconductors.

-

South America:

Emerging market, driven by renewable energy and EV adoption, with Brazil leading growth.

-

Middle East & Africa:

Gradual growth, mainly due to investments in renewable energy and EV infrastructure, with Saudi Arabia and UAE as key contributors.

Total Market by Segment:

Global Zirconium Dioxide Oxygen Sensors market, by Type, 2020-2025, 2026-2031 ($ millions) & (K Units)

Global Zirconium Dioxide Oxygen Sensors market segment percentages, by Type, 2024 (%)

- Thimble Type

- Planar Type

- Others

Global Zirconium Dioxide Oxygen Sensors market, by Application, 2020-2025, 2026-2031 ($ Millions) & (K Units)

Global Zirconium Dioxide Oxygen Sensors market segment percentages, by Application, 2024 (%)

- Automotive

- Motorcycle

- Industrial

- Others

Competitor Analysis

The report also provides analysis of leading market participants including:

- Key companies Zirconium Dioxide Oxygen Sensors revenues in global market, 2020-2025 (estimated), ($ millions)

- Key companies Zirconium Dioxide Oxygen Sensors revenues share in global market, 2024 (%)

- Key companies Zirconium Dioxide Oxygen Sensors sales in global market, 2020-2025 (estimated), (K Units)

- Key companies Zirconium Dioxide Oxygen Sensors sales share in global market, 2024 (%)

Further, the report presents profiles of competitors in the market, key players include:

- NGK-NTK

- Bosch

- Denso

- Delphi

- Bacharach

- Figaro

- FAE

- SST Sensing

- Ceradex

- First Sensor

- Walker Products

- Eaton

- Fujikura

- AMI

- Cubic Sensor and Instrument

- Pucheng

- Ampron

- Volkse

- Lambda Electronic

Drivers

Increasing Automotive Production

The expanding global automobile industry, particularly in emerging economies, is fueling the demand for zirconium dioxide oxygen sensors.

Rising Demand for Fuel Efficiency

Vehicle manufacturers are integrating oxygen sensors to improve fuel efficiency and reduce carbon emissions.

Advancements in Sensor Technology

Innovations like planar oxygen sensors are improving performance and reliability, further driving market growth.

Restraints

High Cost of Advanced Sensors

The price of technologically advanced oxygen sensors can be a limiting factor for cost-sensitive markets.

Market Shift Towards Electric Vehicles

The transition to electric vehicles reduces the demand for oxygen sensors, as EVs do not use combustion engines.

Complex Manufacturing Process

The production of zirconium dioxide oxygen sensors requires specialized materials and processes, which can limit scalability.

Opportunities

Adoption in Industrial Applications

Growing use in industries such as power generation, chemical processing, and manufacturing is expanding the market scope.

Expansion in Emerging Markets

Increasing vehicle production and industrial development in regions like Asia-Pacific present lucrative opportunities.

Integration with IoT and Smart Technologies

Smart oxygen sensors with IoT capabilities are enhancing real-time monitoring and diagnostics, opening new growth avenues.

Challenges

Intense Market Competition

Major players like Bosch, NGK-NTK, and Denso dominate the market, making it challenging for new entrants to compete.

Supply Chain Disruptions

Fluctuations in raw material availability and global supply chain issues can affect sensor production and pricing.

Regulatory Compliance

Meeting diverse regulatory standards across different regions can be complex and resource-intensive for manufacturers.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Market?

Which key companies operate in Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/wi-fi-6-chip-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/grating-scale-displacement-sensor-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/golf-gps-tracker-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/sports-wearable-tracking-system-marke

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/refrigerator-camera-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/hologram-mesh-screen-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/custom-capacitor-assemblies-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/active-optical-module-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/remote-control-rf-modules-market

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

Second-hand Semiconductor Equipment Market:Analysis, Key Players, and Strategic Insights 2025–2032

By SemiconductorinsightPrerana, 2025-09-16

Second-hand Semiconductor Equipment Market Size, Trends, Business Strategies 2025-2032

MARKET INSIGHTS

The global FTTX Active Equipment Market size was valued at US$ 4.8 billion in 2024 and is projected to reach US$ 8.2 billion by 2032, at a CAGR of 6.5% during the forecast period 2025-2032.

Download Sample Report https://semiconductorinsight.com/download-sample-report/?product_id=41128

Second-hand Semiconductor Equipment Market Analysis:

The global Second-hand Semiconductor Equipment market was valued at US$ 8997.6 million in 2023 and is projected to reach US$ 14760 million by 2030, at a CAGR of 8.0% during the forecast period.

Second-hand Semiconductor Equipment Market Overview

This research report provides a comprehensive analysis of the Second-hand Semiconductor Equipment market, focusing on the current trends, market dynamics, and future prospects. The report explores the global Second-hand Semiconductor Equipment market, including major regions such as North America, Europe, Asia-Pacific, and emerging markets. It also examines key factors driving the growth of Second-hand Semiconductor Equipment, challenges faced by the industry, and potential opportunities for market players.

The global Second-hand Semiconductor Equipment market has witnessed rapid growth in recent years, driven by increasing environmental concerns, government incentives, and advancements in technology. The Second-hand Semiconductor Equipment market presents opportunities for various stakeholders, including Used Deposition Equipment, Used Etch Equipment. Collaboration between the private sector and governments can accelerate the development of supportive policies, research and development efforts, and investment in Second-hand Semiconductor Equipment market. Additionally, the growing consumer demand present avenues for market expansion.

Second-hand Semiconductor Equipment Key Market Trends :

- Growing Demand for Used Semiconductor Equipment

Many companies are opting for second-hand semiconductor equipment due to cost-effectiveness and high demand for older technology nodes. - Advancements in Refurbishment Technology

Improved refurbishment techniques are enhancing the performance and reliability of used semiconductor equipment, making them more appealing to buyers. - Rise of Asia-Pacific Market

Countries like China, India, and South Korea are significantly increasing their adoption of second-hand semiconductor equipment due to expanding manufacturing industries. - Sustainability and Circular Economy Initiatives

Environmental concerns and sustainability initiatives are pushing companies to reuse and recycle semiconductor equipment rather than purchasing new ones. - Increased Government Incentives

Governments are offering incentives and tax benefits to encourage the adoption of second-hand semiconductor equipment, boosting market growth.

Second-hand Semiconductor Equipment Market Regional Analysis :

-

North America:

Strong demand driven by EVs, 5G infrastructure, and renewable energy, with the U.S. leading the market.

-

Europe:

Growth fueled by automotive electrification, renewable energy, and strong regulatory support, with Germany as a key player.

-

Asia-Pacific:

Dominates the market due to large-scale manufacturing in China and Japan, with growing demand from EVs, 5G, and semiconductors.

-

South America:

Emerging market, driven by renewable energy and EV adoption, with Brazil leading growth.

-

Middle East & Africa:

Gradual growth, mainly due to investments in renewable energy and EV infrastructure, with Saudi Arabia and UAE as key contributors.

Second-hand Semiconductor Equipment Market Segmentation :

Second-hand Semiconductor Equipment market is split by Type and By Equipment Type. For the period 2019-2030, the growth among segments provides accurate calculations and forecasts for consumption value by Type, and By Equipment Type in terms of value.

Major players covered

- SurplusGLOBAL

- Sumitomo Mitsui Finance and Leasing Company

- Macquarie Semiconductor and Technology

- Conation Technologies,LLC

- Moov Technologies, Inc.

- Genes Tech Group

- EquipNet

- Intel Resale Corporaton

- Hakuto Co., Ltd

- SOS Group

- ASE Semiconductor

- Hightec Systems

- Rihou Shoji Co., Ltd

- AG Semiconductor Services (AGSS)

- PJP TECH

- E-tech Solution

- CIS Corporation

- iGlobal Inc

- Somerset ATE Solutions

- Axus Technology

- Maestech Co., Ltd

- CMTec

- Intertec Sales Corp.

- SDI Fabsurplus

- RS Technologies Co., Ltd.

- Hightec Systems Corporation

- Trust Technology Corporation

- CSE Co., Ltd.

- AG Semiconductor Services, LLC

- TOWA CORPORATION

- ULVAC TECHNO, Ltd.

Market segment by Type

- 300mm Used Equipment

- 200mm Used Equipment

- 150mm and Others

Market segment By Equipment Type

- Used Deposition Equipment

- Used Etch Equipment

- Used Lithography Machines

- Used Ion Implant

- Used Heat Treatment Equipment

- Used CMP Equipment

- Used Metrology and Inspection Equipment

- Used Track Equipment

- Others

Market Drivers

- Cost-Effectiveness

Buying used semiconductor equipment is more affordable compared to new machinery, making it a preferred choice for small and mid-sized manufacturers. - Growing Demand for Semiconductor Chips

The rising demand for chips in automotive, consumer electronics, and AI applications is fueling the need for second-hand semiconductor equipment. - Technological Advancements in Equipment Refurbishment

Enhanced refurbishment techniques are increasing the lifespan and efficiency of used semiconductor equipment, making them a viable alternative.

Market Restraints

- Limited Supply of High-Quality Used Equipment

The availability of well-maintained and high-performance used semiconductor equipment is limited, restricting market growth. - Rapid Technological Obsolescence

Frequent advancements in semiconductor technology make some older equipment models obsolete, reducing their demand. - Regulatory and Compliance Challenges

Different countries have strict regulations regarding the resale and use of second-hand semiconductor equipment, creating barriers for market expansion.

Market Opportunities

- Emerging Markets Expansion

The rising semiconductor demand in emerging markets presents new opportunities for second-hand equipment providers. - Increasing Focus on Sustainable Practices

Companies are investing in circular economy practices, increasing the demand for refurbished semiconductor equipment. - Strategic Partnerships and Collaborations

Collaboration between equipment manufacturers and refurbishment companies can enhance product availability and quality.

Market Challenges

- High Maintenance and Upgradation Costs

Used semiconductor equipment often requires frequent maintenance and upgrades, adding to the total cost of ownership. - Competition from New Equipment Manufacturers

The presence of advanced and affordable new semiconductor equipment poses a challenge for the second-hand market. - Supply Chain Disruptions

Global supply chain issues may affect the availability of used semiconductor equipment and spare parts.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Market?

Which key companies operate in Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/wi-fi-6-chip-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/grating-scale-displacement-sensor-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/golf-gps-tracker-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/sports-wearable-tracking-system-marke

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/refrigerator-camera-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/hologram-mesh-screen-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/custom-capacitor-assemblies-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/active-optical-module-market

https://sites.google.com/view/semiconductorindightreports/home/semiconductor-reports/remote-control-rf-modules-market

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

help@semiconductorinsight.com

FTTX Active Equipment Market: Growth Trends, Opportunities, and Forecast 2025–2032

By SemiconductorinsightPrerana, 2025-09-16

FTTX Active Equipment Market , Trends, Business Strategies 2025-2032

MARKET INSIGHTS

The global FTTX Active Equipment Market size was valued at US$ 4.8 billion in 2024 and is projected to reach US$ 8.2 billion by 2032, at a CAGR of 6.5% during the forecast period 2025-2032.

Download Sample Report https://semiconductorinsight.com/download-sample-report/?product_id=107588

FTTX active equipment refers to critical components in fiber-to-the-x (FTTx) networks that enable high-speed data transmission through optical fibers. These include optical line terminals (OLTs), optical network terminals (ONTs), photoelectric converters, optical receivers, and amplifiers, which collectively manage signal conversion, distribution, and amplification. The increasing demand for bandwidth-intensive applications, such as 4K/8K video streaming, cloud computing, and IoT, is driving significant investments in fiber infrastructure worldwide. While North America and Asia-Pacific dominate deployments, emerging economies are accelerating FTTx adoption to bridge the digital divide. Key players like Huawei, Nokia, and ZTE continue to innovate with energy-efficient and scalable solutions, further propelling market expansion.

MARKET DYNAMICS

The FTTX active equipment market faces growing complexity from competing technology standards and proprietary solutions. While GPON dominates with 76% market share, emerging alternatives like XGS-PON, NG-PON2, and active Ethernet create compatibility challenges for network operators. This fragmentation increases operational costs as service providers must maintain multiple equipment inventories and train personnel on different systems. The lack of universal standards for software-defined access network management further complicates large-scale deployments, forcing operators to make long-term technology commitments that may limit future flexibility.

Climate Considerations Impacting Network Reliability

Extreme weather events are increasingly affecting FTTX network reliability, particularly for outdoor active equipment installations. Temperature fluctuations, humidity, and power surges can significantly impact the performance and lifespan of optical components. Equipment manufacturers are responding with ruggedized designs, but these solutions typically carry 20-30% cost premiums. The growing frequency of climate-related outages is prompting operators to reassess deployment strategies, with some regions now requiring climate-resilient equipment specifications that weren’t necessary a decade ago.

Emerging Markets Present Untapped Growth Potential

Developing economies in Asia, Africa, and Latin America represent significant growth opportunities as governments prioritize digital inclusion initiatives. These regions currently have fiber penetration rates below 15%, compared to over 60% in developed markets, indicating substantial unmet demand. Successful public-private partnership models in countries like India and Brazil demonstrate how cooperative funding approaches can accelerate FTTX deployment. Equipment vendors are adapting products for these markets with cost-optimized designs and simplified maintenance features to address local infrastructure challenges.

Software-Defined Networking Revolutionizing Equipment Capabilities

The integration of SDN/NFV technologies into FTTX equipment creates new value propositions for service providers. Virtualized OLT functions and cloud-based management platforms enable more flexible service delivery and reduced operational expenses. Recent innovations allow network slicing on shared FTTX infrastructure, permitting operators to offer differentiated service levels on the same physical network. This technological evolution is driving a refresh cycle as providers upgrade legacy equipment to support these advanced capabilities, with the virtualized FTTX equipment segment projected to grow at 28% CAGR through 2030.

Edge Computing Driving Demand for Low-Latency FTTX Solutions

The proliferation of edge computing applications is creating specialized requirements for FTTX networks to deliver ultra-low latency connectivity. Emerging use cases in industrial IoT, autonomous vehicles, and augmented reality require sub-5ms latency that can only be achieved through optimized fiber infrastructure. Equipment manufacturers are responding with time-sensitive networking capabilities and precision timing protocols in their FTTX products. This represents a premium market segment where performance rather than cost is the primary purchase driver, enabling higher margins for vendors offering cutting-edge solutions.

List of Key FTTX Active Equipment Manufacturers

- TE Connectivity (Switzerland)

- Amphenol Corporation (U.S.)

- Molex (Koch Industries) (U.S.)

- Fujikura Ltd. (Japan)

- Sumitomo Electric Industries (Japan)

- Coherent Corp. (U.S.)

- Broadcom (Avago Technologies) (U.S.)

- HKT (Hong Kong)

- Zhongtian Technology (China)

- Optisis (South Korea)

- Briticom (U.K.)

Segment Analysis:

By Type

Photoelectric Converter Segment Leads Due to Increasing Fiber Network Deployments

The market is segmented based on type into:

- Photoelectric Converter

- Optical Receiver

- Others

By Application

Commercial Segment Dominates the FTTX Equipment Market

The market is segmented based on application into:

- Residential

- Commercial

By Component