Category: news

PFAS Remediation Services Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2032

By siddheshkapshikar, 2025-08-26

According to a new report from Intel Market Research , the global PFAS Remediation Services market was valued at USD 801.68 million in 2023 and is projected to reach USD 1,633.92 million by 2029 , growing at a CAGR of 12.60% during the forecast period. This growth is fueled by heightened awareness of PFAS-related health risks and growing stringency of environmental regulations worldwide.

What are PFAS Remediation Services?

PFAS Remediation Services refer to specialized environmental solutions designed to remove or neutralize Per- and Polyfluoroalkyl Substances (PFAS) from contaminated sites including soil, groundwater and surface water. These synthetic "forever chemicals" resist environmental degradation and are commonly found in firefighting foams, non-stick cookware, and industrial applications.

The remediation process employs multiple technologies including:

- Activated carbon filtration

- Ion exchange resins

- Advanced oxidation processes

- Thermal destruction methods

Download Sample Report :

PFAS Remediation Services Market - View in Detailed Research Report

Key Market Drivers

1. Regulatory Push for Environmental Safety

The U.S. EPA's PFAS Strategic Roadmap and EU REACH regulations are driving compliance requirements, with over 3,000 contamination sites identified in the U.S. alone as of 2023. These mandates compel industries to invest in cleanup solutions.

2. Growing Litigation and Public Awareness

High-profile cases like the 2017 DuPont settlement ($670 million) have intensified scrutiny, with over 6,000 PFAS-related lawsuits filed globally since 2020. Communities near industrial zones increasingly demand remediation.

3. Military and Industrial Contamination Legacy

Defense departments worldwide face mounting pressure to clean 700+ military sites with historic PFAS use in firefighting foams. The U.S. Department of Defense has allocated $1.1 billion for site investigations through 2024.

Market Challenges

- Technical Complexity: PFAS molecules' stability makes complete destruction challenging

- High Costs: Full-site remediation can exceed $50 million for large industrial facilities

- Emerging Regulations: Evolving standards require adaptable solutions

Innovation Opportunities

Emerging technologies show promise:

- Electrochemical oxidation achieving 99.9% destruction efficiency in pilots

- Supercritical water oxidation demonstrating complete mineralization

- Enhanced bioremediation approaches under development

The Asia-Pacific market presents significant growth potential, with China investing $280 million in environmental remediation projects through its 14th Five-Year Plan.

Regional Market Insights

- North America: 45% market share in 2023 due to robust EPA enforcement

- Europe: Rapid growth from EU's PFAS restriction proposals

- Asia-Pacific: Projected 18% CAGR with industrial expansion and new regulations

Competitive Landscape

Market leaders include:

- Xylem (Evoqua Water Technologies)

- AECOM

- Veolia

- Clean Harbors

- Jacobs Engineering

Recent industry developments:

- April 2024: Veolia's New York treatment facility achieves non-detect PFAS levels

- June 2024: AECOM-Aquatech partnership advances DE-FLUORO™ destruction technology

Get Full Report :

PFAS Remediation Services Market - View in Detailed Research Report

Market Segmentation

By Technology:

- Physical/Chemical Treatment

- Bioremediation

- Thermal Treatment

By Application:

- Groundwater Remediation

- Soil Remediation

- Surface Water Treatment

By End User:

- Industrial

- Municipal

- Defense

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in environmental services , industrial remediation , and regulatory compliance . Our research capabilities include:

- Real-time competitive benchmarking

- Global regulatory change monitoring

- Technology adoption tracking

- Over 500+ specialized reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to navigate complex markets with confidence.

Website : https://www.intelmarketresearch.com

International : +1 (332) 2424 294

LinkedIn : Follow Us

https://sites.google.com/view/intel-market-research/home/dry-mortar-market-growth-2025

https://sites.google.com/view/intel-market-research/home/rotating-tracked-dumper-market-growth-analysis-market-dynamics-2025

https://sites.google.com/view/intel-market-research/home/mobile-robot-lithium-battery-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/mechanical-rubber-tracks-market-growth-analysis-market-dynamics-key-playe?read_current=1

https://sites.google.com/view/intel-market-research/home/burn-in-test-system-for-semiconductor-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/oral-rehydration-solution-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/industrial-microfocus-x-ray-tube-market-2025_1

https://sites.google.com/view/intel-market-research/home/server-liquid-cold-plate-market-2025

https://sites.google.com/view/intel-market-research/home/endpoint-backup-software-market-2025

Global Duty-Free and Travel Retail Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2032

By siddheshkapshikar, 2025-08-26

According to new market research findings, the global Duty-Free and Travel Retail market was valued at USD 68.2 billion in 2024 and is projected to reach USD 108.5 billion by 2032 , growing at a Compound Annual Growth Rate (CAGR) of 6.4% during the forecast period (2024-2032). This expansion is driven by rebounding international travel demand, airport infrastructure development, and growing consumer preference for premium retail experiences in transit hubs.

What is Duty-Free and Travel Retail?

The Duty-Free and Travel Retail sector comprises retail operations exempt from domestic taxes and duties for international travelers. These storefronts operate in airports, cruise terminals, border crossings , and onboard vessels/aircraft, offering products ranging from luxury goods to everyday essentials. Unlike traditional retail, this sector's unique value proposition lies in tax-free pricing, exclusive product lines , and curated shopping experiences tailored to transient customers. Jurisdictional regulations significantly impact merchandise mix - for instance, Singapore's Changi Airport offers broader product categories than most European Union border shops due to differing customs policies.

Key Market Drivers

1. Resurgent Global Travel Demand

Post-pandemic travel recovery continues gaining momentum, with international tourist arrivals reaching 88% of pre-pandemic levels in 2023 according to UNWTO data. Airports Council International reports that major hub airports now handle 10-15% more passengers than 2019 figures, directly increasing potential customer bases for duty-free operators. High disposable income travelers - particularly from China, India, and Middle Eastern countries - spend on average 300-400% more in duty-free shops compared to domestic retail environments.

2. Airport Modernization Wave

Global airport capital expenditures surpassed $128 billion in 2024, with terminal redesigns prioritizing retail space optimization. Notable projects like Dubai's Al Maktoum International expansion dedicate over 35% of terminal space to retail, while Singapore Changi's Terminal 5 blueprint incorporates AI-powered personalized shopping experiences. These developments enable duty-free operators to create immersive brand environments rather than traditional corridor boutiques.

3. Premiumization Trend Acceleration

Luxury goods now account for 41% of global duty-free sales , up from 29% in 2019. Chinese travelers' average duty-free basket value grew 62% year-over-year in 2023 post-border reopening, with cognacs, Swiss watches, and designer accessories leading purchases. Brands like LVMH and Richemont have tripled exclusive product lines for travel retail channels, while beauty conglomerates launch airport-exclusive skincare sets at 30-50% premium to regular retail pricing.

Market Challenges

Despite strong fundamentals, the industry contends with multiple friction points. Customs regulation complexity creates operational headaches - for example, the UK's post-Brexit duty-free revival came with 47 new product category restrictions . Price sensitivity emerged in 2023, with 15-20% of travelers comparing duty-free prices against online retailers mid-purchase. Supply chain volatility persists, particularly for perfumes and cosmetics requiring temperature-controlled logistics from European production hubs.

Emerging Opportunities

Several white spaces offer growth potential for forward-thinking operators. The cruise sector's retail spend per passenger jumped 140% since 2019, creating demand for seaport duty-free concepts . Digital integration presents upside - Lotte Duty Free's app-driven reservation system now captures 29% of Seoul airport sales pre-flight. Emerging markets show promise: India's newly operational 34 airport duty-free zones generated $870 million in 2023, while Africa's Duty Free Africa initiative targets 300% retail footprint expansion by 2027.

Regional Market Analysis

Asia-Pacific dominates with 48% market share , led by South Korea's $12.3 billion travel retail sector and China's resurgent outbound tourism. Regional operators pioneered omnichannel "reserve & collect" systems that now set global standards.

Europe maintains legacy strength through airport retail innovation - Heathrow's new luxury "avenue" concept increased dwell time by 22 minutes per shopper. Schengen Area border shops benefit from cross-border day tripper traffic currently at 125% of pre-pandemic levels.

Middle East hubs leverage transit passenger demographic of 85 million annually. Dubai Duty Free's concierge-style retail approach achieves $2,100 average transaction values from premium cabin travelers.

Americas show diverging trends - while U.S. airports lag in retail innovation, Latin American border retail flourishes with Argentina-Brazil duty-free zones growing at 18% CAGR. Canada's pre-clearance airport stores capture 73% of U.S.-bound travelers' last-minute purchases.

Competitive Landscape

Dufry AG maintains category leadership after merging with Autogrill, operating 2,300 stores across 64 countries. Their 2024 rollout of AI-powered personalized promotions boosted conversion rates by 17%.

Lotte Duty Free dominates Asian travel retail with $7.5 billion annual sales . Their immersive "K-Culture" stores blend retail with K-pop experiences, driving 2.5x longer dwell times versus competitors.

China Duty Free Group captures 62% market share in China's $16 billion duty-free sector. Strategic Hainan Island expansions leverage tax-free island policies attracting mainland shoppers.

Gebr. Heinemann pioneers sustainability initiatives, with 23 carbon-neutral stores and plastic-free packaging across 2,900 SKUs. Their European rail station boutiques outperform airport locations by 31% in sales per sqm .

Product Segmentation

By Category:

Perfumes & Cosmetics (38% market share)

Wines & Spirits (22%)

Luxury Goods (19%)

Tobacco (12%)

Confectionery & Food (9%)

By Channel:

Airports (68%)

Border Stores (18%)

Cruise/Ferries (9%)

Rail Stations (5%)

Report Highlights

This comprehensive analysis provides:

-

2024-2032 market forecasts with COVID-19 impact adjustment models

-

Competitive intelligence on 18 major operators and 200+ brands

-

Emerging technology analysis including AR mirrors and AI assistants

-

Regulatory outlook covering 45 key travel markets

Access Full Research: Global Duty-Free and Travel Retail Market Report 2024-2032

Download Sample: FREE Sample Report with Market Data

About Intel Market Research

Intel Market Research delivers actionable insights in technology and infrastructure markets. Our data-driven analysis leverages:

-

Real-time infrastructure monitoring

-

Techno-economic feasibility studies

Competitive intelligence across 100+ countries

Trusted by Fortune 500 firms, we empower strategic decisions with precision.

International: +1(332) 2424 294 | Asia: +91 9169164321

Website: https://www.intelmarketresearch.com

Follow us on LinkedIn: https://www.linkedin.com/company/intel-market-research

https://sites.google.com/view/intel-market-research/home/dry-mortar-market-growth-2025

https://sites.google.com/view/intel-market-research/home/rotating-tracked-dumper-market-growth-analysis-market-dynamics-2025

https://sites.google.com/view/intel-market-research/home/mobile-robot-lithium-battery-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/mechanical-rubber-tracks-market-growth-analysis-market-dynamics-key-playe?read_current=1

https://sites.google.com/view/intel-market-research/home/burn-in-test-system-for-semiconductor-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/oral-rehydration-solution-market-growth-analysis-2025

Leisure Travel Services Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2032

By siddheshkapshikar, 2025-08-26

According to Intel Market Research 's latest analysis, the global Leisure Travel Services market reached USD 87,490 million in 2023 and is expected to expand to USD 169,148.78 million by 2032 , advancing at a steady CAGR of 7.60% . North America accounted for USD 25,864.31 million of this total in 2023, with projected growth at 6.51% CAGR through 2032. This expansion mirrors consumers' growing appetite for unique experiences and increased disposable incomes worldwide.

Defining Leisure Travel Services

Leisure Travel Services comprise an integrated ecosystem facilitating recreational journeys through comprehensive solutions including itinerary planning, accommodation sourcing, transportation coordination, and guided experiences. Unlike corporate travel, this sector prioritizes personal enrichment, cultural immersion, and relaxation through offerings from:

- Traditional travel agencies adapting to digital transformation

- Tech-first Online Travel Agencies (OTAs) like Expedia and Booking.com

- Specialized tour operators crafting immersive regional experiences

Download FREE Sample Report :

Leisure Travel Services Market - View in Detailed Research Report

Market Growth Catalysts

1. Demographic Shifts Reshaping Demand

The global middle class expansion - particularly across Asia-Pacific - has created 160 million new potential travelers since 2020. Young professionals now allocate 28% of disposable income to travel, favoring authentic local experiences over packaged tours.

2. Digital Disruption Enhancing Accessibility

AI-powered platforms now handle 62% of trip planning activities, with chatbots resolving 89% of customer inquiries without human intervention. Mobile adoption enables real-time booking adjustments during trips, increasing satisfaction rates.

3. Experience Economy Taking Priority

73% of travelers under 40 now prioritize meaningful interactions with local cultures over traditional sightseeing. This has spurred growth in:

- Culinary tourism programs

- Adventure travel packages

- Volunteer-based itineraries

Industry Challenges

While the sector shows strong growth potential, operators face several headwinds:

- Geopolitical tensions have caused 22% of travelers to reconsider international destinations

- OTA commission structures compress operator margins to 8-12% on average

- Climate change concerns prompt 41% of European travelers to reevaluate flight frequency

Emerging Opportunities

Forward-looking operators are capitalizing on several transformative trends:

Sustainability Integration

Copenhagen's certification program for eco-conscious hotels saw 300% adoption growth since 2021, demonstrating market appetite for verified green options.

Technology Convergence

Augmented reality now enhances 19% of major attraction experiences, with the Vatican Museums' VR tours increasing off-season attendance by 37%.

Niche Market Development

"Bleisure" travel (combining business and leisure) now accounts for 42% of extended corporate trips, creating premium extension service opportunities.

Geographic Market Analysis

| Region | Key Characteristics | Growth Factors |

|---|---|---|

| North America | Dominance of tech-savvy OTAs | Rebound of international travel post-pandemic |

| Europe | High cultural tourism demand | Schengen visa reforms attracting long-haul visitors |

| Asia-Pacific | Explosive outbound market growth | Rising affluence in secondary Chinese cities |

Service Innovation Spotlight

Leading providers are redefining leisure travel through:

- Dynamic Packaging: Delta Vacations' AI-driven bundling tool increases ancillary revenue by 29%

- Personalized Curation: Abercrombie & Kent's concierge app achieves 92% customer satisfaction

- Seamless Integration: Airbnb's Experiences platform now books 3 million activities monthly

Get Full Report Here :

Leisure Travel Services Market - View in Detailed Research Report

Competitive Landscape

The market features several strategic groupings:

- Global Powerhouses: Expedia Group, Booking Holdings

- Regional Specialists: Traveloka (SE Asia), WeChat Travel (China)

- Experience Curators: Black Tomato, GeoEx

Market Segmentation

By Travel Type

- Solo Adventurer Packages

- Family Vacation Solutions

- Multi-Generational Itineraries

By Service Level

- Budget-Conscious Offerings

- Premium Concierge Services

- Ultra-Luxury Experiences

Future Outlook

The sector's evolution will likely focus on:

- Blockchain adoption for secure credential sharing

- Predictive analytics for hyper-personalization

- Carbon-neutral certification programs

Download FREE Sample Report :

Leisure Travel Services Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology , pharmaceuticals , and healthcare infrastructure . Our research capabilities include:

- Real-time competitive benchmarking

- Global clinical trial pipeline monitoring

- Country-specific regulatory and pricing analysis

- Over 500+ healthcare reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website : https://www.intelmarketresearch.com International : +1 (332) 2424 294

Asia-Pacific : +91 9169164321

LinkedIn : Follow Us

PCD Cutting Tools Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2031

By siddheshkapshikar, 2025-08-26

According to the latest industry analysis by Intel Market Research , the global PCD Cutting Tools market reached a valuation of US$ 971 million in 2023 with strong projections indicating growth to US$ 1,320 million by 2030 , expanding at a steady CAGR of 5.1% from 2024-2030. This upward trajectory reflects intensifying demand across precision manufacturing sectors and technological advancements reshaping modern machining capabilities.

Download FREE Sample Report :

PCD Cutting Tools Market - View in Detailed Research Report

The PCD Cutting Tool Advantage

Polycrystalline Diamond cutting tools represent the pinnacle of machining technology, combining engineered diamond particles with metal binders to create instruments that outperform traditional carbide tools by 5-10 times in lifespan while delivering superior surface finishes. Their unique properties stem from diamond's exceptional hardness and thermal conductivity, making them indispensable for:

- High-speed machining of non-ferrous materials

- Precision components requiring tight tolerances

- Difficult-to-machine composites and alloys

Market Growth Catalysts

1. The Lightweighting Revolution in Automotive & Aerospace

The automotive sector's shift toward aluminum engine blocks (representing over 60% of new models ) and aerospace's adoption of titanium aluminide components has created unprecedented demand for PCD tooling solutions. Major automakers now utilize these tools for:

- Engine block machining

- Transmission components

- E-motor housings

2. Semiconductor Industry Expansion

With the global semiconductor market projected to reach $1 trillion by 2030, PCD tools have become critical for machining:

- Silicon wafer handling components

- Precision ceramic substrates

- Optical mold surfaces

3. Industry 4.0 Integration

The fusion of IoT-enabled PCD tools with smart manufacturing systems allows real-time monitoring of tool wear, with leading manufacturers reporting 30-40% reductions in unplanned downtime through predictive maintenance implementations.

Market Challenges

While demand grows, several factors currently limit market penetration:

- Ferrous material limitations - Chemical reactions with iron restrict steel machining applications

- Entry barriers - High initial tool costs and required machine tool rigidity create adoption hurdles for SMEs

- Skill gaps - Specialized training needed for optimal PCD tool application

These constraints explain why carbide tools still maintain 68% market share in metal cutting applications despite PCD's superior performance characteristics in compatible materials.

Emerging Opportunities

The market presents attractive opportunities through:

- Niche material applications - Growing use of carbon fiber composites in wind energy

- Hybrid tool development - Combining PCD with other superhard materials

- Custom tool geometries - Meeting complex machining requirements

Leading tool manufacturers are expanding their custom engineering teams to capitalize on these specialized applications.

Regional Market Analysis

Market dynamics vary significantly by geography:

- Asia-Pacific : Commands 42% market share led by China's manufacturing expansion and Japan's leadership in precision tooling

- North America : Aerospace and defense sectors drive premium tool demand with strict quality requirements

- Europe : Strong automotive presence supports adoption, particularly in Germany's high-end vehicle production

Technological Innovations

Recent advances include:

- Nano-grained PCD - For ultra-fine finish requirements

- Functionally graded tools - Custom material properties by tool zone

- 3D printed PCD tool blanks - Enabling complex geometries

Competitive Landscape

The market features a mix of established players and specialist manufacturers:

| Company | Specialization | Recent Developments |

|---|---|---|

| Element Six (De Beers Group) | Advanced PCD materials | New diamond bonding technology |

| Sandvik Coromant | Complete machining solutions | Expanded PCD insert line |

| Sumitomo Electric | Specialized tool geometries | New micro-tool offerings |

Get Full Report Here :

PCD Cutting Tools Market - View in Detailed Research Report

Market Segmentation

By Tool Type

- Milling tools

- Turning tools

- Drilling tools

- Grooving tools

By Application Sector

- Automotive

- Aerospace

- Electronics

- Energy

Frequently Asked Questions

1. What makes PCD tools superior to carbide for certain applications?

PCD tools provide significantly longer tool life and better surface finishes when machining non-ferrous metals, composites, and other abrasive materials, though they cost 3-5x more initially.

2. Which industries drive the most PCD tool demand?

The automotive and aerospace sectors combined account for over 60% of current PCD tool consumption.

3. How are manufacturers addressing the high cost of PCD tools?

Through tool life extension programs, improved regeneration services, and design optimizations that reduce material requirements.

Get Full Report Here :

PCD Cutting Tools Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in manufacturing technology , industrial equipment , and advanced materials . Our research capabilities include:

- Plant-level production analysis

- Technology adoption tracking

- Supply chain evaluation

- Over 200+ industrial reports annually

Trusted by Fortune 500 manufacturers, our insights help optimize production strategies and technology investments.

Website : https://www.intelmarketresearch.com International : +1 (332) 2424 294

Asia-Pacific : +91 9169164321

LinkedIn : Follow Us

https://sites.google.com/view/intel-market-research/home/fish-counters-market-growth-analysis-market-dynamic-2025

https://sites.google.com/view/intel-market-research/home/travel-esim-market-growth-analysis-market-dynamics-2025

https://sites.google.com/d/1FmIQXbPYxpXHWg8EhgH39IzQaZD-THYX/p/1tiaBv8RsqnH94NPgJpuvUJH-AOzJH3sY/edit

https://sites.google.com/view/intel-market-research/home/test-handler-market-growth-analysis-market-dynamics-key-players-2025

https://sites.google.com/view/intel-market-research/home/smd-thermistor-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/euv-photoresists-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/shower-wall-panel-market-2025

https://sites.google.com/view/intel-market-research/home/kilowatt-fiber-laser-market-growth-analysis-market-dynamics-2025

Mass Flow Controller (MFC) for Semiconductor Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2031

By siddheshkapshikar, 2025-08-26

A mass flow controller (MFC) is a precision device used to measure and control the flow rate of gases in various semiconductor fabrication processes. These devices employ technologies such as thermal mass flow, differential pressure, or Coriolis flow measurement to ensure accuracy and reliability. MFCs are critical components in semiconductor manufacturing as they regulate the precise flow of gases in processes like chemical vapor deposition (CVD), etching, and plasma-enhanced applications. Typically integrated into gas delivery systems, they are operable through digital or analog signals, enabling high precision in maintaining process integrity.

https://www.intelmarketresearch.com/manufacturing-and-construction/527/mass-flow-controller-mfc-semiconductor-market

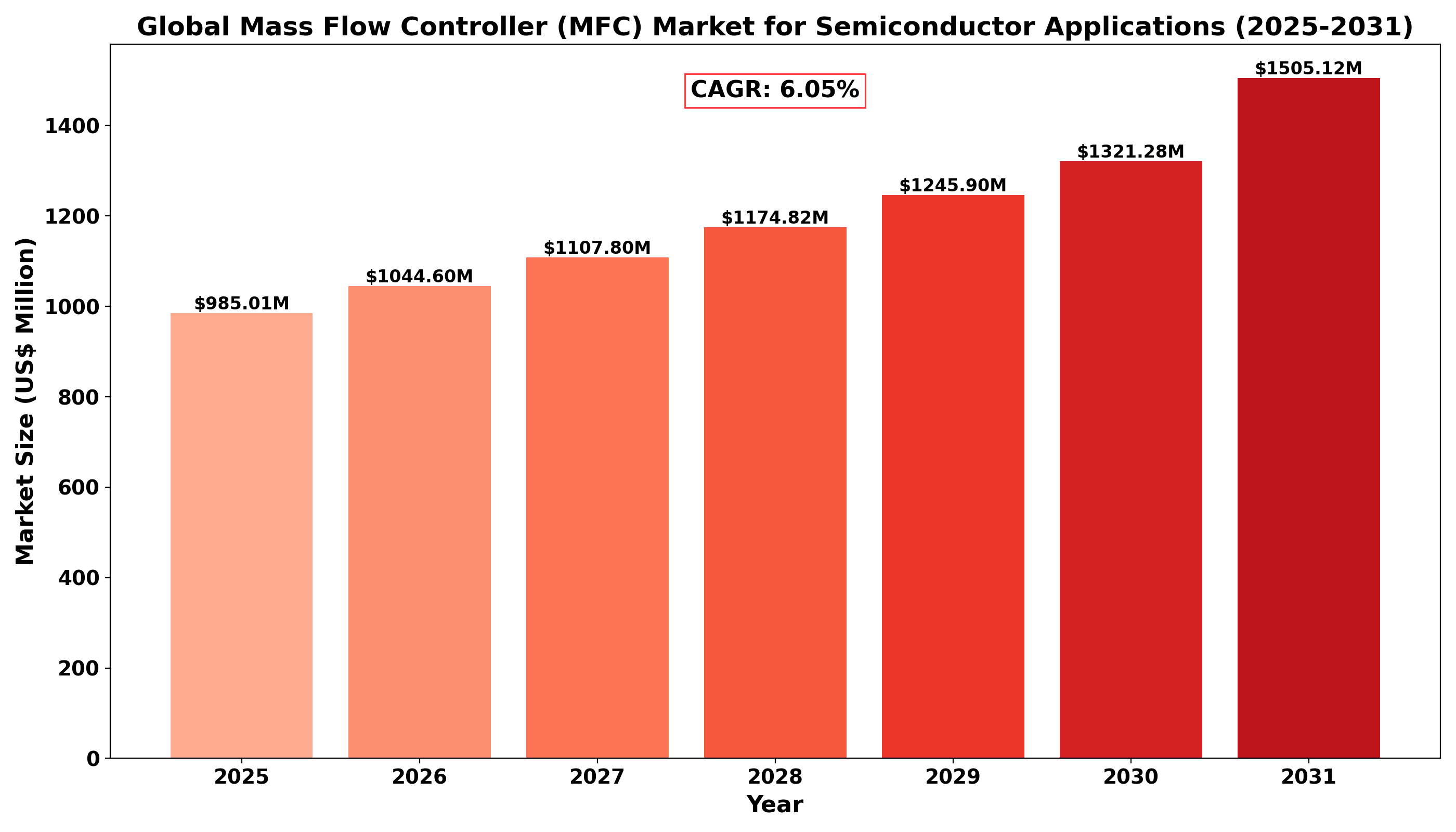

Market Size

The global market for Mass Flow Controller (MFC) for Semiconductor applications was valued at approximately USD 985.01 million in 2024. It is projected to reach USD 1,505.12 million by 2031, growing at a compound annual growth rate (CAGR) of 6.05% during the forecast period from 2025 to 2031. This growth is attributed to the expanding semiconductor industry, technological advancements in fabrication processes, and increasing demand for high-performance electronic devices. Historically, the market has shown a consistent upward trend due to advancements in miniaturization and integration in semiconductor devices, further driving the need for precise gas flow control solutions.

Market Dynamics (Drivers, Restraints, Opportunities, and Challenges)

Drivers:

-

Rising Semiconductor Demand: The growing adoption of smart devices, IoT, and advanced computing solutions is fueling demand for semiconductors, consequently boosting the MFC market.

-

Technological Advancements: Innovations in MFC technologies, such as enhanced thermal mass flow meters and digital communication capabilities, are driving market growth.

-

Stringent Process Requirements: The increasing complexity of semiconductor manufacturing processes requires high-precision gas delivery systems, where MFCs play a pivotal role.

Restraints:

-

High Initial Investment: The cost of deploying advanced MFCs can be prohibitive for small and medium-sized semiconductor manufacturers.

-

Maintenance and Calibration Needs: Frequent calibration to maintain accuracy can add to operational costs and downtime.

Opportunities:

- Emerging Markets: Rapid industrialization in Asia-Pacific countries like China, India, and Vietnam presents significant opportunities for MFC manufacturers.

- Sustainable Manufacturing: The integration of energy-efficient and eco-friendly MFCs in semiconductor processes aligns with global sustainability goals, creating new market prospects.

Challenges:

-

Technological Barriers: Developing MFCs with higher precision, durability, and adaptability to diverse gases remains a technical challenge.

-

Supply Chain Issues: Fluctuations in raw material availability and geopolitical factors can disrupt the supply chain.

Regional Analysis

- North America: The North American region remains a significant market for MFCs, driven by advancements in semiconductor technology and robust investments in R&D. The U.S., in particular, is a major contributor, hosting key players and a well-established semiconductor manufacturing base.

- Asia-Pacific: Asia-Pacific dominates the global MFC market, with countries like China, South Korea, and Japan leading due to their extensive semiconductor manufacturing industries. China’s rapid industrialization and government incentives further bolster market growth.

- Europe: Europe’s market is primarily driven by innovation in semiconductor processes and the presence of high-tech industries. Germany, France, and the Netherlands are key contributors to the region’s market share.

- Rest of the World: Regions such as Latin America and the Middle East & Africa are emerging markets, gradually adopting advanced semiconductor technologies and investing in infrastructure development.

Competitor Analysis

The Mass Flow Controller (MFC) for Semiconductor market is characterized by a high degree of competition among prominent players. In 2024, the top three companies—HORIBA, Fujikin, and MKS Instruments—accounted for approximately 80.54% of the market revenue. These companies focus on technological advancements, strategic partnerships, and mergers and acquisitions to maintain their competitive edge. Other key players include:

-

Beijing Aurasky

-

Hitachi Metals, Ltd

-

Pivotal Systems

-

MKP

-

AZBIL

-

Bronkhorst

-

Lintec

Global Mass Flow Controller (MFC) For Semiconductor: Market Segmentation Analysis

This report provides a deep insight into the global Mass Flow Controller (MFC) for Semiconductor market, covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trends, niche market, key market drivers and challenges, SWOT analysis, and value chain analysis.

The analysis helps readers shape competition strategies, enhance potential profit, and evaluate the position of their businesses in the competitive environment. Furthermore, it introduces in detail the market share, market performance, product situation, operation situation, etc., of the main players, aiding stakeholders in deeply understanding the competition pattern of the market.

Market Segmentation (by Application)

-

Semiconductor Processing Furnace

-

PVD & CVD Equipment

-

Etching Equipment

-

Others

Market Segmentation (by Type)

-

Thermal Type

-

Pressure Type

Key Company

The following companies are leading players in the global Mass Flow Controller (MFC) for Semiconductor market:

-

HORIBA

-

Fujikin

-

MKS Instruments

-

Beijing Aurasky

-

Hitachi Metals, Ltd

-

Pivotal Systems

-

MKP

-

AZBIL

-

Bronkhorst

-

Lintec

Geographic Segmentation

-

North America: U.S., Canada, Mexico

-

Asia-Pacific: China, Japan, South Korea, Southeast Asia, India

-

Europe: Germany, France, U.K., Italy, Benelux, Rest of Europe

-

South America, Middle East & Africa: Brazil, Middle East, Africa

FAQ

What is the current market size of the Mass Flow Controller (MFC) for Semiconductor market?

▶ The market was valued at USD 985.01 million in 2024 and is expected to reach USD 1,505.12 million by 2031.

Which are the key companies operating in the Mass Flow Controller (MFC) for Semiconductor market?

▶ Key players include HORIBA, Fujikin, MKS Instruments, Beijing Aurasky, and Hitachi Metals, Ltd, among others.

What are the key growth drivers in the Mass Flow Controller (MFC) for Semiconductor market?

▶ Rising demand for semiconductors, advancements in MFC technologies, and stringent process requirements drive market growth.

Which regions dominate the Mass Flow Controller (MFC) for Semiconductor market?

▶ Asia-Pacific leads the market, followed by North America and Europe.

What are the emerging trends in the Mass Flow Controller (MFC) for Semiconductor market?

▶ Trends include the adoption of eco-friendly MFCs, integration of IoT for better control, and advancements in miniaturization technology.

https://www.intelmarketresearch.com/download-free-sample/527/mass-flow-controller-mfc-semiconductor-market

https://sites.google.com/view/intel-market-research/home/fish-counters-market-growth-analysis-market-dynamic-2025

https://sites.google.com/view/intel-market-research/home/travel-esim-market-growth-analysis-market-dynamics-2025

https://sites.google.com/d/1FmIQXbPYxpXHWg8EhgH39IzQaZD-THYX/p/1tiaBv8RsqnH94NPgJpuvUJH-AOzJH3sY/edit

https://sites.google.com/view/intel-market-research/home/test-handler-market-growth-analysis-market-dynamics-key-players-2025

https://sites.google.com/view/intel-market-research/home/smd-thermistor-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/euv-photoresists-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/shower-wall-panel-market-2025

https://sites.google.com/view/intel-market-research/home/kilowatt-fiber-laser-market-growth-analysis-market-dynamics-2025

https://sites.google.com/view/intel-market-research/home/industrial-shredder-market-growth-analysis-market-dynamics-2025

Dry Mortar Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2031

By siddheshkapshikar, 2025-08-25

According to recent market analysis, the global Dry Mortar market was valued at US$ 53,824 million in 2023 and is projected to reach US$ 81,536 million by 2030 , growing at a Compound Annual Growth Rate (CAGR) of 6.30% during the forecast period (2024-2030). This growth trajectory stems from rapid urbanization, infrastructure development, and superior functional benefits over traditional wet-mix mortar systems.

What is Dry Mortar?

Dry mortar represents a revolutionary advancement in construction materials - a factory-prepared blend of cement, sand, mineral additives and polymers that only requires water addition on-site. Engineered for specific applications like masonry, tiling and plastering, these pre-mixed formulations deliver consistent quality, reduced waste and labor savings compared to conventional site-mixed mortars. Major types include tile adhesives, waterproofing compounds, self-leveling underlayments and thermal insulation products.

Key Market Drivers

1. Construction Industry Boom

Global construction output is projected to grow by 42% to $15.2 trillion by 2030 (Global Construction Perspectives). This creates massive demand for time-saving building materials like dry mortar that can accelerate project timelines while maintaining structural integrity.

2. Sustainability Imperatives

With the construction sector accounting for 36% of global energy use (UNEP), dry mortar's precise mix ratios reduce material waste by up to 30% compared to traditional methods. Its reduced water usage and CO₂ emissions align with green building certifications like LEED and BREEAM.

Market Challenges

Despite advantages, higher upfront costs (15-20% premium over wet mixes) and limited technical expertise in developing regions slow adoption. Transportation costs for bagged products also impact competitiveness beyond 300km from production facilities.

Opportunities Ahead

The emergence of specialty formulations (epoxy-modified mortars, rapid-setting repair compounds) commands premium pricing. Meanwhile, automated dispensing systems integrated with BIM platforms represent the next efficiency frontier for commercial construction.

Regional Market Insights

-

Asia-Pacific (58% market share): China's infrastructure push and India's housing shortage ( 29 million unit deficit ) drive consumption

-

Europe (22% share): Strict building codes and renovation wave ( 35 million buildings needing retrofit ) sustain demand

-

North America (13% share): Commercial construction recovery and disaster resilience projects fuel growth

Competitive Landscape

The market features both global chemical specialists and regional manufacturers:

-

Sika AG : Technology leader in polymer-modified formulations

-

Saint-Gobain Weber : Strong position in masonry and tile adhesives

-

Mapei : Innovator in decorative finishes and restoration products

Recent developments include BASF's 2023 launch of MasterProtect 8000 antimicrobial tile adhesive for healthcare facilities.

Market Segmentation

By Application:

- Tile Adhesives & Grouts

- Wall Renders & Plasters

- Floor Screeds

- Masonry Mortars

- Waterproofing Compounds

By End-Use Sector:

- Residential Construction

- Commercial Construction

- Infrastructure

- Repair & Maintenance

Report Scope & Offerings

This comprehensive analysis provides:

- Granular 2024-2030 market forecasts by product and region

- Competitive benchmarking of 15+ manufacturers

- SWOT and value chain analysis

- Emerging technology assessment

Access Full Report: Dry Mortar Market - Comprehensive Research

Download Sample: Free Market Analysis Excerpt

About Intel Market Research

Intel Market Research delivers actionable insights in technology and infrastructure markets. Our data-driven analysis leverages:

- Real-time infrastructure monitoring

- Techno-economic feasibility studies

Competitive intelligence across 100+ countries

Trusted by Fortune 500 firms, we empower strategic decisions with precision.

International: +1(332) 2424 294 | Asia: +91 9169164321

Website: https://www.intelmarketresearch.com

Follow us on LinkedIn: https://www.linkedin.com/company/intel-market-research

https://sites.google.com/view/intel-market-research/home/fish-counters-market-growth-analysis-market-dynamic-2025

https://sites.google.com/d/1FmIQXbPYxpXHWg8EhgH39IzQaZD-THYX/p/1tiaBv8RsqnH94NPgJpuvUJH-AOzJH3sY/edit

https://sites.google.com/view/intel-market-research/home/test-handler-market-growth-analysis-market-dynamics-key-players-2025

According to new market research, the global Rotating Tracked Dumper market was valued at USD 204.38 million in 2023 and is projected to reach USD 318.29 million by 2030 , expanding at a Compound Annual Growth Rate (CAGR) of 6.53% during the forecast period (2024-2030). This growth trajectory reflects increasing infrastructure development projects globally and the rising demand for efficient material handling equipment in construction, mining, and agriculture sectors.

What is a Rotating Tracked Dumper?

A rotating tracked dumper represents a significant advancement over traditional wheeled dump trucks, featuring continuous tracks for superior traction on challenging terrain and a 180-degree rotating dump bed for precise material placement. These specialized vehicles excel in environments where conventional dump trucks struggle—steep slopes, muddy conditions, or confined workspaces. Their tracks distribute weight evenly , preventing sinkage on soft ground while enabling access to areas inaccessible to wheeled vehicles.

The rotating mechanism provides unparalleled flexibility, allowing operators to dump loads sideways or backward without repositioning the machine—a critical advantage in tight urban construction sites or underground mining operations. Major manufacturers like Morooka and Prinoth have incorporated advanced hydraulic systems and ergonomic controls to enhance operator efficiency.

Key Market Drivers

1. Global Infrastructure Expansion

Construction booms in emerging economies and infrastructure renewal programs in developed nations are creating unprecedented demand. The U.S. Infrastructure Investment and Jobs Act ( $1.2 trillion allocation ) and China's Belt and Road Initiative are driving adoption across multiple regions. These machines prove indispensable for:

- Bridge construction in difficult terrain

- Highway projects with limited workspace

- Tunnel excavation where maneuvering space is constrained

2. Mining Sector Modernization

With underground mining operations expanding to meet metal demand for electrification, rotating tracked dumpers are replacing traditional haulage methods. Their zero-tail-swing designs and explosion-proof variants make them ideal for confined underground environments. The global mining equipment market's projected 7.2% annual growth directly benefits specialized dumper manufacturers.

Market Challenges

While demand grows steadily, several factors constrain faster market expansion:

| Challenge | Impact | Industry Response |

| High acquisition costs ( $150,000-$300,000 per unit) | Limits adoption among small contractors | Leasing programs and financing options |

| Technical complexity | Requires specialized operator training | VR simulation training solutions |

| Supply chain disruptions | Lead time extensions up to 6 months | Localized component manufacturing |

Opportunities Ahead

Manufacturers are capitalizing on several emerging trends:

Technological Convergence

Integration of telematics systems allows real-time monitoring of:

- Engine performance

- Fuel efficiency

- Preventive maintenance alerts

Autonomous operation prototypes are being tested in controlled mining environments.

Sustainable Solutions

Electric and hybrid models address:

- Stringent emissions regulations

- Underground air quality requirements

- Corporate sustainability targets

Yanmar recently demonstrated a hydrogen-fuel-cell powered prototype with zero emissions.

Regional Market Insights

-

Asia-Pacific dominates with 42% market share , driven by Japan's manufacturing leadership and China's infrastructure projects. Key growth markets include India's smart cities initiative and Southeast Asian urban development.

-

North America shows strongest growth in mining applications, particularly in Canadian oil sands and U.S. copper mining expansions. Strict emissions standards accelerate equipment modernization.

-

Europe's mature market focuses on replacement cycles and sustainable equipment. German engineering firms lead in precision control systems for specialized applications.

-

Latin America and Africa present untapped potential, with mining concessions driving demand. Local assembly facilities are being established to circumvent import barriers.

Competitive Landscape

The market features strong competition among established players:

-

Morooka maintains technology leadership with patented track systems and dominates the >10-ton capacity segment

-

Prinoth excels in forestry applications with armored undercarriages and biomass handling configurations

-

Yanmar focuses on compact urban construction models with advanced noise reduction

-

Regional players like Canycom and Messersi compete through distribution networks and localized service

Recent developments include Takeuchi's strategic partnership with a major construction firm to develop autonomous dumpers for high-risk environments.

Market Segmentation

By Application:

-

Construction

-

Mining

-

Agriculture

-

Forestry

-

Specialty Applications

By Capacity:

-

Light Duty (<5T)

-

Medium Duty (5-10T)

-

Heavy Duty (>10T)

Report Scope & Offerings

This comprehensive analysis provides:

-

Market size projections through 2030 with COVID-19 impact assessment

-

Competitive intelligence on 8 major players and 12 emerging competitors

-

Technology trend analysis including automation and electrification

-

Regional demand forecasts with regulatory impact assessments

Access Full Market Study: Comprehensive Rotating Tracked Dumper Market Analysis

https://sites.google.com/view/intel-market-research/home/fish-counters-market-growth-analysis-market-dynamic-2025

https://sites.google.com/view/intel-market-research/home/travel-esim-market-growth-analysis-market-dynamics-2025

https://sites.google.com/d/1FmIQXbPYxpXHWg8EhgH39IzQaZD-THYX/p/1tiaBv8RsqnH94NPgJpuvUJH-AOzJH3sY/edit

https://sites.google.com/view/intel-market-research/home/test-handler-market-growth-analysis-market-dynamics-key-players-2025

https://sites.google.com/view/intel-market-research/home/smd-thermistor-market-growth-analysis-2025

Industrial Microfocus X-ray Tube Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2031

By siddheshkapshikar, 2025-08-25

According to a new report from Intel Market Research , the global Industrial Microfocus X-ray Tube market was valued at US$ 92.57 million in 2023 and is projected to reach US$ 133.46 million by 2030 , growing at a CAGR of 5.41% during the forecast period (2024-2030). This growth is driven by increasing demand for precise non-destructive testing and quality control across multiple industrial sectors.

What are Industrial Microfocus X-ray Tubes?

Industrial Microfocus X-ray Tubes are specialized radiation sources that generate highly focused X-ray beams with spot sizes typically between 1-50 microns. These precision instruments enable high-resolution imaging for applications requiring micron-level detail, such as semiconductor inspection, aerospace component analysis, and materials research. Unlike conventional X-ray tubes, microfocus variants provide superior image sharpness by concentrating electron beams onto extremely small focal points.

The technology has become indispensable for modern industrial quality assurance, with major manufacturers like Oxford Instruments and Hamamatsu Photonics leading innovation in tube design. In 2023, the top five vendors accounted for over 56% of global revenue, reflecting the concentrated nature of this specialized market.

Download Sample Report:

Industrial Microfocus X-ray Tube Market - View in Detailed Research Report

Key Market Drivers

1. Expanding Adoption in Electronics Manufacturing

The semiconductor and electronics sector has emerged as the largest application area, accounting for over 35% of market share. As chip geometries shrink below 7nm, manufacturers increasingly rely on microfocus X-ray systems for:

- PCB inspection: Detecting micro-cracks and solder joint defects

- Chip packaging analysis: Verifying wire bonding and interconnects

- Wafer-level testing: Identifying subsurface defects in silicon wafers

2. Regulatory Pressure for Quality Assurance

Stringent quality requirements in aerospace, medical devices, and automotive sectors are driving adoption. For instance, the FAA mandates X-ray inspection for critical aircraft components, while automotive EV battery manufacturers use microfocus systems to examine lithium-ion cell integrity. These regulatory drivers create sustained demand across multiple industries.

3. Advancements in Tube Technology

Recent innovations include:

- High-power microfocus tubes (up to 300kV) for dense materials

- Rotating anode designs that extend tube lifespan by 40-50%

- Compact tubes enabling portable inspection systems

Market Challenges

The market faces several barriers to growth:

- High equipment costs: Complete microfocus X-ray systems can exceed $500,000 , limiting adoption among SMEs

- Radiation safety compliance: Requires specialized facilities and trained personnel

- Competition from alternative methods: Ultrasonic and CT scanning offer alternatives for some applications

Emerging Opportunities

The market presents significant growth potential through:

1. Additive Manufacturing Quality Control

3D printed metal components require thorough internal inspection - an application perfectly suited for microfocus X-ray capabilities. Major aerospace firms are already implementing these systems for additively manufactured turbine blades and structural components.

2. EV Battery Inspection

Electric vehicle manufacturers are adopting microfocus X-ray to examine:

- Electrode alignment

- Separator integrity

- Welding quality in battery packs

3. Emerging Markets Expansion

Countries like China, India and Brazil are investing heavily in domestic manufacturing capabilities, creating new demand for quality inspection technologies. Local partnerships and distribution networks will be key to capturing this growth.

Download Sample Report:

Industrial Microfocus X-ray Tube Market - View in Detailed Research Report

Regional Market Insights

- North America: Dominates with 38% market share, driven by aerospace and semiconductor industries

- Europe: Strong in automotive and industrial manufacturing applications

- Asia-Pacific: Fastest growing region due to electronics production expansion

- Rest of World: Emerging opportunities in energy and infrastructure sectors

Market Segmentation

By Type

- Sealed Tube

- Open Tube

By Application

- Electronics

- Automotive

- Aerospace & Defense

- Energy

- Industrial Manufacturing

- Others

By End User

- Manufacturing Facilities

- Research Institutions

- Service Providers

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Get Full Report Here:

Industrial Microfocus X-ray Tube Market - View in Detailed Research Report

Competitive Landscape

The market features a mix of established players and specialized innovators:

- Oxford Instruments

- Hamamatsu Photonics

- Nikon Metrology

- Bruker Corporation

- Comet Group

- Rigaku Corporation

- Excillum AB

Recent developments include Nikon's acquisition of X-Tek Systems and Hamamatsu's launch of a new 200kV microfocus tube for industrial CT applications.

Report Deliverables

- Market size and forecasts through 2030

- Application and end-user analysis

- Competitive benchmarking

- Technology trend analysis

- Regional market assessments

Get Full Report Here:

Industrial Microfocus X-ray Tube Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in industrial technologies , manufacturing , and advanced materials . Our research capabilities include:

- Real-time competitive benchmarking

- Technology adoption tracking

- Market sizing and forecasting

- Over 500 industrial reports annually

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website: https://www.intelmarketresearch.com

International: +1 (332) 2424 294

Asia-Pacific: +91 9169164321

LinkedIn: Follow Us

https://sites.google.com/view/intel-market-research/home/fish-counters-market-growth-analysis-market-dynamic-2025

https://sites.google.com/view/intel-market-research/home/travel-esim-market-growth-analysis-market-dynamics-2025

https://sites.google.com/d/1FmIQXbPYxpXHWg8EhgH39IzQaZD-THYX/p/1tiaBv8RsqnH94NPgJpuvUJH-AOzJH3sY/edit

https://sites.google.com/view/intel-market-research/home/test-handler-market-growth-analysis-market-dynamics-key-players-2025

https://sites.google.com/view/intel-market-research/home/smd-thermistor-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/euv-photoresists-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/shower-wall-panel-market-2025

Endpoint Backup Software Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2031

By siddheshkapshikar, 2025-08-25

According to a comprehensive market analysis, the global Endpoint Backup Software market was valued at US$ 2.94 billion in 2023 and is projected to reach US$ 5.60 billion by 2030 , growing at a Compound Annual Growth Rate (CAGR) of 8.83% during the forecast period (2024-2030). This growth trajectory reflects the escalating need for robust data protection solutions amidst rising cybersecurity threats and increasing enterprise digital transformation initiatives.

What is Endpoint Backup Software?

Endpoint Backup Software represents a specialized category of data protection solutions designed specifically for securing information on endpoint devices like laptops, desktops, mobile phones, and tablets . These solutions address critical vulnerabilities from hardware failures, malware attacks, accidental deletions, and ransomware incidents . Modern solutions feature automated backup scheduling, cloud integration, version control, and military-grade encryption to ensure data integrity and availability across distributed work environments.

Key Market Drivers

1. Escalating Cybersecurity Threats

The dramatic increase in sophisticated cyberattacks, particularly ransomware targeting endpoints, has become a primary growth driver. Recent analyses show that 68% of organizations experienced endpoint attacks in 2023, with average ransomware payments exceeding $1.5 million. Endpoint backup solutions mitigate these risks by enabling rapid data restoration without paying ransoms.

2. Remote Workforce Expansion

The global shift to hybrid work models has expanded the attack surface, with 87% of enterprises now allowing employees to work remotely at least partially. This paradigm shift necessitates reliable endpoint backup solutions to protect data across geographically dispersed devices while maintaining compliance with data protection regulations.

Market Challenges

The market faces significant headwinds including high implementation costs for SMEs and integration complexities with legacy systems . Additionally, challenges persist in regions with inadequate IT infrastructure, where limited bandwidth and unstable connectivity hinder cloud-based backup operations. Data sovereignty laws in some jurisdictions further complicate deployment strategies for multinational corporations.

Opportunities Ahead

Emerging markets in Asia-Pacific and Latin America present substantial growth potential as digital transformation accelerates. The integration of AI-driven predictive analytics enhances backup efficiency by anticipating failures before they occur. Furthermore, the rise of hybrid backup architectures combining on-premises control with cloud scalability offers vendors significant product differentiation opportunities.

Regional Market Insights

-

North America dominates with 42% market share, driven by stringent compliance requirements and high cybersecurity spending. The region's early adoption of advanced technologies and prevalence of remote work contribute to its leadership position.

-

Europe follows closely, with GDPR compliance acting as a major adoption driver. The region shows particular strength in cloud-based backup solutions adopted by financial services and healthcare sectors.

-

Asia-Pacific emerges as the fastest-growing region, with projected 11.2% CAGR through 2030. Rapid digitization in India, China, and Southeast Asian nations fuels demand for cost-effective endpoint protection solutions.

Competitive Landscape

-

Dell Technologies and Veeam collectively hold over 25% market share, leveraging their established enterprise IT ecosystems and comprehensive data protection suites.

-

Acronis and Commvault differentiate through AI-powered ransomware detection and blockchain-based verification capabilities in their endpoint solutions.

-

Emerging players like Druva and Backblaze are gaining traction with cloud-native platforms offering streamlined deployment and pay-as-you-go pricing models attractive to SMBs.

Market Segmentation

By Type:

- Cloud-based

- On-premises

By Application:

- SME

- Large Enterprise

By End User:

- Healthcare

- BFSI

- IT & Telecom

- Government

- Education

By Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Report Scope & Offerings

This comprehensive industry report provides:

- Market size projections through 2030 with historical data from 2019

- Competitive analysis of 16 key vendors including market share benchmarks

- SWOT analysis and regulatory impact assessment

- Implementation case studies across verticals

- Technology trend analysis including AI/ML integration

Download FREE Sample Report:

Endpoint Backup Software Market Sample Report

Access Full Research:

Endpoint Backup Software Market Comprehensive Report

About Intel Market Research

Intel Market Research delivers actionable insights in technology and infrastructure markets. Our data-driven analysis leverages:

- Real-time infrastructure monitoring

- Techno-economic feasibility studies

Competitive intelligence across 100+ countries

Trusted by Fortune 500 firms, we empower strategic decisions with precision.

International: +1(332) 2424 294 | Asia: +91 9169164321

Website: https://www.intelmarketresearch.com

Follow us on LinkedIn: https://www.linkedin.com/company/intel-market-research

https://sites.google.com/view/intel-market-research/home/fish-counters-market-growth-analysis-market-dynamic-2025

https://sites.google.com/view/intel-market-research/home/travel-esim-market-growth-analysis-market-dynamics-2025

https://sites.google.com/d/1FmIQXbPYxpXHWg8EhgH39IzQaZD-THYX/p/1tiaBv8RsqnH94NPgJpuvUJH-AOzJH3sY/edit

https://sites.google.com/view/intel-market-research/home/test-handler-market-growth-analysis-market-dynamics-key-players-2025

https://sites.google.com/view/intel-market-research/home/smd-thermistor-market-growth-analysis-2025

According to recent market analysis, the global Rosé Wine market was valued at US$ 11,809.2 million in 2023 and is projected to reach US$ 14,670.1 million by 2030 , growing at a Compound Annual Growth Rate (CAGR) of 3.08% during the forecast period (2024-2030). The market's expansion is driven by shifting consumer preferences towards lighter alcoholic beverages, premiumization trends, and the rising popularity of rosé among younger demographics.

What is Rosé Wine?

Rosé Wine is a distinctive wine category produced through limited skin contact with red grape varieties, resulting in its characteristic pink hue that ranges from pale onion-skin to deep ruby depending on production methods. Unlike red wines, rosé's production typically involves only 6-48 hours of maceration , giving it a lighter body and refreshing acidity that has become synonymous with summer consumption. Modern rosés are predominantly dry wines , though semi-sweet and sparkling variants continue to hold significant market share in certain regions.

Key Market Drivers

1. Millennial and Gen Z Consumption Patterns

The 23-38 age demographic accounts for over 42% of rosé consumption globally, according to recent beverage industry surveys. Younger consumers favor rosé's approachable flavor profile, lower alcohol content (typically 11-13% ABV), and photogenic qualities that align perfectly with social media culture . This visual appeal has transformed rosé into an "Instagrammable" beverage, with producers leveraging distinctive packaging and branding to capitalize on this trend.

2. Premiumization and Craft Movement

The market has seen a pronounced shift toward premium rosé offerings , with price segments above $15 showing the fastest growth. Producers are responding with small-batch, terroir-driven rosés from prestigious appellations like Provence, Tavel, and Napa Valley. Limited edition bottles from renowned châteaux and celebrity-backed labels (such as Brad Pitt's Miraval) have created new luxury segments within the category.

Market Challenges

Despite robust growth projections, the rosé market faces several hurdles including seasonal demand fluctuations where 65-70% of annual sales occur between April-September in northern hemisphere markets. Distribution challenges persist in emerging markets where consumer awareness remains limited. Additionally, supply chain volatility has impacted glass bottle availability and transportation costs, with estimates suggesting a 12-18% increase in logistical expenses since 2021.

Emerging Opportunities

The development of year-round consumption occasions presents significant growth potential, with marketers successfully positioning rosé as suitable for winter holiday celebrations and food pairings beyond traditional summer fare. The Asian market shows particular promise, where wine consumption is growing at 6.8% annually and rosé's sweet-to-dry spectrum appeals to diverse palates. Innovative packaging formats including cans, bag-in-box, and single-serve bottles are expanding accessibility and convenience.

Regional Market Insights

-

Europe dominates the global market with a 2023 valuation of US$ 8,542.0 million, expected to reach US$ 10,445.8 million by 2030 (CAGR 2.86%). France alone accounts for 39% of global production, with Provence-style rosé setting international quality benchmarks.

-

North America is projected to grow from US$ 2,029.4 million to US$ 2,557.1 million (CAGR 3.35%), driven by premiumization and the proliferation of domestic producers in California, Oregon, and Washington State.

-

Asia-Pacific represents the fastest-growing region, forecast to expand from US$ 816.0 million to US$ 1,099.9 million (CAGR 4.01%), with China, Japan, and Australia leading adoption through wine education initiatives and tourism.

Competitive Landscape

The market features a mix of global alcohol conglomerates and boutique producers:

-

LVMH (Château d'Esclans) and Pernod Ricard own leading premium brands that define the luxury rosé segment

-

California's E & J Gallo Winery dominates mass-market distribution with brands like Dark Horse and MacMurray Estate

-

Specialist producers like Château Minuty and Gérard Bertrand maintain strong positions through premiumization and organic offerings

Market Segmentation

By Type:

- Still

- Sparkling

By Price Point:

- Value (Under $12)

- Premium ($12-$25)

- Super-Premium ($25+)

By Distribution Channel:

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail

- Direct-to-Consumer

By Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

For additional market segmentation details and regional breakdowns, download our complete research report.

Report Scope & Offerings

This 350-page market intelligence report provides:

-

2024-2030 market forecasts with COVID-19 impact analysis

-

Competitive profiles of 25+ leading producers and brands

-

Pricing analysis across regions and segments

-

Consumer trend analysis by demographic and occasion

Download FREE Sample Report: Rose Wine Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research delivers actionable insights in technology and infrastructure markets. Our data-driven analysis leverages:

-

Real-time infrastructure monitoring

-

Techno-economic feasibility studies

Competitive intelligence across 100+ countries

Trusted by Fortune 500 firms, we empower strategic decisions with precision.

International: +1(332) 2424 294 | Asia: +91 9169164321

Website: https://www.intelmarketresearch.com

Follow us on LinkedIn: https://www.linkedin.com/company/intel-market-research

https://sites.google.com/view/intel-market-research/home/fish-counters-market-growth-analysis-market-dynamic-2025

https://sites.google.com/view/intel-market-research/home/travel-esim-market-growth-analysis-market-dynamics-2025

https://sites.google.com/d/1FmIQXbPYxpXHWg8EhgH39IzQaZD-THYX/p/1tiaBv8RsqnH94NPgJpuvUJH-AOzJH3sY/edit

https://sites.google.com/view/intel-market-research/home/test-handler-market-growth-analysis-market-dynamics-key-players-2025

https://sites.google.com/view/intel-market-research/home/smd-thermistor-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/euv-photoresists-market-growth-analysis-2025

https://sites.google.com/view/intel-market-research/home/shower-wall-panel-market-2025

https://sites.google.com/view/intel-market-research/home/kilowatt-fiber-laser-market-growth-analysis-market-dynamics-2025