Category: Business

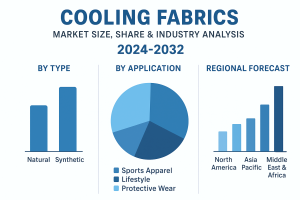

According to Fortune Business Insights, The global cooling fabrics market was valued at USD 2.10 billion in 2023 and is expected to increase from USD 2.21 billion in 2024 to USD 3.25 billion by 2032, reflecting a CAGR of 4.9% during the forecast period (2024–2032). In 2023, North America led the market, accounting for 40% of the global share.

The Cooling Fabrics Market is experiencing robust growth, driven by rising demand for advanced textiles that offer comfort, moisture management, and temperature regulation. Cooling fabrics are engineered using innovative technologies to provide breathability, sweat evaporation, and heat reduction, making them highly popular in sportswear, protective clothing, medical textiles, and lifestyle apparel. With the increasing adoption of sustainable and performance-enhancing fabrics, the market is expected to expand significantly over the next decade. The growing adoption of cooling fabrics by sportswear manufacturers is a key factor fueling market expansion. Their ability to regulate body temperature, wick away perspiration, and deliver a cooling effect has significantly boosted demand. Moreover, the increasing use of these fabrics in the defense and healthcare sectors is expected to further drive market growth, supported by rising defense expenditures. However, the COVID-19 pandemic posed challenges to the industry, causing a sharp decline due to supply chain disruptions. Despite this, a moderate rise in demand from the healthcare sector during the crisis helped mitigate the overall impact on the market.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/cooling-fabrics-market-105768

Key Market Insights

Market Size and Forecast

In 2023, the global cooling fabrics market was valued at USD 2.10 billion.

It is projected to grow to USD 2.21 billion in 2024.

By 2032, the market is expected to reach USD 3.25 billion, expanding at a CAGR of 4.9% during 2024-2032.

Regional Insights

North America dominated the market in 2023 with a share of about 40%.

Significant growth is also expected in Asia-Pacific and Europe, particularly in countries such as China, India, and Germany, due to rising apparel demand and advancements in technical textiles.

LIST OF KEY COMPANIES PROFILED

- Coolcore LLC (U.S.)

- Ahlstrom-Munksjö (Finland)

- Asahi Kasei Advanced Corporation (Japan)

- Formosa Taffeta Co. Ltd. (Taiwan)

- Tex-Ray Industrial Co. Ltd. (Taiwan)

- Nan Ya Plastics Corporation (Taiwan)

- Polartec (U.S.)

- NILIT Ltd. (Israel)

- Hexarmor (U.S.)

- Nanostitch (Belgium)

- Other Players

Market Dynamics

Key Drivers

Growing Sportswear & Activewear Demand – Rising fitness awareness and participation in outdoor sports are fueling the adoption of cooling fabrics in athletic apparel.

Rising Health Awareness – Consumers are shifting towards fabrics that provide skin-friendly, lightweight, and cooling properties.

Technological Innovations – Integration of phase change materials (PCMs), nanotechnology, and advanced fibers has enhanced product functionality.

Climate Change & Rising Temperatures – Increasing global temperatures have boosted the demand for fabrics that keep wearers cool and comfortable.

Restraints

High Production Cost – Advanced raw materials and manufacturing technologies make cooling fabrics expensive compared to conventional textiles.

Limited Awareness in Developing Economies – Consumers in price-sensitive markets are still largely dependent on traditional fabrics.

Opportunities

Expansion in medical and defense applications for thermal regulation.

Rising sustainable textile trends with eco-friendly cooling fabrics.

Increasing penetration in casual wear and home textiles (bed linens, upholstery).

Segmentation Analysis

By Type : Synthetic Cooling Fabrics, Natural Cooling Fabrics

By Application : Sports Apparel, Protective Clothing, Casual Wear, Medical Textiles, Home & Bedding

By Technology : Cooling Finishes, Phase Change Materials, Nanoparticle-Based Cooling

Regional Insights

North America : Leading the market due to strong adoption in sportswear, military clothing, and advanced R&D.

Europe : Growth supported by high demand for sustainable and innovative textiles.

Asia-Pacific : Expected to witness the fastest growth with rising textile manufacturing, growing middle-class income, and increasing awareness of functional fabrics.

Middle East & Africa / Latin America : Emerging markets with opportunities in sports and protective wear.

The global cooling fabrics market research report presents an in-depth analysis of the industry, highlighting key areas such as company profiles, fabric types, and major applications. It also provides valuable insights into prevailing market trends, growth dynamics, and notable industry developments. Furthermore, the report examines multiple factors that have driven the market’s expansion in recent years.

Information Source: https://www.fortunebusinessinsights.com/cooling-fabrics-market-105768

KEY INDUSTRY DEVELOPMENTS

- January 2023: NILIT launched a new version of SENSIL EcoCare. The recycled Nylon 6.6 material is now made entirely from U.S.-sourced materials and manufactured at the company's North American facility in Martinsville, VA.

- January 2022: HeiQ Materials AG launched HeiQ Cool, a new textile cooling technology that delivers both instant contact and continuous evaporative cooling. It's a significant development that could benefit those in hot or humid climates.

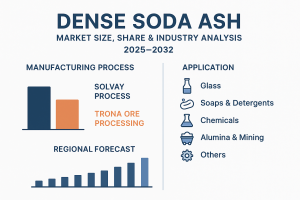

According to Fortune Business Insights, The global dense soda ash market was valued at USD 12.49 billion in 2024. It is anticipated to expand from USD 10.02 billion in 2025 to USD 15.70 billion by 2032, registering a CAGR of 6.6% over the forecast period. In 2024, Asia Pacific led the market, accounting for 61.80% of the total share.

Dense soda ash, also known as sodium carbonate, is a high bulk density chemical compound widely utilized as a raw material across various industrial applications. It plays a vital role in the production of glass, detergents, chemicals, alumina, and mining products. The compound is primarily manufactured through the Solvay process or obtained from natural trona ore deposits. The market is shaped by key factors such as industrial expansion, advancements in production technologies, and stringent environmental regulations. Moreover, the increasing demand from the glass and chemical industries, driven by rapid urbanization and infrastructure growth, is expected to be a major contributor to the market’s expansion.

The Dense Soda Ash Market is witnessing significant growth driven by rising demand across industries such as glass manufacturing, detergents, chemicals, and water treatment. Dense soda ash, also known as sodium carbonate (Na₂CO₃), is a white, odorless, water-soluble salt that plays a critical role as a raw material in various industrial applications. With growing urbanization, infrastructure development, and advancements in manufacturing, the market is set to expand steadily in the coming years.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/dense-soda-ash-market-113691

LIST OF KEY DENSE SODA ASH COMPANIES PROFILED

- Solvay (Belgium)

- Tata Chemicals Ltd. (India)

- Sudarshan Mineral (India)

- Şişecam (Turkey)

- Eti Soda Elektrik (India)

- InoChem. (Saudi Arabia)

- GHCL Limited (India)

- Tokuyama Corporation (Japan)

- QEMETICA (Poland)

- Tangshan Sanyou Group Co., Ltd. (China)

Market Overview

Dense soda ash is primarily produced using two methods: the natural trona ore process and the synthetic Solvay process . The glass industry accounts for the largest share of consumption, followed by detergents, chemicals, metallurgy, and pulp & paper.

Key Market Drivers:

Rising construction activities boosting demand for flat glass and container glass.

Increased use of detergents and cleaning agents in households and industries.

Expanding applications in water treatment, textiles, and metallurgy.

Market Restraints:

Environmental concerns related to soda ash production.

Volatility in raw material supply and energy costs.

Market Segmentation

By Application:

Glass Industry – The dominant segment, as soda ash is essential in manufacturing flat glass, fiberglass, and container glass.

Detergents & Soaps – Used as a builder in powder detergents to improve cleaning efficiency.

Chemical Industry – Key feedstock in the production of sodium silicates, sodium bicarbonate, and other chemicals.

Metallurgy – Plays a role in desulfurizing steel and non-ferrous metal processing.

Pulp & Paper – Used in pulping and bleaching processes.

By End-Use Industry:

Construction & Infrastructure

Automotive (for windshield and safety glass)

Household & Industrial Cleaning

Chemical Manufacturing

Others (Textiles, Water Treatment, etc.)

Regional Insights

North America: Major producer due to abundant trona reserves in the U.S., especially Wyoming.

Europe: Strong demand from glass and detergent industries, though reliant on imports.

Asia-Pacific: Fastest-growing market driven by construction booms in China, India, and Southeast Asia.

Middle East & Africa: Growing industrialization and demand for container glass in beverages.

Latin America: Rising detergent consumption and increasing glass production are supporting market growth.

The global Dense Soda Ash Market is expected to grow steadily over the next decade, driven by construction, automotive, and consumer goods industries. The increasing focus on sustainable production methods and recycling of glass is also likely to create new opportunities for market players.

Key Trends to Watch:

Rising demand for eco-friendly detergents.

Expansion of flat glass production for solar panels.

Adoption of advanced water treatment solutions.

The Dense Soda Ash Market is poised for strong growth due to its wide industrial applications and rising demand in glass and detergent industries. Companies investing in sustainable production and innovative applications will be well-positioned to capture future opportunities.

Information Source: https://www.fortunebusinessinsights.com/dense-soda-ash-market-113691

KEY INDUSTRY DEVELOPMENTS

- December 2023 : Solvay introduced a new soda ash production process named e.Solvay process. This new technology promises to cut CO₂ emissions by 50%, reduce energy, water, and salt consumption by 20%, and decrease limestone use and residues by 30%.

- June 2023: Tata Chemicals has announced a USD 968.0 million capex plan, including a 380 KT salt capacity addition in the U.K. and Mithapur, India. This will boost India's global salt capacity to 2.3 MT and 1.8 MT. The investments support growth, sustainability, and increased production across key product lines.

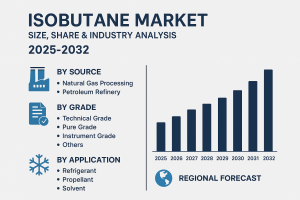

According to Fortune Business Insights, The global isobutane market was valued at USD 20.18 billion in 2024 and is anticipated to increase from USD 21.15 billion in 2025 to USD 30.39 billion by 2032, registering a CAGR of 5.3% over the forecast period. In 2024, Asia Pacific led the market, accounting for a 39.59% share. Isobutane, also known as 2-methylpropane, is a colorless and odorless gas under standard temperature and pressure, though it is typically compressed into a liquid for easier storage and transportation. Classified as a branched-chain alkane with the chemical formula C₄H₁₀, isobutane finds extensive use in refrigerants, aerosol propellants, and as a feedstock in petrochemical processes. Its low global warming potential and zero ozone-depleting properties make it a more environmentally sustainable alternative to conventional hydrocarbons.

The isobutane market is witnessing steady growth, driven by its wide applications in the petrochemical, refrigeration, and fuel sectors. Isobutane, also known as methylpropane, is a colorless, flammable gas derived from crude oil refining and natural gas processing. It plays a crucial role in the production of isooctane, an important blending component in gasoline, as well as in aerosol propellants, refrigerants, and feedstock for chemical manufacturing. With increasing demand for cleaner energy solutions and eco-friendly refrigerants, the global isobutane market is set to expand significantly in the coming years.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/isobutane-market-111014

LIST OF KEY ISOBUTANE COMPANIES PROFILED

- AIR LIQUIDE (France)

- Exxon Mobil Corporation (U.S.)

- Evonik (Germany)

- YEOCHUN NCC CO., LTD. (Korea)

- Mitsui Chemicals India Pvt. Ltd. (India)

- The TotalEnergies Company (France)

- Linde LLC (Ireland)

- Valero (U.S.)

- MATHESON TRI-GAS, INC. (U.S.)

- Vernigastech (India)

Market Drivers

Rising Demand for Refrigerants

Isobutane is widely used in household refrigerators and freezers as a refrigerant (R-600a). With growing environmental concerns, its low Global Warming Potential (GWP) and zero Ozone Depletion Potential (ODP) make it a preferred alternative to conventional refrigerants.

Growth in the Petrochemical Industry

The production of isooctane from isobutane boosts its demand in the fuel industry, as it improves the octane number in gasoline and reduces engine knocking.

Increasing Demand in Aerosol Propellants

Rising use of isobutane in personal care, pharmaceuticals, and household products as a propellant is fueling market growth.

Shift Toward Cleaner Fuels

With the global focus on reducing emissions, isobutane is gaining traction as a cleaner-burning fuel compared to other hydrocarbons.

Market Challenges

Volatility in Crude Oil Prices: Since isobutane is derived from crude oil, fluctuations in oil prices directly impact production costs.

Stringent Regulations: Regulations regarding flammable hydrocarbons and storage safety may affect large-scale adoption in certain regions.

Competition from Alternatives: Alternatives like propane and synthetic refrigerants may pose challenges to isobutane adoption.

Opportunities

Sustainable Refrigerants: Growing adoption of green refrigeration technologies presents lucrative opportunities.

Emerging Economies: Rapid urbanization and industrialization in Asia-Pacific and Latin America will create significant market potential.

Innovation in Petrochemicals: Technological advancements in refining and petrochemical processes are expected to enhance isobutane production efficiency.

Regional Insights

Asia-Pacific (APAC):

- The fastest-growing region, driven by strong demand in refrigeration, petrochemicals, and fuels. Countries like China, India, and South Korea are leading contributors.

North America:

The U.S. is a major player due to high demand for fuel additives and refrigerants. Stringent environmental policies encourage the adoption of eco-friendly refrigerants like isobutane.

Europe:

Focus on sustainable cooling technologies and stringent environmental norms make Europe a strong market for isobutane.

Middle East & Africa (MEA):

Rich crude oil reserves and growing petrochemical investments fuel market growth in this region.

Information Source: https://www.fortunebusinessinsights.com/isobutane-market-111014

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

AIR LIQUIDE, Exxon Mobil Corporation, Evonik, Mitsui Chemicals India Pvt. Ltd., and Linde LLC are the largest players in the market. Companies are making major investments in developing additives to address the evolving demands for sustainability and performance.

The global isobutane market is expected to witness steady growth during the forecast period, driven by rising demand in refrigeration, petrochemicals, and energy sectors. Increasing awareness of eco-friendly refrigerants, coupled with government regulations promoting sustainable alternatives, will shape the industry landscape.

The isobutane market is on a growth trajectory, fueled by demand in multiple industries and the shift toward sustainable solutions. With continuous investments in petrochemical infrastructure, innovation in green refrigeration, and growing demand in emerging economies, the market is poised for long-term expansion.

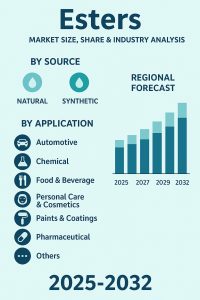

Esters Market Share, Emerging Trends & USD 13.15 Billion Projection by 2032

By ameliasss, 2025-09-09

According to Fortune Business Insights, The global esters market was valued at USD 8.54 billion in 2024 and is anticipated to expand from USD 8.90 billion in 2025 to USD 13.15 billion by 2032, reflecting a CAGR of 5.5% over the forecast period. In 2024, Asia Pacific emerged as the leading region, accounting for 45.55% of the overall market share.

Esters are organic compounds formed through the reaction of acids and alcohols, in which a hydroxyl group is replaced by an alkoxy group. Owing to their unique fragrances, solubility, and chemical adaptability, esters find applications across a wide range of industries. They serve as essential ingredients in the production of solvents, plasticizers, synthetic flavors, fragrances, and biodiesel, making them highly valuable in both industrial and commercial processes. The esters market has been gaining significant momentum in recent years, driven by its wide applications across industries such as lubricants, paints and coatings, plastics, personal care, and food and beverages. Esters are chemical compounds derived from acids and alcohols, offering beneficial properties such as biodegradability, high thermal stability, low volatility, and eco-friendliness, making them increasingly important in sustainable industrial practices.

The global esters market is projected to witness strong growth, supported by rising demand for environmentally friendly lubricants, the expansion of the personal care industry, and the adoption of advanced materials in packaging and coatings. Rapid industrialization, coupled with increasing awareness of green chemistry solutions, is also contributing to the market’s expansion.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/esters-market-113697

LIST OF KEY ESTERS COMPANIES

- Mitsubishi Chemical Group Corporation (Japan)

- Esters and Solvents LLP (India)

- Croda International Plc. (U.K.)

- BASF SE (Germany)

- Estelle Chemicals Pvt. Ltd. (India)

- Exxon Mobil Corporation (U.S.)

- The Dow Chemical Company (U.S.)

- Arkema (France)

- Solvay (Belgium)

- Evonik Industries AG (Germany)

Key Market Drivers

Growing Demand in Lubricants

Esters are extensively used as synthetic lubricants due to their superior lubrication properties, high flash point, and biodegradability. With industries shifting toward sustainable alternatives, demand for ester-based lubricants in automotive, aerospace, and industrial applications is growing.

Rising Applications in Personal Care & Cosmetics

Esters serve as emollients, solvents, and dispersing agents in cosmetics and personal care products. Increasing consumer demand for natural and organic beauty products is pushing manufacturers to use bio-based esters.

Booming Paints and Coatings Industry

In paints, coatings, and inks, esters function as solvents that enhance viscosity and drying properties. The rapid growth of construction and automotive industries is directly fueling this demand.

Shift Toward Biodegradable Plastics

Esters are essential in producing biodegradable polymers and plasticizers, which are gaining traction as governments tighten regulations on single-use plastics.

Market Segmentation

By Type :

Methyl Esters

Polyol Esters

Phosphate Esters

Nitrate Esters

Others

By Application :

Lubricants

Paints & Coatings

Plastics & Polymers

Food & Beverages (as flavoring agents)

Personal Care & Cosmetics

By Region :

North America : Strong demand in synthetic lubricants and coatings.

Europe : Driven by environmental regulations and adoption of green chemistry.

Asia-Pacific : Fastest-growing market, led by China and India due to industrial growth and rising disposable income.

Latin America & Middle East : Expanding automotive and construction industries boosting ester consumption.

Market Trends

Bio-based Esters : Increasing adoption of renewable and bio-based esters is a major trend as industries focus on reducing carbon footprints.

Technological Innovations : Companies are investing in R&D to produce high-performance esters tailored for niche applications like aerospace lubricants and specialty coatings.

Regulatory Support : Stringent government regulations favor biodegradable and low-VOC products, boosting ester demand.

Competitive Landscape

The esters market is moderately fragmented, with global players competing on the basis of product innovation, cost-efficiency, and sustainability. Major players are focusing on mergers, acquisitions, and capacity expansion to strengthen their market position.

The esters market is poised for steady growth over the next decade. Rising awareness of sustainable products, growth in end-use industries, and increasing adoption of bio-based solutions will be the primary drivers. By 2032, the market is expected to expand significantly, supported by global initiatives toward eco-friendly industrial practices.

Information Source: https://www.fortunebusinessinsights.com/esters-market-113697

KEY INDUSTRY DEVELOPMENTS

- March 2024: Mitsubishi Chemical Group announced the expansion of its Sugar Ester emulsifier production capacity by adding a new line at its Kyushu Plant in Japan. The new facility, with a capacity of 2,000 tons per year, has begun its full-scale operation in March 2024, while an additional line with a capacity of 1,100 tons per year is planned to start operations in March 2026.

- December 2023: Croda International Plc. opened a new facility, Pastillator 4 (PS04), at its Seraya site in Jurong Island, Singapore. With an investment of approximately USD 16 million, the expansion increased the site’s production capacity by 4.6 kilotons, bringing the total capacity to 15 kilotons, to serve the growing demand for pastille-format alkoxylates and esters.

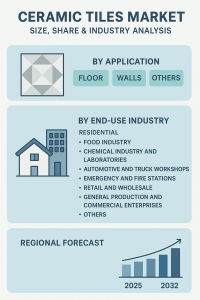

Ceramic Tiles Market Share, Future Outlook & USD 118.96 Billion Valuation by 2032

By ameliasss, 2025-09-09

According to Fortune Business Insights, The global ceramic tiles market was valued at USD 83.30 billion in 2024 and is anticipated to expand from USD 86.97 billion in 2025 to USD 118.96 billion by 2032, reflecting a CAGR of 4.6% over the forecast period. In 2024, Asia Pacific held the largest share of 53.57%, establishing itself as the leading regional market. Key industry participants include Mohawk Industries Inc., Grupo Lamosa, RAK Ceramics, and Kajaria Ceramics Limited. The market is thriving due to its several properties, such as water-resistant, cracking resistance, aesthetic appeal, and high durability, which increase product demand.

The market growth is primarily fueled by rising construction activities and increasing investments in infrastructure development across various countries. Ceramic tiles are gaining traction due to their durability, water resistance, crack resistance, and aesthetic appeal, making them a preferred choice for home renovations, commercial spaces, malls, and other facilities. Additionally, the growing population and higher disposable incomes are further boosting demand, supporting the overall expansion of the market.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/ceramic-tiles-market-102377

List of the Companies Profiled in the Ceramic Tiles Market:

- MOHAWK INDUSTRIES INC. (U.S.)

- SCG CERAMICS (Thailand)

- Grupo Lamosa (Mexico)

- Grupo Cedasa (Brazil)

- RAK CERAMICS (UAE)

- Cerâmica Carmelo Fior (Brazil)

- PAMESA CERÁMICA SL (Spain)

- Kajaria Ceramics Limited (India)

- STN Cerámica (Spain)

- Porcelanosa Group (Spain)

Segmentation-

Rising Governments Initiatives for the Economically Weaker Section Drives Residential Segment

On the basis of end-use, the market is divided into non-residential and residential. The residential segment will expected to rule due to the rising government initiatives to create houses for the economically weaker section of the community and the exponential rise in population.

Growing Demand for Ceramic Tiles Will Favor Market Development

In terms of application, the market is fragmented into floors, wall, and others. The floors segment will gain traction due to the growing demand for ceramic tiles with a variety of colors, textures, and patterns to improve the aesthetic appearance.

Report Coverage

The report provides insights into the regional analysis covering different regions, contributing to the market's growth. The report includes qualitative and quantitative analysis of several factors, such as the key drivers and restraints that will impact the market. Adopting strategies by major players to introduce partnerships, collaboration, and new products will contribute to the market's growth.

Drivers and Restraints

Increase in the Development of Infrastructural Activities to Fuel Market Expansion

The increase in the development of infrastructural activities combined with the growing investment is among the crucial factor that has led to the growth of the market. Furthermore, the shifting preferences of consumers toward ceramic tiles for the renovation of malls, houses, and shops are stimulating the market's growth. Meanwhile, the environmental impact caused by the production of ceramic tiles could impede market growth.

Regional Insights

Growing Employment in the Veterinary Sector Nurtures Growth in North America

Asia Pacific held a strong foothold in the global ceramic tiles market share during the forecast period. Certain factors, such as the high consumption of ceramic-based tiles and growing infrastructural developments, could spur market growth.

North America is anticipated to have considerable growth due to the burgeoning demand for green and energy-efficient buildings for governmental and commercial offices.

European Market is likely to display prominent growth during the forecast period due to the rising investment by the end-users in renovation and replacement activities across the region.

Competitive Landscape

Prominent Giants are Emphasizing on a Variety of Designs to get an Extra Edge in the Market

Major companies such as RAK ceramics and Mohawk Industries are investing notable sums into the ceramic titles to establish their solid footholds in the marketplace. Furthermore, the prominent giants in this segment are emphasizing on a variety of designs, shapes, sizes, and styles to improve their aesthetics.

Information Source: https://www.fortunebusinessinsights.com/ceramic-tiles-market-102377

Key Industry Development:

- October 2024 - RAK Ceramics partnered with Sobha Constructions LLC to supply premium ceramics and porcelain tiles for Sobha's upcoming projects. With this partnership, RAK Ceramics increases its customer base in the construction industry.

- June 2024- RAK Ceramics PJSC completed the full acquisition of RAK Porcelain LLC. With this acquisition, the company made it a wholly owned subsidiary. Such a development strategy helps a company to strengthen its market presence and capture significant market share across the globe.

Milk Packaging Market Forecast Report, Size & Analysis, USD 7.07 Billion in 2025 to USD 10.53 Billion by 2032, CAGR 5.85% 2025-2032

By ameliasss, 2025-09-08

According to Fortune Business Insights, The global milk packaging market size was valued at USD 6.74 billion in 2024. The market is projected to grow from USD 7.07 billion in 2025 to USD 10.53 billion by 2032, exhibiting a CAGR of 5.85% during the forecast period. Milk packaging refers to the materials and techniques employed to hold and deliver milk while maintaining its freshness, quality, safety, and convenience for consumers. It includes several kinds of containers, such as bottles, cartons, pouches, glass bottles, and cans. The demand for packaged liquid products, especially dairy products, is propelled by the rapid urbanization in developing nations, contributing to market growth. The milk packaging market is witnessing steady growth worldwide, driven by rising dairy consumption, increasing demand for safe and sustainable packaging, and advancements in packaging technologies. Packaging plays a critical role in maintaining milk’s quality, extending shelf life, and ensuring safety during transportation and storage. From traditional glass bottles to modern cartons, pouches, and PET bottles, the industry is continuously evolving to meet consumer preferences and environmental concerns. Tetra Pak International S.A. and Nippon Paper Industries Co. Ltd. are the leading manufacturers, accounting for the largest global market share.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/milk-packaging-market-104414

LIST OF KEY MILK PACKAGING COMPANIES PROFILED

- Tetra Pak International S.A. (Switzerland)

- Nippon Paper Industries Co. Ltd. (Japan)

- Elopak AS (Norway)

- Nampak (South Africa)

- SIG (Switzerland)

- Parksons Packaging (India)

- Liquibox (U.S.)

- Amcor (Switzerland)

- Mondi (U.K.)

- Refresco (Netherlands)

- Adam Pack (Greece)

- Pactiv Evergreen (U.S.)

Key Market Drivers

Rising Dairy Consumption – Growing demand for milk and dairy products in both developed and developing nations.

Shift Toward Sustainable Packaging – Increasing use of recyclable and biodegradable packaging materials.

Technological Advancements – Innovations such as aseptic cartons, smart labeling, and extended shelf-life packaging.

Changing Consumer Preferences – Urban populations prefer convenient, portable, and resealable packaging options.

Growth of Online Grocery & E-Commerce – Boosting the need for durable and tamper-proof packaging.

Market Segmentation

By Packaging Type

Cartons (aseptic, gable-top)

Bottles (PET, glass)

Pouches (flexible plastic, multilayered)

Cans & Others

By Material

Plastic

Paperboard

Glass

Others (metal, biodegradable composites)

By Distribution Channel

Supermarkets/Hypermarkets

Convenience Stores

Online Retail

Dairy Shops

By Region

North America – High adoption of eco-friendly cartons and bottles.

Europe – Strong regulatory framework promoting sustainable packaging.

Asia-Pacific – Fastest-growing region due to rising milk consumption in India, China, and Southeast Asia.

Latin America & Middle East – Expanding dairy production and packaging innovations.

Regional Insights

Asia-Pacific dominates the milk packaging market due to its large population, growing middle class, and increasing dairy production.

Europe focuses on sustainable solutions, with carton-based packaging being the most preferred.

North America shows strong demand for flavored and fortified milk in PET bottles and cartons.

Trends and Opportunities

Eco-friendly packaging using plant-based plastics and paperboard.

Smart packaging solutions with QR codes for traceability and authentication.

Digital printing technologies for branding and consumer engagement.

Expansion of aseptic packaging for long shelf-life products.

The milk packaging market is poised for substantial growth between 2025 and 2032 , supported by rising dairy consumption, sustainability initiatives, and packaging innovations. With increasing demand for eco-friendly and convenient packaging, manufacturers are expected to adopt advanced technologies that not only ensure milk safety but also reduce environmental impact. The global online food delivery sector is expanding rapidly. The increasing consumption of milk products among the millennial population is fueling the need for effective packaging such as cartons, bottles.

Information Source: https://www.fortunebusinessinsights.com/milk-packaging-market-104414

KEY INDUSTRY DEVELOPMENTS

- July 2024: Tetra Pak and Mengniu Group unveiled a limited-edition Milk Deluxe Pure Milk range, featuring 30 unique designs based on masterpieces by Van Gogh and Monet. The products are packaged in Tetra Prisma Aseptic 250 Edge cartons with DreamCap 26 closures, and this special edition range has been launched through a partnership with Meet You Museum. Consumers in Greater China can now find these cartons both online and in physical stores.

- April 2024: Nampak Liquid Cartons, in collaboration with Woodlands Dairy, introduced a tethered cap carton in South Africa. This innovation was created to address the reduction of plastic waste, and the new design aims to keep the cap attached to the carton during its recycling process after consumer use.

Adherence Packaging Market Demand, Industry Insights, and Future Outlook, 2025-2032

By ameliasss, 2025-09-08

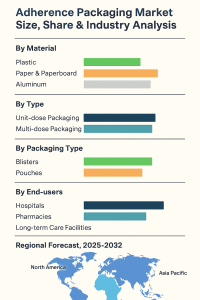

According to Fortune Business Insights, The global adherence packaging market was valued at USD 1.13 billion in 2024 and is anticipated to grow to USD 1.20 billion in 2025, eventually reaching USD 1.89 billion by 2032. This growth reflects a CAGR of 6.67% over the forecast period. In 2024, North America led the market, accounting for 38.05% of the global share.

Adherence packaging is a pharmacy service that organizes a patient’s medications into personalized pouches or blister packs aligned with their dosing schedule. Its primary purpose is to improve medication adherence and, as a result, clinical outcomes. Demand for these solutions is rising—particularly among older adults and people with chronic conditions—and is being further propelled by innovations such as smart packaging and the integration of digital health technologies, which are expanding the global market. Adherence packaging, also called compliance packaging means the method of packaging that makes the adherence of patients to their drug routine easy. The surge in the emphasis of prominent companies on the enhancement of medication adherence through more patient-focused and intelligent packaging methods, which leads to the generation of data from current delivery systems and medicines while aiding in the reduction of wastage of drugs, is fostering the market growth.

Fortune Business Insights presents this information in their report titled " Adherence Packaging Market , 2025–2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/adherence-packaging-market-108330

List of Key Adherence Packaging Companies Profiled

- WestRock Company (U.S.)

- Manrex Limited (Canada)

- Parata Systems LLC (U.S.)

- McKesson Corporation (U.S.)

- Pearson Medical Technologies LLC (U.S.)

- Cardinal Health, Inc. (U.S.)

- Omnicell, Inc. (U.S.)

- Becton, Dickinson, and Company (U.S.)

- Talyst, LLC (U.S.)

- TCGRx (U.S.)

Segmentation:

By material, the market is classified into aluminum, paper & paperboard, and plastic. The plastic segment captured the largest adherence packaging market share in 2023. This can be attributed to the cost-effectiveness, transparency, lightweight, and malleable nature of plastic.

In terms of type, the market is bifurcated into multi-dose and unit-dose. The multi-dose segment accounts for the largest share due to the growing requirement for adherence to medication.

Based on packaging type, the market is segregated into pouches and blisters. The blisters segment holds the largest market share. Enhanced shelf-life, ease of transport, and high resistance to tamper provided by blisters are augmenting the segment expansion.

With respect to end users, the market for adherence packaging is segmented into long-term care facilities, pharmacies, and hospitals.

Geographically, the market is divided into the Asia Pacific, Latin America, the Middle East & Africa, Europe, and North America.

Report Coverage

The research report provides a detailed analysis of the major strategic initiatives opted for by leading players in the market. In addition, it highlights the top trends, key industry developments, and the impact of the COVID-19 pandemic on the market growth. Additional aspects of the report include the notable factors impacting the adherence packaging market size.

Drivers:

Surging Desire to Remove Drug Wastage to Impel the Market Growth

The adherence packaging market growth can be credited to a rise in desire for the removal of wastage of the drug. Moreover, medication waste accounts for a substantial impact on the economy and the healthcare system across the globe and creates detrimental consequences for the environment.

Regional Insights:

North America Dominates Due to Rising Life Science & Medical Research Activities

North America accounts for the dominating position in the market. This is due to the growing spending power on healthcare coupled with the surging medical research & life science research activities.

Europe is the second-leading region in the adherence packaging market owing to the heightened availability of government funding for activities pertaining to research and development.

The Asia Pacific market is observing the fastest growth owing to the growing uptake of the solution along with healthcare sector investments.

Information Source: https://www.fortunebusinessinsights.com/adherence-packaging-market-108330

Competitive Landscape:

Top Players Emphasize Launching New Products to Reinforce Their Industry Position

Mergers & acquisitions, partnerships, and joint ventures are some of the strategies opted for by leading companies to gain a competitive edge in the adherence packaging market. Several firms are also focusing on launching new products to sustain their industry leadership.

Key Industry Development

- In April 2024, Gerresheimer partnered with U.S. digital health company RxCap, acquiring a minority stake. Gerresheimer's subsidiary Center aimed at distributing RxCap's adherence solutions in U.S. pharmacies, leveraging its market leadership in prescription vials to enhance pharmacy workflows with smart technology.

- In April 2024, Jones Healthcare Group launched a new line of smart adherence packages that utilizes technology to monitor medication usage and enhance patient engagement.

Exterior Wall Systems Market Size, Share & Regional Outlook North America, Europe, Asia Pacific 2025-2032

By ameliasss, 2025-09-04

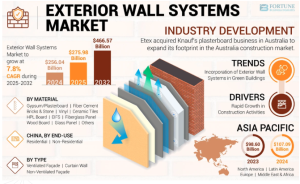

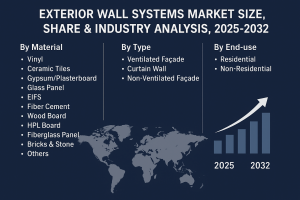

According to Fortune Business Insights, The global exterior wall systems market was valued at USD 256.04 billion in 2024 and is expected to expand from USD 275.98 billion in 2025 to USD 466.57 billion by 2032, registering a CAGR of 7.8% over the forecast period. Asia Pacific led the market in 2024, accounting for 42.14% of the share. In addition, the U.S. exterior wall systems market is anticipated to experience robust growth, projected to reach USD 55.45 billion by 2032. This growth is primarily fueled by the rising adoption of dry construction techniques over traditional wet methods, boosting the demand for exterior wall system products.

Exterior wall systems refer to an enclosure or envelope of a structure that is made to protect the interiors from the external environment. Governments as well as private organizations are increasing their investments in residential, commercial, and industrial establishments, which has augmented the demand for these wall systems. Moreover, the construction sector is rapidly expanding in developing countries, which will further fuel the exterior wall systems market growth.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/exterior-wall-systems-market-104394

List of Key Players Profiled in the Report

- Nippon Sheet Glass Co., Ltd (Japan)

- Saint-Gobain (France)

- AGC Inc. (Japan)

- Sika AG (Switzerland)

- PPG Industries, Inc. (U.S.)

- 3A Composite Holding AG (Switzerland)

- SCG (Thailand)

- Etex Group (Belgium)

- Owens Corning (U.S.)

- Evonik Industries AG (Germany)

- LafargeHolcim (Switzerland)

- USG Boral (Australia)

Segments:

Curtain Walls to Gain Notable Traction Owing to Strong Adoption in the Construction Sector

By type, the market is segmented into ventilated façade, curtain walls, and non-ventilated façade.

The curtain wall segment is expected to account for a dominant exterior wall systems market share due to its strong adoption in the construction sector. Its minimal fabrication time and short duration of construction are expected to enhance its adoption.

Glass Panels to be Widely Demanded Due to their Superior Properties

By material, the market is segmented into ceramic tiles, vinyl, gypsum/plasterboard, glass panels, EIFS, fiber cement, wood board, HPL board, fiberglass panel, bricks & stone, and others. The glass panel segment is expected to dominate the market share due to its superior properties and aesthetics. Further, the introduction of smart glass is expected to enhance the growth of this segment.

Non-Residential End-Users to Increase Product Adoption Due to Increasing Infrastructure Construction

By end-use, the market is bifurcated into residential and non-residential. The non-residential segment is expected to hold a dominant market share due to the rising number of infrastructure and construction projects across the globe. This factor may promote the growth of the segment.

Geographically, the market is segmented into North America, Asia Pacific, Europe, Latin America, and the Middle East & Africa.

Report Coverage

The report analyses the market in depth and highlights crucial aspects such as leading end-users, prominent companies, key disposable types, and distribution channels. It also provides valuable insights into the market dynamics, trends, and covers vital industry developments. Besides the factors mentioned above, the report encompasses various factors that have contributed to the growth of the market in recent years.

Driving Factors

Increasing Construction Projects Globally to Elevate Market Growth

Commercial, industrial, and residential construction activities have increased significantly in recent years across the world, which boosted the demand for exterior wall systems. Governments are also taking various initiatives to modernize the existing infrastructure by increasing the flow of foreign investments in large-scale infrastructure construction projects. These factors are predicted to fuel the market growth.

However, stringent government regulations regarding carbon emission levels are likely to restrict the market growth.

Regional Insights

Increasing Construction Projects in Developing Countries to Boost Market Growth in Asia Pacific

Asia Pacific is projected to dominate the global exterior wall systems market share due to a dramatic increase in construction projects. For example, rising infrastructure projects, such as Beijing’s Daxing International Airport and the Shanghai Urban Rail Transit Expansion projects, are likely to elevate the industry growth.

In Europe, the increasing trends of green buildings and energy efficiency are expected to enhance the adoption of exterior wall systems. These factors may propel the industry growth.

Information Source: https://www.fortunebusinessinsights.com/exterior-wall-systems-market-104394

Competitive Landscape

Companies Undertake Different Growth Strategies to Maintain Leading Market Position

Prominent companies operating in the market are focusing on innovating their existing product ranges to cater to the ever-growing demand for wall systems. These organizations are developing eco-friendly and innovative products to expand their presence. They are also partnering with renowned raw material suppliers and construction companies to stay ahead of their competition. These initiatives will help them maintain their position in the industry.

Key Industry Development

- March 2022: Holcim announced the acquisition of Malarkey Roofing Products with estimated 2022 net sales of USD 600 million. Through this acquisition, Malarkey would help Holcim expand its range of roofing systems in the highly profitable U.S. residential roofing market. This move was important for Holcim to achieve its goal of touching USD 4 billion in roofing net sales by 2025, while also speeding the company's expansion of its product and solution range.

Pharmaceutical Packaging Market Global Expansion & Innovation Outlook 2025-2032

By ameliasss, 2025-09-04

According to Fortune Business Insights, The global pharmaceutical packaging market was valued at USD 110.55 billion in 2024 and is expected to grow to USD 116.58 billion in 2025, reaching USD 177.12 billion by 2032. This growth reflects a CAGR of 6.16% over the forecast period. In 2024, North America led the market, accounting for 30% of the overall share. The surge is due to the escalating prevalence of non-communicable and communicable diseases across various regions.

Pharmaceutical packaging refers to the materials and processes designed to protect, preserve, and deliver pharmaceutical products. Its primary role is to shield drugs from external factors such as moisture, light, and temperature fluctuations, while also ensuring the product stays securely contained, free from leakage or contamination.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/pharmaceutical-packaging-market-102860

List of Key Players Mentioned in the Report:

- Amcor Plc (Switzerland)

- Gerresheimer AG (Germany)

- SCHOTT AG (Germany)

- Westrock (U.S.)

- AptarGroup, Inc. (U.S.)

- Berry Global, Inc (U.S.)

- NIPRO (Japan)

- CCL Industries Inc. (Canada)

- West Pharmaceutical Services (U.S.)

- SGD Pharma (France)

- Ardagh Group S.A. (Luxembourg)

- International Paper (U.S.)

- Comar LLC (U.S.)

- Vetter Pharma (Germany)

- Nolato AB (Sweden)

Segments:

Plastics Segment to Gain Traction Considering its Extensive Usage

Based on material, the market is segmented into plastics, glass, metal, paper & paperboard, and others. The plastic segment is anticipated to depict a notable upsurge over the forecast period. Plastic is the most considerable raw material used in the production of pharmaceutical packaging.

Bottles Segment to Register Prominent Share Impelled by Low Costs

Based on product type, the market is subdivided into bottles, vials & ampoules, caps & closures, blister packs, pre-fillable inhalers, pre-fillable syringes, bags & pouches, jars & canisters, cartridges, and others. Of these, the bottles segment is poised to expand at a substantial pace over the estimated period. The surge is on account of low cost and light weight.

Primary Packaging Segment to Grow at the Fastest Pace Impelled by the Advantage of Protection Against Chemicals

On the basis of packaging type, the market for pharmaceutical packaging is categorized into primary, secondary, and tertiary. The primary packaging segment is estimated to expand at a commendable pace over the study period. The products help in the maintenance of shelf life and protect the drugs from chemicals and moisture.

Oral Drug Delivery Packaging to Hold Dominating Share Owing to Flexibility in Designing Dosage

By drug delivery mode, the market is segregated into oral drug delivery packaging, nasal drug delivery packaging, topical drug delivery packaging, ocular drug delivery packaging, injectable packaging, transdermal drug delivery packaging, pulmonary drug delivery packaging, and others. The oral drug delivery packaging segment held a dominating share in the global market.

By geography, the market has been studied across North America, Asia Pacific, Europe, Latin America, and the Middle East & Africa.

Report Coverage:

The report presents a systematic study of the market’s segments and a thorough analysis of the market overview. An in-depth evaluation of the current market trends as well as future opportunities is offered in the report.

Drivers and Restraints:

Expanding Pharmaceutical Industry Around the Globe to Drive Market Growth

In wealthy nations such as the U.S., the U.K., and Germany as well as in developing nations such as China, India, and Brazil, the pharmaceutical sector is expanding quickly. The population is growing, technological advancements are increasing, and new government regulations are being put in place to stop the spread of infectious diseases. Additionally, the rising demand for biological products and emerging treatments such as cell and gene therapies are expected to promote the pharmaceutical packaging market growth.

However, an escalation in counterfeit drugs could hamper industry expansion to a considerable extent.

Regional Insights:

North America to Lead Backed by Elevated Demand for Packaging due to Rising Healthcare Expenditure

The U.S. is the largest contributor to North America, which has the largest pharmaceutical packaging market share. The region's development is attributable to the pharmaceutical industry's explosive growth. The market growth in this region is being driven by the increased need for primary packaging goods, surging healthcare spending, and rising disease prevalence.

Germany, the U.K., and Italy in Europe accounted for the second-largest market in the globe. Pre-filled syringes, plastic bottles, containers, vials, and ampoules have all aided in the expansion of this industry.

China, Japan, and India are the top three nations in the Asia Pacific contributing to the market expansion.

Information Source: https://www.fortunebusinessinsights.com/pharmaceutical-packaging-market-102860

Competitive Landscape:

Innovative Product Launch Initiatives by Key Players to Bolster Market Growth

The prominent players adopt several strategies to bolster their position in the market as leading companies. One such key strategy is acquiring companies to bolster their brand value among users. Another essential strategy is periodically launching innovative products with a detailed study of the market and its target audience.

Key Industry Development:

January 2024- SGD Pharma launched the extension of its Clareo range to include 10ml and its Sterinity range of ready-to-use vials in sizes 10ml and 20m. The Clareo range of molded glass vials is available in sizes from 10ml to 200ml. These vials are designed to meet American market specifications and have a GPI 20 neck finish.

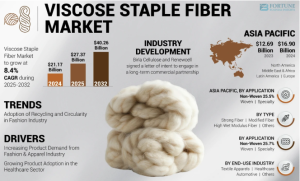

According to Fortune Business Insight, The global v iscose staple fiber market was valued at USD 21.17 billion in 2024 and is expected to expand from USD 27.37 billion in 2025 to USD 40.26 billion by 2032, reflecting a CAGR of 8.4% during the forecast period. Asia Pacific emerged as the leading region, accounting for 79.83% of the market share in 2024. In addition, the U.S. viscose staple fiber market is anticipated to witness robust growth, projected to reach USD 2.17 billion by 2032, supported by its superior properties and increasing recognition as a sustainable alternative to cotton.

Made from regenerated natural materials such as cotton linters or wood pulp, Viscose Staple Fiber (VSF) is a cellulose fiber valued for its softness, drapability, and absorbency, making it widely used in home textiles, clothing, and various consumer products. Increasing consumer awareness of the environmental impact of clothing is fueling demand for sustainable fibers, such as viscose staple fibers.

Fortune Business Insights™ provides this information in its research report, titled “Viscose Staple Fiber Market, 2025-2032”.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/viscose-staple-fiber-market-105431

List of Key Players Mentioned in the Report:

- Grasim Industries Limited. (India)

- LENZING Group (Austria)

- Tangshan Sanyou Group Xingda Chemical Fiber Co.Ltd (China)

- Sateri Holdings Limited (China)

- Kelheim Fibers GmbH (Germany)

- Xinjiang Zhongtai Chemical Co., Ltd. (China)

- Kayavlon Impex Pvt. Ltd. (India)

Segmentation:

Strong Fiber Leads with Rising Demand for Organic and Sustainable Solutions

By type, the market is segmented into strong fiber, modified fiber, high wet modulus fiber, and others. The strong fiber segment secured the largest market share in 2023 and is slated to remain the leading segment during the forecast period. As organic materials, strong viscose fibers meet the growing demand for organic and sustainable materials, positioning them favorably in the market.

Woven Segment Dominates due to Increasing Demand for High-Performance Fabrics

In terms of application, the market is divided into non-woven, woven, and specialty. The woven segment held the key viscose staple fiber market share in 2023. With various industries seeking reliable and durable fabrics, the growing demand for high-performance materials propels the preference for woven fabrics.

Textile Apparels Hold Prominent Position with Amplified Demand from Fashion Sector

Based on end-use industry, the market is fragmented into healthcare, automotive, textile apparels, and others. The textile apparels segment held the largest market share in 2023 fueled by the escalating demand from the fashion industry

In terms of region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- The latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers and Restraints:

Increasing Product Demand from Fashion & Apparel Industry to Bolster Market Growth

Rising demand for sustainable materials in the fashion industry has propelled the adoption of the product due to its eco-friendly properties and versatility. Moreover, with changing consumer buying habits and rising disposable income, the apparel industry is expanding, leading to a higher demand for high-quality textiles and garments made from VSFs.

However, reliance on wood pulp from natural forests instead of sustainably harvested trees restricts viscose staple fiber market growth due to environmental concerns.

Regional Insights:

Asia Pacific Dominates the Market Owing to Surging Demand Across Industries

Asia Pacific holds the dominating position in the global market and held the largest market share in 2023. The increasing textile demand across diverse sectors is driving the need for viscose staple fibers in Asia Pacific.

In Latin America, increasing demand for fabrics in both domestic and industrial applications is fueling market growth, driven by urbanization and changing consumer preferences.

Information Source: https://www.fortunebusinessinsights.com/viscose-staple-fiber-market-105431

Competitive Landscape:

Key Players Adopt Sustainable Practices to Minimize Wastewater Generation

Sateri, Lenzing Group, Kelheim Fibers GmbH, and Xinjiang Zhongtai Chemical Co., Ltd. are major viscose staple fiber market players emphasizing product innovation and sustainable practices. They focus on integrating new technologies to boost efficiency and minimize wastewater generation. Grasim Industries Limited's Nagda unit aims for zero liquid discharge, while LENZING Group is adopting renewable energy at subsidiaries such as Lenzing Nanjing Fibers and PT. South Pacific Viscose, signaling a commitment to eco-friendly operations.

Key Industry Development:

- May 2023 - Kelheim Fibres GmbH and Santoni Spa joined forces to develop a sustainable and advanced menstrual underwear from superior-quality performance viscose fiber and advanced machine technology. The product comprises a softer outer layer and an inlay part made from superior wood-based fibers.

- November 2022 - The LENZING Group completed a milestone of 300,000 tons of LENZING ECOVERO branded fibers production with the target to double the production capacity by 2023 due to rising demand.