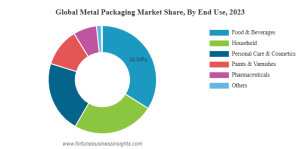

According to Fortune Business Insights, The global metal packaging market was valued at USD 146.70 billion in 2023 and is expected to expand from USD 150.59 billion in 2024 to USD 194.68 billion by 2032, reflecting a CAGR of 3.26% during the forecast period. North America led the market in 2023, accounting for 34.57% of the global share. In particular, the U.S. metal packaging market is anticipated to experience strong growth, reaching USD 53.06 billion by 2032, primarily driven by the high consumption of canned foods, energy drinks, and packaged goods.

Category: Business

Polyethylene Market Growth Driven by Packaging and Construction Demand by 2032

By ameliasss, 2025-10-30

Polyethylene (PE) is one of the most widely used and versatile plastics worldwide. Known for its cost-effectiveness, flexibility, and durability, it plays a critical role in multiple industries such as packaging, construction, automotive, and consumer goods. According to Fortune Business Insights, the global polyethylene market continues to expand due to growing demand across industrial and consumer sectors.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/polyethylene-pe-market-101584

LIST OF KEY COMPANIES PROFILED:

- LyondellBasell Industries N.V. (Netherlands)

- ExxonMobil Chemical (U.S.)

- SABIC (Saudi Arabia)

- Reliance Industries Limited (India)

- INEOS (U.K.)

- China National Petroleum Corporation (China)

- China Petroleum & Chemical Corporation (China)

- Ducor Petrochemicals (Netherlands)

- Formosa Plastic Group (Taiwan)

- Braskem (Brazil)

Market Size & Growth Forecast

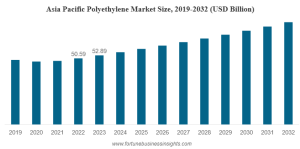

The global polyethylene market was valued at USD 110.23 billion in 2023 and is projected to reach USD 158.49 billion by 2032 , exhibiting a CAGR of around 4.1% during the forecast period (2024–2032).

Earlier estimates showed growth from USD 106.14 billion in 2022 to USD 140.21 billion by 2029 , maintaining the same CAGR of 4.1%.

This consistent growth pattern indicates that the polyethylene market is stable and mature, driven by steady demand rather than rapid expansion.

Key Growth Drivers

Strong Demand from Packaging Sector

Packaging remains the largest application segment for polyethylene. Its light weight, chemical resistance, and flexibility make it ideal for films, containers, pouches, and wraps. The increasing use of flexible packaging in food, beverages, and consumer goods continues to boost PE demand.-

Expanding End-Use Industries

The automotive, electrical & electronics, construction, and agriculture sectors are contributing significantly to polyethylene consumption. Its use in pipes, insulation, tanks, and protective films is increasing as infrastructure projects grow globally.

Manufacturing Expansion

Key producers are investing in new production facilities and advanced polymer technologies, increasing global supply and introducing high-performance PE grades to meet rising demand.

Segmentation Analysis

By Type

High-Density Polyethylene (HDPE)/Medium-Density Polyethylene (MDPE) – Dominates the market due to high tensile strength, chemical resistance, and usage in pipes, containers, and bottle caps.

Low-Density Polyethylene (LDPE) – Used in film applications, coatings, and packaging.

Linear Low-Density Polyethylene (LLDPE) – Offers flexibility and toughness, commonly used in stretch wraps and industrial films.

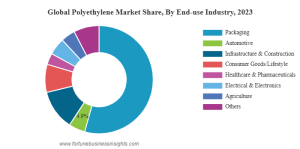

By End-Use Industry

Packaging – Holds the largest market share, driven by flexible packaging for food and e-commerce.

Infrastructure & Construction – Includes HDPE pipes, geomembranes, and insulation materials.

- Healthcare & Pharmaceuticals – Used for medical packaging and devices.

Regional Insights

Asia-Pacific – The largest and fastest-growing market due to rapid industrialization, urbanization, and increasing infrastructure projects in China, India, and Southeast Asia.

North America – Growth driven by advanced packaging and construction applications, supported by low-cost shale gas feedstock.

Europe – Focused on sustainability, recycling, and regulatory compliance in plastic usage.

Middle East & Africa – Emerging as a key production hub due to abundant raw materials and growing downstream demand.

Latin America – Steady growth supported by food packaging and consumer goods demand.

Market Challenges

Feedstock Price Volatility

Polyethylene production depends on ethylene derived from petroleum or natural gas. Fluctuations in crude oil prices directly impact production costs and profit margins.

Environmental & Regulatory Pressure

Increasing bans on single-use plastics and mandates for recyclable materials challenge producers to innovate in sustainable and bio-based polyethylene alternatives.

Competition from Substitutes

Materials like polypropylene (PP), polyethylene terephthalate (PET), and biodegradable plastics are gaining traction as alternatives to conventional PE.

Market Saturation in Mature Regions

In developed economies, where packaging markets are already highly penetrated, growth is slower compared to emerging regions.

Strategic Insights

Companies should focus on developing sustainable and recyclable polyethylene grades to align with global circular economy goals.

Regional integration and cost optimization will be key for maintaining competitiveness as global supply expands.

Investment in advanced recycling technologies and eco-friendly production methods will help companies meet regulatory demands and enhance brand value.

Information Source: https://www.fortunebusinessinsights.com/industry-reports/polyethylene-pe-market-101584

Future Trends

Increasing adoption of bio-based and recycled polyethylene to meet sustainability targets.

Greater focus on chemical recycling for circular polymer supply chains.

Continued expansion in Asia-Pacific and the Middle East driven by infrastructure development and feedstock availability.

The polyethylene market is projected to maintain steady growth over the next decade, reaching approximately USD 158.49 billion by 2032 . Packaging remains the dominant application, while innovation in sustainable and advanced polymer technologies will shape the industry’s future.

Although the market faces challenges related to cost fluctuations and regulatory pressures, opportunities in recycling, lightweight materials, and emerging economies provide significant potential for long-term expansion.

KEY INDUSTRY DEVELOPMENTS:

- November 2023: NOVA Chemicals Corporation and Amcor announced the signing of a Memorandum of Understanding (MoU) for mechanically recycled polyethylene. As per the agreement, NOVA Chemicals Corporation, the leading producer of polyethylene, would supply mechanically recycled polyethylene to Amcor, a prominent global packaging solutions manufacturer.

Posted in: Business

| 0 comments

Metal Packaging Market Top Growth Cities: Urbanization’s Role in Packaging Demand

By ameliasss, 2025-10-30

The global metal packaging market is gaining traction as demand for durable, sustainable, and recyclable packaging solutions continues to rise across industries such as food & beverage, healthcare, and personal care. Metal packaging offers superior protection, extended shelf life, and high recyclability, making it a preferred choice for both manufacturers and environmentally conscious consumers.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/metal-packaging-market-103867

Competitive Landscape

The metal packaging market is moderately consolidated, with key players focusing on strategic partnerships, product innovations, and capacity expansions. Companies are emphasizing lightweight materials and advanced coatings to meet evolving consumer preferences.

Prominent Companies Include:

- Ball Corporation (U.S.)

- Crown Holdings Inc. (U.S.)

- Silgan Holdings (U.S.)

- Amcor Limited (Australia)

- Ardagh Group SA (Europe)

- Tata Steel (India)

- Toyo Seikan Group Holdings Inc. (Japan)

- Grief Incorporated (U.S.)

- Ton Yi Industrial (China)

- Can-Pack SA (Netherlands)

- CCL Containers (U.S.)

- Sonoco Products Company (U.S.)

- Mauser Packaging Solutions (U.S.)

Market Drivers

1. Rising Demand for Sustainable Packaging Solutions

Sustainability is one of the major factors propelling the metal packaging market growth . Metals such as aluminum and steel can be recycled indefinitely without losing quality, aligning with global sustainability and circular economy goals. Governments and brands are adopting eco-friendly materials to reduce plastic waste, further boosting the market demand.

2. Expanding Food and Beverage Industry

The food & beverage sector dominates the market, with increasing use of metal cans for food, soft drinks, beer, and energy beverages . Metal packaging offers excellent barrier properties, protecting contents from light, moisture, and contaminants, ensuring product safety and extended shelf life.

3. Technological Advancements in Metal Packaging

Modern innovations such as lightweight can designs, improved coating technologies, and easy-open lids have enhanced the functionality and appeal of metal packaging. Manufacturers are investing in advanced printing and design technologies to attract consumers through visually appealing packaging.

Market Restraints

Despite its benefits, the metal packaging industry faces challenges such as fluctuating raw material prices of aluminum and steel, which can affect production costs. Additionally, the shift toward alternative packaging materials , including biodegradable plastics and paper, poses a competitive challenge to metal packaging manufacturers.

Regional Insights

Asia Pacific

Asia Pacific holds the largest share in the global metal packaging market , led by China, India, and Japan. Rapid urbanization, rising disposable income, and growing consumption of packaged foods and beverages are key growth factors.

North America

The North American market is characterized by strong demand for canned beverages and processed foods , coupled with high recycling rates of metal packaging. The U.S. remains a major market player due to the presence of leading packaging manufacturers.

Europe

Europe has a well-established recycling infrastructure and stringent environmental regulations promoting sustainable packaging. The region’s focus on circular economy initiatives supports continuous demand for metal-based packaging .

Segmentation Overview

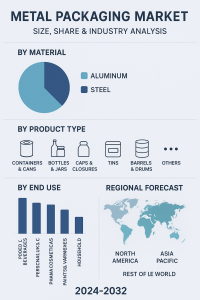

By Material Type

Aluminum

Steel

Tin

By Product Type

Cans

Caps & Closures

Barrels & Drums

Tubes

By End-Use Industry

Food & Beverage

Personal Care & Cosmetics

Healthcare

Industrial

Others

Recent Industry Developments

2024: Ball Corporation introduced lightweight aluminum cans aimed at reducing carbon emissions during transportation.

2023: Ardagh Group expanded its production capacity in Europe to cater to growing beverage can demand.

2023: Crown Holdings partnered with beverage brands to launch eco-friendly, fully recyclable metal packaging.

The future of the metal packaging market looks promising, driven by increasing sustainability efforts, growth in e-commerce packaging, and continuous innovation in design and materials. The adoption of smart packaging technologies such as QR codes and digital printing will further enhance consumer engagement and brand value.

The global metal packaging market is set for steady growth through 2032, fueled by its unmatched recyclability, durability, and safety features. As industries shift toward sustainable packaging solutions, metal packaging will remain a cornerstone of the global packaging ecosystem.

Information Source: https://www.fortunebusinessinsights.com/metal-packaging-market-103867

KEY INDUSTRY DEVELOPMENTS:

- November 2022 – Trivium Packaging announced the launch of a new segment in the packaging market, which can benefit mainly from aluminum bottle packaging, further releasing aluminum bottles for edible oil. The company has adapted its bottle to be feasible for edible oil closures in the U.S.

- July 2022 – a leading sustainable aluminum solutions provider, Novelis declared the expansion of its evercycle portfolio specifically designed for the cosmetic packaging market. Evercycle Cosmetics is certified, contains 100% recycled aluminum, and can meet customers' anodized quality requirements.

Posted in: Business

| 0 comments

The global hydrogen peroxide market is experiencing robust growth, driven by increasing demand across industries such as pulp & paper, textiles, healthcare, and wastewater treatment. Hydrogen peroxide (H₂O₂) is widely used as a bleaching, oxidizing, and disinfecting agent due to its environmentally friendly nature, as it decomposes into water and oxygen without leaving harmful residues.

Market Overview

According to Fortune Business Insights, The global hydrogen peroxide market was valued at USD 1.82 billion in 2023 and is expected to grow from USD 1.89 billion in 2024 to USD 2.56 billion by 2032, registering a CAGR of 3.8% during the forecast period. Asia Pacific emerged as the leading regional market, accounting for 45.05% of the global share in 2023.

The growing versatility of hydrogen peroxide across multiple industries is a key factor driving market expansion. It is extensively used in pulp and paper production, chemical manufacturing, textiles, water treatment, home care products, cosmetics, and various specialty sectors, including food and beverages, electronics, and pharmaceuticals. To capitalize on these opportunities, major market players are actively investing in capacity expansion. For example, in July 2019, Solvay S.A. increased its production capacity across Belgium, Germany, Finland, and the Middle East to meet the rising demand from customers across the Europe, Middle East, and Africa (EMEA) region.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/hydrogen-peroxide-market-103920

Key Market Drivers

1. Growing Demand in Pulp and Paper Industry

Hydrogen peroxide is a key bleaching agent in the pulp and paper industry. The growing demand for recycled paper and sustainable bleaching processes has significantly boosted its consumption globally.

2. Expansion in Wastewater Treatment Applications

Rising concerns about water pollution and stringent environmental regulations have increased the use of hydrogen peroxide for wastewater treatment. It helps in the oxidation of pollutants and enhances water purification efficiency.

3. Increasing Use in the Healthcare and Food Sectors

The compound’s strong disinfectant and sterilizing properties make it a preferred choice in healthcare facilities and food processing industries, particularly after the COVID-19 pandemic.

4. Rising Focus on Green Chemistry

As industries shift toward sustainable and non-toxic chemical solutions, hydrogen peroxide’s environmentally friendly profile positions it as a preferred alternative to chlorine-based oxidants.

Market Segmentation

By Grade

<5% Hydrogen Peroxide

35% Hydrogen Peroxide

50% Hydrogen Peroxide

Others

By Application

Pulp & Paper

Textiles

Chemicals

Water & Wastewater Treatment

Electronics

Healthcare

Food Processing

Others

By Region

North America: Driven by strong industrial and healthcare applications in the U.S. and Canada.

Europe: Growth supported by stringent environmental policies and the adoption of green chemicals.

Asia Pacific: Dominates the market due to large-scale paper manufacturing and textile industries in China, India, and Japan.

Latin America & Middle East & Africa: Emerging markets driven by growing industrialization and infrastructure development.

Regional Insights

Asia Pacific holds the largest share of the global hydrogen peroxide market, accounting for over XX% in 2024 , due to robust demand from the pulp & paper and chemical sectors. China remains the leading producer and consumer, supported by favorable government policies and low production costs. North America and Europe are expected to witness steady growth driven by sustainability trends and wastewater treatment initiatives.

Key Market Players

Leading companies in the hydrogen peroxide market include:

Solvay S.A.

Evonik Industries AG

Arkema S.A.

Mitsubishi Gas Chemical Company, Inc.

Taekwang Industrial Co., Ltd.

Kemira Oyj

OCI Company Ltd.

National Peroxide Limited

These players focus on capacity expansions, technological advancements, and eco-friendly production methods to strengthen their global footprint.

Recent Developments

Solvay expanded its hydrogen peroxide production capacity in Asia to meet rising demand from electronics and semiconductor industries.

Evonik introduced high-purity hydrogen peroxide grades for use in pharmaceuticals and food processing.

Arkema invested in sustainable hydrogen peroxide production technologies to reduce carbon emissions.

Information Source: https://www.fortunebusinessinsights.com/hydrogen-peroxide-market-103920

The hydrogen peroxide market is projected to witness substantial growth by 2032 due to increased adoption in environmental applications, healthcare sterilization, and green chemical manufacturing. The trend toward sustainable industrial processes and advanced oxidation technologies (AOT) will further drive market expansion.

The global hydrogen peroxide market is set for steady growth through 2032, supported by its wide-ranging applications and eco-friendly benefits. As industries prioritize sustainable and efficient chemical solutions, hydrogen peroxide will continue to play a pivotal role in achieving cleaner and greener industrial operations.

KEY INDUSTRY DEVELOPMENTS

- January 2024: Solvay and Huatai announced plans to expand their hydrogen peroxide production capacity in China. The decision to expand their production capacity was taken considering the growing demand for hydrogen peroxide in the photovoltaic sector, where it is used as a cleaning agent in the production of photovoltaic cells. As a part of the expansion plan, the joint venture aims to produce 48,000 tons/year of photovoltaic-grade hydrogen peroxide by 2025.

Posted in: Business

| 0 comments

The global graphite market is witnessing significant growth due to rising demand from electric vehicles (EVs), renewable energy storage, and industrial applications. Graphite, known for its exceptional electrical conductivity, lubricity, and high-temperature stability, is a crucial material in several modern technologies, including lithium-ion batteries, steelmaking, and refractories.

Market Overview

According to Fortune Business Insights, The global graphite market was valued at USD 7.80 billion in 2024 and is anticipated to expand from USD 8.32 billion in 2025 to USD 13.35 billion by 2032, registering a CAGR of 6.9% during the forecast period. Asia Pacific held the largest share of 56.02% in 2024, driven by robust industrial activity and strong demand for electric vehicle (EV) batteries. Additionally, the U.S. graphite market is expected to experience substantial growth, reaching approximately USD 1,964.7 million by 2032, supported by the increasing adoption of battery-powered vehicles.

Graphite is a lightweight, naturally soft material that exhibits both metallic and nonmetallic characteristics, making it suitable for a wide range of industrial applications. Its metallic traits include excellent thermal and electrical conductivity, while its nonmetallic attributes—such as chemical inertness, corrosion resistance, high-temperature stability, and lubricity—enhance its versatility. With a melting point of 3,927°C, graphite is extensively used in industries that demand materials capable of withstanding extreme temperatures.

Natural and synthetic graphite are both widely used — natural graphite primarily in batteries and refractories, while synthetic graphite finds applications in electrodes, anodes, and industrial uses.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/graphite-market-105322

Key Market Drivers

1. Rising Electric Vehicle Production

Graphite plays a critical role in lithium-ion batteries, serving as the dominant anode material. With global EV sales surging, demand for battery-grade graphite is expected to increase exponentially.

2. Expanding Steel Industry

The steel industry continues to be a major consumer of graphite electrodes used in electric arc furnaces (EAF). The shift toward electric steelmaking supports the expansion of the graphite market.

3. Renewable Energy Storage Growth

Graphite’s use in energy storage systems and grid-scale batteries is boosting its market prospects, particularly with governments supporting renewable energy integration.

Market Segmentation

By Type: Natural Graphite, Synthetic Graphite

By Application: Refractories, Batteries, Lubricants, Foundry, Others

By End-Use Industry: Automotive, Metallurgy, Electronics, Energy, Others

By Region: North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Regional Insights

Asia Pacific

Asia Pacific dominates the global graphite market due to abundant raw material availability, growing steel production, and rapid EV adoption in China, Japan, and South Korea. China remains the world’s largest producer and exporter of graphite.

North America

The U.S. is focusing on establishing domestic graphite supply chains to reduce dependency on imports, especially for EV battery manufacturing.

Europe

European countries are investing heavily in gigafactories and sustainable materials to support the EV transition, creating strong demand for both natural and synthetic graphite.

LIST OF KEY COMPANIES PROFILED:

- AMG (Germany)

- Asbury Carbons (U.S.)

- Eagle Graphite (Canada)

- Grafitbergbau Kaisersberg GmbH (Austria)

- Imerys S.A. (France)

- Stoker Concast Pvt. Ltd. (India)

- BTR NEW Material Group Co., Ltd. (China)

- Nacional de Grafite (Brazil)

- SGL Carbon (Germany)

- Mineral Commodities Ltd. (Australia)

- Superior Graphite (U.S.)

- Tirupati Carbons & Chemicals Pvt. Ltd. (India)

These players focus on expanding production capacity, forming strategic partnerships, and developing advanced graphite materials for high-performance applications.

Future Outlook

The graphite market outlook remains highly positive, supported by:

Increasing lithium-ion battery demand

Green energy transition policies

Emerging graphite recycling and synthetic production technologies

The graphite market is poised for robust growth through 2032, fueled by technological advancements and the global push for sustainable and electric mobility. Companies investing in graphite processing and battery-grade production are expected to gain a competitive edge in this rapidly evolving industry.

Information Source: https://www.fortunebusinessinsights.com/graphite-market-105322

KEY INDUSTRY DEVELOPMENTS:

- July 2023: Graphite One Inc. Company announced that the company’s wholly owned subsidiary, Graphite One (Alaska), Inc., was awarded USD 37.5 million in technology investment agreement grant by the U.S. Department of Defense (DoD). Through this investment fund, DoD is planning to build the necessary production capacity and supply of graphite materials to meet the growing demand for graphite battery anodes for electric vehicles and other energy storage applications.

- June 2023: Superior Graphite, one of the leading manufacturers, announced its plan to construct a new anode materials facility with an investment of USD 180 million. The move will enable the company to meet the rising demand for its product from electronic vehicles and energy storage industries in Europe and North America.

Posted in: Business

| 0 comments

Green Building Materials Market Analysis Report, Growth Drivers, and Forecast 2032

By ameliasss, 2025-10-28

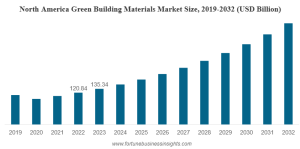

According to Fortune Business Insights, The global green building materials market was valued at USD 422.27 billion in 2023 and is expected to expand from USD 474.21 billion in 2024 to USD 1,199.52 billion by 2032, registering a CAGR of 12.3% during the forecast period. North America led the market in 2023, accounting for 32.05% of the global share. In the U.S., the market is projected to experience substantial growth, reaching approximately USD 289.50 billion by 2032, fueled by rising demand across residential, commercial, industrial, and infrastructure sectors—particularly for roofing, insulation, and framing applications.

Green building materials are utilized to create environmentally responsible structures that minimize the depletion of non-renewable resources. Their integration into construction projects helps lower the ecological footprint by reducing the impact associated with material extraction, manufacturing, transportation, installation, and end-of-life processes such as recycling or disposal. Owing to these advantages, green building materials are increasingly replacing traditional construction materials as the preferred sustainable alternative.

Green building materials, also known as sustainable construction materials, are designed to reduce environmental impact by improving energy efficiency, minimizing waste, and promoting the use of renewable resources. These materials include recycled steel, bamboo, insulation made from renewable fibers, low-VOC paints, solar panels, and smart glass.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/green-building-materials-market-102932

Key Market Drivers

Rising Environmental Awareness

Governments and organizations worldwide are implementing green building codes and certifications such as LEED, BREEAM, and IGBC , driving demand for eco-friendly materials.

Government Initiatives & Incentives

Incentive programs, tax benefits, and subsidies for green construction projects are fueling market expansion, particularly in North America, Europe, and Asia-Pacific .

Energy Efficiency Demands

The construction sector accounts for nearly 40% of global energy consumption. Green materials that enhance insulation and energy savings are increasingly in demand.

Corporate Sustainability Goals

Real estate developers and corporates are adopting green construction to meet ESG (Environmental, Social, and Governance) standards and reduce operational costs.

Market Segmentation

By Type:

Structural Materials (Bamboo, Recycled Steel, Wood)

Interior Materials (Low-VOC Paints, Flooring, Panels)

Exterior Materials (Roofing, Cladding)

Solar Products & Smart Glass

By Application:

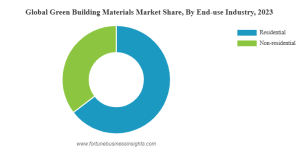

Residential

Commercial

Industrial

Institutional

Regional Insights

North America dominates the green building materials market, supported by strong sustainability regulations and high LEED certification adoption in the U.S. and Canada.

Europe follows closely with initiatives such as the European Green Deal , promoting zero-emission buildings.

Asia-Pacific is the fastest-growing region due to rapid urbanization, smart city projects, and rising construction in countries like China, India, and Japan .

Key Industry Players

Leading companies operating in the green building materials market include:

BASF SE

Holcim Ltd

Saint-Gobain S.A.

Kingspan Group

CEMEX S.A.B. de C.V.

Sika AG

These companies are focusing on innovation, product launches, and partnerships to expand sustainable product portfolios.

The future of the green building materials market looks promising, driven by the global push toward net-zero carbon buildings and sustainable urban infrastructure . The integration of AI, IoT, and smart construction technologies is expected to further enhance energy efficiency and building performance.

The Green Building Materials Market is set to play a pivotal role in shaping the sustainable cities of tomorrow. With strong government backing, growing awareness of environmental conservation, and technological advancements, the market will continue its robust growth trajectory through 2032 .

Information Source: https://www.fortunebusinessinsights.com/green-building-materials-market-102932

KEY INDUSTRY DEVELOPMENTS:

- January 2022: Binderholz GmbH, a subsidiary of the Austrian Binderholz Group, acquired BSW Timber Ltd. The company manufactures more than 1.2 million m3 of sawn timber annually. With this acquisition, Binderholz GmbH became Europe's largest sawmill and solid wood processor.

- April 2021: Lafarge Egypt, a member of LafargeHolcim, introduced Ecolabel cement for the first time in Egypt. This new product meets the company's green criteria and reduces the carbon footprint.

Posted in: Business

| 0 comments

The global aluminum forging market is witnessing substantial growth, driven by increasing demand from the automotive, aerospace, and industrial machinery sectors. The market size was valued at USD 49.63 billion in 2023 and is projected to grow from USD 52.41 billion in 2024 to USD 83.08 billion by 2032, exhibiting a CAGR of 6.0% during the forecast period.

Aluminum forging is a manufacturing process that enhances the strength, durability, and reliability of aluminum components by shaping them under high pressure. The process is widely used to produce high-performance parts for critical applications where lightweight yet strong materials are essential.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/aluminum-forging-market-109544

Key Market Drivers

1. Growing Demand in Automotive and Aerospace Industries

The rapid expansion of the automotive industry , particularly the shift toward electric and lightweight vehicles, has significantly boosted aluminum forging demand. Forged aluminum parts reduce overall vehicle weight, improving fuel efficiency and performance.

Similarly, in the aerospace sector , forged aluminum components are preferred for structural parts due to their high strength-to-weight ratio, corrosion resistance, and fatigue performance.

2. Focus on Lightweight and Sustainable Materials

As sustainability becomes a central theme across industries, aluminum forging offers an eco-friendly manufacturing alternative. Aluminum’s recyclability and lower carbon footprint compared to steel have made it an ideal choice for green manufacturing initiatives.

3. Technological Advancements in Forging Processes

The adoption of advanced forging techniques such as precision forging, isothermal forging, and computer-aided process simulation has enhanced productivity and reduced material wastage. These innovations have improved dimensional accuracy, making aluminum forging suitable for complex applications in defense, aerospace, and industrial machinery.

Market Segmentation

By Type

Open Die Forging

Closed Die Forging

Rolled Ring Forging

By Application

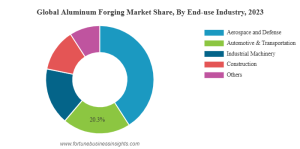

Automotive

Aerospace

Industrial Equipment

Defense

Others

By Region

North America: Dominates the global market due to strong aerospace and defense manufacturing base.

Europe: Major growth driven by sustainable automotive production and technological innovation.

Asia Pacific: Expected to exhibit the fastest growth due to expanding automotive manufacturing in China, India, and Japan.

Regional Insights

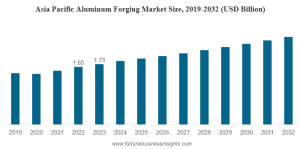

Asia Pacific held a significant share in 2023 and is projected to continue its dominance through 2032. The region’s large-scale automotive production, coupled with rapid industrialization, supports market expansion. China and India are the leading contributors, with increasing investments in lightweight manufacturing and export-oriented production.

North America is another crucial market, supported by advanced aerospace production in the U.S. and strong demand for high-performance materials. The region’s technological leadership in forging processes also supports growth.

Competitive Landscape

The aluminum forging market is moderately fragmented, with leading players focusing on strategic expansions, mergers, and product innovations. Key companies are investing in automation and digital forging technologies to enhance precision and sustainability.

Major Companies in the Aluminum Forging Market Include:

Arconic Corporation

Otto Fuchs KG

Bharat Forge Limited

thyssenkrupp AG

CFS Forge

Anchor Harvey Components

KOBELCO

Alcoa Corporation

Trenton Forging

Recent Developments

Arconic Corporation expanded its forged components business to support growing demand from EV manufacturers.

Bharat Forge Limited announced investments in green forging technologies to reduce emissions and energy consumption.

Otto Fuchs KG introduced new high-strength aluminum alloy forgings for aerospace applications.

Information Source: https://www.fortunebusinessinsights.com/aluminum-forging-market-109544

Future Outlook

The future of the aluminum forging market looks promising, with continuous advancements in material science and forging technologies. Increasing adoption in EV manufacturing , defense modernization, and renewable energy infrastructure will further accelerate market expansion.

As industries move toward lightweight, energy-efficient, and recyclable materials, aluminum forging will remain a vital process supporting global sustainability goals.

The aluminum forging market is set to grow steadily over the next decade, driven by technological innovation, sustainability initiatives, and rising industrial applications. With strong demand across automotive, aerospace, and industrial sectors, manufacturers are focusing on enhancing production efficiency and forging capabilities to meet evolving market needs.

Posted in: Business

| 0 comments

Airless Packaging Market Future Outlook and Revenue Growth Predictions Till 2032

By ameliasss, 2025-10-27

The global airless packaging market is witnessing robust growth driven by rising demand for innovative, sustainable, and contamination-free packaging solutions across various industries. Airless packaging is designed to protect sensitive formulations, prevent oxidation, and enhance product shelf life — making it highly popular in cosmetics, personal care, pharmaceuticals, and food industries.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/airless-packaging-market-106855

Market Overview

Airless packaging systems use a non-pressurized vacuum mechanism that dispenses products without allowing air to enter the container. This ensures maximum product usage, reduced waste, and superior protection against external contamination. The increasing preference for premium skincare and cosmetic products has been one of the primary factors fueling the demand for airless packaging.

Key Market Drivers

Growing Beauty and Personal Care Industry

The global beauty sector’s rapid expansion is a major catalyst for the airless packaging market. Consumers are increasingly opting for high-quality, hygienic, and sustainable packaging that preserves the integrity of cosmetic formulas.

Sustainability and Eco-friendly Packaging Trends

Manufacturers are focusing on recyclable and refillable airless packaging materials, aligning with global sustainability goals. Bio-based plastics and recyclable PET and PP are gaining traction among eco-conscious brands.

Rising Demand from Pharmaceuticals

The pharmaceutical industry is adopting airless dispensing systems to protect sensitive formulations like serums, gels, and lotions from contamination and ensure accurate dosage.

Technological Innovations

Companies are investing in smart and digital packaging solutions — such as 3D printing and integrated sensors — to improve consumer convenience and traceability.

Segmentation Insights

By Packaging Type: Bottles, Jars, Tubes, and Others

By Material: Plastic, Glass, and Metal

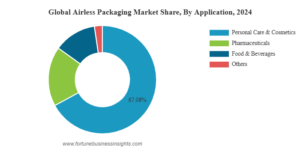

By End-use Industry: Cosmetics & Personal Care, Pharmaceuticals, Food & Beverages, and Household Products

Among these, plastic airless packaging holds the largest market share due to its lightweight, cost-effectiveness, and design flexibility. However, glass-based packaging is increasingly preferred for luxury and premium products.

Regional Analysis

North America : Dominates the airless packaging market due to strong demand for skincare and cosmetic innovations.

Europe : Shows significant growth with strict regulations promoting eco-friendly packaging materials.

Asia Pacific : Expected to register the fastest growth rate, driven by the booming beauty and personal care industry in countries such as China, Japan, and South Korea.

Competitive Landscape

Leading companies in the airless packaging market focus on product innovation, sustainable materials, and strategic collaborations to enhance market presence. Key players are investing in advanced dispensing systems and customizable designs to meet brand requirements and improve user experience.

Prominent manufacturers include:

AptarGroup, Inc.

Silgan Holdings Inc.

Quadpack Industries

Albea Group

Raepak Ltd.

HCP Packaging

Future Outlook

The airless packaging market is poised for steady expansion over the next decade, driven by consumer preference for sustainable, hygienic, and user-friendly packaging. The integration of digital technologies, biodegradable materials, and innovative dispensing systems will shape the future of this industry.

The global airless packaging market is evolving rapidly with growing sustainability concerns and technological advancements. With expanding applications across cosmetics, pharmaceuticals, and food sectors, the market presents lucrative opportunities for manufacturers and investors alike through 2032.

Information Source: https://www.fortunebusinessinsights.com/airless-packaging-market-106855

KEY INDUSTRY DEVELOPMENTS:

-

February 2023 – Quadpack declared the launch of a new refillable airless pen, Light Me Up. The refillable airless pen has several tips and can be utilized in both the skincare and makeup sectors. The refill system is also convenient and intuitive.

- November 2022 – Embelia introduced a new and refillable version of the Baia pouch airless system. The new airless system was manufactured in partnership with Lablabo, an expert in pouch airless packaging solutions.

Posted in: Business

| 0 comments

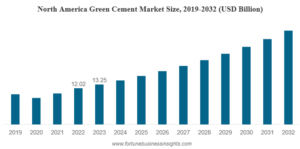

According to Fortune Business Insights, The global green cement market was valued at USD 35.65 billion in 2023 and is expected to grow from USD 39.32 billion in 2024 to USD 83.28 billion by 2032, registering a CAGR of 9.9% during the forecast period. North America led the global market with a 37.17% share in 2023. In the U.S., the green cement market is anticipated to witness substantial growth, reaching approximately USD 28.89 billion by 2032, fueled by the increasing adoption of sustainable cement alternatives in both residential and non-residential construction projects.

Green cement is an eco-friendly alternative to conventional cement, primarily produced using industrial by-products such as blast furnace slag and fly ash. Its production process is highly energy-efficient, as leading manufacturers employ advanced technologies to minimize carbon emissions. As per JK Lakshmi Cement Ltd., the use of green cement in construction can help reduce carbon footprints by up to 40%, making it a crucial component of sustainable building practices.

The global green cement market is witnessing strong growth as the construction industry increasingly adopts sustainable materials to reduce carbon emissions. Green cement, an eco-friendly alternative to traditional Portland cement, is produced using industrial waste such as fly ash, slag, and recycled aggregates. This shift supports global efforts toward carbon neutrality and sustainable infrastructure development.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/green-cement-market-107251

Market Overview

The green cement market is projected to experience substantial expansion from 2024 to 2032. Rising environmental awareness, stringent government regulations on carbon emissions, and growing investment in green infrastructure projects are key drivers fueling market growth. Increasing urbanization and demand for energy-efficient buildings further accelerate adoption across residential, commercial, and industrial sectors.

Key Market Drivers

1. Growing Focus on Sustainability and Carbon Reduction

The construction sector is one of the largest contributors to global CO₂ emissions. Green cement reduces carbon output by up to 30–40% compared to conventional cement, aligning with global sustainability goals such as the Paris Agreement. Governments and corporations are actively promoting low-carbon materials to meet green building certification standards such as LEED and BREEAM.

2. Rising Demand in Infrastructure Development

Massive infrastructure projects in emerging economies—such as smart cities, transportation networks, and renewable energy plants—are propelling demand for sustainable building materials. Green cement’s durability and low environmental impact make it an ideal choice for large-scale construction.

3. Technological Innovations and Product Advancements

Continuous R&D has led to innovative formulations of green cement incorporating materials like geopolymers, rice husk ash, and silica fume. These advancements enhance product performance while minimizing clinker usage, further lowering emissions and energy consumption during production.

Market Segmentation

By Type:

Fly Ash-Based Cement

Slag-Based Cement

Recycled Aggregate Cement

Others (Geopolymer Cement, Limestone Calcined Clay Cement, etc.)

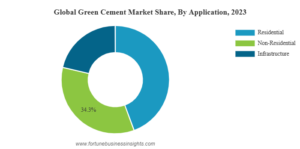

By Application:

Residential

Non-Residential (Commercial, Industrial)

Infrastructure (Roads, Bridges, Dams, etc.)

By Region:

North America: Driven by strict environmental policies and green building initiatives.

Europe: Leading in eco-friendly construction standards and carbon-neutral targets.

Asia Pacific: Expected to dominate the market, fueled by rapid urbanization in China, India, and Southeast Asia.

Latin America and Middle East & Africa: Emerging markets showing growing awareness and adoption of sustainable materials.

Regional Insights

Asia Pacific holds the largest market share owing to robust construction activities and government-led sustainability programs. India and China are heavily investing in green infrastructure, supported by public-private partnerships.

Europe continues to be a pioneer in adopting sustainable construction materials, backed by stringent EU environmental regulations.

North America is seeing increased adoption due to corporate ESG commitments and government incentives for green buildings.

Key Industry Players

Leading companies in the global green cement market are focusing on strategic mergers, partnerships, and sustainable manufacturing technologies to strengthen their positions. Major players include:

LafargeHolcim Ltd.

HeidelbergCement AG

CEMEX S.A.B. de C.V.

CRH plc

UltraTech Cement Ltd.

Calera Corporation

Anhui Conch Cement Co., Ltd.

These players are actively investing in carbon capture technologies, alternative fuel use, and waste material integration to meet sustainability targets.

The future of the green cement market looks promising as governments, corporations, and consumers increasingly prioritize sustainability. The demand for carbon-neutral buildings, coupled with the growing use of recycled materials in cement production, will continue to propel market growth through 2032.

The green cement market is set to redefine the global construction industry by offering sustainable, durable, and cost-effective alternatives to traditional cement. As eco-conscious construction practices become the norm, innovations in green cement manufacturing will play a pivotal role in achieving a low-carbon future.

Information Source: https://www.fortunebusinessinsights.com/green-cement-market-107251

KEY INDUSTRY DEVELOPMENTS:

- November 2023: Heidelberg Cement launched the low-carbon cement brand to reduce greenhouse gas emissions during the cement manufacturing and mixing process.

- October 2022 : JSW Cement planned to invest USD 390 million to begin an integrated green cement production facility in Madhya Pradesh and a split grinding unit in Uttar Pradesh. The proposed investment includes a 2.5 MTPA grinding capacity, 15 MW Waste heat recovery system, and 2.5 MTPA clinker capacity.

Posted in: Business

| 0 comments

According to Fortune Business Insights, The global neopentyl glycol market was valued at USD 1,327.7 million in 2024 and is anticipated to increase from USD 1,407.1 million in 2025 to USD 2,219.1 million by 2032, registering a CAGR of 6.7% during the forecast period. Asia Pacific held the largest share of 44.16% in 2024, leading the global market.

Neopentyl Glycol (NPG) is a multifunctional chemical widely used across diverse industries. It serves as a key raw material in the production of polyester resins, coatings, and lubricants. The market growth is primarily fueled by the increasing utilization of NPG in automotive coatings, powder coatings, and construction materials. Its superior durability, weather resistance, and environmentally friendly attributes make it a preferred choice for manufacturers. This growth is driven by rising demand across coatings, resins, lubricants, and plasticizers industries, supported by expanding automotive and construction activities worldwide.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/neopentyl-glycol-market-110106

Market Dynamics

Key Growth Drivers

Increasing demand from coatings and resins:

Neopentyl glycol is a vital component in polyester and alkyd resins used for automotive, industrial, and powder coatings. Its ability to enhance chemical resistance, hardness, and weather durability fuels its consumption in these applications.

Automotive industry expansion:

With rising global automobile production and demand for durable, lightweight coatings, NPG usage continues to grow in automotive surface treatments and high-performance coatings.

Industrial lubricants and plasticizers:

NPG-derived esters are widely used as lubricants and plasticizers, improving performance and longevity in various industrial products.

Technological advancements and sustainability:

Manufacturers are focusing on developing environmentally friendly NPG production methods and bio-based derivatives to meet regulatory standards and reduce environmental impact.

Market Segmentation

By Grade

Flakes

Molten

Slurry

Each grade serves specific industrial requirements, depending on storage, transportation, and processing needs.

By Application

Coatings & Resins

Plasticizers

Lubricants

Others

Among these, coatings and resins hold the largest market share due to NPG’s extensive use in producing durable and weather-resistant paints.

By End-Use Industry

Automotive

Construction

Electronics

Pharmaceutical

Others

The automotive and construction sectors lead global consumption, supported by infrastructure growth and vehicle production.

Regional Insights

Asia Pacific

Asia Pacific dominates the Neopentyl Glycol market, driven by large-scale manufacturing activities in China, India, Japan, and South Korea . Growing industrialization, automotive output, and coating applications contribute to strong regional demand.

Europe

Europe represents a mature market supported by well-established coating and resin industries. Stringent environmental regulations are also encouraging the adoption of advanced and sustainable NPG-based formulations.

North America

The North American market benefits from high demand in industrial coatings, automotive refinishing, and specialty chemicals, with the U.S. as a key contributor.

Rest of the World

Emerging economies in Latin America and the Middle East are witnessing gradual growth in NPG usage, driven by construction and industrial developments.

Competitive Landscape

Leading market participants are focusing on:

LIST OF KEY NEOPENTYL GLYCOL COMPANIES PROFILED

- LG Chem (South Korea)

- Perstorp Holding AB (Sweden)

- BASF (Germany)

- OQ Chemical GmbH (Germany)

- MITSUBISHI GAS CHEMICAL COMPANY, INC. (Japan)

- Eastman Chemical Company (U.S.)

- Zibo Ruibao Chemical Co., LTD. (China)

- Ataman Chemicals (Istanbul)

- The Chemical Company (U.S.)

- DHALOP CHEMICALS (India)

Companies are also pursuing mergers and strategic collaborations to enhance market presence and product portfolios.

Opportunities and Challenges

Opportunities

Rising adoption of powder coatings in the automotive and construction industries.

Growing trend toward green chemistry and sustainable production routes.

Increasing investments in emerging markets for coating and lubricant applications.

Challenges

Fluctuations in raw material prices affecting production costs.

Environmental regulations related to chemical manufacturing.

Competition from alternative polyols in certain applications.

Key Market Highlights

2024 Market Size: USD 1,327.7 million

2025 Market Value: USD 1,407.1 million

2032 Forecast: USD 2,219.1 million

CAGR (2025–2032): 6.7%

Dominant Region: Asia Pacific

Top Applications: Coatings & Resins, Lubricants, Plasticizers

The Neopentyl Glycol Market is poised for steady growth through 2032, fueled by expanding applications in coatings, automotive, and construction industries. Its chemical stability, resistance to oxidation, and compatibility with eco-friendly technologies position it as a key material for next-generation coatings and resins.

Manufacturers investing in bio-based innovations , capacity expansions , and regional market development are likely to capture significant opportunities during the forecast period.

Information Source: https://www.fortunebusinessinsights.com/neopentyl-glycol-market-110106

KEY INDUSTRY DEVELOPMENTS

- July 2023 : Zhejiang Guanghua Technology Co., Ltd. and BASF entered a letter of intent to provide Neopentyl glycol from the Zhanjiang Verbund site to KHUA. This collaboration will help BASF cater to the increasing demand for low-emission powder coatings in the Asia Pacific region and China.

- October 2022: BASF invested in a new Neopentyl glycol in China with a production capacity of 80,000 metric tons. The new plant will boost BASF’s Neopentyl glycol capacity to 335,000 metric tons annually. The new plant will mainly cater to the growing demand for powder coatings in China.

Posted in: Business

| 0 comments

Caustic Soda Market Industry Insights, Trends, Size & Forecast to USD 55,557.7 Million by 2027

By ameliasss, 2025-10-17

The global caustic soda market was valued at USD 44,959.2 million in 2019 and is expected to grow to USD 55,557.7 million by 2027, registering a CAGR of 3.1% during the forecast period. Asia Pacific emerged as the leading region, accounting for 56.23% of the total market share in 2019.

Caustic soda serves as a fundamental raw material in the production of various essential products, including plastics, pharmaceuticals, and water treatment additives. It is produced through the electrolysis of sodium chloride solution using technologies such as diaphragm cells or membrane cells. Major end-use industries driving demand for caustic soda include pulp and paper, detergents, alumina, oil and gas, textiles, and chemicals. The increasing demand for caustic soda across diverse industries such as paper & pulp, textiles, chemicals, and water treatment is expected to fuel market expansion globally.

Key Market Insights

Caustic soda, also known as sodium hydroxide (NaOH), is a vital industrial chemical used in a wide range of manufacturing processes. It serves as an essential raw material for producing alumina, soaps, detergents, and petroleum products. The growing demand for these end-use applications, coupled with expanding industrialization in emerging economies, drives the market’s steady growth trajectory.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/caustic-soda-market-104711

Driving Factors

Rising Demand from the Pulp and Paper Industry

Increasing consumption of paper-based products and packaging materials boosts caustic soda use for pulp digestion and paper bleaching.

Expanding Chemical Manufacturing Sector

Caustic soda acts as a key reactant in producing various chemicals, including solvents, plastics, and synthetic fibers, enhancing its market value.

Growing Application in Water Treatment

Rapid urbanization and rising concerns about clean water availability are increasing the adoption of caustic soda for pH regulation and water purification processes.

Restraining Factors

Despite positive growth prospects, fluctuations in raw material prices and stringent environmental regulations on chemical production may hinder market expansion to some extent.

Market Segmentation

By Form: Lye, Flake, Pellet

By Application: Alumina, Pulp & Paper, Organic Chemicals, Inorganic Chemicals, Textiles, Water Treatment, Others

By Region: North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Regional Insights

Asia Pacific dominated the caustic soda market in 2023, holding over 50% of the global share . The region’s strong industrial base in China, India, and Japan supports the growth of paper, textile, and alumina industries. Meanwhile, North America and Europe show steady demand due to the chemical and manufacturing sectors' stability and growing water treatment applications.

Competitive Landscape

Leading companies are investing in technological advancements and sustainable production methods to minimize environmental impact and enhance product efficiency. Major players operating in the global caustic soda market include:

- Olin Corporation (Clayton, Missouri, United States)

- Tata Chemicals Limited (India)

- Aditya Birla Chemicals (India) Limited (India)

- Gujarat Alkalies and Chemical Limited (India)

- Occidental Petroleum Corporation (OXY) (Houston, Texas, United States)

- Formosa Plastics Corporation (Taiwan)

- PPG Industries (Pittsburgh, Pennsylvania, United States)

- Xinjiang Zhongtai Chemical Co., Ltd. (China)

- Hanwha Chemical (South Korea)

- Brenntag North America, Inc. (North America)

Strategic mergers, capacity expansions, and innovations in membrane cell technology are helping these companies strengthen their market position.

Information Source: https://www.fortunebusinessinsights.com/caustic-soda-market-104711

Future Outlook

The caustic soda market is poised for steady growth over the next decade, driven by ongoing industrialization, the shift toward sustainable manufacturing, and consistent demand from key downstream sectors. The integration of green chemistry and energy-efficient production methods will further shape the market dynamics through 2032.

Conclusion:

The Caustic Soda Market continues to show promising potential, supported by growing applications in manufacturing and environmental sectors. With sustainability becoming a key focus, market players are expected to emphasize cleaner production processes and efficient resource utilization, ensuring long-term market stability and profitability.

KEY INDUSTRY DEVELOPMENTS:

- In May 2021, Olin Corporation announced the reduction in the Chlor alkali production capacity by shutting down 20% of its diaphragm grade at its Plaquemine facility.

- In January 2021 , the GACL-NALCO Alkalies & Chemicals Ltd (GNAL) delayed the commissioning of the new caustic soda production line to August 2021. The production facility is situated at Dahej and has a production capacity of 266667 tons/year for caustic soda.

Posted in: Business

| 0 comments