Category: Business

Tinplate Packaging Market Share and USD 2.65 Billion Growth Forecast 2025-2032

By ameliasss, 2025-09-03

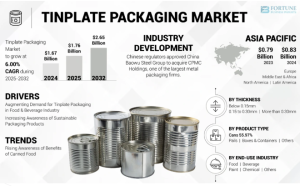

According to Fortune Business Insights, The global tinplate packaging market was valued at USD 1.67 billion in 2024 and is expected to expand steadily, reaching USD 1.76 billion in 2025 and further advancing to USD 2.65 billion by 2032. This reflects a compound annual growth rate (CAGR) of 6.00% over the forecast period. In 2024, Asia Pacific led the market, accounting for 49.70% of the global share. Meanwhile, the U.S. tinplate packaging market is anticipated to experience substantial growth, projected to achieve USD 425.71 million by 2032, fueled by the rising demand for packaged and processed food products.

Tinplate is a product made from steel that offers a lustrous and sturdy appearance to a product packaged with this item. The material is used to pack canned beverages, foods, paints, and cosmetics. The growing demand for sustainable packaging solutions will help this market grow. The material’s ability to withstand high pressure, temperature, and physical damage during the manufacturing process and transportation is fueling the growth of this market. Furthermore, high recyclability, durability, and easy printability are some of the factors driving the product’s sales.

Fortune Business Insights™ displays this information in a report titled, "Tinplate Packaging Market, 2025-2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/tinplate-packaging-market-109390

LIST OF KEY COMPANIES PROFILED IN THE REPORT:

- CPMC Holdings Limited (China)

- Tata Steel (India)

- AJ Packaging Limited (India)

- ColepPackaging (Portugal)

- ArcelorMittal (Luxembourg)

- Toyo Kohan Co., Ltd. (Japan)

- United States Steel Corporation (U.S.)

- Crown (U.S.)

- Italtin S.r.l. (Italy)

- Mauser Packaging Solutions (U.S.)

- Nampak Ltd. (South Africa)

Segmentation:

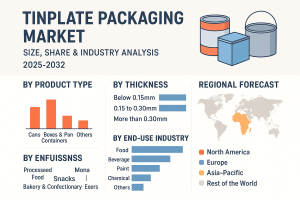

Cans Dominate Market Due to Their Ease of Use

Based on product type, the market is segmented into cans, boxes & containers, pails, and others. The can segment is dominating the tinplate packaging market share as it offers a wide range of benefits, such as ease of use, durability, and sustainability.

Increasing Use in Several Industries Boosted Demand for Tinplate Sheets of 0.15-0.30mm Thickness

Based on thickness, the market is segmented into below 0.15mm, 0.15 to 0.30mm, and more than 0.30mm. Tinplate sheets in the thickness range of 0.15 to 0.30 mm dominate the market as they are lightweight and reduce the need for additional packaging materials, thereby increasing their use in several industries.

Food Industry Emerges as Major End-User Due to Supreme Preservation Properties of Tinplate Packaging

Based on end-use industry, the market is segmented into food [processed food, snacks, bakery & confectionary, edible oil, others], beverage [alcoholic, non-alcoholic], paint, chemical, and others. The food segment is dominating the market as tinplate packaging products are widely used in this industry due to their excellent food preservation features.

With respect to region, the market covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report has conducted a detailed study of the market and highlighted several critical areas, such as leading product types and key market players. It has also focused on the latest market trends and the key industry developments. Apart from the aforementioned factors, the report has given information on many other factors that have helped the market grow.

Drivers and Restraints:

Rising Demand for Tinplate Packaging in Food & Beverage Industry to Boost Market Growth

The adoption of tinplate packaging solutions is rising in the food & beverage sector as they offer a wide range of beneficial features, such as excellent food preservation properties. These properties prevent air, moisture, and other external factors from entering the food item, thereby protecting its quality and shelf life.

However, the high production costs associated with these packaging solutions will hinder the tinplate packaging market growth.

Regional Insights:

Asia Pacific Dominates Global Market Owing to High Consumption of Canned Foods

Asia Pacific held a dominant market share in 2023 as the region is witnessing strong growth in the sales of canned foods due to factors, such as rapid urbanization and rising disposable income of the population.

North America is the second-dominating region in the global market owing to the rising preference for processed foods.

Competitive Landscape:

Key Market Players to Offer Sustainable Packaging Solutions to Gain Strong Competitive Edge

The tinplate packaging market is quite competitive and fragmented, with a few companies leading the market’s growth. These firms are using a wide range of innovative technologies to develop sustainable packaging solutions. This move will help them strengthen their market position and expand their customer base.

Information Source: https://www.fortunebusinessinsights.com/tinplate-packaging-market-109390

Notable Industry Development:

February 2024 - Chinese regulators approved China Baowu Steel Group to acquire CPMC Holdings, which is one of the largest metal packaging firms. The acquisition will help China Baowu Steel Group increase its customer base in the metal canning industry and boost the firm’s profitability.

July 2023 - Tata Steel joined hands with its subsidiary company Tinplate Company of India to recycle tin cans to prevent the reuse of cans due to health and safety issues. Such initiatives will increase awareness among people and also set new standards for other competitors.

Packaging Waste Management Market Analysis by Service Type & Region 2025-2032

By ameliasss, 2025-09-02

According to Fortune Business Insights, The global packaging waste management market was valued at USD 92.19 billion in 2024 and is expected to grow to USD 96.53 billion in 2025, reaching USD 137.15 billion by 2032. This growth represents a CAGR of 5.15% over the forecast period. In 2024, Asia Pacific led the market, accounting for 31.45% of the total share.

The packaging waste management market covers the collection, sorting, recycling, recovery (including waste-to-energy), and safe disposal of post-consumer and post-industrial packaging materials such as paper & board, plastics, glass, metals, and bioplastics. Demand is being reshaped by circular-economy policies, brand-owner sustainability targets, and rapid growth in e-commerce that changes both the volume and composition of packaging waste. Across regions, governments are tightening regulations (EPR, landfill taxes, deposit return systems), while technology providers are scaling advanced sorting and chemical recycling to increase recovery rates and material quality.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/packaging-waste-management-market-112352

List of the Key Companies Profiled in the Report:

- Waste Mission (U.K.)

- BEWI (Austria)

- Frigorifico Allana Pvt. Ltd. (Austria)

- Bayer AG (Austria)

- ITENE (Austria)

- Merivaara Corporation (Austria)

- Greenbank Recycling Solutions (U.K.)

- Stevcon Packaging & Logistics Ltd (Austria)

- JBS (Austria)

- WM Intellectual Property Holdings, L.L.C. (U.S.)

- PreZero International (Austria)

- Affordable Waste Management Ltd. (Austria)

Key Market Drivers

Policy pressure & EPR : Extended Producer Responsibility (EPR) schemes shift end-of-life costs to producers, accelerating design-for-recycling and funding for collection/sorting infrastructure.

Corporate sustainability targets : FMCG, retail, and consumer brands are committing to higher recycled content and 100% recyclable packaging—creating stable demand for high-quality recyclate.

Surge in e-commerce : More secondary and tertiary packaging (corrugated, flexible plastics) increases volumes and complexity, pushing cities and haulers to adapt collection models.

Landfill/incineration constraints : Rising tipping fees and landfill scarcity in many markets make recovery more economical and politically favored.

Market Challenges

Economics of recycling : Volatile commodity prices and quality variability can make recycled feedstock less competitive versus virgin materials without policy support.

Collection & contamination : Mixed waste streams and low participation rates undermine material value and plant efficiency.

Fragmented regulations : Divergent rules across countries (and even states) complicate compliance for global brands and recyclers.

Difficult-to-recycle formats : Multi-layer films, dark plastics, and small-format items still pose technical and economic hurdles.

Market Segmentation

By Material

Paper & Paperboard

Plastics (PET, HDPE, LDPE/LLDPE, PP, PS, PVC, multi-layer/films)

Glass

Metals (Aluminum, Steel)

Bioplastics/Compostables

By Source

Residential (municipal)

Commercial & Industrial (retail, foodservice, manufacturing, logistics)

By Service

Collection & Transportation

Sorting/Material Recovery (MRF operations)

Recycling & Reprocessing (mechanical and chemical)

Energy Recovery (RDF, waste-to-energy)

Landfill & Other Disposal

Consulting & Compliance (EPR, ESG reporting)

By End Use of Recyclate

Food & Beverage Packaging

Personal Care & Household

Industrial & Logistics (pallets, straps, films)

Construction & Automotive (downstream uses for fibers, glass cullet, metals)

By Region

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Regulatory Landscape (What’s Shaping Demand)

EPR & Packaging Taxes : Funding for collection and MRF upgrades; eco-modulated fees reward recyclable designs.

Deposit Return Systems (DRS) : Raising PET, aluminum, and glass return rates and improving quality (low contamination).

Recycled Content Mandates : Minimum rPET/rHDPE content for beverage bottles and certain rigid/film applications.

Green Claims & Traceability : Stricter substantiation requirements drive investment in chain-of-custody and mass-balance systems.

Technology & Innovation Trends

AI-enabled sorting & robotics : Higher throughput, lower labor dependency, and improved purity levels.

Digital watermarks & markers : Enhancing identification of packaging types at MRF speed.

Chemical recycling (pyrolysis, depolymerization, solvent-based) : Targeting hard-to-recycle plastics to yield near-virgin monomers.

Advanced washing & de-inking : Upgrading recyclate quality for food-grade and high-performance use.

Closed-loop & reuse systems : Refillable packaging, reverse logistics, and durable containers for e-commerce and foodservice.

Biodegradable/compostable packaging : Scaling in targeted applications with appropriate organics collection and composting infrastructure.

Competitive Landscape

The market features a mix of global and regional players across the value chain:

Waste management & MRF operators : Waste Management, Republic Services, Veolia, SUEZ, REMONDIS, Biffa.

Technology & equipment providers : TOMRA, Pellenc ST, AMP Robotics (AI/robotics), Bollegraaf, Stadler (MRF lines).

Recyclers & reprocessors : Indorama Ventures (PET), ALPLA Recycling, Evergreen/CarbonLITE (rPET), Novelis (aluminum), Ardagh (glass).

Energy recovery & WtE : Covanta, EEW Energy from Waste.

Compliance & EPR organizations : PROs and stewardship bodies partnering with municipalities and brands.

Strategic Opportunities for Stakeholders

Design for recycling : Shift to mono-materials, eliminate problem additives, standardize labels (e.g., “widely recyclable”).

Invest in high-purity streams : DRS and curbside upgrades that deliver food-grade PET/HDPE and high-quality OCC.

Flexible packaging solutions : Scale film collection pilots, store drop-off, and chemical recycling feedstock supply.

Data & traceability : Implement digital product passports, batch-level analytics, and verifiable recycled content accounting.

Reuse ecosystems : Target high-frequency, closed environments (stadiums, campuses, QSR chains) to prove economics.

Outlook (2025–2032)

Higher recovery, better quality : Expect steady increases in PET, aluminum, and OCC capture; focus shifts to films and flexible plastics.

Policy-driven investment : EPR and recycled-content mandates sustain capex in MRF modernization, advanced reprocessing, and DRS expansion.

Consolidation & specialization : Larger operators acquire niche recyclers (e.g., films, food-grade PCR), while equipment makers bundle AI, robotics, and optical sorting as turnkey solutions.

Balanced portfolio of solutions : Mechanical recycling remains the backbone; chemical recycling scales selectively where economics and policy align; reuse systems grow in targeted channels.

Emerging markets leapfrog : With EPR funding and digital tools, APAC and parts of LATAM/MEA accelerate from low baselines to modernized systems.

Information Source: https://www.fortunebusinessinsights.com/packaging-waste-management-market-112352

KEY INDUSTRY DEVELOPMENTS

In December 2024, Bisleri International Pvt. Ltd, in collaboration with Sampurn(e)arth Environment Solutions Pvt. Ltd. and the Mineral Foundation of Goa, launches a Material Recovery Facility (MRF) Center in Harvalem, Goa. The facility is designed to handle 360 MT of plastic waste each year. Bisleri's 'Bottles for Change' program seeks to reduce plastic waste in landfills and foster a cleaner, more sustainable ecosystem in the area. The facility will mostly focus on promoting 100% plastic waste separation at the source, beginning with the Curchorem-Cacora area.

In October 2024, At the PPMA Show, Waste Mission, a prominent UK waste management firm, introduced its tailor-made Waste Management Portal. This cutting-edge platform is tailored exclusively for contracted clients, allowing them to handle their waste more efficiently and sustainably than ever while keeping them informed about waste streams, compliance, and ESG goals.

According to Fortune Business Insights, In 2018, the global cellulose market was estimated at USD 219.53 billion and is forecast to attain USD 305.08 billion by 2026, corresponding to a compound annual growth rate (CAGR) of 4.2% over the forecast period. North America dominated the market in 2018, holding a 28.91% share. The U.S. market is anticipated to register significant growth, reaching an estimated USD 88.01 billion by 2032, driven primarily by increased demand for cellulose-based applications in the paper and construction industries. Driven by applications across diverse industries, the market will exhibit considerable growth in the coming years. According to a report published by Fortune Business Insights, titled “ Cellulose Market Size, Share & Industry Analysis, By Derivative Type (Commodity Cellulose Pulp, Cellulose Fibers, Cellulose Ethers, Cellulose Esters, Microcrystalline Cellulose, Nano-cellulose, and Others), By End-Use Industry (Textile, Food, Chemical Synthesis, Pharmaceuticals, Construction, Paper & Pulp, Paints & Coatings, and Others), and Regional Forecast, 2025-2032 ”

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/cellulose-market-102062

Some of the leading companies that are operating in the global cellulose market are:

- Daicel Corporation

- Sigma Aldrich

- DuPont De Nemours Company

- Akzo Nobel

- Ashland inc.

- Celanese Corporation

- International Paper

- Fulida Group Holding Co., Ltd.

- Nylstar S.L.

- FiberVisions Corporation

- Invista

- Bracell

- Sigachi Industries Pvt. Ltd.

- FMC Biopolymer

Cellulose is a natural polymer made of glucose units linked together in a straight chain. Found in wood (40–45%) and plants (up to 90%), it is the most common solid material on Earth. It comes mainly from sources such as wood, cotton, flax, hemp, and jute. Cellulose is valued for its strength, water-loving nature, and ability to absorb moisture.

Cellulose is a pulp that is derived from plant sources. The substance possesses exceptional properties such as its hydrophile nature, good mechanical performance, and hygroscopic nature. These properties have led to applications across diverse industries, including chemical, textile, and food and beverages. Recent advancements in fabrication technologies have opened up a huge potential for the growth of the companies operating in this market. The shift of preference from petroleum-based products to sustainable resources will contribute to the growing demand for cellulose across the world. Moreover, availability of cellulose-originating products will lead to a wider product adoption, subsequently aiding the growth of the cellulose market in the coming years.

The report provides an in-depth analysis of the global cellulose market. It highlights the latest product launches and labels major innovations in the market. In addition to this, it states the impact of these products on the growth of the market. The competitive landscape has been discussed in detail and predictions are made with respect to leading companies and products in the coming years. Forecast values have been provided for the market for the period of 2019-2026. The factual figures have been obtained through trusted sources. Moreover, these predictions are made on the basis of extensive research analysis methods, coupled with the opinions of experienced market research professionals.

Increasing Number of Company Collaborations to Aid Growth

The report encompasses several factors that have constituted an increase in the cellulose market size in recent years. It has been observed that company collaborations are a growing trend among major companies across the world. In January 2020, The Anhui Guozhen Group announced that it has initiated a joint venture with Chemtex. The company plans to establish a large scale commercial plant in China for the production of cellulosic ethanol. The ethanol production will be centred around residues that are normally obtained from the agriculture industry. The plant will have an annual production capacity of 50 KT. Such a huge venture will not only benefit the country but will also have a direct impact on the growth of the overall cellulose market in the coming years.

Asia Pacific Accounts for a Dominating Market Share; Increasing Product Demand Across Diverse Industries to Aid Growth

The market is segmented on the basis of regional demographics into North America, Latin America, Europe, Asia Pacific, and the Middle East and Africa. Among these regions, Asia Pacific currently accounts for the highest cellulose market share. The widespread product applications across diverse industries, and the subsequent rise in the demand for these products will have a direct impact on the growth of the market in this region. Besides Asia Pacific, the market in North America will witness considerable growth in the coming years. As of 2018, the market in North America was worth USD 63.46 billion and this value is projected to rise further in the coming years, driven by product uses in the paper industry.

Information Source: https://www.fortunebusinessinsights.com/cellulose-market-102062

Key Industry Developments

- In January 2020, The Anhui Guozhen Group and Chemtex signed a joint venture to build a first full-scale commercial plant in China for cellulosic ethanol production from residues obtained from agriculture industry. Clariant Specialty Chemicals have granted a license for its sunliquid cellulosic ethanol technology to the joint venture. The plant is to be situated in Fuyang city in the Anhui province of China and is expected to have an annual capacity of 50 KT.

- In May 2019, Bracell announced launch of ‘Project Star’, an expansion plan to increase the production capacity of its pulp mill based in Lencois Paulista, Sao Paolo, Brazil, from 250 KT to 1500 KT by the end of 2021. The project is expected to reach an annual production capacity of 2000 KT pulp with the completion of the project, making them one of the largest pulp producer in the world.

Diethylene Glycol Market Rising Demand Across Industrial Applications 2025-2032

By ameliasss, 2025-09-01

According to Fortune Business Insights, The global diethylene glycol market was valued at USD 5.0 billion in 2024 and is anticipated to expand from USD 5.2 billion in 2025 to USD 6.8 billion by 2032, registering a CAGR of 3.9% during the forecast period. In 2024, Asia Pacific led the market, accounting for 61.4% of the overall share. The Diethylene Glycol (DEG) market is gaining momentum across various industries due to its versatile applications in resins, polyurethanes, plasticizers, coolants, and lubricants. DEG, a clear, hygroscopic, and odorless liquid, is primarily produced as a byproduct of ethylene oxide hydrolysis. Its demand is strongly influenced by the growth of construction, automotive, and textile industries, which are major consumers of resins and polyurethanes.

The global Diethylene Glycol market is projected to witness significant growth between 2025 and 2032, driven by rising consumption in coatings, adhesives, and plastics manufacturing. Additionally, DEG is widely used as a solvent and chemical intermediate, which enhances its importance in chemical processing.

List of Key Diethylene Glycol Players Profiled

- Mitsubishi Chemical Group Corporation (Japan)

- Reliance Industries Limited (India)

- Shell (U.K.)

- SABIC (Saudi Arabia)

- NIPPON SHOKUBAI CO., LTD. (Japan)

- BASF (Germany)

- China Petrochemical Corporation (Sinopec) (China)

- PETRONAS (Malaysia)

- MEGlobal (Kuwait)

- Junsei Chemical Co., Ltd. (Japan)

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/diethylene-glycol-market-113453

Key drivers include:

Expanding polyurethane and polyester resin industries .

Rising demand in construction, automotive, and packaging sectors .

Increasing application in unsaturated polyester resins (UPR) for reinforced plastics.

Widening use as a dehydrating agent in natural gas processing .

However, health hazards and toxicity concerns associated with DEG, along with strict regulatory guidelines, may hinder market expansion.

Diethylene Glycol (DEG) is a versatile, colorless, odorless, and water-soluble organic compound extensively utilized as a solvent, plasticizer, and chemical intermediate. One of the primary growth drivers for DEG is the expanding global polyester industry, where it plays a vital role in the production of unsaturated polyester resins used in coatings, adhesives, and composite materials.

With industries such as packaging, construction, and automotive increasingly adopting polyester-based products, the demand for DEG continues to accelerate. Beyond polyester applications, DEG is also widely employed in brake fluids, hydraulic systems, and cosmetics, further broadening its market scope. Demand is particularly strong in developing regions, where rapid industrialization and urbanization are fueling consumption.

The market is characterized by the presence of several major players, including Mitsubishi Chemical Group Corporation, SABIC, BASF, Sinopec, Reliance, and Shell, among others. Their diverse product portfolios and global reach ensure a competitive landscape and continuous innovation in DEG applications.

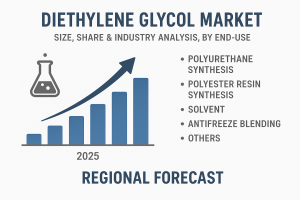

Market Segmentation

By Application:

Polyester Resins – A major segment, driven by demand in reinforced plastics, coatings, and adhesives.

Plasticizers – Used in flexible PVC production.

Polyurethanes – Expanding applications in construction and automotive.

Lubricants & Coolants – Growing adoption in industrial and automotive cooling systems.

Others – Gas dehydration, cosmetics, and chemical intermediates.

By End-use Industry:

Construction – Usage in UPR, polyurethanes, and adhesives.

Automotive – Lubricants, coolants, and resins.

Textile – Fiber processing and resin production.

Plastics & Packaging – Plasticizers and polymers.

Oil & Gas – Natural gas dehydration applications.

By Region:

Asia Pacific dominates the global DEG market, led by China, India, and Japan , due to strong industrial growth and expanding chemical manufacturing.

North America and Europe follow, with significant usage in automotive, plastics, and construction.

Middle East & Africa show potential growth in natural gas dehydration applications.

Market Trends

Increasing focus on eco-friendly and sustainable chemical processes .

Rising demand for lightweight plastics and resins in automotive and aerospace.

Expanding construction sector driving polyurethane and polyester resin demand.

Strategic capacity expansions and joint ventures by leading DEG producers.

Competitive Landscape

Key players in the Diethylene Glycol market include:

SABIC

Royal Dutch Shell

Dow Chemical Company

Reliance Industries Limited

LyondellBasell Industries

Formosa Plastics Corporation

These companies are focusing on R&D, partnerships, and product innovations to strengthen their market position.

The Diethylene Glycol market is set for robust growth between 2025 and 2032 , supported by its expanding applications in resins, polyurethanes, and plasticizers . Asia Pacific will continue to dominate, while technological advancements and regulatory compliance will shape the competitive dynamics of the market.

Information Source: https://www.fortunebusinessinsights.com/diethylene-glycol-market-113453

KEY INDUSTRY DEVELOPMENTS

- January 2024 – SABIC announced its decision to invest USD 6.5 billion to establish a petrochemical complex in China's Fujian province. This petrochemical complex will have the capability of producing ethylene glycol along with polyethylene, polypropylene and polycarbonate, among others.

- December 2023 – SABIC announced that they have signed a MoU with Scientific Design (SD) and Linde Engineering. As part of this collaboration, these companies will explore the opportunities to decarbonize ethylene oxide and ethylene glycol production.

Activated Carbon Market Latest Technological Advancements and Forecast 2025-2032

By ameliasss, 2025-09-01

According to Fortune Business Insights, The global activated carbon market was valued at USD 5.70 billion in 2024 and is anticipated to expand from USD 5.62 billion in 2025 to USD 10.04 billion by 2032, reflecting a CAGR of 8.7% over the forecast period. In 2024, Asia Pacific led the market, accounting for 40.7% of the global share. Meanwhile, the U.S. market is expected to reach USD 2.00 billion by 2032, driven by rising demand across water purification, air filtration, and diverse industrial applications.

Activated carbon, also referred to as activated charcoal, is widely recognized for its excellent adsorption capabilities. It is extensively used in applications such as air treatment, water purification, and various industrial processes. The market has witnessed notable growth, largely driven by rising environmental concerns and the enforcement of stringent regulatory standards. Increasing awareness around sustainability and the implementation of strict emission control guidelines continue to fuel demand for activated carbon.

Fortune Business Insights™ displays this information in a report titled, "Activated Carbon Market, 2025-2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/activated-carbon-market-102175

List of Key Companies Profiled In the Report:

- Osaka Gas Chemicals Co., Ltd. (Japan)

- Donau Carbon GmbH (Germany)

- Cabot Corporation (U.S.)

- PURAGEN ACTIVATED CARBONS (U.S.)

- CARBOTECH AC GMBH (Germany)

- Kuraray Co., Ltd. (Japan)

- KUREHA CORPORATION (Japan)

- Activated Carbon Technologies (Australia)

- Silcarbon Aktivkohle GmbH (Germany)

- Ingevity (U.S.)

- Iluka Resources (Australia)

- James Cumming & Sons (Australia)

- Universal Carbons (India)

Segmentation:

Granular Carbon to Gain Traction Due to its Rising Use in Many End-use Industries

Based on type, the global market is segmented into powdered, granular, and others. The Granulated Activated Carbon (GAC) segment is the fastest-growing segment as this type of carbon finds major usage in several industries, such as air & gas purification and water treatment.

Activated Charcoal to be Increasingly Used in Water Treatment Applications Due to Rising Industrial Activities

Based on application, the market is categorized into water treatment, air & gas purification, food & beverage, pharmaceutical & healthcare treatment, and others. The water treatment segment held the largest activated carbon market share in 2022 as the product is widely used in water treatment applications to eliminate organic compounds and toxic substances.

With respect to region, the market covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report studies the market in detail and underlines critical aspects, such as key product types, applications, and top market players. The report also offers valuable insights into the market’s drivers, trends, and prominent industry developments. Besides the abovementioned factors, the report also lists other factors that have helped the market grow.

Drivers and Restraints:

Growing Adoption of Air Purification Systems to Accelerate Market Growth

Air pollution is becoming a major cause of concern globally as it is one of the primary causes of many severe health problems. Individuals in residential areas are suffering from breathing difficulties due to the lack of clean air. This is why many people are opting for air purification systems, which contain activated carbon to absorb the tiniest pollutants and impurities present in the air, providing them with clean, breathable air.

However, rising prices of raw materials to make activated charcoal and their shortage may impede activated carbon market growth.

Regional Insights:

Asia Pacific Dominates Due to Presence of Major Active Carbon Consuming Countries

Asia Pacific dominated the global market in 2022 and might retain its dominance during the forecast period as region has two major active carbon consuming countries – India and China. These countries are using this type of carbon in water treatment applications to cater to the growing need for safe and potable water.

North America has also showcased major growth as this product is being widely used in air and water purification applications.

Information Source: https://www.fortunebusinessinsights.com/activated-carbon-market-102175

Competitive Landscape:

Key Market Players to Offer Sustainable Purification Solutions to Boost Their Presence

Some of the key companies operating in this market include Cabot Corporation and Kuraray Co. Ltd. These firms are focusing on providing sustainable purification solutions to various industries, such as oil & gas, water treatment, and food & beverage, which will help them strengthen their market position.

Notable Industry Development:

- May 2024 – Kuraray Co., Ltd. along with its U.S. subsidiary Calgon Carbon Corporation is set to acquire Sprint Environmental Services, LLC’s industrial reactivated carbon business.

- March 2023 – Cabot Corporation launched the EVOLVE technology program that is involved in advancing sustainable reinforcing carbons. The purpose of the new technology launch was to recover the carbon product from the end-life tiers to renew the waste and reduce the carbon content.

Laminate Flooring Market Share, Industry Insights and Future Prospects 2025-2032

By ameliasss, 2025-08-29

The global laminate flooring market size is set to experience dynamic growth in the upcoming years owing to the increasing number of residential buildings across the world, observes Fortune Business Insights™ in its report, titled “ Laminate Flooring Market, 2025-2032”. Laminate flooring is a multi-layered product manufactured through the lamination process. Its top surface, typically made of melamine and aluminum oxide, provides durability with resistance to scratches and moisture. Owing to its easy installation and low maintenance, laminate flooring has gained significant popularity in modern construction. Moreover, the rising volume of commercial construction projects worldwide is expected to drive the growth of the global laminate flooring market.

Over the years, there has been a surging growth in the number of residential and commercial buildings across the world due to the increasing initiatives undertaken by the governments of various countries for the development of construction industry. This has resulted in a high demand for laminate flooring across several regions, which is projected to propel the growth of this market during the forecast period.

However, the change in price and the availability of raw materials is projected to hinder the growth of this market.

Request Free Sample PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/laminate-flooring-market-104891

Key Players Covered:

The global & regional players operating in the laminate flooring market includes, Tarkett SA, Mohawk Industries Inc., Shaw Industries Group Inc. Armstrong Flooring Inc., Beaulieu International Group

Market Segmentation:

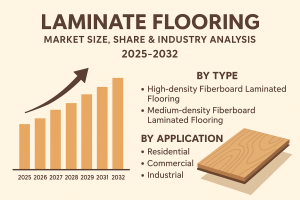

On the basis of type, this market is classified into high-density fiberboard laminated flooring and medium-density fiberboard laminated flooring. Based on application, the market is divided into residential, commercial, and industrial. In terms of geography, the market is clubbed into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

A wide range of commercial spaces—such as hotels, cafes, theaters, galleries, sports stadiums, and boardrooms—are increasingly adopting laminate flooring due to its cost-effectiveness, low maintenance needs, and ability to endure heavy foot traffic. Growing construction projects across various countries are expected to create new opportunities for market expansion in the coming years. However, fluctuations in raw material prices and limited availability remain major challenges for laminate flooring manufacturers, posing obstacles to overall market growth.

Highlights/Summary:

The report provides an exhaustive assessment of each market segment and also offers an in-depth analysis of the market drivers, trends, opportunities, and hindrances. Furthermore, the report contains a granular examination of the regional developments impacting the market, along with a thorough evaluation of the top market players and their key strategies.

Drivers/Restraints:

Rising Number of Hotels and Cafes across the World to Fuel the Market

With the growing number of hotels, cafes, and theatres around the world, there has been a rising demand for laminate flooring that is cost-efficient and can provide attractive look to the interiors of the hotel or café. Further, the laminate flooring requires less maintenance and also possesses the ability to withstand heavy traffic. Thus, this is a major factor responsible for the growth of this market across several regions.

Regional Insights:

Increasing Urbanization Rate to Boost the Asia Pacific Market Growth

The Asia Pacific region is projected to witness substantial growth in the laminate flooring market share on account of the rising urbanization rate and growing construction sector in the countries such as India, China, Japan, and others.

Europe is anticipated to grow steadily in this market owing to the increasing number of laminate flooring manufacturing companies in the countries such as the UK, Germany, France, and others.

Information Source: https://www.fortunebusinessinsights.com/laminate-flooring-market-104891

Competitive Landscape:

Rising Investments by Key Players to Animate Competition

The leading companies in the laminate flooring market are focusing on increasing their investments for the manufacturing of laminate flooring due to a high demand for such flooring from the construction industry. This has resulted in the increasing competition among key companies which will help them to expand their product portfolio and widen their market footprint.

Laminate Flooring Industry Developments

- In January 2018, Tarkett invested USD 85.9 million to expand its Luxury Vinyl Tiles production capacity in Europe and North America. This investment was done to meet the increasing demand for modular vinyl flooring in these regions

- In November 2017, Mohawk Industries purchased the Godfrey Hirst Group (Australia), largest manufacturer of carpets, with the goal of expanding its overseas operations. This aquisition helped Godfrey Hirst's production, marketing and distribution leadership to complement Mohawk's existing distribution and product range.

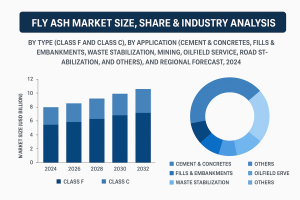

Fly Ash Market Forecast with Key Industry Leaders and Strategic Outlook 2032

By ameliasss, 2025-08-29

According to Forrtune Business Insights, The global fly ash market was valued at USD 13.51 billion in 2023 and is forecast to grow from USD 14.31 billion in 2024 to USD 23.85 billion by 2032, representing a compound annual growth rate (CAGR) of 6.6% over the forecast period. The Asia–Pacific region led the market in 2023, holding a 74.69% share. In the United States, the fly ash market is also expected to expand, reaching an estimated USD 1.07 billion by 2032, driven largely by demand from cement, concrete and road-construction applications.

Fly ash, also known as flue ash, is a fine particulate byproduct released during coal combustion and collected using emission control systems such as scrubbers, electrostatic precipitators, or fabric filters. Thermal power plants generate vast quantities of this ash, and its disposal has long posed significant environmental challenges. Historically, fly ash was regarded as a low-value material, primarily used for landfilling. However, in recent years, its application in cement manufacturing has emerged as a key advancement, as fly ash serves as a pozzolanic additive that enhances the performance of cement.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/fly-ash-market-101087

List of Key Players Profiled in the Report :

- Boral Ltd. (Australia)

- Cemex S.A.B. De C.V. (Mexico)

- Holcim Ltd. (Switzerland)

- Charah, LLC. (U.S.)

- Titan America LLC (U.S.)

- Cement Australia Pty Limited (Australia)

- Salt River Materials Group (U.S.)

- Southeastern Fly Ash Company (U.S.)

- Tarmac Holdings Limited (U.K.)

- Aggregate Industries (U.K.)

Segments:

Class F Segment to Dominate Global Market Owing to Advantage of Less Heat Generation

By type, the market is bifurcated into Class F and Class C. Class F ash is created from bituminous and anthracite coals. This class consists of silica and alumina and lower calcium content. The Class F segment is expected to lead the market due to its advantages such as increased compressive strength and less heat generation.

Cement & Concrete Segment Leads the Market Due to Increased Demand from Construction Sector

Based on application, the market is categorized into cement & concretes, fills & embankments, waste stabilization, mining, oil field service, road stabilization, and others. The cement & concrete segment is anticipated to dominate the global market share due to rising product demand in the construction industry.

Geographically, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report provides insightful data regarding recent trends and advancements in the market. The impact of the COVID-19 pandemic on market expansion has been mentioned along with recent business development strategies adopted by the leading players. Also, drivers and restraints affecting the market growth during the forecast period are highlighted further in this report. Regional insights on segmented areas are given and a list of key market players is mentioned further.

Drivers & Restraints:

Rising Commercialization & Industrialization to Augment Market Growth

The market is expected to grow significantly during the forecast period due to the increasing utilization of fly ash in ceramics. Also, rising renovation and replacement activities are expected to drive market growth in the coming years. Furthermore, increasing product demand from the construction industry is anticipated to fuel the market growth. The rising industrialization and commercialization activities are projected to bolster market development and expansion.

However, poor ash quality and issues pertaining to unavailability may hamper the market growth during the forecast period.

Regional Insights:

Asia Pacific Dominates the Global Market Due to Emerging Construction Industry

Asia Pacific dominates the global fly ash market share due to increasing demand for the product from the cement industry. Also, leading companies in the region are expected to fuel the regional market growth.

Europe holds the second-highest global market share due to the rising demand for civil engineering and construction materials, which is anticipated to fuel the regional market growth. Furthermore, rapid infrastructure development in developed countries is expected to propel industry growth.

Information Source: https://www.fortunebusinessinsights.com/industry-reports/fly-ash-market-101087

Competitive Landscape:

Leading Companies to Augment Growth by Forming Business Agreements

The leading players in the global market focus on forming business agreements with supporting companies to expand their business reach and improve their performance. The companies adopt recent technologies to launch new products to meet customer demands and ensure customer satisfaction. These factors ensure enhanced brand image to strengthen industry footing.

Key Industry Development:

- May 2024 – Bharat Aluminium Company Limited partnered with Shree Cement Limited to supply 90,000 metric tons of fly ash for low-carbon cement production, highlighting industry efforts toward sustainability.

- April 2022 – Charah Solutions completed the full Acquisition of Cheswick Generating Station. Also, it has acquired related facilities from GenOn for sustainable environmental remediation and redevelopment of properties.

According to Fortune Business Insights, The global natural fragrance market is projected to witness significant growth in the coming years, driven by shifting lifestyles and rising consumer preference for light, organic products. Natural fragrances are derived from organic and naturally occurring sources in the environment. The human body interacts with these aromatic molecules either through the olfactory system or by absorption through the skin.

The demand for natural fragrances is increasing as consumers become more aware of the benefits of using natural over synthetic alternatives, particularly due to their lower toxicity. Essential oils and natural extracts remain the primary sources used to impart fragrance to perfumes and other products. Since many natural fragrance ingredients are rare and difficult to obtain, they hold greater value compared to synthetic counterparts. The report is titled, “ Natural Fragrance Market Size, Share & Industry Analysis, By Ingredient (Essential Oils, Natural Extracts), By Type of Scent (Top note, Middle Note, Base Note), By Application (Fine Fragrances, Personal Care & Cosmetics, Household Care) Others and Regional Forecast, 2025-2032.”

Request Free Sample PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/natural-fragrance-market-102359

Some of the Key Players of the Natural Fragrance Market include:

- Fragrance Oils (International) Limited

- Alpha Aromatics

- Robertet SA

- Royal Aroma

- Symrise

- Agilex Fragrances

- Carmi Flavor & Fragrance Co., Inc.

- Givaudan SA

- Ogawa & Co.Ltd.

- Lebermuth, Inc.

- MJ Biopharm Pvt. Ltd

- Multiflora

- Firmenich SA

What Are the Highlights of the Report?

The report offers a comprehensive overview of the market and highlights the vital factors promoting, repelling, challenging, and bringing new opportunities for the market. It also discusses the current trends, recent industry developments and various interesting insights that will help financers accordingly invest in the market for the future. The report also mentions the names of major segments and the prominent players operating in the market. For more information on the report, refer to the company website.

Drivers & Restraints-

Low-Toxicity Characteristics of Natural Fragrance to Augment Growth

The rising demand for natural ingredients in fragrances from various end-user products is a key factor in promoting the global natural fragrance market growth. In addition to this, natural fragrance is long-lasting and have low toxicity as compared to the synthetic fragrance. Therefore, it’s increasing popularity will aid in the expansion of the market. Besides this, the increasing demand for strong musk-scented and earthly scented perfumes will bode well for the market in the forecast period.

On the flip side, the fact that natural fragrances are quite similar to one another neutralizes the brand essence when it comes to various players operating in the market. Moreover, the manufacturing of natural fragrance is time-consuming and more expensive, as compared to synthetic perfumes. The factors mentioned above may cause significant hindrance to the market in the long run.

Segment:

The market is categorized into:

The market for natural fragrance is categorized based on ingredient, type of scent, and application. The ingredient segment is bifurcated into natural extracts and essential oils. The kind of scent segment is classified into the base note, middle note, and top note. The application segment is grouped into household care, personal care and cosmetics, and fine fragrances.

Regional Analysis-

Europe Dominating Market Attributable to Rising Consumer Preference

Regionally, Europe earned the largest natural fragrance market share and emerged dominant. Growth of this region is attributed to the changing lifestyle and increasing consumer preference towards naturally scented end-user products. North America follows Europe on account of the increasing number of premium consumers in the region. Furthermore, Asia Pacific will exhibit the fastest CAGR in the forecast years on account of increasing disposable incomes of people in the developing nations, coupled with a rise in the exposure of adopting premium perfume brands with natural flavours.

Information Source: https://www.fortunebusinessinsights.com/natural-fragrance-market-102359

Competitive Landscape-

Players Investing in Product Development and New Launches to Gain Prominent Position

The global market for natural fragrance is highly fragmented on account of the presence of many players. Most of them are investing in the development of premium quality fragrances with a natural essence. The other players are engaging in strategic collaborations, such as contracts and agreements, joint ventures, and others. These schemes are likely to help the players gain a competitive edge in the market.

Major Industry Developments of the Market for Natural Fragrance include:

- November, 2019, – Givaudan, a manufacturer of wide range fragrances, announced the acquisition of US based flavour, Fragrance and Specialty Ingredients company- Ungerer & Company.

- September, 2019, – Firmenich S.A., a Switzerland based premium fragrance and ingredients manufacturer, announced the acquisition of minority stake of 17% in the France based natural ingredient company Robertet.

Injection Molded Plastics Market USD 561.58 Billion Projection with CAGR 4.2% 2032

By ameliasss, 2025-08-28

According to Fortune Business Insights, The global injection molded plastics market was valued at USD 387.51 billion in 2023 and is expected to increase from USD 403.85 billion in 2024 to USD 561.58 billion by 2032, registering a CAGR of 4.2% during 2024–2032. Asia Pacific held the leading position in 2023, accounting for 49.25% of the market share. In the United States, the market is forecast to witness substantial growth, reaching USD 65.32 billion by 2032, fueled by strong demand across the electrical & electronics and medical sectors.

Injection molding is a widely used manufacturing process for producing plastic components. It finds applications across several industries, including automotive, packaging, building & construction, electrical & electronics, medical, and more. Among these, the packaging industry represents the largest application area, where injection molding is utilized to manufacture containers, food packaging, cosmetic and pharmaceutical bottles, as well as various types of closures.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/injection-molded-plastics-market-101970

List of Key Players Covered in the Report

- BASF SE (Germany)

- Dow Inc. (U.S.)

- DuPont (U.S.)

- HTI Plastics (U.S.)

- LyondellBasell (Netherlands)

- Coastal Plastic Molding, Inc. (U.S.)

- Huntsman Corporation. (U.S.)

- Magna International Inc.(Canada)

Report Coverage

We provide our reports which are conducted with an all-inclusive examination approach that majorly emphasizes on delivering precise material. Our scholars have applied a data triangulation method which further assists us to offer trustworthy estimations and test the general market dynamics accurately. Further, our analysts have received admission to numerous international as well as regional funded registers for providing the up-to-date material so that the stakeholders and business professionals invest only in essential zones.

Segmentation

On the basis of resin, the global market for injection molded plastics is bifurcated into Polypropylene (PP), Acrylonitrile butadiene styrene (ABS), High-density polyethylene (HDPE), Polystyrene (PS), and Others.

Based on application, the market is further divided into Automotive, Packaging, Building & Construction, Electrical & Electronics, Medical, and Others. The packaging segment held the largest share in this market. This segment is driven by food & beverages, pharmaceutical, and retail applications.

In terms of geography, the market for injection molded plastics is segregated into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Drivers and Restraints

Innovation in Injection Molding Technologies is a Prominent Trend

There has been incessant improvement in technologies regarding injection molding such as the increasing predisposition towards incorporated method to product design which has accentuated the production operation. This has further tapered down the space between the structuring and production stage, principally in case of complicated products, such as medical apparatuses. This is famously known as micro injection molding in production of medical apparatuses where the procedure is engaged at a microscopic level. This is expected to boost the injection molded plastics market growth during the forecast period.

Regional Insights

Escalating Product Demand to Boost Growth in Asia Pacific

Asia Pacific is estimated to hold majority of the injection molded plastics market share and endure as a dominant region in the market during the mentioned period owing to the increasing demand for the product from the packaging and automobile industries. The market size of Asia Pacific was USD 162.98 billion in 2020.

The demand for injection molded plastics in North America is projected to upsurge owing to an abrupt demand from the packaging and electronics industries based in this region.

Europe is expected to hold a substantial share in the market. Growing demand for appropriate packaging for food and beverages have prolonged the visualization of packaging goods producers.

Information Source: https://www.fortunebusinessinsights.com/injection-molded-plastics-market-101970

Competitive Landscape

Key Players to Fortify their Positions by Offering New Product Solutions

Principal producers are situated in Asia Pacific, which is leading to a bifurcated injection molding market. The manufacturers positioned in North America and Europe are concentrating towards reinforcing their market positions in several nations in Asia Pacific set to fuel the growth of their respective establishments. Fundamental players in the market such as BASF SE, HTI Plastics, DuPont, and others have advanced robust regional attendance, distribution channels, and product offerings.

Key Industry Development

- February 2024: Kreate announced its takeover of a supplier of injection molded plastics based in Georgetown, TX. The move is anticipated to significantly enhance the production capacity of the company and enhance its logistics network.

- August 2020: Avient Corporation (Formerly PolyOne) introduced injection moldable thermoplastic elastomers to its Versaflex series. The product was formulated without animal derivatives and is able to serve a variety of medical device applications.

Metal Forging Market Size, Share, Growth Trends and Competitive Outlook 2024-2032

By ameliasss, 2025-08-26

According to Fortune Business Insights, The global metal forging market was valued at USD 78.05 billion in 2023 and is expected to expand from USD 67.43 billion in 2024 to USD 94.88 billion by 2032, registering a CAGR of 4.4% during the forecast period. Asia Pacific held the largest share, accounting for 44.61% of the market in 2023. In addition, the U.S. metal forging market is anticipated to reach USD 13.96 billion by 2032, driven by rising demand from the automotive, aerospace, and industrial machinery sectors.

Metal forging is a manufacturing process that shapes metal through localized compressive forces. This technique is vital for producing components with exceptional strength, durability, and precision, making it indispensable in industries such as automotive, aerospace, energy, and construction. Commonly forged materials include steel, aluminum, titanium, and various alloys, each chosen to meet the unique performance requirements of specific applications.

Fortune Business Insights™ mentioned this in a report titled “ Metal Forging Market, 2024-2032 .”

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/metal-forging-market-103175

Segments-

Carbon Steel Remains the Leading Segment due to High Demand from Various End-User Industries

On the basis of raw material, the market is segmented into carbon steel, alloy steel, stainless steel, aluminum, magnesium, titanium, and others. The carbon steel segment held the major share in 2022. Carbon steel is a widely used alloy in various end-user industries, including general manufacturing, automotive, industrial, and others.

Open Die Segment to be Rapidly Growing Due to High Product Demand

Based on technology, the market is divided into open die, closed die, and others. The closed die segment dominated the market. Closed die forging offers exceptional strength as compared to alternative methods.

Automotive to Lead End-User Segment Due to High Product Demand

The market is fragmented into aerospace & railways, automotive, mechanical equipment, and others, based on end-user. The automotive segment led the market in 2022 and is anticipated to dominate the market share in 2030. The automotive industry is one of the prime consumers of forged products such as engines, frames, gear components, drive shafts, clutch, and others.

Geographically, the market is studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

List of Key Players Present in the Report :

- Wyman Gordon (U.S.)

- Shultz Steel (U.S.)

- Consolidated Industries, Inc. (U.S.)

- Pacific Forge Incorporated (U.S.)

- Otto Fuchs KG (Germany)

- Weber Metals California (U.S.)

- ATI Ladish LLC (U.S.)

- Patriot Forge Co. (Canada)

- Arconic Corporation (U.S.)

- Alcoa Corporation (U.S.)

- voestalpine BÖHLER Aerospace GmbH & Co KG (Austria)

- China National Erzhong Group Deyang Wanhang Die Forging Co., Ltd. (China)

Report Coverage-

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- Latest industry developments such as product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints-

Growing Demand for Titanium for the Production of Aircraft Components to Propel the Market Growth

Rising population, urbanization, and the surging pace of transportation & tourism are the key drivers of the aerospace industry growth. The aerospace industry uses forged materials to produce components for landing gear, airframe structure, and engine components, and other aerospace applications, thereby driving the metal forging market growth. Titanium alloys and commercially available titanium are majorly used for aircraft manufacturing that features a density than 60% of steel with better strength and effective corrosion resistance.

Forging and casting are the two most famous metal transformation and manufacturing processes to create parts and components for various end-use industries. Forging has limitations in terms of thickness of the metal and product size.

Regional Insights-

Asia Pacific to Dominate the Market Due to the Presence of Major Metal Forging Nations

Asia Pacific dominated the largest metal forging market share in 2022 and is the fastest-growing region due to the presence of major metal forging nations such as Japan, China, and India. Furthermore, rising manufacturing capabilities of end-use industries such as general manufacturing and automotive are major factors driving the regional growth.

Europe is anticipated to witness subsequent growth by the end of the projected period. The growth in this region is due to increasing adoption of forged metal in automotive applications.

Information Source: https://www.fortunebusinessinsights.com/metal-forging-market-103175

Competitive Landscape-

Business Expansion is a Strategic Initiative Implemented by Companies

The global market is fragmented in nature. The prominent strategies major companies adopt include new product launches to increase their regional presence and improve their portfolio. The market comprises players, such as ThyssenKrupp AG, Bharat Forge, and Schuler AG, which will strive to consolidate their position during the projected period.

Key Industry Developments:

- February 2024: Ovako and Tibnor, well-known material manufacturing and distributing companies, announced a strategic partnership to promote low-carbon footprint solutions in steel production. Various industrial players are committing to science-based environmental targets, while legislative representatives are insisting companies decrease their emissions or face the true cost of pollution.

- May 2023: Arconic Corporation announced a definitive agreement to be acquired by the Apollo Global Management Inc. fund holders in an all-cash transaction deal with the approximate value of USD 5.2 billion. This deal would provide Arconic with access to one of the world's premier investment firms and deliver substantial value to customers and the end users of their products.