Category: Business

According to Fortune Business Insights, the global advanced ceramics market was valued at USD 102.32 billion in 2023 and is projected to grow from USD 113.29 billion in 2024 and reach USD 250.30 billion by 2032, exhibiting a CAGR of 10.1% during the forecast period. Asia Pacific dominated the advanced ceramics market with a market share of 37.37% in 2023. The ongoing technological advancements and rising demand for modern consumer electronic appliances are expected to propel the need for electroceramics. Advanced ceramics is extensively used in such products because of their possession of multiple beneficial properties, such as compressive strength.

Advanced ceramics are referred to as high-tech ceramics, technical ceramics, high-performance ceramics, and engineered ceramics. Technologies such as hydraulic pressing, injection molding, isostatic pressing, tape casting, and pressure casting are used to provide better-quality ceramics products. The property spectrum of ceramics ranges from heat, wear, temperature, and corrosion resistance to food compatibility and biocompatibility.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/advanced-ceramics-market-105073

A list of reputed advanced ceramics providers operating in the global market:

- International Syalons (UK)

- KYOCERA Corporation (Japan)

- S&S Advance Ceramics (India)

- Advanced Ceramics Manufacturing (U.S.)

- Nishimura Advanced Ceramics (Japan)

- CeramTec GmbH (Germany)

- CoorsTek Inc. (U.S.)

- Saint-Gobain (U.S.)

- Morgan Advanced Materials (UK)

- Technocera (India)

- Other Key Players

Kyocera Corporation Acquires 100% Shares of H .C. Starck Ceramics GmbH

In February 2019, Kyocera Corporation, a multinational ceramics and electronics manufacturer based in Japan, announced that Kyocera Fineceramics GmbH, its Germany-based European headquarters signed an agreement to acquire 100% shares of H.C. Starck Ceramics GmbH. This acquisition will help Kyocera to introduce its state-of-the-art fine ceramic manufacturing assets, innovative technologies, and production lineup in Europe. Such initiatives by prominent companies are likely to surge the demand for advanced ceramics worldwide.

Report Coverage-

The research report of the advanced ceramics industry offers a comprehensive analysis of existing companies that can affect the market outlook throughout the forthcoming years. In addition to that, it provides an accurate assessment by highlighting data on multiple aspects that may contain growth drivers, opportunities, trends, and hindrances. It also represents the overall market size from a global perspective by analyzing historical data and qualitative insights.

Drivers & Restraints-

Rising Usage in Making Implant Abutments and Artificial Bones to Propel Growth

Advanced ceramics are gaining more importance in the medical industry. The product has excellent aesthetic, physical, and biological properties. Therefore, it is extensively utilized for making endosseous implants, artificial bones, and implant abutments. The industry is also anticipated to use zirconia ceramics. These factors are set to accelerate the advanced ceramics market growth in the forthcoming years. However, the production process of this ceramic involves high cost spending as it includes inspection, diamond grinding, sintering, forming, and raw material processing. It may hinder growth.

Segments-

Transportation Segment Generated 21.2% Share in China in 2020: Fortune Business Insights™

Based on the material, the market is divided into alumina, zirconia, titanate, silicon carbide, silicon nitride, and others. Below is a brief note on the end-use criterion:

- By End-use : The market is categorized into electrical & electronics, transportation, medical, chemical, and others. Out of these, the transportation segment held 2% in terms of the China advanced ceramics market share in 2020. This growth is attributable to the rising usage of the product in aerospace engines and electric water pumps. On the other hand, the medical segment earned 18.0% in 2020 on account of the high demand for biodegradable splints and other similar products.

Regional Insights-

Increasing Usage of Titanate in Automotive Industry to Propel Growth in Asia Pacific

- Asia Pacific : The region held USD 30,783.0 million in terms of revenue in 2020. It is expected to remain at the forefront on account of the high demand for the product from the medical industry. Besides, increasing usage of titanate in the automotive industry, especially in China, is set to aid growth.

- North America : The increasing shift of manufacturers towards this ceramic over plastic or other metals is anticipated to help the region remain in the second position. Additionally, the rising production of electronic devices and electrical equipment in the region would boost growth.

- Europe : The presence of a well-established automotive industry in the region is set to augment growth in the forecast period. Coupled with this, the urgent need to reduce emissions in the atmosphere would also result in the rising adoption of electric vehicles in the region.

Competitive Landscape-

Key Companies Aim to Participate in Acquisition Strategy to Compete with Their Rivals

The market houses several prominent manufacturers that are focusing on various organic and inorganic strategies to compete with their rivals. Among them, acquisition is the most significant strategy. International Syalons, for instance, is a leading producer of silicon nitride and sialon-based ceramics. It often participates in mergers and acquisitions to broaden its footprints and generate more sales.

Information Source: https://www.fortunebusinessinsights.com/advanced-ceramics-market-105073

KEY INDUSTRY DEVELOPMENTS

April 2023 – Kyocera Corporation made a deal to acquire 37 acres of land for a new smart factory in Isahaya City, Japan. The move is part of the company’s strategy to increase the production capacity of fine ceramic components, considering the rising demand for products used in semiconductor-related applications.

July 2022- Bosch Advanced Ceramics collaborated with BASF and Karlsruhe Institute of Technology (KIT) to develop first of its kind 3D printed micro-reactor using advanced ceramics materials. This reactor is currently being used by BASF to perform chemical reactions for research purposes. 3D printing technical ceramics can create new opportunities in the future.

Refinery Catalyst Market In-depth Analysis, Key Metrics, and Future Projections to 2032

By ameliasss, 2025-06-13

According to Fortune Business Insights, The global refinery catalyst market size was USD 4.82 billion in 2023 and is projected to grow from USD 5.01 billion in 2024 to USD 6.77 billion by 2032 at a CAGR of 3.8% during the 2024-2032 period. Asia Pacific dominated the refinery catalyst market with a market share of 35.68% in 2023.

Refinery catalysts are chemical ingredients used during the refining process to remove unwanted impurities such as nitrogen, metal contamination, and sulfur. These catalysts include zeolites, calcium carbonate, molybdenum, palladium, zirconium, which are used independently or in different combinations to improve the operating effectiveness of petroleum. The global refinery catalyst market is witnessing steady growth, driven by tightening environmental regulations, rising fuel demand, and increasing investments in complex refinery infrastructure. As refineries shift focus toward producing cleaner fuels and value-added petrochemicals, the demand for advanced catalysts is on the rise.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/refinery-catalyst-market-101090

LIST OF KEY COMPANIES PROFILED

- Albemarle Corporation (U.S.)

- BASF SE (Germany)

- Haldor Topsoe A/S (Denmark)

- Honeywell International Inc. (U.S.)

- Clariant (Switzerland)

- Axens (France)

- Johnson Matthey (U.K.)

- China Petroleum & Chemical Corporation (China)

- Royal Dutch Shell plc (Netherlands)

Key Segments :

By Type : Fluid catalytic cracking (FCC) catalysts, hydrotreating catalysts, hydrocracking catalysts, catalytic reforming catalysts.

By Ingredient : Zeolites, metals (molybdenum, cobalt, nickel), chemical compounds.

By Application : Gasoline production, diesel treatment, residue upgrading, petrochemical processing.

Market Drivers

1. Stringent Fuel Emission Standards

Global mandates for ultra-low sulfur diesel (ULSD) and cleaner gasoline are boosting the demand for hydroprocessing and FCC catalysts. These catalysts are critical for removing impurities like sulfur, nitrogen, and heavy metals from crude oil derivatives.

2. Growing Petrochemical Demand

The shift toward producing light olefins and aromatics from heavier feedstocks is accelerating the use of FCC and reforming catalysts. The expansion of petrochemical complexes globally also supports this trend.

3. Processing Heavy and Renewable Feedstocks

Modern refineries are increasingly handling heavier, high-sulfur crudes and integrating renewable feedstocks such as used cooking oils and bio-oils. Specialized catalysts are essential to improve conversion efficiency and product yield in these scenarios.

4. Technological Advancements

Catalyst innovation—including multi-functional catalysts, zeolite-based structures, and AI-guided optimization—is enhancing operational efficiency. New-generation catalysts are also enabling higher selectivity and lower coke formation during cracking and reforming.

Challenges

Volatile crude oil prices impact refinery operations and investment in catalyst technologies.

Transition to electric vehicles (EVs) is likely to reduce gasoline and diesel consumption, though this may be balanced by growing petrochemical production.

Regional Insights

Asia-Pacific

The fastest-growing market, driven by large-scale refinery projects in China and India. The region also leads in the production and export of FCC and hydrocracking catalysts.

North America

Significant demand for hydrotreating and reforming catalysts due to strict environmental regulations. The U.S. is a major contributor with a strong domestic refining industry.

Europe

Focus on clean energy transition and biofuel mandates is shaping the demand for sustainable catalyst technologies.

Middle East & Africa

Large investments in refinery expansion and modernization, especially in countries like Saudi Arabia and the UAE, are creating long-term opportunities.

Emerging Trends

Bio-refining catalysts are gaining traction as more refineries integrate renewable raw materials.

Zeolite-based catalysts are growing rapidly due to their superior thermal stability and selectivity.

Digital catalyst modeling using AI and machine learning is shortening development cycles and improving performance prediction.

Future Outlook

Between 2024 and 2032, the refinery catalyst market is expected to witness consistent growth. The focus will increasingly shift toward:

Catalysts tailored for renewable and alternative feedstocks

Eco-efficient technologies that support decarbonization

Customized regional solutions to cater to local fuel regulations and feedstock availability

Despite the long-term impact of EV adoption, demand for refinery catalysts will remain robust due to sustained global fuel needs and rising petrochemical production.

The refinery catalyst market stands at the intersection of regulatory compliance, technological innovation, and energy transition. As the global refining landscape evolves, catalysts will play a crucial role in enabling cleaner, more efficient, and more sustainable fuel and chemical production. Companies that invest in advanced catalyst development and adapt to shifting energy dynamics are poised for long-term success.

Information Source: https://www.fortunebusinessinsights.com/industry-reports/refinery-catalyst-market-101090

KEY INDUSTRY DEVELOPMENTS

- January 2023 – Albemarle Corporation announced the brand launch of “Ketjen”, a wholly-owned subsidiary that created customized, sophisticated catalyst solutions for the specialty chemical, refining, and petrochemical sectors.

- February 2021 – Bharat Petroleum Corporation Limited subsidiary, Numaligarh Refinery Limited (NRL has designated Axens for supplying advanced technologies in the gasoline block for its Numaligarh Refinery Expansion Project (NREP). The company has planned to expand the refinery capacity 9000 KT per annum.

According to Fortune Business Insights™, the global oleochemicals marke t size was valued at USD 37.88 billion in 2023 and is projected to grow from USD 40.37 billion in 2024 to USD 65.38 billion by 2032, exhibiting a CAGR of 6.3% during the forecast period. Asia Pacific dominated the oleochemicals market with a market share of 48.86% in 2023. Increasing demand for oleochemicals from the food and chemical industries is expected to increase market growth. Demand for biofuels keeping in mind environmental and health concerns is set to drive market growth. Rising demand from several end-use industries is expected to boost market development and offer lucrative opportunities for market growth. Fortune Business Insights ™ shares this information in its report titled “ Oleochemicals Market, 2024-2032. ”

Oleochemicals are chemicals produced by chemical and enzymatic reactions from vegetable oils and animal fats. They are analogous to petrochemicals products. The market is set to experience high growth rate due to increased demand from the food and chemical industries. Increasing preference for sustainable fuels is expected to surge product demand during the forecast period.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/oleochemicals-market-106250

List of Key Players Profiled in the Report

- Cargill Inc. (U.S.)

- Kuala Lumpur Kepong Berhad (Malaysia)

- BASF SE (Germany)

- Oleon N.V. (Belgium)

- IOI Group Berhad (Malaysia)

- Wilmar International (Singapore)

- Kao Chemicals (Japan)

- Twin Rivers Technologies (U.S.)

- Croda Industrial Chemicals (U.K.)

- Evonik Industries (Germany)

- Emery Oleochemicals (Malaysia)

- Godrej Industries (India)

Segments

Fatty Acid to Lead Due to Easy Availability of Raw Materials

On the basis of type, the market is divided into fatty acids, fatty alcohols, methyl esters, and glycerin. Fatty acid is anticipated to have the dominant part due to easy availability of raw materials and growing demand for organic personal care products. Fatty acids are an important part as they serve as a raw material to produce several downstream derivatives, including elastomers, toiletry, biocides, softeners, and wax.

Food & Beverages Segment to Lead Due to Wide Adoption of Various Additives and Stabilizers

On the basis of application, the market is divided into food & beverages, chemicals, animal feed, and others. Food & beverages segment is anticipated to have the dominant part due to increasing adoption of bio-based thickeners, stabilizers, and other food additives in the food industry. The chemical segment is expected to be growing at the fastest CAGR due to high demand for sustainable alternatives for petroleum-derived chemicals.

Report Coverage

The report provides a detailed analysis of the top segments and the latest trends in the market. It comprehensively discusses the driving and restraining factors and the impact of COVID-19 on the market. Additionally, it examines the regional developments and the strategies undertaken by the market's key players.

Drivers and Restraints

Increasing Demand from Various End-use Industries to Drive Market Expansion

Rising demand from various end-user industries is anticipated to drive the oleochemicals market growth. These chemicals are highly employed by various sectors, including personal care, cosmetics, food & beverages, pharmaceuticals, and plastics. They are used in skincare and haircare products. They are used due to their high demand for hypoallergenic and chemical-free ingredients, which is expected to propel market development. Lower cost and sustainability of raw materials used are set to boost market growth. Increasing demand for biofuels is expected to push market growth.

However, VOC production at the time of pre-treatment of glycerin is expected to hinder the market growth.

Regional Insights

Asia Pacific to Lead Market Share Due to Growing Awareness Regarding Harmful Effects of Fossil Fuels

Asia Pacific is anticipated to head the oleochemicals market share due to growing awareness amongst people regarding the harmful effects of the exploitation of fossil fuels and petrochemical resources. The majority demand in the region is backed by ASEAN countries and China. The region is a major producer and exporter of oleochemical feedstock and its derivatives.

North America is expected to have considerable growth due to stringent regulations regarding practicing sustainability and the growing demand for plant-based products.

Information Source: https://www.fortunebusinessinsights.com/oleochemicals-market-106250

Competitive Landscape

Upgrading of Product Portfolio by Key Market Players to Set Market Progression

Key players of market are BASF, Evonik, Emery Oleochemicals, Twin River Technologies, Cargill Inc., and Croda Industrial Chemicals. They have been updating and elevating their product portfolios for enhancing their market share. In December 2021, Cargil Inc. decided to remove iTFAs from its entire global edible oil portfolio. The purpose of the new edible oil range is to support food manufacturers to produce healthier products for consumers.

Key Industry Development

- August 2022 - The Kuala Lumpur Kepong Berhad Group offered a product named DavosLife E3, which can be used in food and nutrition applications. According to Kuala Lumpur Kepong Berhad, the product has wide-reaching, clinically proven health benefits for heart health, liver health, and brain health.

- July 2022 BASF SE offered the first rainforest alliance-certified personal care ingredients based on coconut oil. The company established a renewable supply chain, which will help the company maximize its revenue.

Secondary Packaging Market Insights: USD 519.41 Billion in 2024 to USD 720.70 Billion by 2032

By ameliasss, 2025-06-12

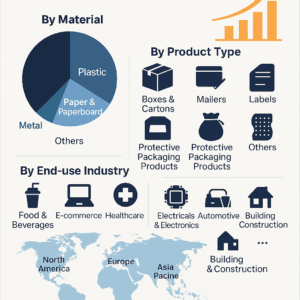

According to Fortune Business Insights, the global secondary packaging marke t size was valued at USD 501.27 billion in 2023 and is projected to grow from USD 519.41 billion in 2024 to USD 720.70 billion by 2032, exhibiting a CAGR of 4.18% during the forecast period. Moreover, the secondary packaging market in the U.S. is projected to expand substantially, reaching USD 196.62 billion by 2032.

his growth is attributed to the increasing emphasis on branding, product protection, and logistics efficiency across various industries, including e-commerce and retail. North America dominated the secondary packaging market with a market share of 33.48% in 2023. The external packaging of primary packaging is known as secondary packaging. Growing usage of paper & paperboard materials and increased preference for sustainable packaging solutions are fostering market expansion.

F ortune Business Insights presents this information in their report titled " Secondary Packaging Market, 2025–2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/secondary-packaging-market-107321

List of Key Players Profiled in the Market Report

- Amcor plc (Switzerland)

- International Paper Company (U.S.)

- Berry Global Inc. (U.S.)

- Mondi (U.K.)

- DS Smith (U.K.)

- WestRock (U.S.)

- Crown Holdings Inc. (U.S.)

- UFP Industries, Inc. (U.S.)

- Graphic Packaging International, LLC (U.S.)

- Huhtamaki Oyj (Finland)

- Packaging Corporation of America (U.S.)

- Rengo Co. Ltd. (Japan)

- Sealed Air Corp. (U.S.)

Segments

Paper and Paperboard Segment Dominates the Market as They are 100% Recyclable

By material, the market is divided into plastic, paper & paperboard, metal, and others. The paper and paperboard segment holds the highest secondary packaging market share as they are 100% recyclable and do not damage the environment. Increased usage of high demand for boxes and cartons is boosting segment expansion.

Boxes & Cartons Gain Popularity as They are Eco-friendly and Highly Durable

On the basis of product type, the market is categorized into films & wraps, mailers, boxes & cartons, labels, bags & pouches, protective packaging products, and others. Boxes & cartons command the global market as they are the most famous types of product packaging and are widely utilized to transport anything. Boxes & cartons are gaining traction as they are eco-friendly, highly durable, appealing, and customizable.

Rapid Change in Consumer Lifestyles Boosts Secondary Packaging Demand in the Food and Beverage Sector

Based on the end-use industry, the market is segmented into food & beverages, e-commerce, healthcare, electricals & electronics, personal care & cosmetics, automotive, building & construction, and others. The food and beverages segment dominates the market due to rapid changes in consumer lifestyles and purchasing behavior. Surging demand for convenient food products is also driving segment growth.

From the regional ground, the market is classified into Europe, Latin America, North America, Asia Pacific, and the Middle East & Africa

Report Coverage

The market research report presents a complete market examination, highlighting essential elements, including the competitive environment and noticeable product categories. Furthermore, the report provides valuable insights on market trends and significant industry developments. Apart from the factors above, the report includes several aspects that have fostered market expansion in recent times.

Drivers and Restraints

Rapid Expansion of the E-commerce Sector Propels Market Growth

The rapid expansion of the e-commerce industry is boosting the adoption of boxes, cartons, and other products across the globe. Secondary packages are crucial in keeping transit packaging smooth for creators of essential products, including packaging for food, medical, consumer goods, and pharmaceutical products. The demand for food, specifically from online outlets, is rising enormously. Increased demand for secondary packaging is attributed to the growing emphasis on online food delivery and online shopping of essential products by millennials and the working women population. This factor fosters global secondary packaging market growth.

Nevertheless, varying prices of raw materials are impeding market growth.

Regional Insights

Rising Preference for Online Food Delivery in the U.S. Augments Market Growth in North America

North America emerges as a leading region in the global market due to the rapid expansion of the food and beverages sector. Rising preference for online food delivery, especially in the U.S., is also driving market expansion in the region.

Europe is the second-ruling region in the global market owing to increased focus on sustainability due to rising concerns around the environment. Surging adoption of environmentally friendly packaging solutions propels market growth in the region.

Competitive Landscape

Key Players Offer Innovative Packaging Solutions to Boost Their Market Positions

Some of the key players in the market are Amcor plc, International Paper Company, Berry Global Inc., Mondi, DS Smith, and WestRock. Top secondary packaging solution providers reign supreme in the market by offering innovative packaging solutions.

Information Source: https://www.fortunebusinessinsights.com/secondary-packaging-market-107321

Key Industry Development

- May 2024 – Mondi declared the launch of a new secondary paper packaging solution, TrayWrap, that replaces plastic shrink film utilized for bundling food and beverage products. The new sustainable packaging option is developed using Mondi’s Advantage StretchWrap range and is majorly utilized by a coffee brand in Sweden to safeguard 12 coffee packages for transportation purposes.

- September 2023 – Tetra Pak, a world-renowned leader in paper-based carton packaging, teamed up with Flow Beverage, the largest carton water brand in North America, and Live Nation Canada. Together, they unveiled new carton designs that showcase Tetra Pak Custom Printing. It is the "one-of-a-kind" inkjet-based system that enables brands to create premium, tailor-made, and affordable packaging solutions.

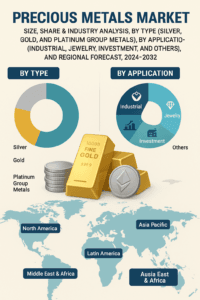

According to Fortune Business Insights , The global precious metals market size was USD 306.44 billion in 2023 and is projected to grow from USD 323.71 billion in 2024 to USD 501.09 billion by 2032 at a CAGR of 5.6% during the forecast period. Asia Pacific dominated the precious metals market with a market share of 52.33% in 2023.

The global precious metals market is experiencing robust growth, driven by increased demand from both traditional and emerging sectors. Precious metals such as gold, silver, platinum, and palladium have long been valued for their rarity, economic significance, and intrinsic value. Today, they continue to play a vital role in industries ranging from jewelry and electronics to automotive and renewable energy technologies. Increasing disposable incomes and changing lifestyle choices are a few of the factors driving the market. The demand for these metals is estimated to propel globally for jewelry and investment applications as gold and silver are of prime importance in wedding ceremonies of Southeast Asian countries.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/precious-metals-market-105747

LIST OF KEY COMPANIES PROFILED:

- Newmont Corporation (U.S.)

- Barrick Gold Corporation (Canada)

- AngloGold Ashanti Limited (South Africa)

- Kinross Gold Corporation (Canada)

- Newcrest Mining Limited (Australia)

- Gold Fields Limited (South Africa)

- Freeport-McMoRan (U.S.)

- Wheaton Precious Metals (Canada)

Market Overview

The precious metals market is fundamentally influenced by a balance of investment sentiment, industrial consumption, and macroeconomic trends. As of recent years, growing geopolitical tensions, currency volatility, and inflation concerns have led investors to seek refuge in precious metals, particularly gold and silver. Simultaneously, industrial demand—especially for silver and platinum—has surged due to advancements in electronics, solar power, and clean energy technologies.

Key Precious Metals and Their Applications

Gold : Often seen as a safe-haven asset, gold continues to dominate the investment landscape. It is also widely used in jewelry, accounting for a significant portion of global demand. Additionally, its use in electronics and medical devices is expanding.

Silver : Known for its excellent conductivity, silver is crucial in electronics, solar panels, batteries, and medical applications. Demand for silver has grown considerably with the increasing deployment of photovoltaic (PV) systems worldwide.

Platinum : This metal is extensively used in automotive catalytic converters, as well as in the chemical, petroleum, and medical industries. Platinum is also a key element in hydrogen fuel cell technology, which is gaining momentum in the clean energy sector.

Palladium : Like platinum, palladium is primarily used in emission control devices in vehicles. The tightening of environmental regulations globally has significantly boosted demand for palladium.

Market Drivers

1. Rising Industrial Applications

One of the primary drivers of the precious metals market is the increasing range of industrial applications. The shift towards electric vehicles (EVs), stricter emissions regulations, and growth in renewable energy have created substantial demand for metals like silver, platinum, and palladium. For example, silver is indispensable in the production of solar panels, while platinum and palladium are essential in catalytic converters and hydrogen fuel cells.

2. Growing Investment Demand

Gold and silver have historically been used as hedges against inflation and currency fluctuations. With ongoing geopolitical tensions, economic uncertainty, and fluctuating fiat currency values, investment in precious metals through ETFs, bullion, and coins has increased. Central banks in many countries are also diversifying their reserves by adding more gold.

3. Jewelry Market Growth

The demand for precious metals in the jewelry sector remains strong, especially in emerging markets such as India and China. These countries account for a significant share of global gold consumption, driven by cultural traditions and increasing disposable income. Platinum and silver are also gaining popularity in modern jewelry design.

Regional Insights

Asia-Pacific : The region dominates the global precious metals market due to high demand in India and China. In addition to strong jewelry demand, industrial use is also expanding, particularly in China’s rapidly growing electronics and renewable energy sectors.

North America : The U.S. is a major market for investment in precious metals, especially gold and silver. The region also houses significant reserves and mining operations.

Europe : Demand in Europe is driven by environmental regulations and green energy initiatives. European automakers are increasingly turning to platinum and palladium for emission-reducing technologies.

Latin America and Africa : These regions are rich in mineral resources and play a critical role in the global supply chain. Countries like South Africa and Peru are key exporters of platinum, gold, and silver.

Challenges in the Market

Despite strong growth prospects, the precious metals market faces several challenges:

Price Volatility : Precious metals prices can be highly volatile due to speculation, interest rate changes, and geopolitical events.

Environmental Concerns : Mining operations often raise environmental and social concerns, which can affect project approvals and timelines.

Supply Chain Disruptions : Geopolitical tensions and logistical constraints can disrupt the supply of precious metals, impacting prices and availability.

Information Source: https://www.fortunebusinessinsights.com/precious-metals-market-105747

Future Outlook

The future of the precious metals market looks promising, with several trends expected to shape its trajectory:

Green Energy and Electrification : As the world transitions to cleaner energy, demand for silver, platinum, and palladium will rise due to their roles in solar panels, fuel cells, and electric vehicles.

Technological Integration : Advancements in electronics, 5G technology, and medical devices will further boost industrial demand for silver and gold.

Sustainable Mining Practices : Companies are increasingly investing in green mining technologies and circular economy initiatives to reduce their environmental footprint and ensure long-term viability.

Digital Transformation : The use of blockchain in precious metals trading and the rise of digital gold platforms are improving transparency, accessibility, and investor confidence.

The precious metals market is evolving rapidly, influenced by a mix of traditional drivers and new-age technologies. Whether as investment instruments, industrial components, or cultural artifacts, precious metals will continue to hold their intrinsic value and strategic importance. With growing interest from both consumers and industries, the market is set to expand in the coming years—making it a compelling area for investment, innovation, and policy focus.

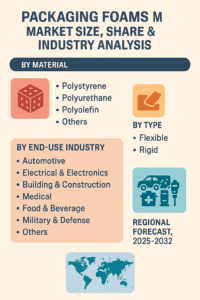

Packaging Foams Market Revenue and Volume Forecast with Regional Breakdown 2025-2032

By ameliasss, 2025-06-11

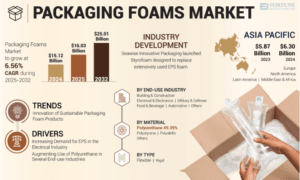

According to Fortune Business Insights, the global packaging foams market size was valued at USD 15.12 billion in 2024. The market is projected to grow from USD 16.03 billion in 2025 to USD 25.01 billion by 2032, exhibiting a CAGR of 6.56% during the forecast period. Asia Pacific dominated the packaging foam market with a market share of 41.66% in 2024.

Packaging foams are used to cushion and protect goods during storage and shipping. These materials are made of either polystyrene, polyurethane, polyethylene, or expanded polyethylene foam, providing numerous properties to the products during handling. These versatile materials come in a variety of sizes and shapes and are often tailored to a specific use or purpose. The increasing trade among countries and the augmenting use of packaging foams for insulation, cushioning soundproofing, and void filling are contributing to the packaging foams market growth.

Fortune Business Insights™ mentions this in a report titled, “ Packaging Foams Market, 2025-2032 ”

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/packaging-foam-market-109408

List of Key Players Present in the Report :

- Sealed Air (U.S.)

- Smurfit Kappa (Ireland)

- UFP Technologies, Inc. (U.S.)

- Sonoco Products Company (U.S.)

- BASF SE (Germany)

- JSP (Japan)

- Zotefoams plc (U.K.)

- Rogers Foam Corporation (U.S.)

- The Supreme Industries Ltd (India)

- Atlas Molded Products (U.S.)

- NEFAB GROUP (Sweden)

- American Foam Corporation (U.S.)

Segments

High Flexibility of Polyurethane Packaging Boosts Segment Growth

Based on material, the market is classified into polystyrene, polyurethane, polyolefin, and others. The polyurethane segment accounts for the largest packaging foams market share due to its high flexibility, large use in many end-use industries, and ease of cutting and fabricating.

he packaging foams market experienced negative growth during the pandemic, as there was a temporary ban on trade activities. Major end-use industries of packaging foams, such as automotive and building and construction, electrical and electronics, food, and beverage, had declining demands. The medical military and defense sectors observed positive and moderate demands, respectively. However, the post-pandemic phase has brought new opportunities to the market due to the surging e-commerce industry.

Flexible Segment Dominates the Market Due to the Durability of Flexible Foams

By type, the market is categorized into flexible and rigid. The flexible segment dominates the market in terms of share owing to the durability and capability of flexible foams to extend the product lifecycles by maintaining the product’s appearance.

Surging Demand for Packaging in the Automotive Sector Drives Segment Expansion

On the basis of end-use, the market is divided into automotive, electrical & electronics, building & construction, medical, food & beverage, military & defense, and others. The automotive segment is dominating the market, fueled by the high demand for packaging that provides shock absorption, sound insulation, structural reinforcement properties, and vibration dampening from the automotive industry.

Geographically, the market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- The latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints

Surging Demand for Expanded Polystyrene (EPS) to Boost Market Expansion

The increasing demand for Expanded Polystyrene (EPS) for electronic device packaging due to the change in the consumer electronics industry drives the packaging foams market growth. The market is also driven by the increasing use of antistatic foam to protect electrical devices owing to the rising threats of static electricity accumulation to electronic components while transporting or storage.

However, the non-biodegradable nature of the expanded polystyrene poses a threat to the environment, including marine pollution may impede market expansion.

Regional Insights

Growing Demand for Electronic Products to Drive Market Expansion in Asia Pacific

Asia Pacific is the dominating and is anticipated to be the fastest-growing region in the market. The increasing demand for electronic products drives the growth, and the presence of the biggest exporter and manufacturer nation of electronic products in the region is expected to drive the market growth.

Europe is the second-leading region in the market for packaging foams due to the surging awareness, innovation, and use of green packaging in the region.

Information Source: https://www.fortunebusinessinsights.com/packaging-foam-market-109408

Competitive Landscape

Key Players are Offering Innovative Packaging to Strengthen Their Market Position

In terms of the competitive landscape, the packaging foams market comprises key players, such as Sealed Air, Smurfit, and others. These players are offering innovative packaging in the packaging industry to strengthen their market position.

Key Industry Development

March 2024 - Seawise Innovative Packaging launched Styrofoam, an alternative form of packaging that is designed to replace extensively used EPS foam. The new packaging is designed to be a cost-effective solution for companies trying to reduce the use of plastics in their supply chain.

December 2023 - Woamy launched a bio-foam product for plastic-free packaging in collaboration with Paptic and Secto Design. The new packaging foam products are fully bio-based, plastic-free, biodegradable, and recyclable.

Airless Packaging Market Technology Advancements Enhance Product Shelf Life, 2025-2032

By ameliasss, 2025-06-11

According to Fortune Business Insights™, the global airless packaging market size was valued at USD 8.45 billion in 2024. The market is projected to grow from USD 8.99 billion in 2025 to USD 12.98 billion by 2032, exhibiting a CAGR of 5.38% during the forecast period. Europe dominated the airless packaging market with a market share of 27.93% in 2024.

The use of airless packaging solutions prevents the contact of the inside product with the air. The solutions offer numerous benefits, including extended shelf life and enhanced functionality. The market expansion can be attributed to the globally rising sales of cosmetic products and the escalating demand for natural skincare products. Airless packaging solutions are dispensing systems that do not allow air contact with the product inside. The packaging offers significant benefits, such as improved functionality and extended shelf life, which adds noteworthy value to the consumer experience. Along with eliminating the risk of contamination, using airless technology in product packaging also prevents the loss of fragrance, financial waste, and evaporation, further driving the market growth. The increasing demand for natural skincare products, the growing number of working women, and the rising sales of cosmetic products globally also boost market share.

Fortune Business Insights™ provides this information in its research report, titled “Airless Packaging Market, 2025-2032”.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/airless-packaging-market-106855

List of Key Players Mentioned in the Report:

- AptarGroup Inc. (U.S.)

- Silgan Holdings Inc. (U.S.)

- Quadpack (Spain)

- HCP Packaging (China)

- APackaging Group (U.S.)

- LUMSON S.p.A (Italy)

- Hangzhou ABC Packaging Co. Ltd. (China)

- Albéa Group (France)

- PrimePac (Australia)

- The Packaging Company (U.S.)

- Berk (U.S.)

- SR Packaging (China)

Segmentation:

Plastic Segment Leads the Market Owing to Various Benefits Offered by the Material

By material, the market is fragmented into glass, plastic, aluminum, and others. The plastic segment dominates the market due to the high demand for the material. Plastic solutions offer excellent protection, helping the prevention of spoilage, leakage, and contamination of a product.

Bottles & Jars Segment Holds Major Share Due to Escalating Product Deployment

Based on product type, the market is segmented into tubes, bottles & jars, and others. The bottles & jars segment registers a key market share. This is due to the rising deployment of the product owing to the availability of various customized options.

Personal Care & Cosmetics Segment Registers Key Share Owing to Growing Product Usage to Increase Shelf Life of Cosmetics

On the basis of application, the market is fragmented into food & beverages, pharmaceuticals, personal care & cosmetics, and others. The personal care & cosmetics segment accounts for a leading market share. The product usage helps increase the shelf life of cosmetic products, which is a major factor driving segment growth.

Based on geography, the market for airless packaging has been studied across North America, Asia Pacific, Latin America, Europe, and the Middle East & Africa.

Report Coverage:

The report gives an account of the major trends in the global market. An analysis of the industry on the basis of various segments has also been presented in the report. The market has been studied based on material, product type, application, and geography.

Drivers and Restraints:

Market Value to Surge with Growing Demand for Cosmetic Products

The escalating cosmetic product demand has led to an increased demand for sustainable packaging solutions among manufacturers. Some of the products requiring effective packaging comprise skin care creams, serums, foundations, moisturizers, and anti-ageing products. These factors are poised to drive the airless packaging market growth.

Nonetheless, the fluctuating prices of raw materials may hinder the industry's expansion to a certain extent.

Regional Insights:

Europe Dominates the Market Due to Expanding Beauty Industry

Europe accounts for a dominating market share. In 2022, the market size in the region stood at USD 2.36 billion. The regional growth can be attributed to the presence of key manufacturing companies and the expanding beauty sector.

Latin America is the fastest-growing regional market. The regional airless packaging market share is set to expand, driven by the soaring airless technology demand from food & beverage manufacturers.

Information Source: https://www.fortunebusinessinsights.com/airless-packaging-market-106855

Competitive Landscape:

Companies Launch Advanced Products to Increase Customer Base

Major industry players are centered on the development and launch of advanced products. These initiatives are being deployed to expand their clientele base. Some of the leading industry players comprise Silgan Holdings Inc., AptarGroup, Inc., APackaging Group, and others.

Key Industry Development:

February 2023 – Quadpack declared the launch of a new refillable airless pen, Light Me Up. The refillable airless pen has several tips and can be utilized in both the skincare and makeup sectors. The refill system is also convenient and intuitive.

November 2022 – Embelia introduced a new and refillable version of the Baia pouch airless system. The new airless system was manufactured in partnership with Lablabo, an expert in pouch airless packaging solutions.

According to Fortune Business Insights, the palladium market size was USD 20.0 billion in 2024. The market is expected to grow from USD 20.4 billion in 2025 to USD 23.6 billion by 2032 at a CAGR of 2.1% during the forecast period. Asia Pacific dominated the palladium market with a market share of 44.00% in 2024.

Palladium is a chemical element and a member of Platinum Group Metals (PGMs), a group of rare precious metals. Its high melting point and corrosion resistance have made it an ideal ingredient in many industrial processes. The industrial uses of this element range from catalytic converters, chemicals, and dental to jewelry. Its most common use is in automotive catalytic converters, which help reduce the carbon emissions from automotive engines. The ability to ensure effective chemical reactions throughout a vehicle’s life cycle has made palladium an irreplaceable catalyst in catalytic converters. It is also an important raw material in certain stages of semiconductor manufacturing, specifically in MultiLayer Ceramic Capacitors (MLCCs).

Fortune Business Insights™ displays this information in a report titled, "Palladium Market, 2025-2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/palladium-market-108959

LIST OF KEY COMPANIES PROFILED IN THE REPORT:

- Anglo American Platinum Limited (South Africa)

- Heraeus (Germany)

- Impala Platinum Holdings Limited (South Africa)

- Ivanhoe Mines Ltd. (Canada)

- Nornickel (Russia)

- New Age Metals Inc. (Canada)

- Northam Platinum Holdings Limited (South Africa)

- Platinum Group Metals Ltd. (Canada)

- Sibanye-Stillwater (South Africa)

- Southern Palladium Limited (Australia)

Segmentation:

Growing Efforts Toward Achieving Circular Economy to Fuel Adoption of Recycled Palladium

Based on source, the market is segmented into mined and recycled. The recycled segment is expected to record a faster CAGR as compared to the mined segment as countries are looking for various ways to create a circular economy, and recycled palladium can help them achieve that goal.

Automotive to Emerge as Major End-Use Industry Due to Growing Need for Reducing Carbon Emissions

Based on end-use industry, the market is segregated into automotive, electronics, chemical & petroleum, and others. The automotive segment will dominate the palladium market share during the forecast period due to the rising need for decreasing carbon emissions from fossil-fueled vehicles.

With respect to region, the market covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report conducts an in-depth analysis of the market and focuses on critical areas, such as leading product types, end-user industries, and key market players. It also sheds light on the latest market trends and prominent industry developments. Apart from the factors mentioned above, the report covers several other factors that have helped this market grow.

Drivers and Restraints:

Growing Use of Platinum Group Metals in Vehicles to Fuel Market Expansion

The use of Platinum Group Metals (PGMs) is steadily increasing across the automotive industry, despite a decrease in the production and sales of vehicles. The use of catalytic converters in vehicles has increased considerably due to the introduction of stringent regulations with regards to carbon emissions. This scenario has compelled vehicle manufacturing companies to use more PGMs per catalytic converter and develop innovative exhaust treatment systems, which will further strengthen the market growth.

However, the ongoing conflict between Russia and Ukraine can impede the palladium market growth.

Regional Insights:

Asia Pacific to Dominate Market Due to Rapid Expansion of Key Industries

Asia Pacific dominated the global market in 2022 as several industries across the region, such as chemical, automotive, and electronics are growing at a robust pace. The region is considered a hub of these sectors, which is why it has created several lucrative opportunities for the key market players to grow.

Europe is predicted to showcase moderate growth during the forecast timeline due to the declining demand for diesel cars and growing production of hybrid and gasoline vehicles.

Information Source: https://www.fortunebusinessinsights.com/palladium-market-108959

Competitive Landscape:

Market Players to Increase Focus On Capacity Expansions to Cement Their Positions

Sibanye-Stillwater, Anglo American Platinum Limited, Ivanhoe Mines Ltd., Impala Platinum Holdings Limited, and Nornickel are the top market players. These companies are focusing on increasing their production capacities and boosting the network of their recycling plants to fulfill the rising need for eco-friendly products in green hydrogen and automotive applications.

Notable Industry Development:

- July 2023: Nornickel plans to develop a palladium catalyst to tap the future potential of electrolysis technology for water disinfection. As per the company’s plan, the development phase of the catalyst may be completed by the end of 2023.

- February 2022: Heraeus Precious Metals formed a joint venture with BASF that will be built in Pinghu, China, to recover the precious metals from automotive catalysts.

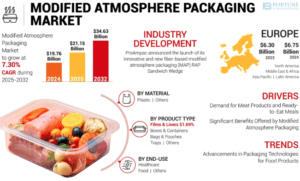

Modified Atmosphere Packaging Market Technological Innovations and Forecast 2025–2032

By ameliasss, 2025-06-10

According to Fortune Business Insights, the global modified atmosphere packaging marke t size was valued at USD 19.76 billion in 2024. The market is projected to be worth USD 21.15 billion in 2025 and reach USD 34.63 billion by 2032, exhibiting a CAGR of 7.30% during the forecast period. Europe dominated the modified atmosphere packaging market with a market share of 34.15% in 2024.

The Modified Atmosphere Packaging (MAP) Market is rapidly gaining traction as the global food and pharmaceutical industries strive for extended shelf life, improved product quality, and reduced food waste. By altering the internal atmosphere of packaging—typically using gases like carbon dioxide, nitrogen, and oxygen—MAP helps preserve freshness, color, flavor, and texture without the need for chemical preservatives.

As consumer demand for fresh, minimally processed food products rises, MAP technology continues to emerge as a critical innovation in modern packaging solutions.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/modified-atmosphere-packaging-market-107311

List of Top Modified Atmosphere Packaging Companies:

- Klöckner Pentaplast (Luxembourg)

- Amcor (Switzerland)

- Mondi (U.K.)

- ProAmpac (U.S.)

- Graphic Packaging International (U.S.)

- Winpak Ltd (Canada)

- StePac (Israel)

- Berry Global (U.S.)

- Coveris (Austria)

- Sealed Air (U.S.)

- Total Packaging Solutions LLC (U.S.)

- Sealpac (Germany)

Key Market Drivers

1. Rising Demand for Packaged and Ready-to-Eat Foods

Busy lifestyles and urbanization have significantly increased the demand for ready-to-eat and packaged foods. MAP helps maintain product freshness and safety during extended distribution and storage, making it ideal for meat, poultry, seafood, dairy, bakery, and fresh produce.

2. Focus on Reducing Food Waste

Governments and consumers are increasingly focusing on sustainability and reducing food waste. MAP extends the shelf life of perishable products, helping reduce spoilage across the supply chain from farm to fork.

3. Technological Advancements in Packaging

Ongoing innovation in high-barrier films, sensors, and gas flushing systems has improved MAP efficiency and cost-effectiveness. Automation and smart packaging technologies further enhance the performance of modified atmosphere systems.

4. Stringent Food Safety Regulations

Globally, regulatory bodies are enforcing stricter guidelines to ensure food quality and safety. MAP complies with these standards by preventing microbial growth and oxidation without the use of artificial additives.

Market Segmentation

By Material

Polyethylene (PE)

Polyethylene Terephthalate (PET)

Polyvinyl Chloride (PVC)

Ethylene Vinyl Alcohol (EVOH)

Others

Polyethylene holds the largest share due to its excellent moisture barrier properties and cost-effectiveness, while PET is gaining momentum for its recyclability and strength.

By Packaging Type

Trays

Bags & Pouches

Films & Wraps

Containers & Boxes

Trays and pouches dominate the market due to their widespread use in fresh meat, seafood, and convenience food packaging.

By Gas Mixture

Carbon Dioxide (CO₂)

Nitrogen (N₂)

Oxygen (O₂)

Others

Carbon dioxide is widely used for its antimicrobial properties, while nitrogen helps in displacing oxygen to prevent oxidation and spoilage.

By Application

Food & Beverages

Pharmaceuticals

Industrial

Others

The food and beverage segment accounts for the largest market share, with applications in meat, dairy, fruits, vegetables, and bakery products. The pharmaceutical sector is also emerging as a key adopter of MAP for sterile and stable packaging.

Regional Insights

North America

North America holds a significant share of the MAP market, driven by high consumer demand for fresh, packaged food and advanced cold chain logistics. The U.S. is a leading market due to strong retail infrastructure and food safety regulations.

Europe

Europe is one of the fastest-growing regions, supported by stringent sustainability policies, strong demand for eco-friendly packaging, and a well-established food processing sector.

Asia-Pacific

The Asia-Pacific region is witnessing rapid growth due to rising urbanization, expansion of the food retail sector, and increasing awareness of food hygiene. Countries like China, India, and Japan are key contributors.

Latin America and Middle East & Africa

These regions are expected to show steady growth, supported by growing disposable incomes, expansion of retail chains, and rising imports of packaged foods.

Key Market Trends

Smart Packaging Integration: Incorporating sensors and indicators to monitor freshness, gas levels, and temperature in real-time.

Sustainable Materials : Growing demand for recyclable and biodegradable packaging films to reduce environmental impact.

Automation and AI : Integration of automated MAP systems in production lines for precise gas flushing and sealing.

Expansion into Non-food Sectors : Use of MAP in pharmaceuticals, electronics, and cosmetics for product preservation.

Information Source: https://www.fortunebusinessinsights.com/modified-atmosphere-packaging-market-107311

Future Outlook

The future of the Modified Atmosphere Packaging market looks promising, with strong opportunities in both developed and developing markets. As sustainability becomes a top priority and technological advancements continue, MAP is set to play a vital role in the global packaging ecosystem. Market players that innovate with eco-friendly materials and digital integration are likely to lead the market in the coming decade.

KEY INDUSTRY DEVELOPMENTS:

June 2023 – A renowned manufacturer in flexible packaging and material science, ProAmpac, announced the launch of its innovative and new fiber-based modified atmosphere packaging (MAP) RAP Sandwich Wedge. The product is launched in the North American market, especially for sandwiches and wraps.

January 2023 – Solidus Solutions invested USD 11.5 million into FUTURLINE, an innovative range of retail-ready packaging solutions such as MAP (Modified Atmosphere Packaging), skin packaging, and punnets that are being rolled out across France, Spain, the U.K., Germany, Benelux, and Poland. The packaging offers more sustainability while maintaining the need for convenience.

According to Fortune Business Insights, the global metal packaging market size was valued at USD 146.70 billion in 2023 and is projected to grow from USD 150.59 billion in 2024 to USD 194.68 billion by 2032, exhibiting a CAGR of 3.26% during the forecast period. North America dominated the metal packaging market with a market share of 34.57% in 2023.

Metal packaging is the packaging solution offered to varied end-use industries with the usage of aluminum and steel. The properties such as recyclability, high density, mechanical durability, toughness, and high thermal conductivity improve its use in various applications. Metal packaging helps to restrict sunlight and keeps the product from safe; hence, an increase in demand is anticipated to drive the market growth.

Fortune Business Insights™ mentioned this in a report titled “ Metal Packaging Market, 2024-2032 .”

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/metal-packaging-market-103867

List of Key Players Present in the Report :

- Ball Corporation (U.S.)

- Crown Holdings Inc. (U.S.)

- Silgan Holdings (U.S.)

- Amcor Limited (Australia)

- Ardagh Group SA (Europe)

- Tata Steel (India)

- Toyo Seikan Group Holdings Inc. (Japan)

- Grief Incorporated (U.S.)

- Ton Yi Industrial (China)

- Can-Pack SA (Netherlands)

- CCL Containers (U.S.)

- Sonoco Products Company (U.S.)

- Mauser Packaging Solutions (U.S.)

- Tubex GmbH (Germany)

- DS Containers Inc. (U.S.)

Segments-

Aluminum Dominates the Market Share Owing to Significant Benefits of the Material

On the basis of material, the market is divided into steel and aluminum. Aluminum dominates the market share. The material consists of properties, such as corrosion-resistant, lightweight, and non-toxic, which increase its usage in several end-use industries. Thus, these factors are expected to propel the metal packaging market growth.

Containers & Cans Segment Holds the Highest Share Due to their High Usage in FMCG Products

According to product type, the market is segregated into containers & cans, bottles & jars, caps & closures, tins, barrels & drums, and others. Containers & cans segment leads the market owing to the surge in demand from end-use industries such as personal care, food and beverages, and household due to their recyclable and versatile properties.

Food & Beverages Leads the Market Owing to Increasing Demand for Metal Packaging in the Food Industry

As per end user, the market is segmented into food & beverages, personal care & cosmetics, pharmaceuticals, paints & varnishes, household, and others. The increasing demand for packaged and processed food products due to the changing lifestyle trends is the key factor propelling the growth of the food & beverages segment.

Geographically, the market is analyzed across North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa.

Report Coverage-

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- Latest industry developments such as product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints-

Increasing Demand for Metal Packaging in Varied Industries Foster the Market Growth

Metal packaging is broadly used in many industries such as personal care & cosmetics, consumer goods, food & beverages, and pharmaceuticals. Rapid growth and demand in these industries are predicted to propel market growth. Due to their longer shelf-life, the extensive use of metals such as aluminum and steel for packaging food & beverage products also fosters global market growth.

Steel has very poor chemical stability, low resistance to acid and alkali, and easily prone to rust. Metal packaging is quite expensive than other packaging materials, so the overall production cost is higher, which is expected to restrict market growth.

Regional Insights-

North America to Dominate the Market Share During the Forecast Period

The largest metal packaging market share is held by North America. The huge reliance on energy drinks and goods and canned in the U.S. also contributes to the rising demand for metal packaging in the North America region.

Asia Pacific led the market growth, followed by North America. The growth is credited to the rapid expansion of the steel industry in the region over the last 10 years.

China is the biggest steel producer, thus contributing to market growth. Europe is a rapidly-growing region due to the rising use of metal cans consisting of alcoholic and non-alcoholic beverages, the growing household, cosmetics industries, personal care, and processed foods.

Information Source: https://www.fortunebusinessinsights.com/metal-packaging-market-103867

Competitive Landscape-

Prominent Players in the Market Witness Noteworthy Growth Opportunities

Key players in the market include Crown Holdings, Ardagh Group, Ball Corporation, Silgan Holdings, Amcor Limited, and others. Numerous other players operating in the industry are focused on providing advanced packaging solutions.

Key Industry Development-

November 2022 – Trivium Packaging announced the launch of a new segment in the packaging market, which can benefit mainly from aluminum bottle packaging, further releasing aluminum bottles for edible oil. The company has adapted its bottle to be feasible for edible oil closures in the U.S.

July 2022 – a leading sustainable aluminum solutions provider, Novelis declared the expansion of its evercycle portfolio specifically designed for the cosmetic packaging market. Evercycle Cosmetics is certified, contains 100% recycled aluminum, and can meet customers' anodized quality requirements.