Adherence Packaging Market Innovations in Medication Compliance Packaging 2025-2032

By ameliasss, 2025-07-04

According to Fortune Business Insights, The global adherence packaging market size was valued at USD 1.13 billion in 2024. It is projected to be worth USD 1.20 billion in 2025 and reach USD 1.89 billion by 2032, exhibiting a CAGR of 6.67% during the forecast period. North America dominated the adherence packaging market with a market share of 38.05% in 2024.

Adherence packaging, also called compliance packaging means the method of packaging that makes the adherence of patients to their drug routine easy. The surge in the emphasis of prominent companies on the enhancement of medication adherence through more patient-focused and intelligent packaging methods, which leads to the generation of data from current delivery systems and medicines while aiding in the reduction of wastage of drugs, is fostering the market growth. Adherence packaging is a specialized method utilized by pharmacies to provide medications in a more systematic and user-friendly way.

Fortune Business Insights presents this information in their report titled " Adherence Packaging Market , 2025–2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/adherence-packaging-market-108330

Major Players Profiled in the Report:

- Westrock Company (U.S.)

- Omnicell Inc. (U.S.)

- Cardinal Health, Inc. (U.S.)

- Keystone Folding Box Co. (U.S.)

- Jones Healthcare Group (Canada)

- CuePath Innovation (Canada)

- Manrex Limited (Canada)

- Medicine-On-Time LLC (U.S.)

- Becton, Dickinson and Company (U.S.)

- ARxIUM, Inc. (U.S.)

Segmentation:

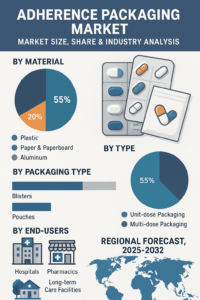

By material, the market is classified into aluminum, paper & paperboard, and plastic. The plastic segment captured the largest adherence packaging market share in 2023. This can be attributed to the cost-effectiveness, transparency, lightweight, and malleable nature of plastic.

In terms of type, the market is bifurcated into multi-dose and unit-dose. The multi-dose segment accounts for the largest share due to the growing requirement for adherence to medication.

Based on packaging type, the market is segregated into pouches and blisters. The blisters segment holds the largest market share. Enhanced shelf-life, ease of transport, and high resistance to tamper provided by blisters are augmenting the segment expansion.

With respect to end users, the market for adherence packaging is segmented into long-term care facilities, pharmacies, and hospitals.

Geographically, the market is divided into the Asia Pacific, Latin America, the Middle East & Africa, Europe, and North America.

Report Coverage

The research report provides a detailed analysis of the major strategic initiatives opted for by leading players in the market. In addition, it highlights the top trends, key industry developments, and the impact of the COVID-19 pandemic on the market growth. Additional aspects of the report include the notable factors impacting the adherence packaging market size.

Drivers:

Surging Desire to Remove Drug Wastage to Impel the Market Growth

The adherence packaging market growth can be credited to a rise in desire for the removal of wastage of the drug. Moreover, medication waste accounts for a substantial impact on the economy and the healthcare system across the globe and creates detrimental consequences for the environment.

Regional Insights:

North America Dominates Due to Rising Life Science & Medical Research Activities

North America accounts for the dominating position in the market. This is due to the growing spending power on healthcare coupled with the surging medical research & life science research activities.

Europe is the second-leading region in the adherence packaging market owing to the heightened availability of government funding for activities pertaining to research and development.

The Asia Pacific market is observing the fastest growth owing to the growing uptake of the solution along with healthcare sector investments.

Competitive Landscape:

Top Players Emphasize Launching New Products to Reinforce Their Industry Position

Mergers & acquisitions, partnerships, and joint ventures are some of the strategies opted for by leading companies to gain a competitive edge in the adherence packaging market. Several firms are also focusing on launching new products to sustain their industry leadership.

Information Source: https://www.fortunebusinessinsights.com/adherence-packaging-market-108330

Key Industry Development

- In April 2024, Gerresheimer partnered with U.S. digital health company RxCap, acquiring a minority stake. Gerresheimer's subsidiary Center aimed at distributing RxCap's adherence solutions in U.S. pharmacies, leveraging its market leadership in prescription vials to enhance pharmacy workflows with smart technology.

- In April 2024, Jones Healthcare Group launched a new line of smart adherence packages that utilizes technology to monitor medication usage and enhance patient engagement.

- In October 2023, JFCRx, a provider of technology solutions and automation for pharmacies, announced its entry into the pharmacy automation market. Founded and managed by experienced professionals in the pharmacy sector, JFCRx offers pouch and blister adherence packaging, inspection systems, and vial fillers for the pharmaceutical market.

India Water Purifier Market Competitive Landscape and Key Players 2025-2032

By ameliasss, 2025-07-03

According to Fortune Business Insights, The India water purifier market size was valued at USD 2.19 billion in 2024. The market is expected to grow from USD 2.54 billion in 2025 to USD 7.72 billion by 2032 at a CAGR of 17.2% during the forecast period.

The India water purifier market is witnessing rapid growth, driven by increasing awareness of waterborne diseases, rising health consciousness, and the need for safe drinking water. With urbanization accelerating and groundwater contamination becoming a concern, water purifiers have become a necessity in Indian households and institutions. The growing urban population, coupled with increasing disposable income, is fostering strong demand for technologically advanced purification systems across urban and semi-urban regions.

Water purifiers are devices designed to remove impurities from water, making it safe for drinking and household use. These systems utilize various filtration technologies—such as reverse osmosis (RO), ultraviolet (UV), and others—to eliminate contaminants. Based on the type of filter used, water purifiers are categorized into different types. They not only improve the taste of water but also provide multiple health benefits by ensuring it is clean and safe for consumption. Widely used in residential, light commercial, and commercial settings, the rising need for clean water coupled with increasing awareness around health and hygiene is significantly boosting the demand for water purifiers.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/india-water-purifier-market-113101

LIST OF KEY PLAYERS PROFILED

- Eureka Forbes Ltd. (India)

- Kent RO Systems Ltd. (India)

- Livpure Smart Homes Pvt Ltd. (India)

- TATA Chemicals Limited (India)

- Franke Faber India Private Limited (India)

- Havells India Limited (India)

- Brita GmbH (Germany)

- A.O. Smith Corporation (U.S.)

- Unilever PLC (U.K.)

- Panasonic Corporation (Japan)

- LG Electronics (South Korea)

- 3M (U.S.)

Key Market Drivers

Rising Health Awareness

Consumers are more aware of waterborne illnesses like cholera, typhoid, and diarrhea, pushing demand for purification systems that ensure safe drinking water.

Government Initiatives and Regulations

Government schemes like ‘Jal Jeevan Mission’ and increased investment in rural water supply infrastructure are further boosting market penetration.

Technological Advancements

Innovations in RO (Reverse Osmosis) , UV (Ultraviolet) , and UF (Ultrafiltration) technologies have led to smarter, more efficient, and IoT-integrated water purifiers that appeal to modern consumers.

Growing Demand in Rural Areas

As rural India continues to face water quality issues, the need for affordable and efficient purifiers is rising, supported by government and NGO outreach programs.

Market Segmentation

By Technology:

RO Purifiers

UV Purifiers

Gravity-Based Purifiers

Multi-Stage Purifiers (RO+UV+UF)

By End-User:

Residential

Commercial (Schools, Offices, Hospitals, etc.)

Industrial

By Sales Channel:

Offline Retail

Online (E-commerce platforms like Amazon, Flipkart)

Regional Insights

Urban Areas : Leading in adoption due to greater awareness and affordability.

Tier II & III Cities : Fastest-growing segment owing to rising income levels.

Rural India : Emerging market with growing opportunities due to water contamination issues and increasing government focus.

Challenges

High Maintenance Costs of advanced RO purifiers.

Lack of Awareness in rural and remote areas.

Water Wastage in RO Systems , which has led to regulatory scrutiny.

Future Outlook (2025–2032)

The India water purifier market is poised for robust growth, fueled by:

Expansion into rural markets.

Emergence of eco-friendly and zero-waste technologies .

Increased adoption of smart water purifiers with IoT and app connectivity.

The India water purifier market is undergoing a transformation as health concerns, technological advancements, and government initiatives converge. With increasing consumer demand and innovation, the market is set to grow significantly through 2032, playing a vital role in improving public health across the country.

The rise in water-borne diseases caused by pathogens such as bacteria, viruses, protozoa, algae, and parasitic worms has intensified public concern over health and hygiene. Drinking water contaminated with these microorganisms can lead to serious illnesses, including diarrhea, cholera, typhoid, and lead poisoning. According to the World Health Organization (WHO), approximately 1.5 million deaths occur globally each year due to water-related diseases, highlighting the urgent need for access to safe and purified drinking water.

Information Source: https://www.fortunebusinessinsights.com/india-water-purifier-market-113101

KEY INDUSTRY DEVELOPMENTS

-

July 2024 - A.O. Smith Corporation signed an agreement for the acquisition of Pureit from Unilever for approximately USD 120 million in cash. The acquisition is expected to be completed by the end of 2024.

- July 2022 - Brita GmbH selected sustainable Styrenics solutions - Terluran ECO, Styrolution PS ECO, and NAS ECO materials for its water filter jugs’ portfolio. The move is expected to enable the company to reduce its carbon footprint significantly.

According to Fortune Business Insights, The global synthetic leather market size is expected to display robust growth during the forecast period of 2025-2032. Synthetic leather is a type of leather produced from artificial sources and has gained significant traction among eco-conscious customers. There are several uses of this leather, such as in car seats, armrests, and headrests. The increasing adoption of synthetic leather due to its high durability and easy usage will drive the market growth.

The furniture and upholstery industry is a major driver of the synthetic leather market. Widely used for upholstering items such as sofas, chairs, recliners, and ottomans, synthetic leather provides the aesthetic and tactile appeal of real leather at a lower cost and with less upkeep. Additionally, rising awareness around animal welfare has led to a growing preference for cruelty-free materials. As an animal-friendly option, synthetic leather is seeing increased adoption, further fueling market growth.

Fortune Business Insights presents this information in a report titled " Synthetic Leather Market, 2025-2032 ."

Request Sample PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/synthetic-leather-market-108674

Major Players Profiled in the Report:

- Kuraray Co. Ltd.

- H.R. Polycoats Pvt. Ltd.

- Alfatex Italia SRL

- Filwel Co., Ltd.

- Yantai Wanhua Synthetic Leather Group Co. Ltd.

- Jasch Industries Limited

- Responsive Industries Ltd.

- San Fang Chemical Industry Co. Ltd.

- Mayur Uniquoters Limited

- Nan Ya Plastics Corporation

- Teijin Cordley Limited

Segments:

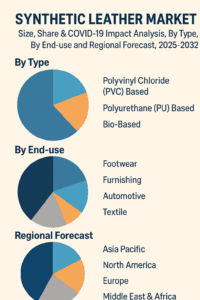

By type, the market is divided into Polyvinyl Chloride (PVC)-based, Polyurethane (PU)-based, and bio-based.

By end-use, the market is segregated into footwear, furnishing, automotive, textile, and others.

With respect to geography, the market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report has conducted a detailed analysis of the market and focused on several critical aspects, such as leading types, end-uses, and top market players. It has also highlighted the most recent market trends and the key developments in the industry. In addition to the factors mentioned above, the report delves into several other factors that have helped the market grow.

The growing demand for bags, wallets, and garments—driven by synthetic leather’s affordability and superior durability—is significantly contributing to market expansion. Ongoing advancements in manufacturing techniques have enhanced the material’s strength, appearance, and overall quality, further accelerating its adoption. Additionally, synthetic leather is widely used in travel bags, suitcases, and other luggage products due to its lightweight nature and resistance to wear and tear, making it an ideal choice for travel-related applications and further propelling market growth.

Share of Major Countries in Global Leather Production

- China - 25%

- India – 6.4%

- Brazil – 9.5%

- Russia – 7.0%

- Africa - 6%

Drivers:

Strong Growth of Automotive Sector to Fuel Market Progress

The automotive industry has witnessed tremendous growth in recent years owing to the rising annual sales of vehicles in both developed and developing countries. This factor has increased the demand for attractive interiors to enhance the overall aesthetic appeal of the car. Synthetic leather is being widely used in these interiors, such as door panels, seats, covers for gear shift, and steering wheels. Since this type of leather gives the overall feel and look of real leather, its demand will rise across the automotive sector.

Regional Insights

Asia Pacific Dominates Global Market Due to High Use in India and China

Asia Pacific is dominating the synthetic leather market share as this material is being widely used in countries, such as India and China.

Moreover, countries across North America, such as the U.S. are also playing a significant role in the regional market’s progress as the country manufactures the largest number of vehicles every year.

Information Source: https://www.fortunebusinessinsights.com/synthetic-leather-market-108674

Competitive Landscape

Key Players to Focus On New Product Launches to Maintain Dominance

Some of the top companies operating in this market include Kuraray Co. Ltd., Alfatex Italia SRL, H.R. Polycoats Pvt. Ltd., Yantai Wanhua Synthetic Leather Group Co. Ltd., Filwel Co. Ltd., Responsive Industries Ltd., and Jasch Industries Ltd., among many others. These market players are focusing on the launch of new products to expand their existing range and maintain their dominance.

Key Industry Development

- April 2023 - General Silicones, a Taiwanese company, announced the launch of vegan synthetic leather with customizable fabric lining used in bags and shoes.

- June 2022 - Kuraray Co., Ltd. announced CLARINO, an artificial leather product that Lenovo Japan has chosen for its ThinkPad Z13 laptop computer series. This product is used in the Lenovo laptop computer series for the first time.

According to Fortune Business Insights, The global blended cement market was valued at USD 371.2 billion in 2024 and is projected to reach USD 500.6 billion by 2032, growing at a compound annual growth rate (CAGR) of 3.8% during the forecast period from 2025 to 2032. In 2024, the Asia Pacific region emerged as the dominant market, accounting for a substantial 70.85% share of the global blended cement market.

Blended cement is a sustainable alternative to traditional cement, in which a portion of the Portland cement clinker is substituted with supplementary materials such as fly ash, slag, silica fume, or calcined clay. This composition enhances the durability, workability, and chemical resistance of the cement, while also optimizing the use of raw materials. One of the primary factors driving its demand is the construction industry's growing commitment to reducing carbon emissions and promoting environmentally friendly building practices. As sustainable construction gains momentum worldwide, the market for blended cement is projected to witness significant growth in the coming years. Governments and private sectors alike are prioritizing green building practices, thus propelling demand.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/blended-cement-market-113035

List of Key Blended Cement Companies Profiled

- HOLCIM (Switzerland)

- UltraTech Cement Ltd. (India)

- Cemex S.A.B DE C.V. (Mexico)

- Heidelberg Materials (U.S.)

- TAIHEIYO CEMENT CORPORATION (Japan)

- JSW Cement (India)

- Dalmia Bharat Limited (India)

- Anhui Conch Cement Co., Ltd. (China)

- Martin Marietta Materials (U.S.)

- Votorantim Cimentos (Brazil)

Key Market Drivers

1. Environmental Sustainability

Blended cement significantly reduces greenhouse gas emissions during production. By using industrial byproducts like fly ash or slag, it helps lower the demand for clinker, which is the most energy-intensive part of cement manufacturing.

2. Government Regulations

Several governments have implemented stringent policies to cut down CO₂ emissions, particularly in the construction industry. This has encouraged the adoption of environmentally friendly cement blends.

3. Cost Efficiency

Blended cement not only reduces carbon emissions but also lowers the overall cost of construction materials. It offers better workability and durability, which can reduce maintenance expenses over time.

4. Rapid Urbanization and Infrastructure Growth

Developing countries are investing heavily in infrastructure projects such as highways, bridges, commercial complexes, and housing. This fuels the demand for high-performance and cost-effective cement solutions.

Market Segmentation

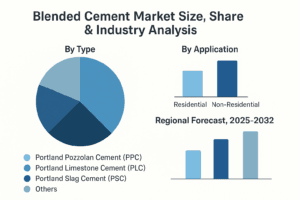

By Type:

- Fly Ash-Based

- Slag-Based

- Silica Fume-Based

- Others (Natural Pozzolans)

By Application:

- Residential Construction

- Commercial Construction

- Infrastructure

- Industrial Projects

By Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Regional Insights

Asia-Pacific:

Asia-Pacific dominates the blended cement market due to rapid infrastructure development in countries like China, India, and Indonesia. Government initiatives such as "Smart Cities" and affordable housing schemes are accelerating market growth.

Europe:

Europe is at the forefront of sustainability and green construction initiatives, making it a strong adopter of blended cement technologies.

North America:

The U.S. market is driven by reconstruction activities, increasing environmental consciousness, and innovations in construction technology.

Challenges

- Variability in Raw Material Quality

- Lack of Awareness in Certain Markets

- Resistance from Traditional Builders

Opportunities

Increasing demand for green buildings

Growing use in marine and infrastructure projects

Technological advancements enabling customized blends

The blended cement market is poised for robust growth, driven by the dual need for sustainable construction practices and cost-effective building solutions. With increasing global emphasis on reducing the carbon footprint of infrastructure, blended cement offers a practical and impactful solution. Players in the industry must continue to innovate and educate the market to unlock its full potential.

The global blended cement market analysis offers comprehensive insights into market size and growth forecasts across all key segments included in the report. It provides an in-depth examination of market dynamics, including drivers, restraints, and emerging trends expected to influence the market throughout the forecast period. The report also presents regional and country-level analyses, highlighting developments in key markets, along with details on new product launches, strategic partnerships, and mergers & acquisitions. Additionally, it features a thorough competitive landscape, including market share analysis and detailed profiles of leading industry players.

Information Source: https://www.fortunebusinessinsights.com/blended-cement-market-113035

KEY INDUSTRY DEVELOPMENTS

-

March 2025: Heidelberg Materials has announced that it will be commissioning an MVR vertical roller mill of the type MVR 5000 C-4 from Gebr Pfeiffer at its existing plant in Airvault, France. The mill will grind and produce ultra-fine Portland cement that will be used in blended cement and other products.

-

February 2025: UltraTech commissioned an additional 0.6 Million Tons Per Annum (MTPA) capacity at its existing plant in West Bengal, India. The move is part of the company’s plan to meet the rising demand for cement.

According to Fortune Business Insights, The global white oil market size was valued at USD 2.88 billion in 2022 and is projected to grow from USD 2.43 billion in 2023 to USD 3.26 billion by 2030, exhibiting a CAGR of 4.3% during the forecast period. Asia Pacific dominated the white oil market with a market share of 59.37% in 2022.

White oil is a complex mixture of hydrocarbons refined intensively from mineral oils. These mineral oils primarily consist of paraffin. They are highly pure, have low toxicity, and possess chemical stability, making them an ideal choice for industries such as personal care, pharmaceuticals, and food. Given that products from these industries come into contact with human skin or are ingested, mineral oils with high purity find widespread use. White oil is a complex mix of various hydrocarbons derived from refining mineral oil. These high-purity oils, with low toxins and chemical stability, find suitability across pharmaceuticals, personal care, and food industries. The broad applications and increased awareness of its benefits are projected to fuel market growth.

Fortune Business Insights™ displays this information in a report titled, "White Oil Market, 2025-2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/white-oil-market-108783

List of Key Companies Profiled In the Report:

- Exxon Mobil Corporation (U.S.)

- Bharat Petroleum Corporation Limited (India)

- Calumet Refining, LLC (U.S.)

- Petro‐Canada Lubricants LLC (Canada)

- RENKERT OIL (U.S.)

- Repsol (Spain)

- A. White Oil Company (U.S.)

- Sasol (South Africa)

- Shell plc (U.K.)

- TotalEnergies (France)

Segmentation:

Use of Pharmaceutical-Grade White Oil to Rise Due to Its Wide-Ranging Applications

Based on grade, the market is categorized into pharmaceutical and technical. The pharmaceutical segment dominated the white oil market share in 2022 and is anticipated to continue its dominance till 2030. The segment’s growth is attributed to the several applications of this type of oil in personal care, cosmetics, and pharmaceuticals.

Personal Care & Cosmetics Industries to Widely Use White Oil Due to Rising Demand for Personal Grooming Products

Based on end-use industry, the market is segmented into pharmaceutical, personal care & cosmetics, food & beverages, textile, plastic & polymer, and others. The personal care & cosmetics segment captured the largest market share in 2022 and is estimated to dominate due to the growing demand for personal grooming products, such as skincare, personal care, and cosmetic items.

With respect to region, the market covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report has conducted an in-depth analysis of the market and focused on key aspects, such as leading product grades, end-use industries, and prominent market players. It also provides important insights into the latest market trends and top industry developments. In addition to the factors mentioned above, the report covers many other factors that have contributed to the market’s progress.

Drivers and Restraints:

Rising Product Use in Pharma Industry to Accelerate Market Expansion

The demand for white oil is increasing in the pharmaceutical industry as it is a major ingredient in many medications and formulations due to its stable, safe, and non-irritation properties. This oil is used in several ointments, oral medicines, lotions, and creams to boost the drug’s solubility, offer lubrication, and improve the efficacy of medicinal products. These factors are expected to fuel the product demand in the pharmaceutical industry, thereby positively influencing the market progress.

However, price fluctuations in raw materials such as crude oil may hinder white oil market growth.

Regional Insights:

Asia Pacific to Dominate Global Market Due to Rapid Expansion of Cosmetics Industry

Asia Pacific is expected to dominate the global market as the region is witnessing robust growth in its personal care and cosmetics industry due to factors such as large-scale urbanization and a growing middle-class population.

North America is also predicted to showcase steady growth due to the notable expansion of the region’s personal care and cosmetics industry.

Information Source: https://www.fortunebusinessinsights.com/white-oil-market-108783

Competitive Landscape:

Leading Market Players to Implement Business Expansion Strategies to Increase Presence

Some of the top market players are formulating a wide range of business expansion strategies to increase their presence and customer base. Some of the key areas where these companies compete include product quality, price, and service. They also focus on expanding their business by developing specialized products for niche applications.

The research report provides a detailed analysis of the market and focuses on crucial aspects, such as leading companies, applications, and products. It also offers insights into the key white oil market trends and highlights vital industry developments. In addition, the report encompasses various factors that have contributed to the growth of the market in recent years.

According to Fortune Business Insights, The global optical coating market size was valued at USD 15.38 billion in 2023 and is projected to grow from USD 16.66 billion in 2024 to USD 30.62 billion by 2032, exhibiting a CAGR of 8.0% during the forecast period. Asia Pacific dominated the optical coatings market with a market share of 47.53% in 2023. Moreover, the optical coatings market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 3.37 billion by 2032, driven by the rising usage of optical coating in the automotive industry.

The rising footfall of thin-film optical coatings across military equipment, semiconductor technologies, solar energy and scientific equipment will augur well for the industry outlook. Technological advancements and rising demand for powerful optical products will drive market growth in the ensuing period.

Major Players Profiled in the Report:

- Jenoptik (Germany)

- SCHOTT (Germany)

- Optimax Systems, Inc. (U.S.)

- Surface Optics Corporation (U.S.)

- GELEST, INC. (U.S.)

- Materion Corporation (U.S.)

- VAMPIRE OPTICAL COATING (U.S.)

- Reynard Corporation (U.S.)

- VIAVI Solutions Inc. (U.S.)

- PPG Industries, Inc. (U.S.)

- DuPont (U.S.)

- ZEISS International (Germany)

- Nippon Electric Glass Co., Ltd. (Japan)

- Newport Corporation (U.S.)

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/optical-coatings-market-102138

Segments

In terms of type, the market is segmented into filter coatings, reflective coatings, anti-reflective coatings, electrochromic coatings, conductive coatings, and others.

Based on the end-use industry, the industry is segregated into telecommunication, consumer electronics, medical, aerospace & defense, transportation, and others.

As per region, the market covers Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage

The report offers a comprehensive perspective of the market size, share, revenue, and volume. It has also delved into Porters’ Five Force Analysis SWOT analysis. Quantitative and qualitative assessments have been used to provide a holistic view of the market. The primary interviews validate assumptions, findings, and the prevailing business scenarios. The report also includes secondary resources such as annual reports, press releases, white papers, and journals.

Drivers and Restraints

Bullish Demand from Telecommunication Sector to Spur Industry Growth

With a surge in optical fiber networks expansion across developing economies, the optical coatings market share could witness an upward trajectory. Optical elements have become sought-after to boost commercial revenue and reduce costs. The rising efficiency standards of thin-film optical filters will redefine the global landscape. Moreover, the rising footfall of anti-reflection coatings will bolster the investment outlook. Considering the application of optical coatings in automotive glazing for versatility, leading companies are poised to inject funds into the landscape.

Meanwhile, the adoption of the evaporation deposition process could lead to systematic failure, thereby impeding the industry growth.

Regional Insights

Asia Pacific to Provide Compelling Opportunities with Investments in Consumer Electronics

Stakeholders project Asia Pacific as a lucrative region in the wake of surging demand for consumer electronics, including cameras, cell phones, laptops, LED TVs, and cameras. Moreover, the rising footprint of video game consoles and personal computers has added fillip to the regional market growth. Asia Pacific market size garnered USD 6.04 billion in 2021 and will witness a similar trend with the rising popularity of consumer electronics.

The North America optical coatings market growth will witness a noticeable gain due to the demand for environment-friendly coatings in semiconductor and sensor applications. Additionally, rising investments from military and defense sectors will propel the demand for beam attenuators, vision cameras, and range finding. Furthermore, the rising footfall of laser systems and aerospace applications will augur well for the industry outlook.

Industry players envisage Europe as a favorable investment region, largely due to increasing privatization, liberalization and competition in the telecommunication sector. Following the application of optical coating solutions in automobile displays, car windows and headlamps, the U.K., France, Germany and Italy could witness investments galore in the ensuing period.

Information Source: https://www.fortunebusinessinsights.com/optical-coatings-market-102138

Competitive Landscape

Stakeholders Focus on Mergers & Acquisitions to Tap into Markets

Leading companies are slated to inject funds into organic and inorganic strategies, including technological advancements, mergers & acquisitions, product rollouts and R&D activities. Moreover, focusing on product offerings could foster a geographical footprint over the next few years.

Key Industry Development

- June 2021 – Jenoptik announced plans to increase its manufacturing capacities and invest in a new office complex at its Dresden, Germany in response to rising demand for sensors for the semiconductor sector and optics.

- March 2021 – Surface Optics Corporation was awarded a Phase II NAVAIR Small Business Innovation Research (SBIR) contract to develop antireflection coatings for aerodynamic missile domes.

Nutraceutical Packaging Market Industry Size, Revenue Share & Dynamics 2025-2032

By ameliasss, 2025-07-01

According to Fortune Business Insights, The global nutraceutical packaging market size was valued at USD 3.90 billion in 2023 and is projected to be worth USD 4.08 billion in 2024 and reach USD 6.24 billion by 2032, exhibiting a CAGR of 5.45% during the forecast period. Moreover, the nutraceutical packaging market in the U.S. is set for steady expansion, reaching USD 1.79 billion by 2032. The rising consumer preference for health supplements and functional foods is fueling the demand for innovative and sustainable packaging solutions. Asia Pacific dominated the nutraceutical packaging market with a market share of 47.69% in 2023.

The rising emphasis on eco-friendly packaging is set to drive the product demand, propelling industry expansion. The use of nutraceutical packaging helps enhance resistance to oxidation and offers protection against contamination.

Fortune Business Insights™ provides this information in its research report, titled “Nutraceutical Packaging Market, 2025-2032”.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/nutraceutical-packaging-market-108091

List of Key Players Mentioned in the Report:

- Avient Corporation (U.S.)

- Glenroy, Inc. (U.S.)

- Maco Pkg (U.S.)

- JohnsByrne (U.S.)

- NuEra Nutraceuticals Inc. (Canada)

- MOD-PAC Corp (U.S.)

- Hughes Enterprises (U.S.)

- Amgraph Packaging (U.S.)

- Elis Packaging Solutions, Inc. (U.S.)

- MRP Solutions (U.S.)

Segmentation:

Plastic Segment Accounts for Prominent Share Owing to Rising Product Usage for Making Jars and Bottles

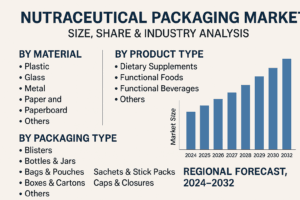

Based on material, the market for nutraceutical packaging is fragmented into metal, plastic, glass, and paper and paperboard. The plastic segment holds a dominant share in the market. This can be attributed to the increasing adoption of various plastic resins for making pouches, jars, and bottles.

Bottles Segment Holds Dominating Share Due to Increasing Product Deployment for Packaging Soft Gels and Pills

By packaging type, the market for nutraceutical packaging is divided into cans & jars, bottles, bags & pouches, and others. The bottles segment leads the market. This is due to the extensive usage of bottles for packaging soft gels, supplements, pills, gummies, capsules, and other products.

Online Retail Stores Segment Records Major Share Impelled by Easy Accessibility and Other Benefits

Based on distribution channel, the market is subdivided into supermarkets & hypermarkets, drug stores & pharmacies, specialty stores, online retail stores, and others. The online retail stores segment holds a dominating share in the market. This is due to an array of benefits provided by online retail stores such as easy accessibility, home delivery services, higher discounts, and affordability.

Based on geography, the market for nutraceutical packaging has been studied across North America, Asia Pacific, Europe, Latin America, and the Middle East & Africa.

Report Coverage:

The report gives an overview of the latest industry trends. It also presents an analysis of the market on the basis of various segments. The market has been studied on the basis of material, packaging type, distribution channel, and geography. The key factors driving the global business landscape have also been presented in the report.

Drivers and Restraints:

Mounting Dietary Supplement Demand to Propel Industry Growth

The increasing demand for nutraceutical products and dietary supplements is driving the nutraceutical packaging market growth. Additional factor favoring industry expansion is the rise in online shopping and e-commerce.

Nevertheless, the industry expansion could be hindered due to the high cost associated with these packaging solutions.

Regional Insights:

North America Holds Dominant Position Owing to Increasing Health Awareness

North America leads the global market. The dominance is due to the growing health awareness in the region.

Europe nutraceutical packaging market share accounts for a significant position in the global market. This is driven by the growing consumption of nutritional supplements and increasing focus on health & fitness.

Information Source: https://www.fortunebusinessinsights.com/nutraceutical-packaging-market-108091

Competitive Landscape:

Major Companies Deploy New Strategies to Sustain Market Competition

Leading companies design and adopt new strategies for strengthening their positions in the global market. Some of these steps comprise merger agreements, partnerships, and the launch of new businesses. Companies are adopting these initiatives to gain an edge over competitors.

Key Industry Development:

- June 2024 – The Keystone Folding Box, a specialist in cardboard packaging, launched a paperboard blister for medical tablets under the Push-Pak brand. The solution's simple push-open system eliminates the need for complicated opening instructions and features a recessed, more efficient push-up layout that reduces package size.

- April 2024 – Berry Global launched two lightweight packages for the protein powder market. The cabin design uses less material than previous models. The combination of the new design and the reduction of cabin air makes the company stand out. The new packaging is part of B Berry's comprehensive product and packaging solutions, which use engineering expertise and proprietary cell technology to reduce the environmental impact of its products.

Pet Food Packaging Market Size and Competitive Outlook for Stakeholders 2025-2032

By ameliasss, 2025-06-27

The global pet food packaging market size was valued at USD 11.38 billion in 2024. The market is projected to grow from USD 12.05 billion in 2025 to USD 18.48 billion by 2032, exhibiting a CAGR of 6.30% during the forecast period.

Packaging has a crucial role in the pet food industry as a protection against aroma loss and a barrier against external factors, including moisture, oxygen, and light. The rising demand for customized printing and graphic printing to attract pet owners is boosting market growth. As a barrier against external influences such as light, moisture, and oxygen, and protection against aroma loss, packaging plays a vital role in the pet food industry. Dogs, in particular, can use their keen sense of smell to detect changes in food aroma and reject their food long before people notice the spoilage.

Fortune Business Insights™ provides this information in its research report, titled “Pet Food Packaging Market, 2025-2032”.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/pet-food-packaging-market-108345

List of Key Players Mentioned in the Report:

- Amcor plc (Switzerland)

- Mondi (U.K.)

- Berry Global (U.S.)

- Huhtamaki (Finland)

- Sonoco Products Company (U.S.)

- Crown (U.S.)

- Transcontinental Inc. (Canada)

- Silgan Holdings Inc. (U.S.)

- Winpak (Canada)

- Sealed Air (U.S.)

- American Packaging Corporation (U.S.)

- Constantia Flexibles (Austria)

- ProAmpac (U.S.)

Segmentation:

Plastic Packaging Leads Market with Superior Durability and Preservation Qualities

In terms of material, the market is divided into metal, plastic, and paper & paperboard. Plastic holds the prominent position favored by its high durability and resistance to oxygen, air, dust, and moisture, effectively preserving the organoleptic properties of the packaged food.

Less Messy Nature of Dry Food to Stimulate Segment Expansion

On the basis of food type, the market is segregated into pet treats, wet food, and dry food. The dry food segment accounts for the major pet food packaging market share as dry food does not possess a strong odor, takes considerably less cleanup time, and is less messy.

Bags & Pouches Segment Dominates Due to Durable Attribute

With respect to product type, the market is classified into jars & containers, boxes & cartons, bags & pouches, cans, and others. The bags & pouches segment registers the largest share as bags & pouches can be easily transported and have a durable nature.

More Active Nature of Dogs to Accelerate Segment Expansion

By pet type, the market is categorized into fish, cat, dog, and others. The dog segment captures the largest market share as dogs offer protection to owners, are more active, and can be trained more.

On the regional front, the market is segmented into the Asia Pacific, Europe , the Middle East & Africa, North America, and Latin America.

Report Coverage

The report provides a comprehensive coverage of the key driving and restraining factors impacting the market growth. In addition, it highlights the latest trends, the COVID-19 pandemic impact, and notable industry developments. Besides this, the report offers vital insights into the strategic initiatives undertaken by market leaders to stand out from the competition.

Drivers and Restraints:

Surging Innovation and the Usage of Smart Packaging in the Pet Food Industry to Fuel Market Growth

Intelligent packaging solutions, including freshness indicators, QR codes, and RFID tags are being deployed increasingly in a frequent manner. Through these technologies, pet owners can access real-time product information with expiration dates, feeding recommendations, and nutritional updates. Thus, these factors are boosting the pet food packaging market growth.

However, issues can be presented by manufacturing packaging products, including containers, bags, and pouches with high barriers, specifically for wet food with renewable sources.

Regional Insights:

Europe Dominates Due to Consistent Surge in Geriatric Population

Europe secures the largest pet food packaging market share. The consistent rise in the geriatric population has resulted in an increase in the number of pet adoptions to enhance the physical and mental health of the pet owner.

Asia Pacific’s market for pet food packaging is witnessing the fastest growth due to the rising younger population.

Competitive Landscape:

Key Companies Leverage Product Innovation Strategies to Broaden Their Portfolio

Berry Global, Sonoco Products Company, Amcor, Huhtamaki, and Sealed Air are some of the prominent companies in the pet food packaging market. Different strategic moves are being adopted by top companies to keep ahead of the competition. Many companies are focusing on innovative pet food packaging solutions for the expansion of their portfolios.

Information Source: https://www.fortunebusinessinsights.com/pet-food-packaging-market-108345

Key Industry Development:

August 2023 - Mondi collaborated with Fressnapf, one of the leaders for pet supplies, to shift their packaging for dry pet food to a new range of premium mono-material recyclable solutions manufactured by Mondi named FlexiBag Recyclable, Recyclable StandUp Pouches, and BarrierPack Recyclable. The mono-material packaging solutions offer strong barrier properties, protecting fat, moisture, and odor, and they are strong and flexible enough to pack and store.

May 2023 - Berry Global, ExxonMobil, and Peel Plastic Products Ltd. collaborated to incorporate International Sustainability and Carbon Certificate (ISCC) PLUS certified-circular plastics into pet food packaging. The collaboration includes advanced recycling technologies from ExxonMobil, which processes plastic waste and attributes it to new plastic for food-grade packaging.