Modified Atmosphere Packaging Market Technological Innovations and Forecast 2025–2032

By ameliasss, 2025-06-10

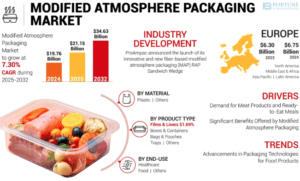

According to Fortune Business Insights, the global modified atmosphere packaging marke t size was valued at USD 19.76 billion in 2024. The market is projected to be worth USD 21.15 billion in 2025 and reach USD 34.63 billion by 2032, exhibiting a CAGR of 7.30% during the forecast period. Europe dominated the modified atmosphere packaging market with a market share of 34.15% in 2024.

The Modified Atmosphere Packaging (MAP) Market is rapidly gaining traction as the global food and pharmaceutical industries strive for extended shelf life, improved product quality, and reduced food waste. By altering the internal atmosphere of packaging—typically using gases like carbon dioxide, nitrogen, and oxygen—MAP helps preserve freshness, color, flavor, and texture without the need for chemical preservatives.

As consumer demand for fresh, minimally processed food products rises, MAP technology continues to emerge as a critical innovation in modern packaging solutions.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/modified-atmosphere-packaging-market-107311

List of Top Modified Atmosphere Packaging Companies:

- Klöckner Pentaplast (Luxembourg)

- Amcor (Switzerland)

- Mondi (U.K.)

- ProAmpac (U.S.)

- Graphic Packaging International (U.S.)

- Winpak Ltd (Canada)

- StePac (Israel)

- Berry Global (U.S.)

- Coveris (Austria)

- Sealed Air (U.S.)

- Total Packaging Solutions LLC (U.S.)

- Sealpac (Germany)

Key Market Drivers

1. Rising Demand for Packaged and Ready-to-Eat Foods

Busy lifestyles and urbanization have significantly increased the demand for ready-to-eat and packaged foods. MAP helps maintain product freshness and safety during extended distribution and storage, making it ideal for meat, poultry, seafood, dairy, bakery, and fresh produce.

2. Focus on Reducing Food Waste

Governments and consumers are increasingly focusing on sustainability and reducing food waste. MAP extends the shelf life of perishable products, helping reduce spoilage across the supply chain from farm to fork.

3. Technological Advancements in Packaging

Ongoing innovation in high-barrier films, sensors, and gas flushing systems has improved MAP efficiency and cost-effectiveness. Automation and smart packaging technologies further enhance the performance of modified atmosphere systems.

4. Stringent Food Safety Regulations

Globally, regulatory bodies are enforcing stricter guidelines to ensure food quality and safety. MAP complies with these standards by preventing microbial growth and oxidation without the use of artificial additives.

Market Segmentation

By Material

Polyethylene (PE)

Polyethylene Terephthalate (PET)

Polyvinyl Chloride (PVC)

Ethylene Vinyl Alcohol (EVOH)

Others

Polyethylene holds the largest share due to its excellent moisture barrier properties and cost-effectiveness, while PET is gaining momentum for its recyclability and strength.

By Packaging Type

Trays

Bags & Pouches

Films & Wraps

Containers & Boxes

Trays and pouches dominate the market due to their widespread use in fresh meat, seafood, and convenience food packaging.

By Gas Mixture

Carbon Dioxide (CO₂)

Nitrogen (N₂)

Oxygen (O₂)

Others

Carbon dioxide is widely used for its antimicrobial properties, while nitrogen helps in displacing oxygen to prevent oxidation and spoilage.

By Application

Food & Beverages

Pharmaceuticals

Industrial

Others

The food and beverage segment accounts for the largest market share, with applications in meat, dairy, fruits, vegetables, and bakery products. The pharmaceutical sector is also emerging as a key adopter of MAP for sterile and stable packaging.

Regional Insights

North America

North America holds a significant share of the MAP market, driven by high consumer demand for fresh, packaged food and advanced cold chain logistics. The U.S. is a leading market due to strong retail infrastructure and food safety regulations.

Europe

Europe is one of the fastest-growing regions, supported by stringent sustainability policies, strong demand for eco-friendly packaging, and a well-established food processing sector.

Asia-Pacific

The Asia-Pacific region is witnessing rapid growth due to rising urbanization, expansion of the food retail sector, and increasing awareness of food hygiene. Countries like China, India, and Japan are key contributors.

Latin America and Middle East & Africa

These regions are expected to show steady growth, supported by growing disposable incomes, expansion of retail chains, and rising imports of packaged foods.

Key Market Trends

Smart Packaging Integration: Incorporating sensors and indicators to monitor freshness, gas levels, and temperature in real-time.

Sustainable Materials : Growing demand for recyclable and biodegradable packaging films to reduce environmental impact.

Automation and AI : Integration of automated MAP systems in production lines for precise gas flushing and sealing.

Expansion into Non-food Sectors : Use of MAP in pharmaceuticals, electronics, and cosmetics for product preservation.

Information Source: https://www.fortunebusinessinsights.com/modified-atmosphere-packaging-market-107311

Future Outlook

The future of the Modified Atmosphere Packaging market looks promising, with strong opportunities in both developed and developing markets. As sustainability becomes a top priority and technological advancements continue, MAP is set to play a vital role in the global packaging ecosystem. Market players that innovate with eco-friendly materials and digital integration are likely to lead the market in the coming decade.

KEY INDUSTRY DEVELOPMENTS:

June 2023 – A renowned manufacturer in flexible packaging and material science, ProAmpac, announced the launch of its innovative and new fiber-based modified atmosphere packaging (MAP) RAP Sandwich Wedge. The product is launched in the North American market, especially for sandwiches and wraps.

January 2023 – Solidus Solutions invested USD 11.5 million into FUTURLINE, an innovative range of retail-ready packaging solutions such as MAP (Modified Atmosphere Packaging), skin packaging, and punnets that are being rolled out across France, Spain, the U.K., Germany, Benelux, and Poland. The packaging offers more sustainability while maintaining the need for convenience.

According to Fortune Business Insights, the global metal packaging market size was valued at USD 146.70 billion in 2023 and is projected to grow from USD 150.59 billion in 2024 to USD 194.68 billion by 2032, exhibiting a CAGR of 3.26% during the forecast period. North America dominated the metal packaging market with a market share of 34.57% in 2023.

Metal packaging is the packaging solution offered to varied end-use industries with the usage of aluminum and steel. The properties such as recyclability, high density, mechanical durability, toughness, and high thermal conductivity improve its use in various applications. Metal packaging helps to restrict sunlight and keeps the product from safe; hence, an increase in demand is anticipated to drive the market growth.

Fortune Business Insights™ mentioned this in a report titled “ Metal Packaging Market, 2024-2032 .”

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/metal-packaging-market-103867

List of Key Players Present in the Report :

- Ball Corporation (U.S.)

- Crown Holdings Inc. (U.S.)

- Silgan Holdings (U.S.)

- Amcor Limited (Australia)

- Ardagh Group SA (Europe)

- Tata Steel (India)

- Toyo Seikan Group Holdings Inc. (Japan)

- Grief Incorporated (U.S.)

- Ton Yi Industrial (China)

- Can-Pack SA (Netherlands)

- CCL Containers (U.S.)

- Sonoco Products Company (U.S.)

- Mauser Packaging Solutions (U.S.)

- Tubex GmbH (Germany)

- DS Containers Inc. (U.S.)

Segments-

Aluminum Dominates the Market Share Owing to Significant Benefits of the Material

On the basis of material, the market is divided into steel and aluminum. Aluminum dominates the market share. The material consists of properties, such as corrosion-resistant, lightweight, and non-toxic, which increase its usage in several end-use industries. Thus, these factors are expected to propel the metal packaging market growth.

Containers & Cans Segment Holds the Highest Share Due to their High Usage in FMCG Products

According to product type, the market is segregated into containers & cans, bottles & jars, caps & closures, tins, barrels & drums, and others. Containers & cans segment leads the market owing to the surge in demand from end-use industries such as personal care, food and beverages, and household due to their recyclable and versatile properties.

Food & Beverages Leads the Market Owing to Increasing Demand for Metal Packaging in the Food Industry

As per end user, the market is segmented into food & beverages, personal care & cosmetics, pharmaceuticals, paints & varnishes, household, and others. The increasing demand for packaged and processed food products due to the changing lifestyle trends is the key factor propelling the growth of the food & beverages segment.

Geographically, the market is analyzed across North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa.

Report Coverage-

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- Latest industry developments such as product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints-

Increasing Demand for Metal Packaging in Varied Industries Foster the Market Growth

Metal packaging is broadly used in many industries such as personal care & cosmetics, consumer goods, food & beverages, and pharmaceuticals. Rapid growth and demand in these industries are predicted to propel market growth. Due to their longer shelf-life, the extensive use of metals such as aluminum and steel for packaging food & beverage products also fosters global market growth.

Steel has very poor chemical stability, low resistance to acid and alkali, and easily prone to rust. Metal packaging is quite expensive than other packaging materials, so the overall production cost is higher, which is expected to restrict market growth.

Regional Insights-

North America to Dominate the Market Share During the Forecast Period

The largest metal packaging market share is held by North America. The huge reliance on energy drinks and goods and canned in the U.S. also contributes to the rising demand for metal packaging in the North America region.

Asia Pacific led the market growth, followed by North America. The growth is credited to the rapid expansion of the steel industry in the region over the last 10 years.

China is the biggest steel producer, thus contributing to market growth. Europe is a rapidly-growing region due to the rising use of metal cans consisting of alcoholic and non-alcoholic beverages, the growing household, cosmetics industries, personal care, and processed foods.

Information Source: https://www.fortunebusinessinsights.com/metal-packaging-market-103867

Competitive Landscape-

Prominent Players in the Market Witness Noteworthy Growth Opportunities

Key players in the market include Crown Holdings, Ardagh Group, Ball Corporation, Silgan Holdings, Amcor Limited, and others. Numerous other players operating in the industry are focused on providing advanced packaging solutions.

Key Industry Development-

November 2022 – Trivium Packaging announced the launch of a new segment in the packaging market, which can benefit mainly from aluminum bottle packaging, further releasing aluminum bottles for edible oil. The company has adapted its bottle to be feasible for edible oil closures in the U.S.

July 2022 – a leading sustainable aluminum solutions provider, Novelis declared the expansion of its evercycle portfolio specifically designed for the cosmetic packaging market. Evercycle Cosmetics is certified, contains 100% recycled aluminum, and can meet customers' anodized quality requirements.

According to Fortune Business Insights, the global titanium dioxide market size was valued at USD 22.28 billion in 2024. The market is projected to grow from USD 24.81 billion in 2025 to USD 40.07 billion by 2032 at a CAGR of 7.1% during the 2025-2032 forecast period. Asia Pacific dominated the titanium dioxide market with a market share of 53.95% in 2024. Titanium dioxide (TiO2) is generally odorless and absorbent that is widely adopted as a pigment for imparting opacity and whiteness to the materials. It is used as an opacifying and bleaching agent in various porcelain enamels that enables them to exhibit properties such as hardness, brightness, and acid resistivity. Owing to its number of unique properties, TiO2 is ideally favored in several different applications such as paints, and plastics, among others. Additionally, they also serve the purpose of insulators and are insoluble in water.

Fortune Business Insights, publishes the information, in its upcoming report, titled “Titanium Dioxide (TiO2) Market Size, Share & Industry Analysis By Grade (Rutile, Anatase), By End-use industry (Paints & coatings, Plastic, Pulp & Paper, Cosmetics, Others) Others and Regional Forecast, 2025-2032.” Te report further observes that the market is witnessing considerable demand from industries such as cosmetics, paper & pulp, plastics, and paints & coatings during the forecast period.

Get a Sample PDF Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/titanium-dioxide-tio2-market-102390

List of the Companies Operating in the Market:

- Tronox Lomon billions

- Cinkarna Celje

- Chemours

- Venator Materials PLC

- KRONOS

- Evonik Industries

- DOGOIDE Group

- GROUP DF

- The Kerala Minerals & Metals Ltd.

- Argex Titanium Inc.

- Among others

What does the Report Include?

The market report includes quantitative and qualitative analysis of several factors such as the key drivers and restraints that will affect market growth. The report provides insights into the regional analysis that covers the different regions, which are contributing to the growth of the market. It includes the competitive landscape that involves leading companies and adoption of strategies by them to introduce new products, announce partnerships, and collaboration that will contribute to the growth of the market between 2019 and 2026. Moreover, the research analyst has adopted several research methodologies such as PESTEL and SWOT analysis to extract information about the current trends and industry developments that will drive the market growth in the forthcoming years.

DRIVING FACTORS

Increasing Focus on Renovation of Buildings to Favor Growth

Rapid Urbanization and high disposable income amongst the population is driving the demand for renovation and construction activities across the globe. The favorable government policies to promote the renovation of damaged, old and defective buildings is anticipated to bode well for the global titanium dioxide (TiO2) market growth during the forecast period. In addition to this, growing infrastructural projects owing to an increasing population worldwide is likely to drive the market in the forthcoming years. Growing investments in the quality infrastructural projects and the majority of the population turning towards urban cities are propelling the demand for construction activities that will favor the market growth.

REGIONAL INSIGHTS

Advent of Residential & Commercial Projects in Asia Pacific to Surge Demand

Among all regions, the market in Asia Pacific is expected to witness significant growth and hold the highest global titanium dioxide (TiO2) market share during the forecast period. This is attributable to increasing focus on developing residential and commercial projects in countries such as China, Vietnam, India, and Philippines in the region. For instance, the India Government plans to construct around 100 new airports by 2032 along with other construction projects that will drive the market in Asia-Pacific. On the other hand, North America is anticipated to witness steady growth in the market during the projected horizon. This is ascribable to factors such as large presence of established production facilities in countries such as the U.S. In addition to this, growing demand from the plastic and cosmetics industry will contribute to the market growth in the region between 2019 and 2026.

Information Source: https://www.fortunebusinessinsights.com/titanium-dioxide-tio2-market-102390

COMPETITIVE LANDSCAPE

Aleddra Launching New De-odorization LED Lamp to Strengthen Demand

In March 2020, Aleddra announced the launch of its patented product, a de-odorization lamp that is designed to purify the air by eliminating bacteria and viruses, along with removing bad odors. The lamp includes a fan that draws bad odor and allows it to pass through a ceramic pre-filter which is coated with titanium dioxide, a photocatalyst material. The photocatalyst material further creates a hyperactive oxidation layer that decomposes the bacteria and viruses into carbon dioxide and water, while purifying the air.

According tp Fortune Business Insights, the global geocomposites market size was valued at USD 447.1 million in 2023 and is projected to grow from USD 476.0 million in 2024 to USD 768.6 million by 2032, exhibiting a CAGR of 6.2% during the forecast period. North America dominated the geocomposites market with a market share of 36.48% in 2023. Rising construction activities and increasing awareness of the material’s benefits are expected to fuel the market development. Fortune Business Insights ™ presents this information in its report titled “ Geocomposites Market, 2024-2032. ”

Geocomposites are used for filtration, reinforcement, separation, and drainage of roads. It increases the durability and strength of soil in roadways, thereby increasing its adoption. Rising construction projects and rapid development fuel the adoption of the product. The construction of railways, highways, roads, and others is likely to increase sales. Further, rising awareness regarding geocomposites' benefits is expected to boost its adoption in several construction projects. In addition, rising focus on infrastructure development by governments worldwide may propel market growth.

Get a Sample PDF Report on Geocomposites Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/geocomposites-market-105292

List of Key Players Profiled in the Report

- CLIMAX SYNTHETICS PVT. LTD. (Gujrat, India)

- TenCate Geosynthetics Americas (Georgia, the U.S.)

- Leggett & Platt, Incorporated (North Carolina, the U.S.)

- GSE Environmental (Texas, the U.S.)

- Thrace Group (Alimos, Greece)

- ABG Ltd. (Meltham, U.K.)

- HUESKER (Gescher, Germany)

- Officine Maccaferri Spa (Bologna, Italy)

- Terram (Maldon, U.K.)

- Ocean Global (New Delhi, India)

- SKAPS Industries (Georgia, the U.S.)

Segments

By product, the market is segmented into geotextile - geogrid composites, geomembrane - geogrid composites, geotextile – geomembrane composites, geotextile - geonet composites, and others. As per function, it is categorized into reinforcement, drainage, separation, and others. Based on application, it is classified into soil reinforcement, landfill & mining, road & highway, water & wastewater management, and others. Regionally, it is grouped into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage

The report provides a detailed analysis of the top segments and the latest trends in the market. It comprehensively discusses the driving and restraining factors and the impact of COVID-19 on the market. Additionally, it examines the regional developments and the strategies undertaken by the market's key players.

Drivers and Restraints

Development in the Construction Sector to Propel Market Progress

Rapid developments in the construction industry and the rising demand for effective materials are expected to boost the product's demand drastically. Governments invest heavily in infrastructure developments to develop cities and provide excellent facilities to citizens, which, in turn, may boost the product demand. Furthermore, the emergence of railroads, highways, constructions, and other projects is likely to bolster the material’s adoption. Moreover, rising investments in redevelopment projects are likely to drive market development. In addition, the rapid adoption of the material in residential building developments is expected to drive the geocomposites market growth.

However, fluctuations in raw material prices are expected to hinder the market's progress.

Regional Insights

Rising Investments in Construction Sector to Bolster Market Development in North America

North America is expected to dominate the geocomposites market share due to government and private sector investments in the construction sector. The market in North America stood at USD 138.7 million in 2020 and is expected to gain a majority of the market share in the coming years. Furthermore, the rapid development of residential buildings, roads, transportation, highways, roads, bridges, and other modern infrastructure is expected to bolster the product demand. These factors may propel the market development.

In Asia Pacific, rising demand for the product from the infrastructure and construction industries is expected to foster market development. Furthermore, rising investments in infrastructure development from China, India, and other Southeast Asian countries are expected to foster the product demand. These factors may propel industry development.

Competitive Landscape

Major Players Focus on Acquisition Strategies to Bolster Market Position

The prominent companies operating in the market deploy acquisition strategies to boost their production capacity and improve their market position. For example, Solomax completed the acquisition of TenCate Geosynthetics in June 2021 to improve its resources, geographic presence, and operational capacity, enabling them to boost its market position globally. Furthermore, companies deploy novel product launches to gather consumer attention and boost sales. This strategy may enable the companies to boost their annual revenues. In addition, the adoption of research and development may enable companies to develop better products and improve their brand image.

Information Source: https://www.fortunebusinessinsights.com/geocomposites-market-105292

Industry Development

- January 2023- Genap signed an exclusive partnership with Watershed Geo, a key geosynthetics manufacturer, for the distribution and installation of ClosureTurf, a synthetic end capping system for landfills.

- February 2022 – Freudenberg Performance Materials, a Germany-based geosynthetics manufacturer, introduced EnkaGrid MAX C, a new geogrid geocomposite. The geocomposite consists of nonwoven geotextiles that are reinforced using geogrids and can provide functions such as separation and filtration in soil media.

Disposable Gloves Market Market Penetration Strategies and Forecast to 2032

By ameliasss, 2025-06-05

According to Fortune Business Insights, the global disposable gloves market size was valued at USD 17.12 billion in 2023 and is projected to grow from USD 19.88 billion in 2024 to USD 51.75 billion by 2032, exhibiting a CAGR of 12.7% during the forecast period. Southeast Asia dominated the disposable gloves market with a market share of 52.69% in 2023. Moreover, the disposable gloves market in the U.S. is projected to grow significantly, reaching an estimated value of USD 3,728.5 million by 2032, driven by the surge in chronic diseases coupled with the rise in the country's aging population.

The gloves that were usually limited to healthcare workers are now commonly utilized by the common public. Since gloves carries a vital role in protection against virus infection, the market witnessed significant growth owing to rising demand from both frontline workers and the general public. The global disposable gloves market share is highly competitive. The products are mainly produced by large firms. Due to the pandemic, small companies have also started glove production leading to a high competitive rivalry rate. Most small companies are focusing on the domestic market.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/disposable-gloves-market-106777

LIST OF KEY COMPANIES PROFILED:

- Top Glove Corporation Bhd (Malaysia)

- Hartalega Holdings Berhad (Malaysia)

- Kossan Rubber Industries Bhd (Malaysia)

- ANSELL LTD (Australia)

- Sempermed (Austria)

- Cardinal Health (U.S.)

- Supermax Corporation Berhad (Malaysia)

- Intco Medical (China)

- Bluesail Medical Co., Ltd. (China)

- Riverstone Holdings Limited (Malaysia)

- YTY Group (Malaysia)

Market Dynamics

Key Growth Drivers

- Healthcare Sector Expansion : The rising number of surgical procedures and diagnostic tests globally has led to increased demand for disposable gloves in medical settings. In the U.S. alone, over 48 million surgeries are performed annually, each requiring multiple glove changes.

- Industrial and Food Safety Regulations : Stricter safety standards in industries such as food processing, pharmaceuticals, and manufacturing have boosted glove usage to prevent contamination and ensure worker safety.

- Post-Pandemic Hygiene Awareness : The COVID-19 pandemic has heightened global awareness of hygiene practices, leading to increased glove usage in both professional and personal settings.

Material Trends

- Nitrile Gloves : Preferred for their durability and resistance to chemicals, nitrile gloves are gaining popularity, especially among users with latex allergies.

- Natural Rubber Gloves : Despite the rise of synthetic alternatives, natural rubber gloves remain significant, accounting for 36.4% of global revenue demand in 2024.

- Powder-Free Gloves : Due to concerns over allergic reactions and contamination, powder-free gloves have become the dominant product segment, holding 75% market share in 2023.

Regional Insights

- North America : Leading the market with a 37.41% share in 2024, driven by a well-established healthcare system and stringent safety regulations.

- Asia-Pacific : Expected to witness the fastest growth due to rapid industrialization, urbanization, and healthcare infrastructure development in countries like China and India.

- Europe : Maintains a significant market presence, with increasing demand for sustainable and biodegradable glove options in response to environmental concerns.

Challenges and Opportunities

Challenges

- Raw Material Price Volatility : Fluctuations in the prices of latex, nitrile, and vinyl can impact manufacturing costs and supply stability.

- Environmental Concerns : The disposal of non-biodegradable gloves contributes to environmental pollution, prompting calls for more sustainable solutions.

Opportunities

- Biodegradable Gloves : Growing demand for eco-friendly products is encouraging manufacturers to develop gloves made from biodegradable materials.

- Technological Advancements : Innovations in glove design, such as enhanced grip and touchscreen compatibility, are expanding their applicability across various sectors.

The disposable gloves market is poised for continued growth, driven by increased hygiene awareness, regulatory requirements, and technological innovations. While challenges such as raw material price volatility and environmental concerns persist, opportunities in biodegradable products and advanced glove technologies offer promising avenues for market expansion.

Information Source: https://www.fortunebusinessinsights.com/disposable-gloves-market-106777

KEY INDUSTRY DEVELOPMENTS :

January 2021 – Ansell Limited, completed the acquisition of the Primus brand and related assets that consist of the Life Science business belonging to Primus Gloves and Sanrea Healthcare Products (“Primus”). In addition, Ansell and Primus have entered into a long-term supply partnership. Primus is an Indian manufacturer and marketer of gloves sold in the Life Science and Specialty Medical sectors and is one of the few global producers of long cuff gloves with strong brand recognition. This acquisition increases the company’s presence in this important Indian market and provides them with the opportunity to further speed up the growth of their Life Sciences business.

May 2021 - Honeywell and Premier Inc. established a new business partnership aimed at increasing nitrile exam glove production in the U.S. In the first year alone, this new alliance is estimated to create at least 750 million nitrile test gloves. The partnership is anticipated to provide access to domestically produced exam gloves for hospitals, clinics, and other healthcare professionals in the U.S.

Gypsum Board Market End-Use Sector Insights and Key Developments – 2025-2032

By ameliasss, 2025-06-04

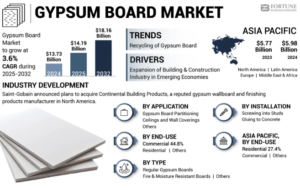

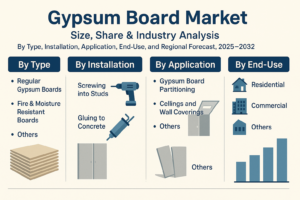

According to a report published by Fortune Business Insights, titled “ Gypsum Board Market Size, Share & Industry Analysis, By Type (Regular Gypsum Boards, Fire & Moisture Resistant Boards, and Others), By Installation (Screwing into Studs and Gluing to Concrete), By Application (Gypsum Board Partitioning, Ceilings and Wall Coverings, and Others), By End-Use (Residential, Commercial, and Others), and Regional Forecast, 2025-2032. ”

The global gypsum board market size was valued USD 13.73 billion in 2024. The market is projected to grow from USD 14.19 billion in 2025 to USD 18.16 billion by 2032 at a CAGR of 3.6% during the forecast period. Asia Pacific dominated the gypsum board market with a market share of 43.55% in 2024.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/gypsum-board-market-102718

List of companies profiled in the report:

- Saint-Gobain

- Knauf

- USG Corporation

- National Gypsum Company

- Yoshino Gypsum Co. Ltd.

- USG Boral

- Eagle Materials Inc.

- China National Building Material Co., Ltd.

- Taishan Gypsum Co., Ltd

- Fletcher Building

- Cabot Gypsum ULC

A gypsum board is a type of material that is used as a dry wall in several infrastructure construction activities. Accounting to the exceptional properties of the product such as low cost, ease of installation, and resistance to external factors such as water and fire, the product is being widely adopted by major businesses across the world. The presence of several large scale companies, coupled with the variations in product offerings will have a positive impact on the growth of the overall market in the coming years. The emphasis recycling products will create a subsequent demand for gypsum boards across the world. Increasing environmental concerns and depletion of resources have been the triggering factors that have encouraged manufacturers to incorporate dry walls or gypsum boards. The rising construction activities as well as industrialization will open up a huge potential for the companies operating in the global market.

Increasing Number of Company Mergers and Collaborations Will Aid Growth

The report encompasses several factors that have made influenced the growth of the market in recent years. With a bid to acquiring a wider customer base, several large scale companies are looking to acquire smaller and medium enterprises. A few of the major company mergers have been highlighted in the report. In November 2019, Saint-Gobain announced that it has completed the acquisition of Continental Building Products. The company is a US based manufacturer of construction materials and through its acquisition, Saint-Gobain will look to strengthen its portfolio of gypsum products. Saint-Gobain’s latest acquisition will have a huge impact on the growth of the gypsum board market in the forthcoming years.

Asia Pacific Currently Dominates the Market; Rising Construction Activities to Aid Growth

The report analyzes the ongoing gypsum board market trends across North America, Latin America, Asia Pacific, the Middle East and Africa, and Europe. Among these regions, the market in Asia Pacific currently dominates the market. The constantly rising construction activities, coupled with the increasing industrialization in emerging countries such as India, China, and Japan will aid the growth of the market. Besides Asia Pacific, the market in North America will also witness considerable growth in the coming years. As of 2018, the market in North America was worth USD 16.21 billion and this value is likely to increase further in the coming years.

Gypsum board is one of the most consumed gypsum products in the world. It is predominantly used for ceiling and partition wall applications in the construction industry. Several types of these boards are available in the market including regular boards, moisture resistant boards, fire resistant boards, mobile boards, pre-decorated boards, and others. Regular board is the most commonly used type in the global market.

Information Source: https://www.fortunebusinessinsights.com/gypsum-board-market-102718

Industry Developments

April 2024 - Saint-Gobain Gyproc became the first company in India to produce low-carbon plasters, reducing the global warming potential by 40% over their lifetime. Gypsum plaster is the most effective alternative to traditional cement plaster, offering superior finish. Fewer cracks, zero cement, significant water & energy savings, and increased productivity are boosting its adoption.

October 2023 - Saint-Gobain announced the remaining acquisition of assets and equity interest of Seven Hills Paperboard LLC which also includes a gypsum paper board liner manufacturing facility from its joint venture partner WestRock. The acquisition provided Saint-Gobain with greater control over the supply of critical raw materials and components necessary to manufacture boards and related products. April 2023 - Saint-Gobain began producing plasterboard in Norway using a 100% decarbonized process. Switching from natural gas to hydroelectric power enabled decarbonization of the industrial process, reducing CO2 emission by 23,000 tons annually. Modernization of the plant, better heat recovery, and process efficiency led to a 30% reduction in energy use.

The global bioplastics packaging market size was valued at USD 6.33 billion in 2024. The market is projected to grow from USD 6.92 billion in 2025 to USD 14.07 billion by 2032, exhibiting a CAGR of 10.67% during the forecast period. Asia Pacific dominated the bioplastics packaging market with a market share of 42.18% in 2024.

Bioplastic packaging, made from bio-based and biodegradable materials, serves various sectors such as food & beverage and personal care. Unlike traditional petroleum-based plastics, bioplastics decompose faster and emit fewer greenhouse gases. The rising demand for sustainable packaging has fuelled the growth of the market. The market offers packaging made from renewable resources such as corn, sugarcane, and cassava, which have favorable properties such as recyclability, renewability, and durability. The packaging also extends the shelf life of perishable foods and protects products from contamination, making them suitable for various packaging applications.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/bioplastic-packaging-market-108066

List of Key Players Mentioned in the Report:

- Corbion N.V. (Netherlands)

- Coveris (U.K.)

- Bio Futura (Netherlands)

- Safepack Packaging Solutions (India)

- Amcor Plc. (Australia)

- PLAMFG (U.S.)

- Plantic Technologies (Australia)

- Futamura Group (Japan)

- NatureWorks LLC (U.S.)

- Polymateria Ltd. (U.K.)

Segmentation:

Biodegradable Segment Leads owing to Manufacturer Sustainability Goals

On the basis of material, the market is divided into polybutylene succinate (PBS), biodegradable (starch blends, polylactic acid (PLA), polybutylene adipate terephthalate (PBAT), polyhydroxyalkanoates (PHA), and others), bio-based/non-biodegradable (bio polyethylene terephthalate (PET), bio polyethylene (PE), bio polyamide (PA), bio poly trimethylene terephthalate (PTT), and others). The biodegradable material segment secures the largest bioplastics packaging market share. Increasing prioritization of sustainability by manufacturers is leading to the integration of biodegradable materials, boosting the growth of the segment.

Rigid Packaging Segment Dominates Owing to Advancements in Material and Sustainability

On the basis of packaging type, the market is bifurcated into rigid packaging and flexible packaging. The Rigid packaging segment leads the market. Innovations in bioplastic materials and shift toward sustainable packaging solutions are boosting the use of bioplastic in rigid packaging, enhancing shelf appeal and meeting market demands.

Food & Beverage Segment Dominated Owing to Increased Production Capacity

In terms of end-use industry, the market is divided into food & beverages, pharmaceuticals, cosmetic & personal care, consumer goods, and others. The food & beverages segment is set to led the key bioplastics packaging market share. Expansion in food and beverage production capacity drives demand for packaging solutions, including bioplastics, contributing to segment growth.

Bottle Segment Leads Owing to Growing Focus on Sustainable Packaging

In terms of product type, the market is classified into bottles, cups, trays, clamshell, bags, pouch & sachet, and others. The bottle segment dominates with a rising emphasis on sustainable packaging. Key trends include advancements in biopolymer technology to improve durability and recyclability, alongside a shift towards more compostable options.

In terms of region, the market for bioplastics packaging is categorized into Europe, North America, the Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

This market research report provides an in-depth analysis, focusing on top companies, product/service types, Porter’s five forces, key end-use industries, and competitive dynamics. It also examines significant industry developments, market trends, and factors contributing to recent market growth.

Drivers and Restraints:

Rising Bio-based and Biodegradable Packaging Materials Among Manufacturers to Spur Market Growth

Increasing awareness of plastic pollution is driving demand for the product, which offer recyclability and reduced environmental impact. Moreover, growing calls for sustainable food packaging solutions are prompting innovations in bioplastics, attracting new players and fostering bioplastics packaging market growth and competition.

However, competition for biomass feedstocks and irregular supply due to climatic and geopolitical factors restricts bioplastic production scalability.

Regional Insights:

Asia Pacific Dominates the Market Owing to Expanding Population

The Asia Pacific region holds the top position in this market, largely propelled by its burgeoning population. Emerging countries within the region are poised to witness heightened demand for bioplastics packaging, spurred by growth in local electronics and food & beverages sectors.

The Middle East's evolving lifestyle, fuelled by rising disposable incomes, is driving higher demand for convenience food and contributing to growth in the bioplastic packaging market.

Information Source: https://www.fortunebusinessinsights.com/bioplastic-packaging-market-1080

Key Industry Development:

January 2024 – A leader in the sustainable packaging industry, Print & Pack, launched a new era of eco-friendly packaging solutions tailored for small businesses and eco-conscious brands across North America.

December 2023 – Melodea launched MelOx NGen, a high-performance barrier product designed to enhance the recyclability of plastic food packaging and other applications. This water-based and plant-sourced coating is designed to be applied to various types of packaging materials such as films, pouches, bags, lids, and blister packs.

Packaging Waste Management Market Dynamics and Policy Impact Review 2025–2032

By ameliasss, 2025-06-02

According to Fortune Business Insights, the global packaging waste management market size was valued at USD 92.19 billion in 2024. It is projected to be worth USD 96.53 billion in 2025 and reach USD 137.15 billion by 2032, exhibiting a CAGR of 5.15% during the forecast period. Asia Pacific dominated the packaging waste management market with a market share of 31.45% in 2024.

Packaging waste management is the process of reducing, reusing, and recycling packaging waste. It helps to reduce environmental impact and conserve resources. According to the Organization for Economic Co-operation and Development, global plastic waste production doubled from 2000 to 2019, reaching 353 million tonnes. Almost two-thirds of plastic waste originates from plastics production that lasts less than five years, with 40% arising from packaging, 12% from consumer products, and 11% from apparel and textiles. The Packaging Waste Management Market is gaining significant momentum as global awareness of environmental sustainability increases. With the growing consumption of packaged goods and the resulting waste, effective waste management solutions are becoming essential. Governments, businesses, and consumers are driving demand for eco-friendly packaging and sustainable waste management practices.

Get a Sample PDF Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/packaging-waste-management-market-112352

List of the Key Companies Profiled in the Report:

- BEWI (Austria)

- Frigorifico Allana Pvt. Ltd. (Austria)

- Bayer AG (Austria)

- ITENE (Austria)

- Merivaara Corporation (Austria)

- Greenbank Recycling Solutions (U.K.)

- Stevcon Packaging & Logistics Ltd (Austria)

- JBS (Austria)

- WM Intellectual Property Holdings, L.L.C. (U.S.)

- PreZero International (Austria)

- Affordable Waste Management Ltd. (Austria)

What is Packaging Waste Management?

Packaging waste management involves the collection, sorting, recycling, and disposal of packaging materials such as plastics, paper, glass, metals, and bioplastics. These practices aim to minimize the environmental impact of packaging waste, promote resource efficiency, and support a circular economy.

Market Overview

According to industry analysts, the global packaging waste management market size was valued at USD 92.19 billion in 2024. It is projected to be worth USD 96.53 billion in 2025 and reach USD 137.15 billion by 2032, exhibiting a CAGR of 5.15% during the forecast period. This growth is driven by:

Stringent government regulations on packaging disposal

Rising demand for recyclable and biodegradable packaging

Increased consumer awareness of environmental issues

Rapid urbanization and industrialization

Key Market Segments

1. By Material Type

Plastic (PET, HDPE, LDPE, etc.)

Paper & Paperboard

Glass

Metal

Biodegradable materials

2. By Waste Management Method

Recycling

Landfilling

Incineration

Composting

3. By End-Use Industry

Food & Beverage

Healthcare

Cosmetics & Personal Care

E-commerce & Retail

Industrial Packaging

Market Drivers

✅ Government Regulations

Regulatory frameworks such as the European Union’s Packaging and Packaging Waste Directive (PPWD) and Extended Producer Responsibility (EPR) policies worldwide are pushing industries to adopt sustainable packaging and effective waste management strategies.

✅ Corporate Sustainability Goals

Brands like Unilever, Coca-Cola, and Nestlé are leading efforts to reduce plastic usage and improve recyclability, spurring demand for advanced packaging waste management solutions.

✅ Technological Advancements

Innovations in AI-based waste sorting , chemical recycling , and smart bins are revolutionizing the efficiency of waste collection and processing.

Challenges

High costs of advanced recycling technologies

Lack of infrastructure in emerging economies

Consumer resistance to higher-priced sustainable packaging

Contamination of recyclables leading to landfill disposal

Regional Insights

North America

A mature market with strong regulations and recycling infrastructure. The U.S. leads in technological innovation in waste management.

Europe

The most advanced region in packaging waste legislation. Countries like Germany and Sweden have some of the highest recycling rates globally.

Asia-Pacific

A rapidly growing market, especially in China, India, and Southeast Asia, driven by urban population growth and rising environmental concerns.

Future Outlook

The packaging waste management market will continue to evolve with greater integration of:

Circular economy models

Public-private partnerships

Sustainable packaging materials

Blockchain and IoT for waste tracking

By 2030, a significant portion of packaging waste is expected to be redirected from landfills to recycling and recovery facilities , contributing to a cleaner environment and more sustainable industries.

The packaging waste management market plays a pivotal role in addressing the global packaging pollution crisis. As regulatory pressure and consumer expectations increase, companies must invest in sustainable solutions to remain competitive and responsible. The future of packaging lies not just in how it protects products—but in how we manage what’s left behind.

Information Source: https://www.fortunebusinessinsights.com/packaging-waste-management-market-112352

KEY INDUSTRY DEVELOPMENTS

-

In December 2024, Bisleri International Pvt. Ltd, in collaboration with Sampurn(e)arth Environment Solutions Pvt. Ltd. and the Mineral Foundation of Goa, launches a Material Recovery Facility (MRF) Center in Harvalem, Goa. The facility is designed to handle 360 MT of plastic waste each year. Bisleri's 'Bottles for Change' program seeks to reduce plastic waste in landfills and foster a cleaner, more sustainable ecosystem in the area. The facility will mostly focus on promoting 100% plastic waste separation at the source, beginning with the Curchorem-Cacora area.

-

In October 2024, At the PPMA Show, Waste Mission, a prominent UK waste management firm, introduced its tailor-made Waste Management Portal. This cutting-edge platform is tailored exclusively for contracted clients, allowing them to handle their waste more efficiently and sustainably than ever while keeping them informed about waste streams, compliance, and ESG goals.