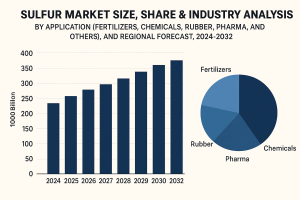

According to Fortune Business Insights, The global sulfur market was valued at USD 6.04 billion in 2023 and is expected to increase from USD 6.23 billion in 2024 to USD 7.99 billion by 2032, reflecting a CAGR of 3.6% during the forecast period (2024–2032). Asia Pacific held the largest share of the market, accounting for 34.11% in 2023. In addition, the U.S. sulfur market is anticipated to witness substantial growth, reaching approximately USD 941.0 million by 2032. This growth is primarily driven by the expanding agricultural sector, as sulfur plays a crucial role in fertilizer production, especially in manufacturing sulfuric acid—an essential component for phosphate fertilizers.

According to Fortune Business Insights, The global neopentyl glycol market was valued at USD 1,327.7 million in 2024 and is anticipated to increase from USD 1,407.1 million in 2025 to USD 2,219.1 million by 2032, registering a CAGR of 6.7% during the forecast period. Asia Pacific held the largest share of 44.16% in 2024, leading the global market.

Neopentyl Glycol (NPG) is a multifunctional chemical widely used across diverse industries. It serves as a key raw material in the production of polyester resins, coatings, and lubricants. The market growth is primarily fueled by the increasing utilization of NPG in automotive coatings, powder coatings, and construction materials. Its superior durability, weather resistance, and environmentally friendly attributes make it a preferred choice for manufacturers. This growth is driven by rising demand across coatings, resins, lubricants, and plasticizers industries, supported by expanding automotive and construction activities worldwide.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/neopentyl-glycol-market-110106

Market Dynamics

Key Growth Drivers

Increasing demand from coatings and resins:

Neopentyl glycol is a vital component in polyester and alkyd resins used for automotive, industrial, and powder coatings. Its ability to enhance chemical resistance, hardness, and weather durability fuels its consumption in these applications.

Automotive industry expansion:

With rising global automobile production and demand for durable, lightweight coatings, NPG usage continues to grow in automotive surface treatments and high-performance coatings.

Industrial lubricants and plasticizers:

NPG-derived esters are widely used as lubricants and plasticizers, improving performance and longevity in various industrial products.

Technological advancements and sustainability:

Manufacturers are focusing on developing environmentally friendly NPG production methods and bio-based derivatives to meet regulatory standards and reduce environmental impact.

Market Segmentation

By Grade

Flakes

Molten

Slurry

Each grade serves specific industrial requirements, depending on storage, transportation, and processing needs.

By Application

Coatings & Resins

Plasticizers

Lubricants

Others

Among these, coatings and resins hold the largest market share due to NPG’s extensive use in producing durable and weather-resistant paints.

By End-Use Industry

Automotive

Construction

Electronics

Pharmaceutical

Others

The automotive and construction sectors lead global consumption, supported by infrastructure growth and vehicle production.

Regional Insights

Asia Pacific

Asia Pacific dominates the Neopentyl Glycol market, driven by large-scale manufacturing activities in China, India, Japan, and South Korea . Growing industrialization, automotive output, and coating applications contribute to strong regional demand.

Europe

Europe represents a mature market supported by well-established coating and resin industries. Stringent environmental regulations are also encouraging the adoption of advanced and sustainable NPG-based formulations.

North America

The North American market benefits from high demand in industrial coatings, automotive refinishing, and specialty chemicals, with the U.S. as a key contributor.

Rest of the World

Emerging economies in Latin America and the Middle East are witnessing gradual growth in NPG usage, driven by construction and industrial developments.

Competitive Landscape

Leading market participants are focusing on:

LIST OF KEY NEOPENTYL GLYCOL COMPANIES PROFILED

- LG Chem (South Korea)

- Perstorp Holding AB (Sweden)

- BASF (Germany)

- OQ Chemical GmbH (Germany)

- MITSUBISHI GAS CHEMICAL COMPANY, INC. (Japan)

- Eastman Chemical Company (U.S.)

- Zibo Ruibao Chemical Co., LTD. (China)

- Ataman Chemicals (Istanbul)

- The Chemical Company (U.S.)

- DHALOP CHEMICALS (India)

Companies are also pursuing mergers and strategic collaborations to enhance market presence and product portfolios.

Opportunities and Challenges

Opportunities

Rising adoption of powder coatings in the automotive and construction industries.

Growing trend toward green chemistry and sustainable production routes.

Increasing investments in emerging markets for coating and lubricant applications.

Challenges

Fluctuations in raw material prices affecting production costs.

Environmental regulations related to chemical manufacturing.

Competition from alternative polyols in certain applications.

Key Market Highlights

2024 Market Size: USD 1,327.7 million

2025 Market Value: USD 1,407.1 million

2032 Forecast: USD 2,219.1 million

CAGR (2025–2032): 6.7%

Dominant Region: Asia Pacific

Top Applications: Coatings & Resins, Lubricants, Plasticizers

The Neopentyl Glycol Market is poised for steady growth through 2032, fueled by expanding applications in coatings, automotive, and construction industries. Its chemical stability, resistance to oxidation, and compatibility with eco-friendly technologies position it as a key material for next-generation coatings and resins.

Manufacturers investing in bio-based innovations , capacity expansions , and regional market development are likely to capture significant opportunities during the forecast period.

Information Source: https://www.fortunebusinessinsights.com/neopentyl-glycol-market-110106

KEY INDUSTRY DEVELOPMENTS

- July 2023 : Zhejiang Guanghua Technology Co., Ltd. and BASF entered a letter of intent to provide Neopentyl glycol from the Zhanjiang Verbund site to KHUA. This collaboration will help BASF cater to the increasing demand for low-emission powder coatings in the Asia Pacific region and China.

- October 2022: BASF invested in a new Neopentyl glycol in China with a production capacity of 80,000 metric tons. The new plant will boost BASF’s Neopentyl glycol capacity to 335,000 metric tons annually. The new plant will mainly cater to the growing demand for powder coatings in China.

Posted in: Business

| 0 comments

Caustic Soda Market Industry Insights, Trends, Size & Forecast to USD 55,557.7 Million by 2027

By ameliasss, 2025-10-17

The global caustic soda market was valued at USD 44,959.2 million in 2019 and is expected to grow to USD 55,557.7 million by 2027, registering a CAGR of 3.1% during the forecast period. Asia Pacific emerged as the leading region, accounting for 56.23% of the total market share in 2019.

Caustic soda serves as a fundamental raw material in the production of various essential products, including plastics, pharmaceuticals, and water treatment additives. It is produced through the electrolysis of sodium chloride solution using technologies such as diaphragm cells or membrane cells. Major end-use industries driving demand for caustic soda include pulp and paper, detergents, alumina, oil and gas, textiles, and chemicals. The increasing demand for caustic soda across diverse industries such as paper & pulp, textiles, chemicals, and water treatment is expected to fuel market expansion globally.

Key Market Insights

Caustic soda, also known as sodium hydroxide (NaOH), is a vital industrial chemical used in a wide range of manufacturing processes. It serves as an essential raw material for producing alumina, soaps, detergents, and petroleum products. The growing demand for these end-use applications, coupled with expanding industrialization in emerging economies, drives the market’s steady growth trajectory.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/caustic-soda-market-104711

Driving Factors

Rising Demand from the Pulp and Paper Industry

Increasing consumption of paper-based products and packaging materials boosts caustic soda use for pulp digestion and paper bleaching.

Expanding Chemical Manufacturing Sector

Caustic soda acts as a key reactant in producing various chemicals, including solvents, plastics, and synthetic fibers, enhancing its market value.

Growing Application in Water Treatment

Rapid urbanization and rising concerns about clean water availability are increasing the adoption of caustic soda for pH regulation and water purification processes.

Restraining Factors

Despite positive growth prospects, fluctuations in raw material prices and stringent environmental regulations on chemical production may hinder market expansion to some extent.

Market Segmentation

By Form: Lye, Flake, Pellet

By Application: Alumina, Pulp & Paper, Organic Chemicals, Inorganic Chemicals, Textiles, Water Treatment, Others

By Region: North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Regional Insights

Asia Pacific dominated the caustic soda market in 2023, holding over 50% of the global share . The region’s strong industrial base in China, India, and Japan supports the growth of paper, textile, and alumina industries. Meanwhile, North America and Europe show steady demand due to the chemical and manufacturing sectors' stability and growing water treatment applications.

Competitive Landscape

Leading companies are investing in technological advancements and sustainable production methods to minimize environmental impact and enhance product efficiency. Major players operating in the global caustic soda market include:

- Olin Corporation (Clayton, Missouri, United States)

- Tata Chemicals Limited (India)

- Aditya Birla Chemicals (India) Limited (India)

- Gujarat Alkalies and Chemical Limited (India)

- Occidental Petroleum Corporation (OXY) (Houston, Texas, United States)

- Formosa Plastics Corporation (Taiwan)

- PPG Industries (Pittsburgh, Pennsylvania, United States)

- Xinjiang Zhongtai Chemical Co., Ltd. (China)

- Hanwha Chemical (South Korea)

- Brenntag North America, Inc. (North America)

Strategic mergers, capacity expansions, and innovations in membrane cell technology are helping these companies strengthen their market position.

Information Source: https://www.fortunebusinessinsights.com/caustic-soda-market-104711

Future Outlook

The caustic soda market is poised for steady growth over the next decade, driven by ongoing industrialization, the shift toward sustainable manufacturing, and consistent demand from key downstream sectors. The integration of green chemistry and energy-efficient production methods will further shape the market dynamics through 2032.

Conclusion:

The Caustic Soda Market continues to show promising potential, supported by growing applications in manufacturing and environmental sectors. With sustainability becoming a key focus, market players are expected to emphasize cleaner production processes and efficient resource utilization, ensuring long-term market stability and profitability.

KEY INDUSTRY DEVELOPMENTS:

- In May 2021, Olin Corporation announced the reduction in the Chlor alkali production capacity by shutting down 20% of its diaphragm grade at its Plaquemine facility.

- In January 2021 , the GACL-NALCO Alkalies & Chemicals Ltd (GNAL) delayed the commissioning of the new caustic soda production line to August 2021. The production facility is situated at Dahej and has a production capacity of 266667 tons/year for caustic soda.

Posted in: Business

| 0 comments

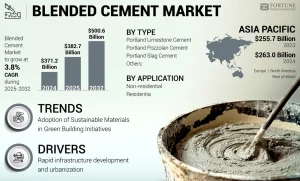

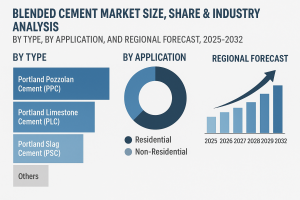

According to Fortune Business Insights, The global blended cement market is experiencing significant growth due to rising demand for sustainable construction materials, strict environmental regulations, and increasing global infrastructure development. Blended cement, made by combining Ordinary Portland Cement (OPC) with supplementary cementitious materials (SCMs) such as fly ash, slag, silica fume, or limestone, helps reduce CO₂ emissions while enhancing strength, durability, and workability.

As the construction industry focuses more on eco-friendly and cost-effective building materials, blended cement has become a vital component of modern infrastructure development worldwide.

Market Size and Growth Forecast

The global blended cement market size was valued at USD 371.2 billion in 2024. The market is projected to grow from USD 382.7 billion in 2025 to USD 500.6 billion by 2032, exhibiting a CAGR of 3.8% during the forecast period. Asia Pacific dominated the blended cement market with a market share of 70.85% in 2024.

This growth is driven by rapid urbanization, large-scale infrastructure projects, and the growing preference for low-carbon building materials across both developed and emerging economies.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/blended-cement-market-113035

Regional Insights

The Asia Pacific region dominated the global blended cement market with a 70.85% share in 2024. Strong construction activity in countries like China, India, and Indonesia, coupled with supportive government policies promoting sustainable development, has boosted demand.

Europe and North America are also witnessing substantial growth due to stricter carbon emission norms and increasing adoption of green building certifications such as LEED and BREEAM. Meanwhile, the Middle East and Africa are expected to show steady growth, supported by rising investments in smart city projects and industrial expansion.

Segmentation Analysis

By Type

Portland Pozzolan Cement (PPC)

Portland Limestone Cement (PLC)

Portland Slag Cement (PSC)

Others

Among these, PPC held the largest market share in 2024 and is expected to retain dominance during the forecast period. Its wide availability, cost-effectiveness, and superior performance in infrastructure and housing projects make it a preferred choice.

PLC is anticipated to record the fastest growth due to its ability to significantly reduce clinker content and associated carbon emissions.

By Application

Residential

Non-Residential

The residential segment leads the market, driven by rapid urbanization, population growth, and increased demand for affordable housing. Blended cement offers enhanced durability and sustainability, making it ideal for residential construction.

The non-residential segment , including commercial, institutional, and industrial projects, is also growing rapidly due to rising infrastructure investments and the need for high-performance, low-carbon building materials.

Market Drivers

Sustainability and Emission Reduction

Blended cement significantly reduces CO₂ emissions by lowering clinker usage, aligning with global sustainability goals and green construction standards.

Government Regulations and Green Building Initiatives

Strict environmental regulations and increasing adoption of eco-friendly building certifications are encouraging the use of blended cement.

Utilization of Industrial By-Products

The use of fly ash, slag, and other industrial by-products not only enhances cement performance but also supports circular economy initiatives by minimizing waste.

Urbanization and Infrastructure Expansion

Rapid growth in infrastructure projects such as roads, bridges, and housing in emerging economies is fueling market demand.

Challenges

Inconsistent Raw Material Availability: Dependence on external industries for fly ash and slag can lead to supply fluctuations.

Standardization Issues: Some regions still rely on outdated standards favoring traditional Portland cement.

Higher Production Costs: Initial investments for adapting production processes and logistics can impact cost efficiency.

Competitive Landscape

Prominent players operating in the global blended cement market include:

- HOLCIM (Switzerland)

- UltraTech Cement Ltd. (India)

- Cemex S.A.B DE C.V. (Mexico)

- Heidelberg Materials (U.S.)

- TAIHEIYO CEMENT CORPORATION (Japan)

- JSW Cement (India)

- Dalmia Bharat Limited (India)

- Anhui Conch Cement Co., Ltd. (China)

- Martin Marietta Materials (U.S.)

- Votorantim Cimentos (Brazil)

These companies are focusing on expanding their blended cement portfolios, improving SCM integration, and investing in R&D to develop low-carbon and high-performance cement products.

Future Trends

The market is expected to reach USD 500.6 billion by 2032, supported by increasing infrastructure spending and environmental awareness.

Technological innovations in cement blending processes and SCM sourcing will further enhance product efficiency.

Growing popularity of Portland Limestone Cement (PLC) is expected to accelerate due to its superior carbon efficiency.

Governments and private sectors are likely to collaborate more closely to promote sustainable cement manufacturing practices.

Information Source: https://www.fortunebusinessinsights.com/blended-cement-market-113035

Key Takeaways

Market Size (2024): USD 371.2 billion

Market Size (2032): USD 500.6 billion

CAGR (2025–2032): 3.8%

Dominant Region: Asia Pacific (70.85% share in 2024)

Leading Type: Portland Pozzolan Cement (PPC)

The blended cement market is positioned for steady expansion over the next decade, driven by global sustainability goals, technological advancements, and increasing infrastructure demand. With governments and corporations prioritizing carbon reduction, the use of blended cement will continue to rise as a cornerstone of eco-friendly construction practices worldwide.

KEY INDUSTRY DEVELOPMENTS

- March 2025: Heidelberg Materials has announced that it will be commissioning an MVR vertical roller mill of the type MVR 5000 C-4 from Gebr Pfeiffer at its existing plant in Airvault, France. The mill will grind and produce ultra-fine Portland cement that will be used in blended cement and other products.

- February 2025: UltraTech commissioned an additional 0.6 Million Tons Per Annum (MTPA) capacity at its existing plant in West Bengal, India. The move is part of the company’s plan to meet the rising demand for cement.

Posted in: Business

| 0 comments

Sulfur is an essential industrial element primarily used in the production of sulfuric acid, a key component in fertilizers, chemicals, and numerous manufacturing processes. The demand for sulfur is closely tied to global agricultural activity, industrial expansion, and refinery output. The sulfur market continues to grow steadily as nations prioritize food security and chemical production efficiency.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/sulfur-market-102143

LIST OF KEY COMPANIES PROFILED

- Suncor Energy Inc. (Canada)

- H.J. Baker & Bro., LLC (U.S.)

- Abu Dhabi National Oil Company (UAE)

- Marathon Petroleum Corporation (U.S.)

- Gazprom (Russia)

- Aramco Trading (ATC) (Saudi Arabia)

- Shell (Netherlands)

- Georgia Gulf Corporation (U.S.)

- Kuwait Petroleum Corporation (Kuwait)

- Petrobras (Brazil)

Regional Insights

The Asia Pacific region dominated the global sulfur market in 2023 with a 34.11% share . This leadership position is primarily due to the region’s expanding agricultural industry, growing demand for fertilizers, and the presence of large refining and chemical processing capacities.

United States: The U.S. sulfur market is projected to reach USD 941.0 million by 2032 , driven by rising agricultural productivity, fertilizer demand, and advancements in sulfuric acid production.

China: China experienced a decline in sulfur imports in 2024, with import volumes dropping below 500,000 tons, the lowest May volume since 2004.

India: India’s sulfur market was impacted during the pandemic due to disruptions in trade and import logistics, though the country continues to represent a significant growth market driven by fertilizer demand.

Overall, Asia Pacific remains the largest and fastest-growing regional market, while North America and Europe maintain strong industrial demand supported by refinery production and chemical manufacturing.

Market Segmentation by Application

According to Fortune Business Insights, the sulfur market is segmented by application into fertilizers, chemicals, rubber, pharmaceuticals, and others .

Fertilizers: The fertilizer segment holds the largest market share, accounting for over 50% of global sulfur demand. Sulfur is used extensively in producing sulfuric acid, which is vital for manufacturing phosphate fertilizers that support agricultural productivity.

Chemicals: Sulfur serves as a raw material in chemical processing, including the production of detergents, dyes, and solvents.

Rubber and Pharmaceuticals: Sulfur is used in vulcanizing rubber and synthesizing various pharmaceutical compounds, further enhancing its industrial relevance.

The dominance of the fertilizer segment underscores sulfur’s critical role in the global food supply chain and agricultural sustainability.

Key Market Drivers

Rising Fertilizer Demand

Agriculture remains the largest consumer of sulfur. Growing food demand, population expansion, and the need for high-yield crop production have significantly increased the use of sulfur-based fertilizers.

Growth in Industrial Applications

Sulfur’s use in metal leaching, detergent manufacturing, and other industrial processes is driving demand from the chemical sector.

Refinery and Byproduct Recovery

The majority of global sulfur production comes as a byproduct of oil and gas refining. Continuous refinery operations and improvements in sulfur recovery technologies have ensured a steady supply to meet industrial needs.

Emerging Economies Driving Consumption

Developing countries such as India, China, and Brazil are witnessing increased sulfur consumption due to the expansion of fertilizer manufacturing and chemical production facilities.

Global Trade Adjustments

Import and export trends play a significant role in sulfur market dynamics. China and India’s changing import volumes indicate the influence of logistics, refinery output, and domestic production capacities on global trade flows.

Challenges

Despite positive growth trends, the sulfur market faces several challenges:

Supply Chain Vulnerabilities: Because sulfur is primarily produced as a refinery byproduct, disruptions in oil and gas refining can affect sulfur supply levels.

Import Dependence: Many agricultural economies rely heavily on sulfur imports, making them susceptible to international price fluctuations and logistics disruptions.

Market Concentration: Heavy dependence on the fertilizer segment makes the sulfur market sensitive to agricultural policy changes and global crop demand fluctuations.

Future Outlook (2024–2032)

The sulfur market outlook remains positive, with steady growth expected through 2032. Rising agricultural output, growing demand for phosphate fertilizers, and industrial expansion in emerging economies will be key growth drivers.

The market is projected to grow at a CAGR of 3.6% , reaching USD 7.99 billion by 2032 .

Asia Pacific is expected to retain its dominant share due to strong agricultural and industrial activity.

North America and Europe will maintain stable growth supported by refinery advancements and chemical sector investments.

The balance between rising demand and controlled supply will continue to influence sulfur prices and trade dynamics globally.

The global sulfur market is poised for consistent growth, fueled by its indispensable role in fertilizers, chemicals, and industrial manufacturing. Asia Pacific leads the market, supported by agricultural expansion and robust industrial demand. While supply chain dependencies and regulatory pressures remain challenges, ongoing technological improvements in sulfur recovery and the rising focus on sustainable fertilizer use present significant opportunities for market players.

With its essential function in global agriculture and chemical production, the sulfur market will remain a critical component of the industrial ecosystem through 2032.

Information Source: https://www.fortunebusinessinsights.com/sulfur-market-102143

KEY INDUSTRY DEVELOPMENTS

- August 2020 – In August 2020, Gazprom Export, a significant part of Gazprom, increased the volume of exports. The company supplied around 1.3 million tons to foreign consumers.

- September 2019 – Gazpromneft-Badra, a subsidiary of Gazprom Neft, began the shipping of granulated product from the Badra oilfield in Iraq.

Posted in: Business

| 0 comments

Polyethylene Furanoate (PEF) Market Sustainability Trends and Bio-Based Growth 2032

By ameliasss, 2025-10-16

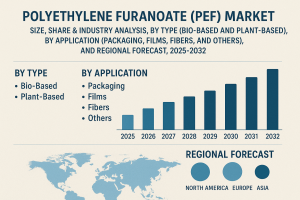

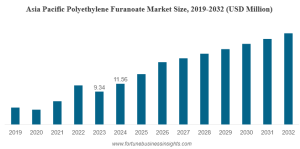

According to Fortune Business Insights, The global polyethylene furanoate (PEF) market was valued at USD 34.34 million in 2024 and is projected to grow from USD 42.28 million in 2025 to USD 73.78 million by 2032, exhibiting a CAGR of 8.3% during the forecast period. Asia Pacific held the dominant share of 33.66% in the global PEF market in 2024.

Polyethylene furanoate (PEF) is a bio-based, recyclable polyester derived from renewable sources such as plant sugars. Recognized for being sustainable, non-toxic, and environmentally friendly, PEF serves as an effective alternative to conventional petroleum-based polymers. Its excellent barrier performance, along with high mechanical strength, thermal stability, and puncture resistance, positions it as a promising substitute for traditional plastics like polyethylene terephthalate (PET) in various packaging and industrial applications.

The global Polyethylene Furanoate (PEF) market is witnessing substantial growth due to the rising demand for sustainable and bio-based packaging materials. PEF, a next-generation polyester derived from renewable resources such as fructose, offers excellent barrier properties against carbon dioxide, oxygen, and water vapor—making it a promising alternative to traditional PET (Polyethylene Terephthalate).

Market Overview

The PEF market is projected to experience robust expansion from 2025 to 2032, driven by the increasing global focus on reducing plastic waste and adopting eco-friendly materials. The material’s superior mechanical strength, lower carbon footprint, and enhanced recyclability make it suitable for applications in bottles, films, and fibers.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/polyethylene-furanoate-pef-market-112577

LIST OF KEY MARKET PLAYERS PROFILED IN THE REPORT

- Swicofil AG (Switzerland)

- Sulzer Ltd (Switzerland)

- TOYOBO CO., LTD. (Japan)

- Avantium (Netherlands)

- ALPLA (Austria)

- Origin Materials (U.S.)

- AVA Biochem AG (Switzerland)

- Danone (France)

- Stora Enso (Finland)

- Sukano (Switzerland)

Key Market Drivers

Rising Demand for Sustainable Packaging:

The shift toward bio-based materials in packaging industries is a major factor fueling PEF adoption. Beverage manufacturers are increasingly using PEF bottles due to their higher shelf life and biodegradability.

Environmental Regulations:

Stringent government policies against single-use plastics have accelerated the adoption of renewable polymers such as PEF.

Technological Advancements in Polymerization:

Continuous R&D efforts to improve production efficiency and cost competitiveness are helping manufacturers scale up PEF production.

Consumer Awareness:

Growing awareness regarding sustainable living and the environmental impact of plastics has boosted demand for bio-based packaging solutions.

Market Segmentation

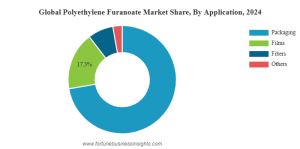

By Application:

Bottles

Films & Sheets

Fibers

Others

-

By End-Use Industry:

Food & Beverages

Personal Care & Cosmetics

Textiles

Pharmaceuticals

By Region:

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Regional Insights

Europe dominates the global Polyethylene Furanoate (PEF) market owing to strong environmental policies, circular economy initiatives, and the presence of key bio-based polymer manufacturers. Asia Pacific is expected to record the fastest growth, driven by high demand for sustainable packaging in countries such as China, Japan, and India. North America also shows steady growth due to advancements in biopolymer R&D and adoption in the beverage industry.

Competitive Landscape

The global PEF market is moderately consolidated, with key players focusing on product innovation and strategic collaborations. Leading companies are investing in large-scale commercial production and working closely with packaging giants to expand their customer base.

Information Source: https://www.fortunebusinessinsights.com/polyethylene-furanoate-pef-market-112577

Future Outlook

The Polyethylene Furanoate (PEF) market is poised for remarkable growth through 2032, supported by the global movement toward a circular economy. As large FMCG and beverage brands pledge to use 100% recyclable or biodegradable packaging, PEF is set to play a vital role in transforming the future of sustainable plastics.

KEY INDUSTRY DEVELOPMENTS

- February 2025 : Avantium N.V. has signed a joint development agreement with Amcor Rigid Packaging U.S., to explore the use of Avantium's PEF in rigid containers for several products, including beverage, food, medical, pharmaceutical, personal care, and home. Also, Amcor has committed to a multi-year capacity reservation for PEF from a future industrial-scale facility, based on a technology license from Avantium. This agreement guarantees Amcor preferred access to PEF volumes produced by Avantium's future licensee network.

- February 2025 : Avantium N.V. signed a collaboration with EPC Engineering & Technologies GmbH, to advance the continuous PEF polyester production technology, with the target of achieving 100 kilotonnes per annum and beyond capacities. This collaboration will combine the expertise of both companies to commercialize continuous polymerization of PEF (“PEF cPol Technology”).

Posted in: Business

| 0 comments

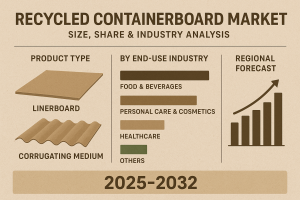

Recycled Containerboard Market Opportunities Driven by Recycling Initiatives 2032

By ameliasss, 2025-10-15

With growing environmental awareness, stringent government regulations, and a global shift toward sustainable packaging, the recycled containerboard market is becoming a vital part of the packaging industry. Recycled containerboard, made from recovered fibers, offers both ecological and commercial benefits. It helps reduce landfill waste, limits deforestation, and supports circular economy initiatives. Industries such as e-commerce, food & beverages, healthcare, and personal care are increasingly adopting recycled containerboard for their packaging needs.

What Is Recycled Containerboard?

Containerboard refers to paperboard used primarily in the production of corrugated boxes and packaging materials. Recycled containerboard is manufactured using fibers recovered from post-consumer or post-industrial sources such as old corrugated containers (OCC), mixed paper, or recycled wood pulp. It is available in several product types, including linerboard and corrugating medium. The performance of recycled containerboard—such as strength, durability, and print quality—depends on the quality of the recycled feedstock and processing methods.

Other industry analyses estimate steady growth in demand, driven by increasing use of eco-friendly packaging and advancements in recycling technology. The broader containerboard market, which includes virgin fiber variants, is also expected to expand moderately in line with global packaging demand.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/recycled-containerboard-market-113852

Key Market Players

Leading companies in the global recycled containerboard market include:

- International Paper (U.S.)

- Georgia-Pacific LLC (U.S.)

- DS Smith (U.K.)

- Greif (U.S.)

- Mondi (U.K.)

- Stora Enso (Finland)

- Cascades Inc. (Canada)

- Kruger (Canada)

- Sappi Ltd. (South Africa)

- Smurfit Kappa (Ireland)

- Daio Paper Corporation (Japan)

- Nine Dragons Paper (China)

These players are focusing on expanding production capacities, investing in recycling innovations, and forming strategic partnerships to strengthen their market presence.

Key Growth Drivers

Sustainability and Regulatory Pressure

Governments across the world are enforcing laws to reduce single-use plastics and encourage recycling. These regulations are accelerating the shift toward recyclable and eco-friendly materials such as recycled containerboard.

Changing Consumer Preferences

Modern consumers favor brands that demonstrate environmental responsibility. Packaging made with recycled materials is increasingly seen as a mark of sustainability, boosting brand reputation and customer loyalty.

Rising E-commerce Demand

The rapid growth of e-commerce has significantly increased demand for corrugated packaging, which primarily uses containerboard. The need for strong, lightweight, and recyclable packaging materials further drives market growth.

Cost and Resource Efficiency

Using recycled fibers reduces dependence on virgin pulp, which can be more expensive and environmentally intensive. Advancements in recycling technologies have made recycled containerboard production more efficient and cost-effective.

Regional Dynamics

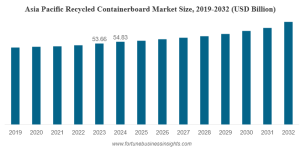

Asia-Pacific dominates the market due to its large production base, strong industrial growth, and rising consumer packaging demand.

Europe is a leader in circular economy initiatives, with stringent recycling targets supporting market expansion.

North America has a mature recycling infrastructure and strong demand from food, retail, and e-commerce sectors.

Major Challenges

Raw Material Quality and Availability

The quality of recovered paper varies significantly. Contaminated or low-grade recycled fiber can reduce the strength and appearance of containerboard, impacting end-use applications.

High Production Costs

Although recycled fibers lower raw material costs, cleaning, de-inking, and energy use during processing can increase overall production costs.

Performance Limitations

After multiple recycling cycles, fiber strength diminishes. Recycled containerboard may face challenges in applications requiring high durability or moisture resistance.

Supply Chain and Infrastructure Gaps

Inadequate collection and sorting infrastructure in some regions leads to inconsistent supply of high-quality recycled materials, increasing transportation and operational costs.

Emerging Market Trends

Innovation in Coatings and Barriers

New recyclable coatings are being developed to enhance moisture and grease resistance, allowing recycled containerboard to expand into food and liquid packaging applications.

Lightweighting of Packaging

Manufacturers are adopting lightweight designs to reduce packaging weight without compromising strength. This helps lower transportation costs and carbon emissions.

Circular Supply Chain Integration

Collaboration among brands, recyclers, and converters is improving waste collection and closed-loop recycling systems, enhancing material recovery efficiency.

Transparency and Certification

Companies are increasingly seeking certifications to verify recycled content and sustainability claims, driven by consumer demand for transparency and compliance with environmental standards.

Information Source: https://www.fortunebusinessinsights.com/recycled-containerboard-market-113852

Future Outlook

The recycled containerboard market is set to witness stable and consistent growth over the next decade. Key factors influencing future expansion include:

Continued investments in recycling infrastructure and advanced fiber recovery technologies

Stricter global regulations promoting eco-friendly packaging

Increased demand for corrugated packaging from e-commerce and logistics sectors

Rising awareness among consumers and brands toward sustainability

As businesses transition to circular economy models, recycled containerboard will play a central role in balancing environmental responsibility with packaging performance and cost efficiency.

The recycled containerboard market is rapidly evolving as industries embrace sustainable packaging solutions. Despite challenges such as fiber quality and cost pressures, the market outlook remains positive. Continuous innovation, growing regulatory support, and consumer demand for eco-friendly packaging are expected to drive strong and steady growth in the years ahead.

Posted in: Business

| 0 comments

Polyurethane Protective Gloves Market Industry Forecast and Regional Breakdown 2032

By ameliasss, 2025-10-15

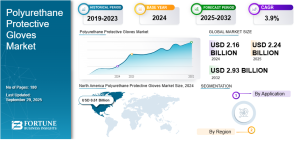

According to Fortune Business Insights, The global polyurethane protective gloves market size was valued at USD 2.16 billion in 2024. The market is projected to grow from USD 2.24 billion in 2025 to USD 2.93 billion by 2032, exhibiting a CAGR of 3.9% during the forecast period. North America dominated the polyurethane protective gloves market with a market share of 23.61% in 2024.

Polyurethane protective gloves are specialized hand-protection gear coated with a thin layer of polyurethane (PU) on a fabric liner. These gloves combine flexibility, grip, and comfort, making them ideal for tasks that require precision and dexterity. Unlike heavier gloves, PU gloves are lightweight, breathable, and provide a “second-skin” feel, suitable for industries such as manufacturing, automotive, electronics, and food processing.

Key Market Players

Prominent companies operating in the polyurethane protective gloves market include:

- ANSELL LTD. (Australia)

- PIP Global (U.S.)

- Radians, Inc. (U.S.)

- Global Glove and Safety Manufacturing, Inc. (U.S.)

- Engelbert Strauss Inc. (Germany)

- HANVO Safety (China)

- NANTONG JIADELI SAFETY PRODUCTS CO., LTD. (China)

- Tilsatec (U.K.)

- Kimberly-Clark Worldwide, Inc. (U.S.)

- HexArmor (U.S.)

These companies focus on product innovation, material enhancement, and regional expansion to maintain competitiveness.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/polyurethane-protective-gloves-market-113851

Key Drivers of Growth

Stringent Safety Regulations

Rising awareness of worker safety and stricter industrial regulations are major factors driving the demand for high-quality protective gloves. PU gloves meet essential safety standards for abrasion resistance, mechanical protection, and durability.

Demand for Dexterity & Precision

Sectors like electronics assembly, inspection, and fine mechanical work require gloves that provide excellent tactile sensitivity. PU coatings are thin and flexible, offering enhanced finger movement and control.

Comfort & Ergonomics

PU gloves are lightweight and breathable, reducing hand fatigue during long hours of use. Their ergonomic design ensures comfort and better performance in repetitive or delicate tasks.

Expansion of End-Use Industries

The growing industrial sectors—automotive, construction, food processing, and healthcare—are fueling the adoption of polyurethane gloves. In electronics manufacturing, in particular, these gloves are preferred for precise handling.

Product Innovation

Manufacturers are developing advanced PU gloves with cut resistance, touchscreen compatibility, and improved grip in oily or wet conditions. These innovations enhance usability and expand application scope.

Challenges & Restraints

Price Sensitivity: PU gloves are typically more expensive than vinyl or latex gloves, which can deter adoption in cost-conscious markets.

Chemical & Heat Resistance: PU coatings have limited resistance to extreme heat and certain chemicals, reducing their use in specific heavy-duty applications.

Durability Issues: In highly abrasive or solvent-heavy environments, PU gloves may wear out faster, leading to higher replacement rates.

Competition from Substitutes: Materials like nitrile and neoprene provide strong competition, especially where higher chemical resistance is needed.

Market Segmentation

| Segment | Description |

|---|---|

| By End-Use Industry | Automotive, Construction, Healthcare, Food & Beverage, Electronics, Logistics, and Others |

| By Product Type | Disposable, Reusable, Cut-Resistant, Work Gloves, and Light Assembly Gloves |

| By Coating Type | Palm Coated, Fingertip Coated, Smooth Finish, and Textured Finish |

| By Thickness / Gauge | Thin (<5 mils), Medium (5–8 mils), Heavy (>8 mils) |

| By Region | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

Regional Insights

-

North America held a significant share in 2024 due to strong occupational safety standards and established industrial sectors.

-

Asia-Pacific is expected to witness the fastest growth, driven by rapid industrialization, expanding electronics and automotive industries, and increased focus on workplace safety.

-

Europe continues to grow steadily, supported by strict safety compliance standards and widespread adoption of advanced PPE technologies.

Emerging Trends

-

Touchscreen-Compatible Gloves: The integration of touchscreen technology into industrial gloves enables workers to operate smart devices without removing protection.

-

Eco-Friendly Manufacturing: Companies are investing in sustainable materials and low-VOC polyurethane coatings to minimize environmental impact.

-

Improved Ergonomic Designs: New glove designs focus on lightweight construction, ventilation, and flexibility for maximum comfort.

-

Specialized Applications: Demand is rising for gloves tailored to high-risk applications, including extreme cut or impact resistance.

Information Source: https://www.fortunebusinessinsights.com/polyurethane-protective-gloves-market-113851

Market Outlook & Opportunities

The polyurethane protective gloves market is poised for consistent growth over the next decade. The greatest opportunities lie in medium-risk work environments that require dexterity and comfort rather than bulk protection. Emerging economies are also increasing their adoption of industrial safety equipment as regulatory frameworks strengthen. Additionally, sectors like healthcare, logistics, and electronics are creating new demand for lightweight and precision-oriented gloves.

The polyurethane protective gloves market is witnessing steady expansion driven by rising industrial safety awareness, ergonomic advancements, and growing industrialization across developing economies. While cost and material limitations remain challenges, innovations in design and sustainability are creating strong opportunities for future growth. PU gloves are expected to remain a preferred choice for industries requiring a balance between protection, precision, and comfort.

KEY INDUSTRY DEVELOPMENTS:

- April 2025: Radians, Inc., a personal protective equipment manufacturer, launched 14 new disposable gloves to meet the growing need for single-use gloves. These gloves help to safeguard people and products from contamination, chemicals, and injuries.

- November 2024: PIP Global announced that they have acquired Honeywell’s Personal Protective Equipment Business, including leading brands Fendall, Fibre-Metal, Howard Leight, KCL, Miller, Morning Pride, North, Oliver, Salisbury, UVEX, and others. This expansion will help the company expand its portfolio and enhance its geographic reach.

Posted in: Business

| 0 comments

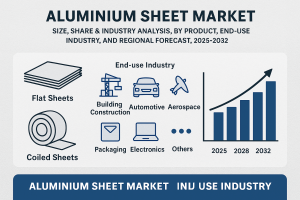

Aluminium Sheet Market Size, Share, and Comprehensive Forecast Analysis 2032

By ameliasss, 2025-10-14

According to Fortune Business Insights, The global aluminium sheet market was valued at USD 62.16 million in 2024 and is projected to increase from USD 66.24 million in 2025 to USD 103.62 million by 2032, reflecting a CAGR of 6.6% during the forecast period. Asia Pacific emerged as the leading region, accounting for 65.95% of the market share in 2024.

An aluminium sheet is a flat-rolled product made from aluminium alloys, known for its lightweight nature, corrosion resistance, and excellent malleability. These sheets are extensively used across industries such as construction, automotive, aerospace, packaging, and electronics, offering a balance between strength and reduced weight.

Market growth is primarily driven by the increasing demand for lightweight materials in infrastructure development and automotive manufacturing. Moreover, rising investments in renewable energy, the expanding electric vehicle (EV) sector, and the global shift toward sustainable and recyclable packaging solutions are fueling market expansion.

Key players in the global aluminium sheet market include Aalco Metals Limited, Henan Chalco, JW Aluminum, Constellium, and Hindalco Industries Ltd.

The aluminium sheet market is experiencing robust growth driven by rising demand across construction, automotive, packaging, and aerospace industries. Known for its lightweight nature, corrosion resistance, and high strength, aluminium sheet products are increasingly replacing traditional steel components to enhance fuel efficiency and performance.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/aluminium-sheet-market-113950

LIST OF KEY ALUMINIUM SHEET COMPANIES

- Aalco Metals Limited (U.K.)

- Henan Chalco (China)

- RusAL (Russia)

- JW Aluminum (U.S.)

- Metalco Extrusions Global LLP (India)

- UACJ Corporation (Japan)

- Constellium (France)

- Aleris International, Inc. (U.S.)

- Hindalco Industries Ltd. (India)

- AMAG Austria Metall AG (Austria)

Market Overview

The global aluminium sheet market is witnessing steady expansion as industries move toward sustainable and energy-efficient materials. Aluminium sheets are flat-rolled products with thicknesses ranging from 0.2 mm to 6 mm and are widely used in the production of vehicle panels, building facades, beverage cans, and industrial equipment. Rapid urbanization, infrastructural investments, and the global shift toward electric mobility are key contributors to the market’s growth.

Key Market Drivers

Rising Automotive Production:

Automakers are adopting aluminium sheets to reduce vehicle weight, improve fuel efficiency, and meet emission standards. The increasing production of electric vehicles (EVs) further boosts demand for lightweight aluminium components.

Expanding Construction Sector:

The construction industry relies heavily on aluminium sheets for roofing, cladding, and insulation applications due to their durability and design flexibility.

Growing Packaging Industry:

Aluminium sheets are widely used in the production of beverage cans, food packaging, and pharmaceutical containers owing to their recyclability and barrier properties.

Sustainability Initiatives:

Governments and manufacturers are emphasizing recyclable materials, and aluminium’s 100% recyclability without loss of quality aligns perfectly with sustainability goals.

Market Segmentation

By Alloy Type: 1xxx, 3xxx, 5xxx, and 6xxx series aluminium sheets

By Application: Automotive, Building & Construction, Packaging, Aerospace, and Others

By Region: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa

Regional Insights

Asia-Pacific dominates the global aluminium sheet market due to rapid industrialization and infrastructure growth in China and India.

Europe focuses on lightweight automotive manufacturing and renewable energy projects.

North America experiences growth through advancements in aerospace and electric vehicle production.

Information Source: https://www.fortunebusinessinsights.com/aluminium-sheet-market-113950

Competitive Landscape

Leading players in the aluminium sheet market include Novelis Inc., Norsk Hydro ASA, Constellium SE, Alcoa Corporation, and Hindalco Industries . These companies are investing in recycling facilities, capacity expansions, and technological innovations to improve production efficiency and sustainability.

Future Outlook

The aluminium sheet market is projected to grow steadily through 2032, fueled by the global transition to sustainable materials, growth in e-mobility, and increased use in packaging and renewable energy sectors. Technological advancements in alloy development and sheet forming processes are expected to create new opportunities for market players.

Posted in: Business

| 0 comments