According to Fortune Business Insights, The global iron ore pellets market was valued at USD 60.82 billion in 2024 and is expected to grow from USD 61.64 billion in 2025 to USD 94.51 billion by 2032, registering a CAGR of 6.3% during the forecast period. Asia Pacific held the largest share of the market in 2024, accounting for 30.61% of the global revenue.

The global Iron Ore Pellets Market is witnessing steady growth, driven by increasing steel production, rising demand for high-grade raw materials, and the growing shift toward environmentally sustainable steelmaking processes. Iron ore pellets — small, spherical balls made from iron ore fines — play a vital role in blast furnaces and direct reduction processes, offering superior performance and reduced emissions compared to sinter and lump ores.

According to industry analysis, the Iron Ore Pellets Market size is projected to grow significantly from 2025 to 2032, supported by robust expansion in the steel and construction industries worldwide.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/iron-ore-pellets-market-113953

Market Overview

Iron ore pellets are formed through agglomeration and thermal treatment of iron ore fines. These pellets are rich in iron (typically over 65%) and are used as feedstock in steel production. The market has gained momentum as steelmakers aim to improve efficiency, reduce energy consumption, and comply with environmental regulations.

The surge in infrastructure projects, urbanization, and automotive manufacturing across developing economies — particularly in Asia Pacific — has fueled the consumption of steel, thereby driving the demand for iron ore pellets.

Key Market Drivers

1. Growing Steel Demand

The global steel industry remains the largest consumer of iron ore pellets. Countries like China, India, and Japan are expanding their steel production capacity to meet construction and industrial needs, thereby boosting pellet consumption.

2. Environmental Sustainability

Iron ore pellets produce fewer CO₂ emissions during steelmaking compared to traditional raw materials. This has positioned pellets as a preferred feedstock amid tightening global emission norms.

3. Technological Advancements

Innovations in pelletizing technology and the adoption of direct reduction (DR) processes have increased pellet efficiency and quality. These advancements are supporting market growth, especially in regions with limited access to high-grade iron ore.

Market Segmentation

By Grade

Blast Furnace (BF) Pellets

Direct Reduction (DR) Pellets

By Application

Steel Production

Construction

Automotive

Others

By Region

Asia Pacific: The largest market, led by China and India.

Europe: Driven by green steel initiatives.

North America: Focused on high-grade DR pellets for electric arc furnaces.

Latin America: Emerging as a key supplier, especially Brazil.

Middle East & Africa: Witnessing growth due to industrial expansion and new steel plants.

Regional Insights

Asia Pacific dominates the global iron ore pellets market, accounting for the largest revenue share. China’s steel industry and India’s infrastructure expansion are primary growth catalysts. Meanwhile, Europe is transitioning toward carbon-neutral steelmaking, favoring the use of DR-grade pellets. Brazil, one of the world’s leading iron ore producers, remains a crucial exporter of high-quality pellets.

LIST OF KEY IRON ORE PELLETS COMPANIES PROFILED

- Samarco (Brazil)

- Vale S.A. (Brazil)

- Ferrexpo PLC (Switzerland)

- Bahrain Steel (GIIC) (Bahrain)

- Jindal Steel & Power Ltd. (JSPL) (India)

- KIOCL Ltd. (India)

- ArcelorMittal (Luxembourg)

- Ansteel Group (China)

- China Baowu Steel Group (China)

- Severstal (Russia)

Recent Industry Developments

Vale S.A. announced expansion of its pelletizing capacity in Brazil to cater to the increasing global demand.

ArcelorMittal initiated R&D projects focusing on green hydrogen-based direct reduction pellets.

LKAB (Sweden) is developing carbon-free pellet production using renewable energy and hydrogen.

Future Outlook

The Iron Ore Pellets Market is expected to experience significant growth through 2032, supported by the ongoing transition toward green steel production. As countries invest in decarbonizing the steel sector, the demand for high-quality, low-emission pellets will accelerate. The integration of digital monitoring and automation in pelletizing plants will further enhance production efficiency.

Information Source: https://www.fortunebusinessinsights.com/iron-ore-pellets-market-113953

Key Takeaways

Rising steel demand and stricter environmental norms are driving market expansion.

Asia Pacific remains the dominant region, led by China and India.

Green steel initiatives are creating new growth opportunities for DR-grade pellets.

Technological advancements in pelletizing and direct reduction processes are transforming the industry landscape.

The Iron Ore Pellets Market is set to play a central role in the sustainable evolution of the steel industry. With major players focusing on innovation and decarbonization, the market outlook for 2025–2032 appears promising. Increasing global infrastructure development and clean energy initiatives are expected to keep the demand trajectory strong in the coming years.

Posted in: Business

| 0 comments

Bioplastics Packaging Market New Product Developments and Growth Strategies 2025-2032

By ameliasss, 2025-10-13

The Bioplastics Packaging Market is witnessing rapid expansion driven by the global shift toward sustainable materials, rising environmental concerns, and growing consumer preference for eco-friendly packaging. Bioplastics, derived from renewable biomass sources such as corn starch, sugarcane, or cellulose, offer a sustainable alternative to conventional petroleum-based plastics.

Market Overview

The global bioplastics packaging market is poised for significant growth due to increasing government regulations on single-use plastics, rising demand from the food & beverage sector, and ongoing advancements in biodegradable materials. Leading manufacturers are investing in research and development to enhance the performance, durability, and cost-efficiency of bioplastic materials.

According to industry estimates, the market is expected to grow at a strong CAGR from 2025 to 2032, driven by the adoption of sustainable packaging solutions across multiple industries, including food & beverages, personal care, pharmaceuticals, and consumer goods.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/bioplastic-packaging-market-108066

List of Top Bioplastics Packaging Companies:

- Corbion N.V. (Netherlands)

- Coveris (U.K.)

- Bio Futura (Netherlands)

- Safepack Packaging Solutions (India)

- Amcor Plc. (Australia)

- PLAMFG (U.S.)

- Plantic Technologies (Australia)

- Futamura Group (Japan)

- NatureWorks LLC (U.S.)

- Polymateria Ltd. (U.K.)

Key Market Drivers

Rising Environmental Awareness:

Growing awareness about plastic pollution and carbon footprint reduction has significantly boosted demand for bioplastic packaging solutions.

Government Initiatives & Regulations:

Stringent policies banning single-use plastics and encouraging compostable packaging materials have accelerated bioplastics adoption.

Innovation in Materials & Processing:

Continuous innovation in PLA (Polylactic Acid), PHA (Polyhydroxyalkanoates), and starch blends is improving the quality and affordability of bioplastic packaging.

Expanding Food & Beverage Sector:

The surge in demand for sustainable food packaging solutions, especially in ready-to-eat meals and beverages, is fueling market growth.

Market Segmentation

By Material Type:

Polylactic Acid (PLA)

Polyhydroxyalkanoates (PHA)

Starch Blends

Bio-PET

Bio-PE

Others

By Application:

Food & Beverage Packaging

Personal Care & Cosmetics

Pharmaceuticals

Household Products

Others

By Region:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Europe currently dominates the market, supported by strong sustainability mandates and consumer demand for green packaging. However, the Asia-Pacific region is expected to exhibit the fastest growth rate due to rising industrialization and increased awareness about sustainable materials in countries like China, Japan, and India .

Competitive Landscape

Key players in the bioplastics packaging market are focusing on strategic partnerships, mergers, and innovation to expand their product portfolios. Companies such as NatureWorks LLC, BASF SE, Novamont S.p.A., Braskem S.A., and Total Corbion PLA are investing heavily in bio-based technologies and expanding global production capacities.

Information Source: https://www.fortunebusinessinsights.com/bioplastic-packaging-market-108066

Future Outlook

The bioplastics packaging market is expected to continue its upward trajectory through 2032, supported by circular economy goals, brand sustainability commitments, and ongoing R&D investments. Technological advancements that enhance material performance and biodegradability will further strengthen the industry’s market position.

The transition toward a greener and more sustainable packaging ecosystem is no longer optional—it’s inevitable. The Bioplastics Packaging Market will play a vital role in shaping the future of the packaging industry by offering innovative, renewable, and environmentally responsible solutions.

KEY INDUSTRY DEVELOPMENTS:

- January 2024 – A leader in the sustainable packaging industry, Print & Pack, launched a new era of eco-friendly packaging solutions tailored for small businesses and eco-conscious brands across North America.

- December 2023 – Melodea launched MelOx NGen, a high-performance barrier product designed to enhance the recyclability of plastic food packaging and other applications. This water-based and plant-sourced coating is designed to be applied to various types of packaging materials such as films, pouches, bags, lids, and blister packs.

Posted in: Business

| 0 comments

Lanthanum Market Key Insights and Emerging Trends USD 75.0 Million in 2025 to USD 114.3 Million by 2032

By ameliasss, 2025-10-13

The Lanthanum market is experiencing steady growth, driven by rising demand from various industrial applications such as electronics, renewable energy, automotive, and metallurgy. Lanthanum, a soft, malleable rare earth metal, plays a crucial role in manufacturing products like batteries, optical lenses, catalysts, and hybrid vehicle components. With the shift towards cleaner technologies and advanced electronics, the global lanthanum market is poised for significant expansion.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/lanthanum-market-113903

LIST OF KEY LANTHANUM COMPANIES

- American Elements (U.S.)

- Lynas Rare Earths Ltd. (Australia)

- Rainbow Rare Earths Limited (U.K.)

- Thermo Fisher Scientific Inc. (U.S.)

- Rare Element Resources Ltd. (U.S.)

- HEFA Rare Earth Canada Co., Ltd. (China)

- IREL Limited (India)

- Stanford Advanced Materials (U.S.)

- Avalon Advanced Materials Inc. (Canada)

- Blue Line Corporation (U.S.)

Key Drivers of the Lanthanum Market

1. Growing Demand in Electronics

Lanthanum is widely used in the production of high-refractive-index glass and camera lenses. Its oxide form, lanthanum oxide (La₂O₃), enhances the optical performance of glass and ceramics. The growing electronics industry, particularly in Asia-Pacific, is fueling demand for lanthanum-based materials.

2. Expansion of the EV and Hybrid Vehicle Market

Lanthanum is a key component in nickel-metal hydride (NiMH) batteries , commonly used in hybrid vehicles. As the automotive industry transitions toward electric and hybrid vehicles, the demand for lanthanum is expected to surge, especially from major EV manufacturers in China, the U.S., and Europe.

3. Catalyst Applications in the Petrochemical Industry

Lanthanum-based catalysts are essential in petroleum refining, particularly for fluid catalytic cracking (FCC). These catalysts improve fuel efficiency and reduce harmful emissions, aligning with environmental regulations worldwide.

4. Clean Energy Transition

The global emphasis on renewable energy and sustainable technologies has pushed for increased adoption of lanthanum in wind turbines, solar panels, and energy storage systems. Lanthanum’s role in enhancing magnet strength and thermal stability makes it valuable for green energy technologies.

Market Segmentation

By Product Type:

Lanthanum Oxide

Lanthanum Carbonate

Lanthanum Metal

Others

By Application:

Electronics

Automotive

Petrochemicals

Optics

Energy Storage

Pharmaceuticals

By Region:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Among these, Asia-Pacific dominates the global lanthanum market, led by China — the largest producer and exporter of rare earth elements.

Challenges in the Lanthanum Market

Geopolitical Risks: China controls over 80% of the world’s rare earth production, creating supply chain vulnerabilities and price volatility.

Environmental Concerns: Mining and refining of lanthanum can lead to ecological damage if not managed responsibly.

Recycling Limitations: Currently, recycling rare earth elements, including lanthanum, remains inefficient and expensive.

The global Lanthanum market is expected to grow at a CAGR of 6.2% from 2025 to 2032 , supported by government initiatives to promote clean energy and electrification. Investment in rare earth exploration outside China is also gaining momentum, with countries like the U.S., Australia, and Canada ramping up production capabilities.

Information Source: https://www.fortunebusinessinsights.com/lanthanum-market-113903

Lanthanum is a strategic metal with rising importance across multiple industries. As the world moves toward sustainable technologies, the Lanthanum market is set for continued growth. However, ensuring supply chain resilience, environmental responsibility, and technological innovation will be key to unlocking its full potential.

REPORT COVERAGE

The lanthanum market report offers a comprehensive analysis of market size and forecasts across all included segments. It provides an in-depth overview of market dynamics, key trends, and growth drivers influencing the industry during the forecast period. The study highlights regional and country-level insights, along with updates on major industry developments, product innovations, strategic partnerships, and mergers & acquisitions. Additionally, the report presents a detailed competitive landscape, featuring the market share and profiles of leading players operating in the global lanthanum market.

Posted in: Business

| 0 comments

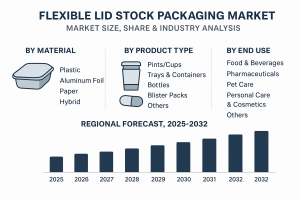

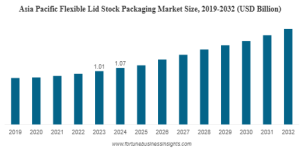

According to Fortune Business Insights, The global Flexible Lid Stock Packaging Market is witnessing strong growth, driven by increasing demand for convenient, lightweight, and sustainable packaging solutions across the food, beverage, and healthcare sectors. According to Fortune Business Insights, the market was valued at USD 2.59 billion in 2024 and is projected to grow from USD 2.74 billion in 2025 to USD 4.09 billion by 2032, exhibiting a CAGR of 6.05% during the forecast period (2025–2032).

Flexible lid stock packaging plays a crucial role in preserving product freshness, extending shelf life, and ensuring tamper-evident sealing — all of which are essential in modern packaging applications.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/flexible-lid-stock-packaging-market-109395

Key Market Drivers

1. Rising Demand in Food & Beverage Sector

The growing consumption of packaged and ready-to-eat foods is one of the primary factors driving market growth. Flexible lid stock packaging provides excellent sealing and barrier properties against oxygen and moisture, making it ideal for packaging dairy products, beverages, and frozen foods.

2. Increasing Adoption of Sustainable Packaging

Manufacturers are focusing on recyclable and eco-friendly materials to align with global sustainability goals. The transition toward mono-material lid stocks and recyclable laminates is enhancing the market’s growth potential.

3. Expansion in Pharmaceutical and Healthcare Applications

Flexible lid stock packaging is gaining popularity in the pharmaceutical industry due to its superior sealing performance, light protection, and contamination resistance — particularly in blister packs and sterile medical packaging.

4. Technological Advancements in Packaging Materials

Innovations in film technologies, barrier coatings, and printing techniques are improving the performance and aesthetics of flexible lid stock packaging, helping brands stand out in competitive retail environments.

Market Segmentation

By Material Type

Plastic (PE, PET, PP, etc.) – Dominates the market due to cost-effectiveness, durability, and versatility.

Aluminum Foil – Preferred for high-barrier applications in food and pharma packaging.

Paper and Others – Growing steadily with the rise of sustainable and recyclable options.

By Application

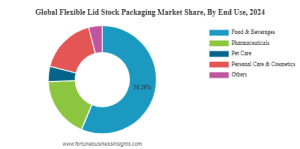

Food & Beverage – Largest segment, driven by the packaging needs of dairy products, ready meals, and snacks.

Pharmaceuticals – Increasing adoption in blister packs and medical trays.

Personal Care & Others – Expanding use in cosmetic containers and hygiene product packaging.

By Region

Asia Pacific dominated the global market with a 41.02% share in 2024 , attributed to high consumption of packaged foods, growing retail infrastructure, and rising disposable incomes in countries like China and India.

North America and Europe continue to see steady growth, supported by innovation and stringent environmental regulations encouraging recyclable packaging solutions.

Latin America and the Middle East & Africa are emerging as high-potential markets due to expanding food processing and pharmaceutical industries.

List of Key Flexible Lid Stock Packaging Companies Profiled

- Tekni-Plex, Inc. (U.S.)

- Huhtamaki (Finland)

- Constantia Flexible (Austria)

- Sealed Air (U.S.)

- Mas Flexible (Turkey)

- Berry Global (U.S.)

- Amcor plc (Switzerland)

- Elite Packaging (U.S.)

- Safepack (India)

- DuPont (U.S.)

- Wipak (Canada)

- KM Packaging Services Ltd. (U.K.)

These companies are focusing on product innovation, sustainability-driven packaging solutions, and regional expansion to strengthen their global presence.

Recent Industry Developments

Leading packaging manufacturers are investing in recyclable and bio-based lid stock materials to meet growing consumer demand for eco-friendly packaging.

Collaborations and acquisitions are increasing across the sector to enhance technological capabilities and expand product portfolios.

Automation and digital printing technologies are being integrated to improve production efficiency and customization in packaging.

Information Source: https://www.fortunebusinessinsights.com/flexible-lid-stock-packaging-market-109395

The Flexible Lid Stock Packaging Market is expected to continue its robust growth through 2032, driven by sustainability trends, material innovations, and expansion of packaged food and pharmaceutical industries. The push for recyclable and lightweight packaging will create new opportunities for manufacturers, while the Asia Pacific region remains the most promising market for future investments.

KEY INDUSTRY DEVELOPMENTS

- In July 2025, Greiner Packaging launched Click On and Click In sealing lids, which are mono-material packaging solutions aimed at improving sustainability and convenience by removing the necessity for aluminum foil while guaranteeing resealability and recyclability for a range of products. Sealing lids operate on a two-component principle: a cup and a lid. This enables the intentional exclusion of a third component such as aluminum foil. The benefit is that both elements can be constructed from the same material, such as PP, PET, or r-PET.

Posted in: Business

| 0 comments

The global bio-naphtha market is witnessing significant growth, driven by increasing demand for sustainable and renewable alternatives to fossil fuels. Bio-naphtha, derived from biological feedstocks such as vegetable oils, agricultural waste, and used cooking oil, serves as an eco-friendly substitute for conventional naphtha in various industries including petrochemicals, transportation, and energy.

Market Overview

The transition toward a circular and low-carbon economy is propelling the demand for bio-naphtha worldwide. This renewable chemical feedstock is primarily used in the production of olefins, plastics, and gasoline blending. Growing awareness about greenhouse gas (GHG) reduction and supportive government regulations encouraging the use of bio-based products further boost the market growth.

According to industry analysis, the bio-naphtha market is expected to grow at a healthy CAGR during 2024–2032 , driven by robust demand from the petrochemical and energy sectors.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/bio-based-naphtha-market-112751

Key Market Drivers

Rising Environmental Concerns: Increasing emphasis on reducing carbon emissions and dependence on fossil fuels is accelerating the adoption of bio-naphtha.

Government Policies and Incentives: Policies promoting bio-based energy sources and renewable feedstocks across Europe and North America are creating new growth avenues.

Growing Demand from Petrochemical Industry: Bio-naphtha is a crucial raw material for producing ethylene and propylene, essential for manufacturing plastics, detergents, and solvents.

Technological Advancements: Innovations in bio-refining and conversion technologies are improving yield efficiency, lowering costs, and enhancing product quality.

Market Segmentation

By Feedstock:

Vegetable Oils

Used Cooking Oils

Animal Fats

Agricultural Residues

Others

By Application:

Fuel Blending

Steam Cracking

Chemical Production

Others

By End-Use Industry:

Petrochemical

Energy & Power

Automotive

Others

By Region:

Europe – Dominates the market owing to strong biofuel mandates and sustainability initiatives.

North America – Rapid expansion of renewable energy infrastructure supports growth.

Asia Pacific – Emerging economies like Japan and South Korea are investing in bio-based alternatives to meet carbon neutrality goals.

Latin America & Middle East – Growing renewable resource availability and refinery investments bolster regional opportunities.

List of Top Bio-naphtha Companies Profiled

- UPM Biofuels (Finland)

- Montana Renewables LLC (U.S.)

- TOPSOE (Denmark)

- Chevron (U.S.)

- Mitsui Chemicals (Japan)

- Eni S.p.A. (Italy)

- TotalEnergies (France)

- Neste Oil Corporation (Finland)

- OMV Group (Austria)

These companies are investing heavily in advanced biorefineries and sustainable sourcing to meet the rising global demand.

Information Source: https://www.fortunebusinessinsights.com/bio-based-naphtha-market-112751

The bio-naphtha market is expected to expand significantly as industries and governments intensify efforts toward achieving carbon neutrality. Increasing use in bio-based plastics, biofuels, and chemical feedstocks will further strengthen market growth. Continuous research and innovation will be key in overcoming production cost challenges and achieving large-scale commercialization.

- December 2024: BASF and INOCAS partnered to develop a sustainable supply of Macaúba oil in Brazil, with a focus on its use in bio-naphtha production. This initiative will involve scaling up INOCAS's Macaúba cultivation program and providing BASF with both kernel and pulp oils. The pulp oil will be used to produce bio-naphtha, which can be transformed into various products, including polymers, solvents, detergents, and fuels. Commercial volumes of the kernel oil are expected by 2025, with a regular supply of pulp oil for bio-naphtha production starting in 2027.

- July 2024: Mitsubishi Corporation and Neste partnered to increase the availability of bio-naphtha in Japan, encouraging its adoption by Japanese downstream companies. This collaboration aims to facilitate the transition from conventional petroleum naphtha to bio-naphtha in the production of various petrochemical products such as plastics and chemicals.

Posted in: Business

| 0 comments

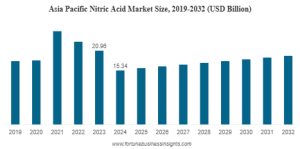

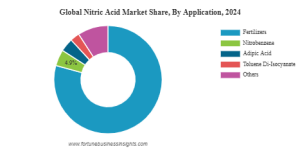

According to Fortune Business Insights, The global nitric acid market size was valued at USD 30.06 billion in 2024. The market is projected to grow from USD 30.84 billion in 2025 to USD 37.41 billion by 2032, exhibiting a CAGR of 2.8% during the forecast period. Asia Pacific dominated the nitric acid market with a market share of 51.03% in 2024.

Vehicle manufacturers are concentrating on cutting-edge technologies owing to the rising demand for lightweight automobiles. This, in turn, is anticipated to propel the demand for HNO3 as companies are transitioning toward nylon to reduce weight and enhance fuel capacity. Fortune Business Insights presents this information in their report titled "Global Nitric Acid Market, 2025–2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/nitric-acid-market-104566

Segments

Dominance of Fertilizers Segment Driven by Growing Agricultural Activities

Based on application, the market is segmented into fertilizers, nitrobenzene, adipic acid, toluene di-isocyanate, and others. The increasing demand for agricultural activities to meet the needs of a growing population has led to the fertilizers segment holding the largest share nitric acid market share. It is utilized in the production of fertilizers such as ammonium nitrate and calcium ammonium nitrate, which play a vital role in achieving high-quality and abundant crop yields.

From the regional ground, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Major Players Profiled in the Report:

- BASF SE (Germany)

- Nutrien (Canada)

- EuroChem (Switzerland)

- CF Industries Holdings, Inc. (U.S.)

- Omnia Holdings Limited (South Africa)

- Dyno Nobel (Australia)

- Enaex S.A. (Chile)

- Sasol (South Africa)

- LSB Industries (U.S.)

- IXOM (Australia)

Report Coverage

The comprehensive report presents an intricate examination of the market, with a specific emphasis on prominent enterprises, cutting-edge technologies, and prominent application domains. Moreover, the research report provides valuable observations on prevailing market trends and showcases noteworthy advancements within the industry. Alongside the aforementioned elements, the report encompasses numerous factors that have played a significant role in fostering the market's expansion in recent times.

Drivers and Restraints

Growing Construction Activities and Infrastructure Projects Propel Market Growth

The market growth is driven by increased construction activities, as Toluene di-isocyanate (TDI) and HNO3 intermediate are essential in the production of polyurethane foams, wood and floor coatings, and insulation materials. Additionally, the growth of the HNO3 market is fueled by improving consumer lifestyles, rising renovation activities, and new infrastructure projects initiated by governments.

However, governmental policies aimed at environmental protection and waste reduction pose challenges to the nitric acid market growth.

Regional Insights

Asia Pacific Emerges as a Prominent Region with Growing Demand across Industries

Asia Pacific achieved a market size of USD 11.78 billion in 2022, driven by the growing demand for the product across diverse industries such as automotive, agriculture, and construction.

North America is projected to hold a substantial share of the global market, which can be attributed to the region's rapid technological advancements and high disposable income of its consumers.

Competitive Landscape

Key Players Focus on Collaborations and Strategies to Maintain Competitive Edge

Major industry players are actively engaged in enhancing their capacities, driving product innovation, pursuing acquisitions and mergers, and fostering collaborations to gain a competitive advantage in the global market.

Information Source: https://www.fortunebusinessinsights.com/nitric-acid-market-104566

Key Industry Development

- In January 2023, BASF's monomers division, which includes MDI, TDI, propylene oxide, caprolactam, adipic acid, polyamide 6 and 6.6, nitric acid, is planning to expand its portfolio of products with a lower CO2 footprint. This expansion will help the company reach net-zero CO2 emissions by 2050.

- In July 2023, Nutrien completed a turnaround project at its Geismar, Louisiana nitrogen facility, aiming to ensure reliable operations and contribute to a more sustainable future. In addition to the direct economic and operational benefits, a voluntary environmental abatement project undertaken during the turnaround is expected to reduce CO2e emissions by approximately 200,000 tons per year from their highest production nitric acid manufacturing unit.

Posted in: Business

| 0 comments

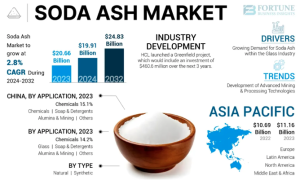

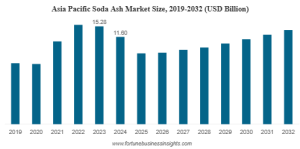

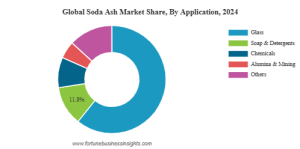

The global soda ash market is experiencing robust growth, driven by increasing demand from key industries such as glass manufacturing, detergents, chemicals, and water treatment. Soda ash, also known as sodium carbonate (Na₂CO₃), is an essential raw material used in several industrial processes due to its strong alkalinity and versatile chemical properties.

Market Size and Forecast

According to Fortune Business Insights, The global soda ash market size was valued at USD 18.74 billion in 2024. The market is projected to grow from USD 15.03 billion in 2025 to USD 23.39 billion by 2032, exhibiting a CAGR of 6.5% during the forecast period. Asia Pacific dominated the soda ash market with a market share of 61.89% in 2024.

The market expansion is primarily driven by rapid industrialization, rising infrastructure development, and increasing consumption of glass products across automotive, construction, and solar industries.

Key Takeaways

Market Value (2024): USD 18.74 billion

Market Value (2032): USD 23.39 billion

Growth Rate (CAGR): 6.5% (2025–2032)

Leading Region: Asia Pacific (61.89% share in 2024)

Major Drivers: Glass manufacturing, detergents, and solar glass demand

Emerging Trend: Transition to sustainable and energy-efficient production

Information Source: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/soda-ash-market-110681

Key Market Segments

By Type

Synthetic Soda Ash:

Synthetic soda ash accounted for the largest market share in 2024 owing to its consistent quality and wide applicability in glass manufacturing, detergents, and chemical synthesis.

Natural Soda Ash:

The natural variant is gaining traction due to its lower energy requirement and reduced carbon emissions during production, aligning with sustainability goals.

By Product Type

Dense Soda Ash:

Dense soda ash dominated the market in 2024, driven by strong demand from the glass industry. It is preferred for its high bulk density, low dust content, and stability in manufacturing operations.

Light Soda Ash:

Light soda ash is primarily used in detergent, chemical, and water treatment applications where fast dissolution is required.

By Application

Glass Manufacturing: The largest segment, fueled by growing demand for flat, container, and solar glass.

Soaps and Detergents: Used as a water-softening and cleaning agent, particularly in household and industrial detergents.

Chemicals and Mining: Employed in the production of sodium silicates, bicarbonates, and alumina.

Water Treatment: Acts as a pH regulator and neutralizing agent for industrial and municipal water systems.

List of Key Soda Ash Companies Profiled

- Tata Chemicals Ltd. (India)

- Ciner Group (Turkey)

- NIRMA (India)

- Solvay (Belgium)

- DCW Ltd. (India)

- Shandong Haihua Group Co., Ltd. (China)

- Sudarshan Mineral (India)

- Şişecam (Turkey)

- Angel Chemicals Private Limited (India)

- Radhe Enterprise (India)

- InoChem (Saudi Arabia)

Regional Insights

The Asia Pacific region dominated the global soda ash market in 2024, accounting for approximately 61.89% of total market share. This dominance is attributed to strong glass and detergent production capacities in China and India, along with rapid infrastructure growth and urbanization.

North America and Europe are witnessing steady demand supported by industrial applications and the development of sustainable soda ash production technologies. Meanwhile, emerging economies in the Middle East, Africa, and Latin America present lucrative opportunities due to increasing construction and water treatment activities.

Market Trends and Developments

Shift Toward Sustainable Production:

Manufacturers are investing in green technologies and low-emission processes such as the e.Solvay process to minimize carbon footprints and improve energy efficiency.

Technological Advancements:

Adoption of advanced mining techniques, real-time monitoring, and automation to optimize production and reduce operational costs.

Rising Solar Glass Demand:

Rapid expansion of the solar energy sector is significantly increasing the consumption of high-purity soda ash used in solar glass manufacturing.

Expansion in Emerging Markets:

Growing population, industrial development, and higher standards of living in Asia, Africa, and Latin America are boosting demand for detergents and consumer goods containing soda ash.

Challenges

Fluctuating Raw Material and Energy Costs:

Price volatility of key inputs such as limestone, salt, and energy resources can impact production economics.

Environmental Regulations:

Stringent emission and waste disposal regulations are compelling producers to adopt cleaner technologies, leading to increased production costs.

Market Price Pressure:

Oversupply in certain regions and intense competition among global producers can affect profitability.

The global soda ash market is set to continue expanding steadily through 2032, driven by high demand from glass and detergent industries and growing emphasis on sustainable production practices. The market’s transition toward low-carbon, energy-efficient processes will shape the competitive landscape in the coming years.

Companies focusing on cost efficiency, environmental sustainability, and technological innovation will gain a strong competitive edge. Furthermore, rising investments in renewable energy infrastructure, particularly solar power, will provide significant opportunities for market participants.

Information Source: https://www.fortunebusinessinsights.com/soda-ash-market-110681

KEY INDUSTRY DEVELOPMENTS

- December 2023: Solvay introduced a new soda ash production process named e.Solvay process. This new technology promises to cut CO₂ emissions by 50%, reduce energy, water, and salt consumption by 20%, and decrease limestone use and residues by 30%.

- June 2023: Tata Chemicals announced a USD 968.0 million capex plan, including a 380 KT salt capacity addition in the U.K. and Mithapur, India. This would boost its global salt capacity to 2.3 MT and India’s to 1.8 MT. The investments aimed to support growth, sustainability, and increased production across key product lines.

Posted in: Business

| 0 comments

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/oleochemicals-market-106250

Segments

Fatty Acid to Lead Due to Easy Availability of Raw Materials

On the basis of type, the market is divided into fatty acids, fatty alcohols, methyl esters, and glycerin. Fatty acid is anticipated to have the dominant part due to easy availability of raw materials and growing demand for organic personal care products. Fatty acids are an important part as they serve as a raw material to produce several downstream derivatives, including elastomers, toiletry, biocides, softeners, and wax.

Food & Beverages Segment to Lead Due to Wide Adoption of Various Additives and Stabilizers

On the basis of application, the market is divided into food & beverages, chemicals, animal feed, and others. Food & beverages segment is anticipated to have the dominant part due to increasing adoption of bio-based thickeners, stabilizers, and other food additives in the food industry. The chemical segment is expected to be growing at the fastest CAGR due to high demand for sustainable alternatives for petroleum-derived chemicals.

List of Key Players Profiled in the Report

- Cargill Inc. (U.S.)

- Kuala Lumpur Kepong Berhad (Malaysia)

- BASF SE (Germany)

- Oleon N.V. (Belgium)

- IOI Group Berhad (Malaysia)

- Wilmar International (Singapore)

- Kao Chemicals (Japan)

- Twin Rivers Technologies (U.S.)

- Croda Industrial Chemicals (U.K.)

- Evonik Industries (Germany)

- Emery Oleochemicals (Malaysia)

- Godrej Industries (India)

Report Coverage

The report provides a detailed analysis of the top segments and the latest trends in the market. It comprehensively discusses the driving and restraining factors and the impact of COVID-19 on the market. Additionally, it examines the regional developments and the strategies undertaken by the market's key players.

Drivers and Restraints

Increasing Demand from Various End-use Industries to Drive Market Expansion

Rising demand from various end-user industries is anticipated to drive the oleochemicals market growth. These chemicals are highly employed by various sectors, including personal care, cosmetics, food & beverages, pharmaceuticals, and plastics. They are used in skincare and haircare products. They are used due to their high demand for hypoallergenic and chemical-free ingredients, which is expected to propel market development. Lower cost and sustainability of raw materials used are set to boost market growth. Increasing demand for biofuels is expected to push market growth.

However, VOC production at the time of pre-treatment of glycerin is expected to hinder the market growth.

Regional Insights

Asia Pacific to Lead Market Share Due to Growing Awareness Regarding Harmful Effects of Fossil Fuels

Asia Pacific is anticipated to head the oleochemicals market share due to growing awareness amongst people regarding the harmful effects of the exploitation of fossil fuels and petrochemical resources. The majority demand in the region is backed by ASEAN countries and China. The region is a major producer and exporter of oleochemical feedstock and its derivatives.

North America is expected to have considerable growth due to stringent regulations regarding practicing sustainability and the growing demand for plant-based products.

Information Source: https://www.fortunebusinessinsights.com/oleochemicals-market-106250

Competitive Landscape

Upgrading of Product Portfolio by Key Market Players to Set Market Progression

Key players of market are BASF, Evonik, Emery Oleochemicals, Twin River Technologies, Cargill Inc., and Croda Industrial Chemicals. They have been updating and elevating their product portfolios for enhancing their market share. In December 2021, Cargil Inc. decided to remove iTFAs from its entire global edible oil portfolio. The purpose of the new edible oil range is to support food manufacturers to produce healthier products for consumers.

Key Industry Development

- August 2022 - The Kuala Lumpur Kepong Berhad Group offered a product named DavosLife E3, which can be used in food and nutrition applications. According to Kuala Lumpur Kepong Berhad, the product has wide-reaching, clinically proven health benefits for heart health, liver health, and brain health.

- July 2022 BASF SE offered the first rainforest alliance-certified personal care ingredients based on coconut oil. The company established a renewable supply chain, which will help the company maximize its revenue.

Posted in: Business

| 0 comments