Adherence Packaging Market Demand, Industry Insights, and Future Outlook, 2025-2032

By ameliasss, 2025-09-08

According to Fortune Business Insights, The global adherence packaging market was valued at USD 1.13 billion in 2024 and is anticipated to grow to USD 1.20 billion in 2025, eventually reaching USD 1.89 billion by 2032. This growth reflects a CAGR of 6.67% over the forecast period. In 2024, North America led the market, accounting for 38.05% of the global share.

Adherence packaging is a pharmacy service that organizes a patient’s medications into personalized pouches or blister packs aligned with their dosing schedule. Its primary purpose is to improve medication adherence and, as a result, clinical outcomes. Demand for these solutions is rising—particularly among older adults and people with chronic conditions—and is being further propelled by innovations such as smart packaging and the integration of digital health technologies, which are expanding the global market. Adherence packaging, also called compliance packaging means the method of packaging that makes the adherence of patients to their drug routine easy. The surge in the emphasis of prominent companies on the enhancement of medication adherence through more patient-focused and intelligent packaging methods, which leads to the generation of data from current delivery systems and medicines while aiding in the reduction of wastage of drugs, is fostering the market growth.

Fortune Business Insights presents this information in their report titled " Adherence Packaging Market , 2025–2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/adherence-packaging-market-108330

List of Key Adherence Packaging Companies Profiled

- WestRock Company (U.S.)

- Manrex Limited (Canada)

- Parata Systems LLC (U.S.)

- McKesson Corporation (U.S.)

- Pearson Medical Technologies LLC (U.S.)

- Cardinal Health, Inc. (U.S.)

- Omnicell, Inc. (U.S.)

- Becton, Dickinson, and Company (U.S.)

- Talyst, LLC (U.S.)

- TCGRx (U.S.)

Segmentation:

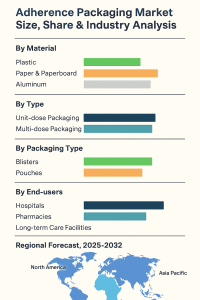

By material, the market is classified into aluminum, paper & paperboard, and plastic. The plastic segment captured the largest adherence packaging market share in 2023. This can be attributed to the cost-effectiveness, transparency, lightweight, and malleable nature of plastic.

In terms of type, the market is bifurcated into multi-dose and unit-dose. The multi-dose segment accounts for the largest share due to the growing requirement for adherence to medication.

Based on packaging type, the market is segregated into pouches and blisters. The blisters segment holds the largest market share. Enhanced shelf-life, ease of transport, and high resistance to tamper provided by blisters are augmenting the segment expansion.

With respect to end users, the market for adherence packaging is segmented into long-term care facilities, pharmacies, and hospitals.

Geographically, the market is divided into the Asia Pacific, Latin America, the Middle East & Africa, Europe, and North America.

Report Coverage

The research report provides a detailed analysis of the major strategic initiatives opted for by leading players in the market. In addition, it highlights the top trends, key industry developments, and the impact of the COVID-19 pandemic on the market growth. Additional aspects of the report include the notable factors impacting the adherence packaging market size.

Drivers:

Surging Desire to Remove Drug Wastage to Impel the Market Growth

The adherence packaging market growth can be credited to a rise in desire for the removal of wastage of the drug. Moreover, medication waste accounts for a substantial impact on the economy and the healthcare system across the globe and creates detrimental consequences for the environment.

Regional Insights:

North America Dominates Due to Rising Life Science & Medical Research Activities

North America accounts for the dominating position in the market. This is due to the growing spending power on healthcare coupled with the surging medical research & life science research activities.

Europe is the second-leading region in the adherence packaging market owing to the heightened availability of government funding for activities pertaining to research and development.

The Asia Pacific market is observing the fastest growth owing to the growing uptake of the solution along with healthcare sector investments.

Information Source: https://www.fortunebusinessinsights.com/adherence-packaging-market-108330

Competitive Landscape:

Top Players Emphasize Launching New Products to Reinforce Their Industry Position

Mergers & acquisitions, partnerships, and joint ventures are some of the strategies opted for by leading companies to gain a competitive edge in the adherence packaging market. Several firms are also focusing on launching new products to sustain their industry leadership.

Key Industry Development

- In April 2024, Gerresheimer partnered with U.S. digital health company RxCap, acquiring a minority stake. Gerresheimer's subsidiary Center aimed at distributing RxCap's adherence solutions in U.S. pharmacies, leveraging its market leadership in prescription vials to enhance pharmacy workflows with smart technology.

- In April 2024, Jones Healthcare Group launched a new line of smart adherence packages that utilizes technology to monitor medication usage and enhance patient engagement.

Exterior Wall Systems Market Size, Share & Regional Outlook North America, Europe, Asia Pacific 2025-2032

By ameliasss, 2025-09-04

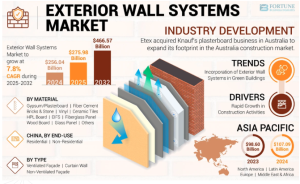

According to Fortune Business Insights, The global exterior wall systems market was valued at USD 256.04 billion in 2024 and is expected to expand from USD 275.98 billion in 2025 to USD 466.57 billion by 2032, registering a CAGR of 7.8% over the forecast period. Asia Pacific led the market in 2024, accounting for 42.14% of the share. In addition, the U.S. exterior wall systems market is anticipated to experience robust growth, projected to reach USD 55.45 billion by 2032. This growth is primarily fueled by the rising adoption of dry construction techniques over traditional wet methods, boosting the demand for exterior wall system products.

Exterior wall systems refer to an enclosure or envelope of a structure that is made to protect the interiors from the external environment. Governments as well as private organizations are increasing their investments in residential, commercial, and industrial establishments, which has augmented the demand for these wall systems. Moreover, the construction sector is rapidly expanding in developing countries, which will further fuel the exterior wall systems market growth.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/exterior-wall-systems-market-104394

List of Key Players Profiled in the Report

- Nippon Sheet Glass Co., Ltd (Japan)

- Saint-Gobain (France)

- AGC Inc. (Japan)

- Sika AG (Switzerland)

- PPG Industries, Inc. (U.S.)

- 3A Composite Holding AG (Switzerland)

- SCG (Thailand)

- Etex Group (Belgium)

- Owens Corning (U.S.)

- Evonik Industries AG (Germany)

- LafargeHolcim (Switzerland)

- USG Boral (Australia)

Segments:

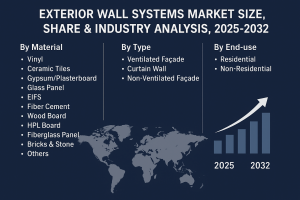

Curtain Walls to Gain Notable Traction Owing to Strong Adoption in the Construction Sector

By type, the market is segmented into ventilated façade, curtain walls, and non-ventilated façade.

The curtain wall segment is expected to account for a dominant exterior wall systems market share due to its strong adoption in the construction sector. Its minimal fabrication time and short duration of construction are expected to enhance its adoption.

Glass Panels to be Widely Demanded Due to their Superior Properties

By material, the market is segmented into ceramic tiles, vinyl, gypsum/plasterboard, glass panels, EIFS, fiber cement, wood board, HPL board, fiberglass panel, bricks & stone, and others. The glass panel segment is expected to dominate the market share due to its superior properties and aesthetics. Further, the introduction of smart glass is expected to enhance the growth of this segment.

Non-Residential End-Users to Increase Product Adoption Due to Increasing Infrastructure Construction

By end-use, the market is bifurcated into residential and non-residential. The non-residential segment is expected to hold a dominant market share due to the rising number of infrastructure and construction projects across the globe. This factor may promote the growth of the segment.

Geographically, the market is segmented into North America, Asia Pacific, Europe, Latin America, and the Middle East & Africa.

Report Coverage

The report analyses the market in depth and highlights crucial aspects such as leading end-users, prominent companies, key disposable types, and distribution channels. It also provides valuable insights into the market dynamics, trends, and covers vital industry developments. Besides the factors mentioned above, the report encompasses various factors that have contributed to the growth of the market in recent years.

Driving Factors

Increasing Construction Projects Globally to Elevate Market Growth

Commercial, industrial, and residential construction activities have increased significantly in recent years across the world, which boosted the demand for exterior wall systems. Governments are also taking various initiatives to modernize the existing infrastructure by increasing the flow of foreign investments in large-scale infrastructure construction projects. These factors are predicted to fuel the market growth.

However, stringent government regulations regarding carbon emission levels are likely to restrict the market growth.

Regional Insights

Increasing Construction Projects in Developing Countries to Boost Market Growth in Asia Pacific

Asia Pacific is projected to dominate the global exterior wall systems market share due to a dramatic increase in construction projects. For example, rising infrastructure projects, such as Beijing’s Daxing International Airport and the Shanghai Urban Rail Transit Expansion projects, are likely to elevate the industry growth.

In Europe, the increasing trends of green buildings and energy efficiency are expected to enhance the adoption of exterior wall systems. These factors may propel the industry growth.

Information Source: https://www.fortunebusinessinsights.com/exterior-wall-systems-market-104394

Competitive Landscape

Companies Undertake Different Growth Strategies to Maintain Leading Market Position

Prominent companies operating in the market are focusing on innovating their existing product ranges to cater to the ever-growing demand for wall systems. These organizations are developing eco-friendly and innovative products to expand their presence. They are also partnering with renowned raw material suppliers and construction companies to stay ahead of their competition. These initiatives will help them maintain their position in the industry.

Key Industry Development

- March 2022: Holcim announced the acquisition of Malarkey Roofing Products with estimated 2022 net sales of USD 600 million. Through this acquisition, Malarkey would help Holcim expand its range of roofing systems in the highly profitable U.S. residential roofing market. This move was important for Holcim to achieve its goal of touching USD 4 billion in roofing net sales by 2025, while also speeding the company's expansion of its product and solution range.

Pharmaceutical Packaging Market Global Expansion & Innovation Outlook 2025-2032

By ameliasss, 2025-09-04

According to Fortune Business Insights, The global pharmaceutical packaging market was valued at USD 110.55 billion in 2024 and is expected to grow to USD 116.58 billion in 2025, reaching USD 177.12 billion by 2032. This growth reflects a CAGR of 6.16% over the forecast period. In 2024, North America led the market, accounting for 30% of the overall share. The surge is due to the escalating prevalence of non-communicable and communicable diseases across various regions.

Pharmaceutical packaging refers to the materials and processes designed to protect, preserve, and deliver pharmaceutical products. Its primary role is to shield drugs from external factors such as moisture, light, and temperature fluctuations, while also ensuring the product stays securely contained, free from leakage or contamination.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/pharmaceutical-packaging-market-102860

List of Key Players Mentioned in the Report:

- Amcor Plc (Switzerland)

- Gerresheimer AG (Germany)

- SCHOTT AG (Germany)

- Westrock (U.S.)

- AptarGroup, Inc. (U.S.)

- Berry Global, Inc (U.S.)

- NIPRO (Japan)

- CCL Industries Inc. (Canada)

- West Pharmaceutical Services (U.S.)

- SGD Pharma (France)

- Ardagh Group S.A. (Luxembourg)

- International Paper (U.S.)

- Comar LLC (U.S.)

- Vetter Pharma (Germany)

- Nolato AB (Sweden)

Segments:

Plastics Segment to Gain Traction Considering its Extensive Usage

Based on material, the market is segmented into plastics, glass, metal, paper & paperboard, and others. The plastic segment is anticipated to depict a notable upsurge over the forecast period. Plastic is the most considerable raw material used in the production of pharmaceutical packaging.

Bottles Segment to Register Prominent Share Impelled by Low Costs

Based on product type, the market is subdivided into bottles, vials & ampoules, caps & closures, blister packs, pre-fillable inhalers, pre-fillable syringes, bags & pouches, jars & canisters, cartridges, and others. Of these, the bottles segment is poised to expand at a substantial pace over the estimated period. The surge is on account of low cost and light weight.

Primary Packaging Segment to Grow at the Fastest Pace Impelled by the Advantage of Protection Against Chemicals

On the basis of packaging type, the market for pharmaceutical packaging is categorized into primary, secondary, and tertiary. The primary packaging segment is estimated to expand at a commendable pace over the study period. The products help in the maintenance of shelf life and protect the drugs from chemicals and moisture.

Oral Drug Delivery Packaging to Hold Dominating Share Owing to Flexibility in Designing Dosage

By drug delivery mode, the market is segregated into oral drug delivery packaging, nasal drug delivery packaging, topical drug delivery packaging, ocular drug delivery packaging, injectable packaging, transdermal drug delivery packaging, pulmonary drug delivery packaging, and others. The oral drug delivery packaging segment held a dominating share in the global market.

By geography, the market has been studied across North America, Asia Pacific, Europe, Latin America, and the Middle East & Africa.

Report Coverage:

The report presents a systematic study of the market’s segments and a thorough analysis of the market overview. An in-depth evaluation of the current market trends as well as future opportunities is offered in the report.

Drivers and Restraints:

Expanding Pharmaceutical Industry Around the Globe to Drive Market Growth

In wealthy nations such as the U.S., the U.K., and Germany as well as in developing nations such as China, India, and Brazil, the pharmaceutical sector is expanding quickly. The population is growing, technological advancements are increasing, and new government regulations are being put in place to stop the spread of infectious diseases. Additionally, the rising demand for biological products and emerging treatments such as cell and gene therapies are expected to promote the pharmaceutical packaging market growth.

However, an escalation in counterfeit drugs could hamper industry expansion to a considerable extent.

Regional Insights:

North America to Lead Backed by Elevated Demand for Packaging due to Rising Healthcare Expenditure

The U.S. is the largest contributor to North America, which has the largest pharmaceutical packaging market share. The region's development is attributable to the pharmaceutical industry's explosive growth. The market growth in this region is being driven by the increased need for primary packaging goods, surging healthcare spending, and rising disease prevalence.

Germany, the U.K., and Italy in Europe accounted for the second-largest market in the globe. Pre-filled syringes, plastic bottles, containers, vials, and ampoules have all aided in the expansion of this industry.

China, Japan, and India are the top three nations in the Asia Pacific contributing to the market expansion.

Information Source: https://www.fortunebusinessinsights.com/pharmaceutical-packaging-market-102860

Competitive Landscape:

Innovative Product Launch Initiatives by Key Players to Bolster Market Growth

The prominent players adopt several strategies to bolster their position in the market as leading companies. One such key strategy is acquiring companies to bolster their brand value among users. Another essential strategy is periodically launching innovative products with a detailed study of the market and its target audience.

Key Industry Development:

January 2024- SGD Pharma launched the extension of its Clareo range to include 10ml and its Sterinity range of ready-to-use vials in sizes 10ml and 20m. The Clareo range of molded glass vials is available in sizes from 10ml to 200ml. These vials are designed to meet American market specifications and have a GPI 20 neck finish.

Tinplate Packaging Market Share and USD 2.65 Billion Growth Forecast 2025-2032

By ameliasss, 2025-09-03

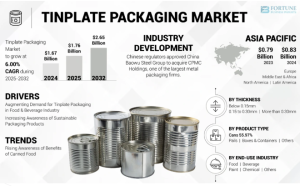

According to Fortune Business Insights, The global tinplate packaging market was valued at USD 1.67 billion in 2024 and is expected to expand steadily, reaching USD 1.76 billion in 2025 and further advancing to USD 2.65 billion by 2032. This reflects a compound annual growth rate (CAGR) of 6.00% over the forecast period. In 2024, Asia Pacific led the market, accounting for 49.70% of the global share. Meanwhile, the U.S. tinplate packaging market is anticipated to experience substantial growth, projected to achieve USD 425.71 million by 2032, fueled by the rising demand for packaged and processed food products.

Tinplate is a product made from steel that offers a lustrous and sturdy appearance to a product packaged with this item. The material is used to pack canned beverages, foods, paints, and cosmetics. The growing demand for sustainable packaging solutions will help this market grow. The material’s ability to withstand high pressure, temperature, and physical damage during the manufacturing process and transportation is fueling the growth of this market. Furthermore, high recyclability, durability, and easy printability are some of the factors driving the product’s sales.

Fortune Business Insights™ displays this information in a report titled, "Tinplate Packaging Market, 2025-2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/tinplate-packaging-market-109390

LIST OF KEY COMPANIES PROFILED IN THE REPORT:

- CPMC Holdings Limited (China)

- Tata Steel (India)

- AJ Packaging Limited (India)

- ColepPackaging (Portugal)

- ArcelorMittal (Luxembourg)

- Toyo Kohan Co., Ltd. (Japan)

- United States Steel Corporation (U.S.)

- Crown (U.S.)

- Italtin S.r.l. (Italy)

- Mauser Packaging Solutions (U.S.)

- Nampak Ltd. (South Africa)

Segmentation:

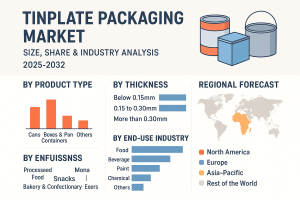

Cans Dominate Market Due to Their Ease of Use

Based on product type, the market is segmented into cans, boxes & containers, pails, and others. The can segment is dominating the tinplate packaging market share as it offers a wide range of benefits, such as ease of use, durability, and sustainability.

Increasing Use in Several Industries Boosted Demand for Tinplate Sheets of 0.15-0.30mm Thickness

Based on thickness, the market is segmented into below 0.15mm, 0.15 to 0.30mm, and more than 0.30mm. Tinplate sheets in the thickness range of 0.15 to 0.30 mm dominate the market as they are lightweight and reduce the need for additional packaging materials, thereby increasing their use in several industries.

Food Industry Emerges as Major End-User Due to Supreme Preservation Properties of Tinplate Packaging

Based on end-use industry, the market is segmented into food [processed food, snacks, bakery & confectionary, edible oil, others], beverage [alcoholic, non-alcoholic], paint, chemical, and others. The food segment is dominating the market as tinplate packaging products are widely used in this industry due to their excellent food preservation features.

With respect to region, the market covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report has conducted a detailed study of the market and highlighted several critical areas, such as leading product types and key market players. It has also focused on the latest market trends and the key industry developments. Apart from the aforementioned factors, the report has given information on many other factors that have helped the market grow.

Drivers and Restraints:

Rising Demand for Tinplate Packaging in Food & Beverage Industry to Boost Market Growth

The adoption of tinplate packaging solutions is rising in the food & beverage sector as they offer a wide range of beneficial features, such as excellent food preservation properties. These properties prevent air, moisture, and other external factors from entering the food item, thereby protecting its quality and shelf life.

However, the high production costs associated with these packaging solutions will hinder the tinplate packaging market growth.

Regional Insights:

Asia Pacific Dominates Global Market Owing to High Consumption of Canned Foods

Asia Pacific held a dominant market share in 2023 as the region is witnessing strong growth in the sales of canned foods due to factors, such as rapid urbanization and rising disposable income of the population.

North America is the second-dominating region in the global market owing to the rising preference for processed foods.

Competitive Landscape:

Key Market Players to Offer Sustainable Packaging Solutions to Gain Strong Competitive Edge

The tinplate packaging market is quite competitive and fragmented, with a few companies leading the market’s growth. These firms are using a wide range of innovative technologies to develop sustainable packaging solutions. This move will help them strengthen their market position and expand their customer base.

Information Source: https://www.fortunebusinessinsights.com/tinplate-packaging-market-109390

Notable Industry Development:

February 2024 - Chinese regulators approved China Baowu Steel Group to acquire CPMC Holdings, which is one of the largest metal packaging firms. The acquisition will help China Baowu Steel Group increase its customer base in the metal canning industry and boost the firm’s profitability.

July 2023 - Tata Steel joined hands with its subsidiary company Tinplate Company of India to recycle tin cans to prevent the reuse of cans due to health and safety issues. Such initiatives will increase awareness among people and also set new standards for other competitors.

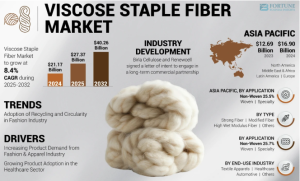

According to Fortune Business Insight, The global v iscose staple fiber market was valued at USD 21.17 billion in 2024 and is expected to expand from USD 27.37 billion in 2025 to USD 40.26 billion by 2032, reflecting a CAGR of 8.4% during the forecast period. Asia Pacific emerged as the leading region, accounting for 79.83% of the market share in 2024. In addition, the U.S. viscose staple fiber market is anticipated to witness robust growth, projected to reach USD 2.17 billion by 2032, supported by its superior properties and increasing recognition as a sustainable alternative to cotton.

Made from regenerated natural materials such as cotton linters or wood pulp, Viscose Staple Fiber (VSF) is a cellulose fiber valued for its softness, drapability, and absorbency, making it widely used in home textiles, clothing, and various consumer products. Increasing consumer awareness of the environmental impact of clothing is fueling demand for sustainable fibers, such as viscose staple fibers.

Fortune Business Insights™ provides this information in its research report, titled “Viscose Staple Fiber Market, 2025-2032”.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/viscose-staple-fiber-market-105431

List of Key Players Mentioned in the Report:

- Grasim Industries Limited. (India)

- LENZING Group (Austria)

- Tangshan Sanyou Group Xingda Chemical Fiber Co.Ltd (China)

- Sateri Holdings Limited (China)

- Kelheim Fibers GmbH (Germany)

- Xinjiang Zhongtai Chemical Co., Ltd. (China)

- Kayavlon Impex Pvt. Ltd. (India)

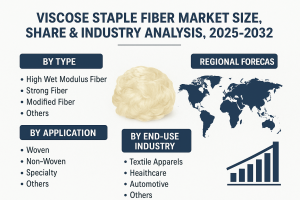

Segmentation:

Strong Fiber Leads with Rising Demand for Organic and Sustainable Solutions

By type, the market is segmented into strong fiber, modified fiber, high wet modulus fiber, and others. The strong fiber segment secured the largest market share in 2023 and is slated to remain the leading segment during the forecast period. As organic materials, strong viscose fibers meet the growing demand for organic and sustainable materials, positioning them favorably in the market.

Woven Segment Dominates due to Increasing Demand for High-Performance Fabrics

In terms of application, the market is divided into non-woven, woven, and specialty. The woven segment held the key viscose staple fiber market share in 2023. With various industries seeking reliable and durable fabrics, the growing demand for high-performance materials propels the preference for woven fabrics.

Textile Apparels Hold Prominent Position with Amplified Demand from Fashion Sector

Based on end-use industry, the market is fragmented into healthcare, automotive, textile apparels, and others. The textile apparels segment held the largest market share in 2023 fueled by the escalating demand from the fashion industry

In terms of region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- The latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers and Restraints:

Increasing Product Demand from Fashion & Apparel Industry to Bolster Market Growth

Rising demand for sustainable materials in the fashion industry has propelled the adoption of the product due to its eco-friendly properties and versatility. Moreover, with changing consumer buying habits and rising disposable income, the apparel industry is expanding, leading to a higher demand for high-quality textiles and garments made from VSFs.

However, reliance on wood pulp from natural forests instead of sustainably harvested trees restricts viscose staple fiber market growth due to environmental concerns.

Regional Insights:

Asia Pacific Dominates the Market Owing to Surging Demand Across Industries

Asia Pacific holds the dominating position in the global market and held the largest market share in 2023. The increasing textile demand across diverse sectors is driving the need for viscose staple fibers in Asia Pacific.

In Latin America, increasing demand for fabrics in both domestic and industrial applications is fueling market growth, driven by urbanization and changing consumer preferences.

Information Source: https://www.fortunebusinessinsights.com/viscose-staple-fiber-market-105431

Competitive Landscape:

Key Players Adopt Sustainable Practices to Minimize Wastewater Generation

Sateri, Lenzing Group, Kelheim Fibers GmbH, and Xinjiang Zhongtai Chemical Co., Ltd. are major viscose staple fiber market players emphasizing product innovation and sustainable practices. They focus on integrating new technologies to boost efficiency and minimize wastewater generation. Grasim Industries Limited's Nagda unit aims for zero liquid discharge, while LENZING Group is adopting renewable energy at subsidiaries such as Lenzing Nanjing Fibers and PT. South Pacific Viscose, signaling a commitment to eco-friendly operations.

Key Industry Development:

- May 2023 - Kelheim Fibres GmbH and Santoni Spa joined forces to develop a sustainable and advanced menstrual underwear from superior-quality performance viscose fiber and advanced machine technology. The product comprises a softer outer layer and an inlay part made from superior wood-based fibers.

- November 2022 - The LENZING Group completed a milestone of 300,000 tons of LENZING ECOVERO branded fibers production with the target to double the production capacity by 2023 due to rising demand.

According to Fortune Business Insights, In 2018, the global cellulose market was estimated at USD 219.53 billion and is forecast to attain USD 305.08 billion by 2026, corresponding to a compound annual growth rate (CAGR) of 4.2% over the forecast period. North America dominated the market in 2018, holding a 28.91% share. The U.S. market is anticipated to register significant growth, reaching an estimated USD 88.01 billion by 2032, driven primarily by increased demand for cellulose-based applications in the paper and construction industries. Driven by applications across diverse industries, the market will exhibit considerable growth in the coming years. According to a report published by Fortune Business Insights, titled “ Cellulose Market Size, Share & Industry Analysis, By Derivative Type (Commodity Cellulose Pulp, Cellulose Fibers, Cellulose Ethers, Cellulose Esters, Microcrystalline Cellulose, Nano-cellulose, and Others), By End-Use Industry (Textile, Food, Chemical Synthesis, Pharmaceuticals, Construction, Paper & Pulp, Paints & Coatings, and Others), and Regional Forecast, 2025-2032 ”

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/cellulose-market-102062

Some of the leading companies that are operating in the global cellulose market are:

- Daicel Corporation

- Sigma Aldrich

- DuPont De Nemours Company

- Akzo Nobel

- Ashland inc.

- Celanese Corporation

- International Paper

- Fulida Group Holding Co., Ltd.

- Nylstar S.L.

- FiberVisions Corporation

- Invista

- Bracell

- Sigachi Industries Pvt. Ltd.

- FMC Biopolymer

Cellulose is a natural polymer made of glucose units linked together in a straight chain. Found in wood (40–45%) and plants (up to 90%), it is the most common solid material on Earth. It comes mainly from sources such as wood, cotton, flax, hemp, and jute. Cellulose is valued for its strength, water-loving nature, and ability to absorb moisture.

Cellulose is a pulp that is derived from plant sources. The substance possesses exceptional properties such as its hydrophile nature, good mechanical performance, and hygroscopic nature. These properties have led to applications across diverse industries, including chemical, textile, and food and beverages. Recent advancements in fabrication technologies have opened up a huge potential for the growth of the companies operating in this market. The shift of preference from petroleum-based products to sustainable resources will contribute to the growing demand for cellulose across the world. Moreover, availability of cellulose-originating products will lead to a wider product adoption, subsequently aiding the growth of the cellulose market in the coming years.

The report provides an in-depth analysis of the global cellulose market. It highlights the latest product launches and labels major innovations in the market. In addition to this, it states the impact of these products on the growth of the market. The competitive landscape has been discussed in detail and predictions are made with respect to leading companies and products in the coming years. Forecast values have been provided for the market for the period of 2019-2026. The factual figures have been obtained through trusted sources. Moreover, these predictions are made on the basis of extensive research analysis methods, coupled with the opinions of experienced market research professionals.

Increasing Number of Company Collaborations to Aid Growth

The report encompasses several factors that have constituted an increase in the cellulose market size in recent years. It has been observed that company collaborations are a growing trend among major companies across the world. In January 2020, The Anhui Guozhen Group announced that it has initiated a joint venture with Chemtex. The company plans to establish a large scale commercial plant in China for the production of cellulosic ethanol. The ethanol production will be centred around residues that are normally obtained from the agriculture industry. The plant will have an annual production capacity of 50 KT. Such a huge venture will not only benefit the country but will also have a direct impact on the growth of the overall cellulose market in the coming years.

Asia Pacific Accounts for a Dominating Market Share; Increasing Product Demand Across Diverse Industries to Aid Growth

The market is segmented on the basis of regional demographics into North America, Latin America, Europe, Asia Pacific, and the Middle East and Africa. Among these regions, Asia Pacific currently accounts for the highest cellulose market share. The widespread product applications across diverse industries, and the subsequent rise in the demand for these products will have a direct impact on the growth of the market in this region. Besides Asia Pacific, the market in North America will witness considerable growth in the coming years. As of 2018, the market in North America was worth USD 63.46 billion and this value is projected to rise further in the coming years, driven by product uses in the paper industry.

Information Source: https://www.fortunebusinessinsights.com/cellulose-market-102062

Key Industry Developments

- In January 2020, The Anhui Guozhen Group and Chemtex signed a joint venture to build a first full-scale commercial plant in China for cellulosic ethanol production from residues obtained from agriculture industry. Clariant Specialty Chemicals have granted a license for its sunliquid cellulosic ethanol technology to the joint venture. The plant is to be situated in Fuyang city in the Anhui province of China and is expected to have an annual capacity of 50 KT.

- In May 2019, Bracell announced launch of ‘Project Star’, an expansion plan to increase the production capacity of its pulp mill based in Lencois Paulista, Sao Paolo, Brazil, from 250 KT to 1500 KT by the end of 2021. The project is expected to reach an annual production capacity of 2000 KT pulp with the completion of the project, making them one of the largest pulp producer in the world.

Packaging Waste Management Market Analysis by Service Type & Region 2025-2032

By ameliasss, 2025-09-02

According to Fortune Business Insights, The global packaging waste management market was valued at USD 92.19 billion in 2024 and is expected to grow to USD 96.53 billion in 2025, reaching USD 137.15 billion by 2032. This growth represents a CAGR of 5.15% over the forecast period. In 2024, Asia Pacific led the market, accounting for 31.45% of the total share.

The packaging waste management market covers the collection, sorting, recycling, recovery (including waste-to-energy), and safe disposal of post-consumer and post-industrial packaging materials such as paper & board, plastics, glass, metals, and bioplastics. Demand is being reshaped by circular-economy policies, brand-owner sustainability targets, and rapid growth in e-commerce that changes both the volume and composition of packaging waste. Across regions, governments are tightening regulations (EPR, landfill taxes, deposit return systems), while technology providers are scaling advanced sorting and chemical recycling to increase recovery rates and material quality.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/packaging-waste-management-market-112352

List of the Key Companies Profiled in the Report:

- Waste Mission (U.K.)

- BEWI (Austria)

- Frigorifico Allana Pvt. Ltd. (Austria)

- Bayer AG (Austria)

- ITENE (Austria)

- Merivaara Corporation (Austria)

- Greenbank Recycling Solutions (U.K.)

- Stevcon Packaging & Logistics Ltd (Austria)

- JBS (Austria)

- WM Intellectual Property Holdings, L.L.C. (U.S.)

- PreZero International (Austria)

- Affordable Waste Management Ltd. (Austria)

Key Market Drivers

Policy pressure & EPR : Extended Producer Responsibility (EPR) schemes shift end-of-life costs to producers, accelerating design-for-recycling and funding for collection/sorting infrastructure.

Corporate sustainability targets : FMCG, retail, and consumer brands are committing to higher recycled content and 100% recyclable packaging—creating stable demand for high-quality recyclate.

Surge in e-commerce : More secondary and tertiary packaging (corrugated, flexible plastics) increases volumes and complexity, pushing cities and haulers to adapt collection models.

Landfill/incineration constraints : Rising tipping fees and landfill scarcity in many markets make recovery more economical and politically favored.

Market Challenges

Economics of recycling : Volatile commodity prices and quality variability can make recycled feedstock less competitive versus virgin materials without policy support.

Collection & contamination : Mixed waste streams and low participation rates undermine material value and plant efficiency.

Fragmented regulations : Divergent rules across countries (and even states) complicate compliance for global brands and recyclers.

Difficult-to-recycle formats : Multi-layer films, dark plastics, and small-format items still pose technical and economic hurdles.

Market Segmentation

By Material

Paper & Paperboard

Plastics (PET, HDPE, LDPE/LLDPE, PP, PS, PVC, multi-layer/films)

Glass

Metals (Aluminum, Steel)

Bioplastics/Compostables

By Source

Residential (municipal)

Commercial & Industrial (retail, foodservice, manufacturing, logistics)

By Service

Collection & Transportation

Sorting/Material Recovery (MRF operations)

Recycling & Reprocessing (mechanical and chemical)

Energy Recovery (RDF, waste-to-energy)

Landfill & Other Disposal

Consulting & Compliance (EPR, ESG reporting)

By End Use of Recyclate

Food & Beverage Packaging

Personal Care & Household

Industrial & Logistics (pallets, straps, films)

Construction & Automotive (downstream uses for fibers, glass cullet, metals)

By Region

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Regulatory Landscape (What’s Shaping Demand)

EPR & Packaging Taxes : Funding for collection and MRF upgrades; eco-modulated fees reward recyclable designs.

Deposit Return Systems (DRS) : Raising PET, aluminum, and glass return rates and improving quality (low contamination).

Recycled Content Mandates : Minimum rPET/rHDPE content for beverage bottles and certain rigid/film applications.

Green Claims & Traceability : Stricter substantiation requirements drive investment in chain-of-custody and mass-balance systems.

Technology & Innovation Trends

AI-enabled sorting & robotics : Higher throughput, lower labor dependency, and improved purity levels.

Digital watermarks & markers : Enhancing identification of packaging types at MRF speed.

Chemical recycling (pyrolysis, depolymerization, solvent-based) : Targeting hard-to-recycle plastics to yield near-virgin monomers.

Advanced washing & de-inking : Upgrading recyclate quality for food-grade and high-performance use.

Closed-loop & reuse systems : Refillable packaging, reverse logistics, and durable containers for e-commerce and foodservice.

Biodegradable/compostable packaging : Scaling in targeted applications with appropriate organics collection and composting infrastructure.

Competitive Landscape

The market features a mix of global and regional players across the value chain:

Waste management & MRF operators : Waste Management, Republic Services, Veolia, SUEZ, REMONDIS, Biffa.

Technology & equipment providers : TOMRA, Pellenc ST, AMP Robotics (AI/robotics), Bollegraaf, Stadler (MRF lines).

Recyclers & reprocessors : Indorama Ventures (PET), ALPLA Recycling, Evergreen/CarbonLITE (rPET), Novelis (aluminum), Ardagh (glass).

Energy recovery & WtE : Covanta, EEW Energy from Waste.

Compliance & EPR organizations : PROs and stewardship bodies partnering with municipalities and brands.

Strategic Opportunities for Stakeholders

Design for recycling : Shift to mono-materials, eliminate problem additives, standardize labels (e.g., “widely recyclable”).

Invest in high-purity streams : DRS and curbside upgrades that deliver food-grade PET/HDPE and high-quality OCC.

Flexible packaging solutions : Scale film collection pilots, store drop-off, and chemical recycling feedstock supply.

Data & traceability : Implement digital product passports, batch-level analytics, and verifiable recycled content accounting.

Reuse ecosystems : Target high-frequency, closed environments (stadiums, campuses, QSR chains) to prove economics.

Outlook (2025–2032)

Higher recovery, better quality : Expect steady increases in PET, aluminum, and OCC capture; focus shifts to films and flexible plastics.

Policy-driven investment : EPR and recycled-content mandates sustain capex in MRF modernization, advanced reprocessing, and DRS expansion.

Consolidation & specialization : Larger operators acquire niche recyclers (e.g., films, food-grade PCR), while equipment makers bundle AI, robotics, and optical sorting as turnkey solutions.

Balanced portfolio of solutions : Mechanical recycling remains the backbone; chemical recycling scales selectively where economics and policy align; reuse systems grow in targeted channels.

Emerging markets leapfrog : With EPR funding and digital tools, APAC and parts of LATAM/MEA accelerate from low baselines to modernized systems.

Information Source: https://www.fortunebusinessinsights.com/packaging-waste-management-market-112352

KEY INDUSTRY DEVELOPMENTS

In December 2024, Bisleri International Pvt. Ltd, in collaboration with Sampurn(e)arth Environment Solutions Pvt. Ltd. and the Mineral Foundation of Goa, launches a Material Recovery Facility (MRF) Center in Harvalem, Goa. The facility is designed to handle 360 MT of plastic waste each year. Bisleri's 'Bottles for Change' program seeks to reduce plastic waste in landfills and foster a cleaner, more sustainable ecosystem in the area. The facility will mostly focus on promoting 100% plastic waste separation at the source, beginning with the Curchorem-Cacora area.

In October 2024, At the PPMA Show, Waste Mission, a prominent UK waste management firm, introduced its tailor-made Waste Management Portal. This cutting-edge platform is tailored exclusively for contracted clients, allowing them to handle their waste more efficiently and sustainably than ever while keeping them informed about waste streams, compliance, and ESG goals.

Diethylene Glycol Market Rising Demand Across Industrial Applications 2025-2032

By ameliasss, 2025-09-01

According to Fortune Business Insights, The global diethylene glycol market was valued at USD 5.0 billion in 2024 and is anticipated to expand from USD 5.2 billion in 2025 to USD 6.8 billion by 2032, registering a CAGR of 3.9% during the forecast period. In 2024, Asia Pacific led the market, accounting for 61.4% of the overall share. The Diethylene Glycol (DEG) market is gaining momentum across various industries due to its versatile applications in resins, polyurethanes, plasticizers, coolants, and lubricants. DEG, a clear, hygroscopic, and odorless liquid, is primarily produced as a byproduct of ethylene oxide hydrolysis. Its demand is strongly influenced by the growth of construction, automotive, and textile industries, which are major consumers of resins and polyurethanes.

The global Diethylene Glycol market is projected to witness significant growth between 2025 and 2032, driven by rising consumption in coatings, adhesives, and plastics manufacturing. Additionally, DEG is widely used as a solvent and chemical intermediate, which enhances its importance in chemical processing.

List of Key Diethylene Glycol Players Profiled

- Mitsubishi Chemical Group Corporation (Japan)

- Reliance Industries Limited (India)

- Shell (U.K.)

- SABIC (Saudi Arabia)

- NIPPON SHOKUBAI CO., LTD. (Japan)

- BASF (Germany)

- China Petrochemical Corporation (Sinopec) (China)

- PETRONAS (Malaysia)

- MEGlobal (Kuwait)

- Junsei Chemical Co., Ltd. (Japan)

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/diethylene-glycol-market-113453

Key drivers include:

Expanding polyurethane and polyester resin industries .

Rising demand in construction, automotive, and packaging sectors .

Increasing application in unsaturated polyester resins (UPR) for reinforced plastics.

Widening use as a dehydrating agent in natural gas processing .

However, health hazards and toxicity concerns associated with DEG, along with strict regulatory guidelines, may hinder market expansion.

Diethylene Glycol (DEG) is a versatile, colorless, odorless, and water-soluble organic compound extensively utilized as a solvent, plasticizer, and chemical intermediate. One of the primary growth drivers for DEG is the expanding global polyester industry, where it plays a vital role in the production of unsaturated polyester resins used in coatings, adhesives, and composite materials.

With industries such as packaging, construction, and automotive increasingly adopting polyester-based products, the demand for DEG continues to accelerate. Beyond polyester applications, DEG is also widely employed in brake fluids, hydraulic systems, and cosmetics, further broadening its market scope. Demand is particularly strong in developing regions, where rapid industrialization and urbanization are fueling consumption.

The market is characterized by the presence of several major players, including Mitsubishi Chemical Group Corporation, SABIC, BASF, Sinopec, Reliance, and Shell, among others. Their diverse product portfolios and global reach ensure a competitive landscape and continuous innovation in DEG applications.

Market Segmentation

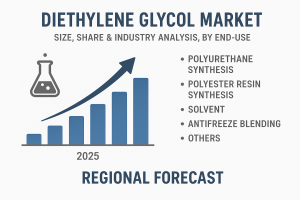

By Application:

Polyester Resins – A major segment, driven by demand in reinforced plastics, coatings, and adhesives.

Plasticizers – Used in flexible PVC production.

Polyurethanes – Expanding applications in construction and automotive.

Lubricants & Coolants – Growing adoption in industrial and automotive cooling systems.

Others – Gas dehydration, cosmetics, and chemical intermediates.

By End-use Industry:

Construction – Usage in UPR, polyurethanes, and adhesives.

Automotive – Lubricants, coolants, and resins.

Textile – Fiber processing and resin production.

Plastics & Packaging – Plasticizers and polymers.

Oil & Gas – Natural gas dehydration applications.

By Region:

Asia Pacific dominates the global DEG market, led by China, India, and Japan , due to strong industrial growth and expanding chemical manufacturing.

North America and Europe follow, with significant usage in automotive, plastics, and construction.

Middle East & Africa show potential growth in natural gas dehydration applications.

Market Trends

Increasing focus on eco-friendly and sustainable chemical processes .

Rising demand for lightweight plastics and resins in automotive and aerospace.

Expanding construction sector driving polyurethane and polyester resin demand.

Strategic capacity expansions and joint ventures by leading DEG producers.

Competitive Landscape

Key players in the Diethylene Glycol market include:

SABIC

Royal Dutch Shell

Dow Chemical Company

Reliance Industries Limited

LyondellBasell Industries

Formosa Plastics Corporation

These companies are focusing on R&D, partnerships, and product innovations to strengthen their market position.

The Diethylene Glycol market is set for robust growth between 2025 and 2032 , supported by its expanding applications in resins, polyurethanes, and plasticizers . Asia Pacific will continue to dominate, while technological advancements and regulatory compliance will shape the competitive dynamics of the market.

Information Source: https://www.fortunebusinessinsights.com/diethylene-glycol-market-113453

KEY INDUSTRY DEVELOPMENTS

- January 2024 – SABIC announced its decision to invest USD 6.5 billion to establish a petrochemical complex in China's Fujian province. This petrochemical complex will have the capability of producing ethylene glycol along with polyethylene, polypropylene and polycarbonate, among others.

- December 2023 – SABIC announced that they have signed a MoU with Scientific Design (SD) and Linde Engineering. As part of this collaboration, these companies will explore the opportunities to decarbonize ethylene oxide and ethylene glycol production.