Blogs

New Update from 24lifesciences

Hormonal replacement therapy (HRT) drugs are pharmaceutical compounds designed to supplement or replace hormones that the body no longer produces in sufficient amounts. These therapies address conditions such as menopause, hypothyroidism, growth hormone deficiency, and male hypogonadism. Key treatment categories include:

- Estrogen Replacement Therapy

- Testosterone Replacement Therapy

- Thyroid Hormone Therapy

- Human Growth Hormone Therapy

HRT drugs aim to restore hormonal balance, improve quality of life, and manage symptoms associated with hormonal deficiencies.

Fromdata to decisions—download the research that powers leaders.

Market Size

The global drugs for HRT market was valued at USD 18.4 billion in 2024 and is projected to reach USD 27.8 billion by 2032 , growing at a CAGR of 5.3% during 2025-2032.

- North America: Dominates due to high healthcare expenditure and awareness

- Asia-Pacific: Fastest-growing region, driven by improving healthcare infrastructure and rising disposable incomes

Market Dynamics

Growth Drivers

- Aging Population: Increasing prevalence of hormonal imbalances in aging individuals

- Awareness and Diagnosis: Rising awareness of hormonal disorders and treatment options

- Advanced Drug Delivery: Technological innovations such as transdermal patches, gels, and long-acting injectables

Market Restraints

- Side Effects: Potential adverse effects of long-term HRT, including cardiovascular risks

- Regulatory Challenges: Stringent approvals for drug safety and efficacy

Opportunities

- Emerging Markets: Expanding healthcare access in Asia-Pacific and Latin America

- New Formulations: Development of safer, patient-friendly drug delivery systems

- Personalized Therapy: Tailored HRT treatments based on individual hormonal profiles

Regional Analysis

North America

- Market Share: Largest region due to advanced healthcare infrastructure

- Key Drivers: High healthcare spending, prevalence of menopause, and well-established pharmaceutical networks

Europe

- Growth Factors: Strong regulatory compliance and growing awareness of HRT benefits

Asia-Pacific

- Fastest-Growing Region: Driven by rising disposable income, expanding healthcare infrastructure, and increasing adoption of advanced therapies

Other Regions

- Latin America & Middle East & Africa: Opportunities due to growing healthcare access and rising chronic conditions requiring HRT

Competitor Analysis

The HRT market is competitive, with global pharmaceutical companies focusing on innovation, strategic partnerships, and regional expansion.

Key Players Include:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- Novo Nordisk A/S (Denmark)

- Eli Lilly and Company (U.S.)

- Abbott Laboratories (U.S.)

- Merck & Co. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- F. Hoffmann-La Roche (Switzerland)

- TherapeuticsMD (U.S.)

Strategies:

- Development of novel drug formulations

- Expansion into emerging markets

- Collaboration with healthcare providers and research institutions

Market Segmentation

By Type

- Estrogen Replacement Therapy: Dominates the market due to rising menopause prevalence

- Subtypes: Oral, Transdermal, Others

- Human Growth Hormone Replacement Therapy

- Thyroid Replacement Therapy:

- Subtypes: Levothyroxine, Liothyronine, Others

- Testosterone Replacement Therapy:

- Subtypes: Injections, Gels, Others

- Others

By Application

- Menopause: Leading segment due to high incidence in women

- Hypothyroidism

- Male Hypogonadism

- Growth Hormone Deficiency

- Others

By Route of Administration

- Oral: Significant share due to convenience and patient preference

- Parenteral

- Transdermal

- Others

By Distribution Channel

- Retail Pharmacies: Leading due to accessibility and prescription fulfillment

- Hospital Pharmacies

- Online Pharmacies

- Others

Fromdata to decisions—download the research that powers leaders.

Explore More Report :

https://24lifescience.blogspot.com/2025/10/medical-dry-and-wet-separation.html

https://24lifescience.blogspot.com/2025/10/gas-chromatography-inlet-septa-market.html

https://24lifescience.blogspot.com/2025/10/professional-blood-pressure-monitor.html

https://24lifescience.blogspot.com/2025/10/oral-ursodeoxycholic-acid-market.html

https://24lifescience.blogspot.com/2025/10/chemotherapy-induced-nausea-and.html

https://24lifescience.blogspot.com/2025/10/pharmaceutical-primary-packaging-market.html

https://24lifescience.blogspot.com/2025/10/patent-drug-market-regional-analysis.html

About 24lifesciences

Founded in 2017, 24LifeScience has emerged as a trusted research and analytics partner for organizations operating within the global life sciences and chemical industries. Our core mission is to provide intelligent, future-ready insights that help clients stay ahead in an increasingly complex and innovation-driven market

International: +1(332) 2424 294 | Asia: +91 9425150513 (Asia)

Website: http://www.24lifesciences.com

Follow us on LinkedIn: http://www.linkedin.com/company/lifesciences24

Functional Flour Market Product Segmentation, Nutritional Benefits, and Consumer Adoption Analysis Report

By saloni dutta, 2025-10-10

Functional Flour Market is expanding rapidly due to diverse product segmentation, enhanced nutritional benefits, and increasing consumer adoption worldwide. Functional flours, enriched with proteins, fibers, vitamins, and other nutrients, are used in bakery products, snacks, cereals, and processed foods. Product segmentation allows manufacturers to target specific dietary needs, including gluten-free, plant-based, and fortified options. Consumer adoption is fueled by health awareness, convenience, and taste preferences. Manufacturers are leveraging nutritional benefits and targeted product offerings to attract health-conscious consumers, expand market share, and establish a strong presence across mature and emerging regions globally.

Industry Overview

The functional flour market has grown steadily due to increasing demand for nutrient-rich, health-focused food products. Consumers are seeking flours that provide additional benefits such as improved digestion, enhanced immunity, and sustained energy. Functional flours include plant-based, gluten-free, organic, and fortified varieties that cater to diverse dietary preferences. Manufacturers are investing in research and development to create innovative formulations that meet consumer needs and regulatory standards. Product segmentation combined with marketing and distribution strategies is enabling companies to expand reach and maintain competitiveness in a rapidly evolving market.

Product Segmentation

Product segmentation is a key strategy in the functional flour market. Manufacturers categorize flours based on nutritional content, application, and dietary preferences. Protein-enriched flours target fitness enthusiasts and health-conscious consumers. Fiber-rich flours support digestive health and weight management. Gluten-free and plant-based flours cater to consumers with dietary restrictions or preferences. Fortified flours with vitamins and minerals appeal to those seeking overall wellness benefits. Segmentation allows companies to design products for specific consumer segments, optimize marketing efforts, and ensure product relevance in diverse markets.

Nutritional Benefits

The nutritional benefits of functional flours drive consumer adoption and market growth. Protein-enriched flours help in muscle building, satiety, and overall wellness. Fiber-enriched flours improve digestive health, regulate blood sugar levels, and aid weight management. Fortified flours with vitamins, minerals, and antioxidants enhance immunity and support daily nutritional requirements. Plant-based flours offer alternative protein sources and cater to vegetarian and vegan diets. Highlighting these nutritional advantages through transparent labeling, educational campaigns, and marketing initiatives helps manufacturers increase consumer trust and product adoption.

Consumer Adoption Patterns

Consumer adoption patterns reflect growing awareness of health, convenience, and dietary trends. Urban populations and busy lifestyles increase the demand for ready-to-use functional flours. Health-conscious consumers prefer fortified and nutrient-enriched options that align with wellness goals. Dietary restrictions, such as gluten intolerance or vegan preferences, drive adoption of specialized flours. Social media, online reviews, and nutrition-focused content influence purchasing behavior. Companies that monitor consumer trends, gather feedback, and adapt products accordingly can improve adoption rates, strengthen brand loyalty, and maintain a competitive edge in the functional flour market.

Regional Insights

Regional variations affect product segmentation, nutritional benefits, and consumer adoption. North America and Europe lead the market with high health awareness and established food industries. Asia-Pacific is an emerging market driven by urbanization, rising disposable incomes, and increasing wellness-focused consumption. Latin America and the Middle East show growth potential through expanding bakery, snack, and convenience food sectors. Manufacturers must tailor product formulations, marketing campaigns, and distribution channels to regional preferences and regulatory requirements to maximize adoption and success across diverse markets.

Market Drivers

Several factors are driving the functional flour market. Rising health awareness encourages consumers to choose fortified, protein-rich, and fiber-enriched flours. Technological advancements in milling, fortification, and processing improve product quality and nutritional content. Urbanization and fast-paced lifestyles increase demand for convenient, ready-to-use flours. Government regulations supporting fortified foods, labeling, and quality standards enhance consumer confidence. The integration of functional flours into processed and packaged foods, particularly in bakery and snack segments, further accelerates adoption and expands market potential globally.

Challenges

Despite strong growth prospects, the functional flour market faces challenges. High production costs, limited availability of specialty ingredients, and regulatory compliance are significant obstacles. Competition from conventional flours and other functional ingredients pressures manufacturers to balance affordability and quality. Consumer skepticism regarding health claims may slow adoption in certain regions. Companies must focus on transparent communication, quality assurance, and continuous innovation to overcome these challenges and ensure sustained growth in competitive markets.

Market Outlook

The functional flour market is expected to continue growing steadily due to product segmentation, nutritional benefits, and consumer adoption trends. Manufacturers focusing on research-driven development, innovation, and targeted marketing strategies are likely to capture larger market shares. Functional flours are increasingly incorporated into home cooking, commercial baking, and processed foods, reflecting the global shift toward wellness-focused diets. By leveraging product diversity, highlighting nutritional advantages, and adapting to consumer preferences, the functional flour industry is positioned for long-term sustainable growth worldwide.

Central Laboratory Market Growth Industry Trends, Segmentation, Business Opportunities

By poojammr, 2025-10-10

The Global Central Laboratory Market is projected to grow from USD 3.84 billion in 2023 to USD 5.73 billion by 2030, at a CAGR of 5.88% during the forecast period.

Central Laboratory Market Report Overview:

The report comprehensively encompasses the analysis of insights concerning the Central Laboratory Market , including its dynamic patterns, industry landscape, and all significant aspects of the market. An in-depth examination of key players is also presented within the Central Laboratory Market report.

Request a sample report: https://www.maximizemarketresearch.com/request-sample/148522/

Central Laboratory Market Scope and Research Methodology

The aim of this report is to assess and predict the size of the Central Laboratory Market . It offers strategic profiles of significant market participants to provide an accurate depiction of the competitive landscape within the global Central Laboratory Market . This includes a comprehensive analysis of recent developments such as new product launches, acquisitions, mergers, joint ventures, brand activities, and major players in the Central Laboratory Market industry. The report presents insights into industry trends, dynamics, and potentials, assisting professionals in staying informed about the latest trends and sector performance. This insight aids in predicting growth and decline in Central Laboratory Market share over the forecast period.

In-depth understanding of the Central Laboratory Market industry was achieved through a combination of primary and secondary research methods. Various methodologies, including PESTLE, PORTER, and SWOT analysis, were employed to ensure accurate findings. SWOT analysis was employed to outline strengths, weaknesses, opportunities, and challenges for key players within the Central Laboratory Market industry. Additionally, the use of PORTER and PESTLE analysis allowed for an understanding of the microeconomic and macroeconomic factors influencing the Central Laboratory Market industry.

Central Laboratory Market Segmentation:

by Service Type

Genetic services

Biomarker services

Anatomic Pathology and Histology

Specimen management and storage

Others

by End User

Pharmaceutical companies

Biotechnology companies

Others

Get your sample report now : https://www.maximizemarketresearch.com/request-sample/148522/

Central Laboratory Market Key Players:

1. Laboratory Corporation of America Holdings (United States)

2. Medpace (United States)

3. ACM Global Central Lab (United States)

4. Frontage Labs (United States)

5. IQVIA Inc. (United States)

6. LabConnect (United States)

7. Thermo Fisher Scientific (United States)

8. MLM Medical Labs (Germany)

North America

1. Rochester Regional Health (United States)

Europe

1. Cerba Healthcare (France)

2. ICON Plc (Ireland)

3. Eurofins Scientific (Luxembourg)

4. Medicover Integrated Clinical Services (Poland)

Central Laboratory Market Regional Analysis:

The report is segmented into several key countries, with market size, growth rate, import and export of Central Laboratory Market in these countries, which covering North America, U.S., Canada, Mexico, Europe, UK, Germany, France, Spain, Italy, Rest of Europe, Asia Pacific, China, India, Japan, Australia, South Korea, ASEAN Countries, Rest of APAC, South America, Brazil, and Middle East and Africa.

Download your free sample : https://www.maximizemarketresearch.com/request-sample/148522/

Key Questions answered in the Central Laboratory Market Report are:

- Which segment grabbed the largest share in the Central Laboratory Market ?

- Which segment is expected to grow at a high rate during the forecast period?

- How is the competitive scenario of the Central Laboratory Market ?

- Which are the key factors driving the Central Laboratory Market growth?

- Which are the factors restraining the Central Laboratory Market growth?

- Which region holds the maximum share in the Central Laboratory Market ?

- What will be the CAGR of the Central Laboratory Market during the forecast period?

- Which are the prominent players in the Central Laboratory Market ?

Key Offerings:

- A detailed Analysis of the Market Overview

- Market Share, Size Forecast by Revenue | 2024−2030

- Market Dynamics – Growth Drivers, Restraints, Investment Opportunities, and Key Trends

- Market Segmentation – A detailed analysis by Route of administration, Application, Facility of use and Region and Region

- Competitive Landscape – Top Key Vendors and Other Prominent Vendors

About Maximize Market Research:

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research:

3rd Floor, Navale IT Park, Phase 2

Pune Banglore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656

📢 New Update from 24lifesciences

Tricorders are portable medical diagnostic devices that integrate multiple sensors and analytical technologies to monitor vital signs, detect diseases, and analyze biological samples. These devices utilize spectroscopy, imaging, molecular diagnostics, and AI-driven analytics to provide rapid, non-invasive health assessments. Modern tricorders can measure heart rate, blood oxygen levels, body temperature, and perform basic blood analysis, making them essential for point-of-care diagnostics and remote healthcare monitoring.

Unlock the market secrets everyone’s talking about—download now!

Market Size

The global tricorders market was valued at USD 1.84 billion in 2024 and is projected to reach USD 3.67 billion by 2032 , growing at a CAGR of 9.0% during 2025-2032.

-

United States: Significant share of global revenue

-

China: Emerging high-growth market due to increasing adoption of healthcare technology

The market expansion is supported by the rising demand for portable diagnostics, miniaturization of sensors, and rapid digitization of healthcare systems worldwide.

Market Dynamics

Growth Drivers

-

Point-of-Care Diagnostics: Rising preference for quick, on-site health assessments in hospitals and clinics

-

Technological Advancements: AI-powered analytics, portable imaging systems, and miniaturized sensors enhance device functionality

-

COVID-19 Impact: Pandemic accelerated adoption of remote monitoring and non-invasive diagnostic devices

Market Restraints

-

High Device Costs: Advanced tricorders may be expensive for small healthcare facilities

-

Regulatory Hurdles: Strict approval processes for medical devices in multiple regions

-

Data Privacy Concerns: Integration with digital health platforms requires secure handling of patient data

Opportunities

-

AI and Machine Learning Integration: Enhances diagnostic accuracy and predictive analytics

-

Mobile Health Applications: USB and wireless tricorders compatible with smartphones and tablets

-

Emerging Markets: Increasing healthcare infrastructure in Asia-Pacific and Latin America presents growth potential

Market Segmentation

By Type

-

Wireless Tricorders: Dominant segment due to portability, connectivity, and real-time data transmission

-

USB Camera Tricorders: Compatible with mobile health apps, showing strong adoption

-

Fiber Optic Camera Tricorders

-

Corded Tricorders

-

Others

By Application

-

Hospitals: Leading segment, catering to emergency care, outpatient clinics, and inpatient units

-

Clinics: Growing adoption for routine diagnostics and preventive care

-

Home Healthcare: Increasing interest due to remote monitoring needs

-

Research Laboratories

-

Others

By Technology

-

AI-Powered Tricorders: Machine learning and deep learning-based systems for advanced diagnostics

-

Basic Diagnostic Tricorders

-

Multimodal Tricorders

-

Portable Imaging Systems

-

Others

By Component

-

Sensor Modules: Largest share due to critical diagnostic function (biosensors, chemical sensors, optical sensors)

-

Display Units

-

Processing Units

-

Power Systems

-

Others

Regional Analysis

North America

-

Market Share: Largest regional market

-

Key Drivers: Advanced medical infrastructure, high healthcare spending, and rapid AI adoption

Europe

-

Growth Factors: Stringent medical device regulations, strong hospital networks, and technological investments

Asia-Pacific

-

Fastest-Growing Region: Driven by healthcare digitization, increasing awareness of point-of-care devices, and growing medical tourism

Other Regions

-

Latin America & Middle East & Africa: Emerging opportunities due to rising healthcare investments and growing telemedicine adoption

Competitor Analysis

The tricorders market features moderate competition, with key players investing in innovation, AI integration, and regional expansion.

Leading Manufacturers:

-

QuantuMDx Group (UK)

-

Ionis Pharmaceutical (U.S.)

-

Cloud DX (Canada)

-

Qualcomm Technologies (U.S.)

-

Basil Leaf Technologies (U.S.)

-

Welfo Fiber Optics (China)

-

Fujikura (Japan)

-

Basler AG (Germany)

-

Hamamatsu Photonics (Japan)

-

Scanadu (U.S.)

Key Strategies:

-

R&D in AI-powered diagnostics

-

Partnerships with hospitals and clinics for pilot programs

-

Expansion into emerging markets with localized manufacturing

Unlock the market secrets everyone’s talking about—download now!

Explore More Report :

https://24lifescience.blogspot.com/2025/10/medical-dry-and-wet-separation.html

https://24lifescience.blogspot.com/2025/10/gas-chromatography-inlet-septa-market.html

https://24lifescience.blogspot.com/2025/10/professional-blood-pressure-monitor.html

https://24lifescience.blogspot.com/2025/10/oral-ursodeoxycholic-acid-market.html

https://24lifescience.blogspot.com/2025/10/chemotherapy-induced-nausea-and.html

https://24lifescience.blogspot.com/2025/10/pharmaceutical-primary-packaging-market.html

https://24lifescience.blogspot.com/2025/10/patent-drug-market-regional-analysis.html

About 24lifesciences

Founded in 2017, 24LifeScience has emerged as a trusted research and analytics partner for organizations operating within the global life sciences and chemical industries. Our core mission is to provide intelligent, future-ready insights that help clients stay ahead in an increasingly complex and innovation-driven market

International: +1(332) 2424 294 | Asia: +91 9425150513 (Asia)

Website: http://www.24lifesciences.com

Follow us on LinkedIn: http://www.linkedin.com/company/lifesciences24

The global aquafeed market was valued at USD 67.50 billion in 2024 and is expected to expand from USD 71.28 billion in 2025 to USD 112.27 billion by 2032, registering a CAGR of 6.71% during 2025–2032. Asia Pacific remained the dominant region, accounting for 73.65% of the global share in 2024. In addition, the U.S. aquafeed market is projected to witness strong growth, reaching USD 2.85 billion by 2032, supported by the presence of leading companies such as Cargill Incorporated, Archer Daniels Midland Company, and Alltech Inc.

The COVID-19 pandemic had a significant and immediate impact on the global aquafeed industry, primarily due to supply chain disruptions and temporary production halts. While the pandemic initially led to reduced output and distribution challenges, the market is expected to regain momentum as demand and operations return to pre-pandemic levels.

The aquafeed sector experienced setbacks as restrictions on transportation and the closure of processing plants disrupted raw material sourcing. The industry, which depends heavily on marine ingredients—many imported from South America—faced delays and logistical challenges. For example, China’s reliance on Chilean fishmeal imports was affected by limited shipping and air freight availability during the pandemic.

Information Source: https://www.fortunebusinessinsights.com/industry-reports/aquafeed-market-100698

Market Dynamics

Key Drivers

The continuous rise in global seafood consumption remains a critical growth driver for the aquafeed market. According to the Food and Agriculture Organization (FAO), global seafood consumption is expected to surpass 20 kg per capita by 2030, underscoring increasing demand for aquaculture feed. Growing seafood trade volumes, coupled with advancements in aquaculture technologies, are expected to further boost demand.

Governments across emerging economies are supporting aquaculture development through subsidies and policy initiatives. For instance, the Government of India allocated USD 73.84 million under the Blue Revolution Scheme (FY 2020–21) to promote marine fishery, aquaculture, and mariculture development, thereby stimulating the adoption of high-quality feed.

Restraints

Despite positive trends, fluctuating prices of raw materials such as fishmeal, soybean, and corn can affect feed production costs and profit margins, posing challenges to market stability.

Market Segmentation

- By Type: Fish, Crustaceans, Mollusks, and Others

- By Ingredient: Soybean, Corn, Fish Oil, Fishmeal, Additives, and Others

- By Form: Dry and Wet

- By Region: North America, South America, Europe, Asia Pacific, and the Middle East & Africa

Regional Insights

Asia Pacific – Market Leader Driven by Expanding Fish Production

The Asia Pacific region continues to dominate the global aquafeed market, primarily due to high fish production levels in China and India, which together contribute over half of the region’s market value. Rising investments in aquaculture infrastructure and strong domestic demand for seafood further strengthen regional growth.

Europe – Growth Supported by Salmon Farming

Europe is anticipated to witness steady growth, fueled by advancements in aquaculture practices and increased interest in salmon farming across Norway, the U.K., and Scotland.

North America – Expanding Through Technological Advancements

In North America, the market is projected to expand at a notable pace due to the presence of major aquafeed producers, robust R&D efforts, and growing seafood exports, particularly from the U.S. and Canada.

Competitive Landscape

Innovation and Expansion Strategies Drive Competition

Leading aquafeed manufacturers are investing in product development, technological innovation, and capacity expansion to strengthen their global footprint. Strategic mergers, acquisitions, and partnerships remain key approaches to enhance market presence and distribution networks.

For example, in January 2020, BioMar A/S opened a new production facility in Wesley Vale, Tasmania, with an annual output capacity of 110,000 tonnes, significantly increasing its regional manufacturing capabilities.

Key Players in the Global Aquafeed Market

- Cargill Incorporated (Minnesota, U.S.)

- Archer Daniels Midland Company (Illinois, U.S.)

- Alltech Inc. (U.S.)

- Purina Animal Nutrition (Missouri, U.S.)

- Ridley Corp Ltd (Australia)

- Nutreco N.V. (Amersfoort, Netherlands)

- Aller Aqua A/S (Christiansfeld, Denmark)

- BioMar A/S (Denmark)

- Dibaq Aquaculture (Spain)

- Beneo GmbH (Germany)

Get Sample PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/aquafeed-market-100698

Recent Industry Development

- May 2021: BP Milling (U.K.) introduced “SmartMix,” a pelleted fish attractant blend enriched with essential vitamins, minerals, and amino acids designed to enhance immunity and promote fish health.

Report Highlights

- Comprehensive industry analysis using Porter’s Five Forces and SWOT frameworks

- Assessment of COVID-19’s impact on supply chains and production

- Detailed profiles of major industry players

- Insights into emerging trends and product developments

- Segmentation analysis by type, form, and ingredient

Market Overview

The global electrolyte drinks market size was valued at USD 36.80 billion in 2024. The market is projected to grow from USD 39.93 billion in 2025 to USD 69.14 billion by 2032, exhibiting a CAGR of 8.16% during the forecast period.

The analysis shows that increasing health awareness, a growing enthusiasm for fitness among all age groups, and rising participation in sports activities are key factors driving the market. The market is further supported by rising disposable incomes and a growing urban population seeking products to support an active lifestyle. Electrolyte drinks are formulated to restore water and essential minerals lost during physical activity or illness.

Major Players Profiled in the Market Report:

- PepsiCo Inc. (U.S.)

- Abbott Nutrition (U.S.)

- The Coca-Cola Company (U.S.)

- Unilever PLC (U.K.)

- Suntory Holdings Limited (Japan)

- PURE Sports Nutrition (New Zealand)

- NOOMA Non Acidic Beverages LLC (U.S.)

- Kill Cliff (U.S.)

- Nestlé S.A. (Switzerland)

- Kingsley Beverages (UAE)

Segments

Wide Accessibility to Drive RTD Drinks Segment Growth

Based on product type, the market is segmented into powder, RTD drinks, and tablet. The RTD drinks segment holds the largest market share due to its convenience, wide availability across retail channels, and ease of consumption for athletes and fitness enthusiasts needing quick rehydration.

Functional Benefits to Bolster Isotonic Segment Expansion

By type, the market is categorized into isotonic, hypotonic, and hypertonic. The isotonic segment leads the market as these drinks contain sugar and salt concentrations similar to the human body, allowing for rapid fluid absorption and efficient rehydration, making them ideal for active individuals.

Convenience and Portability to Drive PET Bottles Segment Growth

By packaging type, the market is segmented into PET bottles, cans/tins, and pouches/sachets. The PET bottles segment holds the largest share due to advantages like lightweight packaging, longer shelf-life, and ease of transport, making it a convenient option for both manufacturers and consumers.

Supermarket/Hypermarket to Dominate the Market Due to Wide Product Availability

Based on distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, convenience stores, and online stores. The supermarket/hypermarket segment holds the largest market share, offering consumers a wide variety of brands, sizes, and flavors in one location, often at competitive prices.

Source: https://www.fortunebusinessinsights.com/electrolyte-drinks-market-113794

Report Coverage

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- The latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints

Increasing Investment and Celebrity Endorsements to Propel Market Growth

Key drivers for the market include significant investments by manufacturers to expand production capacity and adopt new technologies to meet rising demand from millennials and Gen-Z. Additionally, leading brands are increasingly collaborating with celebrities and sports icons for promotional campaigns. These endorsements help brands connect with their target audience, enhance their image, and stand out in a competitive market.

However, the high sugar content in many traditional electrolyte drinks may restrain market growth. Growing health consciousness is leading consumers to avoid sugary beverages due to concerns about weight gain, diabetes, and dental problems. Furthermore, sugar taxes imposed by governments in countries like the U.K. can increase product prices, potentially reducing demand.

Regional Insights

Strong Presence of Key Players in North America Propels Regional Market Growth

North America dominated the market with a share of 47.53% in 2024. The region's growth is fueled by the strong presence of leading global players, high consumer awareness, and continuous investment in product innovation and marketing. The U.S. is the largest market, where consumers increasingly opt for these beverages to enhance physical endurance and stay hydrated.

Europe is the second-largest market, driven by rising health and wellness trends and increasing participation in fitness activities. Asia Pacific is projected to be the fastest-growing region, with factors like rising disposable incomes, urbanization, and government initiatives promoting healthier lifestyles boosting product demand.

Electrolyte Drinks Market Future Growth

The electrolyte drinks market is poised for significant growth, driven by innovation and evolving consumer preferences. A major trend is the shift toward healthier formulations, with manufacturers developing products that are low-sugar, zero-sugar, and free from artificial ingredients to appeal to health-conscious consumers. The market is also seeing a rise in new startups offering innovative and personalized nutrition products, which is attracting venture capital and fostering a dynamic competitive environment. This focus on health and innovation is expected to expand the market's reach and consumer base.

Competitive Landscape

Adoption of New Product Launches and Strategic Partnerships to Strengthen Market Position

The global electrolyte drinks market is fragmented, featuring key players like The Coca-Cola Company, PepsiCo Inc., and Nestlé S.A. These companies focus on launching new products with innovative flavors and health-centric claims (such as zero-added sugar and gluten-free) to meet consumer demand. Strategic collaborations, particularly with celebrities and athletes, are a common tactic to enhance brand visibility and market share in an increasingly competitive landscape.

Key Industry Development

March 2025 – PLEZi Nutrition, an emerging startup, launched a new range of hydration sports drinks in the U.S. The products, available in flavors like Tropical Punch and Lemon Lime, contain electrolytes such as potassium and sodium and are marketed with a no-added-sugar claim. The brand was launched in collaboration with NBA player Steph Curry and former U.S. First Lady Michelle Obama.

The global canned tuna market was valued at USD 28.92 billion in 2024 and is anticipated to grow from USD 29.66 billion in 2025 to USD 36.52 billion by 2032, registering a CAGR of 3.01% during the forecast period. Europe accounted for the largest share of 44.09% in 2024, solidifying its dominance in the global landscape.

Leading manufacturers operating in the market include Bolton Group, Century Pacific Foods Inc., Grupo Albacore S.A., Bumble Bee Foods LLC, Thai Union Group Inc., and several others.

The expansion of the canned tuna market is largely attributed to the rising consumption of packaged and convenience food products worldwide. Canned foods—ranging from meats and fruits to vegetables and seafood—offer consumers ready-to-eat or easy-to-prepare options, catering to fast-paced lifestyles and growing working-class populations. This shift toward convenient food solutions continues to propel global market growth.

Information Source: https://www.fortunebusinessinsights.com/canned-tuna-market-103190

Segmentation Insights

The canned tuna market is segmented by species, type, shape, preservation method, and distribution channel. Among species, Skipjack tuna leads due to its high availability, cost-effectiveness, and suitability for large-scale harvesting. By type, canned white tuna holds the largest share, attributed to its superior nutritional value—rich in omega-3 and omega-6 fatty acids, protein, and vitamin D—along with its mild flavor, tender texture, and versatility in dishes like pasta, casseroles, and salads, making it particularly popular among younger consumers. In terms of shape, the chunk segment dominates as its convenient size and appealing appearance make it ideal for use in sandwiches, wraps, and salads. Based on preservation methods, oil-based tuna products, particularly those canned in olive or sunflower oil, lead the market due to their enhanced flavor, richness, and texture. Regarding distribution channels, the retail segment continues to dominate, supported by the wide availability, affordability, and accessibility of canned tuna through supermarkets, hypermarkets, and convenience stores.

Regional Insights

Market Dynamics

Drivers – Growth of E-commerce to Accelerate Market Expansion

The rapid rise of online grocery and food delivery platforms, particularly among tech-savvy consumers, has made canned tuna more accessible. In addition, the expansion of retail infrastructure, shopping malls, and supply chain networks has supported product availability. The acceleration of e-commerce adoption during the COVID-19 pandemic further boosted sales and market penetration.

Restraints – Rising Demand for Plant-Based Alternatives

The growing popularity of plant-based seafood substitutes—which replicate the taste and texture of fish—poses a challenge to canned tuna sales, slightly restraining overall market growth.

Competitive Landscape

Leading market participants are focusing on product innovation and strategic collaborations to strengthen their portfolios and cater to evolving consumer preferences.

For instance, Thai Union Group introduced five spicy tuna flake flavors in 2020, featuring local Thai ingredients such as turmeric and lemongrass, enhancing product variety and consumer appeal.

List of Key Companies

- Thai Union Group PLC (Thailand)

- StarKist Co. (U.S.)

- A.E.C. Canning Company Limited (Thailand)

- American Tuna Inc. (U.S.)

- Bumble Bee Foods LLC (U.S.)

- Century Pacific Food Inc. (Philippines)

- Crown Prince Inc. (U.S.)

- Grupo Albacora S.A. (Spain)

- Wild Planet Foods Inc. (U.S.)

- Golden Prize Canning Co. Ltd. (Thailand)

- Ocean’s (Canada)

- Dongwon Enterprise Co., Ltd. (South Korea)

Get Sample PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/canned-tuna-market-103190

Recent Developments

- August 2024: Wild Planet Foods announced plans to launch a Wild Tuna Snack Pack in collaboration with Simple Mills and Chosen Foods, expanding its product line and retail visibility.

The global fiber cement market size was valued at USD 13.15 billion in 2023 and is projected to grow from USD 13.60 billion in 2024 to USD 18.41 billion by 2032, exhibiting a CAGR of 3.8% during the forecast period. An advanced material used in construction, fiber cement is made of cellulosic fiber, portland cement, and silica that augments elasticity and structural strength of products. The materials’ advantages over traditional cements increase their demand, propelling the growth of the market during the projected period. Fortune Business Insights presents this information in their report titled "Global Fiber Cement Market, 2025–2032."

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/107812

Segments:

Wide Availability and Cost Effectiveness Augments Portland’s Growth

By material, the market is classified into portland, silica, cellulosic, and others. Portland holds the largest fiber cement market share, owing to advantages offered such as temperature reduction of ceiling walls, cost-effective, and wide availability propels growth.

Siding Dominates Market with Several Advantages over Other Products

By application, the market is categorized into siding, roofing, cladding, molding & trimming, and others. Siding dominates the market with its robust properties that include significant tensile strength, structural flexibility, crackproof, and low maintenance cost.

Rise in Urbanization Drives Dominance of Residential Segment

By end-use, the market is bifurcated into residential and non-residential. Rapid urbanization, increasing population, and growing construction activities drive the growth of the residential segment.

Drivers and Restraints

Robust Properties of Fiber Cement Increases Demand Bolstering Market Growth

Considered as an advanced material in the construction sector, the product has witnessed prolific demand in recent years. The younger population has been observed to shift toward urban areas to experience a better lifestyle, which has surged construction activities giving rise to product demand. Growing industrialization and high demand are anticipated to upscale the fiber cement market growth.

However, strict laws regarding the use of fibrous silicate minerals and health issues associated with it are likely to limit the product’s adoption.

Regional Insights

Asia Pacific Driven by Growing Surge in Residential Projects

Asia Pacific dominates the market and held a market revenue in 2022 for USD 5.49 billion. The growth of the market can be attributed to rising population and increasing residential projects along with surge in exterior and interior designing activities.

North America to observe growth with increasing demand for fiber cement for safety and aesthetic appeal it provides to residential projects.

Competitive Landscape

Strong Regional Presence Solidifies Market Leaders Position

The market consists of large players fiercely competing to solidify their positions. Participants actively focus on innovations, acquisitions, mergers, and collaborations to increase global reach. Industry leaders maintain competitive edge with wide network for distribution, innovative product offerings, and strong presence.

Key Industry Development

- December 2023 - ETEX Group strengthened its presence in the market by acquiring BCG’s fiber cement business. The acquisition focused on maximizing the company’s revenue from the fiber cement business segment.

- November 2022- ETEX Group announced the acquisition of USRA. The acquisition aims to establish a presence in lightweight, sustainable building solutions, including plasterboard and cement.

Major Players Profiled in the Report:

- James Hardie Industries PLC (Ireland)

- ETEX Group (Belgium)

- Evonik Industries (Germany)

- Saint Gobain (France)

- CSR Limited (Australia)

- Nichiha Corporation (Japan)

- Cembrit Group A/S (Denmark)

- The Siam Cement Public Company Limited (Thailand)

- plycem corporation (Costa Rica)

- Beijing Hocreboard Building Materials Co. Ltd. (China)

Get Your Customization Research Report:

https://www.fortunebusinessinsights.com/enquiry/customization/107812

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower,

Baner - Mahalunge Road, Baner,

Pune-411045, Maharashtra, India.

Phone:

US: +18339092966

UK: +448085020280

APAC: +91 744 740 1245

Email: sales@fortunebusinessinsights.com

The global fiber cement market size was valued at USD 13.15 billion in 2023 and is projected to grow from USD 13.60 billion in 2024 to USD 18.41 billion by 2032, exhibiting a CAGR of 3.8% during the forecast period. An advanced material used in construction, fiber cement is made of cellulosic fiber, portland cement, and silica that augments elasticity and structural strength of products. The materials’ advantages over traditional cements increase their demand, propelling the growth of the market during the projected period. Fortune Business Insights presents this information in their report titled "Global Fiber Cement Market, 2025–2032."

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/107812

Segments:

Wide Availability and Cost Effectiveness Augments Portland’s Growth

By material, the market is classified into portland, silica, cellulosic, and others. Portland holds the largest fiber cement market share, owing to advantages offered such as temperature reduction of ceiling walls, cost-effective, and wide availability propels growth.

Siding Dominates Market with Several Advantages over Other Products

By application, the market is categorized into siding, roofing, cladding, molding & trimming, and others. Siding dominates the market with its robust properties that include significant tensile strength, structural flexibility, crackproof, and low maintenance cost.

Rise in Urbanization Drives Dominance of Residential Segment

By end-use, the market is bifurcated into residential and non-residential. Rapid urbanization, increasing population, and growing construction activities drive the growth of the residential segment.

Drivers and Restraints

Robust Properties of Fiber Cement Increases Demand Bolstering Market Growth

Considered as an advanced material in the construction sector, the product has witnessed prolific demand in recent years. The younger population has been observed to shift toward urban areas to experience a better lifestyle, which has surged construction activities giving rise to product demand. Growing industrialization and high demand are anticipated to upscale the fiber cement market growth.

However, strict laws regarding the use of fibrous silicate minerals and health issues associated with it are likely to limit the product’s adoption.

Regional Insights

Asia Pacific Driven by Growing Surge in Residential Projects

Asia Pacific dominates the market and held a market revenue in 2022 for USD 5.49 billion. The growth of the market can be attributed to rising population and increasing residential projects along with surge in exterior and interior designing activities.

North America to observe growth with increasing demand for fiber cement for safety and aesthetic appeal it provides to residential projects.

Competitive Landscape

Strong Regional Presence Solidifies Market Leaders Position

The market consists of large players fiercely competing to solidify their positions. Participants actively focus on innovations, acquisitions, mergers, and collaborations to increase global reach. Industry leaders maintain competitive edge with wide network for distribution, innovative product offerings, and strong presence.

Key Industry Development

- December 2023 - ETEX Group strengthened its presence in the market by acquiring BCG’s fiber cement business. The acquisition focused on maximizing the company’s revenue from the fiber cement business segment.

- November 2022- ETEX Group announced the acquisition of USRA. The acquisition aims to establish a presence in lightweight, sustainable building solutions, including plasterboard and cement.

Major Players Profiled in the Report:

- James Hardie Industries PLC (Ireland)

- ETEX Group (Belgium)

- Evonik Industries (Germany)

- Saint Gobain (France)

- CSR Limited (Australia)

- Nichiha Corporation (Japan)

- Cembrit Group A/S (Denmark)

- The Siam Cement Public Company Limited (Thailand)

- plycem corporation (Costa Rica)

- Beijing Hocreboard Building Materials Co. Ltd. (China)

Get Your Customization Research Report:

https://www.fortunebusinessinsights.com/enquiry/customization/107812

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower,

Baner - Mahalunge Road, Baner,

Pune-411045, Maharashtra, India.

Phone:

US: +18339092966

UK: +448085020280

APAC: +91 744 740 1245

Email: sales@fortunebusinessinsights.com

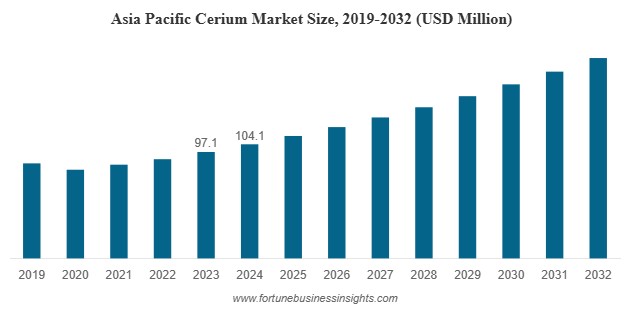

The global cerium market was valued at USD 143.9 million in 2024 and is expected to grow from USD 153.8 million in 2025 to USD 244.9 million by 2032, reflecting a CAGR of 6.9% over the forecast period. In 2024, Asia Pacific led the market, holding a 72.34% share.

This growth is primarily fueled by rising environmental concerns, technological advancements, and the growing need for cleaner and more efficient energy solutions. The widespread application of cerium oxide in catalysts, glass polishing, and fuel cells further boosts market expansion.

List Of Key Cerium Companies Profiled

- The Shepherd Chemical Company (U.S.)

- Avalon Advanced Materials (Canada)

- IREL (India)

- Canada Rare Earth Corporation (Canada)

- Lynas Corporation (Australia)

- MITSUI MINING & SMELTING CO.,LTD. (Japan)

- Vizag chemical (India)

- Star Earth Minerals (India)

- Lobachemie (India)

- Gujarat Mineral Development Corporation Ltd. (India)

- Key Market Drivers

Key Market Drivers

- Growing Demand in Automotive Catalysts

One of the most significant factors driving the cerium market is its use in automotive catalytic converters. Cerium oxide, commonly known as ceria, acts as an oxygen storage component that enhances the performance of catalysts in reducing harmful emissions such as carbon monoxide, nitrogen oxides, and hydrocarbons. As emission standards become stricter worldwide, the adoption of cerium-based catalysts continues to rise, especially in emerging economies where vehicle production is expanding rapidly.

- Expanding Use in Glass and Ceramics

Cerium oxide is widely used for polishing glass surfaces and decolorizing glass in the production of windows, mirrors, optical lenses, and electronic displays. The increasing production of smartphones, tablets, and flat-screen televisions has accelerated the demand for precision glass polishing materials, thereby creating a robust growth opportunity for the cerium market.

- Applications in Clean Energy and Nanotechnology

With the transition toward renewable and sustainable energy sources, cerium is gaining importance in fuel cells, photovoltaic systems, and energy storage applications. Cerium-based materials are being explored for use in solid oxide fuel cells, hydrogen generation, and lithium-ion batteries. In addition, cerium nanoparticles are showing great potential in catalysis, biomedical research, and environmental remediation due to their unique redox properties.

- Growth in Electronics and Phosphor Materials

Cerium compounds are essential in producing phosphors for color displays, LED lighting, and television screens. The growing demand for high-efficiency lighting solutions and advanced display technologies supports the market for cerium-based phosphor materials.

Read More : https://www.fortunebusinessinsights.com/cerium-market-112828

Market Segmentation Insights

By Type

Cerium oxide dominates the market due to its extensive use in catalysts, polishing compounds, and electronics. Other forms of cerium, such as cerium chloride and cerium nitrate, are used in niche applications like specialty coatings and laboratory reagents.

By Application

The glass and ceramics segment holds the largest market share, driven by demand from the electronics and construction industries. The catalyst segment follows closely, supported by emission control mandates. Emerging segments such as energy and nanotechnology applications are expected to grow significantly during the forecast period.

By Region

Asia Pacific remains the leading regional market, accounting for over 70% of global cerium consumption in 2024. China, being a major producer and exporter of rare earth elements, dominates global production and supply. Other key markets such as Japan, South Korea, and India are witnessing increasing usage of cerium in automotive, electronics, and energy sectors. North America and Europe are also expected to register steady growth driven by clean energy initiatives and research investments.

Challenges in the Cerium Market

Despite promising growth prospects, the cerium market faces several challenges. One of the most critical issues is supply chain dependency. A large portion of the world’s rare earth production is concentrated in China, leading to potential supply risks for other regions. Geopolitical tensions, export restrictions, or environmental policies in key producing countries can impact global availability and pricing.

Another concern is environmental sustainability. The mining and processing of rare earth elements, including cerium, involve complex extraction methods that can lead to environmental degradation if not managed responsibly. Increasing regulatory scrutiny and the push for green mining practices are encouraging companies to invest in recycling and cleaner extraction technologies.

Emerging Opportunities

- Recycling and Circular Economy Initiatives

Recycling cerium from used catalytic converters, electronic waste, and industrial residues presents a sustainable solution to reduce supply pressure. The adoption of circular economy models can help stabilize prices and promote resource efficiency.

- Diversification of Supply Sources

Countries such as Australia, India, the United States, and Canada are exploring new mining and refining projects to reduce dependence on Chinese supply. This diversification of supply sources will enhance global market stability and support long-term growth.

- Technological Advancements

Innovations in nanotechnology, catalysis, and material science are expanding the potential uses of cerium-based compounds. For example, cerium oxide nanoparticles are being studied for applications in biomedical imaging, drug delivery, and environmental purification.

- Growing Role in Renewable Energy

As the global transition toward sustainable energy accelerates, cerium’s role in hydrogen production, energy storage, and clean fuels is expected to expand significantly. Its ability to act as a redox catalyst makes it a vital component in next-generation green technologies.

Outlook

The cerium market is poised for steady growth through 2032, driven by its versatile applications in automotive catalysts, glass manufacturing, electronics, and emerging clean energy technologies. With increasing environmental regulations, rising industrialization in Asia Pacific, and growing research in nanotechnology, cerium’s importance in modern industry will continue to rise.

However, to ensure long-term sustainability, stakeholders must focus on responsible sourcing, diversification of supply chains, and recycling initiatives. As global demand for rare earth materials continues to climb, cerium will play a crucial role in supporting the world’s transition toward cleaner, smarter, and more efficient technologies.