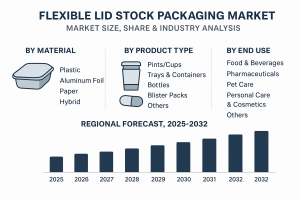

Flexible lid stock packaging refers to thin, versatile films used to seal a wide range of containers, primarily in the food, pharmaceutical, and personal care industries. These films serve as a protective barrier that maintains product freshness and extends shelf life by preventing contamination. They are typically made from materials such as aluminum foil, polyester, or laminated plastics and are heat-sealed onto containers for secure closure. Common materials include polyethylene (PE), polypropylene (PP), aluminum foil, and occasionally paper or non-woven substrates—selected for their flexibility, strength, and excellent sealing properties.

Blogs

The global fiber cement market size was valued at USD 13.15 billion in 2023 and is projected to grow from USD 13.60 billion in 2024 to USD 18.41 billion by 2032, exhibiting a CAGR of 3.8% during the forecast period. An advanced material used in construction, fiber cement is made of cellulosic fiber, portland cement, and silica that augments elasticity and structural strength of products. The materials’ advantages over traditional cements increase their demand, propelling the growth of the market during the projected period. Fortune Business Insights presents this information in their report titled "Global Fiber Cement Market, 2025–2032."

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/107812

Segments:

Wide Availability and Cost Effectiveness Augments Portland’s Growth

By material, the market is classified into portland, silica, cellulosic, and others. Portland holds the largest fiber cement market share, owing to advantages offered such as temperature reduction of ceiling walls, cost-effective, and wide availability propels growth.

Siding Dominates Market with Several Advantages over Other Products

By application, the market is categorized into siding, roofing, cladding, molding & trimming, and others. Siding dominates the market with its robust properties that include significant tensile strength, structural flexibility, crackproof, and low maintenance cost.

Rise in Urbanization Drives Dominance of Residential Segment

By end-use, the market is bifurcated into residential and non-residential. Rapid urbanization, increasing population, and growing construction activities drive the growth of the residential segment.

Drivers and Restraints

Robust Properties of Fiber Cement Increases Demand Bolstering Market Growth

Considered as an advanced material in the construction sector, the product has witnessed prolific demand in recent years. The younger population has been observed to shift toward urban areas to experience a better lifestyle, which has surged construction activities giving rise to product demand. Growing industrialization and high demand are anticipated to upscale the fiber cement market growth.

However, strict laws regarding the use of fibrous silicate minerals and health issues associated with it are likely to limit the product’s adoption.

Regional Insights

Asia Pacific Driven by Growing Surge in Residential Projects

Asia Pacific dominates the market and held a market revenue in 2022 for USD 5.49 billion. The growth of the market can be attributed to rising population and increasing residential projects along with surge in exterior and interior designing activities.

North America to observe growth with increasing demand for fiber cement for safety and aesthetic appeal it provides to residential projects.

Competitive Landscape

Strong Regional Presence Solidifies Market Leaders Position

The market consists of large players fiercely competing to solidify their positions. Participants actively focus on innovations, acquisitions, mergers, and collaborations to increase global reach. Industry leaders maintain competitive edge with wide network for distribution, innovative product offerings, and strong presence.

Key Industry Development

- December 2023 - ETEX Group strengthened its presence in the market by acquiring BCG’s fiber cement business. The acquisition focused on maximizing the company’s revenue from the fiber cement business segment.

- November 2022- ETEX Group announced the acquisition of USRA. The acquisition aims to establish a presence in lightweight, sustainable building solutions, including plasterboard and cement.

Major Players Profiled in the Report:

- James Hardie Industries PLC (Ireland)

- ETEX Group (Belgium)

- Evonik Industries (Germany)

- Saint Gobain (France)

- CSR Limited (Australia)

- Nichiha Corporation (Japan)

- Cembrit Group A/S (Denmark)

- The Siam Cement Public Company Limited (Thailand)

- plycem corporation (Costa Rica)

- Beijing Hocreboard Building Materials Co. Ltd. (China)

Get Your Customization Research Report:

https://www.fortunebusinessinsights.com/enquiry/customization/107812

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower,

Baner - Mahalunge Road, Baner,

Pune-411045, Maharashtra, India.

Phone:

US: +18339092966

UK: +448085020280

APAC: +91 744 740 1245

Email: sales@fortunebusinessinsights.com

Posted in: Packaging

| 0 comments

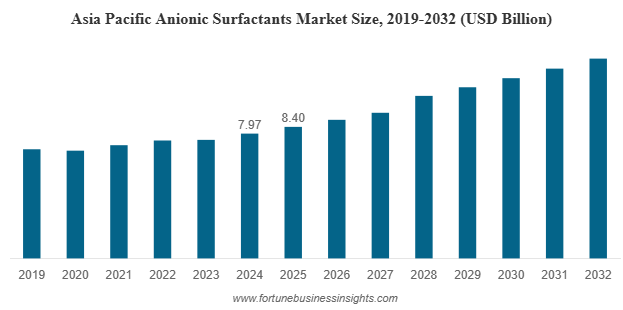

The global anionic surfactants market was valued at USD 21.33 billion in 2024 and is anticipated to rise from USD 22.43 billion in 2025 to USD 32.01 billion by 2032, registering a CAGR of 5.1% during the forecast period. Asia Pacific led the market, accounting for a 37.45% share in 2025.

List Of Key Anionic Surfactant Companies Profiled

- BASF (Germany)

- Nouryon (Netherlands)

- Clariant (Switzerland)

- Dow (S.)

- Croda International Plc (U.K)

- Stepan Company (U.S.)

- Kao Corporation. (Japan)

- Galaxy (India)

- KLK OLEO (Malaysia)

- Pilot Chemical Company (U.S.)

- Esteem Industries (India)

- NOF CORPORATION. (Japan)

Market Overview

The global anionic surfactants market is witnessing significant momentum, driven by increasing consumer awareness about hygiene, expanding demand for personal care and cleaning products, and a growing preference for sustainable and bio-based ingredients. As a crucial component in detergents, soaps, shampoos, and various industrial formulations, anionic surfactants play a vital role in modern lifestyles and industrial processes. The market is expected to continue expanding in the coming years, supported by technological innovations and environmental advancements across industries.

This robust growth trajectory is largely influenced by rising urbanization, changing consumer lifestyles, and the continuous innovation of cleaning and personal care formulations that rely heavily on surfactant technology.

Understanding Anionic Surfactants

Anionic surfactants market are surface-active agents characterized by their negatively charged hydrophilic heads. They help lower surface tension between liquids or between a liquid and a solid, making them highly effective cleansing and foaming agents. Common examples include linear alkylbenzene sulfonates (LAS), alpha olefin sulfonates (AOS), alkyl sulfates (AS), and alkyl ether sulfates (AES). These compounds are extensively used in detergents, shampoos, dishwashing liquids, and industrial cleaners.

Key Growth Drivers

- Rising Demand for Cleaning and Hygiene Products

The surge in awareness about hygiene and sanitation has significantly influenced market demand. Post-pandemic consumer behavior shows a strong inclination toward regular cleaning and disinfection, both in households and public spaces. Detergents, surface cleaners, and hand washes containing anionic surfactants have seen increased consumption across all regions.

- Expanding Personal Care Industry

The booming cosmetics and personal care sector, particularly in Asia Pacific and North America, is another major growth catalyst. Anionic surfactants are essential for producing foaming and emulsifying effects in shampoos, face washes, and body cleansers. Their ability to efficiently remove oil and dirt while creating a rich lather makes them a preferred choice among formulators.

- Industrial and Institutional Applications

Beyond consumer goods, industries such as textiles, agriculture, construction, and oilfield chemicals increasingly use anionic surfactants. They serve as emulsifiers, dispersing agents, and wetting agents in numerous formulations. With industrialization on the rise in developing economies, this segment will continue to support market expansion.

- Innovation Toward Eco-Friendly Alternatives

Growing environmental concerns are encouraging manufacturers to develop biodegradable, renewable, and plant-based surfactants. Companies are investing in research to replace petrochemical-derived surfactants with sustainable alternatives derived from natural oils, fatty acids, and sugars. This shift not only reduces environmental impact but also aligns with consumer demand for “green” and safe products.

Read More : https://www.fortunebusinessinsights.com/anionic-surfactants-market-113516

Market Challenges

Despite their benefits, traditional anionic surfactants face certain limitations. Some synthetic surfactants are known to cause skin irritation and dryness with prolonged exposure. Additionally, non-biodegradable formulations can lead to environmental issues such as aquatic toxicity and soil contamination. Stringent government regulations on chemical usage, especially in developed markets, are compelling manufacturers to enhance product safety and sustainability. Overcoming these challenges through innovation and eco-certification will be crucial for long-term market growth.

Market Segmentation

By Type

The market is segmented into alpha olefin sulfonates (AOS), linear alkylbenzene sulfonates (LAS), lignosulfonates, alkyl ether sulfates (AES), alkyl sulfates (AS), and others. Among these, alpha olefin sulfonates hold a leading share due to their superior biodegradability, excellent foaming properties, and compatibility with diverse formulations.

By Application

Key application areas include household cleaning, personal care, agriculture, textiles, and construction. The household cleaning segment dominates the global market, fueled by the increasing use of detergents, dishwashing products, and multipurpose cleaners. The personal care segment is also witnessing rapid growth, driven by rising demand for premium skin and hair care products.

By Region

The Asia Pacific region remains the largest market for anionic surfactants, accounting for over one-third of global revenue in 2025. High population density, industrial growth, and increased spending on hygiene and personal care in countries such as China, India, and Japan are propelling regional demand. North America and Europe follow closely, with strong emphasis on innovation, eco-friendly formulations, and brand diversification. Meanwhile, emerging economies in Latin America and the Middle East & Africa offer new opportunities for market expansion due to rising consumer awareness and improving economic conditions.

Recent Industry Developments

- Manufacturers are increasing production of alpha olefin sulfonates to meet rising demand from detergent and personal care industries.

- New eco-friendly surfactants derived from natural oils such as coconut and palm are gaining traction in the market.

- Companies are adopting advanced formulation technologies to improve the performance, mildness, and biodegradability of surfactant-based products.

Key Industry Developments

- January 2025: The Planet Chemical Company announced the expansion of its anionic surfactant production capacity at its Middletown, Ohio, manufacturing site. The expansion will help the company to double its alpha olefin sulfonate production and to supply it to the household, industrial and institutional, and personal care markets. The expansion project started in January 2025 and will be completed by 2027.

- June 2023: BASF announced that it has expanded its production capacity for bio-based alkyl polyglucosides in Asia Pacific and North America. The expansion will help the company to strengthen its position and serve customers even faster and more flexibly from the regional supply points.

Future Outlook

Looking ahead, the global anionic surfactants market is poised for continued growth, supported by evolving consumer preferences, sustainability initiatives, and expanding industrial applications. The shift toward biodegradable and bio-based surfactants is expected to reshape the industry landscape. Innovations in formulation science and raw material sourcing will play a pivotal role in balancing performance, safety, and environmental responsibility.

The anionic surfactants market is on a steady growth path, projected to reach USD 32.01 billion by 2032. The demand for hygiene, personal care, and eco-friendly products will remain the primary driving forces. Companies that successfully blend technological innovation with sustainability will gain a competitive edge in this evolving market. As the world moves toward greener chemistry and responsible consumption, anionic surfactants will continue to play an indispensable role in shaping a cleaner and more sustainable future.

Posted in: Chemicals & Advanced Materials

| 0 comments

Market Overview

The global Italian food market size was valued at USD 24.03 billion in 2024. The market is projected to grow from USD 25.52 billion in 2025 to USD 40.77 billion by 2032, exhibiting a CAGR of 6.92% during the forecast period.

The analysis deep-dives into these insights in its latest research report, titled “Italian Food Market, 2025-2032.”

The analysis shows that the surging trend of quick meals and the increasing availability of authentic Italian items contribute to the market’s growing potential. Known for their simplicity and use of fresh ingredients, Italian dishes such as pasta and pizza have gained global popularity, which is further amplified by increasing immigration and the cuisine's adaptability to various dietary needs.

Major Players Profiled in the Market Report:

- Nestlé S.A. (Switzerland)

- Barilla Group (Italy)

- General Mills, Inc. (U.S.)

- McCormick & Company, Inc. (U.S.)

- B&G Foods (U.S.)

- Conagra Brands, Inc. (U.S.)

- Del Monte Foods Private Limited (India)

- MTR Foods Pvt. Ltd. (India)

- Rich Products Corporation (U.S.)

- Dr. Oetker (Germany)

Segments

High Popularity and Consumption to Drive Non-Vegetarian Segment Growth

Based on food type, the market is segmented into vegetarian and non-vegetarian. The non-vegetarian segment holds the largest market share, valued for its high consumption rates and nutritional benefits, including high-quality protein and essential vitamins.

Wide Usage and Functional Advantages to Bolster Wheat Segment Expansion

By raw material, the market is categorized into wheat and gluten-free. The wheat segment leads the market, as wheat (particularly durum wheat) contains gluten, which provides essential texture, elasticity, and shape retention during cooking.

Supermarket/Hypermarket to Dominate the Market Due to Wide Product Availability

Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, grocery stores, and online retail. The supermarket/hypermarket segment holds the largest market share due to the wide availability of international and local brands, bulk purchasing options, and discounted prices.

Source: https://www.fortunebusinessinsights.com/italian-food-market-113792

Report Coverage

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- The latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints

Increasing Global Appeal of Italian Products to Propel Market Growth

The rising global appeal of Italian products is a pivotal driver strengthening the market's momentum. Dishes like pasta, pizza, and lasagna have become staples in numerous countries due to their reliance on fresh, accessible ingredients and their adaptability to various dietary needs. The spread of the cuisine through immigration has further solidified its worldwide popularity.

However, health concerns associated with certain Italian foods, such as the extensive use of high-fat cheese and sauces, may impede market growth. Additionally, fluctuating prices of key raw ingredients like wheat, yeast, and cheese can impact manufacturing costs and profitability.

Regional Insights

Demand for Convenient Meals in Asia Pacific Propels Regional Market Growth

Asia Pacific dominated the market with a share of 51.35% in 2024 and is the leading region globally. Growth is fueled by consumers seeking easy-to-prepare meal options like pizza and pasta amidst increasingly hectic lifestyles and rising participation of women in the workforce.

Europe ranks as the second-largest market, with growth supported by deep-rooted culinary traditions. A strong health and wellness trend is also driving demand for organic, gluten-free, and fiber-enriched Italian products.

Italian Food Market Future Growth

The Italian food market is set for significant growth, driven by technological advancements and evolving consumer trends. The adoption of advanced technologies in production, such as automated lines and AI-powered systems, is creating opportunities for enhanced consistency and efficiency. Furthermore, the growing inclination toward culinary tourism is a major trend, with an increasing number of travelers seeking to explore local cultures through authentic food. This focus on gastronomic experiences is propelling the demand for high-quality and traditional Italian products worldwide.

Competitive Landscape

Adoption of New Product Launches and Partnerships to Strengthen Market Position

The market features prominent players like Nestlé S.A., General Mills, Inc., and Barilla Group. These leading companies are focused on expanding their market share by launching new products that cater to evolving consumer demands. Additionally, firms are entering strategic partnerships and collaborations to strengthen their brand presence and expand their market reach.

Key Industry Development

May 2025 – Nestlé S.A., a Swiss-based food conglomerate, unveiled a new frozen pizza, "Wood Fired Style Crust Pizza," through its DiGorno brand. This item is available in various options, including Supreme Speciale, Four Cheese, and Premium Pepperoni, across the U.S.

Posted in: Italian Food Market

| 0 comments

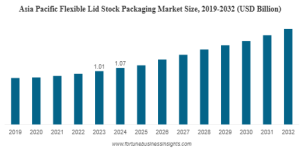

According to Fortune Business Insights, The global Flexible Lid Stock Packaging Market is witnessing strong growth, driven by increasing demand for convenient, lightweight, and sustainable packaging solutions across the food, beverage, and healthcare sectors. According to Fortune Business Insights, the market was valued at USD 2.59 billion in 2024 and is projected to grow from USD 2.74 billion in 2025 to USD 4.09 billion by 2032, exhibiting a CAGR of 6.05% during the forecast period (2025–2032).

Flexible lid stock packaging plays a crucial role in preserving product freshness, extending shelf life, and ensuring tamper-evident sealing — all of which are essential in modern packaging applications.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/flexible-lid-stock-packaging-market-109395

Key Market Drivers

1. Rising Demand in Food & Beverage Sector

The growing consumption of packaged and ready-to-eat foods is one of the primary factors driving market growth. Flexible lid stock packaging provides excellent sealing and barrier properties against oxygen and moisture, making it ideal for packaging dairy products, beverages, and frozen foods.

2. Increasing Adoption of Sustainable Packaging

Manufacturers are focusing on recyclable and eco-friendly materials to align with global sustainability goals. The transition toward mono-material lid stocks and recyclable laminates is enhancing the market’s growth potential.

3. Expansion in Pharmaceutical and Healthcare Applications

Flexible lid stock packaging is gaining popularity in the pharmaceutical industry due to its superior sealing performance, light protection, and contamination resistance — particularly in blister packs and sterile medical packaging.

4. Technological Advancements in Packaging Materials

Innovations in film technologies, barrier coatings, and printing techniques are improving the performance and aesthetics of flexible lid stock packaging, helping brands stand out in competitive retail environments.

Market Segmentation

By Material Type

Plastic (PE, PET, PP, etc.) – Dominates the market due to cost-effectiveness, durability, and versatility.

Aluminum Foil – Preferred for high-barrier applications in food and pharma packaging.

Paper and Others – Growing steadily with the rise of sustainable and recyclable options.

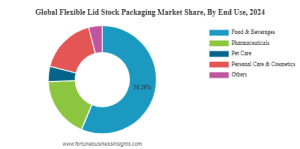

By Application

Food & Beverage – Largest segment, driven by the packaging needs of dairy products, ready meals, and snacks.

Pharmaceuticals – Increasing adoption in blister packs and medical trays.

Personal Care & Others – Expanding use in cosmetic containers and hygiene product packaging.

By Region

Asia Pacific dominated the global market with a 41.02% share in 2024 , attributed to high consumption of packaged foods, growing retail infrastructure, and rising disposable incomes in countries like China and India.

North America and Europe continue to see steady growth, supported by innovation and stringent environmental regulations encouraging recyclable packaging solutions.

Latin America and the Middle East & Africa are emerging as high-potential markets due to expanding food processing and pharmaceutical industries.

List of Key Flexible Lid Stock Packaging Companies Profiled

- Tekni-Plex, Inc. (U.S.)

- Huhtamaki (Finland)

- Constantia Flexible (Austria)

- Sealed Air (U.S.)

- Mas Flexible (Turkey)

- Berry Global (U.S.)

- Amcor plc (Switzerland)

- Elite Packaging (U.S.)

- Safepack (India)

- DuPont (U.S.)

- Wipak (Canada)

- KM Packaging Services Ltd. (U.K.)

These companies are focusing on product innovation, sustainability-driven packaging solutions, and regional expansion to strengthen their global presence.

Recent Industry Developments

Leading packaging manufacturers are investing in recyclable and bio-based lid stock materials to meet growing consumer demand for eco-friendly packaging.

Collaborations and acquisitions are increasing across the sector to enhance technological capabilities and expand product portfolios.

Automation and digital printing technologies are being integrated to improve production efficiency and customization in packaging.

Information Source: https://www.fortunebusinessinsights.com/flexible-lid-stock-packaging-market-109395

The Flexible Lid Stock Packaging Market is expected to continue its robust growth through 2032, driven by sustainability trends, material innovations, and expansion of packaged food and pharmaceutical industries. The push for recyclable and lightweight packaging will create new opportunities for manufacturers, while the Asia Pacific region remains the most promising market for future investments.

KEY INDUSTRY DEVELOPMENTS

- In July 2025, Greiner Packaging launched Click On and Click In sealing lids, which are mono-material packaging solutions aimed at improving sustainability and convenience by removing the necessity for aluminum foil while guaranteeing resealability and recyclability for a range of products. Sealing lids operate on a two-component principle: a cup and a lid. This enables the intentional exclusion of a third component such as aluminum foil. The benefit is that both elements can be constructed from the same material, such as PP, PET, or r-PET.

Posted in: Business

| 0 comments

The global physical vapor deposition market size is expected to experience considerable growth by reaching USD 40.97 billion by 2028 while exhibiting a CAGR of 8.2% between 2021 and 2028. This information is published by Fortune Business Insights in its report, titled “ Physical Vapor Deposition Market, 2025-2032.” The report further mentions that the market stood at USD 22.43 billion in 2020. Factors such as the increasing demand for eco-friendly coating processes and the growing demand for medical equipment amid the COVID-19 crisis are expected to propel the product’s demand in the forthcoming years.

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/physical-vapour-deposition-pvd-market-102364

List of the Companies Profiled in the Market:

- Advanced Energy Industries, Inc. (USA)

- Intevac (USA)

- Oerlikon Balzers (Switzerland)

- Impact Coatings AB (Sweden)

- AJA International, Inc. (USA)

- Dynavac (USA)

- Denton Vacuum (USA)

- Angstrom Engineering, Inc. (Canada)

- CHA Industries, Inc. (USA)

- IHI HAUZER Techno Coating B V (The Netherlands)

- The Kurt J Lesker Company (USA)

- Other Key Players

Market Segmentation

By Category Analysis:

The global physical vapor deposition (PVD) market is segmented into equipment, materials, and services. The equipment segment, comprising thin film deposition devices for thermal evaporation, sputtering, and arc vapor deposition, dominates the market. These are widely used in industries such as solar, microelectronics, data storage, and medical. Asia-Pacific is expected to witness the fastest growth, driven by the rising demand for high-performance coatings offering superior thickness, uniformity, and adhesion.

By Application Analysis:

The microelectronics segment held the largest share in 2023, accounting for over one-third of the market. PVD is extensively used in device fabrication and plating seed layers, providing hard, uniform, and temperature-resistant coatings that enhance microelectronics performance. Rapid industrialization in China, India, Japan, the U.S., Germany, and Brazil supports segment growth.

DRIVING FACTORS

Increasing Demand for Eco-friendly Coating Processes to Promote Growth

According to Eurostat, the industrial sector accounts for more than half of the total emissions in Europe. The rising concern over greenhouse emissions has propelled the demand for environmentally safe products. For instance, the physical vapor deposition process adopts eco-friendly products such as titanium nitride (TiN) and chromium nitride (CrN). These materials are coated on corrosion-resistant electroplating and further enhance the finish of the surface. In addition, they offer superior performance without the risk of environmental hazards. Therefore, owing to this, the high demand for eco-friendly coating processes across several industrial applications is expected to favor the growth of the market during the forecast period.

REGIONAL INSIGHTS

Asia-Pacific – The region stood at USD 10.25 billion in 2020 and is expected to hold the highest position in the market during the forecast period. This is owing to the increasing consumption of medical equipment and solar products in countries such as China. Besides, the presence of eminent physical vapor deposition solution providers will favor regional growth during the forecast period.

North America – The region is expected to experience significant growth owing to the well-established supply chain network and distributorship in the region. Moreover, the increasing adoption of the physical vapor deposition process in the manufacturing of solar panels and cutting tools will boost the growth of the market between 2021 and 2028.

COMPETITIVE LANDSCAPE

Major Companies Focus on Investment in R&D Activities to Brighten Their Market Prospects

The market comprises small, medium, and large companies that are striving to maintain a stronghold. The companies are investing in R&D activities to develop advanced physical vapor deposition solutions to cater to the growing demand from several industrial applications. Moreover, other key players are adopting organic and inorganic growth strategies that are likely to bode well for market growth.

Industry Development:

- April 2022: Impact Coatings established a subsidiary in Shanghai, China, to increase the availability of coating solutions and services in the country.

- February 2021 : Dynavac announced a significant increase in capital investment, facility size, and workforce. The company focuses on competitive advantage based on growth in both the thin film and space simulation markets. These investments will allow them to keep up with the needs of their customers.

Speak to Our Expert:

https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/physical-vapour-deposition-pvd-market-102364

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower,

Baner - Mahalunge Road, Baner,

Pune-411045, Maharashtra, India.

Phone:

US :+1 424 253 0390

UK : +44 2071 939123

APAC : +91 744 740 1245

Posted in: Chemical and Materials

| 0 comments

Pod Vapes Market Global Forecast Report Examines Key Market Segments and Demand Patterns

By Apeksha More, 2025-10-10

Pod Vapes Market represents a vital segment of the electronic cigarette industry, providing convenient, portable, and customizable nicotine delivery solutions. The global forecast report examines key market segments, demand patterns, and emerging opportunities. Growth is driven by advanced device designs, flavor diversity, sustainability initiatives, and regional expansion strategies. Consumer behavior, regulatory developments, and competitive dynamics further shape adoption rates and market growth. Understanding these trends enables companies and stakeholders to optimize strategies, make informed investment decisions, and capitalize on long-term opportunities within the global pod vapes market.

Overview of Market Segments

The pod vapes market is segmented based on device type, flavor preference, and distribution channel. Device types include disposable, refillable, and smart pods. Disposable pods dominate due to convenience and affordability, while refillable pods appeal to environmentally conscious and cost-aware consumers. Smart pods with app-based personalization, usage tracking, and connectivity features attract tech-savvy users. Flavor segmentation includes tobacco, menthol, fruit, dessert, and beverage-inspired options, catering to diverse consumer preferences. Distribution channels range from retail outlets and specialty vape shops to online and e-commerce platforms. Understanding these segments helps companies develop targeted products and marketing strategies.

Consumer Demand Patterns

Consumer demand patterns vary across demographics and regions. Millennials, urban professionals, and health-conscious users prioritize convenience, portability, and aesthetics. Disposable pods attract consumers seeking simplicity, while refillable and premium systems appeal to environmentally aware users. Flavor variety, design, and customizable options significantly influence purchase decisions. Social media, influencer marketing, and online reviews drive awareness and adoption, particularly among younger demographics. Companies that analyze consumer demand patterns can develop tailored products, marketing campaigns, and distribution strategies, ensuring sustained adoption and revenue growth across key market segments.

Technological Innovations

Technological innovation is a major driver of market growth. Improved battery performance, enhanced heating systems, and leak-proof pod designs improve reliability and user experience. Nicotine salt formulations allow smoother inhalation and faster satisfaction. Smart pods with digital connectivity provide personalized settings and usage tracking, enhancing engagement for tech-savvy consumers. Refillable and eco-friendly designs address sustainability concerns and appeal to environmentally conscious users. Continuous innovation in technology ensures product differentiation, attracts new consumers, and strengthens loyalty among existing users, contributing to long-term market growth and adoption.

Regional Market Analysis

Regional dynamics significantly influence growth prospects and demand patterns. North America remains a mature market with high consumer awareness, advanced retail networks, and clear regulatory frameworks. Europe shows steady adoption, supported by harmonized regulations and harm-reduction strategies. Asia-Pacific, led by China, Japan, and South Korea, is expanding rapidly due to rising disposable incomes, urbanization, and changing lifestyle preferences. Latin America and the Middle East are emerging regions with growing interest influenced by cultural perceptions and regulatory developments. Tailoring product offerings and marketing to regional preferences ensures optimal market penetration and revenue generation.

Competitive Landscape

The pod vapes market is highly competitive, with multinational corporations, regional brands, and startups striving for market share. Leading companies invest heavily in research and development, marketing, and distribution to maintain a competitive edge. Strategic collaborations between device manufacturers and e-liquid producers enhance product offerings and customer experience. Mergers and acquisitions expand geographic reach and strengthen technological capabilities. Startups differentiate through innovative designs, unique flavors, and cost-effective solutions. Online platforms, e-commerce channels, and social media marketing improve visibility and accessibility. Companies integrating innovation, strategic partnerships, and effective marketing achieve sustainable growth and profitability.

Regulatory Impact

Regulatory frameworks influence adoption, growth, and demand patterns. Countries impose regulations on nicotine content, flavor restrictions, labeling, and marketing. Some regions promote vaping as a harm-reduction strategy, while others maintain strict regulations to safeguard public health. Compliance is essential for market access, consumer trust, and brand reputation. Companies invest in regulatory monitoring, quality assurance, and advocacy for evidence-based policies. Harmonized regulations facilitate market entry, reduce compliance costs, and support predictable growth, allowing stakeholders to plan long-term strategies and investments effectively.

Sustainability Trends

Sustainability has become a critical factor shaping consumer adoption and product development. Refillable pods, recyclable materials, and eco-friendly packaging appeal to environmentally conscious consumers. Responsible disposal education enhances corporate responsibility and strengthens brand perception. Integrating sustainability with innovation attracts socially aware users and investors. Eco-friendly initiatives support premium pricing and differentiate brands in a competitive market. Sustainability, combined with technological innovation and design, enhances adoption, drives consumer loyalty, and influences future growth patterns in the global pod vapes industry.

Investment Opportunities

The pod vapes market offers substantial opportunities for investment and growth. Smart pods, premium devices, refillable systems, and flavor innovation attract new consumers and increase adoption rates. Expansion into emerging regions provides untapped revenue potential. Strategic partnerships, collaborations, and mergers facilitate technology acquisition, distribution expansion, and market consolidation. Companies prioritizing innovation, regulatory compliance, and sustainability are well-positioned to maximize returns and long-term growth. Investment in online marketing, e-commerce, and social media campaigns enhances visibility, consumer engagement, and market share across key segments.

Future Outlook

The global pod vapes market is expected to sustain robust growth driven by innovation, consumer adoption, and regional expansion. Smart devices, refillable systems, and customizable flavors will shape next-generation products. Emerging consumer groups, including wellness-focused and female users, present additional growth opportunities. Regional expansion, strategic partnerships, and investment in innovation will influence competitive dynamics. Companies aligning product development, marketing, regulatory compliance, and sustainability initiatives are positioned for sustained growth, market leadership, and long-term profitability in the evolving pod vapes industry.

Conclusion

The pod vapes market demonstrates strong growth potential, shaped by technological innovation, consumer demand, and regional dynamics. Analysis of key market segments and demand patterns provides valuable insights for companies seeking strategic opportunities. Flavor diversity, smart devices, sustainability initiatives, and regional expansion are driving adoption and revenue growth. Competitive strategies, regulatory compliance, and targeted investments enhance market positioning. Companies integrating innovation, consumer insights, and sustainable practices are well-positioned for long-term success. With continued focus on technology, adoption, and global expansion, the pod vapes market is set for sustainable growth and global impact.

#PodVapesMarket #GlobalForecast #MarketSegments #ConsumerTrends #Innovation #SustainableVaping #FlavorInnovation #MarketGrowth #CompetitiveStrategy #VapingIndustry

Posted in: other

| 0 comments

Fruit Puree Market packaging technologies driving sustainability and improving supply chain efficiency globally

By saloni dutta, 2025-10-10

Fruit Puree Market is experiencing transformation as advanced packaging technologies enhance sustainability, maintain product quality, and optimize supply chain efficiency. Modern packaging solutions help preserve freshness, extend shelf life, and reduce environmental impact. Companies are adopting biodegradable materials, flexible pouches, and smart packaging with freshness indicators to meet consumer demand for eco-friendly, convenient, and high-quality fruit puree products. By integrating innovative packaging with sustainable supply chain practices, manufacturers improve operational efficiency, reduce waste, and strengthen their position in competitive global markets.

Aseptic Packaging Extending Shelf Life

Aseptic packaging plays a key role in preserving fruit puree freshness while minimizing the need for refrigeration. By sterilizing both the puree and the container, it prevents microbial contamination and maintains flavor, color, and nutritional value. This technology allows products to be stored for extended periods and shipped over long distances without compromising quality. Aseptic packaging reduces waste and spoilage, improving overall supply chain efficiency while supporting global distribution and market expansion.

Flexible Pouches for Convenience and Sustainability

Flexible pouches are gaining popularity due to their lightweight design, portability, and reduced environmental footprint compared to rigid containers. These pouches cater to on-the-go consumption, particularly in baby food, smoothies, and snack products. Resealable closures maintain freshness after opening, increasing usability. Flexible packaging also optimizes warehouse and transportation space, reducing costs and carbon emissions. By combining convenience and sustainability, flexible pouches meet modern consumer expectations and support efficient supply chain operations.

Biodegradable and Recyclable Packaging Materials

Sustainability-driven packaging solutions are increasingly used in the fruit puree market. Biodegradable plastics, paper-based cartons, and compostable films replace conventional plastics, reducing environmental impact. These eco-friendly materials appeal to environmentally conscious consumers while meeting regional regulations on packaging waste. Companies integrating sustainable packaging practices gain competitive advantages, strengthen brand reputation, and contribute to global environmental goals, aligning production and distribution with consumer and regulatory expectations.

Smart Packaging Enhancing Product Monitoring

Smart packaging technologies help improve product quality and supply chain efficiency. QR codes, freshness indicators, and temperature sensors allow real-time monitoring of fruit puree during storage and transport. These tools provide transparency, build consumer trust, and reduce losses due to spoilage or mishandling. Digital monitoring also aids manufacturers in optimizing logistics, inventory management, and distribution routes, ensuring products reach consumers in optimal condition while minimizing operational inefficiencies.

Regional Trends in Packaging Adoption

Packaging innovations are adopted differently across regions depending on consumer preferences, regulations, and production capacities. Europe emphasizes eco-friendly materials and traceable packaging due to strict environmental laws and environmentally conscious consumers. North America focuses on convenience and on-the-go formats combined with sustainability. Asia-Pacific is rapidly adopting flexible packaging to support urban lifestyles and reduce costs, while Latin America emphasizes packaging that enables long-distance transport of tropical fruits. Understanding regional dynamics allows manufacturers to optimize packaging strategies and enhance market penetration.

Packaging’s Role in Brand Differentiation

Packaging serves as a critical factor in brand differentiation and consumer appeal. Eye-catching designs, ergonomic shapes, and informative labeling attract attention and communicate product quality. Highlighting sustainability, nutritional benefits, and functional advantages on packaging resonates with health-conscious and eco-conscious buyers. Effective packaging not only preserves product integrity but also reinforces brand identity and encourages customer loyalty, enhancing competitiveness in both domestic and international markets.

Integration with Supply Chain Efficiency

Innovative packaging directly contributes to improved supply chain efficiency. Lightweight, stackable, and protective packaging reduces shipping costs, minimizes damage, and optimizes storage space. Aseptic and smart packaging technologies ensure products remain safe and fresh during transport, supporting longer distribution networks. Packaging innovations combined with digital monitoring and logistics optimization strengthen overall operational performance, reduce waste, and enable global market expansion.

Future Outlook: Sustainable, Smart, and Efficient Packaging

The future of fruit puree packaging lies in combining sustainability, technology, and operational efficiency. Biodegradable materials, flexible formats, and smart monitoring solutions will become standard. Packaging will not only protect product quality but also support environmental responsibility, convenience, and supply chain optimization. Manufacturers that adopt innovative packaging strategies will enhance consumer satisfaction, reduce environmental impact, and maintain competitive advantage in the global fruit puree market.

Posted in: default

| 0 comments

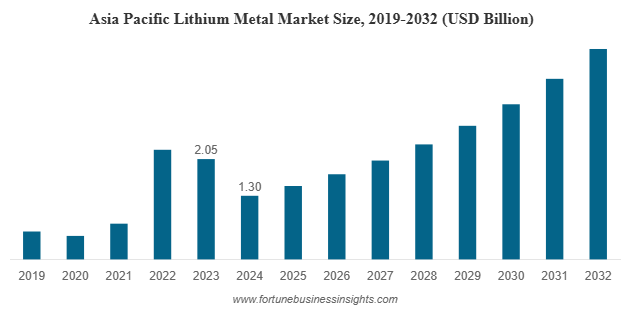

The global lithium metal market was valued at USD 2.21 billion in 2024 and is anticipated to rise from USD 2.55 billion in 2025 to reach USD 7.25 billion by 2032, registering a strong CAGR of 16.0% during the forecast period. Asia Pacific emerged as the leading region, accounting for 58.82% of the market share in 2024.

List Of Key Lithium Metal Companies Profiled

- Ganfeng Lithium Group Co. Ltd. (China)

- Techtone Inorganic Co., Ltd. (China)

- Chengxin Lithium Group Co., Ltd. (China)

- Rio Tinto (U.K.)

- CNNC Jianzhong Nuclear Fuel Co., Ltd. (China)

- Albemarle Corporation (U.S.)

- Li-Metal Corp. (Canada)

- Tianqi Lithium Inc. (China)

- ATT Advanced Elemental Materials Co., Ltd. (U.S.)

- Merck KGaA (Germany)

Market Overview

Lithium metal market is an essential component in next-generation battery technologies, particularly solid-state and lithium-sulfur batteries. These advanced systems offer higher energy density, faster charging, and improved safety compared to traditional lithium-ion batteries. The growing need for efficient energy storage across multiple sectors — from electric mobility to renewable energy integration — has positioned lithium metal as one of the most strategic materials of the decade.

The Asia Pacific region dominated the global market in 2024, accounting for over 58.82% share. Countries like China, Japan, and South Korea continue to lead due to strong investments in EV manufacturing, battery innovation, and local production capacities. Europe and North America are also emerging as significant players, supported by growing clean energy initiatives and strategic collaborations among automakers and battery suppliers.

Market Segmentation

By Form

- Ingot: This segment dominates the market, as lithium ingots are widely used in battery production and alloy manufacturing due to their high purity and uniformity.

- Powder: Lithium powder is gaining popularity in niche applications, including additive manufacturing, chemical synthesis, and compact battery designs.

- Others: Various customized forms of lithium metal cater to research and specialized industrial applications.

By Application

- Batteries: The battery segment leads the global market, driven by rising adoption of solid-state and lithium-sulfur batteries that rely heavily on lithium metal anodes. These batteries promise longer life cycles and higher efficiency for EVs and portable devices.

- Alloys: Lithium metal is also used in aluminum-lithium and magnesium-lithium alloys, offering lightweight strength for aerospace, defense, and automotive sectors.

- Others: Additional uses include electronics, pharmaceutical synthesis, and specialty chemicals.

Key Growth Drivers

- Electric Vehicle Expansion

The surge in global EV production remains the strongest growth catalyst. Lithium metal’s ability to store more energy per unit weight makes it ideal for high-performance batteries that extend vehicle range and reduce charging times. As governments worldwide push for zero-emission mobility, the demand for lithium metal is expected to grow rapidly.

- Rising Renewable Energy Integration

As solar and wind power adoption increases, so does the need for reliable energy storage systems. Lithium metal batteries provide the stability and energy density required for grid-level storage, supporting renewable energy continuity even during fluctuations in generation.

- Advances in Battery Technology

Ongoing research in solid-state batteries and lithium-sulfur batteries is reshaping the energy storage landscape. Lithium metal anodes are central to these innovations, offering up to twice the energy density of conventional lithium-ion systems. These technological breakthroughs are expected to open new growth avenues in both mobility and stationary storage sectors.

- Supportive Policies and Investments

Governments across regions are implementing favorable policies and subsidies for domestic battery manufacturing and raw material sourcing. Major automakers and energy firms are forming joint ventures with lithium producers to secure long-term supply chains, strengthening overall market growth.

Read More : https://www.fortunebusinessinsights.com/lithium-metal-market-113413

Challenges and Restraints

Despite its potential, the lithium metal market faces several obstacles. The high cost and volatility of raw materials continue to impact profitability for producers. Moreover, lithium extraction and purification are resource-intensive, involving significant water consumption and environmental considerations.

Limited global production capacity and supply chain constraints add another layer of challenge, particularly as demand outpaces current output. Furthermore, emerging alternative technologies such as sodium-ion and advanced solid-state chemistries could pose competition in certain applications if they achieve commercial scalability at lower costs.

Emerging Opportunities

The next wave of growth is likely to come from technological advancements in extraction and processing. Innovations such as direct lithium extraction (DLE) and recycling from used batteries could significantly reduce production costs and environmental impact.

Vertical integration is another major trend reshaping the industry. Leading producers are expanding across the value chain — from mining to refining and battery production — to secure raw material availability and enhance supply reliability.

Additionally, aerospace and defense sectors are increasingly adopting lithium-based alloys for lightweight structural components, offering steady niche demand outside the energy domain.

Competitive Landscape

The companies are investing heavily in R&D and capacity expansion to strengthen their foothold. Strategic acquisitions and partnerships are shaping the competitive environment. For example, large corporations are acquiring smaller lithium metal producers to expand production capabilities and secure access to patented technologies.

Key Industry Developments

- March 2025: Rio Tinto completed its USD 6.7 billion acquisition of Arcadium Lithium, positioning itself as a global leader in the supply of energy transition materials and significantly expanding its lithium portfolio to support the growing demand for clean energy solutions.

- August 2024: Arcadium Lithium acquired Li-Metal Corp.’s lithium metal business for USD 11 million in an all-cash deal. This acquisition included intellectual property, patents, and a pilot production facility in Ontario, Canada. This acquisition aimed to enhance Arcadium’s capabilities in producing lithium metal from various grades of lithium carbonate feedstock.

Future Outlook

Looking ahead, the lithium metal market is expected to continue its strong upward trajectory through 2032. The convergence of sustainability goals, EV adoption, and advancements in energy storage technology will create an ecosystem where lithium metal becomes a cornerstone material for the global energy transition.

As the world shifts toward a greener future, lithium metal’s high energy efficiency, lightweight nature, and adaptability across applications will ensure its critical role in shaping tomorrow’s clean energy economy. With ongoing technological progress and increasing investments, the market is set to enter an era of rapid expansion, positioning lithium metal as a key enabler of the next generation of batteries and energy systems.

Posted in: Chemicals & Advanced Materials

| 0 comments

Disposable Caesarean Surgical Pack Market 2025-2032 | Regional Analysis, Demand Trends & Competitive Outlook

By lifesciencesid, 2025-10-10

New Update from 24lifesciences

Disposable Caesarean Surgical Packs are pre-sterilized, single-use medical kits that contain all essential instruments and materials required for Caesarean section procedures. Typically, these packs include surgical drapes, gowns, gloves, sponges, scalpel blades, umbilical clamps, and other necessary tools. Designed to maintain strict aseptic conditions, these packs standardize surgical processes, improve operational efficiency, and reduce the risk of hospital-acquired infections.

Get free sample of this report at : https://www.24lifesciences.com/download-sample/2765/disposable-caesarean-surgical-pack-market-market

Market Size

The global disposable Caesarean surgical pack market was valued at USD 145 million in 2024 and is projected to reach USD 179 million by 2031 , growing at a CAGR of 3.1% .

Historical CAGR (2019-2024): 2.8%

Projected CAGR (2024-2031): 3.1%

The market growth is primarily driven by increasing global C-section rates, enhanced hospital infection control protocols, and expanding healthcare infrastructure in emerging economies.

Market Dynamics

Growth Drivers

- Rising C-section Rates: Currently, over 21% of global births are via C-section, with some regions exceeding 50%, boosting demand for pre-assembled surgical kits.

- Infection Control Regulations: Strict hospital protocols encourage the adoption of disposable products to reduce cross-contamination.

- Healthcare Infrastructure Development: Emerging economies are investing in advanced surgical facilities, increasing demand for standardized surgical packs.

Market Restraints

- Environmental Concerns: Single-use plastics and medical waste disposal pose sustainability challenges.

- Cost Sensitivity: Price constraints, particularly in public healthcare systems, may limit adoption.

- Reusable Alternatives: Sterilizable surgical kits in certain regions provide competition.

Opportunities

- Sustainable Materials: Development of biodegradable and bio-based surgical pack components.

- Smart Packaging: RFID and QR code tracking for authentication and inventory management.

- Anti-Microbial Innovations: New packs incorporating antimicrobial coatings to enhance safety.

Market Segmentation

By Type

- Standard Procedure Pack: Dominates the market with 68% share , widely used in routine C-sections for cost efficiency and operational standardization.

- Custom Procedure Pack: Growing at 4.2% CAGR , tailored for specific hospital protocols or patient needs, popular in specialized surgical centers.

By Application

- Hospitals: Lead the market with 62% share , handling the largest volume of obstetric surgeries.

- Ambulatory Surgical Centers: Fastest-growing segment with 5.3% CAGR , reflecting the shift to outpatient care.

- Clinics and Other Facilities: Show steady adoption, offering cost-efficient same-day procedures.

Regional Analysis

North America

- Market Share: 38% (largest regional market)

- Key Drivers: High healthcare spending, stringent infection control, advanced medical infrastructure

- United States: Accounts for 89% of the regional market ( USD 62 million )

Europe

- Market Share: 28%

- Key Markets: Germany, France, UK, Italy ( USD 38 million combined )

- Growth Rate: 2.8% CAGR, driven by EU medical device regulations and hospital upgrades

Asia-Pacific

- Fastest-Growing Region: 4.8% projected CAGR

- Key Markets: China, India, Japan, Australia ( 75% of regional revenue )

- Drivers: Expanding healthcare access, rising medical tourism, increasing C-section rates

Competitive Landscape

The market is moderately fragmented with the top 5 players holding 48% market share . Key strategies include:

- Product Innovation: 6-8% of revenue invested in R&D for advanced materials and designs

- Regional Expansion: Focus on emerging markets with local manufacturing

- Mergers & Acquisitions: 12 major transactions recorded in 2023-2024

Key Players Include:

- Medline Industries

- Cardinal Health

- Owens & Minor

- Molnlycke

- Lohmann & Rauscher

- Paul Hartmann

- Unisurge

- PrionTex

- Pennine Healthcare

- Rocialle

- Lantian Medical

- Anhui MedPurest Medical Technology

- Boen Healthcare

Technology and Innovation Trends

- Smart Packaging: Integration of RFID and QR codes for inventory and tracking

- Sustainable Materials: Development of eco-friendly, biodegradable pack components

- Anti-Microbial Coatings: Adoption of advanced antimicrobial technologies in 40% of new products

Future Outlook and Recommendations

The market shows strong, stable growth with particular opportunity in:

- Emerging Markets: Asia, Africa, and Latin America will account for 75% of new growth

- Specialized Products: Custom packs for complex cases offer higher margins

- Sustainability Initiatives: Environmentally friendly materials represent the next innovation frontier

Recommendations include:

- Invest in scalable manufacturing with regional presence

- Focus on value-added products rather than price competition

- Develop sustainable solutions to meet future regulations

- Forge partnerships with local healthcare providers and distributors

Get free sample of this report at : https://www.24lifesciences.com/download-sample/2765/disposable-caesarean-surgical-pack-market-market

About 24lifesciences

Founded in 2017, 24LifeScience has emerged as a trusted research and analytics partner for organizations operating within the global life sciences and chemical industries. Our core mission is to provide intelligent, future-ready insights that help clients stay ahead in an increasingly complex and innovation-driven market

International: +1(332) 2424 294 | Asia: +91 9425150513 (Asia)

Website: http://www.24lifesciences.com

Follow us on LinkedIn: http://www.linkedin.com/company/lifesciences24

Posted in: news

| 0 comments

Texting strangers online can lead to exciting conversations, new friendships, or valuable networking opportunities. But it can also go wrong—quickly—if you’re not careful. Whether you're messaging someone through social media, a dating app, or a professional platform, the way you communicate matters. Here are eight common mistakes to avoid when you text strangers online.

1. Starting Without Context

Jumping into a conversation with a vague “Hey” or “Hi” can feel confusing or intrusive. Always provide a brief introduction and explain why you're reaching out.

Better approach: “Hi, I’m Adeel. I saw your post in the photography group and wanted to ask about your camera setup.”

Why it matters: Context builds trust and makes your message feel intentional.

2. Oversharing Personal Information

Sharing sensitive details like your full name, address, phone number, or workplace too early can put your privacy at risk. Keep things general until you’ve built trust.

Avoid:

-

Home address

-

Financial details

-

Personal photos

Why it matters: Protecting your privacy is essential when texting strangers online.

3. Using Generic or Boring Openers

Messages like “What’s up?” or “Hey there” often get ignored. Instead, lead with something specific, playful, or thoughtful.

Better options:

-

“What’s the most interesting thing you’ve read this week?”

-

“I saw your comment about hiking—any favorite trails?”

Why it matters: Creative openers spark curiosity and invite engagement.

4. Ignoring Tone and Timing

Texting late at night or during work hours can feel intrusive. Also, tone matters—avoid sarcasm, passive-aggressive remarks, or overly formal language unless appropriate.

Tips:

-

Match the recipient’s tone

-

Text during reasonable hours

-

Avoid emotionally charged language

Why it matters: Respecting tone and timing shows emotional intelligence.

5. Being Too Personal Too Soon

Jumping into deep or sensitive topics early in the conversation can make strangers uncomfortable. Build rapport gradually before discussing personal matters.

Avoid early topics like:

-

Relationship history

-

Family issues

-

Political or religious debates

Why it matters: Starting light helps establish comfort and safety.

6. Not Respecting Boundaries

If someone doesn’t respond right away, don’t double-text or ask why. Give space and let the conversation evolve naturally.

Better approach: “Just wanted to follow up—no rush at all, reply when it’s convenient.”

Why it matters: Respecting boundaries builds trust and prevents discomfort.

7. Downloading or Clicking Unknown Links

Never download files or click links from strangers unless you’re sure they’re safe. This can expose you to malware, scams, or phishing attempts.

Avoid:

-

Suspicious links

-

Unknown attachments

-

Requests to install apps or software

Why it matters: Digital safety is crucial when chatting with unfamiliar contacts.

8. Forgetting to Exit Gracefully

If the conversation stalls or feels off, end it politely. A respectful exit leaves a good impression and keeps the door open for future interaction.

Examples:

-

“It’s been great chatting—hope we can connect again soon.”

-

“Thanks for the info! I’ll reach out if I have more questions.”

Why it matters: Ending on a positive note shows maturity and respect.

Final Thoughts

Text strangers online can be rewarding when done thoughtfully. By avoiding these eight common mistakes—starting without context, oversharing, using generic openers, ignoring tone, getting too personal, disrespecting boundaries, clicking unknown links, and forgetting to exit gracefully—you’ll create a safer, more engaging experience for both sides.

Posted in: default

| 0 comments