Satin and Lace Prom Dress Market Report: Key Takeaways & Strategic Insights

By Industry Outlook, 2025-09-09

The satin and lace prom dress market has emerged as a dynamic segment of the global formalwear and fashion industry, fueled by rising demand for elegant, breathable, and luxurious attire. According to the latest industry analysis, the global satin and lace prom dress market size was valued at USD 4.24 billion in 2024 and is projected to grow from USD 4.45 billion in 2025 to USD 6.55 billion by 2032, showcasing a CAGR of 5.66%.

As social media, celebrity endorsements, and event culture continue to influence consumer choices, satin and lace-based prom dresses remain at the forefront of youth and women’s fashion. This blog explores the Satin and Lace Prom Dress Market Share, Growth, Trends, and Outlook for 2025–2032.

Request FREE Sample PDF Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/satin-and-lace-prom-dress-market-113032

Satin and Lace Prom Dress Market Size & Share

In 2024, North America dominated the Satin and Lace Prom Dress Market Share with 33.49%, thanks to high consumer spending on formal events, a strong prom culture, and a wide network of specialty boutiques. The United States remains the largest single market, driven by educational institutions, wedding culture, and fashion-forward consumers inspired by celebrity red-carpet appearances.

Globally, long prom dresses accounted for the largest share in 2024, particularly popular for weddings and educational formal events. Ball gowns led the style segment, maintaining their timeless appeal among teenagers and young women. Meanwhile, specialty stores and brand shops commanded the highest market share due to personalized services and rental options, while online channels emerged as the fastest-growing distribution segment.

Satin and Lace Prom Dress Market Growth Drivers

- Rising Popularity of Prom and Formal Events

- Increased spending on educational institution celebrations and cultural gatherings is fueling demand for satin and lace dresses.

- Instagram, TikTok, and celebrity endorsements are accelerating consumer interest in glamorous satin and lace gowns.

- Growing adoption of recycled satin fabrics and eco-friendly lace designs aligns with global sustainability trends, creating fresh growth opportunities.

- Consumers increasingly prefer personalized necklines, embellishments, and hybrid designs that merge traditional elegance with contemporary fashion.

Satin and Lace Prom Dress Market Trends

The Satin and Lace Prom Dress Market Trends highlight the industry’s evolution toward innovation, inclusivity, and sustainability:

- Blended Modern & Classic Designs: Open-back criss-cross styles, delicate straps, and metallic finishes are gaining traction alongside traditional ball gowns.

- Slip Dresses & Beaded Necklines: Minimalist satin slip dresses paired with opulent beadwork are trending as statement pieces.

- Cultural Fusion: In Asia-Pacific markets like India and China, Western-inspired gowns are blending with local cultural preferences.

- E-Commerce Growth: Online platforms are expanding rapidly, making it easier for consumers to access a wide variety of prom dress styles globally.

Regional Insights

- North America: Holds the largest market share, supported by strong prom traditions and high event-related spending. The region generated USD 1.42 billion in 2024.

- Europe: Celebrity-endorsed ball gowns and social media-driven fashion trends are fueling demand in the U.K., Spain, and Italy.

- Asia-Pacific: Expected to grow at the fastest rate during 2025–2032, with China and India driving demand through e-commerce and cultural hybrid fashion choices.

- South America: Brazil and Colombia are witnessing strong demand due to rising disposable income and formalwear spending.

- Middle East & Africa: Wedding-centric cultures in UAE and South Africa, combined with boutique expansion, are fueling market adoption.

Satin and Lace Prom Dress Market Restraints

While the outlook is positive, the Satin and Lace Prom Dress Market Growth faces challenges:

- High Costs: Satin and lace dresses are expensive due to premium materials and production costs.

- Seasonal Demand: Sales heavily depend on prom and wedding seasons, creating fluctuations in revenues.

Satin and Lace Prom Dress Market Opportunities

The market presents exciting opportunities, especially through sustainability and technology:

- Recycled Satin Dresses: Increasing demand for eco-friendly fashion supports the adoption of recycled fabrics.

- Digital Retail Growth: Expanding e-commerce channels enable wider global reach and customized shopping experiences.

- Emerging Economies: Countries in Asia-Pacific, South America, and Africa offer untapped potential due to growing disposable incomes and fashion-conscious youth populations.

Get Full Summary: https://www.fortunebusinessinsights.com/satin-and-lace-prom-dress-market-113032

Competitive Landscape

The Satin and Lace Prom Dress Market Analysis reveals a highly competitive environment with global and regional players introducing new designs, collections, and collaborations.

Key players include:

- Adrianna Papell (U.S.)

- Carolina Herrera (U.S.)

- Rosa Clara (Spain)

- Pronovias (Spain)

- Jovani (U.S.)

- Oscar De La Renta (U.S.)

- Monique Lhuillier (U.S.)

- Marchesa (U.S.)

Recent developments highlight new product launches, strategic collaborations, and prom dress donation campaigns aimed at strengthening market presence and social responsibility. For example, in 2025, Jovani unveiled a collection featuring metallic fabrics, statement corsets, and backless designs, while Windsor Fashions donated 1,500 dresses through Becca’s Closet.

Satin and Lace Prom Dress Market Outlook 2025–2032

Looking ahead, the Satin and Lace Prom Dress Market Outlook is strongly positive, with steady growth forecasted across regions. The industry will be shaped by sustainable innovation, digital retail, and consumer preference for personalized fashion.

With a projected value of USD 6.55 billion by 2032, the market is expected to remain a key part of the global apparel industry, appealing to fashion-forward consumers and prom-goers worldwide.

Final Thoughts

The Satin and Lace Prom Dress Market Analysis shows that this niche segment is thriving due to cultural trends, event-driven demand, and the timeless elegance of satin and lace fabrics. While challenges such as high costs remain, innovations in design and sustainability promise significant future opportunities.

For brands, retailers, and investors, staying ahead of the Satin and Lace Prom Dress Market Trends will be crucial in capturing growth and strengthening their Satin and Lace Prom Dress Market Share in the coming years.

Writing Instrument Market 2025 Trends Reshaping the Stationery Industry

By Industry Outlook, 2025-09-09

The global writing instrument market continues to thrive despite rapid digital transformation. From pens and pencils to highlighters and colouring instruments, writing tools remain indispensable for education, professional use, and creative expression. According to recent estimates, the writing instrument market size was valued at USD 45.36 billion in 2024 and is expected to grow from USD 47.64 billion in 2025 to USD 69.84 billion by 2032, exhibiting a healthy CAGR of 5.62% during the forecast period.

This growth highlights the resilience and evolving nature of the industry, supported by rising literacy rates, expanding educational institutions, and consumer demand for eco-friendly, sustainable stationery products. Let’s dive into the writing instrument market analysis 2025 to understand its size, share, growth drivers, restraints, and trends shaping its future outlook.

Request FREE Sample PDF Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/writing-instrument-market-113154

Writing Instrument Market Size & Share

- 2024 Market Size: USD 45.36 billion

- 2025 Market Size: USD 47.64 billion

- 2032 Forecast Size: USD 69.84 billion

- CAGR (2025–2032): 5.62%

In 2024, Asia Pacific dominated the writing instrument market share, accounting for 39.77% of global revenue. This dominance is attributed to strong education systems, government reforms, and high student enrolment in countries like India and China.

By type, pens remain the largest segment, driven by their universal functionality across academic, office, and personal use. Meanwhile, colouring instruments are projected to record the fastest growth, fueled by increasing interest in art education and creative learning.

From a distribution perspective, stationery stores currently lead due to consumer preference for in-person product assessment, but online channels are witnessing the fastest growth thanks to digital retail penetration, customization, and accessibility.

Writing Instrument Market Growth Drivers

- Educational Expansion

The global rise in school enrolments and new educational institutions directly fuels demand for pens, pencils, and markers. For instance, India’s school enrolment reached 265 million in FY22, reflecting a surge in demand for bulk stationery procurement. - Government Investments

Many countries are prioritizing literacy and education. Initiatives like India’s QHEI program and Rwanda’s literacy programs ensure consistent demand for affordable and premium writing tools. - Technological Advancements in Stationery

Companies such as Faber-Castell, Mitsubishi Pencil Co., and BIC are developing ergonomic designs, sustainable materials, and high-performance inks, enhancing both functionality and aesthetics.

Market Restraints

Despite positive growth, the writing instrument market outlook faces challenges due to:

- Digital Substitutes: Increasing use of laptops, tablets, and smartphones in education and workplaces reduces reliance on traditional stationery.

- Smart Learning Adoption: Schools are integrating digital writing tools, styluses, and smart pens, which may limit physical product demand in certain markets.

Writing Instrument Market Opportunities

- E-commerce Expansion : Online retail has unlocked global accessibility, driving sales across both mature and underserved markets. According to the India Brand Equity Foundation, India’s e-commerce market reached a GMV of USD 60 billion in FY 2023, highlighting the scale of digital opportunities.

- Personalization & Gifting : Custom engraved pens, limited editions, and luxury writing tools are witnessing higher adoption, especially in corporate gifting and premium consumer segments.

Writing Instrument Market Trends

1. Sustainable Stationery on the Rise

Environmental consciousness is reshaping consumer choices. Manufacturers are innovating with biodegradable materials, recycled plastics, and seed-based pens. Notable developments include:

- May 2024 – NOTE launched the world’s first fully biodegradable pen, crafted from newspaper and non-toxic ink.

- April 2023 – EkoPak introduced paper-based pens with plantable seeds.

2. Growth of Colouring Instruments

Art education, creative learning, and hobbies like calligraphy and journaling are fueling the demand for colouring markers, crayons, and pastels. This segment is expected to record the fastest CAGR in the coming years.

3. Luxury & Premium Writing Tools

In regions like North America and Europe, luxury writing instruments are in demand for executive gifts and branding purposes. German brands such as Schneider and STAEDTLER emphasize craftsmanship, sustainability, and eco-label certifications like Blue Angel.

Read Full Report Summary: https://www.fortunebusinessinsights.com/writing-instrument-market-113154

Regional Writing Instrument Market Outlook

- Asia Pacific : Leading market with USD 18.04 billion in 2024, fueled by robust educational infrastructures and literacy initiatives in China, India, and South Korea.

- North America : Strong demand for premium and luxury pens, supported by hybrid work culture and gifting trends.

- Europe : Rising adoption of eco-friendly writing products and a cultural preference for traditional handwriting.

- South America : Increasing disposable incomes in Brazil and Argentina boost consumption of premium tools.

- Middle East & Africa : Literacy-focused initiatives in Uganda, Rwanda, and Angola expand demand for basic pens and pencils.

Competitive Landscape

The writing instrument market analysis 2025 identifies key players focusing on innovation, sustainability, and premiumization.

Leading companies include:

- BIC Corporate (France)

- Faber-Castell AG (Germany)

- Mitsubishi Pencil Co., Ltd. (Japan)

- Pilot Corporation (Japan)

- STAEDTLER Mars GmbH & Co. KG (Germany)

- Newell Brands, Inc. (U.S.)

- Shanghai M&G Stationery Inc. (China)

- Kokuyo Camlin Limited (India)

- Luxor Writing Instruments Pvt. Ltd. (India)

- Linc Pen & Plastics Ltd. (India)

Noteworthy launches include ITC Classmate’s Hook Ball Pen (2023) and Makoba’s luxury pen boutique in India (2022), showcasing how companies are innovating across mass-market and premium segments.

Conclusion

The writing instrument market growth trajectory is promising, with sustainability, e-commerce expansion, and premium product demand shaping its future. While digital alternatives pose challenges, the tactile, cultural, and functional relevance of writing tools ensures continued growth.

As the industry evolves, the writing instrument market outlook reflects a balance between tradition and innovation—where eco-friendly products, digital integration, and luxury positioning will define market opportunities.

For businesses and investors, staying aligned with writing instrument market trends—from sustainable innovations to e-commerce strategies—will be key to capturing market share in this growing USD 69.84 billion industry by 2032.

The global appetite for food experiences is reshaping the travel industry. Culinary tourism—also known as gastronomy or food tourism—has emerged as one of the fastest-growing segments of global tourism, blending cultural exploration with authentic dining.

According to Fortune Business Insights , the global culinary tourism market size was valued at USD 1,009 million in 2024 . It is projected to expand from USD 1,174.27 million in 2025 to USD 3,766.67 million by 2032 , at a robust CAGR of 18.12%. Europe dominated the market in 2024 with a 33.93% market share, reflecting the region’s rich gastronomic heritage.

So, what’s fueling this market growth? Let’s explore the key drivers, restraints, opportunities, and trends that are shaping the future of culinary tourism.

Request FREE sample PDF Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/culinary-tourism-market-113603

Why Culinary Tourism Is Booming

1. The Desire for Authentic Local Experiences

Travelers are increasingly prioritizing meaningful experiences over traditional sightseeing. Food offers one of the most immersive ways to connect with local culture, history, and traditions. Sampling regional dishes, joining cooking classes, or attending food festivals allows tourists to engage directly with communities. According to the World Food Travel Organization (WFTO), travelers spend nearly 25% of their trip budget on food and beverages, underlining the centrality of cuisine in travel decisions.

2. The Power of Social Media and Digital Influence

Food has become one of the most shared experiences on platforms like Instagram, TikTok, and YouTube. Stunning visuals of local delicacies, combined with storytelling by influencers and chefs, have turned food into a major travel motivator. Social media trends are now shaping destination choices, inspiring travelers to visit cities and villages famous for their culinary traditions.

3. Rising Disposable Incomes and International Travel

As middle-class populations expand globally, more people are allocating budgets for unique travel experiences. Culinary tourism has benefited from this trend, as food-focused trips often blend luxury dining with affordable street food adventures, catering to a wide range of budgets.

Market Challenges

Despite the growth potential, the culinary tourism industry faces hurdles:

- Poor Infrastructure in Rural Areas: Many authentic culinary experiences are located in remote destinations with weak transport links and limited accommodation.

- Food Safety Regulations: Small, local food providers often struggle to meet international food safety standards, which can hinder growth.

- Supply Chain Disruptions: Geopolitical uncertainties and fluctuating food prices impact consistency and profitability.

These issues, if not addressed, may limit the accessibility of authentic experiences for global travelers.

Opportunities Ahead

1. Health and Wellness Integration

As health-conscious lifestyles rise, travelers are seeking culinary experiences that align with wellness goals. From farm-to-table dining to detox retreats and cooking classes focused on organic, plant-based meals, destinations that emphasize holistic nourishment stand to benefit.

2. Sustainability and Eco-Food Tourism

Eco-friendly travel is influencing dining choices. Zero-waste events, carbon-neutral restaurants, and farm visits are growing in popularity. This trend not only enriches the traveler’s experience but also supports local farmers and preserves culinary heritage.

Culinary Tourism Market Segmentation

By Type

- Restaurants dominate the market due to accessibility and structured experiences.

- Culinary Trails are the fastest-growing, offering immersive tours through local farms, wineries, and artisanal food hubs.

By Tourist Type

- Domestic Tourism leads, as locals explore food within their own countries.

- International Tourism is expanding rapidly, fueled by cultural curiosity, rising disposable incomes, and government-backed food tourism campaigns.

By Age Group

- Generation X holds the largest market share, thanks to financial stability and a preference for quality experiences.

- Millennials (Gen Y) are the fastest-growing segment, driven by digital engagement and a love for authentic, Instagram-worthy experiences.

By Booking Mode

- Online Travel Agents (OTAs) dominate, offering convenience, price transparency, and instant bookings.

- Direct Bookings are set to grow the fastest, supported by operators’ adoption of apps, optimized websites, and social media promotions.

Get More Info: https://www.fortunebusinessinsights.com/culinary-tourism-market-113603

Regional Insights

- Europe : The global leader, offering diverse food traditions—from French fine dining to Italian pasta culture and Spanish tapas. Its strong wine tourism scene boosts its culinary appeal.

- North America : Experiences like farm-to-table dining, wine tastings, and food festivals are major growth drivers. The U.S. is a hotspot with events like the Aspen Food & Wine Classic.

- Asia Pacific : Expected to grow the fastest, fueled by its rich culinary diversity, affordable street food, and government-led gastronomy campaigns (e.g., Amazing Thailand Gastronomy Tourism ).

- South America : Rising global recognition of cuisines from Peru, Brazil, and Argentina, along with coffee and wine tourism, is boosting growth.

- Middle East & Africa : A growing mix of traditional food and emerging culinary experiences presents steady growth opportunities.

Competitive Landscape

The market is highly competitive, with players focusing on authentic, local, and hyper-curated experiences. Leading companies include:

- Abercrombie & Kent USA, LLC (S.)

- Greaves Travel Ltd (K.)

- India Food Tour (India)

- Classic Journeys, LLC (U.S.)

- The FTC4Lobe Group (U.S.)

- The Travel Corporation (U.K.)

- Gourmet on Tour (U.K.)

- INTERNATIONAL CULINARY TOURS (Argentina)

- Culinary Tours (India)

- Butterfield & Robinson Inc. (Canada)

Recent developments include farm-to-table culinary tours in Southeast Asia (2024) and exclusive Italian food tours by Abercrombie & Kent (2023). Partnerships with local farmers and tourism boards are becoming a key differentiator.

The culinary tourism market is on a strong upward trajectory, blending culture, tradition, and gastronomy into unforgettable travel experiences. With digital platforms driving awareness, wellness and sustainability shaping preferences, and a growing appetite for authentic cultural immersion, the industry is poised for remarkable growth through 2032.

As food continues to be a universal language, culinary tourism will remain one of the most flavorful ways to experience the world.

Kitchen Knife Market Forecast: How Online Channels Are Transforming Sales

By Industry Outlook, 2025-09-08

The kitchen knife is more than just a culinary tool—it’s the heart of every kitchen. Whether it’s a chef at a Michelin-starred restaurant or a home cook experimenting with new recipes, the right knife can transform the cooking experience. As culinary culture continues to evolve worldwide, the global kitchen knife market is carving a promising growth trajectory.

According to Fortune Business Insights recent research, the market size was valued at USD 2,003.71 million in 2024 and is projected to expand from USD 2,112.51 million in 2025 to a remarkable USD 4,017.20 million by 2035, at a CAGR of 6.64%. The U.S. led the market in 2024, holding a 21.46% market share, driven by strong consumer spending on premium kitchenware and artisanal cutlery.

Request FREE Sample PDF Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/kitchen-knife-market-103865

Market Dynamics

Drivers: Innovation Meets Culinary Demand

The surge in the HoReCa sector (Hotels, Restaurants, and Cafés) is a significant growth driver. Professional kitchens demand innovative chef knives that deliver precision, sharpness, and durability. With more restaurants, cafés, and cloud kitchens opening globally, chef knives, santoku knives, and utility knives are increasingly essential.

On the household side, rising numbers of culinary enthusiasts and home cooks are embracing knives designed for paring, mincing, and bread cutting. Cooking shows, food vlogs, and social media recipes have further boosted consumer interest in versatile knife collections.

Opportunities: High-Tech and Ceramic Knives

Recent years have seen a reinvention of ceramic knives. Companies like Kyocera are pioneering patented technologies, blending zirconia and alumina nanoscale particles for sharper, more durable blades. These knives are particularly popular in commercial kitchens for their edge retention and precision cutting.

Luxury knives with innovative materials are also gaining traction as giftable tableware products, a trend that has picked up during festive seasons and culinary tourism.

Restraints and Challenges

However, the market faces challenges from alternative kitchen tools such as food processors, slicers, and electric choppers. These products, with their convenience and multifunctionality, sometimes overshadow traditional knives.

Additionally, rising material costs for steel, brass, and bronze, as well as expenses related to knife manufacturing and blade maintenance, add financial pressure on manufacturers. Consumers’ growing preference for knife-sharpening services also reduces repeat purchases of new knives, posing another hurdle.

Segmentation Analysis

By Product

- Cook’s Knife dominates the segment, thanks to its versatility for slicing, chopping, and dicing.

- Utility Knives are growing in popularity among home cooks, influenced by cooking shows and the need for multipurpose tools.

- Paring Knives are becoming essential for delicate kitchen tasks, while Bread Knives are riding the wave of artisanal bread-making trends.

- Cleavers and Boning Knives serve commercial kitchens and meat-processing centers, ensuring steady demand.

- The “Others” category (santoku, carving, steak knives, etc.) reflects rising interest in diverse culinary tools worldwide.

By Application

- Commercial Segment leads the market, fueled by HoReCa expansion and cloud kitchens.

- Household Segment is expected to grow fastest, supported by rising home ownership, cookbook subscriptions, and the popularity of gourmet cooking at home.

By Price

- Premium Knives dominate due to demand from professional chefs and hotels for high-quality stainless steel and carbon steel products.

- Affordable Knives remain popular among new home cooks and in developing economies, where mass production ensures accessibility.

By Sales Channel

- Online Stores are the fastest-growing channel, supported by direct-to-consumer brands and dropshipping portals.

- Hypermarkets & Supermarkets remain strong with bulk sales and discounts.

- Others (restaurant supply stores, brand outlets) hold steady importance in the commercial sector.

Regional Outlook

- U.S.: Leads the market with artisanal and premium knife demand, alongside innovations in vibration and sensor-based knives.

- Canada: Growth fueled by high homeownership rates and sustainable kitchen solutions.

- Germany: Strong hospitality industry and dining tourism drive professional knife sales.

- China: Robust manufacturing hub with significant domestic consumption of innovative blade designs.

- Japan: Famous for Gyuto, Nakiri, and Santoku knives, catering to both households and professional chefs.

- Rest of the World: Rising eco-conscious demand in markets like the U.K., India, Australia, and Saudi Arabia favors knives made of recycled steel and sustainable materials.

Get More Info: https://www.fortunebusinessinsights.com/kitchen-knife-market-103865

Competitive Landscape

The market is moderately consolidated, with top players holding 33.11% share in 2024. Key names include:

- Groupe SEB (France)

- Zwilling J. A. Henckels AG (Germany)

- WÜSTHOF (Germany)

- Victorinox International (Switzerland)

- Yoshida Metal Industry Co. Ltd. (Japan)

- MAC Corporation (Japan)

- Kai Corporation (Japan)

- Tupperware Brands Corporation (U.S.)

- Marquee Brands (U.S.)

- Mauviel1830 (France)

- Klein Tools (U.S.)

These companies continue to expand globally through product innovation and strategic retail presence. For instance, Victorinox has opened new stores in India, while Yoshida’s brand Global launched the GLOBAL CAMP Black Series in Japan in 2024.

Recent launches like Butterfork’s Purest Series (2025) and Stahl’s Talon Collection (2024) reflect the growing emphasis on premium, performance-driven knives for both chefs and home cooks.

Trends to Watch

- Gift-Giving Culture: Artisanal knives are becoming popular as luxury gifts for food enthusiasts.

- Sustainable Materials: Demand for eco-friendly knives made from recycled steel, bamboo, or organic materials is rising.

- Colorful and Decorative Designs: Bright blade finishes and unique aesthetics are trending in restaurants and home kitchens alike.

- Culinary Tourism: Growing interest in destination food culture boosts premium knife sales.

The kitchen knife market is on a sharp upward path, fueled by innovations, lifestyle changes, and the growing global food culture. While challenges like high production costs and competition from alternative tools remain, opportunities in ceramic technologies, premium gifting trends, and online retail expansion make the market highly attractive for investors and manufacturers.

As kitchens worldwide evolve, the humble kitchen knife is no longer just a tool—it’s a statement of craftsmanship, culture, and culinary exploration.

The smart furniture industry is entering an exciting growth phase, blending design, technology, and functionality to redefine modern living and working spaces. According to the Fortune Business Insights latest study, the global smart furniture market size was valued at USD 837.91 million in 2024 and is projected to reach USD 2,730.69 million by 2032, growing at a striking CAGR of 16.11% during the forecast period. North America currently leads the way, accounting for over 33% of global revenue in 2024, but Asia Pacific is poised to be the fastest-growing region in the years ahead.

So, what’s fueling this surge in demand? Let’s dive into the key insights, drivers, challenges, and trends shaping the future of smart furniture.

Request FREE Sample PDF Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/smart-furniture-market-113604

Why Smart Furniture is Booming

At its core, smart furniture combines technology with traditional design to enhance comfort, convenience, and connectivity. From IoT-enabled automation to wireless charging and posture monitoring features, these innovations are turning everyday items into multifunctional, connected solutions for homes, offices, and hospitality settings.

- Technological Advancements

The rise of IoT, AI, and voice-assistant integration (like Alexa and Google Assistant) is accelerating product adoption. Smart desks, for example, now feature adjustable heights, wireless charging, and even sensors that track posture and stress levels. - Growing Smart Home Culture

With the global rise of smart homes, consumers are investing in furniture that integrates seamlessly into connected ecosystems. A survey by Samsung Electronics revealed that British households spent 7.7% more on smart home solutions in 2024 compared to the year before. - Wellness and Ergonomics

Smart chairs and desks that track heart rates, encourage movement, and correct posture are seeing demand surge, especially with more people working from home or in hybrid office setups. - Sustainability Push

Manufacturers are also tapping into eco-conscious trends by combining reclaimed wood, recycled plastics, and plant-based materials with smart features. This approach not only aligns with sustainability goals but also appeals to environmentally aware consumers.

Market Challenges to Watch

Despite its impressive growth trajectory, the smart furniture market faces a few hurdles:

- High Costs: Advanced features and short product life cycles make smart furniture significantly pricier than traditional options.

- Data Security Concerns: With IoT integration comes the risk of hacking and privacy breaches.

- Power Dependency: Many products rely heavily on charging and power sources, limiting convenience in certain settings.

These challenges underline the importance of innovation in cost reduction, cybersecurity, and energy efficiency.

Key Trends Reshaping the Market

- Foldable and Space-Saving Designs: Demand is rising for modular and foldable furniture with integrated wireless charging, particularly in compact urban homes and coworking spaces.

- Integration with Wellness Tech: Smart beds now monitor sleep patterns, while office furniture offers stress and posture tracking.

- Hospitality Sector Growth: Hotels and spas are increasingly adopting connected beds, ergonomic chairs, and multifunctional desks to enhance guest experiences.

For instance, in February 2024, HNI Corporation opened an experience center in Hyderabad, India, showcasing modular office furniture designed for digitally connected workplaces. Similarly, Ashley Furniture partnered with Samsung to integrate SmartThings into its product line, bridging the gap between home comfort and advanced connectivity.

Market Segmentation Highlights

By Product

- Tables & Desks lead the market, driven by demand from corporate offices and cafes seeking charging-enabled furniture.

- Chairs & Sofas are expected to be the fastest-growing category, thanks to AI-enabled reclining, massage, and wellness features.

- Beds are gaining traction among aging populations and healthcare facilities for their adjustable, remote-controlled features.

By Material

- Wood remains the dominant material, with demand for premium pine and eucalyptus-based products.

- Leather and Glass (in the “Others” category) are expected to grow quickly, with innovations like self-cleaning leather sofas and 3D-printed glass tables.

By End-User

- Residential users dominate, fueled by single-person households and the rising smart home trend.

- Hotels are a close second, increasingly adopting connected furniture to boost guest comfort.

- Offices continue to drive steady demand, especially for ergonomic desks and smart storage systems.

By Distribution Channel

- Specialty stores currently lead sales, benefiting from brand partnerships and in-store experiences.

- Online channels, however, are forecasted to grow the fastest, driven by discounts, convenience, and the shift toward digital retailing.

Read More Info: https://www.fortunebusinessinsights.com/smart-furniture-market-113604

Regional Outlook

- North America leads with USD 282.04 million in revenue (2024), thanks to strong adoption of smart homes and office solutions.

- Asia Pacific is set to grow the fastest, driven by aging populations in China and Japan, rising urbanization, and expanding hotel infrastructure in India and Southeast Asia.

- Europe follows closely, with demand for energy-efficient, space-saving smart furniture across the U.K., Germany, and Italy.

- South America and the Middle East & Africa are emerging markets, fueled by online retail penetration and expanding infrastructure projects.

Competitive Landscape

The market is moderately consolidated, with the top five players accounting for nearly 30% of the share in 2024. Leading companies include:

- HNI Corporation (U.S.)

- La-Z-Boy Incorporated (U.S.)

- Ashley Furniture Industries, Inc. (S.)

- IOF srl (Italy)

- Desktronic (Lithuania)

- Sleep Number Corporation (U.S.)

- StoreBound LLC (U.S.)

- Steelcase, Inc. (U.S.)

- Inter IKEA Systems B.V. (Netherlands)

- Herman Miller, Inc. (U.S.)

These players are focusing on customization, ergonomic innovation, and retail expansion to capture new markets. For example, Desktronic’s dual-motor adjustable desks cater directly to the hybrid work trend, while Sleep Number is pushing into AI-powered smart beds for better sleep health.

Final Thoughts

The smart furniture market is no longer a futuristic concept—it’s here and expanding rapidly. Rising consumer demand for connected, ergonomic, and eco-friendly solutions is driving innovation across residential, office, and hospitality sectors. While challenges such as high costs and cybersecurity risks remain, the long-term outlook is overwhelmingly positive.

As technology and lifestyle needs evolve, smart furniture will continue to play a critical role in shaping how we live, work, and relax—transforming everyday spaces into connected, sustainable, and wellness-focused environments

Athletic Footwear Industry Growth, Market Share & Size Forecast 2025–2032

By Industry Outlook, 2025-09-05

The athletic footwear market size was valued at USD 132.45 billion in 2023 and is expected to be worth USD 138.72 billion in 2024. The market is projected to reach USD 210.94 billion by 2032, recording a CAGR of 5.38% during the forecast period. North America dominated the athletic footwear market with a market share of 34.19% in 2023.

- North America witnessed athletic footwear market growth from USD 43.57 Billion in 2022 to USD 45.29 Billion in 2023.

Athletic footwear encompasses shoes specifically designed for sports and physical activities, offering features that enhance performance, comfort, and durability. The industry includes a variety of products such as running shoes, training shoes, and lifestyle sneakers. A major driver of market growth is the increasing participation in sports and fitness activities, fueled by rising health awareness among consumers.

However, the COVID-19 pandemic adversely impacted the growth of the athletic footwear market. Widespread travel restrictions, lockdowns, and social distancing measures resulted in the cancellation or postponement of numerous sporting events and fitness activities. With limited outdoor movement and reduced consumer spending on non-essential goods, the demand for athletic footwear witnessed a significant decline during this period.

Request FREE Sample PDF Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/athletic-footwear-market-104126

LIST OF KEY COMPANIES PROFILED IN THE REPORT

- Nike, Inc. (U.S.)

- Adidas AG (Germany)

- Mizuno Corporation (Japan)

- PUMA SE (Germany)

- Under Armour, Inc. (U.S.)

- Deckers Outdoor Corporation (U.S.)

- FILA Holdings Corporation (South Korea)

- On Holding AG (Switzerland)

- New Balance Athletics, Inc. (U.S.)

- Lululemon Athletica Inc. (Canada)

Competitive Landscape:

Top Brands Introduce Innovative Products to Expand Consumer Reach

Leading players in the athletic footwear market are actively launching new products equipped with advanced technologies to meet the evolving safety, comfort, and performance needs of consumers. Many manufacturers are integrating smart features such as embedded sensors to provide users with real-time data and insights during workouts or athletic activities, enhancing the overall fitness experience and broadening their appeal to tech-savvy customers.

Notable Industry Development:

August 2024: Puma unveiled its latest innovation in athletic footwear with the launch of MagMax NITRO running shoes. This new model incorporates the brand’s cutting-edge NITROFOAM™ technology , designed to deliver enhanced cushioning and superior energy return. According to the company, MagMax NITRO provides "supermax" comfort and propulsion, aiming to improve performance for both casual runners and professional athletes. The launch reflects Puma’s continued focus on blending advanced technology with performance-driven design to meet the evolving needs of the athletic footwear market.

Segmentation:

Running Shoes See Surge in Demand Amid Growing Marathon Participation

By product type, the athletic footwear market is segmented into training shoes (CrossFit/cross-training), running shoes (performance), lifestyle shoes (skateboarding), outdoor shoes (trail), and others. Among these, the running shoes segment held the largest market share in 2023 , driven by the rising number of marathons worldwide. The increase in marathon events and growing interest in long-distance running have significantly contributed to the rising demand for performance-oriented running shoes.

Men Dominate End-User Segment with Increased Sports Involvement

Based on end users, the market is categorized into men, women, and children. The men’s segment emerged as the leading contributor to market share in 2023 , largely due to the growing participation of men in various sports and fitness activities. This demographic trend has fueled consistent demand for high-performance athletic footwear across multiple categories.

Hypermarkets and Supermarkets Attract More Shoppers with Extensive Product Range

In terms of distribution channels, the market is divided into hypermarkets/supermarkets, specialty stores/sporting goods stores, departmental stores, online stores/e-commerce, and others. The hypermarkets/supermarkets segment led the market in 2023 , benefiting from increased customer footfall. These retail outlets offer a broad assortment of athletic footwear from various brands, allowing consumers to explore and compare products conveniently under one roof.

Regional Overview

Geographically, the athletic footwear market is segmented into North America, Europe, Asia Pacific, South America, and the Middle East & Africa . Each region presents unique growth opportunities influenced by cultural trends, economic conditions, and levels of sports participation.

Regional Insights:

North America Leads the Global Athletic Footwear Market Driven by Growing Health Awareness

North America emerged as the dominant region in the global athletic footwear market, fueled by a heightened focus on health, wellness, and active lifestyles. A growing number of individuals in the region are engaging in regular fitness routines, sports, and outdoor recreational activities, contributing significantly to the demand for high-performance athletic footwear. The United States, in particular, plays a pivotal role due to its large consumer base and strong sports culture. Additionally, the presence of major athletic footwear brands and manufacturers, including Nike, Under Armour, and Skechers, provides the region with a competitive edge and strengthens its leadership in the global market.

Asia Pacific to Witness Rapid Growth Due to Rising Income Levels and Sports Participation

The Asia Pacific region is projected to experience substantial growth in the coming years, driven by rapid urbanization, expanding middle-class populations, and increasing health consciousness. Countries such as India and China are at the forefront of this growth due to their booming economies and rising disposable incomes. As consumers in these countries gain greater purchasing power, their willingness to invest in premium, branded sports footwear has significantly increased. Furthermore, government initiatives promoting sports participation and fitness, along with a growing interest in global sports trends, are expected to accelerate market expansion across the region.

Get Full Report: http://fortunebusinessinsights.com/athletic-footwear-market-104126

Drivers and Restraints:

Rising Sports Participation to Accelerate Market Expansion

The growing global emphasis on health and wellness—especially in the wake of the COVID-19 pandemic—has significantly increased participation in sports and fitness activities. Individuals are increasingly engaging in activities such as running, cycling, hiking, and gym training to improve their physical and mental wellbeing. This shift in lifestyle has fueled the demand for athletic footwear, which is essential for enhancing comfort, performance, and injury prevention during physical activities. As a result, the market is witnessing strong growth driven by evolving consumer preferences and active lifestyle trends.

Environmental Concerns Over Shoe Waste May Limit Market Growth

Despite the positive outlook, the market faces a key challenge in the form of environmental sustainability. The large-scale production and disposal of athletic footwear contribute to growing concerns over non-biodegradable waste and environmental degradation. Most athletic shoes are made using synthetic materials and complex manufacturing processes, making them difficult to recycle. These sustainability issues, if not addressed, could pose a restraint on market growth, as both regulators and consumers demand more eco-friendly solutions.

Segmentation Overview (Athletic Footwear Market):

- Running Shoes Dominate by Product Type:

- Segments include training shoes (CrossFit/cross-training), running shoes (performance), lifestyle shoes (skateboarding), outdoor shoes (trail), and others.

- In 2023, running shoes led the market due to a global rise in marathon participation and increased interest in long-distance running, driving demand for performance footwear.

- Men Lead End-User Segment:

- End users are segmented into men, women, and children.

- The men’s segment held the largest market share in 2023, fueled by increased male participation in sports and fitness activities, boosting demand for high-performance shoes.

- Hypermarkets/Supermarkets Top Distribution Channel:

- Distribution channels include hypermarkets/supermarkets, specialty/sporting goods stores, departmental stores, online stores/e-commerce, and others.

- Hypermarkets and supermarkets dominated in 2023 due to high customer traffic and a wide range of brands, allowing easy product comparison and selection.

- Regional Analysis:

- The market is geographically segmented into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Growth dynamics vary across regions, influenced by economic factors, cultural preferences, and sports participation levels.

Report Coverage – Key Highlights:

- In-depth Market Analysis:

Covers detailed examination of leading product types, end-user segments, and distribution channels. - Focus on Key Players:

Profiles prominent companies in the market, analyzing their strategies, market share, and competitive positioning. - Latest Trends Identified:

Highlights emerging market trends, including technological advancements and shifts in consumer behavior. - Industry Developments Tracked:

Reviews major developments such as product launches, partnerships, mergers, and acquisitions. - Additional Market Insights:

Provides comprehensive insights into various other growth drivers and factors influencing market expansion.

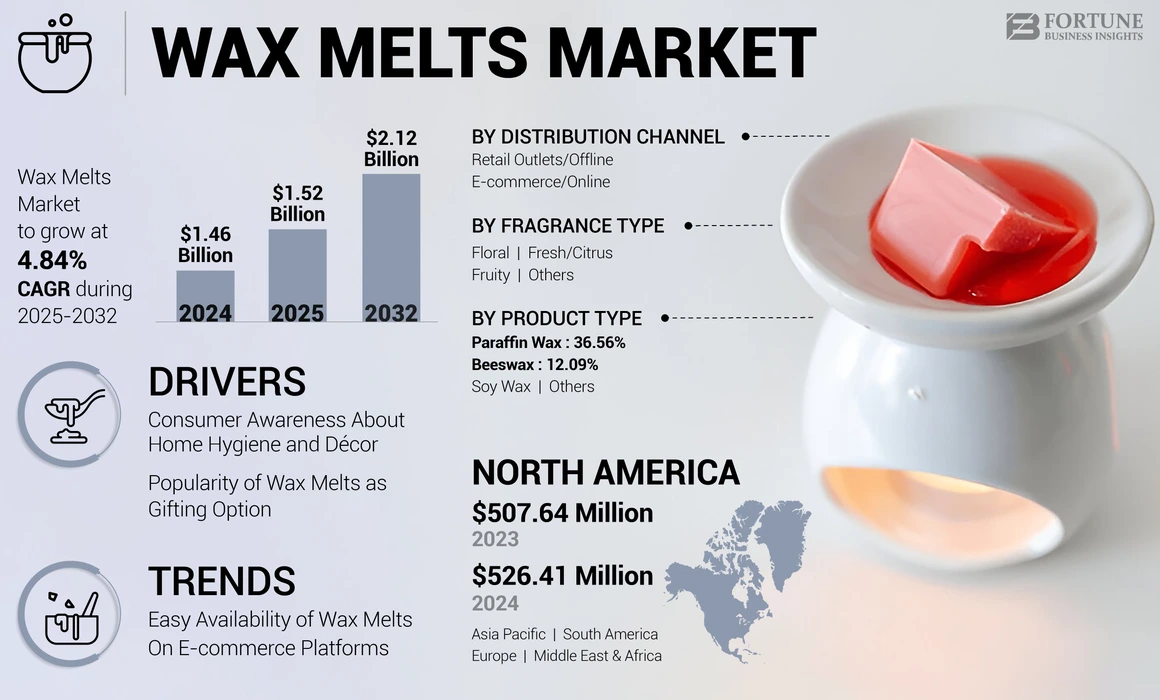

The global wax melts market size was valued at USD 1.46 billion in 2024. The market is projected to grow from USD 1.52 billion in 2025 to USD 2.12 billion by 2032, exhibiting a CAGR of 4.84% during the forecast period. North America dominated the wax melts market with a market share of 36.06% in 2024.

- North America witnessed wax melts market growth from USD 507.64 Million in 2023 to USD 526.41 Million in 2024.

Wax melts are pieces of scented wax that are melted to release a powerful scent into the air of residential and commercial spaces. They are used in office spaces, cafes, restaurants, and other public places to improve the overall ambience. Wax melts come in a wide range of sizes, colors, and fragrances to suit diverse preferences of individuals and enhance their overall experience. Moreover, they are longer lasting and more versatile as compared to the conventional candles, which will boost their demand.

Request FREE Sample PDF Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/wax-melts-market-112079

LIST OF KEY COMPANIES PROFILED IN THE REPORT

- The Yankee Candle Company, Inc. (U.S.)

- East Coast Candles Company (U.S.)

- Bramble Bay Collections (Australia)

- Bridgewater Candle Company (U.S.)

- C. JOHNSON & SON, INC. (U.S.)

- Procter & Gamble (U.S.)

- Hampshire Candles (U.K.)

- Shearer Candles (U.K.)

- OLOR (U.K.)

- Kana Creations (India)

Segmentation:

Demand for Paraffin Wax Rises Owing to Its Widespread Use in Commercial Places

Based on product type, the market includes paraffin wax, beeswax, soy wax, and others. The paraffin wax segment is dominating the global market as this type of wax melt is extensively used in several commercial spaces, such as hotels, spas & salons, and restaurants as it can create a pleasant indoor environment.

Enhanced Mood and Energy Levels to Popularize Fresh/Citrus Fragrance Among Customers

Based on fragrance type, the market is divided into floral, fresh/citrus, fruity, and others. The fresh/citrus segment is expected to dominate the global wax melts market share as this fragrance is known to boost the mood and energy levels of individuals. This is why this wax melts of this fragrance are being widely used in aromatherapy.

Rising Network of Convenience Stores Boosts Product Sales from Retail Outlets/Offline Stores

Based on distribution channel, the market is divided into retail outlets/offline and e-commerce/online. The retail outlets/offline segment accounts for the biggest market share as the network of convenience stores, supermarkets, and hypermarkets is increasing across the world. These stores offer a wide range of wax melts in diverse price ranges.

The global market report analyzes the market’s growth across regions, such as North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Report Coverage:

The report has conducted a detailed study of the market and highlighted several critical areas, such as leading product types, fragrance types, distribution channels, and prominent market players. It has also focused on the latest market trends and the key industry developments. Apart from the aforementioned factors, the report has given information on many other factors that have helped the market grow.

Drivers and Restraints:

Rising Awareness Regarding Home Hygiene and Décor to Bolster Market Growth

Customers across the world are becoming more aware of various home hygiene and décor products, such as candles, room sprays, incense sticks, essential oils, and wax melts. These products play a vital role in creating a pleasant environment at homes and in public spaces. Governments and NGOs are also launching various initiatives and campaigns to promote these home hygiene products. These factors are expected to boost the adoption of wax melts.

However, strong competition from substitutes can hinder the wax melts market growth.

Regional Insights:

North America Dominates Global Market Due to Rise in Construction of Residential Spaces

North America is dominating the global market as the region is witnessing a strong rise in the construction of residential spaces. Countries, such as the U.S., Mexico, and Canada are accelerating the construction of these spaces to accommodate the growing urban population. This factor is expected to boost the demand for modern home décor and hygiene products, such as wax melts.

Europe is also expected to record a commendable growth rate due to the growing popularity of scented home décor and scented products, such as candles to create a comfortable living environment at home.

Competitive Landscape:

Leading Manufacturers to Focus on Business Expansion to Increase Their Product’s Reach

The leading manufacturers operating in the wax melts market are focusing on expanding their business operations in various regions to increase the reach of their products and make more customers aware of their products. They are also launching unique wax melt products to cater to diverse customer requirements and preferences.

To know more about this market, please visit: https://www.fortunebusinessinsights.com/wax-melts-market-112079

Notable Industry Development:

October 2024: IRIS Home Fragrances, an Indian manufacturer of home fragrance products, launched a new collection of four exquisite Diwali gift sets. This set included wax melts, candles, reed diffusers, and other products to help their customers create a calm and peaceful environment at their homes.

August 2023: Classic Candle, a U.K.-based home fragrance brand, announced the launch of MiniPot Wax Melts. These wax melts were created from white wax and featured in the brand’s signature classic packaging.

December 2022: EMME NYC, a U.S.-based natural home fragrance products manufacturer, added two seasonal scents and wax melts to its production line. This launch was expected to enhance the company’s product portfolio.

February 2022: Yankee Candles, a brand of Newell Brands headquartered in the U.S., announced the launch of its Well Living Collection. This collection was created with essential oils, a blend of soy and coconut wax, and natural fiber wicks.

The global air fryer market size was valued at USD 8.07 billion in 2024 and is expected to grow to USD 9.40 billion in 2025, reaching USD 17.71 billion by 2032. This represents a Compound Annual Growth Rate (CAGR) of 9.47% over the forecast period. In 2024, Asia Pacific emerged as the leading regional market, accounting for a dominant share of 46.22%.

Air fryers are multifunctional cooking devices increasingly adopted in both household and commercial environments, such as restaurants and hotels, for preparing a wide range of dishes with minimal oil—supporting healthier eating practices. Rising disposable incomes have encouraged consumers to invest in advanced and high-quality kitchen appliances, thereby fueling market growth. The onset of the COVID-19 pandemic significantly boosted air fryer usage, as many households turned to home cooking to reduce exposure to health risks from food delivery services. Lockdowns and social distancing further spurred the demand for convenient appliances like air fryers and microwave ovens. However, the pandemic also led to the temporary closure of restaurants and food service establishments, causing a short-term dip in commercial demand for air fryers.

Request Free Sample PDF Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/air-fryer-market-107276

LIST OF KEY COMPANIES PROFILED IN THE REPORT

- Groupe SEB (France)

- Midea Group (China)

- Koninklijke Philips N.V. (Netherlands)

- Xiaomi Corporation (China)

- Spectrum Brands, Inc. (U.S.)

- Faber S.p.A. (Italy)

- Conair Corporation (U.S.)

- Meyer Corporation (U.S.)

- TTK Prestige Ltd. (India)

- NuWave, LLC. (U.S.)

Segmentation:

The air fryer market is segmented based on type, model, capacity, distribution channel, and end user. In terms of type, the digital segment led the market in 2024, driven by growing consumer demand for advanced cooking devices featuring multiple functions, digital connectivity, and voice control integration.

By model type, basket style models are expected to register the fastest growth due to their affordability and ability to cook a wide variety of foods evenly. These models offer a cost-effective alternative to toaster and oven-style air fryers, making them increasingly popular among consumers.

When categorized by capacity, 3–5 liter air fryers held the dominant market share in 2024, as this size is ideal for small or nuclear families, offering sufficient cooking volume for 2–3 people without occupying too much kitchen space.

In terms of distribution channels, supermarkets and hypermarkets accounted for the largest market share. Their wide product assortment—including both budget-friendly and high-end air fryers—makes them a preferred destination for shoppers seeking variety and convenience.

Based on end users, the household segment led the market in 2024, fueled by a rising preference for oil-free, healthier cooking alternatives among health-conscious individuals and families.

Geographically, the report evaluates market growth across major regions, including North America, Europe, Asia Pacific, South America, and the Middle East & Africa , offering a comprehensive view of regional performance and opportunities.

Key Highlights of the Report:

- Comprehensive Market Segmentation:

In-depth analysis based on product type, model type, capacity, distribution channel, and end user. - Focus on Leading Market Players:

Detailed profiling of prominent companies, including their market share, strategic initiatives, and recent developments. - Trend Analysis:

Identification of emerging trends shaping the market, such as technological advancements and changing consumer preferences. - Review of Industry Developments:

Coverage of major events like product launches, mergers & acquisitions, partnerships, and regulatory updates impacting market dynamics. - Growth Drivers and Restraints:

Evaluation of key factors propelling market growth, as well as challenges and risks that could hinder future expansion. - Regional Insights:

Analysis of market performance across major regions—North America, Europe, Asia Pacific, South America, and the Middle East & Africa. - Consumer Behavior Insights:

Examination of shifting buying patterns, preferences for healthier cooking methods, and adoption of smart kitchen appliances. - Forecast and Opportunity Assessment:

Market projections and identification of high-growth segments and untapped opportunities.

Regional Insights

In 2024, Asia Pacific led the global air fryer market, driven by strong demand for digital cooking appliances that enhance everyday cooking efficiency. Countries such as China, Japan, India, and South Korea are witnessing particularly high adoption rates, reinforcing the region's dominant market position. North America is also experiencing notable growth, supported by food companies promoting recipes specifically tailored for air fryers, further boosting consumer interest and regional demand.

More Info: https://www.fortunebusinessinsights.com/air-fryer-market-107276

Drivers and Restraints:

Increasing Inclination toward Energy-Efficient Cooking Devices to Fuel Market Growth

The demand for energy-efficient products is rising due to various factors, such as the increasing network of commercial housing complexes, the rising number of residential housing units, and the increasing demand for smart homes. Moreover, homeowners are increasing their spending on renovation and interior décor projects, further accelerating the adoption of aesthetically designed home appliances, such as air fryers.

However, higher prices as compared to traditional cooking appliances, will hinder the air fryer market growth.