The helicopter market was valued at USD 67.46 billion in 2023 and is expected to expand from USD 74.52 billion in 2024 to USD 97.13 billion by 2032, reflecting a CAGR of 3.4% during the forecast period. North America led the market in 2023, accounting for 55.34% of the global share. The U.S. helicopter market is anticipated to witness substantial growth, reaching approximately USD 45.26 billion by 2032, driven by rising military and civil helicopter deliveries across the country.

List of Key Players Profiled in the Helicopter Market Report

- Airbus S.A.S (Netherlands)

- Textron Inc. (U.S.)

- Leonardo S.p.A. (Italy)

- Lockheed Martin Corporation (U.S.)

- The Boeing Company (U.S.)

- Rostec (Russia)

- The Robinson Helicopter Company (U.S.)

- Kawasaki Heavy Industries Ltd. (Japan)

- Hindustan Aeronautics Limited. (India)

- Kaman Corporation (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/industry-reports/helicopter-market-101685

Segmentation:

Civil & Commercial Segment to be Prime Part due to Rising Demand for Emergency Services

According to type, the market is bifurcated into civil & commercial and military. The civil & commercial segment holds the largest share in the segment due to rising demand for emergency services and air transportation. The military segment is estimated to have moderate growth with use in disaster relief and humanitarian missions.

Light t o Lead Due to Demand for Civil and Commercial Helicopters

According to weight, the market is divided into light, medium, and heavy. Light segment dominated in 2022 due to growing demand for civil and commercial helicopters in sightseeing, aerial photography, and transportation of small groups and cargo.

EMS to Lead Due to Increasing Applications in Healthcare

Based on application, the market is divided into Emergency Medical Service (EMS), corporate service search and rescue operation, oil & gas, defense, homeland security, and others. The Emergency Medical Service (EMS) segment is set to dominate due to increasing applications in healthcare. The search and rescue operation segment has the second largest share owing to its applications in disaster management, aerial firefighting activities, and others.

Pre-Owned to Lead the Segment Due to Various Benefits

Based on point of sale, the market is divided into new and pre-owned. Pre-owned segment is set to dominate due to cost-effectiveness of pre-owned and increased backlog deliveries by OEMs.

In terms of geography, the market is studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Report Scope & Segmentation: Helicopter Market

Market Size Value in 2023: USD 67.46 Billion

Market Size Value in 2024: USD 74.52 Billion

Market Size Value in 2032: USD 97.13 Billion

Growth Rate: CAGR of 3.4% (2024-2032)

Study Period: 2019-2032

Base Year: 2023

Historical Data: 2019-2022

Get a Free Sample Research Report:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/helicopter-market-101685

Report Coverage

The report provides a detailed analysis of the top segments and the latest trends in the market. It comprehensively discusses the driving and restraining factors and the impact of COVID-19 on the market. Additionally, it examines the regional developments and the strategies undertaken by the market's key players.

Drivers and Restraints

Demand for Air Ambulance Services to Propel Market Growth

Demand for air ambulance services is projected to drive the helicopter market growth. The demand for air ambulance services has been increasing as they are one of the fastest means of transportation due to their quickness to offer transportation to critical patients. Their ability to reach remote and inaccessible areas makes them an ideal option for transporting patients to medical facilities with speed and efficiency. The demand for ambulance services is set by the growing elderly population, rise in chronic diseases, and the requirement for prompt medical attention during emergencies.

However, delivery backlogs, high operational, and maintenance costs to impede the market expansion.

Regional Insights

North America to Dictate Market Share Due to Modernization and Expansion of Military

North America held the dominating helicopter market share in 2022 due to modernization and expansion of the military fleet. In June 2022, Lockheed Martin Corp received a five-year contract for USD 2.3 billion to manufacture a minimum of 120 H-60M Black Hawks as the U.S. military seeks a successor to its existing fleet. The five-year contract includes an option for 135 additional aircraft worth USD 4.4 billion, available to the Army, U.S. agencies, and allies.

Europe has held the second-largest share as helicopters are used for the transportation of offshore wind farms and maintenance of wind turbines.

Asia Pacific is the fastest-growing region in the market due to defense spending by emerging countries and increasing demand for lightweight helicopters.

Competitive Landscape

New Product Launches by the Key Market Players to Boost Market Progress

The market has key players such as Airbus S.A.S, Textron Inc., Leonardo S.p.A., Lockheed Martin Corporation, The Boeing Company, and others. The key players have been adopting strategies such as mergers, acquisitions, product launches, collaborations, and partnerships. In December 2022, Airbus SAS launched DisruptiveLab for the improvement of rotorcraft performance. DisruptiveLab is a flying laboratory that is designed to test technologies that can enhance the performance of aircraft and reduce CO2 emissions.

Key Industry Development

December 2023: U.K.-based startup Hill Helicopters unveiled the first prototypes of its HX50 single-engine light helicopter. The two completed aircraft feature distinct landing gear configurations—one with skid landing gear and the other with wheeled landing gear.

August 2023: The U.S. State Department approved Poland's request to purchase 96 Boeing AH-64E Apache helicopters along with related equipment, in a deal valued at approximately USD 12 billion. If completed, this acquisition would make Poland the largest operator of the AH-64E outside the United States.

According to Fortune Business Insights, the global magnetometer market was valued at USD 3.64 billion in 2024 and is projected to grow to USD 7.75 billion by 2032, exhibiting a CAGR of 10.2% during the forecast period.

The market is expected to reach USD 3.94 billion in 2025, driven by increasing adoption across industries such as aerospace, defense, automotive, and consumer electronics. North America dominated the market in 2024 with a 38.74% share, supported by strong defense investments and advancements in magnetic sensing technologies.

Magnetometers are critical tools used to measure magnetic fields and are widely deployed in navigation systems, geophysical exploration, space missions, and industrial applications. The rising demand for precision navigation in drones, smartphones, and autonomous vehicles is significantly contributing to market growth. Additionally, ongoing innovation, sensor miniaturization, and growing integration of magnetometers in IoT devices are expected to further drive global market expansion.

List of key magnetometer companies profiled:

- Honeywell International Inc. (U.S.)

- Geometrics, Inc. (U.S.)

- Billingsley Aerospace & Defense (U.S.)

- AlphaLab, Inc. (U.S.)

- Applied Physics Systems (U.S.)

- Metrolab Technology SA (Switzerland)

- Bartington Instruments Ltd. (U.K.)

- FOERSTER Holding GmbH (Germany)

- Lake Shore Cryotronics, Inc. (U.S.)

- Marine Magnetics Corp. (Canada)

Information Source:

https://www.fortunebusinessinsights.com/magnetometer-market-112875

Segmentation: Magnetometer Market

Space Segment to Grow Steadily with Satellite-Based Deployments in LEO and Scientific Missions

By platform , the market is segmented into airborne , ground , maritime , and space . The space segment is expected to witness the fastest growth due to increasing launches of LEO (Low Earth Orbit) satellites, which rely on compact and high-precision magnetometers for navigation and attitude control systems.

Aerospace & Defense to Emerge as Dominant End-User Amid Rising Investments in Geospatial Intelligence

By end-user , the magnetometer market is categorized into aerospace & defense , consumer electronics , marine/naval , automotive , and others . The aerospace & defense segment held the largest share in 2024 due to extensive use in military aircraft, submarines, drones, and satellite missions requiring precise magnetic field detection.

North America Leads Global Adoption, Backed by High Investments in Space and Defense Programs

Regionally, the market is analyzed across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa . North America held the largest share in 2024, bolstered by advanced infrastructure, key magnetometer manufacturers, and robust demand from defense and space agencies such as NASA and the U.S. Department of Defense.

MARKET DYNAMICS

Market Drivers

Rising Integration of Magnetometers in UAVs and Autonomous Systems to Drive Market Growth

The increasing deployment of UAVs and autonomous systems across defense and commercial sectors is significantly fueling the demand for magnetometers. These sensors play a vital role in navigation by detecting Earth’s magnetic field, especially in GPS-denied or challenging environments. Their expanding use in aerospace applications—such as satellite positioning—and in defense for magnetic anomaly detection is further propelling market growth.

Market Restraints

Interference and Calibration Issues May Impede Market Expansion

Magnetometers are susceptible to magnetic interference from surrounding metallic objects and electronic equipment, which can compromise their accuracy and reliability. Moreover, these sensors often require frequent calibration and ongoing maintenance to ensure optimal performance. These technical challenges can increase operational complexity and costs, potentially limiting broader adoption in high-stakes sectors like aerospace and defense.

Key Industry Developments:

December 2024 — MDA Space selected Honeywell to supply Attitude Control Systems and Magnetometer Unit components, including Reaction Wheel Assemblies and 3-axis Space Rate Sensors, for the MDA AURORA satellite line. These systems will support Telesat’s LEO constellation by maintaining orientation and enhancing signal reliability and solar energy absorption.

The global military aircraft market was valued at USD 40.22 billion in 2018 and is projected to reach USD 85.79 billion by 2032, growing at a CAGR of 6.0% during the forecast period. North America led the market in 2018 with a 40.5% share. Military aircraft play a critical role in both combat and non-combat operations and are primarily operated by national defense forces and security agencies. While combat variants such as fighters and bombers are designed for offensive, defensive, and reconnaissance missions, non-combat aircraft support essential functions like transport, training, and surveillance. The market remains highly consolidated, with a limited number of key suppliers and government buyers shaping demand dynamics.

Geopolitical tensions and defense spending continue to be the primary growth drivers for this sector. The Russia-Ukraine war has heightened global interest in air dominance and triggered increased procurement activities, particularly among NATO allies and Eastern European countries. In the Asia Pacific region, governments are accelerating aircraft modernization efforts, driven by regional security challenges. Meanwhile, growth in the Middle East remains constrained due to budgetary pressures. These trends are comprehensively analyzed in Fortune Business Insights™’s report titled, "Military Aircraft Market, 2024–2032."

LIST OF KEY COMPANIES PROFILED IN THE REPORT

- Airbus S.A.S. (Netherlands)

- The Boeing Company (U.S.)

- Dassault Aviation SA (France)

- Lockheed Martin Corporation (U.S.)

- Saab AB (Sweden)

- Embraer S.A. (Brazil)

- GE Aviation (U.S.)

- Hindustan Aeronautics Limited (India)

- Bell Textron Inc. (U.S.)

- Sukhoi Corporation (Russia)

- Korea Aerospace Industries (South Korea)

- Chengdu Aircraft Industry Group (China)

Information Source:

https://www.fortunebusinessinsights.com/military-aircraft-market-102771

Segmentation: Military Aircraft Market

Fixed-Wing Aircraft Led the Market in 2024 Due to Strong Global Investments

Based on type, the market is segmented into fixed-wing and rotary-blade aircraft. The fixed-wing segment dominated the market in 2024, driven by global procurements of advanced multirole and stealth aircraft such as the F-35, Rafale, and Su-35. Meanwhile, rotary-blade aircraft are expected to grow rapidly due to increasing demand in Asia, the Middle East, and Africa.

Multirole Aircraft Dominated Due to Operational Versatility

By application, the military aircraft market is categorized into combat, multirole, transport, maritime patrol, reconnaissance & surveillance, and others. Multirole aircraft held the highest market share in 2024, supported by their flexible mission capabilities. The U.S., India, Russia, and China remain major buyers. The demand for reconnaissance and maritime patrol aircraft is also rising, particularly in emerging economies.

Engine Systems Held the Largest Share; Avionics to Grow Fastest

Based on system, the market is segmented into airframe, engine, avionics, landing gear, and weapon systems. The engine segment led the market in 2024 due to growing interest in fuel-efficient and hybrid propulsion. The avionics segment is projected to witness the fastest growth, as autonomous technology and integrated sensor systems gain prominence.

Drivers and Restraints

Rising Need to Replace Aging Fleets

Military aircraft fleets in countries like the U.S. are aging rapidly, prompting demand for advanced replacements. Modern aircraft with better sensors, fuel efficiency, and versatility are in high demand.

Fifth-Generation Aircraft Drive Innovation

The adoption of fifth-generation jets like the F-35, J-20, and AMCA (India) is reshaping air warfare. These aircraft offer stealth, supercruise, and sensor fusion, becoming central to modern defense strategies.

Global Arms Race to Accelerate Procurement

As geopolitical tensions rise, countries are boosting their air force capabilities. India, South Korea, and France are ramping up fighter programs, while nations like the U.S. continue their modernization with platforms like the B-21 Raider.

UAV Proliferation May Hinder Market Growth

The increasing use of unmanned aerial vehicles (UAVs) for reconnaissance, combat, and logistics could reduce the demand for traditional manned aircraft in some segments.

Regional Insights

North America Dominated the Market in 2018 and Will Retain Lead

The U.S. is expected to continue leading global military aircraft demand, with significant investments in stealth, transport, and bomber programs like the F-35, B-21 Raider, and KC-46.

Europe Boosting Procurement Amid Rising Security Threats

European nations are increasing their defense spending. Collaborative programs like FCAS (France-Germany) are reshaping the regional outlook.

Asia Pacific Rising Fast Due to Border Conflicts and Modernization

Countries like India and China are heavily investing in indigenous aircraft programs. India’s HAL AMCA and Tejas Mk2, along with China’s J-20 and FC-31, are shaping regional capabilities.

Middle East Growth Constrained by Budget Challenges

Despite demand for new aircraft, economic volatility and fiscal pressures are slowing market growth in this region.

Competitive Landscape

Boeing and Lockheed Martin Hold Market Leadership Due to Strategic U.S. Government Contracts

Major players are benefiting from long-term military contracts. Boeing’s $14.3 billion U.S. Air Force deal in April 2019 for the B-1B and B-52 bombers highlights sustained investment in long-range strike capabilities.

Notable Industry Development

April 2019 – The Boeing Company secured a USD 14.3 billion contract from the U.S. Department of Defense

This agreement focused on upgrading and supporting B-1B Lancer and B-52 Stratofortress bombers. The initiative will enhance aircraft survivability, responsiveness, and weapon integration capabilities, including radar and communication system modernization.

Gallium Nitride Device Market Competitive Landscape: Key Players and Strategies 2032

By Miyasingh, 2025-08-08

The global gallium nitride device market was valued at approximately USD 20.56 billion in 2019 and is expected to expand to around USD 39.74 billion by 2032, reflecting a compound annual growth rate (CAGR) of 5.20% from 2020 to 2032. In 2019, North America held a significant portion of the market, accounting for 35.89% of the total share. This growth trajectory indicates a strong demand for GaN devices across various applications in the coming years.

The gallium nitride (GaN) device market is experiencing significant growth, driven by increasing demand across various applications. This expansion reflects advancements in technology and the rising adoption of GaN devices in sectors such as telecommunications, automotive, and consumer electronics. North America is a key player in this market, showcasing a substantial share. Overall, the outlook for the GaN device market remains positive, with expectations for continued innovation and development in the coming years.

A list of all the prominent Gallium Nitride Device Market Key Players:

- Infineon Technologies AG (Germany)

- Efficient Power Conversion Corporation. (The U.S.)

- EPISTAR Corporation (Taiwan)

- GaN Systems (Canada)

- MACOM (The U.S.)

- Microsemi (The U.S.)

- Mitsubishi Electric Corporation (Japan)

- NICHIA CORPORATION (Japan)

- Northrop Grumman Corporation (The U.S.)

- NXP Semiconductors. (Netherland)

- Qorvo, Inc (The U.S.)

- Texas Instruments Incorporated. (The U.S.)

- Toshiba Corporation (Japan)

Information Source:

https://www.fortunebusinessinsights.com/gallium-nitride-gan-devices-market-103367

Segmentation:

The gallium nitride (GaN) device market is segmented by various factors, including device type, wafer size, component, application, end user, and geography. Device types encompass opto-semiconductor, power semiconductor, and RF semiconductor devices. Wafer sizes range from 2-inch to 6-inch and above. Key components include transistors, diodes, rectifiers, and power integrated circuits (ICs). Applications for GaN devices span light detection and ranging, wireless and electric vehicle charging, as well as radar and satellite radio frequencies. End users include sectors such as aerospace, defense, healthcare, renewables, and information and communication technology. Geographically, the market is divided into regions such as North America, Europe, Asia-Pacific, the Middle East, and the rest of the world, with specific countries like the U.S., Canada, China, and Germany highlighted for their device type contributions.

Drivers & Restraints

Expansion of the Telecommunications Sector to Boost Growth

The increasing demand for energy-efficient gallium nitride (GaN) devices is being driven by the rapid expansion of the telecommunications sector. Many internet service providers are now prioritizing lower latency through optical fiber connections, along with enhancing connectivity and network capacity. Additionally, the growing adoption of GaN devices in 5G infrastructure is expected to further accelerate gallium nitride device market growth in the coming years. However, the high costs associated with the maintenance and development of gallium nitride devices may pose a challenge to this growth.

Segmentation- Gallium Nitride Device Market

Opto-semiconductor Device Segment to Grow Rapidly Backed by Increasing Usage in Lasers

Based on device type, the opto-semiconductor device segment procured the highest gallium nitride device market share in 2019. This growth is attributable to their increasing usage in various aerospace applications, such as Light Detection and Ranging (LiDAR) and pulsed lasers. Besides, they are used in optoelectronics, LEDs, lasers, photodiodes, and solar cells.

Regional Insights- Gallium Nitride Device Market

High Demand for Wireless Devices to Favor Growth in Europe

Geographically, North America generated USD 7.38 billion in 2019 because of the presence of numerous prominent manufacturers, such as MACOM, Cree, Inc., Northrop Grumman Corporation, Efficient Power Conversion Corporation, Microsemi, and others in this region.

Europe, on the other hand, is anticipated to grow significantly on account of the rising demand for wireless devices in Germany, France, and the U.K. In Asia Pacific, the rising demand for gallium nitride devices from emerging nations, such as India and China would aid growth.

Key Industry Developments:

January 2025 - Wolfspeed launched its Gen 4 MOSFET technology platform, delivering breakthrough performance for high-power applications, enhancing efficiency and reliability in real-world conditions.

November 2024 - Infineon introduced the world's first 300mm power gallium nitride (GaN) wafer technology at electronica 2024, marking a significant advancement in power electronics manufacturing.

The global aircraft component MRO market was valued at USD 18.13 billion in 2023 and is projected to grow from USD 19.20 billion in 2024 to USD 36.93 billion by 2032, registering a CAGR of 8.52% during the forecast period. North America led the market in 2023, accounting for a dominant share of 30.5%, driven by a strong presence of major MRO service providers, a large commercial aircraft fleet, and increasing investments in maintenance infrastructure.

Fortune Business Insights™ mentioned this in a report titled " Aircraft Component MRO Market Size, Share, Forecast and 2025-2032 ."

List of Key Players Present in the Report :

- Lufthansa Technik (Germany)

- AAR Corp. (U.S.)

- SIA Engineering Company (Singapore)

- ST Aerospace (Singapore)

- ST Engineering (Singapore)

- BOEING Company (U.S.)

- SR Technics (Switzerland)

- GE Aviation (U.S.)

- HAECO (Hong Kong)

- Bombardier Inc. (Canada)

Information Source:

https://www.fortunebusinessinsights.com/aircraft-component-mro-market-104871

Segmentation-

Commercial Aircraft Segment to Dominate due to Growing Demand for Aircraft Component MRO Services

By type, the market is segmented into commercial aircraft, business jets, general aviation aircraft, and helicopters. The commercial aircraft segment had the highest aircraft component MRO market share in 2022. The segment is also estimated to witness the highest growth rate due to increasing demand for aircraft component MRO services during the forecast period.

Flight Control Segment to Dominate due to Cost of the Component's MRO

By component, the market is segmented into wheel and brakes, landing gear, avionics, fuel system, hydraulic system, cockpit systems, flight control, electrical systems, thrust reversers, and others. The flight control segment will dominate the market during the forecast period due to the control’s complexity and cost associated with the component's maintenance, repair, and overhaul.

Process Ensuring Aircraft Performance to Lead to Overhaul Segment’s Dominance

By maintenance service, the market is segmented into inspection, overhaul, repairs, and others. The overhaul segment had the highest market share in 2022. The segment's dominance is attributed to the process ensuring the aircraft performance and tolerance set by its manufacturer.

Geographically, the market is studied across North America, Europe, Asia Pacific, the Middle East & Africa, and Rest of the World.

Report Coverage-

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- The latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints-

Increased Air Fleet Expansion and Aircraft Deliveries to Drive Market Growth

The demand for MRO services will increase due to continuous growth in fleet sizes and aircraft deliveries worldwide. A continuous rise in air travel in developing nations, such as China and India, will increase new aircraft demand in some major countries. There are choices available between independent MROs, aircraft traffic, and components due to increased experiences by the passenger-growth trend.

The high consultancy fees charged by the OEMs have made it difficult for the MRO services providers to expand and diversify their services worldwide, affecting the market growth.

Regional Insights-

Growing Demand for Aircraft Component MRO to Drive Market in North America.

The North America market was valued at USD 5.04 billion in 2022. North America is expected to dominate due to the growing MRO services market and increasing presence of top key players during the forecast period. In February 2022, IBS Software and Lynx Air partnered to implement the iFlight digital platform to manage flight and crew operations.

Asia Pacific is expected to grow at the highest CAGR over 2023-2030 owing to increasing demand for aircraft component MRO services from the commercial airlines of Singapore.

Competitive Landscape-

Rising Focus of Key Players on Providing a Variety of Services to Aid Market Growth

The upcoming trends in the market are technologically advanced aviation MRO software systems, cloud deployment, and new enhancements. Key companies, such as Aar Corp. (U.S.) and Lufthansa Technik, adopting collaboration strategies are driving the aircraft component MRO market growth during the forecast period. The rising investment by key players in the research and development of new technologies will also boost the market during the forecast period.

Key Industry Development

September 2023 – ST Engineering announced that it had secured a multi-year contract to provide Japan Airlines with component Maintenance-By-the-Hour (MBHTM) solutions. The contract stated that ST Engineering will continue to provide Japan Airlines’ Boeing 737-800s with a full suite of component solutions, including component pooling, component modification, repair & overhaul, component predictive health monitoring, and logistics services.

The global LEO satellite market was valued at USD 7.71 billion in 2024 and is projected to grow to USD 11.53 billion by 2032, rising from USD 7.93 billion in 2025, at a CAGR of 5.5% during the forecast period. North America dominated the market in 2024, holding a significant 38.91% share.

Market expansion is being driven by rising demand for high-speed communication, Earth observation, and seamless global connectivity. LEO satellites, positioned closer to Earth than traditional satellites, offer key advantages such as reduced latency and faster data transmission. These capabilities make them well-suited for a range of applications, including broadband internet, disaster response, navigation, and defense-related missions.

GLOBAL LEO SATELLITE MARKET OVERVIEW

- Market Size & Forecast

2024 Market Size: USD 7.71 billion

2025 Market Size: USD 7.93 billion

2032 Forecast Market Size: USD 11.53 billion

CAGR: 5.5% from 2025–2032 - Market Share

North America dominated the LEO satellite market with a 38.91% share in 2024, supported by substantial investments in satellite infrastructure, defense applications, and broadband expansion through large-scale satellite constellations like Starlink and Project Kuiper.

By type, the small satellite segment accounted for the largest share, owing to its lower launch costs, shorter development cycles, and increasing demand for compact, cost-effective systems.

By application, the communication segment led the market, driven by the rising need for global broadband and mobile connectivity, particularly in remote and underserved regions.

By end-use, the commercial segment held the dominant position, backed by rapid growth in IoT networks, satellite imaging, and navigation services across various industries. - Key Country Highlights

United States: Leads the global LEO satellite market with strong involvement from major players such as SpaceX, Amazon (Project Kuiper), and Lockheed Martin, supported by high levels of investment in both defense and commercial satellite capabilities.

Information Source:

https://www.fortunebusinessinsights.com/leo-satellite-market-112113

List of Key Players Mentioned in the Report:

- SpaceX (U.S.)

- Airbus Defense and Space (Germany)

- Lockheed Martin (U.S.)

- OneWeb (U.K.)

- Boeing (U.S.)

- Planet Labs Inc. (U.S.)

- Spire Global Inc. (U.S.)

- Iridium Communications Inc. (U.S.)

- Swarm Technologies (U.S.)

- GomSpace (Denmark)

Segmentation:

The global LEO satellite market is segmented by type, application, end use, and region. By type, the market is categorized into small, medium, and large satellites. In terms of application, it includes communication, Earth observation, navigation, scientific research, and others. By end use, the market is divided into government and military, and commercial sectors. Regionally, the market is analyzed across North America (U.S. and Canada), Europe (U.K., Germany, France, Russia, and the Rest of Europe), Asia Pacific (China, India, Japan, South Korea, and the Rest of Asia Pacific), and the Rest of the World, which includes Latin America and the Middle East & Africa. Each regional segment is further assessed by type, application, and end use to provide comprehensive market insights.

Report Coverage:

The global LEO satellite market report offers an in-depth analysis of market size, forecasts, and segmentation by application, end use, and type. It explores market trends, competition, product pricing, and key developments that have influenced the global market growth.

Drivers and Restraints: LEO Satellite Market

Rise of Small Satellites Constellations and Incorporation of Advanced Technologies to Bolster Market Growth

The launch of 2,402 small satellites in 2022 highlights the growing trend of adopting cost-effective and interconnected satellites. These systems enable extensive constellations that enhance global coverage and connectivity, meeting rising data and connectivity demands. Moreover, LEO satellite systems are becoming increasingly sophisticated, utilizing AI and machine learning to improve operational efficiency, lower costs, and provide low-latency solutions, further accelerating product adoption.

However, stringent regulations for satellite coordination and management can drive up operational costs and add complexity to satellite deployment, deterring LEO satellite market growth.

Regional Insights:

North America to Dominate the Market Owing to Strong Investment in Satellite Systems

North America leads the LEO satellite market with significant investments aimed at improving border surveillance, missile tracking capabilities, and national security. Leading companies such as Amazon, SpaceX, and Boeing are rapidly advancing satellite production and deployment, including Amazon’s Project Kuiper, which aims to produce over 3,000 satellites for enhanced global connectivity in July 2024.

The Asia Pacific region is benefitting from ongoing progress in spaceflight technology and launch systems, which supports the growth of the market. In August 2024, China’s plans to launch LEO satellites for its megaconstellation backed to a significant contract with the NRO, are set to enhance satellite infrastructure and global connectivity.

Competitive Landscape-

Key Players Focus on Mergers and Acquisitions to Sustain their Market Growth

Market leaders are focusing on advancing their product offerings by investing in R&D and developing diverse solutions. They are leveraging mergers, acquisitions, and new product launches to sustain their growth. Additionally, heavy investments in satellite networks are driving the push for global connectivity.

Key Industry Development:

May 2024 - The Ministry of Science and ICT in South Korea announced a USD 234.4 million project to launch two LEO satellites by 2030, leveraging 6G communication technology for advanced satellite-based connectivity.

The global air defense systems market was valued at USD 87.63 billion in 2024. It is expected to grow from USD 95.73 billion in 2025 to USD 154.81 billion by 2032, registering a compound annual growth rate (CAGR) of 7.11% during the forecast period. In 2024, North America led the market, accounting for a dominant share of 34.58%.

The air defense systems market is experiencing steady growth, driven by increasing global defense spending, rising geopolitical tensions, and the need for advanced technologies to counter evolving aerial threats. These systems play a crucial role in national security by detecting, tracking, and neutralizing incoming missiles, aircraft, and unmanned aerial vehicles (UAVs). Ongoing technological advancements, such as the integration of radar, missile interceptors, and command and control systems, are further enhancing system capabilities. With a growing focus on modernizing military infrastructure, countries worldwide are investing heavily in air defense solutions to strengthen their defense preparedness.

List of Key Players Profiled in the Report:

- BAE Systems Plc. (U.K.)

- Elbit Systems Ltd. (Israel)

- General Dynamics Corp. (U.S.)

- Hanwha Aerospace Co., Ltd. (South Korea)

- Israel Aerospace Industries Ltd. (Israel)

- Kongsberg Gruppen ASA (Norway)

- L3Harris Technologies Inc. (U.S.)

- Leonardo S.P.A. (Italy)

- Lockheed Martin Corp. (U.S.)

- Northrop Grumman Corp. (U.S.)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Raytheon Technologies Corp. (U.S.)

- Rheinmetall AG (Germany)

Browse In-depth Summary of This Research Insight:

https://www.fortunebusinessinsights.com/air-defense-systems-market-113430

Segmentation Highlights

Weapon Systems Segment Leads the Market Due to Strategic Defense Focus

By component, the air defense systems market is segmented into command & control systems, weapon systems, fire control systems, radar systems, and support equipment. Weapon systems dominate due to increasing investments in interceptors, missile launchers, and kinetic/directed energy weapons.

Threat Detection Systems Segment Expected to See Rapid Growth

Based on system type, the market is bifurcated into threat detection systems and countermeasure systems. Threat detection systems are expected to register the highest growth due to the escalating need for early-warning and tracking technologies.

Land-Based Segment Holds Largest Share

By platform, the land-based segment leads, attributed to the deployment of mobile and stationary units in conflict-prone regions for border and civilian infrastructure protection.

Short-Range Segment Driven by Rise in Drone and Cruise Missile Threats

On the basis of range, the air defense systems market is divided into short (below 10 km), medium (10–100 km), and long-range (above 100 km) systems. The short-range segment is growing rapidly due to the proliferation of small UAV threats.

Radar & Tracking Dominates Technology Segment

The radar & tracking category leads due to constant advancements in surveillance, tracking, and data fusion systems necessary for intercepting modern aerial threats.

Fixed Installations Remain Critical for Strategic Locations

By deployment mode, fixed installations are projected to maintain a significant share as they are essential for safeguarding key military bases, industrial sites, and cities.

Market Dynamics

Drivers:

- Rising Geopolitical Tensions Fuel Demand for Air Defense

Nations are accelerating procurement of integrated defense systems due to evolving threats from both state and non-state actors. Increased defense budgets are particularly evident in Europe, the Middle East, and Asia Pacific. - Advancements in Directed Energy and Radar Technologies Boost Growth

Technological progress in radar detection, AI-enabled tracking, and laser-based countermeasures enhance air defense efficiency, making these systems more reliable and responsive.

Restraints:

- High Development and Maintenance Costs May Hamper Adoption

Advanced air defense systems require substantial investment, which may challenge adoption in countries with limited defense budgets.

Regional Insights

North America Dominates Global Market Share with Strong Defense Infrastructure

North America accounted for a significant share in 2024, supported by large-scale procurement programs by the U.S. Department of Defense and the presence of major players like Raytheon, Lockheed Martin, and Northrop Grumman.

Europe and Asia-Pacific Emerging as Strategic Markets

Europe’s growth is driven by rising regional tensions and collaborative NATO defense efforts. Asia Pacific, led by China, India, and South Korea, is investing in indigenous air defense capabilities and multi-domain deterrence.

Competitive Landscape

Collaborations and Product Innovation Key to Competitive Edge

Leading defense contractors are forming joint ventures and upgrading their air defense portfolios with new launches. Strategic contracts with governments continue to shape market growth.

Key Industry Development

November 2024 – Anduril received a USD 200 million, five-year Indefinite Delivery/Indefinite Quantity (IDIQ) contract from the U.S. Marine Corps to develop and deliver a Counter Unmanned Aerial System (CUAS) Engagement System (CES) for the Marine Air Defense Integrated System (MADIS). The MADIS CES is designed to offer rapid deployment and effective threat mitigation for expeditionary operations.

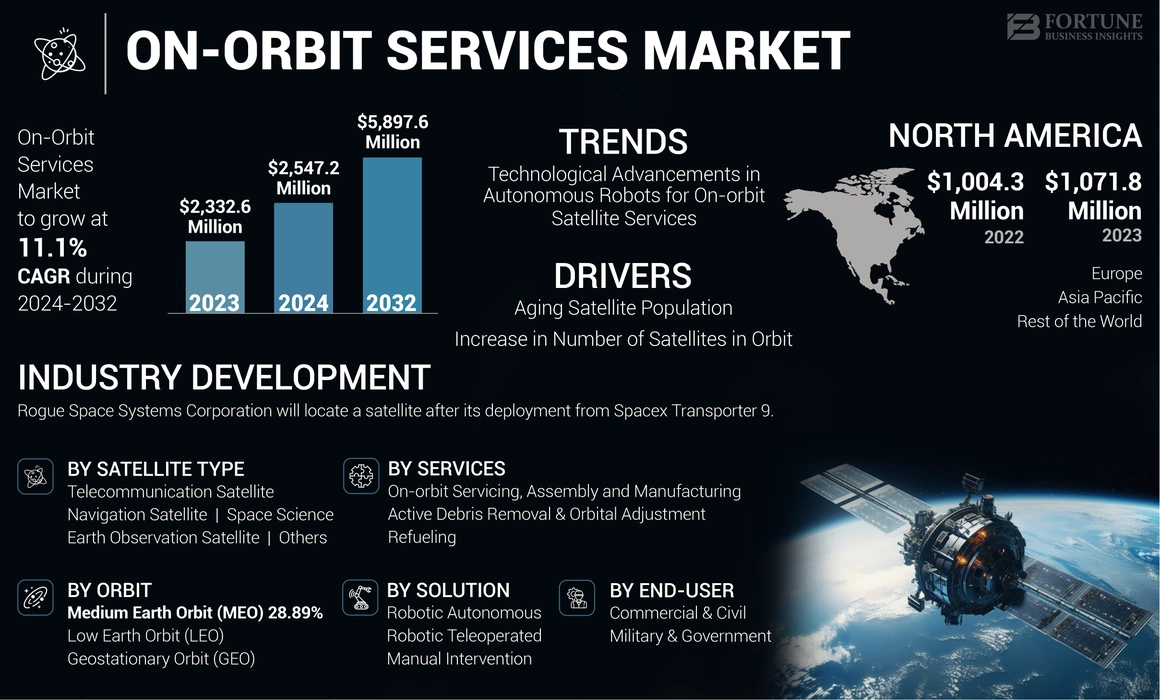

On-Orbit Services Market Growth Opportunities, Trends, and Forecast to 2032

By Miyasingh, 2025-08-06

The global on-orbit services market was valued at USD 2,332.6 million in 2023 and is projected to grow from USD 2,547.2 million in 2024 to USD 5,897.6 million by 2032, exhibiting a CAGR of 11.1% during the forecast period. North America led the market in 2023 with a dominant share of 45.95%.

The on-orbit services market is rapidly expanding, driven by the increasing need for satellite life extension, debris removal, refueling, and in-space manufacturing. As the number of satellites in orbit continues to grow, the demand for sustainable space operations and infrastructure maintenance is becoming more critical. Emerging technologies and partnerships between public and private space agencies are further accelerating innovation in on-orbit servicing capabilities. North America remains at the forefront, supported by strong government funding, a mature aerospace sector, and active participation from key players focused on extending satellite functionality and enhancing space situational awareness.

Key On-Orbit Services Market Players

Several companies are actively shaping the on-orbit services landscape. Leading organizations include:

- Airbus S.A.S (Netherlands)

- Thales Alenia Space (France)

- Lockheed Martin Corporation (U.S.)

- Orbit Fab (U.S.)

- Astroscale (Japan)

- ClearSpace SA (Switzerland)

- Obruta Space Solutions Corp. (Canada)

- D-Orbit SpA (Italy)

- Maxar Technologies (U.S.)

- Eta Space (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/on-orbit-services-market-108399

Market Segmentation

The on-orbit services market is segmented by end-user, orbit, satellite type, service, and solution. Among end-users, the military & government segment is growing rapidly due to investments from agencies like NASA and ESA, while the commercial & civil segment dominated in 2023. By orbit, Low Earth Orbit (LEO) held the largest share owing to increased small satellite deployments, whereas Geostationary Orbit (GEO) is expected to grow at the fastest pace as aging satellites require servicing. In terms of satellite type, Earth observation satellites led the market, while the space science segment is projected to grow fastest due to the critical nature of scientific missions. By service, refueling dominated and is anticipated to continue its strong growth, supported by cost-saving benefits and extended satellite lifespan. Lastly, robotic teleoperated solutions led in 2023 due to precision handling, while robotic autonomous systems are set to expand quickly with advancements in AI and visual perception technologies.

Regional Insights

North America

North America led the on-orbit services market in 2023, holding a dominant market share of 45.95%. The presence of major space companies, robust government funding, and increasing private sector participation have propelled growth in this region.

Europe

Europe is witnessing steady growth due to advancements in satellite servicing technologies and collaborations between government agencies and private firms.

Asia-Pacific

Countries like Japan and China are investing heavily in space missions, driving demand for on-orbit services in this region.

Rest of the World

Other regions, including the Middle East and Africa, are slowly entering the market, focusing on satellite-based communication and Earth observation initiatives.

Industry Developments:

December 2024 – Thales Alenia Space, a joint venture between Thales and Leonardo, signed a first-phase contract valued at €25 million (USD 26.09 million) with the European Space Agency (ESA) to develop and demonstrate a complete cargo delivery service to and from space stations in low-Earth orbit (LEO) by 2028. The company will co-lead the development of this innovative LEO Cargo Return Service, marking a key step toward commercial space logistics.

December 2023 – Rogue Space Systems Corporation, a provider of space situational awareness and satellite servicing solutions, announced its upcoming mission to locate and communicate with a customer’s satellite following its deployment from SpaceX's Transporter-9 mission. The operation will involve establishing contact and initiating in-orbit servicing tasks, supporting the customer’s satellite functionality and mission objectives.

Future Outlook

The on-orbit services market is poised for rapid expansion due to technological innovations, increasing satellite deployments, and the growing need for sustainable space operations. Companies are focusing on automation, AI-powered diagnostics, and in-orbit manufacturing to revolutionize the industry. As demand for satellite servicing rises, the sector is expected to witness increased investments, partnerships, and policy developments, shaping the future of space sustainability.