Defense Electronics Obsolescence Market Segmentation 2025-2032: Detailed Breakdown

By Miyasingh, 2025-08-04

The global defense electronics obsolescence market was valued at USD 2,530.1 million in 2024. It is expected to grow from USD 2,736.3 million in 2025 to USD 5,005.7 million by 2032, registering a compound annual growth rate (CAGR) of 9.0% during the forecast period.

North America dominated the market in 2024 with a 45.6% share, valued at USD 1.15 billion. In the U.S., the FY2025 defense budget exceeds USD 800 billion, with significant investments in predictive analytics and lifecycle forecasting led by key players such as BAE Systems, Raytheon, and Lockheed Martin. India’s FY2025 defense budget is expected to surpass USD 70 billion, emphasizing indigenization and technology-driven obsolescence management. Meanwhile, Germany, France, and the U.K. are collectively projected to exceed USD 300 billion in defense spending by 2025, supported by the European Defence Fund to advance interoperability and address obsolescence challenges.

List of Key Companies Profiled in the Report:

- Raytheon Technologies Corporation (U.S.)

- BAE Systems (U.K.)

- L3 Harris Technologies Inc. (U.S.)

- Thales Group (France)

- Elbit Systems Ltd (Israel)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- General Dynamics Corporation (U.S.)

- Bharat Electronics Ltd (India)

- Leonardo SPA (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/defense-electronics-obsolescence-market-112861

Segmentation Overview:

The defense electronics obsolescence market is segmented by system, platform, and type. Based on system, the market includes communication systems, navigation systems, flight control systems, electronic warfare systems, and others. Among these, the communication system segment held a significant market share in 2024 , largely due to the continuous need for upgrades to maintain secure and interoperable communications across the battlefield.

By platform, the market is categorized into land, naval, and air . The air platform segment is expected to witness robust growth during the forecast period , as airborne systems require frequent technological upgrades to sustain mission effectiveness and respond to emerging threats.

In terms of type, the market is divided into supply chain obsolescence, functional obsolescence, and technical obsolescence . The technical obsolescence segment is anticipated to dominate the market , driven by the rapid pace at which electronic components and technologies become outdated, thereby compelling defense organizations to consistently invest in modernization and system upgrades.

Drivers and Restraints:

Growing Need for System Upgrades to Drive Market Expansion

The rising reliance on electronics for mission-critical operations across defense platforms is creating a growing demand for timely system upgrades. With national security at stake, military forces cannot afford performance degradation due to obsolete parts, thereby driving growth in the defense electronics obsolescence market.

High Replacement Costs and Complexity to Restrain Market Growth

Despite growing demand, the high cost of replacement, integration challenges, and limited compatibility with legacy platforms are expected to restrain market growth. Additionally, managing global supply chains for defense-grade components remains a major concern.

Regional Insights:

North America to Hold Largest Market Share

North America led the global defense electronics obsolescence market in 2024, driven by substantial military spending and early adoption of digital warfare solutions by the U.S. Department of Defense . The region’s strong defense industrial base and focus on electronic warfare capabilities continue to support market expansion.

Europe and Asia-Pacific to Witness Substantial Growth

Europe ranks as the second-largest market due to defense modernization programs in the U.K., France, and Germany . Meanwhile, Asia-Pacific is anticipated to witness robust growth due to rising geopolitical tensions and increased military investments in countries like China, India, and Japan .

Competitive Landscape:

Leading companies are investing heavily in research and development (R&D) to tackle obsolescence proactively. Collaborations with governments, emphasis on modular system design, and digitization of legacy infrastructure are central to their growth strategies. These players are also actively pursuing contracts and modernization projects to expand their global presence.

Key Industry Developments:

-

December 2024 – A contract worth USD 1.2 billion was awarded for six Next-Generation Missile Vessels (NGMVs) . These vessels will enhance naval capabilities with advanced stealth and offensive electronics, emphasizing the urgency of mitigating obsolescence in modern platforms.

-

December 2024 – The Directorate of Defense Research and Development (DDR&D) under the Israel Ministry of Defense finalized several agreements with Elbit Systems to deliver cutting-edge communication systems to the Israel Defense Forces (IDF) . The deal, valued at around USD 130 million , highlights the strategic focus on modernizing defense communication infrastructure.

The land survey equipment market was valued at USD 9.69 billion in 2024 and is expected to grow from USD 9.92 billion in 2025 to USD 13.74 billion by 2032, reflecting a compound annual growth rate (CAGR) of 4.8%. In 2024, North America held the largest share of the market, accounting for 39.53%.

Key highlights include the United States benefiting from government and defense contracts and growing UAV and GNSS-based applications in infrastructure and mining; India modernizing land records using drones and rover technology; China experiencing rapid urbanization that boosts the adoption of domestic surveying tools; Japan maintaining steady demand for precision infrastructure development; and the UAE and Saudi Arabia seeing growth due to pipeline monitoring and infrastructure projects. Additionally, Brazil and Mexico's expanding agricultural and industrial sectors are fueling land demand and equipment sales.

Land Survey Equipment Market Trends

Technological Advancements in Surveying is a Latest Market Trend

The land survey equipment market has undergone a technological transformation in recent years. Surveying has evolved from conventional methods to advanced digital solutions, improving data accuracy, operational efficiency, and survey scope. These innovations have enabled surveyors to complete large-scale projects with higher precision and reduced manpower. The following key technologies are driving these advancements:

- Satellite Positioning Systems (GNSS):

Global Navigation Satellite Systems (GNSS) allow for highly accurate 2D and 3D spatial data collection. These systems enhance real-time surveying capabilities, significantly reducing survey completion time. - Mapping Software:

Advanced mapping platforms integrate database systems and GPS tools to visualize, analyze, and share spatial data. These tools streamline decision-making in large infrastructure and environmental projects. - Laser Scanning:

Laser scanners provide quick and detailed terrain measurements. They enable the creation of accurate 3D models, essential for civil engineering, construction, and geological studies. - Unmanned Aerial Vehicles (UAVs):

UAVs are transforming aerial surveys by capturing high-resolution imagery over large areas. They are particularly useful in agriculture, disaster response, mining, and energy exploration projects.

Information Source:

https://www.fortunebusinessinsights.com/land-survey-equipment-market-103329

List of Key Companies Profiled

- Hexagon AB (Sweden)

- Trimble Inc. (U.S.)

- Topcon Corporation (Japan)

- CHC Navigation (China)

- Hi-Target (China)

- U-Blox Holdings AG (Switzerland)

- Hudaco Industries (South Africa)

- GEOTECH 3D (UAE)

- Geosolution I Goteborg Ab (Sweden)

- Global GPS Systems (Netherlands)

These companies are investing in R&D to develop compact, mobile, and AI-integrated survey systems to meet the growing demand from industrial and government sectors.

Segmentation

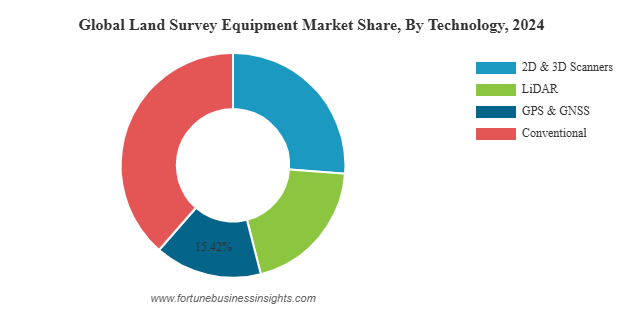

The land survey equipment market is segmented by solution into hardware and software, and by product into laser mapping systems, UAVs, mobile mapping systems (MMS), and total stations. Technologies include 2D & 3D scanners, LiDAR, GPS & GNSS, and conventional methods. Industries served encompass transportation, scientific and geological research, energy and power, precision agriculture, mining and construction, disaster management, forestry, and others. Applications include inspection, layout points, monitoring, and volumetric calculations. End-users are categorized as defense, industrial, commercial, and government. Geographically, the market spans North America, Europe, Asia Pacific, and the rest of the world, with specific focus on countries such as the U.S., Canada, U.K., Germany, France, China, India, Japan, and South Korea, among others.

Regional Insights

North America Led the Market Due to High Infrastructure Spending and Adoption of Advanced Technologies

North America accounted for the largest market share in 2024. The presence of leading companies such as Trimble Inc. and strong adoption of UAVs, LiDAR, and GNSS technologies across public and private sectors fueled regional growth.

Asia Pacific Expected to Grow at the Highest CAGR

Asia Pacific is anticipated to witness the fastest growth rate during the forecast period, driven by rapid urban development, smart city initiatives, and growing industrialization in India, China, and Southeast Asia.

Europe and Middle East Also Show Promising Growth Potential

Europe remains a strong market with ongoing public infrastructure projects and environmental mapping initiatives. Meanwhile, the Middle East & Africa region is experiencing growing demand for advanced land mapping solutions to support oil & gas, construction, and desert reclamation projects.

Competitive Landscape

Key Players Focus on Technological Upgrades and Strategic Collaborations to Expand Market Presence

Leading companies are focusing on expanding their technological capabilities, including integrating AI, real-time data sharing, and multi-sensor systems. Companies are also entering partnerships with governments and construction firms to deploy advanced land survey systems across infrastructure megaprojects.

Key Industry Development

-

May 2024: The Kansas Geological Survey, affiliated with the University of Kansas, launched aerial electromagnetic surveys across northwest Kansas. The initiative aimed to evaluate the state of the Ogallala Aquifer, a critical freshwater resource. These surveys utilized cutting-edge airborne geophysical technology to collect detailed subsurface data, showcasing the growing integration of scientific research and land survey equipment.

The global cargo drone market was valued at USD 1.15 billion in 2024 and is projected to rise to USD 1.82 billion in 2025, reaching USD 33.79 billion by 2032. This reflects a robust CAGR of 51.8% during the forecast period. North America led the market in 2024, accounting for a dominant 42.61% share.

Cargo drones are rapidly transforming the logistics and transportation industry by offering faster, more cost-effective, and environmentally friendly delivery solutions. They are particularly useful in remote and hard-to-reach areas where traditional delivery infrastructure is limited. With increasing investments in drone technology, favorable regulatory developments, and the growing demand for same-day and last-mile delivery, the adoption of cargo drones is expected to surge across sectors such as e-commerce, healthcare, defense, and disaster relief.

List of Key Companies Profiled

- DJI (China)

- Parrot SA (France)

- Natilus (U.S.)

- Dronamics (U.K.)

- Silent Arrow (U.S.)

- Sabrewing Aircraft Company (U.S.)

- Elroy Air (U.S.)

- Volocopter GmbH (Germany)

- Dufour Aerospace (Switzerland)

- H3 Dynamics (Singapore)

- Bell Textron Inc. (U.S.)

- Kaman Corporation (U.S.)

- Airbus (Netherlands)

- Elbit Systems (Israel)

- Israel Aerospace Industries (IAI) (Israel)

Information Source:

https://www.fortunebusinessinsights.com/cargo-drones-market-108151

Cargo Drones Market Drivers and Opportunities

Growth of E-Commerce and On-Demand Delivery Services

The boom in global e-commerce and expectations of faster delivery are fueling the adoption of cargo drones. Major retailers and logistics firms are exploring drone-based delivery systems to enhance operational efficiency and reduce reliance on ground transport in congested areas.

Technological Advancements and Automation

Advancements in VTOL design, battery technology, AI-powered navigation, and lightweight materials are making drones more capable and cost-efficient. Semi and fully autonomous systems are becoming viable for cargo missions over varying distances and terrains.

Regulatory Support and Infrastructure Development

Governments are increasingly supportive of drone logistics, developing regulatory frameworks, test corridors, and UAS traffic management systems. Strategic partnerships with logistics companies, tech firms, and municipal bodies are enabling pilot programs and ecosystem building.

Segmentation Analysis

The cargo drone market is segmented by type, automation level, range, payload capacity, component, application, end user industry, and region. By type, the market includes fixed wing, hybrid, and rotary wing drones. Based on automation level, it is categorized into fully autonomous, semi-autonomous, and remotely controlled systems. By range, cargo drones are classified as very short (up to 45 km), short (45 km to 150 km), medium (150 km to 550 km), and long (above 550 km). In terms of payload capacity, segments include featherweight (0.004 to 5 kg), lightweight (5–45 kg), middleweight (45–150 kg), and heavy-lift (150 kg and above). By component, the market is divided into camera, sensors, equipment, delivery packages, and others. The application segment comprises commercial cargo and military cargo. By end user industry, the market includes e-commerce, construction, government and defense organizations, healthcare, offshore and energy, and others. Regionally, the market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Regional Insights

North America Leads in Innovation and Defense Logistics

North America held the largest share in 2024 due to robust government funding, integration of drones in defense logistics, and active participation from tech giants and startups. FAA’s evolving UAS integration policies and pilot programs are accelerating commercial use cases.

Europe Focused on Eco-Friendly and Humanitarian Use

European countries like France, Germany, and the U.K. are emphasizing sustainable logistics and emergency delivery services using drones. Companies like Dronamics and Airbus are pioneering medium-to-long-range heavy-lift cargo drone solutions.

Asia Pacific Gaining Momentum with Urban Logistics

Rapid urbanization, high e-commerce activity, and government-backed smart city initiatives in China, India, and Southeast Asia are catalyzing drone delivery deployments. Local startups and global players are partnering to test scalable infrastructure.

Competitive Landscape

Innovation and Strategic Alliances Drive Market Dynamics

Leading cargo drone manufacturers are prioritizing R&D, prototype testing, and regulatory approvals. Collaborations with logistics providers, technology developers, and defense agencies are enabling scalable deployments. M&A activity is on the rise as companies race to develop versatile, payload-optimized platforms.

Key Industry Developments

-

April 2025 – Piasecki Aircraft acquired Kaman Air Vehicles’ Kargo UAV to expand its portfolio and accelerate the commercialization of autonomous aerial logistics. The production-ready model is expected by 2026.

The global cloud seeding market was valued at USD 394.9 million in 2024 and is expected to reach USD 428.6 million in 2025, growing further to USD 738.2 million by 2032. This represents a compound annual growth rate (CAGR) of 8.1% during the forecast period.

Cloud seeding is gaining traction worldwide as a weather modification technique aimed at enhancing precipitation, managing water resources, and mitigating the effects of drought. Governments and environmental agencies are increasingly adopting this technology to address water scarcity, improve agricultural productivity, and support ecological sustainability. Technological advancements, coupled with rising awareness of climate change impacts, are expected to drive further adoption of cloud seeding solutions across various regions.

Fortune Business Insights™ provides this information in its research report, titled “Cloud Seeding Market Size, Share, Forecast and 2024-2032”.

List of Key Players Mentioned in the Report:

- Weather Modification Inc. (U.S.)

- RHS Consulting Inc. (U.S.)

- North America Weather Consultants Inc. (U.S.)

- Snowy Hydro Limited (Australia)

- Mettech S.P.A (Chile)

- 3D S.A. (India)

- Cloud Technologies GmbH (Germany)

- Seeding Operations and Atmospheric Research (SOAR) (U.S.)

- Ice Crystal Engineering (ICS), LLC (U.S.)

- Charter Flights Aviation (India)

Information Source:

https://www.fortunebusinessinsights.com/cloud-seeding-market-104073

Segmentation:

Ground Seeding Segment Holds Leading Market Share Due to Increased Preference

Based on type, the market is fragmented into ground cloud seeding and aerial cloud seeding. The ground cloud seeding segment holds the largest market share. The product adoption is rising owing to the mounting demand for cost-effective processes of weather modification.

Glaciogenic Segment Accounted for Major Share Considering its Positive Outcomes

On the basis of technique, the market is bifurcated into hygroscopic and glaciogenic. The glaciogenic segment held a prominent market share owing to the positive results yielded by the process in cold cloud systems.

Drought-Prone Area Segment Holds Key Share Owing to the Issue of Water Scarcity

Based on target area, the market is divided into drought-prone area, agriculture & water supply, urban area, and others. The drought-prone area segment leads the market due to the surging product demand in light of the water scarcity in these regions.

Silver Iodide Segment Garnered Dominant Share Due to Escalating Awareness of Artificial Rains

On the basis of cloud seeding agent, the market is subdivided into silver iodide, sodium chloride, dry ice & potassium iodide, and others. The silver iodide segment captured a major market share driven by the increasing awareness regarding artificially stimulated rain and the increasing use of this agent.

Based on geography, the market has been studied across Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa.

Report Coverage:

The report discusses the latest trends in the market. It further presents an analysis of the key factors expected to propel the business scenario across various regions. An account of the major driving and restraining factors has also been presented in the report.

Drivers and Restraints:

Market Value to Surge Impelled by Climate Anomalies across the Globe

There has been a rising emphasis on the effective management of water resources by the government bodies for addressing issues associated with climate change. The surging demand for sustainable sources of water is poised to escalate their interest in creating artificial rains for the prevention of prolonged droughts and sustaining heat waves.

However, concerns associated with artificial weather modification could restrain cloud seeding market growth over the coming years.

Regional Insights:

Asia Pacific Led the Market Owing to Rising Product Deployment in Natural Disaster Relief

Asia Pacific held a dominating position and the highest cloud seeding market share in 2023. Issues associated with environmental pollution and an increase in natural hazards are some of the key factors driving the product demand for relief measures in the region.

Europe is set to expand at a moderate rate over the analysis period due to growing concerns in the region regarding the enhancement of agriculture and the incidences of wildfires.

Competitive Landscape:

Industry Players Focus on R&D Initiatives to Increase Market Share

Leading market participants are undertaking research and development activities. These initiatives are being adopted for strengthening their market share across various regions. Some of the prominent companies in the market are North America Weather Consultants Inc., and RHS Consulting.

Key Industry Development:

January 2024: Southern California water officials initiated cloud seeding operations as part of a four-year pilot program launched in November 2023, aimed at increasing regional precipitation by 5% to 15% to bolster the water supply. Similarly, in the same month, the government of Zimbabwe introduced a USD 400,000 cloud seeding program to stimulate rainfall and enhance agricultural productivity. This initiative was part of the country’s broader strategy to counter the negative impacts of El Niño-induced weather conditions.

The global AI in aviation market was valued at USD 6,200.0 million in 2024 and is expected to reach USD 7,449.3 million in 2025, before surging to USD 26,997.6 million by 2032, reflecting a strong CAGR of 20.20% during the forecast period. North America led the market in 2024, accounting for a dominant 46.19% share.

Artificial intelligence is transforming the aviation industry by enhancing operational efficiency, improving passenger experience, and optimizing decision-making processes. From predictive maintenance and automated customer service to flight operations and air traffic management, AI technologies are being integrated across multiple domains to increase safety, reduce costs, and enable smarter aviation ecosystems. As digital transformation accelerates, airlines and airports are increasingly investing in AI-driven solutions to remain competitive and resilient in a rapidly evolving landscape.

List of Key Players Mentioned in the Report:

- Intel Corporation (U.S.)

- IBM Corporation (U.S.)

- Airbus S.A.S. (Netherlands)

- Thales Group (France)

- Lockheed Martin Corporation (U.S.)

- General Electric Company (U.S.)

- The Boeing Company (U.S.)

- Garmin Ltd. (U.S.)

- Northrop Grumman Corporation (U.S.)

- Honeywell International Inc. (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/ai-in-aviation-market-113289

Segmentation Highlights:

The global AI in aviation market is segmented by application, offering, technology, end user, and region. By application, the market is categorized into flight operations, maintenance, air traffic management, and others. In terms of offering, it includes software, hardware, and service. Based on technology, the segmentation covers machine learning, computer vision, data analytics, and others. By end user, the market comprises airlines, airports, OEMs, and MROs. Regionally, the market is analyzed across North America (U.S. and Canada), Europe (U.K., Germany, France, Russia, and Rest of Europe), Asia Pacific (China, Japan, India, South Korea, and Rest of Asia Pacific), and the Rest of the World, which includes Latin America and the Middle East & Africa. Each region is further examined based on application, offering, technology, and end user.

Market Dynamics:

Drivers:

Operational Efficiency and Automation to Bolster Market Growth

AI’s growing role in optimizing air traffic management and flight route planning is a key driver. AI algorithms and machine learning systems are improving decision-making and enabling real-time adjustments in response to changing weather, airspace congestion, and fuel efficiency demands.

For example, in April 2025 , Alaska Airlines reported saving 480,000 gallons of jet fuel in six months by using an AI-powered flight route optimizer, showcasing AI’s ability to enhance sustainability and operational savings.

Post-Pandemic Digital Acceleration and Passenger Experience Enhancements

Post-COVID digital transformation has fast-tracked AI implementation across passenger-facing services, including biometric boarding, baggage tracking, and chatbots for customer engagement. Airports and airlines alike are prioritizing seamless, contactless experiences that AI can deliver.

Restraints:

Data Security and Privacy Concerns May Restrict Market Expansion

The integration of AI in aviation raises concerns around data privacy, cybersecurity, and compliance with international data regulations , especially with AI systems processing sensitive operational and passenger data. These challenges may hinder adoption, particularly in regions with stringent privacy laws.

Regional Insights:

North America to Maintain Dominance

North America is expected to lead the global AI in aviation market throughout the forecast period. The region benefits from early adoption of AI technologies, the presence of leading aerospace companies, and high investments in AI-enabled aviation platforms. Strategic collaborations between AI firms and aviation authorities further bolster growth.

Asia Pacific to Register the Fastest Growth

Asia Pacific is anticipated to witness the highest CAGR over the forecast period, driven by rising air passenger traffic , rapid airport modernization , and the growing presence of budget airlines. Countries like China , India , and Singapore are at the forefront of integrating AI into smart airport operations and traffic control systems.

Competitive Landscape:

Companies Focusing on AI Innovation and Aviation-Specific Solutions

Market leaders are investing heavily in developing tailored AI solutions for aviation. Strategies include partnerships with aviation regulatory bodies, collaborations with AI startups, and deployment of cloud-based analytics platforms for predictive and prescriptive intelligence.

Key Industry Developments:

-

March 2025 – The Federal Aviation Administration (FAA) awarded an $80,000 contract titled “ Azure OpenAI CDO ” to develop AI-driven aviation solutions leveraging OpenAI’s models via Microsoft Azure , signaling growing government interest in AI adoption.

-

October 2024 – Thales Group partnered with SITA to enhance air traffic management through real-time AI analytics, focusing on flight delay reduction and improved situational awareness.

The global sustainable aviation fuel market was valued at USD 1,845.2 million in 2024 and is projected to grow significantly, reaching USD 2,723.8 million in 2025 and soaring to USD 28,636.36 million by 2032. This remarkable growth reflects a compound annual growth rate (CAGR) of 48% over the forecast period. In 2024, North America dominated the market, holding a substantial 46% share, driven by strong policy support and investment in cleaner aviation technologies.

The SAF market is structured across several key segments that highlight its diverse growth potential. By type, the market is categorized into biofuel and synthetic fuel. Technological segmentation includes pathways such as HEFA-SPK (Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene), FT-SPK (Fischer-Tropsch Synthetic Paraffinic Kerosene), ATJ-SPK (Alcohol-to-Jet Synthetic Paraffinic Kerosene), and other emerging processes.

In terms of blending capacity, the market includes SAF mixtures ranging from 5% to over 50%, reflecting increasing adoption rates across the aviation industry. The end-use landscape spans commercial aviation, military aviation, and other sectors, with applications across both fixed-wing and rotary-wing aircraft.

From 2025 to 2032, regional forecasts indicate a strong global push toward SAF adoption, fueled by stricter environmental regulations, net-zero emissions targets, and the aviation industry's commitment to decarbonization. As governments and industry stakeholders accelerate their transition to low-emission fuels, SAF is poised to play a pivotal role in shaping the future of sustainable air travel.

Information Source:

https://www.fortunebusinessinsights.com/sustainable-aviation-fuel-saf-market-111563

Key Players:

- Neste (Finland)

- World Energy (U.S.)

- Gevo, Inc. (U.S.)

- Alder Fuels (U.S.)

- SkyNRG (Netherlands)

- Air BP (U.K.)

- Shell Aviation (Netherlands)

- TotalEnergies (France)

- Vitol Aviation (Switzerland)

- LanzaTech (U.S.)

- Fulcrum Bioenergy (U.S.)

Segmentation: Sustainable Aviation Fuel Market

High Compatibility With Existing Aircraft Increased Use of Biomass-based SAF

Based on type, the market is divided into biofuel and synthetic fuel. The biofuel segment captured the biggest market share in 2024 as this type of fuel is quite compatible with the current aircraft, thereby facilitating easier integration when compared to other fuel types.

HEFA-SPK Technology to Gain Major Traction Due to Strong Government Support for Renewable Fuels

Based on technology, the market is classified into HEFA-SPK (Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene), FT-SPK (Fischer-Tropsch Synthetic Paraffinic Kerosene), ATJ-SPK (Alcohol-to-Jet Synthetic Paraffinic Kerosene), and others. Others include HFS-SIP (Hydroprocessed Fermented Sugars to Synthetic Isoparaffins), Co-processing, Electro-fueled sustainable aviation fuel, and other technologies used to develop SAF. The HEFA-SPK segment is anticipated to dominate the global market as governments across the world are implementing various policies to support the production and use of renewable fuels.

Net-Zero Emission Goals of Airlines Boosted Use of Sustainable Aviation Fuel in Blending Capacity of 30-50%

Based on blending capacity, the sustainable aviation fuel market is segmented into 5% to 30%, 30% to 50%, and above 50%. The 30-50% segment held the biggest global Sustainable Aviation Fuel (SAF) market share in 2024 as several airlines and airports across the world have made their commitment to achieving net-zero emissions.

Rising Awareness of Environmental Impact of Conventional Jet Fuel Boosted Product Use in Commercial Aviation

Based on end use, the market is classified into commercial aviation, military aviation, and others. Others include business and general aviation. The commercial aviation segment dominated the market in 2024 as there is a rising global awareness about the environmental effects of using traditional jet fuel in commercial planes.

Product Adoption Rose in Fixed-Wing Aircraft Owing to Government Support for Developing SAF

Based on application, the market is segmented into fixed-wing aircraft and rotary-wing aircraft. The fixed-wing aircraft segment held the biggest market share in 2024 as governments across the world are offering their support in the form of subsidies and incentives to encourage the development and sale of Sustainable Aviation Fuel (SAF). This encouraged fixed-wing aircraft manufacturers to use this fuel.

The global market report analyzes the market’s growth across regions, such as North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report has conducted a detailed study of the market and highlighted several critical areas, such as leading types, technologies, applications, and prominent market players. It has also focused on the latest market trends and the key industry developments. Apart from the aforementioned factors, the report has given information on many other factors that have helped the market grow.

Drivers and Restraints:

Increasing Demand for Alternative Fuels to Boost Product Adoption

Industries across the world, including aviation, are becoming aware of the harmful effects of using fossil fuels on the environment, such as global warming and climate change. This factor has prompted them to take various measures to reduce their greenhouse gas emissions and make their business operations eco-friendlier. This is expected to fuel the adoption of Sustainable Aviation Fuel (SAF) in the aviation sector as this fuel has the potential to decrease emissions by nearly 80%, depending on the production technique and type of feedstock used. This can make the aviation industry more sustainable in its operations.

However, high cost and limited availability of feedstock can hinder the Sustainable Aviation Fuel (SAF) market growth.

Regional Insights:

North America Dominated Global Market Owing to Implementation of Strict Environmental Regulations

North America held the biggest sustainable aviation fuel market share in 2024 and might retain its dominance during the forecast period as well as governments across the region have imposed several stringent environmental regulations to reduce their carbon emissions. They have also formulated various policies to support the adoption of cleaner fuels in various industries.

Europe is also increasing its reliance on Sustainable Aviation Fuel (SAF) owing to the strict regulations imposed by the governments to decrease the carbon emissions of its industries, including aviation.

Competitive Landscape:

Market Players to Focus On Launch of Innovative Fuels to Cater to Wider Audience

Some of the top companies driving the global Sustainable Aviation Fuel (SAF) market growth are focusing on developing and launching a wide range of eco-friendly fuels for different industries. They are increasing their investments in research & development programs to find out about the latest technologies and use them to manufacture SAF.

Notable Industry Development:

September 2024- TotalEnergies signed an agreement with Air France-KLM to help the former deliver around 1.5 million tons of Sustainable Aviation Fuel (SAF) over a period of 10 years until 2035. This deal was one of the biggest SAF purchase agreements for Air France-KLM to date. It strengthened the airline’s dominance in the use of SAF, accounting for 17% and 16% of the global SAF production in 2022 and 2023, respectively.

The global helicopter market was valued at USD 67.46 billion in 2023 and is projected to grow to USD 97.13 billion by 2032, rising from USD 74.52 billion in 2024, at a CAGR of 3.4% during the forecast period. In 2023, North America dominated the market with a substantial 55.34% share, driven by consistent procurement and fleet modernization efforts. Notably, the U.S. helicopter market is expected to reach a valuation of USD 45.26 billion by 2032, reflecting strong growth across both military and civil segments.

The global market is expanding steadily, supported by growing demand for helicopters in military, civil, and commercial applications. Key drivers include increasing investments in defense modernization programs, the expansion of emergency medical services (EMS), and rising use of helicopters in transport, tourism, and offshore operations. Furthermore, technological advancements—such as improved fuel efficiency, advanced avionics systems, and the development of electric and hybrid helicopters—are contributing to the market’s evolution. With continued demand from regions like North America, supported by recurring orders and upgrades, the helicopter market is expected to maintain a positive growth trajectory through 2032.

List of Key Players Profiled in the Report

- Airbus S.A.S (Netherlands)

- Textron Inc. (U.S.)

- Leonardo S.p.A. (Italy)

- Lockheed Martin Corporation (U.S.)

- The Boeing Company (U.S.)

- Rostec (Russia)

- The Robinson Helicopter Company (U.S.)

- Kawasaki Heavy Industries Ltd. (Japan)

- Hindustan Aeronautics Limited. (India)

- Kaman Corporation (U.S.)

Information Source:

https://www.fortunebusinessinsights.com/industry-reports/helicopter-market-101685

Segmentation:

The global helicopter market is segmented based on type, number of engines, maximum take-off weight (MTOW), application, point of sale, and geography. By type, the market is categorized into civil & commercial and military helicopters. Based on the number of engines, it is divided into single-engine and twin-engine helicopters. In terms of MTOW, the market is segmented into less than 3,000 kg, 3,000 kg to 9,000 kg, and greater than 9,000 kg. By application, the segments include emergency medical service, corporate service, search and rescue operations, oil & gas, defense, homeland security, and others. Based on the point of sale, the market is classified into new and pre-owned helicopters. Geographically, the market is studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa—each region further segmented by type, number of engines, MTOW, application, point of sale, and key countries such as the U.S., Canada, U.K., Germany, France, China, India, Brazil, and the U.A.E.

Light t o Lead Due to Demand for Civil and Commercial Helicopters

According to weight, the helicopter market is divided into light, medium, and heavy. Light segment dominated in 2022 due to growing demand for civil and commercial helicopters in sightseeing, aerial photography, and transportation of small groups and cargo.

EMS to Lead Due to Increasing Applications in Healthcare

Based on application, the market is divided into Emergency Medical Service (EMS), corporate service search and rescue operation, oil & gas, defense, homeland security, and others. The Emergency Medical Service (EMS) segment is set to dominate due to increasing applications in healthcare. The search and rescue operation segment has the second largest share owing to its applications in disaster management, aerial firefighting activities, and others.

Pre-Owned to Lead the Segment Due to Various Benefits

Based on point of sale, the market is divided into new and pre-owned. Pre-owned segment is set to dominate due to cost-effectiveness of pre-owned and increased backlog deliveries by OEMs.

In terms of geography, the market is studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Report Coverage

The report provides a detailed analysis of the top segments and the latest trends in the helicopter market. It comprehensively discusses the driving and restraining factors and the impact of COVID-19 on the market. Additionally, it examines the regional developments and the strategies undertaken by the market's key players.

Get A Free Sample PDF:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/helicopter-market-101685

Drivers and Restraints

Demand for Air Ambulance Services to Propel Market Growth

Demand for air ambulance services is projected to drive the helicopter market growth. The demand for air ambulance services has been increasing as they are one of the fastest means of transportation due to their quickness to offer transportation to critical patients. Their ability to reach remote and inaccessible areas makes them an ideal option for transporting patients to medical facilities with speed and efficiency. The demand for ambulance services is set by the growing elderly population, rise in chronic diseases, and the requirement for prompt medical attention during emergencies.

However, delivery backlogs, high operational, and maintenance costs to impede the market expansion.

Regional Insights

North America to Dictate Market Share Due to Modernization and Expansion of Military

North America held the dominating helicopter market share in 2022 due to modernization and expansion of the military fleet. In June 2022, Lockheed Martin Corp received a five-year contract for USD 2.3 billion to manufacture a minimum of 120 H-60M Black Hawks as the U.S. military seeks a successor to its existing fleet. The five-year contract includes an option for 135 additional aircraft worth USD 4.4 billion, available to the Army, U.S. agencies, and allies.

Europe has held the second-largest share as helicopters are used for the transportation of offshore wind farms and maintenance of wind turbines.

Asia Pacific is the fastest-growing region in the market due to defense spending by emerging countries and increasing demand for lightweight helicopters.

Competitive Landscape

New Product Launches by the Key Market Players to Boost Market Progress

The helicopter market has key players such as Airbus S.A.S, Textron Inc., Leonardo S.p.A., Lockheed Martin Corporation, The Boeing Company, and others. The key players have been adopting strategies such as mergers, acquisitions, product launches, collaborations, and partnerships. In December 2022, Airbus SAS launched DisruptiveLab for the improvement of rotorcraft performance. DisruptiveLab is a flying laboratory that is designed to test technologies that can enhance the performance of aircraft and reduce CO2 emissions.

Key Industry Development

In August 2023 , Airbus Helicopters and Korea Aerospace Industries (KAI) signed an agreement to initiate the serial production phase of the Light Armed Helicopters (LAH) program. This partnership marks a significant milestone, transitioning the project into large-scale manufacturing at KAI’s facility in Sacheon, South Korea.

In June 2023 , Safran Helicopter Engines and MTU Aero Engines signed a Memorandum of Understanding (MoU) to form a 50/50 joint venture focused on developing a new engine for the European Next Generation Rotorcraft Technologies (ENGRT) program. Backed by the European Defense Fund, ENGRT aims to drive innovation and lay the technological foundation for Europe’s next generation of military rotorcraft.

The global drone simulator market is experiencing rapid expansion, fueled by the growing integration of drones into a wide range of industries and the increasing necessity for trained, certified drone operators. These simulators offer a virtual environment that mimics real-world flight scenarios, enabling both novice and experienced pilots to develop skills without risking damage to expensive hardware.

Rising Demand Across Industries

The growing deployment of drones across sectors such as agriculture, logistics, construction, mining, insurance, and public safety has created a parallel demand for high-quality pilot training. Drone simulators serve as essential tools in this regard, offering scalable and cost-effective solutions that reduce operational risk while enhancing operator proficiency.

Meanwhile, military and defense organizations continue to lead in drone simulator adoption. Drones are now critical to modern warfare—used for intelligence gathering, reconnaissance, combat, and disaster response missions. Simulators provide defense personnel with hands-on training in high-stakes scenarios, enabling rapid decision-making and reducing the learning curve for complex unmanned aerial vehicle (UAV) operations.

Information Source:

https://www.fortunebusinessinsights.com/drone-simulator-market-108155

Technological Advancements Fuel Market Growth

Breakthroughs in augmented reality (AR) and virtual reality (VR) have transformed simulation technology, allowing immersive training experiences that replicate real-time flight dynamics. These advancements not only enhance learning outcomes but also reduce costs associated with live flight training programs.

The integration of mixed reality (MR) and AI-based analytics into simulation platforms is further boosting the effectiveness of these tools. In addition, the development of portable simulator systems is making training more accessible in field and remote environments.

Key Players in the Global Drone Simulator Market

- Garmin Ltd.

- Northrop Grumman Corporation

- BAE Systems

- Qualcomm Technologies

- Hexagon AB

- Novatel

- Raytheon Technologies

- WR Systems

- Saab

- Telespazio

- Thales Group

- Orolia Holding SAS

- Booz Allen Hamilton

- Safran

COVID-19 Accelerates Adoption

The COVID-19 pandemic served as a catalyst for the drone industry. Drones were used extensively for medical supply delivery, public surveillance, disinfection spraying, and remote monitoring during lockdowns. This unprecedented demand accelerated the need for certified operators and, consequently, for drone simulators. As a result, the simulator market witnessed a surge in interest from both public and private sectors during and post-pandemic.

Regional Outlook

North America is expected to maintain a leading position in the global drone simulator market through 2032. This growth is supported by substantial R&D investments and the presence of key players such as Raytheon Technologies , Northrop Grumman , and Garmin Ltd.

Asia Pacific , particularly India , China , and Japan , is poised for significant growth. Increased government spending on drone-based services in agriculture, defense, and transport is pushing demand for simulation-based training programs.

Key Industry Developments

-

In October 2022 , Israel-based Xtend secured a USD 9 million contract from the U.S. Pentagon to develop multi-payload drones integrated with autonomous features and simulator support.

-

In December 2022 , a USD 47.8 million deal between the U.S. and Lithuania was signed to supply Switchblade 600 drones, which includes simulator-based training.

- In May 2022 , Maryland-based ANRA Technologies partnered with Raytheon Intelligence and Space to provide SmartSkies simulation solutions for live drone flight operations.

Market Segmentation

The drone simulator market is segmented by:

- Component : Hardware, Software

- Technology : Augmented Reality (AR), Virtual Reality (VR)

- Drone Type : Fixed-Wing, Rotary Wing, Others

- System Type : Fixed, Portable

- Application : Commercial, Military

Outlook

Despite challenges such as high initial costs and complex regulatory landscapes , the drone simulator market is poised for robust growth between 2025 and 2032. As the global drone fleet continues to expand and industries increasingly adopt unmanned aerial technologies, simulation platforms will play an indispensable role in ensuring operational safety, regulatory compliance, and workforce readiness.

With advancements in immersive tech and growing investments across defense and commercial applications, drone simulators are set to become a cornerstone of UAV training ecosystems worldwide.