Category: Chemical and Materials

Solution Styrene Butadiene Rubber Market Size, Share, Growth, and Industry Analysis 2032

By Pallavi G, 2025-10-30

The Global Solution Styrene Butadiene Rubber Market has recently been analyzed and explored by Fortune Business Insights™ in their latest market research report. The team of dedicated analysts and researchers has gone to great lengths to provide a comprehensive overview of both current and future scenarios pertaining to the Solution Styrene Butadiene Rubber Market. As a result, this report is packed with valuable insights that will be highly advantageous for industry players looking to maintain a competitive edge.

The global solution styrene butadiene rubber market size was valued at USD 4.49 billion in 2022 and is projected to grow from USD 4.67 billion in 2023 to USD 6.25 billion by 2030, exhibiting a CAGR of 4.2% during the forecast period. Solution Styrene Butadiene Rubber (S-SBR) is a type of synthetic rubber extensively utilized in tire manufacturing and various rubber-based products. It is produced by polymerizing two primary monomers—styrene and butadiene—in a solution. By adjusting the ratio of these monomers and fine-tuning the polymerization process, manufacturers can tailor the rubber’s properties to meet specific performance requirements.

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/108707

Segmentation Analysis:

By Application Analysis:

The tires segment accounts for the largest share of the solution styrene butadiene rubber (S-SBR) market. S-SBR is widely utilized in the production of high-performance tires due to its superior viscoelasticity compared to other rubber types. Its unique physical structure provides exceptional tear strength, enhanced mechanical properties, and improved functional performance. These characteristics contribute to better braking efficiency and overall tire durability, while also offering cost-effectiveness—factors that drive the segment’s dominance.

The polymer modification segment also plays a key role in market expansion. Through advanced modification techniques, manufacturers can fine-tune the polymer structure of S-SBR to achieve specific performance attributes such as higher abrasion resistance, improved wet grip, and greater fuel efficiency. This ability to customize material properties makes S-SBR an increasingly preferred choice across industries, particularly in automotive tire production.

Market Drivers

- Increasing Automotive Production: Rapid growth in automotive manufacturing, especially in emerging economies, fuels the demand for high-performance tires.

- Stringent Environmental Regulations: Global initiatives to reduce carbon emissions have accelerated the adoption of fuel-efficient tire materials.

- Superior Material Properties: S-SBR offers excellent abrasion resistance, wet traction, and low rolling resistance, enhancing both safety and efficiency.

- R&D Investments: Continuous research in advanced polymerization techniques enhances S-SBR’s versatility and performance characteristics.

Market Restraints

- Fluctuating Raw Material Prices: Price volatility of butadiene and styrene affects production costs.

- High Production Costs: The complex polymerization process and technology requirements may limit adoption by smaller manufacturers.

- Availability of Alternatives: Competition from emulsion SBR (E-SBR) and natural rubber could restrain market growth in cost-sensitive regions.

Key Industry Development:

- August 2023 – Goodyear partnered with the German automotive manufacturer Opel to develop a custom-designed tire for the Opel Experimental concept car. This collaboration highlights Goodyear’s dedication to improving vehicle aerodynamics and achieving superior energy efficiency.

- May 2023 – ARLANXEO announced plans to build a state-of-the-art rubber production facility in Jubail, Saudi Arabia, with an annual capacity of 140 kilotons. The plant will manufacture two high-performance elastomers: Lithium Butadiene Rubber and ultra-high cis Polybutadiene.

Major Players Profiled in the Ferrovanadium Market Report:

- ARLANXEO (Netherlands)

- SIBUR (Russia)

- LG Chem (South Korea)

- The Goodyear Tire & Rubber Company (U.S.)

- Sinopec (China)

- JSR Corporation (Japan)

- Dynasol Group (Spain)

- Asahi Kasei Corporation (Tokyo)

- Sumitomo Chemical Asia Pte Ltd. (Japan)

- Trinseo (U.S.)

- Versalis (Italy)

What are the New Additions in Solution Styrene Butadiene Rubber Market Report?

Comprehensive Market Analysis : The 2023 report provides a detailed industry overview, analyzing key market trends, growth drivers, challenges, and opportunities. It covers various sectors within the industry and offers insights into market size, market share, and market segmentation.

Customization and Analyst Support : The report offers customized services and analyst support upon request. This may include tailored research, specific data requirements, or personalized insights based on the client's needs and preferences.

Recent Market Developments : The report incorporates the latest market developments that have occurred since the previous edition. It includes recent mergers and acquisitions, product launches, collaborations, regulatory changes, and other significant events shaping the industry landscape.

Futuristic Growth Opportunities : The report identifies and presents future growth opportunities in the industry. It explores emerging technologies, market trends, consumer preferences, and regulatory factors that are expected to drive growth and innovation in the coming years.

Get Your Customization Research Report:

https://www.fortunebusinessinsights.com/enquiry/customization/108707

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower, Baner - Mahalunge Road,

Baner, Pune-411045, Maharashtra, India.

Phone:

US: +18339092966

UK: +448085020280

APAC: +91 744 740 1245

Email: sales@fortunebusinessinsights.com

The global ferrovanadium market size was valued at USD 3.12 billion in 2024. The market is projected to grow from USD 3.25 billion in 2025 to USD 4.30 billion by 2032, exhibiting a CAGR of 4.1% during the forecast period. Fortune Business Insights™ has deep-dived these inputs in its latest research report titled, “ Ferrovanadium Market , 2025-2032 .”

The global ferrovanadium market is witnessing notable growth, driven by its critical role in steel manufacturing and the increasing demand for high-strength alloys across infrastructure, automotive, and aerospace sectors. Ferrovanadium (FeV) is a key alloying element that enhances steel’s strength, hardness, and resistance to corrosion and fatigue. The market expansion is further supported by the growing adoption of high-strength low-alloy (HSLA) steels in construction and energy industries.

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/ferrovanadium-market-114050

Report Coverage:

The report offers a comprehensive perspective of the market size, share, revenue, and volume. It has deep-dived into SWOT analysis. Quantitative and qualitative assessments have provided a holistic view of the market. The primary interviews validate assumptions, findings, and the prevailing business scenarios. The report also includes secondary resources such as annual reports, press releases, white papers, and journals.

Segmentation Analysis:

Which type segment dominates the global ferrovanadium market?

The FeV80 segment holds the largest share in the global ferrovanadium market. Its dominance is attributed to superior structural performance and high vanadium concentration. FeV80 is primarily used in high-strength low-alloy (HSLA) and micro-alloyed steels, which are essential in critical applications such as oil pipelines, construction-grade rebar, and automotive chassis. The high vanadium content allows manufacturers to achieve desired mechanical properties with minimal material addition, ensuring both cost-efficiency and enhanced product strength.

Which application segment leads the ferrovanadium market?

The steel manufacturing segment accounts for the majority share of the ferrovanadium market. Ferrovanadium is crucial in improving the strength, hardness, and fatigue resistance of various steel grades, including HSLA, tool, and spring steels. It enables the production of lighter yet more durable components and enhances grain refinement, which improves weldability, toughness, and overall performance. These characteristics make FeV indispensable in modern steelmaking processes.

Market Drivers:

What are the primary factors driving the growth of the ferrovanadium market?

a. Rising Demand from the Steel Manufacturing Sector:

The growing need for durable and high-strength steel in infrastructure development and industrial construction is a key growth driver. Ferrovanadium improves steel’s mechanical properties—such as toughness, ductility, and tensile strength—making it highly valuable in producing HSLA and tool steels for bridges, buildings, and pipelines.

b. Expansion of the Automotive and Aerospace Industries:

In the pursuit of lightweight and high-performance materials, the automotive and aerospace sectors are increasingly adopting ferrovanadium-alloyed steels. The alloy enhances strength while enabling weight reduction, which supports fuel efficiency and performance optimization.

c. Technological Advancements in Alloy Production:

Recent improvements in smelting and aluminothermic reduction technologies have enhanced production efficiency, lowered energy consumption, and improved purity levels. As a result, high-grade FeV alloys have become more accessible to end-use industries.

What are the key restraints impacting the ferrovanadium market?

a. Fluctuating Vanadium Prices:

Volatility in vanadium ore and raw material prices significantly affects production costs and profitability. This price instability can disrupt supply chains and limit long-term planning for ferrovanadium producers.

b. Environmental and Regulatory Challenges:

Stringent environmental regulations concerning mining activities and metal processing are likely to constrain production capacity expansion. Regions with strict emission standards may face higher compliance costs, impacting overall output.

Key Trends:

What are the emerging trends shaping the ferrovanadium market?

- Growing adoption of vanadium microalloying: Manufacturers are increasingly using small quantities of vanadium in steel production to achieve superior strength and flexibility in end products.

- Shift toward sustainable steel manufacturing: The industry is focusing on recycling vanadium-bearing materials and adopting eco-efficient production methods to reduce carbon emissions.

- Rising investments in renewable energy infrastructure: Expanding wind energy projects are driving demand for high-strength steels used in turbine towers and components, indirectly boosting ferrovanadium consumption.

Key Industry Development:

- March 2021: MG Vanadium announces the groundbreaking of a new spent catalyst recycling facility in Zanesville, Ohio. The new plant, a significant investment exceeding USD 200 million, will double AMG's spent catalyst recycling and ferroalloy production capacity.

Major Players Profiled in the Ferrovanadium Market Report:

- AMG (U.S.)

- Bear Metallurgical Company. (U.S.)

- Treibacher Industrie AG (Austria)

- Masterloy Products Company (Canada)

- Bushveld Minerals (South Africa)

- Hickman Williams & Company (U.S.)

- TAIYO KOKO Co.,Ltd. (Japan)

- (India)

- NTPF Etalon LTD (Russia)

- Arth Metallurgicals Pvt. Ltd. (India)

Inquire Before Buying This Research Report:

https://www.fortunebusinessinsights.com/enquiry/queries/ferrovanadium-market-114050

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Address:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower, Baner – Mahalunge Road,

Baner, Pune-411045, Maharashtra, India.

Phone:

US: +1 424 253 0390

UK: +44 2071 939123

APAC: +91 744 740 1245

The global plastics market size was valued at USD 524.48 billion in 2024. The market is projected to grow from USD 533.59 billion in 2025 to USD 754.23 billion by 2032, exhibiting a CAGR of 5.1% during the forecast period. Fortune Business Insights™ has deep-dived these inputs in its latest research report titled, “ Plastics Market , 2025-2032 .”

According to the study, synthetic material has gained considerable traction due to easy manufacturing, lightweight, low cost, and versatility. Amidst depleting sources of polymers, recyclable products could gain considerable traction globally. Notably, healthcare & pharmaceutical, automotive, and packaging sectors will exhibit stellar demand for sustainable packaging solutions.

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/plastics-market-102176

Segments:

What are the major types of plastics in the market?

The plastics market is segmented by type into polyethylene, polyethylene terephthalate (PET), polyvinyl chloride (PVC), polypropylene (PP), polyamide, acrylonitrile butadiene styrene (ABS), polycarbonate (PC), polyurethane (PU), polystyrene (PS), and others. Among these, polyethylene holds the largest market share of 23.3% in 2024, driven by its extensive use in packaging and automotive applications. Manufacturers prefer polyethylene for packaging because of its durability and strong moisture barrier properties, which help protect products effectively.

Which end-use industries are driving the demand for plastics?

By end-use industry, the plastics market is segmented into automotive & transportation, packaging, consumer goods/lifestyle, infrastructure & construction, healthcare & pharmaceutical, electrical & electronics, textile, and others. The packaging segment dominates the market with a 44.9% share in 2025 and is projected to grow at the highest CAGR during the forecast period. This growth is attributed to rising demand for rigid and flexible packaging solutions across personal care, food & beverage, and pharmaceutical sectors. Plastics are favored due to their versatility, cost-effectiveness, and durability, making them ideal for various packaging applications.

Drivers and Restraints:

What factors are driving the growth of the plastics market?

The market growth is fueled by the expanding footprint of engineering plastics, which offer superior mechanical and thermal properties. Increasing demand for metal substitution is another key driver, as industries shift toward lightweight and durable polymer solutions. Additionally, the food industry is witnessing higher adoption of plastics that prevent contamination and preserve product quality. Growing usage of plastics in fashion, sports, and toys further supports the market expansion.

What challenges could restrain the plastics market growth?

The major restraint to market growth is the stringent government regulations and plastic reduction policies aimed at minimizing environmental pollution. These initiatives could limit plastic production and usage, challenging market expansion.

Regional Insights:

Which region is expected to dominate the plastics market?

The Asia Pacific region is expected to remain the leading market during the forecast period, driven by abundant raw material availability and rapid growth in construction and packaging sectors. Countries such as China, India, and Australia are witnessing increasing demand for plastics in sports goods, textiles, and toys, attracting significant investments from major companies.

How is the North American plastics market performing?

In North America, especially the U.S., strong demand from healthcare, pharmaceuticals, automotive, and transportation sectors supports market growth. Furthermore, the rising adoption of recyclable plastics is reshaping the regional market as industries shift toward sustainable alternatives.

What is the outlook for the plastics market in the Middle East & Africa?

The Middle East & Africa region presents promising investment opportunities for plastic manufacturers and suppliers. Growth in packaging and textile industries, coupled with the trend toward lightweight packaging, is expected to fuel market expansion. Increasing polymer applications continue to strengthen investor confidence in the region.

Competitive Landscape:

Major Players Prioritize Collaboration to Tap into Markets

Prominent players could inject funds into mergers & acquisitions, product rollouts, technological advancements and R&D activities. Besides, major companies could invest in innovations and product offerings in the ensuing period.

Key Industry Development:

- November 2023 – LyondellBasell announced plans to build an advanced recycling plant in Germany, capable of processing 50,000 tons of plastic annually. The project, set for completion by 2050, aims to boost the company’s plastic segment revenue.

- July 2023 – Total Energies partnered with Plastic Energy to recycle plastic waste using TACOIL produced at Plastic Energy’s Spain facility, targeting over 15,000 tons of recycled plastic per year.

Major Players Profiled in the Plastics Market Report:

- LyondellBasell Industries N.V. (Netherlands)

- ExxonMobil Chemical (U.S.)

- China National Petroleum Corporation (China)

- INEOS (U.K.)

- China Petroleum & Chemical Corporation (China)

- SABIC (Saudi Arabia)

- Ducor Petrochemicals (Netherlands)

- Reliance Industries Limited (India)

- Formosa Plastic Group (Taiwan)

- Total S.A. (France)

- Braskem (Brazil)

- BASF SE (Germany)

- Repsol (Spain)

- Borouge (UAE)

- Borealis AG (Austria)

- MOL Group (Hungary)

- Beaulieu International Group (Belgium)

Inquire Before Buying This Research Report:

https://www.fortunebusinessinsights.com/enquiry/queries/plastics-market-102176

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Address:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower, Baner – Mahalunge Road,

Baner, Pune-411045, Maharashtra, India.

Phone:

US: +1 424 253 0390

UK: +44 2071 939123

APAC: +91 744 740 1245

Transformer Oil Market Size & Share Analysis, Key Players, and Forecast 2032

By Pallavi G, 2025-10-29

The global transformer oil market size was USD 2.97 billion in 2022. The market is slated to surge from USD 3.15 billion in 2023 to USD 4.88 billion by 2030, exhibiting a CAGR of 6.4% over the study period.

Transformer oils are used in numerous applications on account of several advantages. These applications comprise circuit breakers, rectifiers, distribution and power transformers, switch gears, and others. The rising electricity demand from numerous emerging sectors, such as the electric vehicles industry, is set to fuel industry expansion over the coming years.

Fortune Business Insights™ provides this information in its research report, titled “Transformer Oil Market, 2025-2032”.

Get a Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/transformer-oil-market-104024

Segmentation Analysis:

Which type of transformer oil dominates the market?

- The mineral oil segment (including naphthenic and paraffinic types) dominates the market.

- Reason: Mineral oil exhibits exceptional cooling and insulating properties, making it the most preferred choice in transformers.

- Its cost-effectiveness and high thermal stability further support its widespread adoption.

What is the leading application segment in the transformer oil market?

- The transformers segment accounts for the largest market share.

- Transformer oil is widely used for temperature regulation and insulation, ensuring smooth and reliable operation of transformers.

- The segment’s growth is fueled by the rising need for energy transmission stability across industrial and utility applications.

Which end-use segment holds a prominent position?

- The transmission & distribution (T&D) segment holds a key share of the market.

- The segment’s growth is driven by the increasing deployment of distribution transformers in residential and commercial infrastructures.

- Growing urbanization and power demand are accelerating investments in T&D networks globally.

How is the market segmented geographically?

- The market is analyzed across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Each region shows varying levels of transformer oil demand based on infrastructure development, grid modernization, and renewable energy projects.

Drivers and Restraints:

What key factors are driving the transformer oil market growth?

- Growing emphasis on ultra-high voltage (UHV) power transmission for long-distance electricity distribution.

- Rising renewable energy generation leading to a higher need for stable transmission networks.

- Ongoing grid modernization projects to improve transmission efficiency and reduce energy loss.

What are the major challenges restraining market expansion?

- Drawbacks associated with liquid-filled transformers, such as potential leakage and flammability risks, can limit market growth.

- Environmental concerns and regulatory restrictions on mineral oils may also hinder adoption, encouraging the shift toward bio-based alternatives.

Regional Insights:

Which region leads the transformer oil market?

- Asia Pacific dominates the global market, valued at USD 1.48 billion in 2022.

- Growth is driven by massive investments in grid network expansion across emerging economies like China and India.

- The region benefits from rapid industrialization and increasing energy consumption.

How is the European market performing?

- Europe holds a significant share, supported by replacement of aging grid infrastructure.

- Countries are focusing on sustainable and energy-efficient solutions, which enhances the demand for bio-based transformer oils.

Competitive Landscape:

How are companies strengthening their market presence?

- Key players such as Nynas AB and Cargill Inc. are introducing bio-based transformer oils to promote eco-friendly solutions.

- Companies are emphasizing organic growth strategies, including product innovations and regional expansions.

- Focus on green energy alignment and sustainability helps boost brand image and market share.

Report Coverage Overview:

What does the report include?

- Comprehensive analysis of the market dynamics, including drivers, restraints, and opportunities.

- Segmentation by type, application, end-use, and geography.

- Insight into strategic initiatives adopted by leading players to consolidate their global market position.

Key Industry Development:

- June 2023: M&I Materials Ltd. launched a new product in its range of ester transformer fluids. Through recycling of in-service fluid, the ester transformer fluid is derived, which makes it environment friendly.

- May 2023: Apar Industries Limited launched 99% biodegradable natural ester transformer oil. This strategic product launch would allow the company to compete against foreign companies in foreign markets such as the U.S., Germany and others.

List of Key Players Mentioned in the Report:

- Apar Industries Limited (India)

- Cargill (U.S.)

- Sinopec Corp (China)

- Nynas AB (Sweden)

- Total Energies (France)

- Dow (U.S.)

- Calumet Specialty Products Partners, L.P. (U.S.)

- Powerlink Oil Refinery Ltd (India)

- Wacker Chemie AG (Germany)

- HP Lubricants (India)

Inquire Before Buying Report

https://www.fortunebusinessinsights.com/enquiry/queries/transformer-oil-market-104024

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Address:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower, Baner –Mahalunge Road,

Baner, Pune-411045, Maharashtra, India.

Phone

US: +1 424 253 0390

UK: +44 2071 939123

APAC: +91 744 740 1245

Email : sales@fortunebusinessinsights.com

The global calcium carbide market size was valued at USD 16.00 billion in 2023 and is projected to grow from USD 16.75 billion in 2024 to USD 24.09 billion by 2032, exhibiting a CAGR of 4.6% during the forecast period. This information is provided by Fortune Business Insights , in its report, titled, “ Calcium Carbide Market, 2025-2032 .”

Calcium carbide (CaC₂) is primarily used to produce acetylene gas, which is further utilized in manufacturing polyvinyl chloride (PVC), calcium cyanamide, and other industrial products. It also finds applications in steelmaking for desulfurization, slag conditioning, and furnace injection. The growing demand for PVC-based plastics, along with the expansion of the chemical, steel, and agriculture industries, is driving market growth. Producing PVC from CaC₂ is considered efficient, as it eliminates dependence on petroleum and offers superior plasticizing properties.

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/calcium-carbide-market-101580

Segmentation Analysis:

What are the key segments of the calcium carbide market?

The calcium carbide market is segmented by application, end-user, and region.

- By application: acetylene gas, calcium cyanamide, reducing & dehydrating agents, steel making, and others.

- By end-user: chemicals, steel, and others.

The chemicals segment is projected to register a significant CAGR during the forecast period, driven by the increasing demand for acetylene and its derivatives from the pharmaceutical and plastics industries, and calcium cyanamide from the agriculture sector.

How is the market geographically divided?

Geographically, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

Drivers and Restraints:

What are the main drivers of the calcium carbide market?

The primary growth driver is the surging demand for acetylene and its derivatives, which are widely used in industries such as plastics, pharmaceuticals, dyes, and rubber. Acetylene derivatives also serve as raw materials in the production of polyurethane fibers and synthetic rubber, and are found in consumer goods like cosmetics, hair sprays, and sunscreens. Additionally, China’s strong PVC production based on acetylene further boosts product demand.

What are the major restraints affecting market growth?

One of the key restraints is the health hazard associated with calcium carbide exposure. Prolonged contact can be harmful, and its use in food treatment is particularly dangerous due to the presence of phosphorus and arsenic impurities, which generate acetylene gas upon contact with water.

Regional Insights:

Asia Pacific to Dominate Backed by Bolstering Production of Steel

Asia Pacific stood at USD 14.16 billion in 2021. The region is predicted to observe the highest calcium carbide market growth during the forecast period. The thriving chemical and steel manufacturing industry in the region is a prime driver of the market.

North America was responsible for a considerable calcium carbide market share in 2021 and is predicted to preserve its position as a pivotal market region during the forecast period owing to the augmented demand from chemical, steel, and industrial applications.

Europe is expected to record a substantial growth in the market. The surging demand for calcium cyanamide from the agricultural industry is likely to make impressive contribution to the growth of the market in the region.

Competitive Landscape:

Vital Business-associated Publications by Crucial Players to Sway Market Aspects

Prominent corporations in the market often make critical declarations concerning a few business happenings, which impacts the market either favorably or adversely. Companies procure other smaller firms, introduce novel products or technologies, involve in partnership contracts, sign important agreements with government establishments, and others.

List of Key Players Mentioned in the Report:

- Carbide Industries LLC (U.S.)

- APH - Regency Power Group (India)

- MCB Industries Sdn. Bhd. (Malaysia)

- KC Group (India)

- DCM Shriram Ltd. (India)

- AlzChem (Germany)

- Denka Company Limited (Japan)

- American Elements (U.S.)

- Inner Mongolia Baiyanhu Chemical Co., Ltd. China)

- Lonza (Switzerland)

- Mil-Spec Industries Corporation (U.S.)

- Xiahuayuan Xuguang Chemical (China)

- PT Emdeki Utama Tbk (Indonesia)

Get Your Customization Research Report:

https://www.fortunebusinessinsights.com/enquiry/ask-for-customization/calcium-carbide-market-101580

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Address:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower, Baner – Mahalunge Road,

Baner, Pune-411045, Maharashtra, India.

Phone

US: +18339092966

UK: +448085020280

APAC: +91 744 740 1245

Email : sales@fortunebusinessinsights.com

The global containerboard market size was valued at USD 132.88 billion in 2023 owing to the rising demand for sustainable packaging worldwide. Containerboards are paperboards used generally for packaging material due to their properties such as lightweight and paperweight, or high grammage. A recently published report by Fortune Business Insights™ titled, “ Containerboard Market Size, Share & Industry Analysis, By Material (Virgin, and Recycled), By End-User (Food & Beverage, Personal Care & Cosmetics, Industrial, and Others), and Regional Forecast, 2025-2032, ” offers a qualitative and quantitative analysis of the market. The global containerboard market size was valued at USD 138.87 billion in 2024. It is projected to be worth USD 141.43 billion in 2025 and reach USD 166.43 billion by 2032, exhibiting a CAGR of 2.35% during the forecast period.

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/containerboard-market-102801

What are the Highlights of the Report?

The report offers an extensive overview of the market and highlights the growth drivers, restraints, upcoming opportunities, and possible challenges of the market. It also discusses the table of segmentation based on factors such as material, end-user, and geography with the names of the leading segment and its attributed factors. It also lists the names of players operating in the market and the key strategies adopted by them. Furthermore, the report discusses significant industry developments, current trends prevalent in the market, and other interesting insights that will help investors to make financial and beneficial decisions in the market.

Market Drivers:

I ncreasing Demand from Pharmaceutical Industries to Boost Growth

With rapid industrialization, there is an increasing need for sustainable packaging from various sectors such as cosmetics, food and beverage, pharmaceutical, personal care, and others. This stands as a major factor in boosting the containerboard market growth. Besides this, the booming food and beverage sector with increasing popularity for ready-to-eat frozen food and convenient food would increase its productivity, thereby demanding more containerboards for package and shipment purposes. This will bode well for the market in the coming years.

On the contrary, regulatory impositions based on the use of nature-friendly resources for the production of containerboards may pose a major challenge for the market players, thereby hampering the overall market size. Nevertheless, the rapidly developing e-commerce industry would aid growth. Apart from that, the rising preference for product-specific corrugated boxes for safety concerns regarding external stress is likely to create lucrative growth opportunities for the market in the forthcoming years.

Segmentaion Analysis:

Which material segment dominates the containerboard market?

The recycled material segment dominates the containerboard market. Recycled containerboard is preferred for its sustainability, as it minimizes the need for virgin fibers—reducing deforestation and carbon emissions during production. With rising environmental awareness, both consumers and businesses are prioritizing recyclable and eco-friendly packaging solutions. Additionally, regulatory initiatives, such as the U.S. EPA’s goal to increase paper recycling rates, are driving the use of recycled paper in containerboard production.

Which end-use industry leads the containerboard market?

The food & beverage industry holds the largest share in the containerboard market. Containerboard provides excellent protection for a wide range of food items—from dry goods to perishables—while maintaining hygiene and durability during transport. Its moisture resistance and strength make it ideal for packaging food products. Moreover, the growing preference for sustainable and biodegradable packaging aligns with the eco-friendly characteristics of containerboard, as food brands aim to reduce their environmental impact.

Competitive Landscape:

Consolidated Nature of Market will Intensify Competition

The competitive landscape of the market is consolidated in nature with the presence of a bunch of players holding about 20% of the overall production capacity. These include Mondi Group, SCG Packaging Public Company Limited, DS Smith, Lee & Man Paper Manufacturing Ltd., and Smurfit Kappa. Major vendors are investing massively on the research and development of recyclable and water-resistant containerboard products to attract high revenue in the coming years. Besides this, the players are also engaging in collaborative efforts such as agreements and contracts, mergers and acquisitions, joint ventures, and others for gaining a competitive edge in the market.

List of Containerboard Market Manufacturers Include:

- Stora Enso

- Nine Dragons Paper (Holdings) Limited

- Hamburger Containerboard

- Georgia-Pacific LLC

- Rengo Co., Ltd.

- WestRock Company

- Oji Fibre Solutions (NZ) Ltd.

- International Paper

- Smurfit Kappa

- Lee & Man Paper Manufacturing Ltd.

- DS Smith

- SCG PACKAGING PUBLIC COMPANY LIMITED

- Mondi Group

- Other Players

Key Industry Development:

- January 2024: WestRock Company announced plans to build a new corrugated box plant in Pleasant Prairie, Wisconsin, to serve growing demand in the Great Lakes region. The company will close its North Chicago facility once construction is complete.

- May 2023: Smurfit Kappa completed the expansion of its Pruszków corrugated plant in Poland, making it the company’s largest and most advanced packaging facility in the country.

Get Your Customization Research Report:

https://www.fortunebusinessinsights.com/enquiry/ask-for-customization/containerboard-market-102801

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Address:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower, Baner – Mahalunge Road,

Baner, Pune-411045, Maharashtra, India.

Phone

US: +18339092966

UK: +448085020280

APAC: +91 744 740 1245

Email : sales@fortunebusinessinsights.com

The Global Semiconductor Gases Market has recently been analyzed and explored by Fortune Business Insights™ in their latest market research report. The team of dedicated analysts and researchers has gone to great lengths to provide a comprehensive overview of both current and future scenarios pertaining to the Semiconductor Gases Market. As a result, this report is packed with valuable insights that will be highly advantageous for industry players looking to maintain a competitive edge.

The report also highlights limiting factors and regional industrial presence that may impact market growth trends beyond the forecast period of 2032. The market research aims to gain a complete understanding of the industry's potential and provide information that will help companies to make informed decisions. The Semiconductor Gases Market Report is an impressive 100+ page document that includes a comprehensive table of contents, a list of figures, tables and graphs, as well as a comprehensive analysis.

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/104121

Forecast Growth Projected:

The global semiconductor gases market size was valued at USD 10.07 billion in 2023 and is projected to grow from USD 10.83 billion in 2024 to USD 19.34 billion by 2032, exhibiting a CAGR of 7.5% during the forecast period.

List of the Key Players in the Semiconductor Gases Market:

- Air Liquide (France)

- Air Products and Chemicals, Inc. (U.S.)

- Linde plc (U.K.)

- Solvay (Belgium)

- Iwatani Corporation (Japan)

- Messer Group (Germany)

- American Gas Products (U.S.)

- Electronic Fluorocarbons, LLC (U.S.)

- SUMITOMO SEIKA CHEMICALS CO.,LTD. (Japan)

- Taiyo Nippon Sanso JFP Corporation (Japan)

- SHOWA DENKO K.K. (Japan)

Segmentation Analysis:

Which product segment dominated the electronic gases market in 2023?

The electronic special gas segment dominated the market in 2023. These gases, such as nitrogen fluoride, are specifically produced for the electronics manufacturing industry. With the shift toward advanced semiconductors smaller than 5 micrometers, the demand for high-precision gases and chemicals is rising. This growing need for high-density semiconductor chips is driving demand for electronic special gases.

What are the main application segments of the electronic gases market, and which segment held the major share?

The market is segmented into Memory , Logic , and Others . The logic segment held the largest market share, as logic chips act as the core processors in electronic devices such as CPUs, GPUs, and NPUs. With rapid advancements in AI, IoT, and 5G technologies that require high computational power, demand for logic chips—and consequently electronic gases—is expected to grow significantly in the coming years.

Market Drivers:

- Rising Demand for Advanced Semiconductors: Growing use of miniaturized chips (<5 nm) in smartphones, wearables, and automotive electronics is increasing the consumption of high-purity specialty gases.

- Expansion of Semiconductor Fabrication Facilities: Significant investments by major chip manufacturers such as TSMC, Samsung, and Intel are creating strong demand for semiconductor gases globally.

- Technological Advancements in AI and 5G: Rapid adoption of AI-enabled devices, IoT networks, and 5G infrastructure is fueling the need for complex semiconductor components, supporting market growth.

- Supportive Government Initiatives: Incentives and funding for semiconductor manufacturing, especially in the U.S., South Korea, Japan, and India, are boosting local gas production and supply chains.

Market Restraints:

- High Cost of Specialty Gases and Purification: Maintaining gas purity standards and storage infrastructure involves high costs, which can limit adoption among smaller fabs.

- Environmental and Safety Concerns: Some semiconductor process gases, such as perfluorocarbons, have high global warming potential, leading to regulatory restrictions.

Key Industry Development:

- July 2022 – Iwatani Corporation partnered with Helious Specialty Gases, making Helious the first company in India with three helium transfill facilities. The move aims to strengthen Helious’ position as a key helium supplier to major OEMs.

- July 2022 – SK Materials and Showa Denko signed an MoU to collaborate on producing high-purity specialty gases for semiconductor manufacturing. The companies plan to establish a production facility in the U.S. to meet growing semiconductor demand.

Get Your Customization Research Report:

https://www.fortunebusinessinsights.com/enquiry/customization/104121

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower,

Baner - Mahalunge Road, Baner,

Pune-411045, Maharashtra, India.

Phone:

US: +18339092966

UK: +448085020280

APAC: +91 744 740 1245

Email: sales@fortunebusinessinsights.com

The global conformal coatings market size was valued at USD 992.1 million in 2023 and is projected to grow from USD 1,047.1 million in 2024 to USD 1,647.9 million by 2032, exhibiting a CAGR of 5.8% during the forecast period. Robust adoption of the electric automotive sector and increasing miniaturization trends are likely to foster the industry’s growth. Fortune Business Insights ™ presents this information in its report titled “ Conformal Coatings Market, 2025-2032. ”

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/conformal-coatings-market-102867

Segmentation Analysis:

Acrylic Segment to Lead Owing to Strong Adoption from the Electronic Manufacturing Industry

By product, the market is segmented into acrylic, epoxy, urethane, silicone, parylene, and others. The acrylic segment is expected to dominate, owing to robust demand from the electronic manufacturing industry.

Consumer Electronics Segment to Lead Owing to Strong Demand for Miniaturized Electronic Applications

As per end-use industry, the market is classified into automotive, medical, aerospace & defense, consumer electronics, and others. The consumer electronics segment may dominate due to increasing demand for miniaturized electronic applications.

Regionally, the market is grouped into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

Drivers and Restraints

Strong Demand from Consumer Electronics Industry to Foster Market Growth

Conformal coatings are polymer-based materials applied on PCB. It is a thin layer that protects several products at hand. The increasing demand for conformal coatings from the consumer electronics industry may bolster the product adoption. Further, the extensive adoption of coatings from automotive, consumer electronics, and other industries may bolster the product adoption. Also, the rising implementation of novel technologies such as Artificial Intelligence (AI) and Machine Learning (ML) is anticipated to drive the conformal coatings market growth.

However, strict environmental regulations by governments may hinder the industry’s progress.

Get Your Customization Research Report:

https://www.fortunebusinessinsights.com/enquiry/customization/conformal-coatings-market-102867

Regional Insights

Robust Demand from the Electronics Manufacturing Industry to Fuel Market Growth in Asia Pacific

Asia Pacific is expected to dominate the conformal coatings market share due to robust demand from the electronics manufacturing industry. The market in Asia Pacific is expected to touch USD 767.3 million in 2021 and is likely to gain a huge portion of the global market share in the coming years.

In North America, the robust demand for electric vehicles is likely to foster the product adoption. Furthermore, the rising adoption of electronics in hybrid and electric vehicles is likely to foster the market’s progress in the upcoming years.

In Europe, the increasing product adoption from the automotive sector is expected to foster the industry’s growth.

Competitive Landscape

Major Players Devise Novel Product Launches to Enhance their Brand Image

The prominent companies operating in the market announce novel products to boost their brand image. For example, Electrolube introduced its novel UV Cure Coating Xtra (UVCLX) in October 2021. The product is developed by utilizing organic content sourced from renewable means. This strategy may enable the company to boost its brand image globally. Furthermore, key players deploy research and development, mergers, expansions, acquisitions, and expansions to elevate their market position.

Key Industry Development

-

March 2022 – HumiSeal launched its UV500-2 conformal coating, offering enhanced PCB protection and improved performance under thermal and mechanical stress, ideal for automotive and white goods applications.

-

April 2022 – Shin-Etsu Silicones of America introduced the MR-COAT-01F and 02F conformal coating series, featuring high hardness, excellent elongation, and superior abrasion resistance to minimize stress on PCB components.

List of Key Players Profiled in Conformal Coatings Market Report

- Chemtronics (South Korea)

- Henkel AG & Company (Germany)

- Shin-Etsu Chemical Co., Ltd (Japan)

- Dow (U.S.)

- Chase Corporation (U.S.)

- Dymax Corporation (S.)

- Specialty Coating Systems (U.S.)

- Electrolube (K.)

- B. Fuller (U.S.)

- G. Chemicals (Canada)

Inquire Before Buying Report:

https://www.fortunebusinessinsights.com/enquiry/queries/conformal-coatings-market-102867

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Address:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower, Baner –

Mahalunge Road, Baner, Pune-411045,

Maharashtra, India.

Phone:

US: +1 424 253 0390

UK: +44 2071 939123

APAC: +91 744 740 1245

mailto:sales@fortunebusinessinsights.com

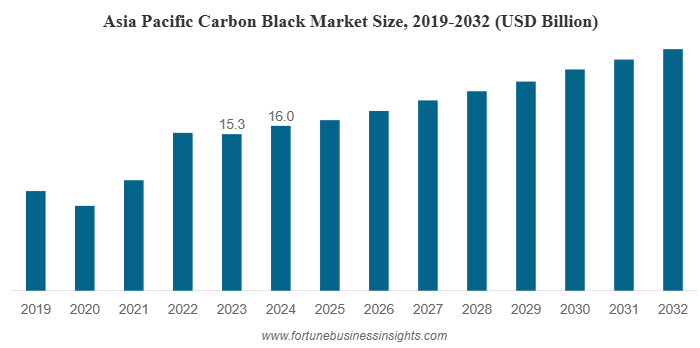

The global carbon black market size was valued at USD 27.44 billion in 2023 and is projected to grow from USD 28.76 billion in 2024 to USD 41.28 billion by 2032, exhibiting a CAGR of 4.6% during the forecast period. The rise is driven by the increasing deployment of the product in tire manufacturing and the growing plastic demand for automotive, consumer goods, and electronics industries.

Fortune Business Insights™ provides this information in its research report, titled “Carbon Black Market, 2025-2032”.

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/carbon-black-market-101718

Segmentation Analysis:

Furnace Black Segment to Lead Due to Rising Demand from Rubber Manufacturers

Based on process type, the market is segmented into acetylene black, furnace black, thermal black, and others.

- The furnace black segment is expected to dominate the market with a notable CAGR during the forecast period.

- This dominance is attributed to the increasing use of furnace black as a strengthening agent by rubber manufacturers across the globe.

Q: Why is the furnace black segment leading the carbon black market?

A: Furnace black is widely preferred by rubber manufacturers because it enhances product strength and performance, making it ideal for use in tire and industrial rubber applications.

Standard Grade Segment to Grow Rapidly with Expanding Industrial Use

By grade, the market is bifurcated into standard grade and specialty grade.

- The standard grade segment is projected to grow significantly over the analysis period.

- This growth is driven by the rising adoption of standard-grade carbon black in diverse industrial applications, including plastics, coatings, and rubber products.

Q: What factors are fueling the demand for standard-grade carbon black?

A: Its versatility and cost-effectiveness make it a preferred material across various industries, particularly in manufacturing and construction sectors.

Tire Segment to Dominate Supported by Automotive Industry Growth

On the basis of application, the market is divided into tire, non-tire rubber, inks & toners, plastics, and others.

- The tire segment is projected to hold the largest market share and register robust growth.

- The surge is primarily driven by the rapid expansion of the automotive industry and the increasing production of vehicles worldwide.

Q: How does the automotive industry influence the carbon black market?

A: The growing global automotive production directly boosts the demand for carbon black, as it is a key component in tire manufacturing to improve durability and performance.

Drivers and Restraints:

Expansion of the Rubber Industry to Propel Market Growth

- Rising demand from consumer goods, electronics, construction, and automotive sectors is driving the rubber industry’s growth.

- This expansion, in turn, amplifies the need for carbon black, particularly as a reinforcing material in rubber-based products.

Q: What is the main growth driver for the carbon black market?

A: The growing rubber and automotive industries are the primary catalysts, as carbon black is a critical input in tire and rubber product manufacturing.

Restraint – Environmental Concerns May Hinder Growth

- The production process of carbon black releases hazardous gases, which pose environmental challenges.

- Stricter emission regulations could potentially limit production expansion and impact overall market growth.

Q: What is the major challenge facing the carbon black market?

A: Environmental concerns related to carbon emissions during production remain a key restraint for manufacturers.

Regional Insights:

Asia Pacific to Lead the Global Market

- The Asia Pacific region is anticipated to register strong growth and dominate the global carbon black market.

- This is attributed to the high demand from the tire and plastic manufacturing industries, particularly in China, India, and Japan.

North America to Record Steady Growth

- The North American market is expected to grow at a healthy pace due to increasing product utilization in vibration isolation devices and rubber-based industrial goods.

Q: Which region holds the largest share of the carbon black market?

A: Asia Pacific remains the dominant region owing to large-scale tire manufacturing and expanding industrial applications.

Q: What drives carbon black demand in North America?

A: The growing automotive aftermarket and rising use of carbon black in vibration control products and industrial rubber applications are key drivers.

Key Industry Development:

- May 2023 : Orion Engineered Carbons increased its gas black production capacity in Germany, reinforcing its position as a leading player in the specialty carbon black market.

- December 2022 : International CSRC Investment Holdings Co., Ltd announced a short-term (2022–2024) investment plan focused on research and development to produce advanced specialty carbon blacks, including antistatic, static dissipative, and conductive grades. This strategic initiative aims to enhance the company’s global market share.

List of Key Players Mentioned in the Report:

- Birla Carbon Thailand Public Co. Ltd. (Thailand)

- Cabot Corporation (U.S.)

- Orion Engineered Carbons SA (Germany)

- Phillips Carbon Black Limited (India)

- CSRC Group (Taiwan)

- Omsk Carbon Group (Germany)

- OCI COMPANY Ltd. (South Korea)

- Himadri Speciality Chemicals Ltd. (India)

- Longxing Chemical Industry Co., Ltd. (China)

- Mitsubishi Chemical Holdings Corporation (Japan)

Get Your Customization Research Report:

https://www.fortunebusinessinsights.com/enquiry/ask-for-customization/carbon-black-market-101718

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Address:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower, Baner –

Mahalunge Road, Baner, Pune-411045,

Maharashtra, India.

Phone

US: +18339092966

UK: +448085020280

APAC: +91 744 740 1245

The global ceramic inks market size was valued at USD 2.60 billion in 2023. The market is projected to grow from USD 2.79 billion in 2024 to USD 4.86 billion by 2032 at a CAGR of 7.3% during the forecast period. The market growth is primarily driven by the rising building and construction activities worldwide. Ceramic inks are widely utilized in ceramic tile printing for flooring and wall applications, glass printing for interior and exterior architectural designs, and printing on food containers to enhance visual appeal. Additionally, the growing adoption of ceramic inks in the automotive sector is anticipated to further boost market expansion during the forecast period.

Moreover, the rapid growth of the food, beverage, cosmetics, and packaging industries is expected to support market demand. The COVID-19 pandemic initially disrupted operations in China, where the government temporarily shut down several chemical manufacturing facilities in early 2020. Despite these restrictions, China’s ink industry demonstrated resilience throughout the pandemic. In contrast, ink manufacturers across Europe faced reduced supplies of key raw materials such as ethanol and n-propanol, as reported by the British Coatings Federation (BCF).

Get a Free Sample PDF Brochure:

https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/105521

Segmentation Analysis:

By Product Type: In 2023, the decorative inks segment dominated the global ceramic inks market. Ceramic inks are widely used in glass printing, ceramic tile printing, and food container printing. They are available in a broad spectrum of colors and shades, including black, white, blue, brown, maroon, red, and more, with purple, blue, and brown pigments seeing particularly high demand. Decorative inks are especially popular for ceramic tile applications, as they enhance the appearance of ceramics, glass, metal, and tiles.

By Technology: The digital printing segment held the largest share of the market in 2023. The industry is increasingly transitioning from analog to digital printing technology due to its efficiency and flexibility. Digital printing enables ceramic decorators to produce short runs, reduce inventory costs, and quickly respond to changing design trends. This technology allows rapid adaptation to evolving market demands and customer preferences, making it a preferred choice for ceramic ink applications.

By Application: The market is segmented into ceramic tiles, glass printing, food container printing, and others. Among these, ceramic tiles accounted for a significant share in 2023. Ceramic inks are widely used for printing decorative patterns on tiles used in homes and bathrooms. These inks are highly durable and resistant to water and other liquids, making them ideal for ceramic tile applications. Additionally, ceramic inks are increasingly being adopted for glass decoration, providing an effective alternative for enhancing the visual appeal of glass products.

Market Dynamics:

Trends:

- Increasing preference for digital printing technology over analog methods due to short-run printing capabilities and faster adaptation to design changes.

- Rising demand for eco-friendly inks, including water-based solutions that reduce emissions and odours.

- Expansion of color options, particularly purple, blue, and brown pigments, for enhanced decorative appeal.

Drivers:

- Growth in construction and real estate sectors, boosting demand for ceramic tiles and glass decoration.

- Rising adoption of ceramic inks in automotive and consumer packaging industries.

- Increasing focus on sustainability and reduced environmental impact by ink manufacturers.

List of Key Companies Profiled:

- Ferro Corporation (Ohio, U.S.)

- Torrecid Group (Castellón, Spain)

- ZSCHIMMER & SCHWARZ CHEMIE GMBH (Lahnstein, Germany)

- LAURIER ARCHITECTURAL (Quebec Canada)

- Megacolor Ceramic Products (Castellón, Spain)

- BASF SE (Ludwigshafen, Germany)

- FRITTA (Comunidad Valenciana, Spain)

- Colorobbia Holding S.p.A (Gujarat, India)

- Esmalglass-Itaca Grupo (Castellón, Spain)

- Chromaline (Minnesota, U.S.)

- Electronics for Imaging, Inc. (California, U.S.)

- sedak GmbH & Co. KG (Gersthofen, Germany)

- SOLUTEC GLASS (Biscay, Spain)

- Sun Chemical (New Jersey, U.S.)

Key Industry Development:

- June 2024 - The company unveiled its HCR inkjet inks, featuring three new intense colours: Yellow, Blue, and Beige. These inks enhance printing quality and offer more uniform tones, expanding the colour range for ceramic digital printing.

- January 2025 - Torrecid launched ECOINKCID, a water-based ink that reduces organic carbon emissions and odours by 85%. Additionally, their 2LOWINKCID inks achieve a 30% reduction in organic carbon emissions and a 75% decrease in odours, emphasizing their commitment to environmental sustainability.

Get Your Customization Research Report:

https://www.fortunebusinessinsights.com/enquiry/customization/105521

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights Pvt. Ltd.

9th Floor, Icon Tower,

Baner - Mahalunge Road, Baner,

Pune-411045, Maharashtra, India.

Phone:

US: +18339092966

UK: +448085020280

APAC: +91 744 740 1245

Email: sales@fortunebusinessinsights.com