Light Weapons Market Growth, Insights, Segmentation and Forecast, 2024–2032

By Rishika19, 2025-09-25

According to Fortune Business Insights™, the global Light Weapons Market is anticipated to record significant growth in the coming years, reaching an estimated value of USD 25.61 billion. The market is forecast to expand at a compound annual growth rate (CAGR) of 5.6% over the period 2024-2032.

The report on the Light Weapons Market provides an in-depth assessment of the current industry landscape as well as future opportunities. It examines crucial aspects including market size, emerging trends, growth drivers, restraints, and potential opportunities. Furthermore, the study evaluates consumer behavior, regional developments, demand dynamics, and technological advancements. These insights are designed to support businesses, investors, and stakeholders in identifying profitable opportunities, formulating strategic decisions, and effectively addressing market challenges.

Latest Trends in the Light Weapons Market

The global Light Weapons Market is undergoing significant transformation, fueled by rapid technological advancements, evolving customer expectations, and shifting global dynamics. A key development is the accelerated adoption of digital technologies and automation, which enable organizations to streamline operations, improve efficiency, and lower operational costs.

Sustainability has emerged as a central focus, with leading companies investing in eco-friendly solutions such as energy-efficient systems, green manufacturing practices, and sustainable supply chains. At the same time, the integration of artificial intelligence (AI), machine learning (ML), and advanced analytics is revolutionizing decision-making, enhancing productivity, and enabling data-driven solutions across the industry.

The market is also seeing rising demand for product customization and enhanced user experiences, prompting businesses to innovate in design and deliver tailored offerings. In addition, the rapid expansion of e-commerce and digital platforms is reshaping customer engagement strategies, allowing deeper market penetration and opening new avenues for growth and differentiation in the Light Weapons Market.

Key Companies

The global Light Weapons Market is characterized by the presence of several leading companies that significantly influence the competitive landscape. These players focus on continuous product innovation, strategic collaborations, mergers and acquisitions, and international expansion to reinforce their market positions.

Some of the prominent companies operating in the market include:

- ARSENAL (Bulgaria)

- BAE Systems (The U.K)

- FN HERSTAL (Belgium)

- General Dynamics Corporation (The U.S.)

- Heckler & Koch GmbH (Germany)

- Lockheed Martin Corporation (The U.S.)

- Northrop Grumman Corporation (The U.S.)

- Raytheon Technologies Corporation (The U.S.)

- Rheinmetall AG (Germany)

- Saab AB (Sweden)

- Thales Group (France)

These key players are expected to remain instrumental in shaping the industry’s future by advancing technologies, setting new benchmarks, and driving the overall growth and transformation of the Light Weapons Market in the years ahead.

Information Source:

https://www.fortunebusinessinsights.com/light-weapons-market-103529

Report Scope

This report offers a comprehensive analysis of the Light Weapons Market, delivering actionable insights for businesses, investors, policymakers, and other stakeholders. It provides an in-depth evaluation of market size, growth trajectories, key drivers, challenges, and emerging opportunities that are shaping the industry’s future.

The study encompasses detailed market segmentation by product type, application, end-user, and region, enabling a granular perspective on different market segments. Additionally, it examines the competitive landscape by profiling leading companies, analyzing their strategies, and highlighting recent innovations, mergers, acquisitions, and partnerships.

With its broad coverage, the report equips stakeholders with a clear understanding of market dynamics, supporting informed decision-making, effective strategic planning, and sustainable long-term growth initiatives.

Driving Factors

The growth of the Light Weapons Market is being fueled by a combination of influential factors that are driving demand and fostering innovation. Key drivers include rapid technological advancements, shifting consumer preferences, and the increasing adoption of products and solutions across multiple industries.

Rising investments, supportive government initiatives, and growing disposable incomes are further accelerating market expansion. At the same time, evolving lifestyle trends and heightened awareness of sustainability are pushing companies to prioritize eco-friendly innovations, energy-efficient systems, and smarter product designs.

In addition, organizations are ramping up research and development (R&D) efforts to deliver advanced solutions, improve performance, and enhance user experiences—further strengthening market competitiveness. Collectively, these factors are expected to sustain growth momentum and open up new opportunities within the Light Weapons Market over the forecast period.

Market Segmentation

The Light Weapons Market is segmented to provide a detailed understanding of the industry landscape, based on key parameters such as product type, application, end-user, and region. This structured segmentation enables the identification of emerging trends, growth opportunities, and challenges within each category, supporting more informed strategic decisions for stakeholders.

By Type (Heavy machine guns, MANPAT, Infantry Mortar, Anti-Tank Weapons, Recoilless Rifles, Launchers, Light Cannon, Anti-Tank Missiles, MANPADS, Grenade, Landmines), Guidance (Guided, Unguided), Application (Defense, Homeland Security), and Regional Forecast, 2024-2032

Regional Insights

Regional segmentation highlights how the market performs across different geographies, analyzing consumer behavior, investment patterns, and regulatory environments that shape market growth. The key regions covered include:

North America – Comprising the United States and Canada, this region leads with strong innovation, advanced technology adoption, and significant R&D investments.

Europe – Including Germany, the U.K., France, and other major economies, the region emphasizes industrial modernization, sustainability initiatives, and stringent regulatory frameworks.

Asia Pacific – Covering high-growth economies such as China, India, Japan, South Korea, and Southeast Asia, the region benefits from a vast consumer base, expanding digital infrastructure, and robust manufacturing capacity.

Latin America – Encompassing markets such as Brazil, Mexico, and Argentina, where infrastructure development, industrial expansion, and rising economic growth are driving demand.

Middle East & Africa – Featuring markets like GCC countries and South Africa, with increasing investments in energy, defense, construction, and smart technologies fueling market expansion.

According to Fortune Business Insights™, the global Remote Towers Market is anticipated to record significant growth in the coming years, reaching an estimated value of USD 727.60 million. The market is forecast to expand at a compound annual growth rate (CAGR) of 25% over the period 2024-2032.

The report on the Remote Towers Market provides an in-depth assessment of the current industry landscape as well as future opportunities. It examines crucial aspects including market size, emerging trends, growth drivers, restraints, and potential opportunities. Furthermore, the study evaluates consumer behavior, regional developments, demand dynamics, and technological advancements. These insights are designed to support businesses, investors, and stakeholders in identifying profitable opportunities, formulating strategic decisions, and effectively addressing market challenges.

Information Source:

https://www.fortunebusinessinsights.com/remote-towers-market-102523

Latest Trends in the Remote Towers Market

The global Remote Towers Market is undergoing significant transformation, fueled by rapid technological advancements, evolving customer expectations, and shifting global dynamics. A key development is the accelerated adoption of digital technologies and automation, which enable organizations to streamline operations, improve efficiency, and lower operational costs.

Sustainability has emerged as a central focus, with leading companies investing in eco-friendly solutions such as energy-efficient systems, green manufacturing practices, and sustainable supply chains. At the same time, the integration of artificial intelligence (AI), machine learning (ML), and advanced analytics is revolutionizing decision-making, enhancing productivity, and enabling data-driven solutions across the industry.

The market is also seeing rising demand for product customization and enhanced user experiences, prompting businesses to innovate in design and deliver tailored offerings. In addition, the rapid expansion of e-commerce and digital platforms is reshaping customer engagement strategies, allowing deeper market penetration and opening new avenues for growth and differentiation in the Remote Towers Market.

Key Companies

The global Remote Towers Market is characterized by the presence of several leading companies that significantly influence the competitive landscape. These players focus on continuous product innovation, strategic collaborations, mergers and acquisitions, and international expansion to reinforce their market positions.

Some of the prominent companies operating in the market include:

- Frequentis Group

- Saab Group

- Searidge Technologies

- Indra Systems

- Avinor

- Thales Group

- Harris Corporation

- Indra Navia AS

- Leonard Martin Corporation

- Raytheon Corporation

These key players are expected to remain instrumental in shaping the industry’s future by advancing technologies, setting new benchmarks, and driving the overall growth and transformation of the Remote Towers Market in the years ahead.

Report Scope

This report offers a comprehensive analysis of the Remote Towers Market, delivering actionable insights for businesses, investors, policymakers, and other stakeholders. It provides an in-depth evaluation of market size, growth trajectories, key drivers, challenges, and emerging opportunities that are shaping the industry’s future.

The study encompasses detailed market segmentation by product type, application, end-user, and region, enabling a granular perspective on different market segments. Additionally, it examines the competitive landscape by profiling leading companies, analyzing their strategies, and highlighting recent innovations, mergers, acquisitions, and partnerships.

With its broad coverage, the report equips stakeholders with a clear understanding of market dynamics, supporting informed decision-making, effective strategic planning, and sustainable long-term growth initiatives.

Driving Factors

The growth of the Remote Towers Market is being fueled by a combination of influential factors that are driving demand and fostering innovation. Key drivers include rapid technological advancements, shifting consumer preferences, and the increasing adoption of products and solutions across multiple industries.

Rising investments, supportive government initiatives, and growing disposable incomes are further accelerating market expansion. At the same time, evolving lifestyle trends and heightened awareness of sustainability are pushing companies to prioritize eco-friendly innovations, energy-efficient systems, and smarter product designs.

In addition, organizations are ramping up research and development (R&D) efforts to deliver advanced solutions, improve performance, and enhance user experiences—further strengthening market competitiveness. Collectively, these factors are expected to sustain growth momentum and open up new opportunities within the Remote Towers Market over the forecast period.

Market Segmentation

The Remote Towers Market is segmented to provide a detailed understanding of the industry landscape, based on key parameters such as product type, application, end-user, and region. This structured segmentation enables the identification of emerging trends, growth opportunities, and challenges within each category, supporting more informed strategic decisions for stakeholders.

By Operation Type (Single Multiple and Contingency), By System Type (Airport Equipment, Remote Towers Modules, Network Solutions), By Application (Communication, Information & Control, Surveillance, Visualization), and Regional Forecast,2024-2032

Regional Insights

Regional segmentation highlights how the market performs across different geographies, analyzing consumer behavior, investment patterns, and regulatory environments that shape market growth. The key regions covered include:

North America – Comprising the United States and Canada, this region leads with strong innovation, advanced technology adoption, and significant R&D investments.

Europe – Including Germany, the U.K., France, and other major economies, the region emphasizes industrial modernization, sustainability initiatives, and stringent regulatory frameworks.

Asia Pacific – Covering high-growth economies such as China, India, Japan, South Korea, and Southeast Asia, the region benefits from a vast consumer base, expanding digital infrastructure, and robust manufacturing capacity.

Latin America – Encompassing markets such as Brazil, Mexico, and Argentina, where infrastructure development, industrial expansion, and rising economic growth are driving demand.

Middle East & Africa – Featuring markets like GCC countries and South Africa, with increasing investments in energy, defense, construction, and smart technologies fueling market expansion.

US Small Caliber Ammunition Market Growth, Developments, Dynamics and Forecast, 2032

By Rishika19, 2025-09-25

According to Fortune Business Insights™, the global US Small Caliber Ammunition Market is anticipated to record significant growth in the coming years, reaching an estimated value of USD 4431.28 Million. The market is forecast to expand at a compound annual growth rate (CAGR) of 5% over the period 2024-2032.

According to Fortune Business Insights™, the global US Small Caliber Ammunition Market is anticipated to record significant growth in the coming years, reaching an estimated value of USD 4431.28 Million. The market is forecast to expand at a compound annual growth rate (CAGR) of 5% over the period 2024-2032.

The report on the US Small Caliber Ammunition Market provides an in-depth assessment of the current industry landscape as well as future opportunities. It examines crucial aspects including market size, emerging trends, growth drivers, restraints, and potential opportunities. Furthermore, the study evaluates consumer behavior, regional developments, demand dynamics, and technological advancements. These insights are designed to support businesses, investors, and stakeholders in identifying profitable opportunities, formulating strategic decisions, and effectively addressing market challenges.

Information Source:

https://www.fortunebusinessinsights.com/industry-reports/u-s-small-caliber-ammunition-market-101915

Latest Trends in the US Small Caliber Ammunition Market

The global US Small Caliber Ammunition Market is undergoing significant transformation, fueled by rapid technological advancements, evolving customer expectations, and shifting global dynamics. A key development is the accelerated adoption of digital technologies and automation, which enable organizations to streamline operations, improve efficiency, and lower operational costs.

Sustainability has emerged as a central focus, with leading companies investing in eco-friendly solutions such as energy-efficient systems, green manufacturing practices, and sustainable supply chains. At the same time, the integration of artificial intelligence (AI), machine learning (ML), and advanced analytics is revolutionizing decision-making, enhancing productivity, and enabling data-driven solutions across the industry.

The market is also seeing rising demand for product customization and enhanced user experiences, prompting businesses to innovate in design and deliver tailored offerings. In addition, the rapid expansion of e-commerce and digital platforms is reshaping customer engagement strategies, allowing deeper market penetration and opening new avenues for growth and differentiation in the US Small Caliber Ammunition Market.

Key Companies

The global US Small Caliber Ammunition Market is characterized by the presence of several leading companies that significantly influence the competitive landscape. These players focus on continuous product innovation, strategic collaborations, mergers and acquisitions, and international expansion to reinforce their market positions.

Some of the prominent companies operating in the market include:

- Denel SOC Ltd

- Remington Arms Company, LLC.

- RAUG Group

- Olin Corporation

- Aguila Ammunition

- Sellier & Ballot

- PPU USA Ammo

- Barnaul Ammunition

- MESKO

- Hornady

- Wolf Performance Ammunition

- VISTA OUTDOOR OPERATIONS LLC.

- FIOCCHI MUNIZIONI SPA

- Nammo AS

- MAST Technology, Inc

These key players are expected to remain instrumental in shaping the industry’s future by advancing technologies, setting new benchmarks, and driving the overall growth and transformation of the US Small Caliber Ammunition Market in the years ahead.

Report Scope

This report offers a comprehensive analysis of the US Small Caliber Ammunition Market, delivering actionable insights for businesses, investors, policymakers, and other stakeholders. It provides an in-depth evaluation of market size, growth trajectories, key drivers, challenges, and emerging opportunities that are shaping the industry’s future.

The study encompasses detailed market segmentation by product type, application, end-user, and region, enabling a granular perspective on different market segments. Additionally, it examines the competitive landscape by profiling leading companies, analyzing their strategies, and highlighting recent innovations, mergers, acquisitions, and partnerships.

With its broad coverage, the report equips stakeholders with a clear understanding of market dynamics, supporting informed decision-making, effective strategic planning, and sustainable long-term growth initiatives.

Driving Factors

The growth of the US Small Caliber Ammunition Market is being fueled by a combination of influential factors that are driving demand and fostering innovation. Key drivers include rapid technological advancements, shifting consumer preferences, and the increasing adoption of products and solutions across multiple industries.

Rising investments, supportive government initiatives, and growing disposable incomes are further accelerating market expansion. At the same time, evolving lifestyle trends and heightened awareness of sustainability are pushing companies to prioritize eco-friendly innovations, energy-efficient systems, and smarter product designs.

In addition, organizations are ramping up research and development (R&D) efforts to deliver advanced solutions, improve performance, and enhance user experiences—further strengthening market competitiveness. Collectively, these factors are expected to sustain growth momentum and open up new opportunities within the US Small Caliber Ammunition Market over the forecast period.

Market Segmentation

The US Small Caliber Ammunition Market is segmented to provide a detailed understanding of the industry landscape, based on key parameters such as product type, application, end-user, and region. This structured segmentation enables the identification of emerging trends, growth opportunities, and challenges within each category, supporting more informed strategic decisions for stakeholders.

By Caliber (22 LR, 223 Remington, 308 Winchester, 9mm Luger, 357 Magnum, 45 Auto/ACP, 380 ACP, 40 S&W, 38 Special, 30-06 Springfield, and Others), Casing Type (Brass, Steel, Brass-coated Steel), Bullet Type (Lead, Copper, Brass, and Others), Distribution Channel (Online Stores, Retail Stores (Large Outlets, Shooting Ranges, and Local/ Niche Shops)), and Regional Forecast, 2024-2032

Regional Insights

Regional segmentation highlights how the market performs across different geographies, analyzing consumer behavior, investment patterns, and regulatory environments that shape market growth. The key regions covered include:

North America – Comprising the United States and Canada, this region leads with strong innovation, advanced technology adoption, and significant R&D investments.

Europe – Including Germany, the U.K., France, and other major economies, the region emphasizes industrial modernization, sustainability initiatives, and stringent regulatory frameworks.

Asia Pacific – Covering high-growth economies such as China, India, Japan, South Korea, and Southeast Asia, the region benefits from a vast consumer base, expanding digital infrastructure, and robust manufacturing capacity.

Latin America – Encompassing markets such as Brazil, Mexico, and Argentina, where infrastructure development, industrial expansion, and rising economic growth are driving demand.

Middle East & Africa – Featuring markets like GCC countries and South Africa, with increasing investments in energy, defense, construction, and smart technologies fueling market expansion.

According to Fortune Business Insights™, the global Push-To-Talk Market is anticipated to record significant growth in the coming years, reaching an estimated value of USD 46.75 billion. The market is forecast to expand at a compound annual growth rate (CAGR) of 12% over the period 2020-2032.

The report on the Push-To-Talk Market provides an in-depth assessment of the current industry landscape as well as future opportunities. It examines crucial aspects including market size, emerging trends, growth drivers, restraints, and potential opportunities. Furthermore, the study evaluates consumer behavior, regional developments, demand dynamics, and technological advancements. These insights are designed to support businesses, investors, and stakeholders in identifying profitable opportunities, formulating strategic decisions, and effectively addressing market challenges.

Information Source:

https://www.fortunebusinessinsights.com/industry-reports/push-to-talk-market-100079

Latest Trends in the Push-To-Talk Market

The global Push-To-Talk Market is undergoing significant transformation, fueled by rapid technological advancements, evolving customer expectations, and shifting global dynamics. A key development is the accelerated adoption of digital technologies and automation, which enable organizations to streamline operations, improve efficiency, and lower operational costs.

Sustainability has emerged as a central focus, with leading companies investing in eco-friendly solutions such as energy-efficient systems, green manufacturing practices, and sustainable supply chains. At the same time, the integration of artificial intelligence (AI), machine learning (ML), and advanced analytics is revolutionizing decision-making, enhancing productivity, and enabling data-driven solutions across the industry.

The market is also seeing rising demand for product customization and enhanced user experiences, prompting businesses to innovate in design and deliver tailored offerings. In addition, the rapid expansion of e-commerce and digital platforms is reshaping customer engagement strategies, allowing deeper market penetration and opening new avenues for growth and differentiation in the Push-To-Talk Market.

Key Companies

The global Push-To-Talk Market is characterized by the presence of several leading companies that significantly influence the competitive landscape. These players focus on continuous product innovation, strategic collaborations, mergers and acquisitions, and international expansion to reinforce their market positions.

Some of the prominent companies operating in the market include:

- Motorola Solutions Inc. (US)

- Zebra Technologies Corporation (US)

- AT&T Intellectual Property (US)

- Verizon Wireless (US)

- Qualcomm Technologies, Inc. (US)

- Harris Corporation (US)

- ICOM Inc. (Japan)

- Kyocera

- Siyata Mobile (Canada)

- ECOM Instruments GmbH (US)

- RugGear (US)

- Telefonaktiebolaget LM Ericsson (Sweden)

- Sonim Technologies (US)

- Simoco (India)

- Airbus DS Communications (US)

These key players are expected to remain instrumental in shaping the industry’s future by advancing technologies, setting new benchmarks, and driving the overall growth and transformation of the Push-To-Talk Market in the years ahead.

Report Scope

This report offers a comprehensive analysis of the Push-To-Talk Market, delivering actionable insights for businesses, investors, policymakers, and other stakeholders. It provides an in-depth evaluation of market size, growth trajectories, key drivers, challenges, and emerging opportunities that are shaping the industry’s future.

The study encompasses detailed market segmentation by product type, application, end-user, and region, enabling a granular perspective on different market segments. Additionally, it examines the competitive landscape by profiling leading companies, analyzing their strategies, and highlighting recent innovations, mergers, acquisitions, and partnerships.

With its broad coverage, the report equips stakeholders with a clear understanding of market dynamics, supporting informed decision-making, effective strategic planning, and sustainable long-term growth initiatives.

Driving Factors

The growth of the Push-To-Talk Market is being fueled by a combination of influential factors that are driving demand and fostering innovation. Key drivers include rapid technological advancements, shifting consumer preferences, and the increasing adoption of products and solutions across multiple industries.

Rising investments, supportive government initiatives, and growing disposable incomes are further accelerating market expansion. At the same time, evolving lifestyle trends and heightened awareness of sustainability are pushing companies to prioritize eco-friendly innovations, energy-efficient systems, and smarter product designs.

In addition, organizations are ramping up research and development (R&D) efforts to deliver advanced solutions, improve performance, and enhance user experiences—further strengthening market competitiveness. Collectively, these factors are expected to sustain growth momentum and open up new opportunities within the Push-To-Talk Market over the forecast period.

Market Segmentation

The Push-To-Talk Market is segmented to provide a detailed understanding of the industry landscape, based on key parameters such as product type, application, end-user, and region. This structured segmentation enables the identification of emerging trends, growth opportunities, and challenges within each category, supporting more informed strategic decisions for stakeholders.

By Component (Devices, Software, and Services), By Network Type (Push-to-talk over Cellular (PoC), and Land Mobile Radio (LMR)), By Enterprise Size (SMEs, and Large Enterprises), By Sector (Public Safety & Security, Government & Defense, Transportation & Logistics, Energy & Utility, Travel & Hospitality, and Others (Manufacturing, Construction, etc.)) and Regional Forecast, 2020-2032

Regional Insights

Regional segmentation highlights how the market performs across different geographies, analyzing consumer behavior, investment patterns, and regulatory environments that shape market growth. The key regions covered include:

North America – Comprising the United States and Canada, this region leads with strong innovation, advanced technology adoption, and significant R&D investments.

Europe – Including Germany, the U.K., France, and other major economies, the region emphasizes industrial modernization, sustainability initiatives, and stringent regulatory frameworks.

Asia Pacific – Covering high-growth economies such as China, India, Japan, South Korea, and Southeast Asia, the region benefits from a vast consumer base, expanding digital infrastructure, and robust manufacturing capacity.

Latin America – Encompassing markets such as Brazil, Mexico, and Argentina, where infrastructure development, industrial expansion, and rising economic growth are driving demand.

Middle East & Africa – Featuring markets like GCC countries and South Africa, with increasing investments in energy, defense, construction, and smart technologies fueling market expansion.

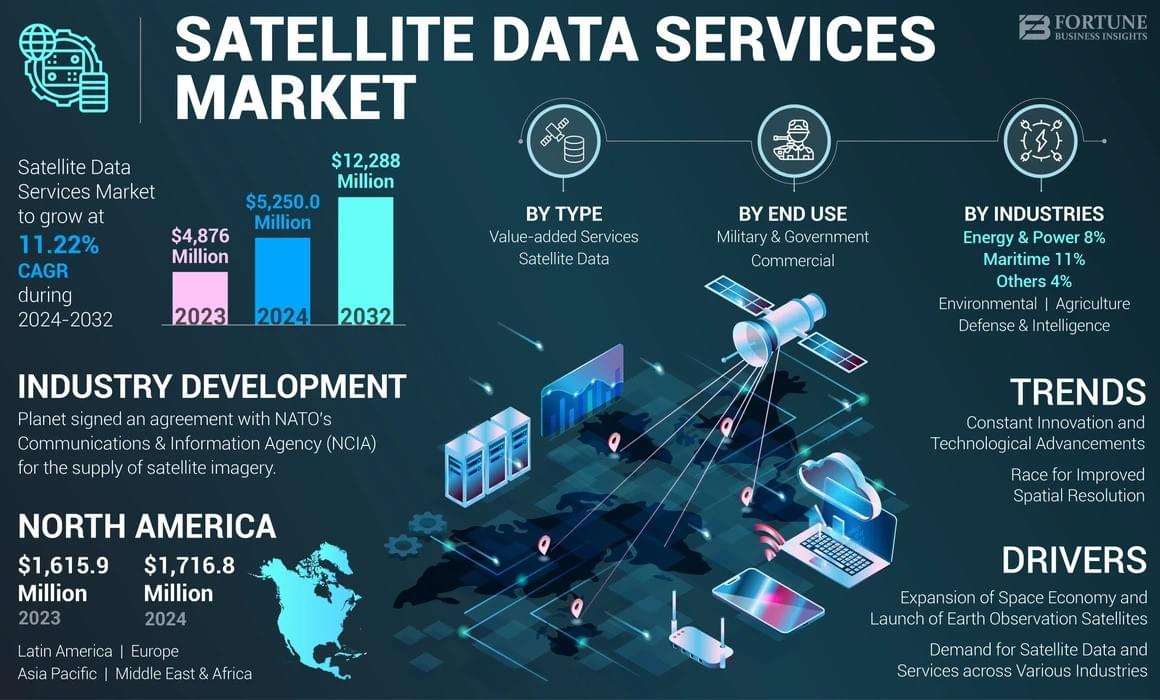

Satellite Data Services Market Size, Share, Segmentation and Forecast, 2024–2032

By Rishika19, 2025-09-24

The satellite data services market is entering a transformative phase, driven by rapid innovation, rising demand for Earth observation, and the growing space economy. From agriculture and defense to disaster management and urban planning, industries are increasingly turning to satellite data for accurate, real-time insights.

According to Fortune Business Insights™, the global satellite data services market was valued at USD 4.87 billion in 2023, is set to reach USD 5.25 billion in 2024, and is projected to expand to USD 12.29 billion by 2032 at a CAGR of 11.22%. North America led the market in 2023, holding 35.21% share, fueled by strong government programs, NASA’s initiatives, and the presence of key players such as Maxar, Planet Labs, and BlackSky.

What are Satellite Data Services?

Satellite data—often called satellite imagery—refers to information captured by satellites in orbit. The main purpose is Earth Observation (EO), which helps monitor climate change, weather patterns, land use, and urban expansion. Two main methods power this data:

Passive remote sensing – relying on natural light sources like the Sun.

Active remote sensing – using radar waves to capture Earth-reflected signals.

Applications are vast, ranging from environmental monitoring, precision farming, and urban planning to defense surveillance and disaster management.

Market Growth Drivers

1. Expansion of the Space Economy

The global space economy is set to hit USD 1.8 trillion by 2035, with Earth observation emerging as a fast-growing segment. Investments in new EO satellites with advanced sensors are fueling demand for higher-resolution and multi-spectral data.

2. Rising Industry Adoption

Agriculture : Boosting crop yields through precision farming and real-time monitoring.

Defense : Enhancing surveillance and reconnaissance capabilities, especially amid ongoing geopolitical conflicts like the Russia-Ukraine war.

Environment : Tracking natural disasters, land use changes, and climate-related risks.

3. Technological Innovations

Companies are rapidly integrating hyperspectral imaging, radar, and RF data into their services. For example, Maxar partnered with Umbra for Synthetic Aperture Radar (SAR) data, while Planet Labs introduced AI-powered analytics to boost spatial resolution up to 10x improvements.

Key Market Trends

Race for Higher Resolution : New entrants like Albedo and EOI Space aim for ultra-high 10 cm resolution, while established leaders like Maxar and Airbus target 15–25 cm imagery.

AI & Data Analytics : AI-driven platforms are transforming raw imagery into actionable insights. Planet Labs’ Planet Insights Platform combines EO datasets with analytics for faster decision-making.

Government-Private Partnerships : Programs like NASA’s Commercial Smallsat Data Acquisition (CSDA) and NATO’s APSS highlight the growing role of private players in global security and monitoring efforts.

Information Source:

https://www.fortunebusinessinsights.com/satellite-data-services-market-108359

Regional Insights

North America : Largest market (USD 1.72 billion in 2023) supported by NASA, DoD, and private sector innovation.

Europe : Strong collaborations under ESA and sustainability projects like the European Green Deal.

Asia Pacific : Fastest-growing, led by China and India investing in EO satellites for disaster response, agriculture, and security.

Latin America & Middle East/Africa : Growing adoption in environmental and maritime monitoring.

Key Industry Players

Leading companies are focusing on M&A, partnerships, and new product launches to stay ahead:

ICEYE (U.K.) – SAR data solutions.

Planet Labs (U.S.) – high-resolution optical imaging and analytics.

Capella Space (U.S.) – SAR-based monitoring.

Maxar Technologies (U.S.) – EO intelligence solutions.

Airbus (Netherlands) – advanced commercial satellite imagery.

BlackSky (U.S.) – AI-powered geospatial intelligence.

Spire Global, EOS Data Analytics, L3Harris Technologies among others.

Challenges Facing the Market

High Capital Investment : Building and launching satellites involves millions in costs, creating entry barriers for startups.

Data Management Complexity : With more satellites generating vast datasets, managing and analyzing information at scale is a growing challenge.

Geopolitical Tensions : While conflicts drive demand for surveillance data, regulatory restrictions may impact global market collaboration.

Outlook and Future Opportunities

The satellite data services market is set for robust expansion with the convergence of AI, big data analytics, and next-gen satellites. With governments, defense agencies, and commercial industries relying more heavily on EO, the market will see deeper penetration into agriculture, climate monitoring, and disaster response.

The trend toward high-resolution, multi-sensor intelligence solutions positions satellite data services as a critical enabler of global decision-making in the coming decade.

KEY INDUSTRY DEVELOPMENTS

In September 2024, ICEYE secured a five-year contract with NASA under its Commercial Smallsat Data Acquisition (CSDA) Program. The indefinite-delivery/indefinite-quantity (IDIQ) agreement enables ICEYE to supply Synthetic Aperture Radar (SAR) data, which will support NASA’s Earth Science Division in advancing scientific research, analysis, and application objectives.

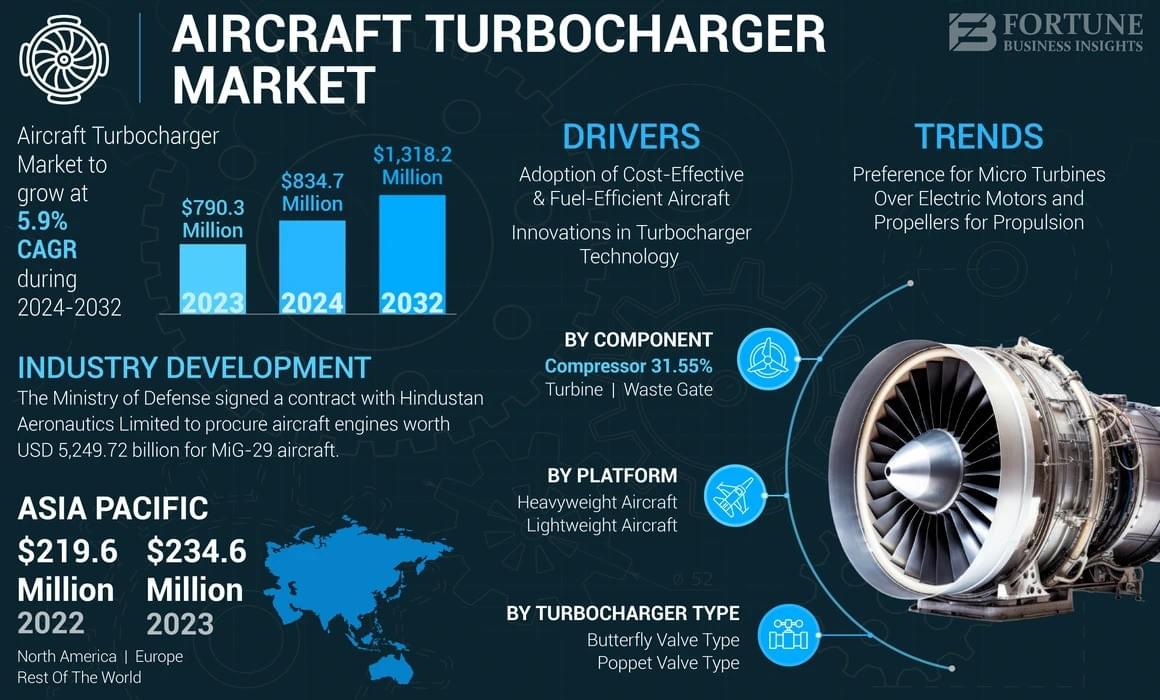

The aircraft turbocharger market is witnessing strong growth as the aviation industry prioritizes fuel efficiency, performance, and sustainable operations. Valued at USD 790.3 million in 2023, the market is expected to expand from USD 834.7 million in 2024 to USD 1,318.2 million by 2032, reflecting a healthy CAGR of 5.9% over the forecast period.

Asia Pacific led the global market in 2023 with a 29.68% share, driven by booming civil aviation, military modernization, and investments in advanced aircraft propulsion systems.

What is an Aircraft Turbocharger?

An aircraft turbocharger is a forced induction device that harnesses exhaust gas energy to compress intake air, ensuring more oxygen enters the combustion chamber. This process boosts engine performance, particularly at high altitudes, where reduced air density often hampers efficiency. Turbochargers allow piston engines to maintain near sea-level performance up to a critical altitude, making them indispensable in modern aviation.

Key Market Highlights

2023 Market Size: USD 790.3 million

2024 Estimate: USD 834.7 million

2032 Projection: USD 1,318.2 million

CAGR (2024–2032): 5.9%

Leading Region: Asia Pacific (29.68% share in 2023)

Market Trends

Shift Towards Micro Turbines

Growing interest in micro turbines over electric motors and propellers is reshaping aviation propulsion. Unlike electric systems that face battery limitations, micro turbines deliver higher power, quicker refueling, and extended endurance. For example, FusionFlight’s AB6 JetQuad, powered by four micro-turbines, represents the next step in drone propulsion for emergency and monitoring applications.

Technological Advancements in Turbochargers

Innovations such as intercooled turbochargers and electric turbochargers (E-Turbos) are improving thrust, responsiveness, and fuel efficiency. E-Turbos, powered by electric motors, address turbo lag and can cut NOx emissions by up to 20%, making them essential in meeting stringent environmental regulations.

Growth Drivers

Rising demand for cost- and fuel-efficient aircraft across commercial and defense aviation.

Fleet modernization programs in Asia Pacific, North America, and Europe.

Increasing defense budgets fueling demand for high-performance propulsion systems.

Sustainability initiatives pushing airlines to adopt cleaner and efficient technologies.

Restraints

Long engine lifespans reduce the frequency of turbocharger replacements.

Aircraft production backlogs continue to delay new deliveries, slowing market expansion.

Information Source:

https://www.fortunebusinessinsights.com/aircraft-turbocharger-market-111198

Segmentation Overview

By Platform

Heavyweight Aircraft: Largest share, fueled by demand for high-efficiency engines in commercial and defense aviation.

Lightweight Aircraft: Growing adoption in general aviation and UAVs.

By Turbocharger Type

Butterfly Valve Type: Leading and fastest-growing segment, favored for its reliability, low maintenance, and cost-effectiveness.

Poppet Valve Type: Rising demand driven by eco-friendly and efficient technologies.

By Component

Turbine: Dominant segment due to rapid innovations and adoption in both commercial and defense aircraft.

Compressor & Waste Gate: Significant growth supported by expanding aviation traffic and engine modernization.

Regional Insights

Asia Pacific: Largest market, led by China and India, driven by rapid aviation growth and military modernization.

North America: Strong growth expected with technological advancements and presence of industry leaders like Honeywell and GE Aviation.

Europe: Demand fueled by strict emission norms and adoption of next-gen turbochargers.

Middle East & Latin America: Moderate growth from fleet modernization and aviation development projects.

Key Players

Prominent companies shaping the aircraft turbocharger market include:

Honeywell International Inc. (U.S.)

General Electric Company (U.S.)

BorgWarner Inc. (U.S.)

Hartzell Engine Technologies LLC (U.S.)

ABB Ltd. (Switzerland)

Kawasaki Heavy Industries Ltd. (Japan)

PBS Group A.S. (Czech Republic)

Rajay Parts LLC (U.S.)

Victor Aviation Service Inc. (U.S.)

Airmark Overhaul Inc. (U.S.)

These players focus on advanced designs, hybrid propulsion integration, and long-term partnerships with airlines and defense organizations.

Recent Developments

March 2024: Indian Ministry of Defense signed a major contract with Hindustan Aeronautics Limited (HAL) for MiG-29 engine procurement and localization.

January 2024: Rolls-Royce entered a 7-year agreement with Azad Engineering (India) to manufacture military engine components.

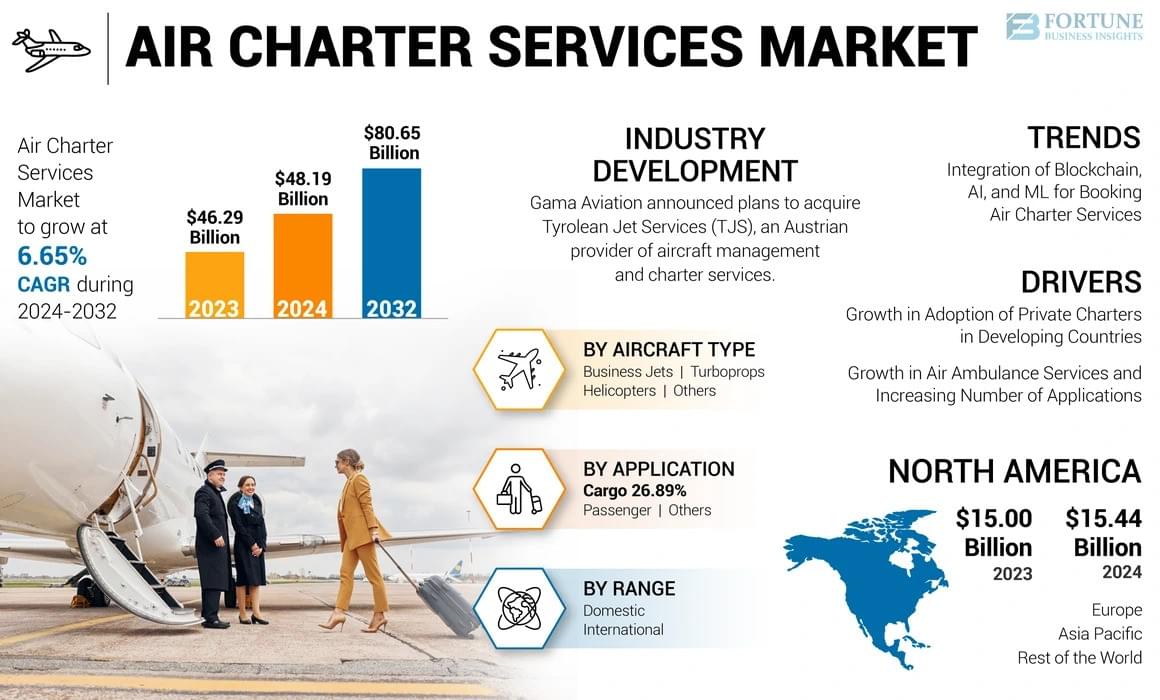

Air Charter Services Market Drivers, Restraints, Challenges and Opportunities, 2024–2032

By Rishika19, 2025-09-24

The global air charter services market is soaring, driven by growing demand for luxury travel, corporate mobility, and air ambulance operations. Valued at USD 46.29 billion in 2023, the sector is projected to expand from USD 48.19 billion in 2024 to an impressive USD 80.65 billion by 2032, at a steady CAGR of 6.65% (2025–2032).

North America continues to dominate with 33.35% market share in 2023, backed by a strong presence of major players and increasing adoption of private charters for both business and leisure travel.

Global Market Highlights

2024 Market Size : USD 48.19 billion

2025 Market Size : USD 51.39 billion

2032 Forecast Size : USD 80.65 billion

CAGR : 6.65% (2025–2032)

What’s Driving Growth?

Rise of High-Net-Worth Individuals (HNWIs): Customized, luxury travel experiences continue to fuel private charter demand.

Air Ambulances on the Rise: Growing medical emergencies and disaster relief operations are boosting demand for critical air transport.

Tech-Driven Travel: Integration of AI, ML, and blockchain in booking systems enhances efficiency, personalization, and payment security.

Corporate Mobility & Events: From site visits to destination weddings, air charters are becoming the go-to choice for convenience and speed.

Information Source:

https://www.fortunebusinessinsights.com/air-charter-service-market-108388

Market Segmentation Insights

By Aircraft Type

Business Jets: This segment holds the largest market share, driven by strong demand for MRO services, cabin refurbishments, and premium in-flight experiences. Business jets remain the preferred choice for corporate executives and high-net-worth individuals due to their speed, comfort, and flexibility.

Helicopters: Widely utilized across industries such as oil & gas, pilgrimage, and emergency rescue services, helicopters are gaining traction for their ability to operate in remote and hard-to-reach areas. Their role in medical evacuations and short-distance travel is fueling growth.

Turboprops & Others: Known for their fuel efficiency and lower operating costs, turboprops and other small aircraft are increasingly adopted for regional routes and cost-effective operations. These aircraft are particularly valuable for short-haul flights and underserved destinations.

By Application

Passenger Services: This is the leading application segment, supported by rising demand for corporate and luxury travel. Growing per capita income and the need for flexible mobility solutions have strengthened passenger charter adoption globally.

Others (Air Ambulance, Air Taxi): This segment is the fastest-growing, as governments and private operators expand medical transport and on-demand air mobility services. The rising importance of air ambulances during emergencies is a key growth driver.

Cargo: Playing a vital role in logistics, the cargo charter segment supports time-critical and specialized transport needs. From high-value goods to urgent deliveries, cargo charters provide unmatched flexibility and reliability.

Regional Outlook

North America – USD 15.44 billion market size (2023); led by U.S. private jet adoption and corporate mobility.

Europe – Driven by luxury tourism, destination weddings, and new eco-efficient aircraft designs.

Asia Pacific – Fastest growth; rising disposable income in China & India, government support for air ambulances.

Middle East & Africa – Oil & gas, remote connectivity, and luxury tourism fueling expansion.

Key Players Reshaping the Market

NetJets (U.S.)

Air Charter Service Pvt. Ltd. (U.K.)

Gama Aviation (U.K.)

Air Partner (U.K.)

Delta Private Jets (U.S.)

Flexjet LLC (U.S.)

Jet Aviation AG (Switzerland)

GlobeAir AG (Austria)

Recent Developments:

Aug 2024 : Air Charter Service opened a new Dublin office, expanding its global footprint.

Feb 2024 : NetJets announced takeover of Signature Aviation South FBO terminal to better serve fractional aircraft owners.

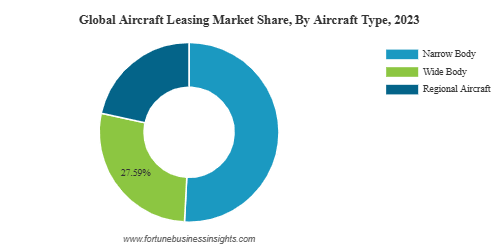

The global aircraft leasing market was valued at USD 172.88 billion in 2023 and is projected to grow from USD 183.23 billion in 2024 to USD 401.67 billion by 2032, exhibiting a CAGR of 11.1% during the forecast period. Europe led the market in 2023 with a 50.32% share, driven by the dominance of leasing companies in Ireland and the rising adoption of leasing models by low-cost carriers (LCCs).

Aircraft leasing offers airlines the flexibility to operate without the financial burden of purchasing aircraft. Lessors purchase aircraft and lease them to operators in return for periodic payments, providing airlines with liquidity, fleet consistency, and capacity flexibility. Leasing is typically short-term (not exceeding 10 years), after which the aircraft is returned to the lessor.

Key Market Insights

- 2023 Market Size : USD 172.88 billion

- 2024 Market Size : USD 183.23 billion

- 2032 Forecast Market Size : USD 401.67 billion

- CAGR (2024–2032) : 11.1%

- Leading Region (2023) : Europe (50.32% share)

Growth Drivers

1. Expansion of Low-Cost Carriers (LCCs)

The rapid expansion of low-cost carriers is a key driver. LCCs typically lease most of their fleets to minimize operational costs and increase route coverage. With rising domestic air travel, budget airlines are connecting regional and rural markets, significantly boosting leasing demand.

2. Rising Passenger Air Traffic

Global passenger traffic reached 6.8 billion in 2022, with approximately 400 commercial departures per hour worldwide. This surge in air travel has encouraged both new and established airlines to lease aircraft for efficient fleet management and cash flow optimization.

3. Financial Liquidity and Cash Flow Agility

Leasing enables airlines to reduce debt and maintain liquidity. The sale-and-leaseback model, where lessors purchase aircraft ordered by airlines and lease them back, has gained momentum and strengthens airline balance sheets.

Restraining Factors

- Lack of Modern Airport Infrastructure : Many developing regions face challenges in providing sufficient storage, parking, and maintenance facilities for leased aircraft.

- Regional Imbalances : Market dominance remains concentrated in Europe and North America due to favorable tax policies and established lessors, while emerging economies face expansion limitations.

Market Trends

- Fleet Modernization & Green Aviation : Leasing companies and airlines are investing in next-generation, fuel-efficient aircraft and adopting Sustainable Aviation Fuel (SAF). IATA reported SAF production of 300 million liters in 2022, triple the 2021 levels.

- Government Initiatives : Governments are supporting leasing hubs to strengthen the aviation sector. For example, India introduced IFSC tax exemptions in 2023 to encourage domestic aircraft leasing.

- Post-COVID Resilience : Lessors provided cash flow relief to airlines during the pandemic, reducing airline failures and reinforcing the role of leasing in aviation stability.

Information Source:

https://www.fortunebusinessinsights.com/aircraft-leasing-market-107476

Segmentation Analysis

By Aircraft Type Analysis

Narrow Body Segment – Market Dominance by Budget Airlines

The narrow body segment is estimated to be the largest in 2023, driven by strong demand from budget airlines and low-cost carriers (LCCs). Full-service airlines are also expanding their narrow-body fleets as next-generation aircraft can now cover longer routes. Despite pandemic impacts, airlines continue to place bulk orders, highlighting resilient demand.

Example : In February 2024, Airbus SE awarded an Indian company a manufacturing contract for its A220 narrow-body aircraft doors under the “Make in India” program, announced by India’s Civil Aviation Minister.

Wide Body Segment – Growth from International Air Traffic

The wide body segment is expected to witness significant growth due to increasing international passenger traffic. Modern wide-body aircraft can now fly over 15 hours continuously with improved fuel efficiency. Given the high cost of purchasing such aircraft, airlines prefer leasing to maintain cash flow and reduce operating costs.

Example : Lease rentals for a Boeing 777-300 ER or Boeing 777-200 LR stand at about USD 1.2 million per month, compared to a purchase price of USD 279 million. Over a 10-year lease, airlines pay nearly half the purchase cost, making leasing highly economical. The segment is expected to account for 27.59% market share in 2023.

By Lease Type Analysis

Dry Lease Segment – Substantial Growth from Cost Advantages

The dry lease segment is projected to witness substantial growth as it offers low maintenance and operational costs. In this model, the lessor provides only the aircraft, while the lessee handles crew, insurance, and maintenance, giving airlines complete cost control. Widely adopted by LCCs, dry leasing is increasingly being embraced by larger airlines as well. This growing trend has also created new job opportunities in the aviation sector.

Wet Lease Segment – Moderate Growth from Seasonal Demand

The wet lease segment is anticipated to grow moderately due to limited adoption. Here, the leasing company provides not only the aircraft but also the crew, insurance, and maintenance. Airlines opt for wet leasing during peak passenger traffic seasons when they lack resources to rapidly expand operations. Although it offers quick scalability, the lack of full operational control makes it less preferred than dry leasing.

Regional Insights

- Europe : Dominated the market in 2023 (USD 87.0 billion), supported by Ireland’s favorable tax regime and the presence of leading lessors such as AerCap and Avolon.

- North America : Moderate growth expected; Boeing Capital Corporation drives regional leasing activity.

- Asia Pacific : Fastest-growing region, led by China and India, supported by rapid aviation expansion and government-backed leasing initiatives.

- Middle East & Rest of World : Strong leasing demand from carriers like Emirates and Qatar Airways for long-haul wide-body aircraft.

Competitive Landscape

The market is moderately consolidated, with Ireland dominating global leasing activity. Key players focus on fleet expansion, strategic acquisitions, and next-gen aircraft procurement.

Key Companies:

- AerCap (Ireland)

- Avolon (Ireland)

- SMBC Aviation Capital (Ireland)

- BBAM (U.S.)

- Nordic Aviation Capital (Ireland)

- BOC Aviation (Singapore)

- Air Lease Corporation (U.S.)

- ICBC Leasing (China)

- DAE Capital (UAE)

- Boeing Capital Corporation (U.S.)

Key Industry Developments

- Apr 2022 – Air Lease Corp. ordered 32 additional Boeing 737 MAX aircraft to expand its portfolio.

- Jul 2022 – AerCap ordered 5 additional Boeing 787-9 Dreamliners, strengthening its wide-body fleet.