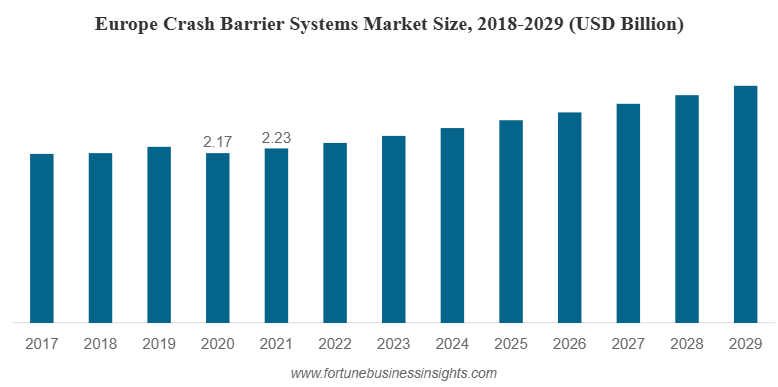

The global crash barrier system market was valued at USD 6.79 billion in 2021 and is expected to expand from USD 7.01 billion in 2022 to USD 9.35 billion by 2029, registering a CAGR of 4.2% during the forecast period. Asia Pacific held the largest share of 32.84% in 2021, reflecting the region’s rapid infrastructure growth. In addition, the U.S. crash barrier system market is projected to witness substantial growth, reaching around USD 2.23 billion by 2032, fueled by advancements in technology and innovative construction practices.

Road safety is a universal concern, and with the increasing number of vehicles on highways and city roads, the need for effective safety infrastructure has never been greater. One of the most important components of modern road safety is the crash barrier system. These barriers play a critical role in preventing vehicles from colliding with dangerous obstacles, veering off roads, or crossing into oncoming traffic. As a result, the crash barrier system market has witnessed strong growth in recent years and is expected to expand further as infrastructure development continues worldwide.

A crash barrier system market is a protective structure installed along roadsides, medians, bridges, and work zones to minimize the severity of road accidents. By absorbing impact energy and redirecting vehicles, these barriers reduce the risk of fatalities and severe injuries. They are available in different forms such as rigid, semi-rigid, and flexible designs, depending on the level of safety required and the type of road environment.

List of Top Crash Barrier Systems Companies:

- Tata Steel (India)

- Lindsay Corporation. (U.S.)

- Transpo Industries Inc. (U.S.)

- Hill and Smith (UK)

- RoadSafe Traffic Systems, Inc. (U.S.)

- Trinity Highway Products, LLC. (U.S.)

- Valmont Industries (U.S.)

- Pinax Steel Industries (India)

- Volkmann & Rossbach GmbH & Co. KG (Germany)

Market Overview

The global crash barrier system market has been on a steady rise, supported by rapid urbanization, large-scale infrastructure development projects, and stricter government regulations regarding road safety. Valuations of the industry suggest strong growth momentum, with a healthy compound annual growth rate expected in the coming years.

Asia Pacific currently dominates the market, fueled by massive highway construction in India, China, and Southeast Asian countries. Europe and North America also represent significant shares due to advanced road safety standards, while the Middle East, Africa, and Latin America are emerging regions where investments in infrastructure are creating fresh opportunities.

Types of Crash Barrier Systems

- By Type

- Fixed Barriers: These are permanently installed along highways, bridges, and sharp curves. They hold the largest market share as they provide long-term protection and require less frequent repositioning.

- Portable Barriers: Often used in temporary construction or work zones, portable barriers are growing in demand due to their flexibility and ease of relocation.

- Rigid Systems: Usually made of concrete or heavy steel, rigid barriers are designed to withstand high-impact crashes with minimal deflection.

- Semi-Rigid Systems: The most common type, such as W-beam guardrails, which absorb some impact while preventing vehicles from crossing into dangerous areas.

- Flexible Systems: Often made of wire ropes or other flexible materials, these systems deflect more under impact but significantly reduce the severity of crashes.

- Roadside Barriers: Installed on curves, embankments, and hilly terrains to prevent vehicles from leaving the roadway.

- Median Barriers: Positioned between opposing lanes to prevent head-on collisions.

- Bridge Barriers: Designed to stop vehicles from falling off bridges and elevated roads.

- Work Zone Barriers: Temporary barriers that safeguard construction workers and divert traffic safely.

Key Drivers of Market Growth

- Infrastructure Expansion

Developing nations are investing heavily in road networks, highways, and bridges. Every new project requires safety installations, boosting demand for crash barriers. - Government Regulations

Road safety standards have become stricter worldwide. Many countries mandate the installation of crash barriers on highways, mountain roads, and accident-prone zones. - Technological Advancements

New materials and smart designs are improving the performance of barrier systems. Innovations such as modular barriers, corrosion-resistant coatings, and smart sensors integrated into barriers are reshaping the industry. - Rising Road Accidents

The growing number of vehicles and increasing traffic density make road safety infrastructure more critical than ever. Crash barriers provide an effective solution to minimize loss of life and property damage.

Read More : https://www.fortunebusinessinsights.com/crash-barrier-system-market-106084

Regional Insights

- Asia Pacific: The fastest-growing region due to government investments in highways, urban roads, and rural connectivity projects. India and China are the largest contributors.

- Europe: A mature market with advanced technologies and strict road safety regulations. Continuous modernization of highways supports steady demand.

- North America: Growth is driven by highway renovation, increased urbanization, and a strong focus on reducing accident fatalities.

- Middle East, Africa, and Latin America: Emerging markets where rapid urban growth and new infrastructure projects are opening opportunities, though cost barriers remain.

Future Opportunities

The future of the crash barrier system market looks promising, with new opportunities such as:

- Smart Crash Barriers: Integration of IoT sensors and monitoring systems for real-time data collection and improved safety.

- Eco-Friendly Materials: Increased focus on using recycled metals and sustainable coatings.

- Public-Private Partnerships: Collaborations between governments and private firms to finance large infrastructure projects.

- Expansion in Emerging Economies: With rapid urbanization and rising awareness of road safety, demand will continue to surge in developing nations.

Key Industry Developments:

- June 2021: Trinity Highway Products, LLC signed an agreement with Highway Care Ltd. to produce, sell, and rent the MASH-tested HighwayGuard Barrier in North America. With this partnership, Trinity Highway broadened its commitment to offer innovative roadway solutions of HighwayGuard to Mexico, the U.S., and Canada.

- August 2019: Lindsay Corporation launched ABSORB-M, a new, non-redirective, water-filled crash cushion system. The product is suited for unanchored and anchored barriers. With this launch, the company would expand its product line.

Challenges in the Market

While growth prospects are positive, the crash barrier system market also faces challenges:

- High Costs: The installation and maintenance of barriers, especially rigid ones, involve significant expenses.

- Raw Material Price Volatility: Fluctuations in steel, aluminum, and other raw material prices affect profitability.

- Design Limitations: Not all barriers are suitable for every type of road. Choosing the wrong design can reduce effectiveness.

- Regulatory Gaps: In some developing regions, lack of enforcement and budget constraints hinder widespread adoption.

Future Outlook

The crash barrier system market is expected to grow steadily in the coming years, supported by global infrastructure expansion, stricter safety regulations, and increasing awareness of accident prevention. As technology advances and governments prioritize safer roads, crash barrier systems will play a vital role in creating secure and efficient transportation networks worldwide.

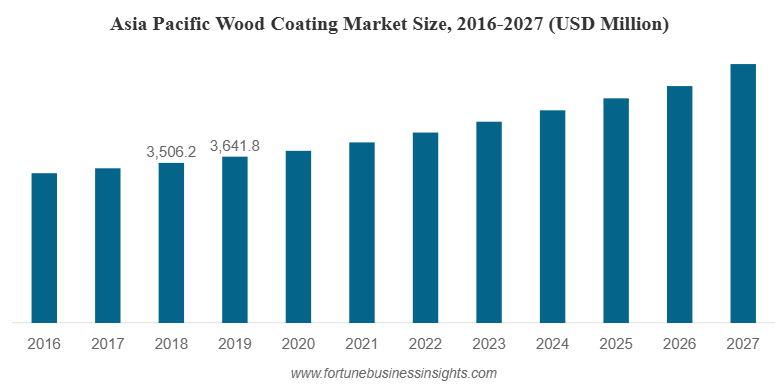

The global wood coating market was valued at USD 8,656.6 million in 2019 and is anticipated to expand to USD 12,323.2 million by 2027, growing at a CAGR of 4.8% during the forecast period. In 2019, Asia Pacific held the leading position with a 42.07% market share.

The wood coating market has witnessed steady growth over the last few years, driven by rising construction activities, the booming furniture industry, and a global shift toward sustainable and eco-friendly solutions. Wood coatings are an essential part of the wood and furniture value chain, offering not just protection but also aesthetic enhancement. As urbanization and lifestyle upgrades accelerate worldwide, the demand for durable, stylish, and sustainable wood products continues to surge — directly impacting the coatings industry.

List of Top Wood Coating Companies:

- Evonik (Essen, Germany)

- DSM (Heerlen, Netherlands)

- Dow (Michigan, U.S.)

- Akzo Nobel N.V. (Amsterdam, Netherlands)

- Asian Paints (Mumbai, India)

- BASF SE (Ludwigshafen, Germany)

- Kansai Nerolac Paints Limited (Osaka, Japan)

- PPG Industries, Inc. (Pennsylvania, U.S.)

- RPM International Inc. (Ohio, U.S.)

- The Sherwin-Williams Company (Ohio, U.S.)

- Teknos Group (Helsinki, Finland)

- Axalta Coating Systems (Pennsylvania, U.S.)

Importance of Wood Coating Market

Wood coating market are finishes applied to wood surfaces such as furniture, cabinets, flooring, siding, and doors. Their primary role is to protect wood against moisture, insects, UV radiation, and physical wear. Beyond protection, coatings also enhance the natural beauty of wood by adding shine, texture, or color.

The coatings can be based on different technologies and resins, such as:

- Polyurethane coatings – popular for durability and resistance.

- Nitrocellulose coatings – widely used for furniture with smooth finishes.

- Polyester coatings – preferred in high-end applications.

- Water-borne and UV-cured coatings – gaining traction for their eco-friendly and low-VOC features.

As consumers increasingly seek high-performance products that are both stylish and environmentally responsible, these coatings play a vital role in meeting expectations.

Key Growth Drivers in the Wood Coating Market

- Shift Toward Eco-Friendly Solutions

One of the strongest forces shaping the wood coating industry is the move toward water-borne, UV-cured, and powder coatings. These solutions emit fewer volatile organic compounds (VOC) and meet stricter environmental regulations. Governments and consumers alike are pushing for greener alternatives, and companies are responding with innovation. - Boom in Construction and Housing

Rapid urbanization, especially in Asia Pacific countries like India and China, is driving demand for residential and commercial buildings. This growth translates directly into rising demand for wooden furniture, cabinets, flooring, and decorative applications — all of which require coatings. - Rising Disposable Incomes and Lifestyle Changes

As middle-class populations expand, consumers are spending more on home décor and high-quality furniture. This trend boosts the demand for wood coatings that combine both beauty and durability. - Technological Advancements

Continuous R&D in resins and formulations is leading to stronger, longer-lasting coatings. UV-cured coatings, for instance, are gaining popularity in flooring and panel applications due to their quick curing time and high performance.

Emerging Trends in Wood Coatings

- Powder Coating for Wood

Once limited to metals, powder coating is now being adapted for wood surfaces such as MDF furniture. It offers durability, low maintenance, and an eco-friendly profile. - Low-VOC and Bio-Based Coatings

The push for sustainability is fueling innovation in bio-based resins and water-borne coatings. Products with lower formaldehyde and VOC content are becoming industry standards. - Smart and Functional Coatings

Beyond protection and decoration, coatings with anti-microbial, scratch-resistant, or heat-resistant properties are gaining attention, especially in high-end furniture markets.

Read More : https://www.fortunebusinessinsights.com/wood-coating-market-104605

Regional Insights

- Asia Pacific dominates the global market, accounting for more than 40% of the share. Strong demand from China, India, and Southeast Asia is fueled by population growth, rapid housing development, and industrial expansion.

- North America and Europe are mature markets, with growth driven by renovation, sustainable coatings, and technological adoption.

- Middle East, Africa, and Latin America are emerging regions where infrastructure development and increasing consumer spending are opening new opportunities.

Key Industry Developments:

- In February 2021, Axalta, a major global provider of liquid and powder coatings, has released a new Wood Coatings Pro mobile app for iOS and Android smartphones. For the wood coatings market, the new app provides easy and quick access to product information, industry color trends, and best practices.

- In February 2021, Dunn-Edwards introduced DECOPRIME, a new water-based wood primer. This new range is designed for inside wood cabinets, doors, and trim in kitchens and bathrooms. The DECOGLO paint, which will be available this fall, is part of a two-product solution for interior cabinets, doors, and trim.

Opportunities for Businesses and Investors

The growing wood coating market offers promising opportunities for manufacturers, distributors, and investors. Companies that focus on sustainable innovation, advanced technologies, and cost-effective solutions are likely to capture significant market share. For furniture brands and builders, adopting eco-friendly coatings can enhance product value and appeal to environmentally conscious consumers.

For investors, regions like Asia Pacific represent strong growth potential. As housing and infrastructure development continues, demand for coated wood products will remain robust.

Challenges and Restraints

While the wood coating market is growing, it also faces challenges:

- Raw Material Price Volatility: Many coatings rely on petroleum-based inputs. Fluctuations in oil prices impact production costs.

- Strict Regulations: Environmental and health standards require manufacturers to reformulate products, which can increase expenses.

- Supply Chain Issues: Global disruptions, like those experienced during the COVID-19 pandemic, have affected manufacturing and distribution.

Despite these hurdles, the long-term outlook for the wood coatings industry remains positive due to strong consumer demand and the global trend toward sustainable solutions.

Outlook

The wood coating market is not just about finishing touches — it is about innovation, sustainability, and performance. From protecting furniture to transforming interiors with stylish finishes, coatings are becoming a vital part of modern living spaces. With growing emphasis on eco-friendly solutions, rapid construction, and lifestyle upgrades, the market is poised for steady growth in the coming years.

For businesses and stakeholders, the time is right to embrace new technologies, invest in sustainable solutions, and capture opportunities in this dynamic and evolving market.

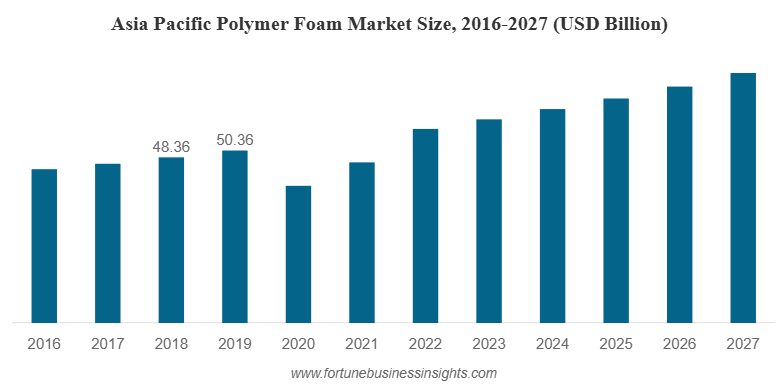

The global polymer foam market was valued at USD 114.88 billion in 2019 and is expected to reach USD 157.63 billion by 2027, registering a CAGR of 7.73% during the forecast period. In 2019, Asia Pacific led the market with a 43.84% share, driven by rapid industrial and infrastructure growth. Meanwhile, the U.S. polymer foam market is projected to hit USD 23.49 million by 2027, fueled by rising demand across furniture, automotive, and construction insulation applications.

List Of Key Companies Covered:

- Sealed Air (U.S.)

- Arkema (France)

- Armacell International S.A. (Germany)

- Borealis AG (Austria)

- Polymer Technologies, Inc. (U.S.)

- Zotefoams plc (UK)

- Synthos (Poland)

- Sekisui Alveo (Switzerland)

- BASF SE (Germany)

- Total SA (France)

Market Size and Forecast

The polymer foam market is expanding rapidly, supported by its wide applications across industries like construction, automotive, packaging, furniture, and consumer goods. These lightweight materials have become indispensable thanks to their excellent thermal insulation, cushioning, durability, and versatility. As industries evolve and global sustainability concerns rise, polymer foams are undergoing significant transformation, making the sector one of the most dynamic in the materials landscape.

Polymer foam market is a material created by incorporating air or gas bubbles into a polymer matrix, giving it a lightweight yet strong structure. The most common types include:

- Polyurethane (PU) foam – widely used in furniture, bedding, and automotive.

- Polystyrene (PS) foam – popular in packaging and insulation.

- Polyethylene (PE) foam – used in protective packaging and sports goods.

- Polyvinyl chloride (PVC) foam – often found in construction and signage.

Each type of foam has unique properties, from flexibility and cushioning to rigidity and insulation, making polymer foams a preferred choice in both industrial and consumer applications.

Key Applications Driving Growth

- Building & Construction

The construction sector is the largest consumer of polymer foams. Their lightweight nature, excellent insulation, and moisture resistance make them ideal for roofing, flooring, gap filling, and wall insulation. As governments tighten energy-efficiency standards, demand for polymer foams in green buildings is expected to rise.

- Automotive

In the automotive industry, polymer foams are critical for reducing vehicle weight, enhancing comfort, and improving energy efficiency. They are commonly used in seating, interior panels, soundproofing, and vibration absorption. With electric vehicles and fuel efficiency becoming a global priority, polymer foams will continue to play a central role in automotive design.

- Packaging

The packaging sector is witnessing steady demand for lightweight, durable, and protective materials. Polymer foams are extensively used to package food, electronics, medical devices, and fragile goods. Their shock-absorbing and insulating properties make them one of the most reliable materials for protective packaging.

- Furniture & Bedding

The popularity of memory foam mattresses, pillows, and cushions has brought polymer foams into the spotlight. Consumers are increasingly drawn to products that enhance comfort, ergonomics, and sleep quality, driving consistent demand in the furniture and bedding sector.

- Appliances and Consumer Goods

Polymer foams are widely used in refrigerators, air conditioners, and water heaters for insulation and energy efficiency. Their ability to provide both functional benefits and design flexibility has made them indispensable across appliances and consumer products.

Read More : https://www.fortunebusinessinsights.com/industry-reports/polymer-foam-market-101698

Market Trends to Watch

- Rising Demand for Memory Foam

Health-conscious consumers are investing in premium bedding and seating products. Memory foam, a type of polyurethane foam, is gaining momentum for its comfort, pressure relief, and orthopedic benefits. - Sustainability Focus

Environmental concerns are pushing companies to develop recyclable, bio-based, and eco-friendly foams. Regulations against single-use plastics and non-biodegradable materials are shaping new opportunities in the polymer foam market. - Innovation in Manufacturing

Advances in foam processing techniques are enabling better density control, improved fire resistance, and enhanced acoustic and thermal properties. These innovations expand the scope of applications across industries. - Growth in Emerging Economies

Countries in Asia, Latin America, and the Middle East are investing heavily in construction and infrastructure, providing strong growth opportunities for the polymer foam industry.

Key Industry Developments

- August 2019: Sheela Foam Limited, largest manufacturer of mattresses and foam based in India, acquired Interplasp SL, a Spanish Company, which has an annual production of 11,000 tons (total capacity 22,000 tons) of polyurethane foam for bedding and furniture applications.

- March 2019: Sika AG, a specialty chemical manufacturer of bonding, damping, sealing, reinforcing solutions for automotive and construction industries, acquired Belineco LLC, a Belarus-based producer of polyurethane foam systems. With this acquisition, Sika is further expected to develop its technology to manufacture polyurethane foams.

Challenges in the Polymer Foam Market

Despite its growth, the market faces several challenges:

- Environmental Impact: Many foams are petroleum-based and difficult to recycle, creating ecological concerns.

- Regulatory Pressures: Governments worldwide are enforcing strict standards on emissions, recyclability, and product safety.

- Raw Material Volatility: Fluctuations in crude oil and resin prices affect the cost of production.

- Competition from Alternatives: Natural materials and advanced composites are competing with polymer foams in certain applications.

Future Outlook

The future of the polymer foam market looks promising. Demand is expected to surge across construction, automotive, packaging, and consumer goods. Key developments include:

- Adoption of eco-friendly foams made from bio-based polymers.

- Expansion of lightweight materials in transport and automotive sectors.

- Growth in energy-efficient building projects, where foams play a central role.

- Rising demand for comfort-focused products in furniture and bedding.

As industries seek sustainable, efficient, and cost-effective solutions, the polymer foam market will continue to evolve with innovation and green alternatives.

The polymer foam market is set for significant expansion, driven by rapid urbanization, automotive innovation, and the growing need for lightweight, versatile materials. While challenges like sustainability and raw material costs remain, advancements in eco-friendly solutions and manufacturing technology are reshaping the industry.

For businesses and investors, the opportunities are clear: focus on sustainability, invest in R&D, and tap into emerging markets. With the right strategies, stakeholders can thrive in the ever-growing polymer foam market.

Nepheline Syenite Market Insights, Challenges, Key Players & Forecast 2032

By Sharvari06, 2025-08-29

The global nepheline syenite market was valued at USD 79.7 million in 2019 and is anticipated to reach USD 87.6 million by 2027, registering a CAGR of 1.3% during the forecast period. North America led the market in 2019 with a 55.46% share, while the U.S. market alone is expected to hit USD 43.9 million by 2027, driven by growing demand in glass manufacturing and ceramic applications.

Market Overview

Nepheline syenite market, an igneous rock rich in feldspathoid minerals, has emerged as a valuable industrial material due to its unique chemical composition and wide-ranging applications. Known for being free from quartz and high in alumina and alkali, it is increasingly used across industries such as glass, ceramics, coatings, plastics, and adhesives. The global market for nepheline syenite market has been showing steady growth, driven by rising demand for sustainable and energy-efficient raw materials, along with strong utilization in the glass and ceramics sectors.

List of Top Nepheline Syenite Companies:

- SCR-Sibelco N.V. (Belgium)

- FINETON Industrial Minerals Limited (China)

- The 3M Company (USA)

- PhosAgro Group of Companies (Russia)

- Anglo Pacific Minerals Ltd. (UK)

- RUSAL PLC (Russia)

Key Growth Drivers

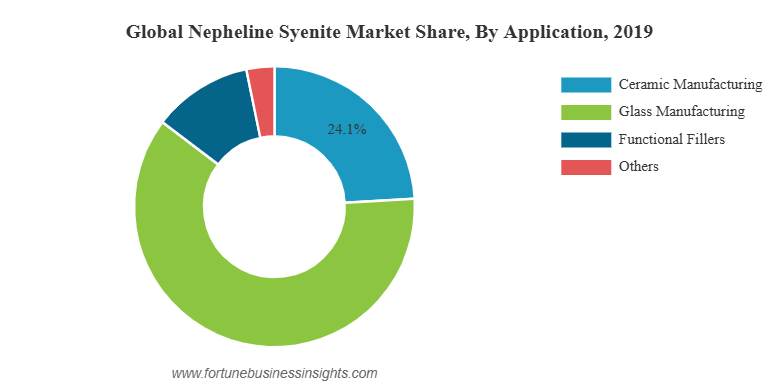

- Expanding Glass Industry

The glass industry is the largest consumer of nepheline syenite market. Its high alumina and alkali content reduces energy consumption during the melting process and enhances the chemical durability and clarity of glass products. With rising demand for container glass, flat glass, and specialty glass, especially in sectors like construction, automotive, and packaging, the consumption of nepheline syenite market is expected to rise steadily. - Ceramics Sector on the Rise

Ceramics represent another major application area, with tiles, sanitaryware, and tableware being the most common uses. Nepheline syenite market acts as a fluxing agent, lowering firing temperatures and improving the strength and brightness of ceramics. The construction boom across Asia Pacific and the Middle East is driving significant demand for tiles and sanitaryware, which in turn fuels the consumption of nepheline syenite market. - Functional Fillers in Coatings and Plastics

Beyond glass and ceramics, nepheline syenite market is increasingly being used as a functional filler in paints, coatings, plastics, adhesives, and sealants. Its low iron content, high brightness, and chemical stability make it a desirable alternative to traditional fillers. The shift toward eco-friendly coatings and sustainable construction materials is further accelerating its adoption in this segment. - Sustainability Advantage

Nepheline syenite market is considered more sustainable compared to some other raw materials used in similar applications. It offers improved efficiency during processing, requires lower energy for melting, and contributes to reducing carbon emissions in glass and ceramic production. With industries prioritizing greener solutions, this mineral is likely to play a more prominent role in the years ahead.

Read More : https://www.fortunebusinessinsights.com/nepheline-syenite-market-103434

Regional Insights

- North America: The region dominates the global market, accounting for more than half of the total share. The United States is a major consumer due to its large glass and ceramics industries, while Canada serves as a key supplier of nepheline syenite market.

- Asia Pacific: Countries like China and India are emerging as strong growth markets, driven by rapid urbanization, infrastructure development, and high demand for tiles, glass, and coatings.

- Europe: The region shows steady demand, particularly in specialty glass and ceramics, as well as in eco-friendly coatings.

- Rest of the World: The Middle East and Latin America are also witnessing gradual growth, supported by construction and industrial development.

Competitive Landscape

The market is moderately consolidated, with a few global players dominating production and supply. Companies are focusing on expanding capacity, improving supply chain efficiency, and exploring new applications to strengthen their market presence. Key industry participants include:

- SCR-Sibelco N.V.

- PhosAgro Group

- RUSAL PLC

- Anglo Pacific Minerals

- 3M

- Fineton Industrial Minerals Ltd.

Strategic initiatives such as mergers, acquisitions, and product innovations are common trends as players compete to meet growing demand while addressing sustainability concerns.

Key Industry Developments:

- January 2018: Unimin Corporation announced multi-million investment to modernize its nepheline facility in Cana da. This investment was done to improve mining & manufacturing operations in the Kawartha Lakes Region and to reduce environmental impact.

Future Opportunities

While the market currently reflects modest growth, several opportunities are expected to drive its expansion in the coming years:

- Rising Urbanization: Increased infrastructure development and housing demand, particularly in Asia Pacific, will continue to boost demand for tiles, glass, and ceramics.

- Eco-Friendly Coatings: The push for low-VOC and sustainable coatings presents new avenues for nepheline syenite market as a filler.

- Technological Advancements: Innovations in glass manufacturing and ceramics are likely to enhance the use of nepheline syenite market as a cost-effective and efficient raw material.

- Expanding End-Use Industries: Growth in automotive, packaging, and construction sectors will support long-term demand for this mineral.

Future Outlook

Nepheline syenite market may not yet be a widely recognized raw material, but its significance in industrial applications is steadily rising. From enhancing the durability and clarity of glass to lowering production costs in ceramics and serving as a sustainable filler in coatings, this mineral is gaining traction worldwide. While North America continues to lead the market, Asia Pacific is expected to be the fastest-growing region, fueled by construction and manufacturing growth.

The global nepheline syenite market may appear modest in size, but its future potential is far greater. As industries shift toward sustainable and energy-efficient solutions, nepheline syenite market is poised to become an essential material for long-term industrial growth.

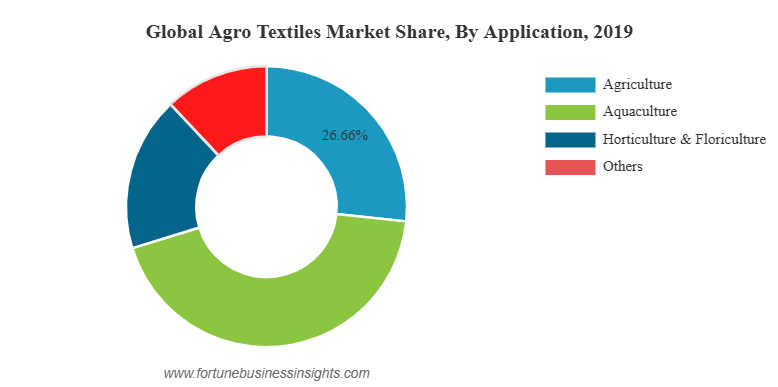

The global agro-textiles market was valued at USD 9,612.8 million in 2019 and is anticipated to reach USD 13,458.7 million by 2027, registering a CAGR of 5.2% during the forecast period. Asia Pacific led the market in 2019 with a 34.36% share, while the U.S. agro-textiles market is expected to hit USD 1,766.4 million by 2027, driven by innovations in crop protection and the growing focus on sustainable farming practices.

The global agro-textiles market is witnessing steady growth as the demand for advanced and sustainable solutions in agriculture and aquaculture continues to rise. Agro-textiles, which include products such as shade nets, mulch nets, crop covers, and fishing nets, are specially designed fabrics that support agricultural productivity and resource efficiency. They are manufactured from polymers such as polyethylene, polypropylene, and polyester, offering properties like durability, resistance to abrasion, biodegradability, and effective protection against environmental stress.

Key Market Drivers

- Rising Demand in Aquaculture

One of the most significant drivers of the agro-textiles market is the rapid growth of aquaculture. Fishing nets hold the largest market share due to the increasing global demand for fish as a source of protein, as well as its use in food, oils, and skincare products. The rise in aquaculture practices, particularly in Asia-Pacific regions, continues to support the consumption of agro-textiles.

- Expansion of Agriculture and Floriculture

Agro-textiles such as shade nets and crop covers are increasingly used to protect crops from solar radiation, pests, and environmental stress. Shade nets are widely utilized in agriculture and floriculture to enhance crop yields and preserve soil moisture. As climate challenges intensify, farmers are relying more on such innovative solutions to ensure productivity.

- Properties and Benefits of Agro-Textiles

The demand for agro-textiles is supported by their advantageous properties, including high tensile strength, resistance to adverse weather, and ability to retain water and nutrients in the soil. Moreover, innovations in biodegradable and eco-friendly polymer-based agro-textiles are boosting market growth, as sustainability has become a priority for both governments and consumers.

List of Top Agro Textiles Companies:

- SRF Limited (India)

- B&V Agro Irrigation Co. (India)

- (Japan)

- Beaulieu Technical Textiles. (Belgium)

- Meyabond Industry & Trading (Beijing) Co., Ltd. (China)

- Belton Industries. (U.S.)

- Neo Corp International Limited. (India)

- Hy-Tex (UK) Limited (U.K.)

- Diatex (France)

- Zhongshan Hongjun Nonwovens Co., Ltd. (China)

- Other Key Players

Market Segmentation

The agro-textiles market is segmented based on product type and application.

- By Product Type:

- Fishing nets

- Shade nets

- Mulch nets

- Crop covers

- Others

Among these, fishing nets dominate the global market share, while shade nets are showing fast adoption rates across agriculture.

- By Application:

- Agriculture

- Horticulture

- Aquaculture

- Floriculture

- Others

Aquaculture remains the leading application segment, supported by rising seafood demand and the growth of commercial fish farming.

Read More : https://www.fortunebusinessinsights.com/agro-textiles-market-102963

Regional Insights

Asia-Pacific

Asia-Pacific is the leading regional market, accounting for over one-third of the global share in 2019. Countries such as China and India are key contributors due to their large-scale agricultural and aquaculture industries. The increasing population and growing food demand further support the adoption of agro-textiles in the region.

North America

North America is witnessing growing demand for agro-textiles as the region invests more in sustainable agricultural solutions. The aquaculture industry in the United States is expanding, creating fresh opportunities for fishing nets and related products.

Europe

Europe represents a mature market with a steady demand for agro-textiles. The region is focusing on bio-based and eco-friendly polymer textiles in line with strict environmental regulations. Countries such as Germany, France, and Spain are adopting advanced agricultural technologies, which support the use of innovative agro-textiles.

Latin America, Middle East & Africa

These regions are emerging markets for agro-textiles. Favorable climatic conditions, government support for agriculture, and growing awareness about resource-efficient farming are expected to drive steady growth in these areas.

Key Industry Developments:

- January 2020– Diatex presented in the world’s leading trade fair IPM ESSEN 2020 for horticulture that took place in Germany. The company will present a tailor-made plant protection system and other crop field protection products at the IPM ESSEN 2020.

Challenges in the Market

While the agro-textiles industry is growing, it faces certain challenges:

- Raw Material Price Fluctuations: The volatility in the prices of polymers such as PET and polypropylene often affects production costs, which in turn impacts pricing and profitability.

- Lack of Awareness: In developing regions, farmers and small-scale producers are still less aware of the benefits of agro-textiles. Limited adoption restricts faster market penetration.

- Regulatory Concerns: Environmental regulations regarding plastic-based products could pose restrictions, prompting the need for more biodegradable solutions.

Future Outlook

The future of the agro-textiles market looks promising as innovation and sustainability drive the industry forward. Manufacturers are focusing on developing advanced materials that are not only durable but also environmentally friendly. The integration of smart technologies, such as microporous irrigation systems and UV-resistant fabrics, is expected to further enhance the value of agro-textiles in modern agriculture.

With growing global food demand, rising aquaculture practices, and increased awareness of resource-efficient farming, agro-textiles are set to play a vital role in shaping the agricultural sector of the future. The market is expected to expand steadily across developed and developing regions, with Asia-Pacific maintaining its leadership while North America and Europe continue to adopt advanced and sustainable solutions.

The agro-textiles market is steadily evolving, driven by the rising need for sustainable farming and aquaculture practices. With a forecasted growth from USD 9.6 billion in 2019 to USD 13.46 billion by 2027, the industry is on a positive trajectory. Key applications in aquaculture, agriculture, and floriculture will continue to fuel demand, while innovative and eco-friendly solutions will shape its future. Despite challenges such as raw material price fluctuations and low awareness in certain regions, the market holds significant opportunities for growth, innovation, and sustainability.

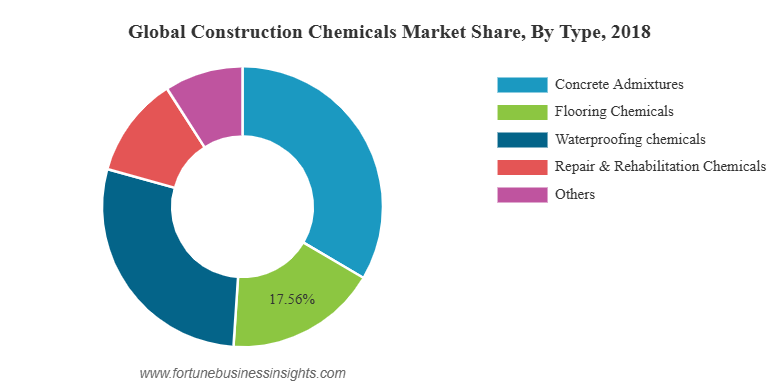

The global construction chemicals market was valued at USD 42.32 billion in 2018 and is expected to expand to USD 70.91 billion by 2026, registering a CAGR of 6.7% during the forecast period. In 2018, North America led the market with a 23.28% share, while the U.S. market alone is anticipated to reach USD 12.73 billion by 2026, fueled by rapid urbanization and ongoing infrastructure development.

The construction industry has undergone a significant transformation over the past few decades, with advanced materials playing a pivotal role in shaping modern infrastructure. Among these, construction chemicalsmarket have emerged as indispensable solutions that not only enhance the strength, durability, and efficiency of structures but also align with the growing demand for sustainable development.

Construction chemicals market are specialized formulations used at various stages of construction to improve the performance of building materials and ensure long-term durability. These chemicals include concrete admixtures, adhesives, sealants, protective coatings, waterproofing compounds, flooring chemicals, and repair materials. With global urbanization accelerating and infrastructure projects expanding, the demand for construction chemicals is experiencing steady growth across both developed and emerging markets.

Market Growth

The global construction chemicals market has witnessed robust growth over the years and is projected to continue expanding at a strong pace. The market size, valued in the tens of billions, is expected to nearly double over the next decade. Increasing urbanization, industrialization, and the rising need for sustainable construction solutions are among the primary growth drivers.

Concrete admixtures, which enhance workability, setting time, and strength of concrete, remain the largest and most significant product segment. They are extensively used in large-scale projects like highways, bridges, dams, commercial complexes, and residential developments. Adhesives and sealants are also gaining momentum, supported by the rising demand for energy-efficient and leak-proof building systems.

The growing adoption of green building materials has provided an additional boost to the industry. Eco-friendly admixtures and sustainable chemical solutions are being introduced by key players to minimize environmental impacts while ensuring high performance.

List of Key Companies Profiled In Construction Chemicals Market:

- BuildCore Chemicals

- Croda International Plc

- ACC Limited

- Evonik

- BASF SE

- Fosroc, Inc.

- CHRYSO India

- SWC Brother Company Limited.

- Sika AG

- 3M Company

- Other Key Players

Key Market Drivers

- Rapid Urbanization and Infrastructure Growth

Developing countries, especially in Asia-Pacific, are witnessing unprecedented growth in residential, commercial, and public infrastructure. Nations like India, China, and South Korea are investing heavily in smart cities, housing projects, and transportation networks. This surge in construction activity directly fuels the demand for advanced construction chemicals. - Sustainability and Green Building Practices

The construction sector is under growing pressure to reduce its carbon footprint. Construction chemicals such as polycarboxylate-based admixtures, waterproofing systems, and energy-efficient coatings are being widely adopted to promote sustainability. These products contribute to lower water consumption, reduced cement usage, and improved thermal insulation, supporting eco-friendly building practices. - Technological Advancements

Innovations in nanotechnology, polymer chemistry, and hybrid materials are creating high-performance construction chemicals that offer enhanced durability, flexibility, and corrosion resistance. Companies are focusing on research and development to launch next-generation products that meet the evolving needs of modern infrastructure.

Read More : https://www.fortunebusinessinsights.com/construction-chemicals-market-102539

Regional Insights

- Asia-Pacific: This region dominates the global market and is projected to continue its leadership in the coming years. Rapid industrialization, government initiatives for affordable housing, and large-scale infrastructure investments make Asia-Pacific the fastest-growing region.

- North America: Renovation and repair activities, coupled with strict sustainability regulations, drive demand for advanced chemical solutions.

- Europe: The focus is on green construction and regulatory compliance, especially in energy efficiency and emissions reduction.

- Latin America, Middle East, and Africa: Emerging markets with abundant natural resources and growing urban development are gradually contributing to market growth.

Key Industry Developments:

- In July 2021 – Saint-Gobain entered into an agreement to acquire Chryso, a leading global player in the construction chemicals market. The acquisition of Chryso perfectly fits within Saint-Gobain’s strategic vision of worldwide leadership for sustainable construction. It will further expand the Group’s presence in the growing construction chemicals market with combined sales of more than €3 billion across 66 countries.

- In June 2021 – JSW Cement, India’s leading Green cement company, has entered the Construction Chemical sector with the launch of a unique green product range in the category. The Construction Chemical category offers new opportunities for JSW Cement to combine innovation in concrete mix products with responsible construction. With this development, the company will expand its business.

- In October 2020 – MBCC Group acquired BASF construction chemicals business after its acquisition by an affiliate of Lone Star. MBCC Group has been carved out from BASF Group over the past 18 months and is now a fully standalone organization. With this acquisition, the company will be able to meet the consumer demand for the construction industry.

Challenges Restraining the Market

Despite strong growth prospects, the construction chemicals market faces challenges. One of the key concerns is the emission of volatile organic compounds (VOCs) from certain chemicals, which can negatively impact human health and the environment. Increasingly strict regulations on VOC content are pushing manufacturers to invest in cleaner, safer, and sustainable alternatives. Additionally, fluctuating raw material prices may impact the cost-effectiveness of products, posing another challenge for producers and end-users.

Strategic Developments

Recent years have witnessed strategic moves like acquisitions and expansions. Global leaders have invested in production facilities in high-growth regions to meet the rising demand. Additionally, mergers between chemical companies and construction solution providers highlight the trend toward integrated, sustainable solutions.

Future Outlook

The future of the construction chemicals market looks promising, fueled by a combination of population growth, urban infrastructure projects, and increasing awareness about sustainability. Smart cities, green buildings, and advanced transport systems will continue to rely heavily on chemical innovations that ensure durability, safety, and efficiency.

As governments and industries worldwide commit to reducing carbon emissions, the adoption of eco-friendly construction chemicals will accelerate. The market is also expected to benefit from digital technologies such as Building Information Modeling (BIM) and smart construction systems, which will create opportunities for customized, performance-oriented chemical solutions.

The global construction chemicals market is more than just a supporting industry—it is a driving force behind modern infrastructure and sustainable development. By enabling stronger, greener, and more durable structures, construction chemicals are redefining the future of the built environment. With strong growth drivers, rapid innovation, and a clear shift toward sustainability, the market is poised for significant expansion in the years ahead.

The global potassium formate market was valued at USD 730.53 million in 2023 and is expected to rise from USD 756.54 million in 2024 to reach USD 1,073.08 million by 2032, registering a CAGR of 4.5% during 2024–2032. In 2023, North America led the market, accounting for 32.5% of the overall share.

The global Potassium Formate Market is experiencing strong growth driven by its wide range of applications and rising demand across oil & gas, de-icing, and heat-transfer industries. Known for its excellent properties such as high density, thermal stability, and eco-friendly nature, potassium formate is becoming a preferred choice for industries that prioritize safety, performance, and sustainability.

Market Overview

Potassium formate is a salt of formic acid that is widely used in drilling fluids, completion fluids, de-icing agents, and heat-transfer fluids. Its non-corrosive and biodegradable nature makes it an environmentally friendly solution compared to traditional salts and chemicals. Over the past few years, the market has seen a steady rise in demand due to growing environmental regulations and the need for safer, more effective chemical solutions.

One of the most significant contributors to market expansion is the oil and gas industry, where potassium formate is extensively used in high-pressure high-temperature (HPHT) drilling operations. Its ability to maintain stability under extreme conditions while minimizing corrosion risks has made it a popular choice among drilling companies.

List Of Key Market Players Profiled In The Report

- Hawkins (U.S.)

- Geocon Products (India)

- Weifang Tainuo Chemical Co., Ltd. (China)

- Shandong Xinhua Pharma. (China)

- Dongying Shuntong Chemical (Group) Co., Ltd. (China)

- Sidley Chemical Co., Ltd. (China)

- Perstorp AB (Sweden)

- Honeywell International Inc. (U.S.)

- ADDCON GmbH (Germany)

- Dynalene, Inc. (U.S.)

Key Market Drivers

- Rising Demand in Oil & Gas Exploration

The oil and gas sector continues to be the backbone of potassium formate demand. With increasing exploration activities in deepwater and ultra-deepwater fields, the requirement for high-performance drilling fluids has intensified. Potassium formate brines provide the necessary density and stability, ensuring smooth operations even in challenging conditions. This trend is expected to significantly boost the market over the forecast period.

- Growth in De-Icing Applications

Another critical driver of market growth is the rising use of potassium formate in de-icing applications. Airports, roadways, and railway systems increasingly prefer potassium formate-based solutions because they are safer for the environment, less corrosive to infrastructure, and effective at lower temperatures. With growing concerns over climate change and extreme winters, the demand for efficient de-icing solutions is projected to rise further.

- Expanding Use in Heat-Transfer Fluids

Potassium formate is also gaining traction in heat-transfer systems, particularly in industrial refrigeration and HVAC applications. It provides excellent thermal performance, is non-toxic, and poses minimal risk to both equipment and the environment. The rapid expansion of the cold chain and frozen food industry has further accelerated the adoption of potassium formate in this segment.

- Environmental Sustainability

One of the strongest factors supporting the market is the global push towards sustainability. Governments and industries alike are focusing on reducing harmful emissions and adopting eco-friendly chemicals. Potassium formate, being biodegradable and safe, is emerging as a sustainable alternative to conventional de-icing salts and drilling fluids.

Read More : https://www.fortunebusinessinsights.com/potassium-formate-market-109687

Regional Insights

- North America

North America dominates the global potassium formate market, accounting for a significant share of the total revenue. In 2023, the region held over 32% market share, with the United States alone valued at nearly USD 200 million. Strong oil and gas exploration activities, coupled with high demand for eco-friendly de-icing solutions, are fueling market growth in this region.

- Europe

Europe is another important market, driven largely by stringent environmental regulations and the region’s focus on reducing carbon footprints. The increasing adoption of potassium formate in de-icing and industrial refrigeration systems is supporting the market’s expansion in countries such as Germany, the UK, and Scandinavia.

- Asia Pacific

The Asia Pacific region is witnessing rapid growth due to industrialization, expanding oil and gas projects, and growing food logistics needs. China and India are expected to be key growth engines as demand for frozen food, refrigeration, and efficient drilling solutions rises.

- Rest of the World

Other regions, including Latin America and the Middle East, are also showing promising growth. The Middle East, with its strong oil exploration activities, presents a major opportunity for potassium formate manufacturers.

Key Industry Developments

- October 2021 – BASF SE introduced a new line of potassium formate-based fluids specifically designed for aviation de-icing and anti-icing applications.

- August 2021 – Perstorp Potassium Formate (PoFO) was registered as a fertilizer under EC 2002/2003, simplifying the process for farmers using PoFO-based fertilizers like Amicult K 42. This registration eliminated the need for local raw material registration, thereby enhancing crop quality and yields.

Segmentation Insights

- By Application:

- Oil & Gas (largest segment)

- De-Icing

- Heat-Transfer Fluids

- Others

- By Form:

- Solid Potassium Formate

- Liquid Potassium Formate

- By End-User Industry:

- Oil & Gas

- Aviation & Transportation

- Food & Beverages (cold chain logistics)

- Industrial & Commercial Refrigeration

Future Outlook

The future of the potassium formate market looks promising, with demand expected to rise steadily across all major industries. By 2032, the market will cross the USD 1 billion mark, representing a growth of nearly 47% compared to 2023.

Key growth opportunities will lie in:

- Increasing drilling activities in emerging economies.

- Growing frozen food and cold chain logistics industries.

- Rising adoption of eco-friendly de-icing solutions.

- Technological advancements in heat-transfer systems.

The global Potassium Formate Market is poised for steady growth over the coming decade. Its unique combination of high performance, safety, and environmental sustainability makes it a valuable chemical across multiple industries. With strong demand from oil and gas exploration, rising applications in de-icing and heat-transfer, and increasing regulatory support for eco-friendly products, the potassium formate market is expected to remain on a positive trajectory.

By 2032, potassium formate will not only play a crucial role in industrial operations but also contribute to building a safer and more sustainable future.

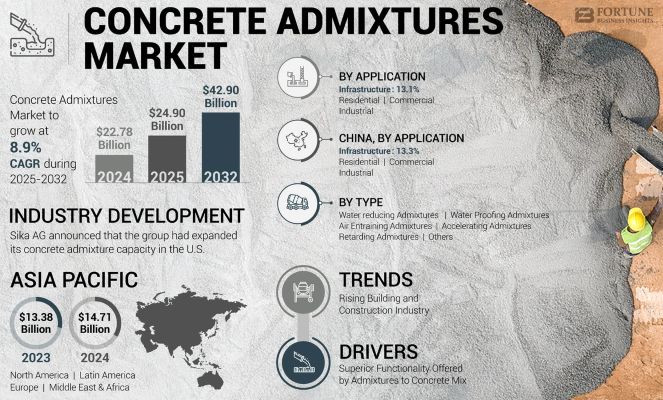

The global concrete admixtures market was valued at USD 22.78 billion in 2024 and is expected to expand from USD 24.90 billion in 2025 to USD 42.90 billion by 2032, reflecting a strong CAGR of 8.9% during the forecast period. Asia Pacific emerged as the leading region, capturing 64.57% of the market share in 2024. In addition, the U.S. market is set to witness notable growth, projected to reach USD 3.08 billion by 2032, fueled by rising adoption of high-performance concrete solutions.

The global concrete admixtures market is witnessing remarkable growth, driven by rapid urbanization, large-scale infrastructure development, and the increasing need for sustainable construction materials. Concrete admixtures are chemical formulations added to concrete mixtures to improve strength, durability, and performance. They also enhance workability, reduce water content, and ensure faster construction, making them indispensable in modern building practices.

Key Market Drivers

- Urbanization and Infrastructure Expansion

The construction industry continues to grow steadily, especially in emerging economies where governments are investing heavily in smart cities, highways, and housing projects. Urban migration is also fueling the demand for new residential complexes, which directly boosts the use of concrete admixtures.

- Performance Advantages of Admixtures

Concrete admixtures improve critical properties such as strength, durability, slump retention, and resistance to adverse weather conditions. By enhancing workability, they allow contractors to reduce costs, accelerate project timelines, and improve overall concrete quality.

- Focus on Sustainability

With rising environmental concerns, the demand for eco-friendly and low-carbon admixtures has increased. These admixtures enable the production of green concrete, which reduces the carbon footprint of construction activities while complying with stringent government regulations.

List of Top Concrete Admixtures Companies:

- Buildtech Products (India)

- Sika AG (Switzerland)

- RAZON ENGINEERING COMPANY PRIVATE LIMITED (India)

- Flowcrete Group Ltd. (U.K.)

- CEMEX S.A.B. de C.V. (Mexico)

- BASF SE (Germany)

- GCP Applied Technologies (U.S.)

- RPM International Inc. (U.S.)

- Fosroc International Inc. (UAE)

- Mapei S.P.A (Italy)

Market Segmentation Insights

- By Type

Among the different types of admixtures, water-reducing admixtures dominate the global market. These are widely used to enhance the workability and strength of concrete while minimizing water content. Other categories include superplasticizers, accelerating admixtures, air-entraining agents, and retarding admixtures, each serving unique applications in diverse construction projects.

- By Application

- Residential Construction: This segment holds the largest market share, driven by rising demand for housing and single-family homes. The availability of affordable credit and government-backed housing schemes further supports this growth.

- Infrastructure Projects: With investments in roads, bridges, airports, and metro networks, infrastructure construction has emerged as a key application area. It currently accounts for around 13% of the total market and is expected to grow steadily.

- Commercial and Industrial: Rapid growth in industrialization and commercial complexes also boosts demand for high-performance admixtures.

Read More : https://www.fortunebusinessinsights.com/concrete-admixtures-market-102832

Regional Insights

- Asia Pacific – The Growth Engine

Asia Pacific leads the global market with nearly 65% share in 2024. Countries like China and India are heavily investing in infrastructure and housing, making the region the largest consumer of admixtures. The growing population, rising disposable income, and government initiatives such as affordable housing schemes continue to drive demand.

- North America

The U.S. market is projected to reach around USD 3.08 billion by 2032, supported by infrastructure modernization, demand for high-strength concrete, and sustainable construction practices. Renovation of old bridges, highways, and public buildings adds further momentum.

- Europe

Germany and other European nations are focusing on eco-friendly admixtures to comply with strict environmental standards. Adoption of low-VOC and low-carbon admixtures is rising in commercial and industrial projects.

- Latin America

Brazil and Mexico are witnessing strong demand due to infrastructure projects and urban housing development. Investments in roads, ports, and airports are creating significant opportunities for admixture manufacturers.

- Middle East & Africa

Countries like Saudi Arabia and the UAE are boosting demand through mega projects such as NEOM and Vision 2030. Rising focus on tourism, smart cities, and transport infrastructure ensures steady consumption of advanced admixtures.

Key Industry Developments:

- November 2023: Sika AG announced that the group had expanded its concrete admixture capacity in the U.S. The company continues to invest in its polymer production at its Sealy site in the U.S. state of Texas. Sika’s latest move marks its second polymer investment in the state of Texas in just five years. The company requires polymers for chemical building blocks that are needed to produce Sika ViscoCrete, a high-performance, resource-saving concrete admixture. The company initiated this expansion to meet the growing demand for its products in the U.S. and Canada.

- June 2023: Fosroc India launched a state-of-the-art Concrete Lab in Chennai that will provide advanced building material testing facilities to developers, contractors, and other construction professionals.

Challenges Facing the Market

- Environmental Regulations: Strict rules on the use of petrochemical-based raw materials pose a challenge for manufacturers.

- High Costs of Advanced Admixtures: Premium products such as superplasticizers may increase project costs, limiting adoption in cost-sensitive markets.

- Volatility in Raw Material Prices: Fluctuations in crude oil and petrochemical markets can affect profitability for manufacturers.

Competitive Landscape and Recent Developments

The market is highly competitive, with global and regional players focusing on product innovation, sustainability, and geographic expansion. Major companies include Sika AG, CEMEX, BASF SE, Mapei, GCP Applied Technologies, Fosroc, CHRYSO, Master Builders Solutions, and Tremco CPG.

Recent industry moves highlight the sector’s dynamism:

- Sika AG expanded polymer production in the U.S. to meet rising demand for high-performance admixtures.

- Fosroc India launched a state-of-the-art Concrete Lab in Chennai to support advanced testing and research.

- CHRYSO introduced EnviroMix ULC 5500, an ultra-low carbon admixture for sustainable cement solutions.

- Tremco CPG India inaugurated a large facility in Rajasthan to strengthen supply in South Asia.

Future Outlook

The concrete admixtures market is expected to maintain its strong growth momentum over the coming decade. Rising emphasis on sustainability, coupled with the construction boom in Asia Pacific, will continue to drive demand. At the same time, advancements in R&D are expected to result in next-generation admixtures that balance cost-efficiency with environmental compliance. By 2032, the industry is likely to play a central role in building smarter cities, eco-friendly infrastructure, and resilient housing across the globe.