Polytetrafluoroethylene (PTFE) Filter Membranes Market Industrial Use Cases and Applications | 2025–2032

By ameliasss, 2025-08-04

According to Fortune Business Insights, The global polytetrafluoroethylene (PTFE) filter membranes market size was valued at USD 2,073.8 million in 2024. The market is projected to grow from USD 2,204.5 million in 2025 to USD 3,381.0 million by 2032, exhibiting a CAGR of 6.3% during the forecast period. Asia Pacific dominated the polytetrafluoroethylene (PTFE) filter membranes market with a market share of 41.15% in 2024.

Polytetrafluoroethylene (PTFE) filter membranes are synthetic membranes used for air and liquid filtration. PTFE is classified into hydrophobic & hydrophilic type that repels water and other liquids, making it an excellent choice for filtering gases and liquids. Polytetrafluoroethylene filter membranes are often used in applications that require high chemical resistance, high temperatures, or high purity. They are commonly used in the pharmaceutical, food and beverage, and chemical industries.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/polytetrafluoroethylene-ptfe-filter-membranes-market-108725

LIST OF KEY COMPANIES PROFILED:

- HYUNDAI MICRO Co., Ltd. (South Korea)

- Hangzhou IPRO Membrane Technology Co., Ltd (China)

- Suzhou Unique New Material Science & Technology Co., Ltd. (China)

- Hangzhou Cobetter Filtration Equipment Co.Ltd (China)

- GVS S.p.A. (Italy)

- General Electric (U.S.)

- Pall Corporation. (U.S.)

- Corning Incorporated (U.S.)

- Donaldson Company, Inc. (U.S.)

Regional Landscape

North America dominates the current market, holding ~ 40% share in 2023, with projected market share around 27–28% by 2025 , supported by stringent regulations such as FDA or EPA compliance standards in pharmaceutical, chemical, and wastewater sectors.

Europe also contributes 20% of the market, with growth driven by regulatory pressures such as REACH and environmental mandates.

Product Types & Segments

Hydrophobic vs Hydrophilic

Hydrophobic PTFE membranes lead the market and are expected to grow fastest—with 63.1% share by 2025 —because of their superior moisture resistance, making them ideal for pharmaceutical, biotech, and industrial applications.

Hydrophilic PTFE membranes currently hold 40–60% share in some reports, reflecting their use in certain liquid‑filtration applications.

Key Industrial Applications

Industrial filtration is the dominant application area—used in chemical processing, cement, power generation, and petrochemical industries due to PTFE’s excellent chemical resistance and thermal stability.

Other sectors include water & wastewater treatment , food & beverage processing , and medical/pharmaceutical filtration , particularly for sterile venting, drug manufacturing, and biotechnology processes.

Market Drivers & Opportunities

Strict environmental and industrial regulations globally, especially in waste discharge, emissions control, and clean‑water mandates, are driving demand for high‑performance filtration systems—PTFE membranes meet these standards.

Rapid industrialization and urbanization , particularly in APAC countries (e.g., China, India), fuel demand for treated water and high‑purity filtration in chemical and pharmaceutical manufacturing.

Technological innovation —including nano‑engineering, electrospinning, development of ePTFE composites and hybrid membranes—is enhancing membrane efficiency and opening new use‑cases such as fuel cells, hydrogen separation, and biotech applications.

Challenges & Market Constraints

High manufacturing cost : PTFE-based membranes remain costlier than alternative materials (ceramic or polymeric) due to specialized processing and raw material volatility.

Regulatory compliance barriers : Multiple regional safety and environmental standards can delay product rollouts and raise entry costs for new players.

Emerging competition : Substitute technologies and materials—such as ceramic membranes or alternative fluoropolymers—pose pressure, particularly in price-sensitive market segments.

Competitive Landscape

Leading players include Pall Corporation , Saint‑Gobain , Corning , Donaldson Company , W. L. Gore & Associates , Fiberflon , Hawach Scientific , Merck KGaA , Cytiva , and Hyundai Micro Co. , among others.

Recent moves: Merck expanded PTFE membrane capacity in Ireland (~€440M investment) and Pall launched new hydrophobic PTFE lines targeting high-purity pharmaceutical and medical filtration markets in 2022–2023.

Forecast Outlook (2025–2035)

APAC remains the fastest expanding region , with China and India leading in demand; North America and Europe sustain growth through regulatory and infrastructure-driven opportunities.

Hydrophobic PTFE membranes take an increasingly larger market share due to advances in performance and increasing penetration in pharma, biotech, and industrial filtration.

Information Source: https://www.fortunebusinessinsights.com/polytetrafluoroethylene-ptfe-filter-membranes-market-108725

KEY INDUSTRY DEVELOPMENTS:

- In February 2023, Donaldson Company, Inc. acquired Isolere Bio, Inc., a biotechnology company known for developing IsoTag reagents and its filtration processes, which are commonly used in manufacturing biopharmaceuticals. This acquisition is expected to expand Donaldson Company's capabilities while streamlining its manufacturing processes.

- In May 2022, GVS announced the acquisition of the entire share capital of Haemotronic, a prominent Italian group specializing in producing advanced filtration solutions for highly critical applications. In addition, Haemotronic is a leading manufacturer of medical components and bags, with plants in Italy and Mexico. This acquisition represents a significant acquisition of this company and will help it expand its product portfolio. It will also help the company strengthen its presence in the healthcare sector in both Europe and North America.

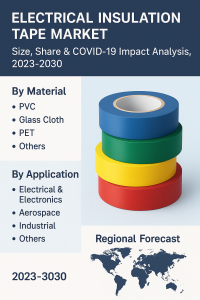

According to Fortune Business Insights, The global electrical insulation tape market size valued at USD 13.65 billion in 2022 and is projected to grow from USD 14.27 billion in 2023 to USD 20.11 billion by 2030, exhibiting a CAGR of 5.0% during the forecast period. Asia Pacific dominated the electrical insulation tape market with a market share of 56.85% in 2022.

Electrical insulation tapes are specialized adhesive tapes designed specifically for electrical applications. The market anticipates growth due to increased demand for higher-efficiency electric motors and the rise in electric charging stations. Electrical insulation tapes serve as specialized adhesive tapes intended for electrical applications. Typically, these tapes consist of a flexible backing material, often Polyvinyl Chloride (PVC) or Polyethylene Terephthalate (PET), coated with a rubber-based adhesive.

Fortune Business Insights™ mentioned this in a report titled, “ Electrical Insulation Tape Market, 2023-2030 .”

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/electrical-insulation-tape-market-103476

List of Key Players Present in the Report :

- tesa SE (Germany)

- Saint-Gobain (France)

- Nitto Denko Corporation (Japan)

- Avery Dennison Corporation (U.S.)

- 3M (U.S.)

- IPG (U.S.)

- HellermannTyton (U.K.)

- TERAOKA SEISAKUSHO CO., LTD. (Japan)

- Shurtape Technologies, LLC (U.S.)

- Pidilite Industries Ltd. (India)

Global Electrical Insulation Tape Market Overview

Market Size & Forecast:

- 2022 Market Size: USD 13.65 billion

- 2023 Market Size: USD 14.27 billion

- 2030 Forecast Market Size: USD 20.11 billion

- CAGR (2023–2030): 5.0%

Market Share:

- Asia Pacific dominated with 56.85% share in 2022

Regional Insights

- Asia Pacific: Largest share at 56.8%, driven by electronics manufacturing and urbanization.

- North America: Second-largest market; growth supported by infrastructure upgrades and renewable energy projects (solar, wind).

- Europe: Growth linked to investments in renewable energy infrastructure requiring robust insulation solutions.

- Latin America & Middle East & Africa: Growth driven by expanding industrial sectors and construction activities.

Segments

Affordability and Flexibility of PVC Insulation Tape to Propel PVC Segment Growth

Based on material, the market is classified into PVC, glass cloth, PET, and others. In 2022, the PVC segment held the largest market share owing to the affordability and flexibility of PVC insulation tape, driving its growth.

Growing Demand from Electronics Manufacturing Industry to Drive Electrical & Electronics Segment Growth

By application, the market is segmented into electrical & electronics, aerospace, industrial, and others. The electrical & electronics segment dominates the market and is expected to be the fastest-growing segment. This growth is fueled by increasing demand from the electronics manufacturing sector for component protection, insulation, and wire harnessing.

Geographically, the market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- The latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints

Growing Use of Insulation Tape in Consumer Electronics to Propel Market Growth

The growing use of electrical insulation tape in consumer electronics, safeguarding wires from wear and tear and accidental shocks, is expected to propel the electrical insulation tape market growth. It is mainly used to prevent accidental shocks and cover exposed wire connections.

However, alternative insulation technologies pose a challenge to market growth during the forecast period.

Regional Insights

Growing Electronic Industry to Drive Market in Asia Pacific

Asia Pacific leads the market, accounting for 56.8% of the electrical insulation tape market share in 2022. This dominance is attributed to the rapidly growing electronics industry in the region, driving demand and market growth.

North America follows as the second leading region, attributed to the growing industrial sector during the forecast period.

Information Source: https://www.fortunebusinessinsights.com/electrical-insulation-tape-market-103476

Competitive Landscape

Increasing Key Players Focus on Product Offerings to Propel Market Growth

Key market players are concentrating on developing a robust regional presence, enhancing product offerings, and strengthening distribution channels to bolster their market position, expected to drive market share growth.

Key Industry Development

- December 2022: Shurtape Technologies, LLC announced the acquisition of Pro Tapes & Specialties, Inc., a tape manufacturing company that serves several markets, including graphic arts, precision die-cutting and fabricating, library and school supply, retail and general industrial, and contract and custom converting. The acquisition is anticipated to enable the company to provide its customers with a broad range of product options and enhanced service capabilities to meet their ever-evolving needs.

Conductive Inks Market Share by Material Type and Application Insights 2032

By ameliasss, 2025-08-01

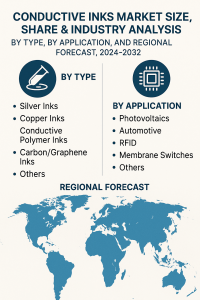

According to Fortune Business Insights, The global conductive inks market size was USD 2.73 billion in 2023 and is projected to grow from USD 2.84 billion in 2024 to USD 3.98 billion by 2032 at a CAGR of 4.2% during the forecast period. Asia Pacific dominated the conductive inks market with a market share of 35.53% in 2023.

Conductive ink combines the ability to conduct electricity with the utility of ink. The product is widely used in various applications, such as printing RFID tags, which are preferably used in modern transit tickets, computer keyboards, and windshield defrosters. According to the analysis, the ink has gained traction across applications, including printing RFID tags for computer keyboards and modern transit tickets. Moreover, the product has become highly sought-after for energy storage components globally.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/conductive-inks-market-106520

Major Players Profiled in the Market Report:

- DuPont (Delaware, U.S.)

- Henkel AG & Co. KGaA (Düsseldorf, Germany)

- Creative Materials Inc. (Massachusetts, U.S.)

- Heraeus Holding (Hanau, Germany)

- Poly-ink (Paris, France)

- CHASM (Massachusetts, U.S.)

- Johnson Matthey (London, U.K.)

- Vorbeck Materials Corp. (Maryland, U.S.)

- Daicel Corporation (Osaka, Japan)

- NovaCentrix (Texas, U.S.)

Segments

Type, Application, and Region are Studied

In terms of type, the market is fragmented into copper inks, silver inks, conductive polymer inks, carbon/graphene inks, and others.

Based on application, the market is segmented into RFID, automotive, membrane switches, photovoltaics, and others.

With respect to region, the market is segregated into North America, Asia Pacific, Europe, Latin America, and the Middle East & Africa.

Global Conductive Inks Market Overview

Market Size & Forecast:

- 2023 Market Size: USD 2.73 billion

- 2024 Market Size: USD 2.84 billion

- 2032 Forecast Market Size: USD 3.98 billion

- CAGR (2024–2032): 4.2%

Market Share:

- Asia Pacific: Dominated with a 35.53% share in 2023.

- United States: Projected to reach USD 497.45 million by 2032 due to rising EV sales.

Regional Insights:

- Asia Pacific: Growth from demand in photovoltaics, microelectronics, and consumer electronics. Strong solar energy initiatives in China and India.

- North America: Growth due to rising EV adoption and automotive electronics.

- Europe: Strong renewable energy targets and solar expansion supporting demand.

- Latin America: Slower growth due to economic and political instability.

- Middle East & Africa: Limited expansion due to underdeveloped electronics sector.

Report Coverage

The report is prepared with the use of qualitative and quantitative assessments. The use of primary sources, such as interviews with key opinion leaders has boosted the dynamics and insights with respect to trends. The report includes secondary sources, including SEC filings, press releases, annual reports, and paid databases. The report also delves into top-down and bottom-up approaches to forecast market size, revenues, and growth of major players in the landscape.

Drivers and Restraints

Bullish Investments in Electronics Industry to Foster Return on Investment (RoI)

The unprecedented growth of the electric sector is poised to foster conductive inks market share over the next few years. End-users will continue to exhibit traction for lightweight and efficient electronics across the advanced and emerging economies. IoT sensors, RFID tags, printed heaters, and touch displays are likely to set the trend. Prominently, the advent of 5G networks will potentially augment RoI. Robust outlook will be driven by the need for faster electronic devices and organic biosensors.

Meanwhile, fluctuating prices of raw materials, along with soaring costs of silver, could dent the market growth.

Regional Insights

Expansion of Electronics Sector to Underscore Asia Pacific Market Growth

Emerging economies, such as China and India, are slated to spearhead the adoption of touch screens, photovoltaics, and microelectronics. The trend for consumer electronics will underpin the Asia Pacific conductive inks market growth during the assessment period. Besides, robust government policies to curb fossil fuel consumption will bolster regional growth.

North America industry outlook will be strong with the presence of leading companies across the U.S. and Canada. Industry players are likely to bank on the penetration of automotive players such as Tesla and Ford. An exponential rise in the footfall of electric vehicles will drive the trend for inks. Surging demand for advanced features in the auto sector will further the penetration of conductive inks.

Information Source: https://www.fortunebusinessinsights.com/conductive-inks-market-106520

Competitive Landscape

Industry Players to Inject Funds into Product Rollouts to Bolster Footfall

Leading companies are poised to up their investments in mergers & acquisitions, R&D activities and technological advancements. The market’s competitiveness indicates key players could invest in geographical expansion and product portfolio expansion.

Key Industry Developments

- March 2023 - - OKdo, a subsidiary of RS Group, entered into a strategic partnership with Bare Conductive company. This partnership will help the company to scale its manufacturing facility, invent new products, and better serve customers.

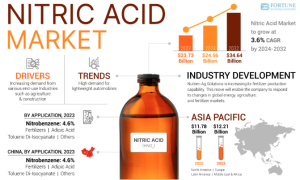

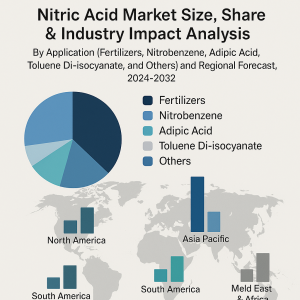

According to Fortune Business Insights, The global nitric acid market size was valued at USD 23.73 billion in 2023 and is projected to grow from USD 24.56 billion in 2024 to USD 32.64 billion by 2032, exhibiting a CAGR of 3.6% during the forecast period. Asia Pacific dominated the nitric acid market with a market share of 51.45% in 2023. Nitric acid (HNO3), also known as aqua fortis, is a colorless compound that turns yellow over a period of time due to the decomposition of nitrogen and water into oxides.

Vehicle manufacturers are concentrating on cutting-edge technologies owing to the rising demand for lightweight automobiles. This, in turn, is anticipated to propel the demand for HNO3 as companies are transitioning toward nylon to reduce weight and enhance fuel capacity. Fortune Business Insights presents this information in their report titled "Global Nitric Acid Market, 2024–2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/nitric-acid-market-104566

Major Players Profiled in the Report:

- BASF SE (Germany)

- Nutrien (Canada)

- EuroChem (Switzerland)

- CF Industries Holdings, Inc. (U.S.)

- Omnia Holdings Limited (South Africa)

- Dyno Nobel (Australia)

- Enaex S.A. (Chile)

- Sasol (South Africa)

- LSB Industries (U.S.)

- IXOM (Australia)

Segments

Dominance of Fertilizers Segment Driven by Growing Agricultural Activities

Based on application, the market is segmented into fertilizers, nitrobenzene, adipic acid, toluene di-isocyanate, and others. The increasing demand for agricultural activities to meet the needs of a growing population has led to the fertilizers segment holding the largest share nitric acid market share. It is utilized in the production of fertilizers such as ammonium nitrate and calcium ammonium nitrate, which play a vital role in achieving high-quality and abundant crop yields.

From the regional ground, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Global Nitric Acid Market Overview

Market Size & Forecast:

- 2023 Market Size: USD 23.73 billion

- 2024 Market Size: USD 24.56 billion

- 2032 Forecast Market Size: USD 32.64 billion

- CAGR: 3.6% (2024–2032)

Market Share:

- Asia Pacific dominated with 51.45% market share in 2023

- U.S. market projected to reach USD 3.19 billion by 2032

Regional Insights:

- Asia Pacific: Largest market with USD 12.21 billion in 2023, driven by demand in automotive, agriculture, and construction sectors in China, India, and Japan.

- North America: Significant share supported by technological advancements, demand for fuel-efficient vehicles, and construction activities.

- Europe: Substantial growth expected, led by demand for lightweight, eco-friendly automobiles and stringent environmental standards, with Germany as a key player.

- Latin America & Middle East & Africa: Moderate growth driven by food demand, industrialization, construction technology, and availability of raw materials lowering production costs.

Report Coverage

The comprehensive report presents an intricate examination of the market, with a specific emphasis on prominent enterprises, cutting-edge technologies, and prominent application domains. Moreover, the research report provides valuable observations on prevailing market trends and showcases noteworthy advancements within the industry. Alongside the aforementioned elements, the report encompasses numerous factors that have played a significant role in fostering the market's expansion in recent times.

Drivers and Restraints

Growing Construction Activities and Infrastructure Projects Propel Market Growth

The market growth is driven by increased construction activities, as Toluene di-isocyanate (TDI) and HNO3 intermediate are essential in the production of polyurethane foams, wood and floor coatings, and insulation materials. Additionally, the growth of the HNO3 market is fueled by improving consumer lifestyles, rising renovation activities, and new infrastructure projects initiated by governments.

However, governmental policies aimed at environmental protection and waste reduction pose challenges to the nitric acid market growth.

Regional Insights

Asia Pacific Emerges as a Prominent Region with Growing Demand across Industries

Asia Pacific achieved a market size of USD 11.78 billion in 2022, driven by the growing demand for the product across diverse industries such as automotive, agriculture, and construction.

North America is projected to hold a substantial share of the global market, which can be attributed to the region's rapid technological advancements and high disposable income of its consumers.

Competitive Landscape

Key Players Focus on Collaborations and Strategies to Maintain Competitive Edge

Major industry players are actively engaged in enhancing their capacities, driving product innovation, pursuing acquisitions and mergers, and fostering collaborations to gain a competitive advantage in the global market.

Information Source: https://www.fortunebusinessinsights.com/nitric-acid-market-104566

Key Industry Development

January 2023: Dorogobuzh introduced a new 135-ktpa UKL nitric acid unit in Smolensk region. The company’s engineering research and design center is designing this project, which costs around USD 17 million. The company’s nitric acid production capacity will reach 1.5 million tons per annum with the help of this launch.

According to Fortune Business Insights, The global trash bags market size was valued at USD 10.69 billion in 2024. The market is projected to grow from USD 11.27 billion in 2025 to USD 16.83 billion by 2032, exhibiting a CAGR of 5.90% during the forecast period. Trash bags are majorly plastic packaging that is deployed for hygiene applications in different fields. The lifestyle of urban people and their impact on rural people have witnessed a considerable change due to changing preferences. The surging concerns pertaining to hygiene are poised to be the new trend for greater product demand, augmenting market growth. Trash bags are mostly plastic packaging that is used for hygiene purposes in various fields. These bags are leakage-proof and have tear resistance, making them suitable for usage in carrying industrial and commercial trash.

Fortune Business Insights™ provides this information in its research report, titled “ Trash Bags Market, 2025-2032”.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/trash-bags-market-107323

List of Key Players Mentioned in the Report:

- Berry Global (U.S.)

- Novolex (U.S.)

- Reynolds Consumer Products (U.S.)

- Poly-America, L.P. (U.S.)

- International Plastics (U.S.)

- Inteplast Group (U.S.)

- Plasta Group (Lithuania)

- Four Star Plastics (U.S.)

- Cosmoplast (UAE)

- The Clorox Company (U.S.)

- Novplasta (Slovakia)

- Alpha Omega Plastic Manufacturing L.L.C. (UAE)

Segmentation:

Affordable Nature of Polyethylene (PE) to Propel Segment Expansion

On the basis of material, the market is segregated into Polypropylene (PP), Polyethylene (PE) [low Density Polyethylene (LDPE), High Density Polyethylene (HDPE), Linear Low Density Polyethylene (LLDPE)], and others. The Polyethylene (PE) segment registers the major trash bags market share. The easy recyclability, affordable nature, availability, and resistance to chemicals and water are augmenting the Polyethylene (PE) segment growth.

Presence of Built-in Drawstrings to Impel Segment Growth

In terms of type, the market is divided into handle tie, twist tie, drawstring, and others. The drawstring segment accounts for the largest share. The presence of built-in drawstrings in these bags, which make them easy to close and tie securely, removing the requirement for closures and extra ties and preventing odor and garbage spillage.

Growing Waste Generation from the Residential Sector to Spur the 14-50 Gallons Segment Expansion

By capacity, the market for trash bags is classified into 14-50 gallons, above 50 gallons, and 3-13 gallons. The 14-50 gallons segment registers the largest share with the rise in the generation of waste in residential and commercial sectors.

Flexible Attribute of the Product to Expedite the Residential Segment Growth

With respect to end user, the market is categorized into commercial, industrial, and residential. The residential segment occupies the largest share owing to its lightweight and flexible nature, and the ease of handling of products.

On the basis of region, the market is classified into Asia Pacific, Europe, the Middle East & Africa, Latin America, and North America.

Report Coverage

The research report offers a comprehensive coverage of the strategic measures implemented by top companies to stand out from the competition. In addition, it provides an in-depth analysis of the top trends, the COVID-19 pandemic impact, and significant industry developments. Besides this, the major driving and restraining factors have been mentioned in the report.

Drivers and Restraints:

Increasing Demand for Antimicrobial and Scented Products to Proliferate Market Growth

The rising significance of hygiene in residential and commercial places and increasing awareness have boosted the demand for scented bags since they contain fragrances and decrease the foul odor from garbage bins. In addition, they are available in various scents, including citrus, lavender, and certain fresh linen, extensively deployed in bathrooms and kitchens to avoid the smell.

However, the surging plastic pollution and rising concerns pertaining to the environment may hamper the trash bags market growth.

Regional Insights:

Asia Pacific Dominates Due to Rising Population

Asia Pacific captures the largest market share on the back of the surging industrialization, urbanization, and population, which has increased the disposable income of people, resulting in growing living standards and expanding cities. These factors have resulted in rising effective waste management, sanitation, and hygiene concerns, propelling the regional growth.

North American market for trash bags is witnessing a significant growth rate owing to rising demand for antimicrobial bags.

Competitive Landscape:

Top Players Emphasize Product Launches to Boost Their Position

The trash bags market represents a highly competitive and fragmented structure. A wide array of strategic moves, including joint ventures, mergers, acquisitions, and capacity expansions, are being deployed by top companies to gain a competitive edge. Many companies are also focusing on product launches to strengthen their position.

Information Source: https://www.fortunebusinessinsights.com/trash-bags-market-107323

Key Industry Development:

January 2024: Plasta Group announced the release of a new product line, Trash Panda. The products under this brand name are planet-friendly and manufactured using 100% recycled post-consumer plastic.

Precipitated Calcium Carbonate Market Regional Share and Growth Insights 2025–2032

By ameliasss, 2025-07-31

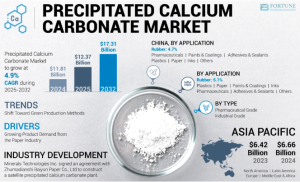

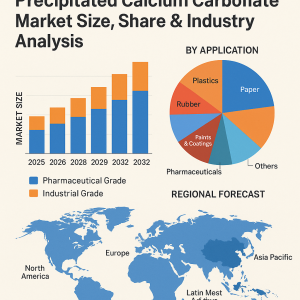

According to Fortune Business Insights, The global precipitated calcium carbonate market size was valued at USD 11.81 billion in 2024. The market is projected to grow from USD 12.37 billion in 2025 to USD 17.31 billion by 2032 at a CAGR of 4.9% during the 2025-2032 period. Asia Pacific dominated the precipitated calcium carbonate market with a market share of 54.36% in 2024.

Precipitated Calcium Carbonate (PCC) is a versatile chemical compound created through the reaction of calcium hydroxide and carbon dioxide. The growing demand for the product from several sectors for different applications is poised to bolster the market expansion.

Moreover, there were significant issues in the market owing to the COVID-19 pandemic, mainly in its supply chain. In addition, the market witnessed a halt in the supply of raw materials necessary for product production, including chemicals and limestone, due to movement restrictions and lockdown measures. There were also delays or halts in the procurement of these materials on account of transportation constraints and quarantine measures in mining areas, which affected production.

Fortune Business Insights™ provides this information in its research report, titled “Precipitated Calcium Carbonate Market, 2025-2032”.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/precipitated-calcium-carbonate-market-105287

List of Key Players Mentioned in the Report:

- Mineral Technologies (U.S.)

- Imerys S.A. (France)

- Mississippi Lime (U.S.)

- M. Huber Corporation (U.S.)

- ILC Resources (U.S.)

- Omya International AG (Switzerland)

- CANADA Chemical (Canada)

- GLC Minerals (U.S.)

Segmentation:

Common Deployment of Industrial Grade in the Rubber Industry to Foster Segment Expansion

In terms of type, the market is bifurcated into industrial grade and pharmaceutical grade. The industrial grade segment secured the largest share in 2023. The common utilization of industrial grade in industries, including paints & coatings, rubber, construction materials, adhesives, plastics, and paper manufacturing, is augmenting the segment growth.

Paper Segment Led Due to Ability of Product to Enhance Paper Attributes

With respect to application, the market is classified into adhesives & sealants, inks, paints & coatings, plastics, paper, pharmaceuticals, rubber, and others. The paper segment occupied the largest precipitated calcium carbonate market share in 2023. The product can improve paper attributes as a filler by boosting bulkiness, brightness, and opacity, enhancing uniformity and printing quality. This factor is propelling the paper segment expansion.

From the regional perspective, the market is categorized into Asia Pacific, Latin America, the Middle East & Africa, North America, and Europe.

Report Coverage

The research report offers a comprehensive coverage of the key driving and restraining factors affecting the market growth. In addition, it offers vital insights into the COVID-19 pandemic impact, the latest trends, and notable industry developments. Other aspects of the report include the strategic measures taken by top companies to stand out from the competition.

Drivers and Restraints:

Inclination Toward Green Production Methods to Impel Market Growth

The market is witnessing the growing adoption of green production methods to reduce environmental impact throughout the manufacturing process. In addition, closed-loop water systems are being used by players to reduce the consumption of water and discharge wastewater while encouraging environmental sustainability and efficient resource deployment. Thus, these factors are boosting the precipitated calcium carbonate market growth.

However, the fluctuations in the price of raw materials may hinder market expansion for precipitated calcium carbonate.

Regional Insights:

Asia Pacific Leads in the Global Market Due to Surging Consumer Goods Production

In 2023, Asia Pacific was valued at USD 6.42 billion in 2023 and holds the dominating position in the market. This can be credited to the rising production of industrial products, automotive components, and consumer goods, which is slated to bolster the product demand in manufacturing processes.

North America market for precipitated calcium carbonate is anticipated to observe significant growth in the coming years. The expansion of the pharmaceutical industry owing to rising healthcare expenditure and an aging population is escalating the regional growth.

Information Source: https://www.fortunebusinessinsights.com/precipitated-calcium-carbonate-market-105287

Competitive Landscape:

Leading Companies Emphasize Agreements to Expand Their Product Line

The precipitated calcium carbonate market is witnessing the implementation of many competitive strategies, such as product innovations, capacity expansions, and mergers and acquisitions to strengthen their position. Many companies are also focusing on entering agreements for the expansion of their product lines.

Key Industry Development:

- July 2023 – Minerals Technologies Inc. formed an agreement with the global paper company to upgrade the company’s precipitated calcium carbonate plant in Brazil by incorporating MTI’s NewYield LO PCC technology.

- April 2021 – Minerals Technologies Inc. signed an agreement with Zhumadianshi Baiyun Paper Co., LTD to construct a satellite precipitated calcium carbonate plant with 50 kiloton per annum capacity at its paper mill in Henan Province, China. This expansion helped the company serve its customers efficiently in China.

According to Fortune Business Insights, The global dispersing agents market size was valued at USD 8.63 billion in 2024. The market is projected to grow from USD 9.20 billion in 2025 to USD 14.90 billion by 2032, exhibiting a CAGR of 7.1% during the forecast period. Asia Pacific dominated the dispersing agents market with a market share of 29.78% in 2024.

The global dispersing agents market size is expected to gain traction in the coming years on account of the increasing demand from various end-use industries such as pulp and paper, paint and coatings, construction, and others. Dispersing agents or simply called dispersants are chemical compounds that can help to improve the separation of particles for preventing clumping or settling. They consist of polysorbate, polyethers, polyacrylates, among others, and are widely used by a variety of industries. A recent report by Fortune Business Insights provides a detailed analysis of the market and its prime growth trajectories. The title of the report is, “ Dispersing Agents Market Size, Share & Industry Analysis, By Surfactant Type (Anionic, Cationic, Non-Ionic), By End-Use Industries (Paints, Inks & Coating, Building & Construction, Pharmaceutical, Agrochemicals, Detergents & Consumer goods, Paper & Pulp, Oil & Gas, Others) Others and Regional Forecast, 2025-2032.”

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/dispersing-agents-market-102332

List of Dispersing Agents Market Manufacturers include:

- Ashland Inc.

- Elementis Specialties, Inc.

- NIPPON PAPER INDUSTRIES CO., LTD.

- Dow Chemical Company

- Evonik

- Toray Chemicals

- Lubrizol

- Croda International Plc.

- Clariant AG

- RUDOLF Group

- BASF SE

- Arkema Group

- Troy Corporation

- Other Players

What is the Scope of the Report?

The report offers a comprehensive overview of the market and factors propelling, repelling, challenging, and creating opportunities for the market. It also discusses major industry developments, current trends, and other interesting insights. The report also highlights the table of segmentation and mentions the names of the leading segments. It also lists the names of players operating in the market and the significant strategies adopted by them to emerge dominant in the competition. The report is available for sale on the company website.

Market Drivers

Increasing Demand from Oil and Gas Sector will Add Impetus to Market

Most of the end-use industries use dispersants for the composition and production of end products. Some of these industries are pulp & paper, oil & gas, paints & coatings, detergents, construction, and others. The increasing demand from industries listed above stands as a major dispersing agent market growth driver. Besides this, the increasing population, rise in construction activities, and infrastructural development are also expected to aid in the expansion of the market.

On the contrary, the government is imposing strict norms and regulations concerning the use of harmful chemicals in dispersants and this may cause major hindrance to the market in the coming years.

Regional Segmentation

Increasing Demand from Paint and Coatings Industries will Help Asia Pacific Dominate Market

Asia Pacific is holding the dominant dispersing agent market share with China leading the region. This is attributed to the substantial growth of the pharmaceutical and paint & coatings industry in the region. There is a high demand from developing nations such as India, Thailand, Vietnam, Indonesia, and others whereas South Korea and Japan are considered mature markets. Additionally, the market in Europe will witness considerable growth on account of the increasing demand from Italy, France, the UK, and Germany. Moreover, the North American market will witness a moderate growth owing to the increasing uses of paint and coating and pharmaceutical industries. Furthermore, Saudi Arabia, South Africa, and Egypt are considered significant markets for paint and coatings and will, therefore, witness sluggish growth in the forecast duration.

Information Source: https://www.fortunebusinessinsights.com/dispersing-agents-market-102332

Competitive Landscape

Increasing Investment on Product Portfolio will Intensify Competition

Major vendors of the dispersing agents market are engaged in the production and development of dispersants that are suitable for specific end-user applications such as special architectural coatings, sprays for planes and boats, and others. Besides this, players are engaging in collaborative efforts such as contracts and agreements, joint ventures, mergers and acquisitions, and others to reach the top position in the market competition. Such initiatives are expected to help attract high revenue to the overall market in the coming years.

KEY INDUSTRY DEVELOPMENTS:

- August 2023: BASF SE introduced a new production plant in Dilovasi, Turkey for the production of water-soluble dispersants based on acrylic acid. This investment aimed to support BASF’s customers in the detergent, cleaning and chemical processing industry across Europe, the Middle East and Africa.

- July 2022: Evonik launched its new sustainable dispersing additive, TEGO Dispers 658. The TEGO dispersing agent is readily biodegradable, improving the sustainability of pigment and coloured coatings production, while offering formulators a similar high-performance profile to other comparable Evonik products.

According to Fortune Business Insights, The global flexitank market was valued at USD 268.62 million in 2024 and is expected to expand to USD 644.69 million by 2032, growing at a CAGR of 11.63% during the forecast period. In 2024, Asia Pacific held the largest share of the market, accounting for 42.26%. The U.S. flexitank market is anticipated to witness substantial growth, reaching approximately USD 419.71 million by 2032, fueled by rising demand for food-grade oils, chemicals, and beverages, especially across the food & beverage, chemical, and pharmaceutical sectors.

The increasing investment in the development of sustainable products associated with the manufacturing of flexitank will aid the growth of the market in the coming years. The increasing number of regulatory approvals for transport and distribution networks will bode well for the market. According to a report published by Fortune Business Insights, titled “ Flexitank Market Size, Share & Industry Analysis, By Reusability (Single Use and Reusable), By Product (Monolayer and Multilayer), By Loading Type (Top Loading and Bottom Loading), By Application (Food-Grade Liquids [Alcoholic Beverages; Edible Oils; Juices, Concentrates, and Syrups; and Others], Non-Hazardous Liquid Chemicals, and Pharmaceutical Liquids), and Regional Forecast, 2025-2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/flexitank-market-103047

List of companies profiled in the report:

- Qingdao BLT Packing Industrial Co., Ltd. (China)

- Qingdao LET Flexitank Co., Ltd. (China)

- LiquA Europe SLU (Spain)

- Qingdao LAF Packaging Co., Ltd. (China)

- LSM SA (Argentina)

- UWL Inc. (U.S.)

- FTS Container Packaging Co., Ltd. (China)

- SIA Flexitanks (Ireland, USA, Malaysia)

- BeFlexi (Cyprus)

- Hinrich Industries (Malaysia)

- TIBA (Spain)

- Flexible World Company Ltd. (Vietnam)

- Flexitank Group (Spain)

Flexitank is a lightweight disposable bladder that is normally made out of plastic. The product is normally used for shipping of non-hazardous liquid materials that is transported through shipping containers. The advancements in the materials used in manufacture of flexitank will lead to a wider product adoption. The increasing applications of the product are attributable to the favorable properties of the material used in manufacturing. The stringent guidelines associated with the use of this product, set by organizations such as the Containers Owners Association (COA) will ensure safety of the product, subsequently leading to a wider product adoption across the world. The growing investment in R&D of the material associated with flexitank will contribute to the growth of the market in the coming years. Additionally, the presence of several large scale companies will emerge in favor of market growth.

Increasing Regulatory Approvals will Help Companies Generate Huge Revenues

The report encompasses several factors that have contributed to the growth of the market in recent years. Among all factors, the increasing number of regulatory approvals has made the highest impact on market growth. In November 2019, SIA Flexitanks got approval from the Canadian CN Rail network and Norfolk Southern Rail network for shipping of flexitanks. SIA already has shipping approvals from CSX and BNSF rail networks and this approval will help the company expand its transportation over other regions. These approvals will open new territories and markets for the company and subsequently generate massive revenues in the coming years. SIA’s approval from CN and NSR networks will not just benefit the company but will also have a direct impact on the growth of the overall market in the coming years. The report highlights a few of the other industry developments, similar to this and discusses their impact on market growth.

Information Source: https://www.fortunebusinessinsights.com/flexitank-market-103047

Asia Pacific to Emerge Dominant; Increasing Food and Chemical Manufacturing Hubs Will Aid Growth

The report analyses the ongoing market trends across five major regions, including North America, Latin America, Europe, Asia Pacific, and the Middle East and Africa. Among all regions, the market in Asia Pacific is projected to emerge dominant in the coming years. The increasing number of food as well as chemical manufacturing units in several countries across this region will have a direct impact on the growth of the regional market. Additionally, the increasing efforts put in import as well as export activities will create several opportunities for market growth. As of 2019, the market in Asia Pacific was worth USD 245.42 million and this value is projected to increase further in the coming years. The market in North America will also witness considerable growth driven by the increasing transport activities for liquid chemicals through rail-based containers.

KEY INDUSTRY DEVELOPMENTS:

-

June 2022 – Mediterranean Shipping Company became one of the companies to provide in-house liquid cargo solutions by introducing flexibag for shipping liquid cargo. Flexibags can carry up to 24,000 liters of non-hazardous liquids such as wine, edible oils, petroleum products, and chemicals, offering a cost-effective and safe alternative to other bulk liquid transportation solutions.

- March 2022 – SIA Flexitanks launched its innovative trinity tank. This three-pod reefer flexitank system would enable shippers to load multiple flexitanks in the same container to transport the bulk liquids. The tank has a total capacity of 27,000 liters, and one of the triple tanks can hold 9,000 liters.