According to Fortune Business Insights, The contract packaging market size was valued at USD 93.26 billion in 2024. The market value is projected to increase from USD 98.77 billion in 2025 to USD 141.14 billion by 2032, exhibiting a CAGR of 5.23% during the forecast period. Asia Pacific dominated the contract packaging market with a market share of 34.15% in 2024.

Contract packaging refers to the process of outsourcing packaging and assembly of products to third party packaging service providers. This helps companies increase their focus on their core competencies. Availing these packaging services also helps firms decrease their capital investments in specialized packaging machineries, which reduces their financial burden. Outsourcing packaging functions allows companies to reduce capital investments in machinery and facilities, and benefit from economies of scale achieved by the companies. Contract packaging service providers offer the expertise to design and implement customized packaging strategies that meet evolving consumer demands.

Fortune Business Insights™ displays this information in a report titled, "Contract Packaging Market, 2025-2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/contract-packaging-market-106869

LIST OF KEY COMPANIES PROFILED IN THE REPORT

- Silgan Unicep (U.S.)

- Summit Packaging Solutions (U.S.)

- Stamar Packaging (U.S.)

- Sharp Services, LLC (U.S.)

- Aaron Thomas Company Inc. (U.S.)

- Green Sustainable Packaging (U.S.)

- Co-Pak Packaging Corporation (U.S.)

- Assemblies Unlimited Inc. (U.S.)

- AmeriPac Inc. (U.S.)

- Asiapack Ltd. (China)

- Wepackit Inc. (U.S.)

- Sterling Contract Packaging Inc. (U.S.)

- Pharma Packaging Solutions (U.S.)

- The Shippers Group (U.S.)

- Sonic Packaging Industries (U.S.)

Segmentation:

Plastic Material Gains Notable Traction Due to Various Benefits

Based on material type, the market is segmented into plastic, glass, paper & paperboard, and others. The plastic segment holds the largest contract packaging market share as this material has several attractive properties, such as high versatility and flexibility, making it a highly preferred packaging material in various industries.

Key Role in Product Protection Makes Secondary Packaging Popular Among Customers

Based on packaging type, the market is segmented into primary packaging, secondary packaging, and tertiary packaging. The secondary packaging segment holds a majority part due to its major role in protecting the product’s quality and integrity from external elements, such as temperature changes and moisture.

Food & Beverage Industry is Major End-User Due to Varied Packaging Requirements of Different Products

Based on end-use industry, the market is segmented into food & beverage, personal care & cosmetics, pharmaceuticals, electronics, e-commerce, and others. The food & beverage segment is dominating the market due to the diverse packaging requirements of a wide range of products manufactured in this industry.

With respect to region, the market covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report analyzes the market in detail and highlights several key aspects, such as leading product types, packaging types, end-users, and top market players. It also offers important information regarding the top industry developments and latest market trends. Besides the factors listed above, the report covers many other factors that have fueled the market’s growth.

Drivers and Restraints:

Growing Outsourcing of Packaging Services by Manufacturers to Spur Market Progress

An increasing number of companies in various industries are outsourcing their product packaging functions to help them increase their focus on their core operations. They are realizing the potential benefits of using contract packaging services, such as reduced cost, access to specialized expertise of packaging professionals, and proper utilization of resources. These benefits are encouraging firms to avail the services of contract packagers to enhance their business performance.

However, strict regulations on the use of plastics in packaging can hinder the contract packaging market growth.

Regional Insights:

Asia Pacific Dominates Global Market Due to Expansion of Leading Sectors

Asia Pacific is dominating the global market as some of the leading industries, such as manufacturing, pharmaceuticals, and food & beverage are growing at a notable pace, offering more growth opportunities to contract packaging service providers.

North America is the second-dominating region in the market due to the presence of a strong regulatory framework and strict quality standards.

Information Source: https://www.fortunebusinessinsights.com/contract-packaging-market-106869

Competitive Landscape:

Leading Companies to Launch Innovative Packaging Solutions to Expand Business Operations

The market has a highly fragmented competitive landscape as a small percentage of reputed companies are dominating the market by introducing smart packaging solutions for their customers. Some of the key market players include Summit Packaging Solutions, Silgan Unicep, Stamar Packaging, Aaron Thomas Company Inc., Sharp Services, LLC, and others.

Notable Industry Development:

- October 2023 – Sharp, a global leader in commercial pharmaceutical packaging and clinical trial supply services, announced the acquisition of Berkshire Sterile Manufacturing (BSM). BSM is a Massachusetts-based fill-finish Contract Development and Manufacturing Organization (CDMO) for clinical and commercial sterile injectable products.

- August 2023 – The Shippers Group partnered with Pacific Coast Producers to stock the shelves of local food banks.

The global titanium dioxide market size was valued at USD 22.28 billion in 2024. The market is projected to grow from USD 24.81 billion in 2025 to USD 40.07 billion by 2032 at a CAGR of 7.1% during the 2025-2032 forecast period. Asia Pacific dominated the titanium dioxide market with a market share of 53.95% in 2024, observes Fortune Business Insights™ in its report, titled, “ Titanium dioxide Market Size, Share & Industry Impact Analysis, By Process (Sulfate, and Chloride), By Application (Paints & coatings, Plastics, Paper, and Others), and Regional Forecast, 2025-2032. ”

Titanium Dioxide (TiO₂) is a white, powdered inorganic compound renowned for its exceptional brightness and high refractive index, making it a widely used white pigment. It finds extensive applications across various industrial and consumer sectors, such as paints and coatings, plastics, cosmetics, paper, textiles, and food colorants. In the construction and automotive industries, TiO₂ plays a critical role as a primary pigment in paints and coatings used for roofing materials, flooring, automotive finishes, and printing inks.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/titanium-dioxide-tio2-market-102390

A List of Key Manufacturers Operating In the Global Market:

- Tronox Holdings plc (Connecticut, U.S.)

- The Chemours Company (Delaware, U.S.)

- Argex Titanium Inc. (Québec, Canada)

- Evonik Industries (Essen, Germany)

- The Kish Company, Inc. (Ohio, U.S.)

- Ishihara Sangyo Kaisha Ltd. (Osaka, Japan)

- Venator Materials PLC. (Texas, U.S.)

- Tayca Corporation (Osaka, Japan)

- Huntsman Corporation (Texas, U.S.)

- NL Industries, Inc. (Texas, U.S.)

- INEOS (Maryland, U.S.)

- Others

Highlights of the Report:

The report includes a detailed company profile of key players and in-depth analysis of various market segments. It also includes close study of the various drivers and restraints that drive the market along with comprehensive understanding of the positive and negative impacts of regional developments on the market.

Drivers & Restraints-

Increasing Demand for Light-weight Vehicles to Drive Growth

According to the Office of Energy Efficiency and Renewable Energy, by reducing the weight of the vehicle by 10%, its fuel efficiency can be enhanced by 6%-8%. Stringent regulations from governments across the world regarding emission are driving manufacturers to adopt lightweight materials and components, such as alloys and polymer composite, for making fuel-efficient vehicles. This is projected to spur the growth of the global market. In addition, growing applications of the material in the construction industry is anticipated to further enhance growth. However, the evident decrease in the supply of titanium dioxide owing to the prolonged shutdown of production units is anticipated to hinder its growth.

Segment-

Extensive Utilization in Automobile Space to Help Paints and Coatings Segment Flourish

On the basis of application, the paints and coatings segment dominated the by holding the largest share in 2019. This is attributed to increasing application in automobiles and growing construction activities. The plastics segment showed impressive growth by holding 26.09% share of the market.

Regional Insights-

Rising Demand for Titanium dioxide from End-user Industries to Aid Growth in Asia Pacific

Asia Pacific is estimated to dominate the global titanium dioxide market with a share of USD 7,575.7 million in 2019. Rising demand for the chemical compound from various end-use industries in the region including automobile, construction, plastic, and papers is one of the major factors driving the growth of this market. In addition, improving economic stability in major countries of the region including India and China and the resultant expenditure on infrastructure are increasing the demand from the construction industry.

The market in North America is anticipated to grow potentially in the projected timeline. The increasing technological advancement in the construction space coupled with the high disposable income of consumers is expected to enhance the growth of titanium dioxide in the region.

Information Source: https://www.fortunebusinessinsights.com/titanium-dioxide-tio2-market-102390

Competitive Landscape-

Business Expansion to Help Key Players Gain Competitive Edge

Key players operating in the global titanium dioxide market comprise manufacturers and developers that are currently focused on business expansion. For example, DuPont recently improved its production capacity in order to gain competitive advantage over other players. The company constructed a new plant to produce TiO 2 in Mexico and upgraded the existing one.

Industry Developments-

- December 2024: Chemours plans to expand its DeLisle plant through a partnership with PCC Group, which will build a chlor-alkali facility to ensure a steady chlorine supply for titanium dioxide production. With a 340,000 metric ton capacity, the facility aims to enhance efficiency and reduce costs. The construction is set to begin in 2026, reinforcing Chemours’ 45-year commitment to the region.

- July 2024: Kronos Worldwide, Inc. has taken full ownership of Louisiana Pigment Company (LPC), boosting its North American market position with LPC’s 156,000 metric tons of annual titanium dioxide production capacity and diversified product offerings.

Superabsorbent Polymers Market Strategic Developments and M&A Trends Through 2032

By ameliasss, 2025-07-28

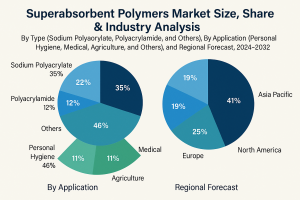

According to Fortune Business Insigths, The global superabsorbent polymers market size was valued at USD 5.82 billion in 2023. The market is projected to grow from USD 6.13 billion in 2024 to USD 9.69 billion by 2032 at a CAGR of 5.9% during the forecast period. Asia Pacific dominated the superabsorbent polymers market with a market share of 29.38% in 2023.

Superabsorbent Polymers (SAPs) are advanced polymeric networks composed of a variety of monomeric units such as sodium polyacrylate, polyacrylamide, and other specialized constituents. These innovative materials are poised to experience substantial market expansion due to the increasing consumer demand for personal care essentials, including baby diapers, adult incontinence products, and feminine hygiene items. Fortune Business Insights presents this information in their report titled "Global Superabsorbent Polymers Market, 2024–2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/superabsorbent-polymers-market-104602

Major Players Profiled in the Report:

- Sumitomo Seika Chemicals (Japan)

- Nippon Shokubai (Japan)

- Sanyo Chemical/SDP Global (Japan)

- BASF (Germany)

- Evonik (Germany)

- LG Chem (South Korea)

- Taiwan Plastics (Taiwan)

- Yixing Danson (China)

- Satellite Science & Technology (China)

- Shenghong Holding Group (China)

- Quan Zhou Technology (China)

Segments

Sodium Polyacrylate Dominates Market Fueled by Growing Demand in Personal Hygiene

By type, the market is segmented into sodium polyacrylate, polyacrylamide, and others. Sodium polyacrylate has emerged as a dominant force in the market, capturing a substantial share due to its heightened demand in personal hygiene and medical applications. The product boasts exceptional absorption properties while also providing protection against skin irritation.

Personal Hygiene Segment Takes the Lead due to Rising Population and Health Awareness

By application, the market is segmented into personal hygiene, medical, agriculture, and others. The personal hygiene segment is poised to emerge as the frontrunner in the market due to growing population and heightened health consciousness among individuals propelling the demand for a wide range of personal hygiene products. This includes baby diapers, feminine sanitary napkins, adult incontinence products, and similar items.

From the regional ground, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- Latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers and Restraints

Surging Pediatric Population Fuels Demand for Hygiene Products

The utilization of SAP in the manufacturing of baby diapers takes precedence among all hygiene products, primarily due to a significant rise in the pediatric population. Projections from the World Bank Group indicate that the population within the age group of 0 to 14 is expected to reach 2.08 billion by 2050. This substantial growth in population is anticipated to drive an increased demand for personal hygiene products, thereby fueling the market growth.

However, declining population growth in some countries due to low fertility rate may stifle the superabsorbent polymers market growth.

Regional Insights

Asia Pacific Takes the Lead with Strong Government Programs in Childcare and Women’s Health

Asia Pacific has emerged as the frontrunner, commanding the largest superabsorbent polymers market share. It is also projected to experience the highest CAGR due to the successful implementation of government programs focused on childcare and women's health in major economies such as China and India within the region.

North America exhibits a notable penetration of personal hygiene products within its population. Furthermore, the region's growing elderly population is expected to be a significant driver of market growth specifically for adult incontinence products in the foreseeable future.

Information Source: https://www.fortunebusinessinsights.com/superabsorbent-polymers-market-104602

Competitive Landscape

Market Players Invest in R&D to Focus on Prioritizing Sustainability

Major industry players are actively investing in research and development endeavors to produce products using bio-based raw materials, aiming to minimize their environmental impact. Additionally, these market players are collaborating to incorporate recycled materials into the manufacturing process, further promoting sustainability within the SAP market.

Key Industry Development

- October 2024 : BASF announced the completion of the capability upgradation for Superabsorbent Polymers in North America. The company invested USD 19.2 million to enhance the efficiency and expansion of its SAP facility in North America. The move is anticipated to support the company’s growth in North America and meet developing trends in the market.

- August 2024 : Nippon Shokubai announced its plan of expansion of superabsorbent polymer in Indonesia. The plan is to build a plant for superabsorbent polymers manufacturing with capacity of 50,000/year. The move is part of its strategy to take advantages of its strength from the vertically integrated production from AA to SAP to meet the strong demand growth in Asian region and the expectation for synergistic effect with the existing plant.

The global sustainable packaging market size was valued at USD 310.00 billion in 2022 and is projected to be worth USD 329.26 billion in 2023 and reach USD 518.33 billion by 2030, exhibiting a CAGR of 6.70% during the forecast period. The growing awareness regarding environmental issues among consumers, along with the rising need for such packaging solutions, led to the rapid adoption of sustainable packaging by businesses.

Sustainable packaging refers to development and utilization of sustainable packaging materials to store, ship, wrap, or shelve products that results in enhanced sustainability. The increasing awareness related to environmental issues among consumers and the growing need for such packaging solutions to boost market growth.

Fortune Business Insights™ mentioned this in a report titled, “ Sustainable Packaging Market, 2023-2030 .”

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/sustainable-packaging-market-108946

List of Key Players Present in the Report :

- Amcor Plc (Switzerland)

- Ardagh Group S.A. (Luxembourg)

- Ball Corporation (U.S.)

- Crown Holdings Inc. (U.S.)

- DS Smith (U.K.)

- Sealed Air Corporation (U.S.)

- Mondi Group (U.K.)

- Sonoco Products Company (U.S.)

- Tetra Pak International S.A. (Switzerland)

- WestRock Company (U.S.)

- Smurfit Kappa (Ireland)

- Huhtamaki Oyj (Finland)

- International Paper (U.S.)

Segments

Easy Recyclability Features of Paper & Paperboard Material Boosts Paper & Paperboard Segment Growth

By material, the market is classified into paper & paperboard, glass, plastic, metal, and others. The paper & paperboard segment dominates the market. The paper & paperboard material is a biodegradable and renewable packaging solution as it can be recycled easily.

Benefits of Bags & Pouches to Drive Bags & Pouches Segment Growth

Based on product type, the market is classified into boxes & cartons, bags & pouches, bottles & cans, films & wraps, trays, mailers, and others. The bags & pouches segment dominates the market owing to the benefits offered by bags and pouches, such as transportation and shopping costs and lightweight and compactness.

Growing Health-Conscious Consumers to Boost Food & Beverages Segment Expansion

By application, the market is segmented into food & beverages, personal care & cosmetics, pharmaceuticals, consumer goods, e-commerce, and others. The food & beverages segment is dominating the market and is expected to grow significantly during the forecast period. The segment’s growth is attributed to the increasing health-conscious consumers and increasing consumer health concerns among the food & beverage producers.

Geographically, the market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Global Sustainable Packaging Market Overview

Market Size & Forecast:

- 2022 Market Size: USD 310.00 billion

- 2023 Market Size: USD 329.26 billion

- 2030 Forecast Market Size: USD 518.33 billion

- CAGR: 6.7% (2023–2030)

Market Share:

- North America dominated with a 32.5% share in 2022

- U.S. market projected to reach USD 143.86 billion by 2032

Regional Market Insights:

- North America: Market leader, supported by strong government regulations, consumer preferences, and recycling infrastructure.

- Asia Pacific: Second largest; growth driven by expanding pharmaceutical and food & beverage sectors and raw material availability.

- Europe: Growth fueled by single-use plastic bans and demand for recyclable packaging; key players from the U.K., Germany, etc.

- Latin America: Moderate growth driven by expanding food & beverage industry.

- Middle East & Africa: Steady growth linked to healthcare and pharmaceutical sector expansion.

Report Coverage

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- The latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints

Increasing Demand for Compostable Packaging Solutions to Boost Market Expansion

The increasing demand for environmentally friendly and compostable packaging solutions owing to the consumers’ increasing awareness regarding the environmental issues driving the sustainable packaging market growth. Compostable packaging solutions are important as they diminish a large portion of plastic pollution by driving it away from landfills and waterways.

However, the high costs and limited availability of raw materials that result in producers facing difficulty in planning their production schedules and fulfilling customers’ demands, may impede market growth.

Regional Insights

Rising Government Regulations to Boost Market Expansion in North America

North America dominates the sustainable packaging market share. The market’s growth is attributed to increasing government regulations, changing consumer preferences, the presence of top food packaging companies in the U.S., and the sustainability initiatives that propel market growth.

Information Source: https://www.fortunebusinessinsights.com/sustainable-packaging-market-108946

Competitive Landscape

Growing Key Players’ Focus on Customer Base Expansion to Drive Market Growth

The sustainable packaging market comprises key players, such as Amcor Plc, Ardagh Group S.A., Ball Corporation, Crown Holdings Inc., DS Smith, and others. The increasing focus of these key players on their customer base expansion across regions by innovating their existing product range drives the market growth.

Key Industry Development

- August 2023 – Leading packaging manufacturer Sonoco Products Company has declared the launch of new sustainable packaging solutions with two EnviroFlex Paper Pre-qualifications, especially for the How2Recycle® Labeling range.

According to Fortune Business Insights, The global paper bag packaging market size was valued at USD 6.91 billion in 2023. It is projected to grow from USD 7.26 billion in 2024 to USD 11.30 billion by 2032, exhibiting a CAGR of 5.69% during the forecast period. Asia Pacific dominated the paper bag packaging market with a market share of 33.29% in 2023.

Paper bag packaging deploys paper bags and is mainly utilized for the transportation of goods or sale in retail sectors. The surging demand for the product from end users, which can be attributed to its reusable offerings and more brand visibility, leading to the reduction in landfills, is impelling the market growth. A paper bag is an essential packaging solution made from recycled paper. The rising adoption of biodegradable flat-bottom paper bags packaging across various end-use industries drives market growth.

Fortune Business Insights presents this information in their report titled " Paper Bags Packaging Market , 2024–2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/paper-bags-packaging-market-108337

Major Players Profiled in the Report:

- Smurfit Kappa (Ireland)

- International Paper Company (U.S.)

- Westrock Company (U.S.)

- Huhtamaki Oyj (Finland)

- Mondi Plc (U.K.)

- Oji Holdings Corporation (Japan)

- Welton Bibby & Baron Ltd (U.K.)

- Novolex Holdings Inc. (U.S.)

- Ronpack (U.S.)

- Packman Packaging (India)

- Primepac Industrial Limited (New Zealand)

- Bee Dee Bags (Australia)

Segmentation:

By material, the market is bifurcated into white kraft and brown kraft. The brown kraft segment accounted for the largest paper bags market share in 2023. The extensive usage of brown kraft material among several end-use industries is propelling the segment growth.

In terms of packaging type, the market is classified into pasted valve, pasted open mouth, flat bottom, pinched open bottom mouth, and sewn open mouth. The flat bottom segment registers the largest paper bags packaging market share due to their rising demand in grocery shops and retail.

With respect to application, the market is categorized into agriculture, retail, pharmaceuticals, personal care & cosmetics, food & beverages, and others.

Based on geography, the market for paper bags packaging is segregated into the Asia Pacific, Europe, the Middle East & Africa, North America, and Latin America.

Report Coverage

The competitive strategies implemented by market leaders to strengthen their position have been mentioned in the report. Besides this, it provides an in-depth analysis of the latest trends, the COVID-19 pandemic impact, and significant industry developments. The report further offers a comprehensive coverage of the major factors affecting the paper bags packaging market size.

Drivers:

Increasing Demand for Customizable Packaging Solutions and Efficient Carriers of Goods to Spur the Market Growth

The paper bags packaging market growth is being boosted by a surge in the demand for efficient goods carriers coupled with the rising demand for customizable packaging solutions. Moreover, the market growth is further driven by the extensive advantages provided by paper packaging.

However, the less durability of the product as compared to other packaging materials may hamper the market growth.

Regional Insights:

Asia Pacific Dominates Due to Flourishing Retail Sector

The Asia Pacific witnesses the largest share in the market. The growth of the retail sector, along with the robust presence of prominent manufacturers, is fostering the regional expansion.

North America is witnessing the fastest growth in the paper bags packaging market owing to tightening regulations on the consumption of plastic and a considerable rise in e-commerce.

Europe market for paper bags packaging is observing quick demand for the product on the back of the presence of prominent cosmetic brands.

The market in Latin America is poised to witness moderate growth during the forecast period on account of the expansion in the food & beverage industries.

Information Source: https://www.fortunebusinessinsights.com/paper-bags-packaging-market-108337

Competitive Landscape:

Prominent Companies Emphasize Various Strategic Moves to Bolster Their Share

The market leaders are incorporating various strategic initiatives such as mergers & acquisitions, joint ventures, and product innovations to reinforce their industry position. Many companies are deploying collaboration strategies to maximize their revenue.

Key Industry Development

- June 2024- Mondi collaborated with Cemex and introduced its ground-breaking SolmixBag to the building industry in the Mallorca, Balearic Islands of Ibiza, and Menorca. The SolmixBag is a one-ply paper bag made from 100% kraft paper, designed to easily store and transports products such as screed, dry cement, and coarse pre-mixes.

- April 2023 - ProAmpac, a leader in flexible packaging and material science, launched its patent-pending PRO-EVO Recyclable platform. This addition to the ProActive Recyclable series of products, PRO-EVO Recyclable, is an efficient multiwall paper-based self-opening-sack (SOS) bag, certified for curbside recycling, ideal for dry pet food.

According to Fortune Business Insights, The global squalene market size was valued at USD 169.6 million in 2024. The market is projected to grow from USD 185.03 million in 2025 to USD 359.5 million by 2032, exhibiting a CAGR of 9.9% during the forecast period. Europe dominated the squalene market with a market share of 47.88% in 2024.

Squalene is a naturally derived organic compound most abundantly sourced from shark liver oil. It is also found in lesser quantities in certain plant-based sources, including olive oil, wheat germ, and amaranth seeds. Structurally, squalene is a triterpene hydrocarbon with the chemical formula C₃₀H₅₀. In recent years, it has attracted significant interest for its potential health benefits and versatile applications across multiple industries. Due to its excellent moisturizing qualities and its ability to enhance skin hydration and elasticity, squalene is widely utilized in cosmetic and personal care formulations.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/squalene-market-110069

LIST OF TOP SQUALENE COMPANIES:

- Amyris (U.S.)

- Sophim (France)

- Kishimoto Special Liver Oil Co., Ltd (Japan)

- Empresa Figueirrense de Pesca, Lda (Portugal)

- Matrix Life Science Private Limited (India)

- Croda International Plc (U.K.)

- Aasha Biochem (India)

- Evonik Healthcare (Germany)

1. Market Segmentation

End-Use Verticals

The personal care & cosmetics segment remains dominant, accounting for around 70% of total demand , due to squalene’s moisturizing and antioxidant properties in skin care, serums, creams, and hair care products.

The pharmaceutical sector , particularly in vaccine adjuvants and drug delivery systems, is the fastest-growing segment. Its importance surged during and after the COVID-19 pandemic, with applications in immune-boosting formulations.

Source Type

Animal-derived squalene , traditionally extracted from shark liver oil, has historically held significant market share due to low cost and availability.

Plant-based and biosynthetic sources —from olive oil, amaranth, rice bran, sugarcane, or fermentation processes—are gaining ground due to ethical and sustainability concerns.

2. Regional Landscape

Europe led the global market in 2024, with a market valuation of approximately USD 81.2 million , representing nearly 48% of global market share . The region's strong preference for sustainable and ethical products supports the dominance of plant-based squalene.

The Asia-Pacific region is the fastest-growing, driven by rapid expansion in the beauty and pharmaceutical industries, particularly in countries like China, Japan, India, and South Korea.

Latin America , the Middle East , and Africa are emerging markets with increasing adoption of squalene in both personal care and healthcare industries.

3. Growth Drivers

Ethical & Sustainability Trends

The push for cruelty-free, environmentally friendly, and sustainable ingredients is prompting manufacturers and consumers to move away from shark-derived squalene.

Booming Cosmetics Sector

The rise in demand for clean beauty, anti-aging skincare, and natural ingredients continues to drive squalene use in moisturizers, sunscreens, and other personal care products.

Pharmaceutical Advancements

Squalene’s use in vaccine adjuvants and lipid-based drug delivery systems contributes significantly to market growth, particularly in pandemic preparedness and immunization programs.

Biotechnological Innovation

Breakthroughs in biosynthetic squalene production via sugarcane fermentation or yeast enable high-purity, scalable, and eco-friendly production, reducing dependence on traditional extraction.

6. Outlook & Challenges

Market Forecast

The market is expected to grow from USD 169.6 million in 2024 to USD 359.5 million by 2032 , with a CAGR of 9.9% . Plant-based and synthetic sources are expected to increase their share, gradually replacing animal-derived squalene.

Key Challenges

High production costs of plant-based and biosynthetic squalene compared to traditional sources.

Supply chain constraints for plant feedstocks such as olive and amaranth.

Regulatory complexities related to GMO and synthetic ingredient approvals.

Maintaining quality and consistency in large-scale, sustainable production.

7. Regional Highlights

Europe : Currently the largest market, with strong regulatory backing for sustainable ingredients and a highly developed cosmetic and pharmaceutical industry.

Asia-Pacific : Expected to witness the highest CAGR, fueled by rising consumer spending, awareness of ethical beauty, and local pharmaceutical innovation.

Latin America & Middle East & Africa : Gaining momentum through increased healthcare investments and local cosmetic demand.

Key Takeaways

| Theme | Insight |

|---|---|

| Market Size | USD 169.6 million (2024) → USD 359.5 million (2032) |

| Growth Rate | CAGR of 9.9% |

| Top Region | Europe leads; Asia-Pacific grows fastest |

| Main Application | Personal care & cosmetics (largest share), followed by pharmaceuticals |

| Dominant Source Trend | Transition from animal-derived to plant-based and synthetic |

| Key Players | Amyris, SOPHIM, Evonik, Croda, Matrix Life Science |

Information Source: https://www.fortunebusinessinsights.com/squalene-market-110069

KEY INDUSTRY DEVELOPMENTS :

-

October 2023 – Sophim, a company dedicated to producing natural ingredients for personal care and cosmetics, completed a USD 21.5 million funding round which is expected to double the company's production capacity at two its industrial sites —located in Peyruis, in the south of France, and in Almeria, Spain further accelerating its international expansion.

-

October 2023 – Evonik launched a GMP-quality plant-based squalene for commercial and clinical use. This product can be used as an adjuvant component for parenteral drug delivery applications.

Flexible Plastic Packaging Market: Who’s Leading and What’s Next, 2025-2032

By ameliasss, 2025-07-23

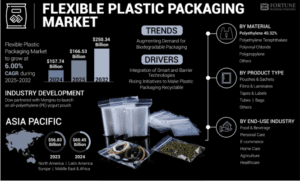

According to Fortune Business Insights, The global flexible plastic packaging market was valued at USD 157.74 billion in 2024. The market is projected to grow from USD 166.53 billion in 2025 to USD 250.34 billion by 2032, exhibiting a CAGR of 6.00% during the forecast period. Asia Pacific dominated the flexible plastic packaging market with a market share of 38.32% in 2024.

A massive range of protective attributes and assurance pertaining to minimal material usage is provided by flexible plastic packaging. The minimal cost of production, extensive deployment of the packaging in many end-use industries, and ease of customization and reusability are fostering the market growth. Plastic as a packaging material is enjoying great popularity due to its technical versatility and malleability. It offers excellent protection for food while being very lightweight and cost-effective. Flexible plastic packaging offers a wide range of protective properties while ensuring minimal material consumption.

Fortune Business Insights™ provides this information in its research report, titled “Flexible Plastic Packaging Market, 2025-2032”.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/flexible-plastic-packaging-market-108075

List of Key Players Mentioned in the Report:

- Amcor (Switzerland)

- Berry Global (U.S.)

- Sealed Air (U.S.)

- Aluflexpack AG (Switzerland)

- Bak Ambalaj Sanayi (Türkiye)

- Constantia Flexibles (Austria)

- Clondalkin Group (Netherlands)

- Danaflex Group (Russia)

- Printpack, Inc. (U.S.)

- ProAmpac Intermediate, Inc. (U.S.)

- Huhtamaki (Finland)

- Mondi (U.K.)

Segmentation:

Polyethylene (PE) Segment Dominates Due to its Growing Use in Food & Beverage Packaging

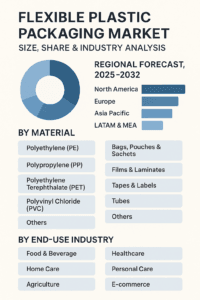

In terms of material, the market is divided into polypropylene (PP), polyethylene (PE), polyvinyl chloride (PVC), polyethylene terephthalate (PET), and others. The polyethylene (PE) segment accounts for the dominating position. The gradually surging deployment of polyethylene (PE) in food & beverage packaging is augmenting the segment growth.

Robust Expansion in the Usage of Single-use Medical Devices to Spur the Bags Segment Expansion

By product type, the market is classified into films & laminates, tubes, bags, pouches & sachets, tapes & labels, and others. The bags segment registers the largest flexible plastic packaging market share. The robust growth in the utilization of single-use medical devices, all of which are packaged in plastic bags for sterility and ease of use, is boosting the bags segment growth.

Surging Population to Fuel the Food & Beverage Segment Growth

With respect to end-use industry, the flexible plastic packaging market is categorized into e-commerce, food & beverage, agriculture, healthcare, home care, personal care, and others. The food & beverage segment witnesses the largest share. The rising population across the globe is proliferating the food & beverage segment expansion.

On the regional front, the market is segregated into the Asia Pacific, Europe, the Middle East & Africa, North America, and Latin America.

Report Coverage

The report provides a comprehensive coverage of the key driving and restraining factors impacting the market growth. In addition, it offers vital insights into the top trends, the impact of the COVID-19 pandemic on the market growth, and notable industry developments. Besides this, the report mentions the strategic measures implemented by top companies in detail.

Drivers and Restraints:

Surging Demand for Biodegradable Packaging to Escalate the Market Growth

One of the key factors propelling the flexible plastic packaging market growth is a rise in the demand for biodegradable packaging. The market is witnessing the emergence of this type of packaging as a feasible alternative to address concerns related to sustainability. It has more cost-effectiveness than eco-friendly alternatives including glass or metal.

However, the advantages offered by rigid packaging over flexible may hamper the market growth.

Regional Insights:

Asia Pacific Leads Due to Growing E-commerce Industry

The Asia Pacific market for flexible plastic packaging accounts for the largest share. This is on the back of the surging e-commerce industry in emerging countries.

North America is the second-leading region due to initiatives adopted by manufacturers for new product development.

Information Source: https://www.fortunebusinessinsights.com/flexible-plastic-packaging-market-108075

Competitive Landscape:

Leading Companies Deploy Collaboration Strategies to Introduce Innovative Products

The flexible plastic packaging market depicts a highly competitive and fragmented structure. Huhtamaki, Amcor, Sonoco Products Company, Berry Global, Sealed Air, and others are some of the key companies in the market. Many strategic measures, including joint ventures, product innovations, and capacity expansions, are being focused on by leading companies to boost their industry standing. Several companies are also focusing on collaborations to launch innovative products.

Key Industry Development:

- December 2023 - MOPI, one of the pallet stretch film suppliers, announced the launch of Hunter NanoPac Stretch Film. The film is manufactured from at least 30% recycled plastic, which reduces its ecological footprint.

- August 2023 - Dow partnered with Mengniu, a leading dairy company in China, to launch an all-polyethylene (PE) yogurt pouch designed for recyclability. The innovation supports both companies’ commitment to achieving a circular economy in China.

Tea Packaging Market Analysis of Plastic, Paperboard, and Metal Packaging 2025-2032

By ameliasss, 2025-07-23

According to Fortune Business Insights, The global tea packaging market size was valued at USD 5.99 billion in 2024. The market is projected to grow from USD 6.28 billion in 2025 to USD 8.94 billion by 2032, exhibiting a CAGR of 5.17% during the forecast period. Asia Pacific dominated the packaging market with a market share of 40.73% in 2024.

The consumption of tea has grown at a tremendous rate in recent years as individuals are becoming aware of the benefits of consuming this non-alcoholic beverage. This factor has boosted the demand for high-quality packaging to protect the freshness and quality of tea leaves. Moreover, customers are demanding sustainable packaging solutions, which will further augment the adoption of eco-friendly tea packaging solutions.

Fortune Business Insights™ displays this information in a report titled, "Tea Packaging Market, 2025-2032."

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/tea-packaging-market-109703

LIST OF KEY COMPANIES PROFILED IN THE REPORT

- Amcor plc (Switzerland)

- Berry Global (U.S.)

- Sealed Air (U.S.)

- Printpack (U.S.)

- ProAmpac (U.S.)

- Constantia Flexibles (Austria)

- ePac Flexible Packaging (U.S.)

- Swiss Pack (U.K.)

- Huhtamaki (Finland)

- Transcontinental Inc. (Canada)

- NIKITA CONTAINERS PVT. LTD. (India)

- SKS Bottle & Packaging, Inc. (U.S.)

- Packman Industries (India)

Segmentation:

Growing Need for Eco-Friendly Packaging Products Boosts Use of Paper & Paperboard Packaging Materials

Based on material, the market is segmented into plastic, paper & paperboard, metal, and others. The paper & paperboard segment has captured the largest tea packaging market share as customers are looking for eco-friendly and highly biodegradable packaging products.

Recyclable Packaging Gains Major Traction Due to Growing Demand for Sustainable Packaging

Based on type, the market is segmented into recyclable and non-recyclable. The recyclable segment is dominating the market due to the rising demand for sustainable packaging solutions. Moreover, companies are looking for new ways to decrease their impact on the environment, which is further expected to bolster the segment’s dominance.

Primary Packaging Products Become Popular Due to Increasing Need to Expand Product Lifespan

Based on packaging type, the market is segmented into primary and secondary. The primary segment accounts for the biggest market share as this type of packaging is important for expanding the lifespan of products.

Lucrative Benefits Offered by Bags Increases Their Demand for Packaging Different Tea Products

Based on product type, the market is segmented into bags, pouches, stick packs & sachets, jars & containers, boxes & cartons, and others. The bag segment has accounted for the biggest market share as there are several benefits associated with bags, such as high strength, durability, and affordability.

With respect to region, the market covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report has conducted a detailed study of the market and highlighted several critical areas, such as leading product types, materials, and top market players. It has also focused on the latest market trends and the key industry developments. Apart from the aforementioned factors, the report has given information on many other factors that have helped the market grow.

Drivers and Restraints:

Growing Need for Single-Serve Packaging to Boost Market Progress

Tea bags have become quite popular among customers in recent years as they are quite easy to use. Moreover, these bags come in a wide variety of options, such as black, herbal, and green tea. This factor is also contributing to their popularity. In addition to this, tea bags come with one-time use and serve a wide range of settings, ranging from railways, corporate offices, and restaurants, further boosting their use and contributing to the tea packaging market growth.

However, the incorporation of plastic in tea packaging products and the hazards associated with plastics can impede the market’s progress.

Regional Insights:

Asia Pacific Dominates Market Due to High Consumption of Tea

Asia Pacific holds a dominant global tea packaging market share as countries, such as India, China, and other developing countries are the top consumers of tea. Moreover, these nations are the leading producers of tea, which will further increase the demand for tea packaging products.

Europe is the second-dominant region in the global market as many European countries consume tea in large quantities.

Information Source: https://www.fortunebusinessinsights.com/tea-packaging-market-109703

Competitive Landscape:

Key Market Participants to Launch Novel Packaging Solutions to Expand Their Customer Base

The market is highly fragmented and competitive as a small share of companies are leading the market’s growth. These companies are focusing on launching innovative packaging solutions to increase their market share and expand their customer base.

Notable Industry Development:

- September 2023 - The Mitsubishi Chemical Group introduced BioPBS, a bio-based compostable polymer, in EN TEA teabag pouches. The pouches include a sealant layer, zipper closure including adhesives, and a barrier layer.

- March 2021 - Dorset Tea, a premium tea brand, announced the launch of tea bags that are fully sustainable. These bags are made using PLA, a type of plastic manufactured from vegetable starch and wood pulp.