According to Fortune Business Insights, The global polyacrylamide market size was valued at USD 4.22 billion in 2024. The market is projected to grow from USD 4.37 billion in 2025 to USD 6.69 billion by 2032 at a CAGR of 6.3% during the forecast period. Asia Pacific dominated the polyacrylamide market with a market share of 44.54% in 2024.

The global polyacrylamide market size is prophesized to gain impetus from rapid industrialization that promoted the demand for polyacrylamide for water treatment applications. Polyacrylamide or PAM is a synthetic polymer used for the flocculation of solids in a liquid for water treatment procedures, or paper-making, among others. An upcoming report by Fortune Business Insights™ titled, “ Polyacrylamide Market Size, Share & Industry Analysis, By Type (Cationic, Anionic, Non-ionic), By Application (Water Treatment, Oil & Gas, Paper Making, Others) Others and Regional Forecast, 2025-2032,” provides a 360-degree overview of the market and its prime growth trajectories.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/polyacrylamide-market-102196

List of Key Players Functioning in Polyacrylamide Market are as follows :

- Anhui Tianrun Chemicals Co. Ltd.

- Black Rose Chemicals

- Chinafloc

- Ashland Inc.

- SINOPEC

- Xitao Polymer Co. Ltd.

- Shuiheng Chemicals

- Kemira

- BASE SE

- SNF Group

- Envitech Chemical Specialties Pvt. Ltd.

- Other Players

What are the Objectives of the Report?

The report offers a comprehensive overview of the market and important parameters such as drivers, restraints, upcoming opportunities and challenges of the market. It also analyses the table of segmentation in detail considering all sub-segments such as application, type, and geography. The report further discusses the names and key strategies of key players to gain more revenue in the market. Furthermore, the report highlights key industry developments, current polyacrylamide market trends, and other interesting insights into the market. The report is available for sale on the company website.

Market Drivers

Increasing Application from Food and Beverage Industry to Add Impetus to Market

Polyacrylamide is a high molecular weight water-soluble polymer that is created from acrylamide and is used as a suspending agent or thickener. Therefore they are in high demand from paper pulp, oil and gas, wastewater treatment, and other applications. This acts as a major polyacrylamide market growth drivers. Besides this, polyacrylamide can also be used as soil conditioners for increasing the porosity, aeration, soil tilth, and reduce compaction, water run-off, and dustiness of water. This will also aid in the expansion of the market in the forecast period. Apart from this, polyacrylamide is also used in enhanced oil recovery, thus adding impetus to market growth.

On the contrary, the side effects of using polyacrylamides such as clumsiness, muscle weakness, unsteadiness, sweating, and numbness in hands and feet may cause hindrance to the overall market in the coming years. Nevertheless, the rising applications in food and beverage, coal mining, oil and gas, aquaculture and others will create lucrative growth opportunities for the market in the forecast duration.

Regional Segmentation:

Asia Pacific is Dominating Market with Rapid Industrialization

From a regional viewpoint, the global polyacrylamide is widespread into the regions of Asia Pacific, North America, Latin America, Europe, and the Middle East and Africa. Every region is further categorized on the basis of their nations they include. Among these, Asia Pacific is holding the dominant polyacrylamide market share owing to rapid industrialization and the need for water treatment especially in nations such as Japan, China, India, and others. In addition to that, China is increasing the demand for water treatment chemicals, owing to the increasing number of pharmaceutical and chemical industries in the country and this will promote the market growth in the forecast duration

On the other side, the North America market will witness notable growth on account of stringent regulations imposed on wastewater disposal from factories that propelled the demand for polyacrylamide. Besides this, the high use of technology for water purification and recycling will help Europe market to gain impetus in the coming years. The market in Latin America and the Middle East and Afrcia will witness significant growth on account of the increasing need for wastewater treatment and the growing use of polyacrylamide in oil and gas applications.

Information Source: https://www.fortunebusinessinsights.com/polyacrylamide-market-102196

Competitive Landscape:

Vendors Focusing on Brand Expansion for Gaining Competitive Edge

Companies are entering into mergers and acquisitions, company collaborations, contracts, agreements, and partnerships and joint ventures for holding the lion’s share in the market. They are also investing heavily in product development and manufacturing to attract high polyacrylamide market revenue in the forecast duration. Furthermore, companies are focusing on brand expansion to various geographies to gain momentum in the market competition.

Flexible Paper Packaging Market Latest Technological Advancements Analysis to 2032

By ameliasss, 2025-07-15

According to Fortune Business Insights, The global flexible paper packaging market size was valued at USD 117.82 billion in 2023 and is projected to grow from USD 123.82 billion in 2024 to USD 200.02 billion by 2032, exhibiting a CAGR of 6.18% during the forecast period. Asia Pacific dominated the flexible paper packaging market with a market share of 35.06% in 2023.

Flexible paper packaging is a crucial part of the packaging industry that concentrates on the manufacturing, sale, and usage of packaging solutions. These packaging solutions are specifically designed from paper materials that provide flexibility in form and function. Key players prefer lighter-weight packaging solutions to decrease delivery costs and enhance logistics. This packaging decreases the overall weight of packaged products without compromising product safety. The surging adoption of lightweight packaging solutions and a rise in circular economy efforts in packaging is fostering market expansion.

F ortune Business Insights presents this information in their report titled " Flexible Paper Packaging Market , 2024–2032."

List of Key Players Profiled in the Report

- International Paper (U.S.)

- Mondi Group (U.K.)

- NIPPON PAPER INDUSTRIES CO., LTD. (Japan)

- Amcor Limited (Switzerland)

- Smurfit Kappa (Ireland)

- PBFY Flexible Packaging (U.S.)

- Novolex (U.S.)

- TedPack Company Limited (China)

- Northeastern Envelope Company (U.S.)

- DS Smith (U.K.)

- ProAmpac (U.S.)

- Winpak LTD. (Canada)

- Tesa (Germany)

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/flexible-paper-packaging-market-108352

Segments

Kraft Paper Leads the Market Owing to Its Excellent Strength and Durability

By type, the market is classified into kraft paper, parchment paper, greaseproof paper, and glassine paper. Kraft paper takes the lead in the global market with its excellent strength and durability. Kraft paper can endure heavy weights and irregular handling, particularly in industrial and e-commerce packaging.

With Versatility, Bags and Sacks Hold Top Position in the Market

On the basis of product type, the market is divided into wraps, bags and sacks, envelopes, pouches, sachets, and others. Bags and sacks command the global market as they are extremely versatile. Increased usage of bags and sacks in food and beverage, retail, agriculture, and personal care industries is also fueling segment expansion.

Increasing Consumer Preference for Ready-to-eat Food Products Makes the Food Industry a Leading Segment

In terms of the end-use industry, the market is segregated into food, personal care & cosmetics, pharmaceuticals, consumer goods, and others. The food industry emerges as a dominant segment in the global market as a result of increasing consumer preference for packaged and ready-to-eat food products. Surging demand for flexible paper packaging for snacks, bakery items, and dry foods is assisting segment growth.

On a regional scale, the market is divided into distinct regions, such as North America, the Middle East & Africa, Asia Pacific, Europe, and Latin America.

Report Coverage

The market research report presents a comprehensive market study, emphasizing important elements, such as the competitive environment and prominent product categories. Moreover, the report offers crucial insights on market trends and noteworthy industry developments. In addition to the factors above, the report contains numerous aspects that have nurtured market expansion in recent times.

Drivers and Restraints

Rapid Expansion of the E-commerce Industry and Food Delivery Services to Boost Market Growth

There is an increased demand for lightweight, cost-effective, and efficient packaging solutions due to the rapid growth of e-commerce and food delivery facilities. Flexible paper packaging can meet these demands as it is durable, versatile, and lightweight. With an increase in home deliveries and online shopping trends post-pandemic, companies are widely using flexible paper packaging to guarantee product security, improve branding prospects, and accomplish the flexible packaging consumer requirements for sustainable delivery options.

In contrast, inadequate barrier properties and recycling difficulties are impeding the flexible paper packaging market growth.

Regional Insights

Rapid Urbanization Fuels Market Progress in Asia Pacific

Asia Pacific dominates the flexible paper packaging market share attributed to increased urbanization, surging disposable income, and shifting consumer inclination toward sustainability. As per the Federation of Paper Traders’ Associations of India (FPTA), Asia Pacific has attracted around 60% of global investments in new paper machinery over the last 20 years. The region’s producers have adopted technologies, including both entry-level systems and sophisticated, high-performance production lines.

North America accounts for a significant market share, fueled by the rapid expansion of the food and beverage industry and surging demand for sustainable and recyclable packaging solutions in the ready-to-eat and convenience food sectors. Growing consumer consciousness about sustainability and the environmental effect of plastic packaging in the U.S. is also driving market expansion in the region.

Get a Information of Full Report: https://www.fortunebusinessinsights.com/flexible-paper-packaging-market-108352

Competitive Landscape

Top Players Offer Advanced Solutions to Secure their Market Positions

The market analysis emphasizes significant advancements made by these producers. Prominent flexible paper packaging solution providers include International Paper, Mondi Group, NIPPON PAPER INDUSTRIES CO., LTD, Amcor Limited, Smurfit Kappa, and PBFY Flexible Packaging. Additionally, many other firms remain vigilant of industry trends and strive to deliver cutting-edge solutions to secure their positions in the evolving market.

Key Industry Development

- April 2024 – Klöckner Pentaplast (kp), a significant food packaging industry company, declared the launch of the first food packaging trays comprising 100% recycled PET (rPET) deriving from trays. The newly launched kp tray is the first to be composed entirely of recycled tray material. This innovation is the major result of KP's Tray2Tray initiative, intending to rewrite the PET recycling rules. The president of food packaging at KP also stated that this achievement is a breakthrough in the packaging industry.

Green Building Materials Market Sees Strong Investment Flow Toward Sustainability by 2032

By ameliasss, 2025-07-15

According to Fortune Business Insights, The global green building materials market size was valued at USD 422.27 billion in 2023 and is projected to grow from USD 474.21 billion in 2024 to USD 1,199.52 billion by 2032, exhibiting a CAGR of 12.3% during the forecast period. North America dominated the green building materials market with a market share of 32.05% in 2023. An environment-friendly building structure is made from green building materials. Straw, hempcrete, wood, bamboo, bales, recycled plastic, and ferrock are some of these materials. They are used to create structures that are low-energy and support the ecological balance of the environment. Fortune Business Insights presents this information in their report titled "Green Building Materials Market, 2024–2032."

List of Key Players Profiled in the Report

- BASF SE (Germany)

- PPG Industries, Inc. (U.S.)

- I. du Pont de Nemours and Company (U.S.)

- Sika AG (Switzerland)

- Forbo International SA (Switzerland)

- Owens Corning (U.S.)

- REDBUILT (U.S.)

- CERTAINTEED (U.S.)

- HOLCIM (Switzerland)

- Kingspan Group (Ireland)

Segments:

Roofing Segment to Grow Due to its Growing Product Usage in Construction

Based on application, the market is segmented into roofing, flooring, insulation, and others.

Due to the growing popularity of green roofing materials, it is predicted that the roofing segment will continue to be the largest over the projection period. As Nature-based Solutions (NBS) address a number of environmental and socioeconomic issues brought on by climate change, green roofs are becoming more and more important. Given that urban areas already house 55% of the world's population and are expected to grow by as much as 68% by 2050, urban areas are garnering attention in terms of global development. Suburbs, cities, and towns are all part of urban settlements. Urban growth is necessary for urban settlements to flourish sustainably. The New Urban Agenda and the Sustainable Development Goals for 2030 promote cities' commitment to sustainability.

High Preference for Green Buildings will Dominate the Residential Segment

Based on end-use industry, the market is segmented into residential and non-residential.

Due to increase in regulations and rules requiring energy-efficient buildings, the residential segment is anticipated to dominate during the projection period. In the residential sector, green buildings are becoming more popular. Building materials that are both eco-friendly and energy-efficient are now in demand. The main factors driving the market expansion of this category are the growing awareness of the environmental advantages of sustainable building materials and the expanding use of sustainable building methods in the residential sector. Additionally, government regulations and initiatives to encourage the use of eco-friendly building materials in the residential sector, as well as the rising demand for energy-efficient and environment-friendly homes, are likely to propel the green building materials market growth.

Report Coverage:

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into the regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- Latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints:

Increasing Demand for Green Materials Buildings will Propel Market

Wood, straw hemp concrete, recycled plastic, ferrock, straw bales, bamboo rammed earth, wood concrete, and grass concrete are examples of green building materials. The purpose of using these materials is to build structures that are energy-efficient and support the ecological balance of the environment. During construction, design, repair, and maintenance, these materials increase a building's sustainability and efficiency. These materials are made from renewable waste sources and are particularly energy-efficient. Environmental issues including freshwater resource contamination, air pollution, resource depletion, biodiversity loss, and atypical climate change can all be resolved by using environment-friendly building materials. Green building materials are ideal replacements for conventional construction materials, and due to these benefits, the green building materials market share will increase in the coming years.

On the contrary, high demand, fluctuation in price of materials, and declining per capita income in some countries are few factors which may impede the market growth.

Regional Insights

North America Dominates the Market due to High Demand for Infrastructure Applications

Due to its rising demand for roofing, insulation, framing, and numerous other residential, industrial, commercial, and infrastructure applications, North America held the biggest market share in 2022. There is expanding need for buildings that are both energy and value-efficient and reduce their negative effects on the environment. Reduced energy expenses are economic advantages of green buildings. Increased government initiatives have accelerated the market's expansion.

Get a Full Information of Report: https://www.fortunebusinessinsights.com/green-building-materials-market-102932

Competitive Landscape

Businesses Use Strategic Planning to Expand their Market Share

Market players face severe competition from national and regional firms that have vast supply chains, regulatory expertise, and suppliers. In order to grow their present markets, businesses also enter into agreements, make purchases, and form strategic alliances with other industry leaders.

Key Industry Development:

- January 2022: Binderholz GmbH, a subsidiary of the Austrian Binderholz Group, acquired BSW Timber Ltd. The company manufactures more than 1.2 million m3 of sawn timber annually. With this acquisition, Binderholz GmbH became Europe's largest sawmill and solid wood processor.

- April 2021: Lafarge Egypt, a member of LafargeHolcim, introduced Ecolabel cement for the first time in Egypt. This new product meets the company's green criteria and reduces the carbon footprint.

According to Fortune Business Insights, The global base oil market size was valued at USD 41.81 billion in 2023. The market is projected to grow from USD 42.95 billion in 2024 to USD 54.79 billion by 2032, exhibiting a CAGR of 3.1% during the forecast period. Asia Pacific dominated the base oil market with a market share of 48.43% in 2023.

Base oil is an essential part of the global petroleum industry, which plays a crucial role in the production of various lubricants and oils. It is divided into different groups based on its refining process and properties, ranging from Group I to Group V. The market dynamics of material are influenced by factors such as technological advancements, regulatory standards, and the demand for higher-quality lubricants.

Key Market Insights

✅ Market Size and Growth Rate

2023 Market Value: USD 41.81 billion

2024 Estimate : USD 42.95 billion

2032 Forecast : USD 54.79 billion

CAGR (2024–2032) : 3.1%

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/base-oil-market-110063

Market Drivers

Rising Automotive Production

An increase in vehicle manufacturing, particularly in emerging economies, is fueling demand for high-performance engine oils, greases, and transmission fluids — all of which use base oils as key components.

Expanding Industrial Activities

The resurgence of industrial operations in sectors such as mining, energy, manufacturing, and construction is boosting lubricant consumption, thus propelling base oil demand.

Shift Towards Group II & III Base Oils

With stricter environmental regulations and technological advancements, the market is rapidly moving toward Group II and III base oils due to their superior performance and lower sulfur content.

List of Top Base Oil Companies :

- Chevron Corporation (U.S.)

- Shell plc (U.K.)

- Saudi Aramco Base Oil Company - Luberef (Saudi Arabia)

- Abu Dhabi National Oil Company (ADNOC) (UAE)

- Bahrain Petroleum Company (BAPCO) (Bahrain)

- Sepahan Oil Company (Iran)

- GS Caltex Corporation (South Korea)

- PETRONAS Lubricants International (Malaysia)

- Orlen S.A. (Poland)

- Exxon Mobil Corporation (U.S.)

Market Segmentation

By Group

Group I : Cost-effective but being phased out due to environmental concerns

Group II : High-quality oils widely used in modern lubricants

Group III : Premium base oils used in synthetic and semi-synthetic lubricants

Group IV & V : Synthetic and specialty base oils for high-performance applications

By Application

Automotive Oil

Industrial Oil

Hydraulic Oil

Greases

Metalworking Fluids

Others

Regional Insights

Asia-Pacific Dominance

Asia-Pacific leads the global base oil market, accounting for nearly 48.43% of total market share in 2023. Countries like China, India, South Korea, and Japan are driving demand due to rapid industrialization, a booming automotive sector, and significant investments in infrastructure.

Other Key Regions

North America : Steady growth due to demand for synthetic lubricants and advancements in automotive technology.

Europe : Increasing focus on sustainability and high-efficiency lubricants.

Middle East & Africa : Growth in oil & gas operations and industrial sectors.

Trends & Opportunities

Bio-Based and Renewable Base Oils

As sustainability becomes a core priority, manufacturers are investing in renewable and biodegradable base oils to meet regulatory compliance and consumer preferences.

Demand for High-Performance Lubricants

With evolving automotive technology, there is a growing need for lubricants that offer extended drain intervals, oxidation stability, and fuel efficiency — opening up demand for premium base oils.

🚙 Growth of Electric Vehicles (EVs)

While EVs may reduce conventional engine oil demand, they create opportunities for thermal fluids and specialty lubricants for EV systems, battery cooling, and gearboxes.

Challenges

Volatility in Crude Oil Prices : Impacts production cost and profit margins

Stringent Environmental Regulations : Necessitates shift to cleaner base oil technologies

Supply Chain Disruptions : Can affect global trade and refinery operations

Read Full Information of Report: https://www.fortunebusinessinsights.com/base-oil-market-110063

Future Outlook

The base oil market is set to expand steadily, backed by industrial recovery, increasing automotive demand, and the growing need for advanced lubricants. The transition to Group II/III and synthetic base oils, along with innovations in bio-based alternatives, will shape the future of the industry. Companies focusing on technological upgrades, sustainability, and regional expansion are well-positioned to capture emerging opportunities in this evolving market landscape.

KEY INDUSTRY DEVELOPMENTS :

- January 2024 – Shell Deutschland GmbH decided to convert the Wesseling site's hydrocracker into a unit for producing Group III base stock. These oils are used in high-quality lubricants, including engine oils and transmission fluids. The hydrocracker converts heavy, low-quality hydrocarbons into lighter, high-quality products through a high-pressure, high-temperature reaction with hydrogen in the presence of a catalyst.

- October 2023 – Idemitsu Kosan Co., Ltd. partnered with Saudi Aramco Base Oil Company -Luberef, and signed an MOU regarding the supply of refined lubricant base oil "Gr.III." This agreement aims to construct a new Gr.III manufacturing facility in Saudi Arabia to secure long-term stable procurement of Gr.III base stock.

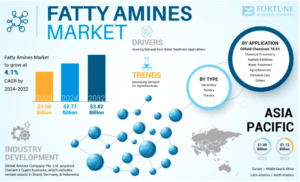

According to Fortune Business Insights, The global fatty amines market size was valued at USD 2.68 billion in 2023. The market is projected to grow from USD 2.77 billion in 2024 to USD 3.82 billion by 2032, exhibiting a CAGR of 4.1% during the forecast period. Asia Pacific dominated the fatty amines market with a market share of 42.16% in 2023.

Fatty amines are a diverse class of oleochemicals derived from natural oils and fats. These compounds possess excellent surfactant properties, enabling their utilization across various industries. The fatty amine family encompasses primary, secondary, and tertiary amines, with commercially significant examples including tallow amine, oleylamine, and coco amine. The growing need for clean water in industrial applications and the effects of climate change, which has resulted in global water scarcity, are driving the demand for fatty amines.

Fortune Business Insights™ displays this information in a report titled, " Fatty Amines Market, 2024-2032".

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/fatty-amines-market-102901

LIST OF KEY COMPANIES PROFILED IN THE REPORT:

- Clariant (Switzerland)

- AkzoNobel (Netherlands)

- Global Amines (Singapore)

- Kao Chemicals Global (Japan)

- Evonik Industries Ag (Germany)

- Arkema (France)

- Nouryon (Netherlands)

- Vantage Leuna GmbH (U.S.)

- Indo Amines Limited (India)

- Huntsman International LLC. (U.S.)

- Ecogreen Oleochemicals (Singapore)

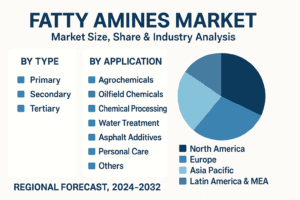

Segmentation:

Tertiary Amines to be Extensively Adopted Owing to Widespread Demand in Several Sectors

Based on type, the market is segmented into primary, secondary, and tertiary. The tertiary segment dominated the market in 2023 and is expected to dominate the market. The segment’s growth can be attributed to the widespread demand for tertiary amines across various industries for diverse applications, including fuel additives, ore floatation, corrosion inhibitors, and chemical intermediates.

Agrochemicals Segment Holds Leading Position Owing to Rising Need for Plant Protection

Based on application, the market is segmented into agrochemicals, oilfield chemicals, chemical processing, water treatment, asphalt additives, personal care, and others. The agrochemicals segment dominated the global market in 2023 as the shift in global climate patterns rendered various crops vulnerable to insects and fungi infestations, subsequently impacting crop yields.

The market is studied regionally across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The report has conducted a detailed study of the market and highlighted several critical areas, such as leading companies, sources, and prominent product applications. It has also focused on the latest market trends and highlights vital industry developments and market outlook. Apart from the aforementioned factors, the report has given information on many other factors that have helped the market grow.

Drivers and Restraints:

Rising Demand from Water Treatment Industry to Aid Market Growth

Fatty amines are a class of compounds derived from raw materials, such as fats, petrochemicals, and oils that contain nitrogen. These compounds can have either a single carbon chain or a combination of carbon chains. Commercially available fatty amines are typically manufactured through the distillation of fatty acids or the reaction of fatty alcohols with ammonia. These compounds have widespread applications in water treatment processes to cater to the rising scarcity of water across the world.

However, the fatty amines market growth may face challenges due to uncertain commodity prices and strict government regulations regarding the hazardous effects of these compounds.

Regional Insights:

Asia Pacific Dominated Market Due to Rapid Growth of Agriculture Industry

Asia Pacific was valued at USD 1.13 billion in 2023, representing the largest global fatty amines market share. The region’s dominance can be attributed to the rapid growth of the agriculture industry and increasing consumer spending in the region.

North America and Europe are experiencing significant growth and expected to continue their trend in the future driven by the presence of oilfield chemicals and chemical processing industries in these regions.

Competitive Landscape:

Companies to Focus on Acquisition Deals with Small Regional Players to Increase Their Global Presence

The leading companies operating in this market include Clariant, Global Amines, AkzoNobel, Kao Chemicals Global, Nouryon, Evonik Industries Ag, Arkema, and others. They are also increasing their focus on undertaking various strategic initiatives, such as entering acquisition deals with small regional players and making use of local networks to increase their global presence.

Get a Full Information of Report: https://www.fortunebusinessinsights.com/fatty-amines-market-102901

Notable Industry Development:

- June 2023: Global Amines Company Pte. Ltd. acquired Clariant’s Quats business, which includes certain assets in Indonesia, Germany, and Brazil. Quats are a group of chemicals used for a range of applications, such as surfactants, preservatives, and antistatic agents. Qauts are utilized in industrial, commercial, and consumer products.

- October 2019: Nouryon launched a demonstration plant in Sweden to display a more sustainable and revolutionary technology platform for manufacturing ethylene amines and their derivatives. The technology is a form of ethylene oxide (EO) that supports the selective production of various end products, empowering Nouryon to enlarge its ethylene amine product offering.

Polybutadiene Rubber Market Report: Size, Share & Growth Analysis 2025-2032

By ameliasss, 2025-07-11

Market Size & Growth

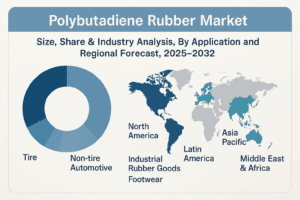

According to Fortune Business Insights, The global polybutadiene rubber market size was valued at USD 9.41 billion in 2024. The market is projected to grow from USD 9.86 billion in 2025 to USD 13.73 billion by 2032, exhibiting a CAGR of 4.8% during the forecast period.

Polybutadiene rubber (PBR), also referred to as butadiene rubber (BR), is a type of synthetic rubber made by polymerizing 1,3-butadiene, a petroleum-based monomer. Classified as an elastomer, it is known for its high resilience, superior abrasion resistance, low glass transition temperature, and remarkable elasticity, enabling it to regain its original shape after being stretched or compressed.

What is Polybutadiene Rubber?

Polybutadiene (BR) is a synthetic elastomer created by polymerizing 1,3‑butadiene. It’s prized for its high resilience, abrasion resistance, low glass transition temperature, and ability to rebound after deformation. Primarily used in high‑performance applications, approximately 70% of PBR is consumed in tire production, while the rest serves as an additive in plastics, golf balls, footwear, and more.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/polybutadiene-rubber-market-113414

LIST OF KEY POLYBUTADIENE RUBBER COMPANIES PROFILED

- ARLANXEO (Netherlands)

- Indian Oil Corporation Ltd (India)

- Reliance Industries Limited (India)

- ENEOS Materials Corporation (Japan)

- Goodyear Tire and Rubber Company (U.S.)

- SIBUR International GmbH (Austria)

- LANXESS (Germany)

- KURARAY CO., LTD. (Japan)

- JSR Corporation (Japan)

- Kumho Petrochemical (South Korea)

Key Market Drivers

1. Automotive & Tire Manufacturing

Superior properties such as low rolling resistance and abrasion resistance favor PBR for tire treads and sidewalls.

With global automotive output climbing, so does the demand for PBR.

2. Infrastructure & Construction Boom

PBR’s flexibility , durability , and weather resistance make it ideal for infrastructure projects like conveyor systems and expansion joints.

Market Trends & Opportunities

Sustainability Push

A growing preference for eco-friendly materials is driving manufacturers to develop bio-based PBR and expand recycling capabilities.

Expanded Use in Consumer Goods

PBR is increasingly used in footwear (soles) , sports equipment , and consumer industrial goods due to its performance benefits.

Challenges Facing the Market

Health Concerns

Exposure to PBR may irritate the eyes, respiratory tracts, and cause neurological symptoms at high levels, prompting stricter workplace regulations.

Environmental Regulations & Production Costs

Emissions, hazardous waste, and mandated clean production are raising compliance costs and entry barriers.

Trade Protectionism

Tariffs and import restrictions may inflate costs and disrupt supply chains.

Segmentation Breakdown

| Segment | Market Role |

|---|---|

| Tire | Dominating segment due to abrasion resistance and durability |

| Non-Tire Automotive | Used in seals, gaskets, and flexible vehicle components |

| Industrial & Footwear | Utilized for soles, industrial goods, and equipment components |

| Others | Includes golf balls, hoses, plastic additives, industrial pads |

- Asia Pacific leads the market, holding over half of global volume (~USD 5.04 billion in 2024), driven by growth in China, India, and Japan.

- North America benefits from a strong automotive and industrial base, though environmental compliance adds pressure.

- Europe is focusing on sustainable production with moderate growth.

- Latin America , Middle East & Africa are emerging markets with infrastructure-led opportunities and slower economic momentum.

Notable developments:

- Arlanxeo launched a 65 ktpa PBR plant in Brazil (Feb 2023).

- Indian Oil planned a 60 ktpa PBR plant in Panipat, India (Mar 2022).

- SIBUR upgraded its Voronezh Nd-BR plant to enhance efficiency (Feb 2019).

- Global synthetic rubber demand

Strategic Insights

- For Investors: The projected growth and shift to green polymers make PBR production and recycling ventures attractive.

- For Manufacturers: Specializing in bio-based and recycled PBR, while prioritizing emissions control, opens new markets.

- For End-Users: Automotive OEMs benefit from PBR’s performance, especially in sustainable and fuel-efficient vehicle production.

The Polybutadiene Rubber market is poised for robust growth driven by rising automotive production, infrastructure expansion, and sustainability initiatives. Despite environmental and regulatory challenges, innovation in bio-based materials and strategic expansion by major players will shape the industry’s future across global markets.

Information Source: https://www.fortunebusinessinsights.com/polybutadiene-rubber-market-113414

KEY INDUSTRY DEVELOPMENTS

-

February 2023: Arlanxeo announced the launch of a polybutadiene rubber production facility with a capacity of 65 ktpa in southern Brazil. Located within the Triunfo petrochemical complex in Rio Grande do Sul, this new plant emphasizes the company's commitment to enhancing its presence in Latin America.

-

March 2022: Indian Oil Corporation Limited planned to build a 60 ktpa polybutadiene rubber (PBR) facility at the current naphtha cracker complex located in Panipat. The project involves an investment of INR 14.6 billion (USD 169 million). It plans to obtain the necessary feedstock, butadiene, from the 138 ktpa butadiene extraction unit (BDEU) already operating within the Panipat complex.

Polyvinyl Chloride (PVC) Market Investment Feasibility and Growth Factors 2030

By ameliasss, 2025-07-11

According to Fortune Business Insights, The global polyvinyl chloride market size was valued at USD 68.96 billion in 2022 and is expected to grow from USD 72.08 billion in 2023 to USD 95.88 billion by 2030, exhibiting a CAGR of 4.2% during the forecast period. Asia Pacific dominated the polyvinyl chloride [pvc] market with a market share of 56.19% in 2023.

Polyvinyl chloride is deployed in an extensive range of applications including electrical & electronics, packaging, transportation, healthcare, and construction. The industry expansion can be attributed to its versatile nature of bonding with several polymers.

Fortune Business Insights™ provides this information in its research report, titled “Polyvinyl Chloride (PVC) Market, 2023-2030”.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/polyvinyl-chloride-pvc-market-109398

List of Key Players Mentioned in the Report:

- Ercros (Spain)

- Formosa Plastics Corporation (Taiwan)

- Hanwha Group (South Korea)

- Ineos (U.K.)

- KEM ONE (France)

- Occidental Petroleum Corporation (U.S.)

- Orbia (Mexico)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Vynova (Belgium)

- Westlake Corporation (U.S.)

Segmentation:

Rigid Segment Accounted for Major Share Considering Increasing Product Deployment for Water Supply and Irrigation

On the basis of product type, the market for polyvinyl chloride is bifurcated into flexible and rigid. The rigid PVC segment held a prominent market share in 2022. This can be credited to the extensive product usage for irrigation, drainage, and water supply on account of corrosion resistance and durability.

Pipe & Fittings Segment to Lead the Market Due to Rising PVC Usage on Account of Durability

On the basis of application, the market for polyvinyl chloride is subdivided into flooring, pipe & fittings, wire & cables, profiles, film & sheet, and others. The pipe & fittings segment is set to dominate the global market over the study period owing to its sustainability and durability, making it a suitable choice for water transportation.

Building & Construction Segment Accounts for Key Share Driven by Extensive Product Adoption

On the basis of end use, the market for polyvinyl chloride is fragmented into packaging, building & construction, electrical & electronics, automotive, and others. The building & construction segment holds the largest share due to its wide product deployment in the construction sector in roofing, cables, profiles, and accessories.

Based on geography, the market for polyvinyl chloride (PVC) has been analyzed across North America, Latin America, Asia Pacific, Europe, and the Middle East & Africa.

Report Coverage:

The report gives an account of the key steps deployed by leading companies to strengthen their market share. It further gives an insight into the vital trends in the market. An analysis of the industry based on numerous segments has also been presented in the report: product type, application, end use, and geography.

Drivers and Restraints:

Surge in Market Value Owing to Growing Demand from Construction Sector

There has been a rise in product application across the construction industry, where it is used for cables, pipes, and roofing materials. The insulating properties of PVC make it a preferred material, ensuring reliability and safety in power distribution. These factors are expected to propel polyvinyl chloride (PVC) market growth.

However, regulatory concerns associated with the release of hazardous chlorine-based byproducts during the manufacturing process may restrain the industry expansion.

Regional Insights:

Asia Pacific to Dominate Owing to Surging Demand in Infrastructure Development and Construction

Asia Pacific polyvinyl chloride (PVC) market share is anticipated to hold a key position in the global market. The region has recorded an increasing product demand in the infrastructure development, construction, and manufacturing sectors.

The North America market size is set to surge considering the rise in construction activities in the region and the escalated product usage in an array of construction applications.

Information Source: https://www.fortunebusinessinsights.com/polyvinyl-chloride-pvc-market-109398

Competitive Landscape:

Industry Players Focus on Investing in Bio-based Products to Cater to Rising Demand

Major industry participants are investing in the development of products made from bio-based materials. These products are being introduced for meeting the soaring demand for green products. KEM ONE and Ineos are some of the key players in the market.

Key Industry Development:

- December 2023 – INEOS launched a new rage of PVC product that has 37% lower carbon footprint than the average carbon footprint of suspension PVC produced in the European Industry.

- July 2023 - Chemplast Sanmar Ltd. shared plans to invest USD 120 million to expand its production capacities of the Specialty Paste PVC unit at Cuddalore and the Custom Manufactured Chemicals Division’s (CMCD) unit at Berigai.

Cellulose Esters Market Size, Share & Industry Analysis (2025-2032)

According to Fortune Business Insights, The global cellulose esters market size was valued at USD 4.63 billion in 2024. The market is projected to grow from USD 4.87 billion in 2025 to USD 6.89 billion by 2032, exhibiting a CAGR of 5.1% during the forecast period.

The global cellulose esters market is projected to witness substantial growth from 2025 to 2032, driven by increasing demand across diverse end-use industries such as textiles, food, pharmaceuticals, paints & coatings, and construction. Cellulose esters are derived from natural cellulose and are widely recognized for their superior film-forming, binding, and thickening properties, making them highly valuable in a wide array of industrial applications.

The cellulose esters market size is anticipated to grow steadily over the forecast period, fueled by innovations in biodegradable and sustainable materials. With increasing environmental concerns and stricter regulations on synthetic polymers, cellulose esters are emerging as eco-friendly alternatives.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/cellulose-esters-market-113410

LIST OF KEY CELLULOSE ESTER COMPANIES PROFILED

- Eastman Chemical Company (U.S.)

- AkzoNobel (Netherlands)

- Borregaard AS (Norway)

- Daicel Corporation (Japan)

- Sichuan Push Acetati Co., Ltd. (China)

- Celanese Corporation (U.S.)

- Alpha Chemika (India)

- Mitsubishi Chemical Group Corporation (Japan)

- RYAM (U.S.)

- Georgia-Pacific (U.S.)

Key Market Segmentation

By Type:

- Cellulose Acetate – Dominates the market due to its wide usage in textiles, photographic films, and cigarette filters.

- Cellulose Acetate Propionate (CAP) – Valued for high transparency and low odor, used in personal care and packaging.

- Cellulose Acetate Butyrate (CAB) – Popular in automotive coatings and plastic applications for its toughness and flexibility.

- Cellulose Nitrate – Used in lacquers and printing inks.

- Others – Includes specialized esters for niche applications.

By End-Use Industry:

- Textiles – Utilized for producing high-performance, breathable fabrics.

- Food – Acts as a thickening and stabilizing agent in food formulations.

- Chemical Synthesis – Used in making specialty chemicals and intermediates.

- Pharmaceuticals – Enhances tablet coatings and drug delivery systems.

- Construction – Incorporated into paints, adhesives, and sealants.

- Paper & Pulp – Improves printability and strength.

- Paints & Coatings – Enhances film properties and durability.

- Others – Includes cosmetics, printing inks, and plastic products.

Market Drivers

- Rising Demand for Eco-Friendly Materials : Cellulose esters are biodegradable and derived from renewable sources, aligning with the global sustainability movement.

- Growing Pharmaceutical and Food Sectors : Increased demand for safe and effective excipients in drug and food formulations is driving market growth.

- Boom in Automotive and Construction Sectors : High usage of CAB and CAP in coatings and construction materials is positively influencing the market.

- Technological Advancements : Innovations in manufacturing processes have improved performance characteristics, enhancing product adoption.

Regional Insights

- North America is a mature market, with strong demand from the pharmaceutical and paints & coatings sectors.

- Europe shows steady growth, driven by strict environmental regulations and focus on green chemistry.

- Asia Pacific is the fastest-growing region due to booming construction, automotive, and food industries, particularly in China and India.

- Latin America and the Middle East & Africa are emerging markets with increasing industrial activities and urbanization.

Market Trends

- Focus on Bio-Based Alternatives : Shift toward non-toxic, biodegradable cellulose esters.

- Expansion in Personal Care Applications : Cellulose esters are increasingly used in skincare and cosmetics.

- Growth in 3D Printing : Cellulose-based materials are being explored for additive manufacturing.

Competitive Landscape

Leading players in the cellulose esters market are focusing on strategic mergers, partnerships, and capacity expansions to strengthen their market position. Continuous investment in R&D to develop high-performance, sustainable cellulose ester variants is a core strategy.

The cellulose esters market is expected to grow consistently through 2032, underpinned by sustainability trends and increasing demand from high-growth sectors. As industries seek alternatives to synthetic polymers, cellulose esters stand out as versatile, biodegradable solutions aligned with circular economy principles.

The global cellulose esters market is poised for strong growth, driven by its multifaceted applications and increasing preference for sustainable materials. Innovations in formulation and application, along with favorable regulatory support, will further cement the role of cellulose esters in the future of industrial chemistry.

Information Source: https://www.fortunebusinessinsights.com/cellulose-esters-market-113410

KEY INDUSTRY DEVELOPMENTS

-

July 2022: Eastman Chemical Company expanded its bio-based cellulose acetate production capabilities. The investment focuses on sustainable manufacturing processes to meet the growing demand for cellulose esters in packaging and coatings.

- January 2022: Solvay launched a new cellulose acetate film designed for food packaging applications, offering superior barrier properties to extend the shelf life of perishable goods. This innovation supports the growing trend toward sustainable and biodegradable packaging solutions.