The side table market is witnessing steady growth worldwide as consumers increasingly seek stylish, functional, and versatile furniture pieces to complement their living spaces. Whether it’s a wooden side table for the living room, a metal design for industrial interiors, or a multifunctional side table with storage, the demand for these compact furniture items continues to rise.

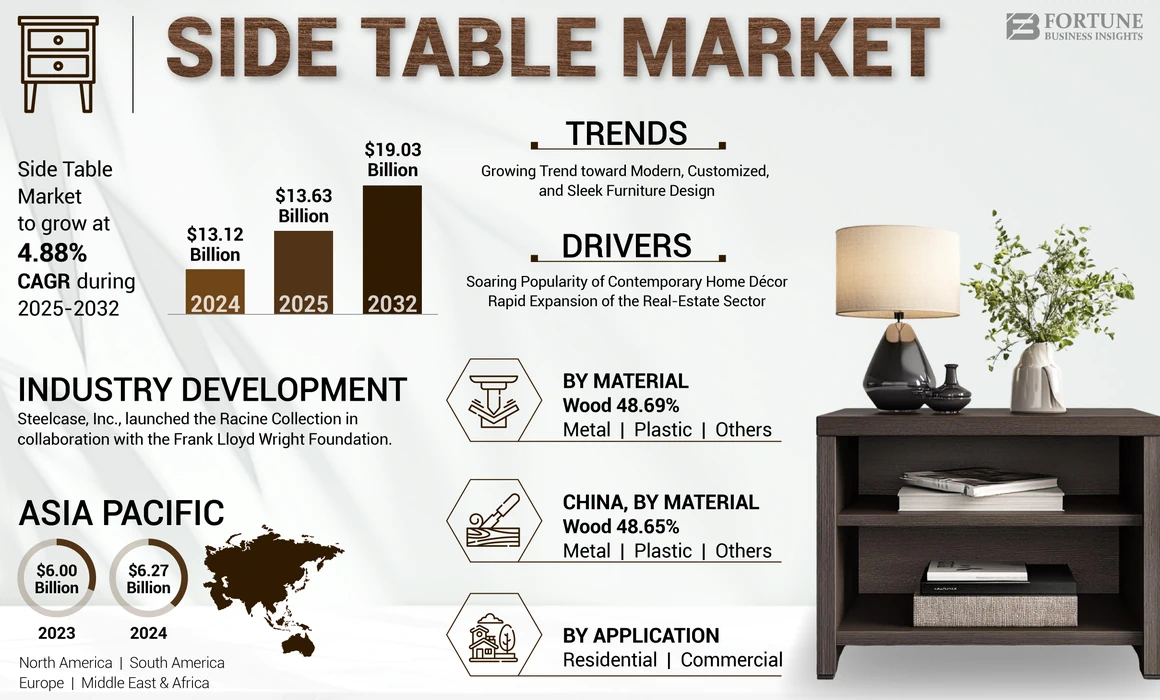

According to the latest market analysis, the global side table market size was valued at USD 13.12 billion in 2024 and is projected to grow from USD 13.63 billion in 2025 to USD 19.03 billion by 2032 , recording a CAGR of 4.88% during the forecast period. This growth is fueled by the increasing emphasis on home décor, urban housing development, and the rising trend of customized and modern furniture designs.

Request FREE Sample PDF Copy of Side Table Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/side-table-market-110179

What is Driving the Side Table Market?

A side table is more than just a decorative element—it is a versatile piece of furniture designed for convenience and style. Available in various materials such as wood, metal, plastic, glass, and rattan , side tables serve multiple purposes, including storage, workspace, or even doubling as nightstands.

Several key factors are shaping the growth of the market:

1. Rising Demand for Home Aesthetics

Consumers are focusing heavily on interior décor, seeking furniture that blends functionality with style. Side tables are increasingly viewed as accent pieces that enhance room design.

2. Customization and Luxury Furniture Trends

Personalized side tables with unique finishes, dimensions, or built-in features are gaining popularity. Luxury furniture buyers are also driving demand for high-end materials like marble, glass, and polished wood.

3. Multifunctional Furniture

With smaller living spaces in urban areas, multifunctional furniture such as side tables with drawers , charging ports, or convertible surfaces is in high demand. These practical designs maximize usability while saving space.

4. Post-Pandemic Lifestyle Changes

The COVID-19 pandemic boosted demand for home office furniture , and side tables became an essential item. Many households repurposed them as compact workstations, further driving sales.

Side Table Market Segmentation

The global side table market is segmented by material , application , and distribution channel :

By Material

- Wood : Expected to dominate with a market share of 48.89% in 2025 , thanks to its timeless appeal, durability, and natural aesthetic.

- Metal : Popular in industrial and modern interiors, offering strength and sleek finishes.

- Plastic and Others (glass, rattan, plywood) : Lightweight and affordable, ideal for budget-conscious or space-saving needs.

By Application

- Residential Segment : Projected to generate USD 8.26 billion in 2025 , driven by rising home ownership, renovations, and interior design trends.

- Commercial Segment : Growing steadily as hotels, offices, and retail spaces incorporate side tables to enhance functionality and aesthetics.

By Distribution Channel

- Bookstores & Furniture Stores remain the primary offline purchase points, but

- Online Channels are growing rapidly due to convenience, availability of unique designs, and access to global brands.

Regional Insights

The Asia Pacific side table market dominated with 47.79% market share in 2024 , valued at USD 6.27 billion . Rapid urbanization, residential construction, and the region’s role as a furniture manufacturing hub (China, India, Vietnam) continue to strengthen growth.

- India : Expected to witness a 7.61% CAGR , supported by rising disposable incomes and booming real estate.

- Japan : Market projected at USD 0.65 billion by 2025 , driven by compact living trends and demand for multifunctional furniture.

North America : Driven by strong home ownership culture, the U.S. market is forecast to reach USD 3.51 billion by 2032 . Stylish designs and evolving décor preferences are major contributors.

Europe : Expected to grow at a 3.25% CAGR , with high spending on home renovations and design-focused purchases. Germany, France, Italy, and Spain are key producers of innovative furniture designs.

South America & Middle East & Africa : Growth fueled by the hospitality sector and increasing urbanization, where side tables are increasingly used in hotels, offices, and apartments.

Side Table Market Trends

- Modern and Sleek Designs : Minimalist and space-efficient side tables are trending among urban dwellers.

- Technological Integration : Smart side tables with wireless charging, USB ports, and integrated speakers are attracting tech-savvy buyers.

- Sustainability : Eco-friendly designs using bamboo, recycled wood, and responsibly sourced materials are gaining traction.

Get Full Insights: https://www.fortunebusinessinsights.com/side-table-market-110179

Restraining Factors

While growth is promising, the market faces challenges such as:

- Fluctuating raw material prices , particularly wood and metal.

- Competition from cheaper alternatives like foldable or plastic furniture.

- High costs of premium designs , limiting affordability for some consumer groups.

Key Players in the Side Table Market

Leading companies are focusing on product innovation, partnerships, and customization to strengthen their market position. Major players include:

- Steelcase Inc. (U.S.)

- MillerKnoll, Inc. (U.S.)

- Ashley Furniture Industries, Inc. (U.S.)

- IKEA (Sweden)

- Godrej & Boyce (India)

- B&B Italia (Italy)

- Natuzzi S.p.A. (Italy)

- Ethan Allen Global, Inc. (U.S.)

Recent developments include Steelcase’s Racine Collection (2023) in collaboration with the Frank Lloyd Wright Foundation, and Tidelli’s Rio collection inspired by Rio de Janeiro.

Conclusion

The side table market is poised for consistent growth through 2032 as consumers embrace modern, multifunctional, and stylish furniture for both residential and commercial use. With Asia Pacific leading in manufacturing and North America driving innovation in design, the global market will continue to evolve.

As home décor trends expand and smart furniture solutions gain traction, the humble side table will remain a staple in households worldwide—not only as a functional piece but also as a style statement.

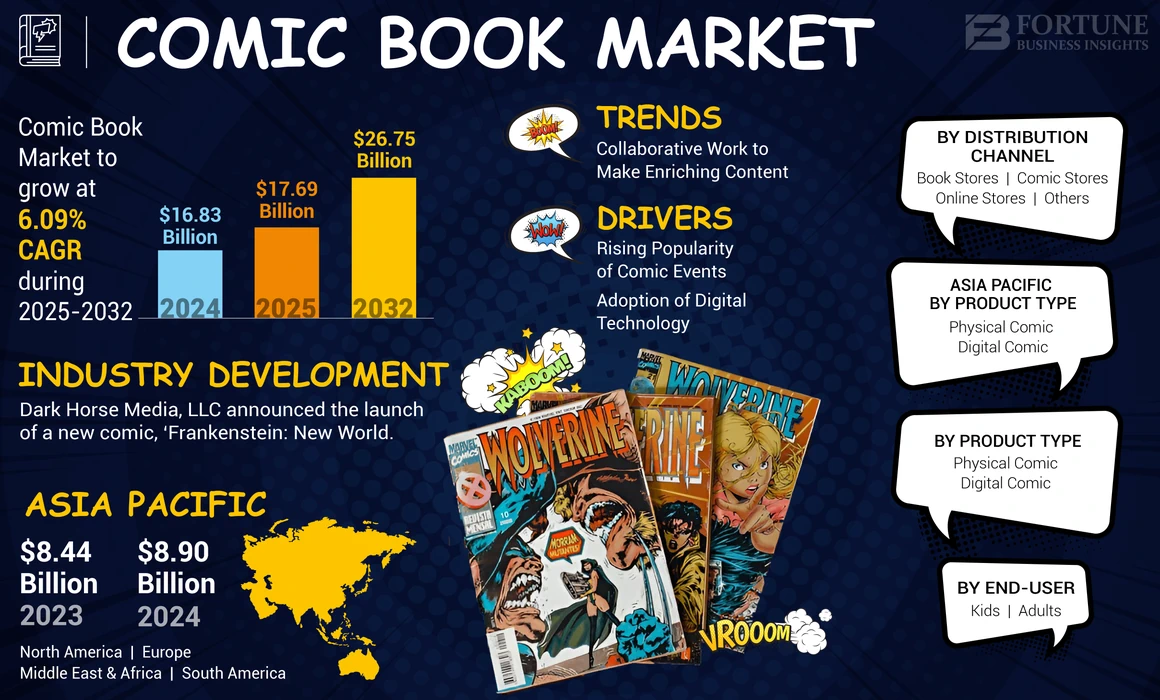

The comic book industry has grown from niche fan culture into a global entertainment powerhouse, capturing readers across generations. With the rise of superhero franchises, anime, and digital comics , comic books have become a vital part of global pop culture. According to the latest research, the global comic book market size stood at USD 16.83 billion in 2024 , is projected to reach USD 17.69 billion in 2025 , and is forecasted to expand to USD 26.75 billion by 2032 , at a CAGR of 6.09% during 2025–2032.

Asia Pacific currently leads the market, accounting for 52.88% of global market share in 2024 , thanks to the thriving anime and manga ecosystem in Japan, South Korea, and China. Meanwhile, the U.S. comic book market is expected to reach USD 4.41 billion by 2032 , driven by the popularity of Comic-Con events and superhero launches.

Request FREE Sample PDF Copy of Comic Book Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/comic-book-market-103903

Why Comic Books Remain Popular

Comic books are no longer just children’s entertainment—they are a creative medium that combines storytelling, art, and culture. Their popularity stems from several factors:

- Engaging narratives and artwork: Readers are drawn to colorful illustrations and immersive stories spanning genres such as fantasy, sci-fi, noir, romance, and adventure.

- Educational value: Comics improve vocabulary, foster creativity, and deliver strong values through positive storytelling.

- Cultural significance: From Japanese manga to Marvel and DC superheroes, comic books are deeply tied to cultural identity and modern entertainment.

Even governments are recognizing their value. For example, India’s Ministry of Education launched 100 educational comic books in 2021 to encourage children to read and learn creatively.

Market Growth Drivers

1. Comic-Con Events and Fan Culture

Events such as San Diego Comic-Con, New York Comic-Con, and Japan Comiket attract hundreds of thousands of fans annually. These gatherings not only boost comic sales but also strengthen global fan communities. Brazil’s São Paulo Comic Con Experience (CCXP) alone attracted over 260,000 visitors in 2021, highlighting how large-scale conventions fuel demand.

2. Smartphone Adoption and Digital Comics

The rise of digital comics is fueled by global smartphone penetration. According to IDC, smartphone shipments rose by 73.6 million units in 2021 compared to 2020. With more readers accessing comics via apps and e-stores, digital editions are gaining momentum, especially among younger audiences.

3. Collectors and Rare Editions

Comic collecting has evolved into a billion-dollar niche market. Rare issues are sold at auctions for massive profits, motivating fans to invest in limited editions and vintage comics . This trend supports growth in both physical and digital formats.

4. Cross-Media Collaborations

Publishers are increasingly collaborating with brands, streaming platforms, and tech companies to expand reach. For example, Marvel partnered with VeVe in 2022 to launch NFT-based Spider-Man comics, appealing to digital collectors and blockchain enthusiasts.

Market Segmentation Analysis

By Product Type

- Physical comics: Still dominant, supported by collectors and auction markets. Cover appeal, nostalgia, and limited editions make physical comics highly valuable.

- Digital comics: Growing rapidly with e-books, apps, and online platforms. Countries like Italy reported a 63% increase in digital comic releases in 2020 .

By End User

- Adults: The largest segment, driven by collectors and hobbyists. Adults often buy comics as investments and as a creative escape.

- Kids: A fast-growing segment, as comics improve reading skills, vocabulary, and creativity. Governments and schools are increasingly adopting comics as educational tools.

By Distribution Channel

- Bookstores and comic shops: Still the backbone of the industry, providing curated experiences for fans. The U.S. has around 2,000 comic shops , boosting sales of both new releases and collectibles.

- Online platforms: Expected to grow steadily, offering convenience, home delivery, and exclusive editions. Digital payment apps and global e-commerce platforms further fuel this channel.

Regional Insights

Asia Pacific – Market Leader

The region accounted for USD 8.90 billion in 2024 , led by Japan’s manga industry, which dominates both domestic and global markets. South Korea’s webtoons and China’s digital platforms also contribute heavily to the region’s dominance.

North America – Home of Superheroes

With USD 88.81 billion expected by 2025 , North America is the second-largest market. The U.S. benefits from its vast comic book stores, superhero movies, and iconic publishers such as Marvel, DC, and Dark Horse .

Europe – Creative Hub

Countries like France, Italy, and Germany produce 3,000–4,000 new comic titles annually . Rising youth readership and strong homegrown creators strengthen Europe’s position.

South America – Fan Conventions Drive Growth

Brazil is a hotspot thanks to Comic Con Experience (CCXP) , the largest comic event in the world. These conventions also promote merchandise, games, and licensing opportunities .

Middle East & Africa – Emerging Market

Urbanization and increasing literacy rates, especially in South Africa , are fueling comic adoption. Mobile accessibility is driving readership among youth.

Key Trends Shaping the Comic Book Market

- Asia Pacific witnessed comic book market growth from USD 8.44 Billion in 2023 to USD 8.90 Billion in 2024.

- NFT Comics & Digital Collectibles: Marvel and other publishers are tapping into blockchain.

- Diverse Storylines & Inclusive Characters: Representation of different cultures, genders, and identities is on the rise.

- Cinematic Synergy: Blockbusters like Spider-Man and Black Panther boost global comic demand.

- Collaborations with Streaming Services: Archie Comics’ partnership with Netflix exemplifies how cross-media exposure increases readership.

Industry Challenges

Despite growth, the comic book market faces:

- Competition from substitutes such as audiobooks and online streaming.

- High production costs and fluctuating paper prices affecting physical comics.

- Counterfeit comics and piracy in digital formats.

Get Full Insights: https://www.fortunebusinessinsights.com/comic-book-market-103903

Competitive Landscape

The comic book industry is highly competitive, with top publishers investing in new characters, storylines, and cross-platform projects . Key players include:

- Marvel Entertainment, LLC (U.S.)

- DC Entertainment (U.S.)

- Dark Horse Media, LLC (U.S.)

- Archie Comics (U.S.)

- Image Comics (U.S.)

- IDW Media Holdings (U.S.)

- Akita Publishing & Futabasha (Japan)

- Rebellion (U.K.)

Recent launches highlight innovation:

- Marvel (2022): Introduced new titles like Ant-Man, Gambit, Iron Cat, and Wolverine: Patch .

- Dark Horse (2022): Released Frankenstein: New World in its Hellboy universe.

- Archie Comics (2022): Partnered with Netflix for a live-action musical.

- Rebellion (2022): Revived classic characters like Cat Girl and Black Beth .

Conclusion

The comic book market is evolving beyond traditional paperbacks, embracing digital platforms, NFTs, and cross-media storytelling . With strong growth expected, particularly in Asia Pacific and North America , the industry is set to thrive as both a cultural phenomenon and a lucrative business.

Publishers that focus on digital expansion, diverse narratives, and collector-driven editions will capture the next generation of readers while retaining loyal fans worldwide.

The cosmetics industry has grown into one of the most dynamic and competitive markets globally, fueled by rising consumer demand for beauty, skincare, and grooming products. According to recent research, the global cosmetics market size was valued at USD 335.95 billion in 2024 and is projected to rise from USD 354.68 billion in 2025 to USD 556.21 billion by 2032 , registering a strong CAGR of 6.64% during the forecast period.

With increasing awareness about self-care, sustainable beauty, and technological innovation, cosmetics are no longer limited to basic skincare and makeup. They have evolved into a broad category covering skincare, haircare, makeup, and personal grooming , catering to both men and women across diverse income groups.

Request FREE Sample PDF Copy of Cosmetics Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/cosmetics-market-102614

Key Market Highlights

- Market Size (2024): USD 335.95 billion

- Forecast (2032): USD 556.21 billion

- CAGR (2025–2032): 6.64%

- Top Region (2024): Asia Pacific (39.57% market share)

- Leading Category: Skincare (35.08% share in 2024)

- Top Companies: L’Oréal, Unilever, Procter & Gamble (P&G), Johnson & Johnson, Estée Lauder

Why the Cosmetics Market is Booming

1. Growing Beauty & Self-Care Awareness

The rising importance of personal grooming and wellness is driving the demand for cosmetics. Skincare and makeup products are now seen as essentials for both everyday routines and lifestyle enhancement. Urbanization, social media influence, and rising disposable incomes are also fueling consumer spending on beauty products.

2. Surge in Organic & Sustainable Cosmetics

A major shift in consumer preference is toward organic and eco-friendly cosmetics . Brands are reformulating products with natural ingredients , avoiding harsh chemicals, and promoting vegan and cruelty-free options . For example, the U.K. Soil Association reported that retail sales of organic health and beauty products reached USD 182.94 million in 2022 , showing the strong global shift toward sustainable beauty.

3. Influence of Social Media & Beauty Influencers

Platforms such as Instagram, TikTok, and YouTube play a significant role in shaping consumer choices. Collaborations between cosmetics brands and influencers amplify brand visibility and directly impact purchasing behavior. A notable example is Dolce Glow’s 2023 partnership with Miley Cyrus , which boosted awareness and sales in the self-tanning category.

Market Segmentation Analysis

By Category

- Skincare: Dominates the market with 35.08% share in 2024 , supported by a surge in new brands and product launches.

- Haircare: Expected to witness robust growth due to increasing awareness of scalp health and hair damage prevention. In 2024, U.S.-based epres launched shampoos using Biodiffusion technology , highlighting innovation in haircare.

- Makeup: A continuously evolving category, driven by fashion trends, influencer promotions, and celebrity collaborations.

By Gender

- Women: Account for 57.19% market share in 2025 , driven by rising beauty consciousness, busy urban lifestyles, and increased pollution exposure leading to skincare demand.

- Men: Expected to grow at 6.99% CAGR (2025–2032) . Grooming products, skincare solutions, and premium haircare items are becoming popular among male consumers.

By Distribution Channel

- Hypermarkets/Supermarkets: Leading with 32.41% share in 2025 , thanks to wide product availability and in-store promotions.

- Online Channels: Expanding at 6.75% CAGR (2025–2032) due to the convenience of e-commerce and competitive pricing.

Regional Insights

Asia Pacific: Market Leader

With a market value of USD 132.92 billion in 2024 , Asia Pacific dominates the cosmetics industry. Key contributors include:

- China: USD 41.31 billion in 2024

- India: USD 25.57 billion in 2024

- Japan: USD 20.75 billion in 2024

Factors such as economic growth, rising middle-class consumers, and the growing appetite for luxury beauty products contribute to the region’s dominance.

Europe

Estimated to reach USD 95.46 billion by 2025 , Europe benefits from its fashion-forward culture, luxury demand, and eco-conscious consumers . Germany, the U.K., and France remain strong markets supported by the presence of top global players like L’Oréal and Beiersdorf AG .

North America

Expected to achieve USD 88.81 billion in 2025 , driven by a fashion-conscious population and high female workforce participation . The U.S. contributes the largest share, with cosmetics becoming a part of daily grooming routines.

South America

Projected to reach USD 20.67 billion in 2025 , South America is influenced by urbanization, lifestyle changes, and social media-driven fashion awareness in countries such as Brazil and Argentina.

Middle East & Africa

Growing steadily, with UAE valued at USD 1.31 billion in 2025 . Rising disposable incomes, premium product demand, and expanding distribution networks drive this market.

Market Challenges

- Side-effects of synthetic chemicals like parabens, sulfates, and phthalates raise consumer concerns.

- Counterfeit cosmetics remain a major hurdle, particularly in emerging markets.

- Regulatory scrutiny such as the U.S. FDA’s Modernization of Cosmetics Regulation Act (MoCRA) of 2022 requires brands to comply with stricter safety guidelines.

Opportunities Ahead

- AI-driven personalized cosmetics: Beauty companies are investing in hyper-personalization . For example, Unilever plc revealed in 2024 its focus on AI-powered skincare recommendations tailored to individual needs.

- Rising male grooming segment: Expanding demand for men’s skincare, beard care, and hair styling products.

- Retail expansion & digital innovation: Leading brands are opening flagship stores and strengthening omnichannel strategies to capture a wider audience.

Get Full Insights: https://www.fortunebusinessinsights.com/cosmetics-market-102614

Competitive Landscape

The cosmetics industry is highly competitive and fragmented. The top five players — L’Oréal, Unilever, Estée Lauder, P&G, and Johnson & Johnson — collectively account for around 34% market share .

Other key players include:

- Beiersdorf AG (Germany)

- Shiseido (Japan)

- Natura & Co. (Brazil)

- Kao Corporation (Japan)

- COTY Inc. (U.S.)

Recent developments highlight expansion efforts:

- August 2024: Kay Beauty launched Hydra Crème Lipsticks in India.

- July 2024: Curology introduced its skincare line across CVS stores in the U.S.

- February 2024: Kao Corporation launched its new haircare brand “melt.”

Conclusion

The cosmetics market is undergoing rapid transformation, powered by sustainable products, digital influence, and technological advancements . With strong growth expected across Asia Pacific, Europe, and North America, brands that embrace innovation, personalization, and eco-friendly practices will stay ahead in this competitive industry.

As consumers increasingly invest in beauty, grooming, and wellness , the cosmetics industry is well-positioned to remain a trillion-dollar powerhouse in the making.

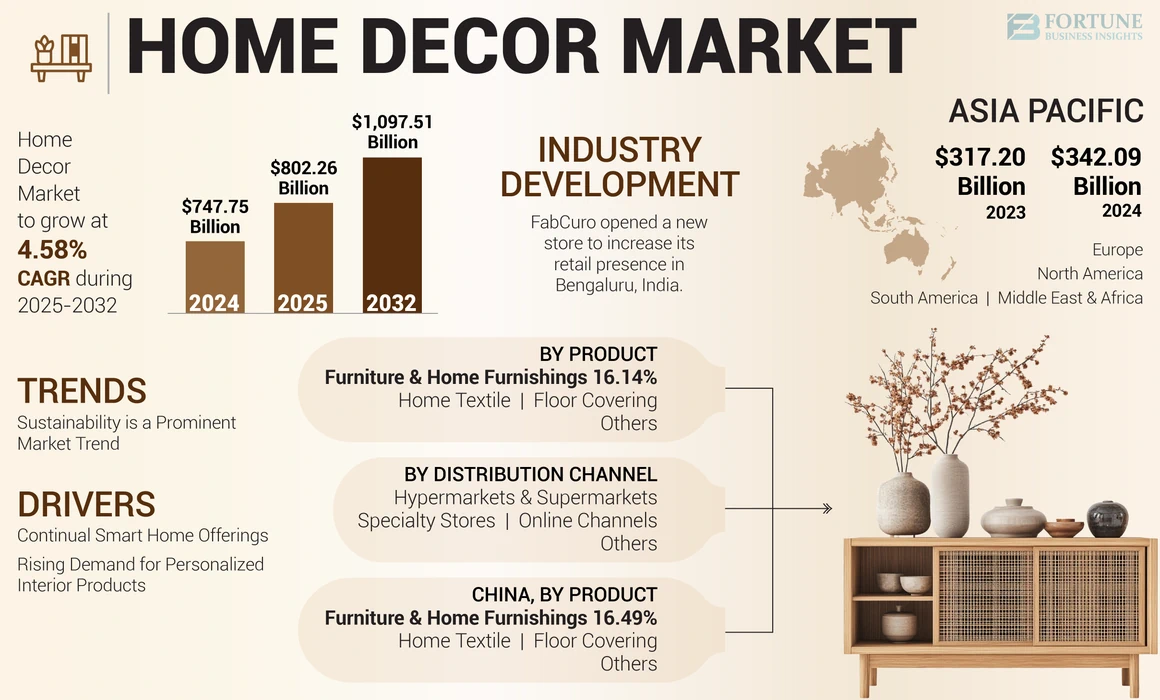

The home decor market is undergoing a significant transformation, fueled by evolving consumer lifestyles, rapid urbanization, and the growing influence of interior design trends worldwide. According to the latest market analysis, the global home decor market size was valued at USD 747.75 billion in 2024 and is projected to grow from USD 802.26 billion in 2025 to reach USD 1,097.51 billion by 2032 , registering a CAGR of 4.58% during the forecast period.

From decorative accents to luxury furniture, consumers are increasingly investing in products that elevate both the functionality and aesthetics of their living spaces.

Request FREE Sample PDF Copy of Home Décor Market: https://www.fortunebusinessinsights.com/home-decor-market-109906

Rising Demand for Home Decor Products

The growing popularity of stylish home decor products—ranging from furniture, floor coverings, home textiles, lighting, and wall art —is reshaping residential and commercial interiors. Decorative accents like candles, throw pillows, and artworks are increasingly being used to create unique, cozy atmospheres.

Moreover, outdoor decor has become a global trend, with more households adding decks, patios, and garden furniture to extend their living spaces. According to the AIA Home Design Trend Survey (2023) , nearly 65% of Americans preferred decorative decks and patios, reflecting a cultural shift toward blending indoor and outdoor living.

Global Home Decor Market Snapshot

- 2024 Market Size : USD 747.75 billion

- 2025 Market Size : USD 802.26 billion

- 2032 Forecast : USD 1,097.51 billion

- CAGR : 4.58% (2025–2032)

- Regional Leader : Asia Pacific with 45.74% market share in 2024

- Top Country Growth : U.S. home decor market expected to hit USD 305.51 billion by 2032

Key Market Drivers

1. Sustainability in Home Decor

Eco-friendly materials are reshaping the home decor market . Consumers are increasingly choosing upcycled and recycled furniture, textiles, and floor coverings . For instance, Laurence Carr Inc. launched a collection of sustainable sculptural vessels made from biomaterials in 2023, highlighting the industry’s push toward greener solutions.

2. Smart Home Integration

The demand for smart decorative lighting, connected home appliances, and voice-controlled decor solutions is driving innovation. In the U.K., 25% of potential homebuyers already view smart technology as a "must-have" in their homes, underscoring the merging of technology and design.

3. Personalized and Luxury Products

Consumers are leaning towards custom-made furniture, DIY décor, and monogrammed accessories . Luxury furniture brands offering curved sofas, vintage-inspired chairs, and multifunctional furnishings are witnessing rapid adoption. This personalization trend is particularly strong among millennials and Gen Z homeowners.

Challenges Restraining Growth

Despite promising expansion, the home decor industry faces challenges:

- High costs of premium furniture and flooring make luxury products less accessible for middle-income households.

- Counterfeit products continue to flood the market, impacting brand trust and revenues.

- Economic disruptions such as the COVID-19 pandemic temporarily reduced retail operations, leading to price hikes in some regions.

Home Decor Market Segmentation

By Product

- Floor Covering : Dominates due to high renovation-related spending. Advanced products like PVC-free flooring by Unilin Technologies are fueling growth.

- Furniture & Home Furnishings : Fastest-growing segment, driven by multifunctional and luxury furniture demand.

- Home Textile : Growth supported by luxury bedding and curtains.

- Others : Includes wall art, lighting, and decorative accents.

By Distribution Channel

- Hypermarkets & Supermarkets : Leading channel due to wide accessibility.

- Specialty Stores : Growing segment for luxury buyers.

- Online Channels : Fastest expansion due to digital shopping trends.

- Others : Includes upholstery shops and wholesale stores.

Get Full Insights: https://www.fortunebusinessinsights.com/home-decor-market-109906

Regional Insights

- Asia Pacific : The largest and fastest-growing region, valued at USD 342.09 billion in 2024 . Strong demand in China, India, and Southeast Asia is driving growth, fueled by residential projects and modern furniture demand.

- North America : High spending on renovations, smart decor, and sustainable furnishings are boosting growth. In 2020 alone, Americans spent USD 420 billion on home renovations.

- Europe : Leading in eco-friendly furniture , with companies like Omega PLC introducing products made entirely from recycled wood.

- South America : Brazil and Argentina are witnessing rising demand for luxury decor and kitchen furnishings.

- Middle East & Africa : Wealthier households are upgrading kitchens and storage solutions, while Africa is seeing growing demand for affordable furniture.

Competitive Landscape

The home decor market is highly competitive, with key players focusing on product innovation, retail expansion, and sustainable offerings .

Leading Companies:

- Inter IKEA Systems B.V. (Netherlands)

- Williams-Sonoma Inc. (U.S.)

- Ashley Furniture Industries, LLC (U.S.)

- Ethan Allen Global, Inc. (U.S.)

- Welspun Flooring (India)

- Herman Miller, Inc. (U.S.)

Recent developments include:

- Williams Sonoma Inc. expanding retail presence with a new store in San Diego (2023).

- Vaaree , a home furnishing startup, raising USD 4 million to enhance online user experiences (2023).

- Remax Furnitures launching a luxury store in New Delhi (2024).

Conclusion

The home decor market is evolving rapidly, driven by sustainability, personalization, and smart technology integration. With Asia Pacific leading global demand and North America embracing renovation projects, the industry is poised for steady growth through 2032.

For brands and businesses, focusing on eco-friendly innovations, online expansion, and personalized luxury offerings will be key to capturing market share in this competitive landscape.

Global Dining Table Market Size, Share & Industry Forecast 2025–2032

By Industry Outlook, 2025-09-02

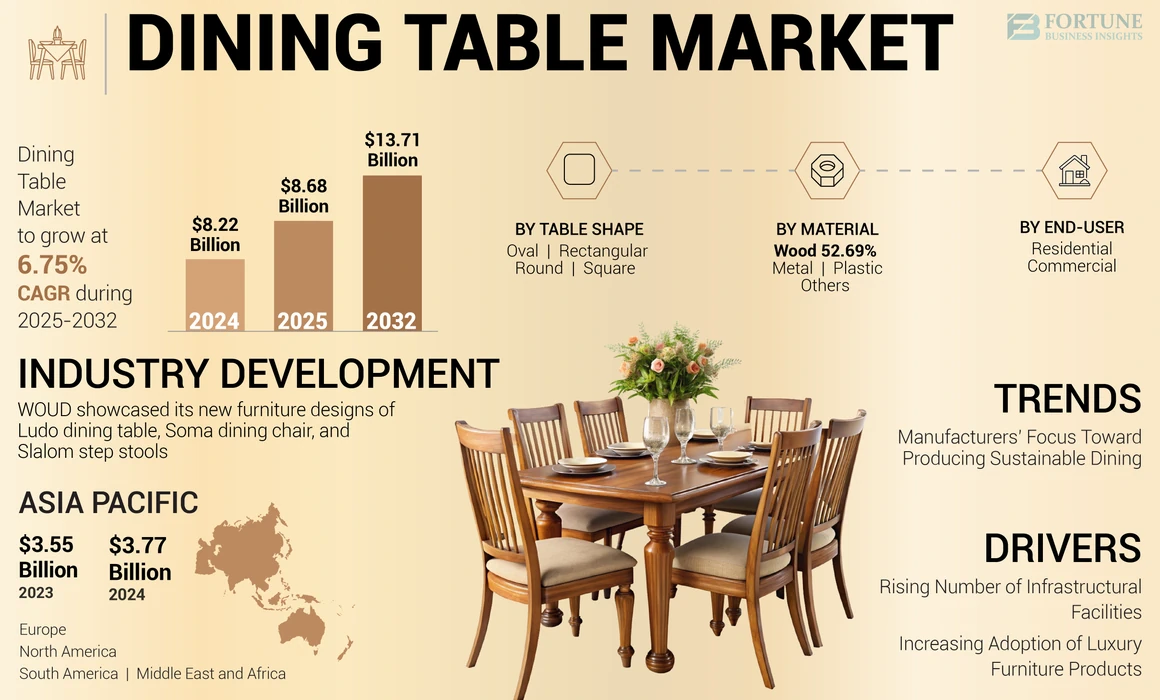

The Dining Table market is witnessing steady growth as evolving home décor trends, rising disposable incomes, and increasing demand for multifunctional furniture shape consumer preferences worldwide. According to recent market analysis, the global Dining Table market size was valued at USD 8.22 billion in 2024 and is projected to grow from USD 8.68 billion in 2025 to USD 13.71 billion by 2032 , reflecting a healthy CAGR of 6.75% .

Among all regions, Asia Pacific dominated the market with a 43.18% share in 2024 , fueled by strong consumer demand in China and India. Meanwhile, the U.S. Dining Table market is expected to reach USD 2.34 billion by 2032 , supported by the rising adoption of luxury furniture and the growth of online retail platforms.

Request FREE Sample PDF Copy of Dining Table Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/dining-table-market-106138

Why Dining Tables Are in Demand

The Dining Table is no longer just a household necessity—it has evolved into a multifunctional centerpiece of modern homes. Beyond dining, tables are now used for work-from-home setups, online classes, family gatherings, and leisure activities . This versatility has made the Dining Table a must-have piece of furniture in both residential and commercial settings.

Consumer preferences have also shifted toward minimalistic, customizable, and contemporary designs that complement modern interiors. In fact, a survey by the National Association of Realtors (NAR) revealed that nearly 30% of homeowners renovate to upgrade worn-out surfaces and finishes , while 20% add new features for livability —boosting demand for modern dining furniture.

Dining Table Market Growth Drivers

1. Rising Urbanization and Disposable Income

Rapid urbanization and an expanding middle-class population are key factors driving Dining Table adoption . Consumers are investing in high-quality, durable tables that add functionality and aesthetic value to their homes.

2. Growth in Hospitality and Commercial Spaces

The rising number of restaurants, cafes, bars, and canteens globally fuels demand for large-sized Dining Tables . For example, China reported 9.17 million restaurants in 2021 , reflecting steady demand for commercial dining furniture.

3. Increasing Popularity of Luxury Furniture

Global consumers are increasingly drawn to luxury Dining Tables made from premium materials such as oak, teak, and glass. Brands like MillerKnoll and Steelcase have reported significant revenue growth from customizable luxury collections.

4. Expansion of Online Furniture Sales

The growth of e-commerce platforms has made Dining Tables more accessible. Leading brands like Coco Republic and Ashley Furniture have expanded their digital presence, enabling consumers to purchase dining sets online with customization options.

Dining Table Market Trends

One of the biggest trends shaping the Dining Table market is the focus on sustainability . Manufacturers are innovating with recycled wood, eco-friendly plastics, and renewable materials to meet rising consumer demand for green furniture.

For instance, Outer, Inc. launched a collection of sustainable outdoor dining furniture in 2022, including tables and foldable chairs, highlighting the industry’s move toward eco-conscious designs.

Another growing trend is the rise of multifunctional and extendable Dining Tables , designed for compact homes and urban apartments where space management is critical.

Market Segmentation Analysis

By Material

- Wood (52.69% share in 2024) : Continues to dominate due to its durability, aesthetic appeal, and natural finish. Oak, teak, and rosewood remain popular choices.

- Metal : Preferred in corporate canteens and restaurants for their strength and easy maintenance.

- Plastic : Growing demand for recycled plastic tables , particularly in cost-sensitive regions such as Africa.

- Others (glass, fabric, stone) : Stylish glass-top Dining Tables are gaining traction in modern households.

By Table Shape

- Rectangular : Holds the largest market share thanks to its versatility and wide range of sizes.

- Round : Increasingly popular for compact apartments and small dining spaces.

- Square : Favored among nuclear families and rental homes.

- Oval : Slowly gaining consumer attention for its aesthetic appeal.

By End-user

- Residential : The largest segment, driven by the multifunctional use of Dining Tables in daily life, home offices, and interior design trends.

- Commercial : Strong demand from restaurants, hotels, offices, and public dining facilities.

Read More Insights: https://www.fortunebusinessinsights.com/dining-table-market-106138

Regional Insights

- Asia Pacific (USD 3.77 billion in 2024) : The fastest-growing market, driven by strong household consumption in China and India . Trade fairs and expos, such as the China International Furniture Expo 2023 , continue to boost innovation and product adoption.

- North America : Growth is fueled by home renovation trends, remote working styles, and luxury furniture purchases in the U.S. and Canada.

- Europe : Rising demand for extendable Dining Tables and ceramic tabletops for modern kitchens drives growth.

- South America : Outdoor dining trends in Brazil and Chile are spurring sales.

- Middle East & Africa : High demand for cost-effective plastic Dining Tables supports steady growth in regions like South Africa.

Competitive Landscape

The Dining Table market is highly competitive, with global and regional players focusing on design innovation, sustainability, and digital sales expansion.

Key Players:

- Steelcase Inc. (U.S.)

- MillerKnoll, Inc. (U.S.)

- Ashley Furniture Industries, Inc. (U.S.)

- GLOBAL FURNITURE USA (U.S.)

- KOKUYO Co., Ltd. (Japan)

- Ethan Allen Global, Inc. (U.S.)

- Godrej & Boyce Mfg. Co. Ltd. (India)

- B&B ITALIA SPA (Italy)

- Sunpan Trading & Importing, Inc. (Canada)

- CB2 (U.S.)

Recent Industry Developments:

- June 2023 : WOUD showcased innovative Dining Table designs at a global design event.

- May 2023 : Transformer Table launched an extendable patio Dining Set across 35 countries.

- February 2022 : Luxury designer Yashika Luthra launched a new furniture studio in India featuring Dining and coffee tables.

- March 2021 : Plüsch introduced high-end dining tables made from natural stone, glass, and wood in Germany.

Conclusion

The Dining Table market is set for substantial growth through 2032, fueled by urbanization, luxury furniture demand, and the rise of eco-friendly designs. While challenges such as counterfeit products and chemical-based finishes persist, opportunities lie in sustainable innovation, multifunctional furniture designs, and digital retail expansion .

As consumer lifestyles evolve, the Dining Table will remain a central piece of furniture—blending style, functionality, and sustainability in modern homes and commercial spaces.

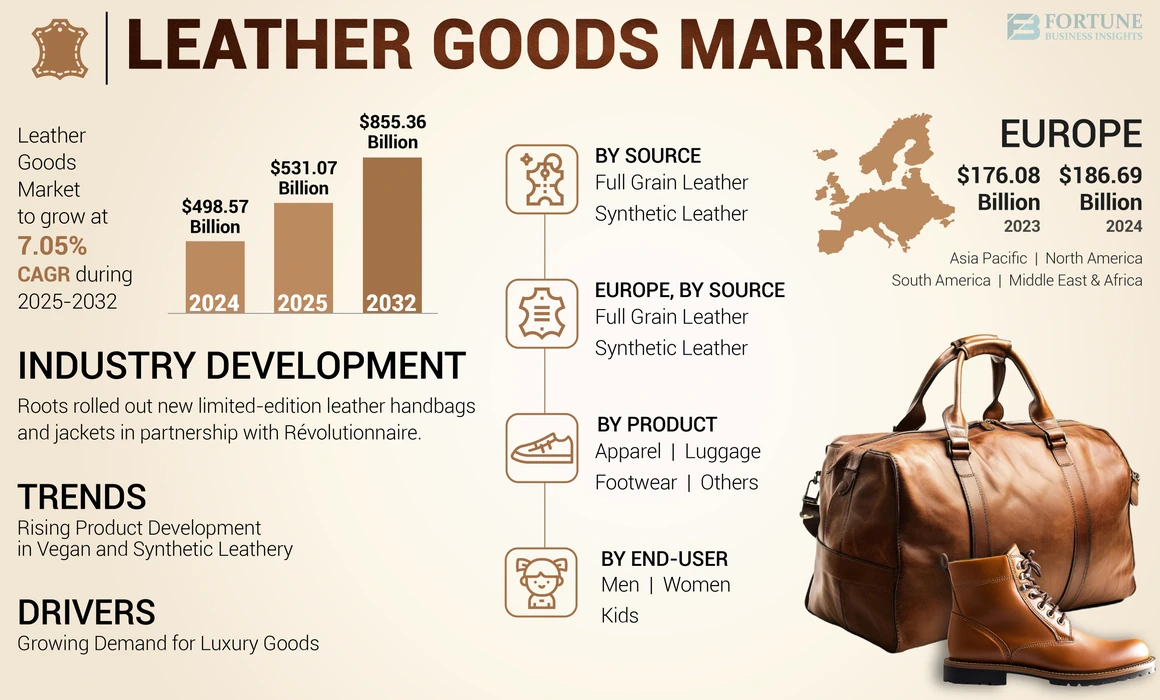

The global leather goods market is on a strong growth trajectory, driven by rising consumer demand for luxury fashion, durable accessories, and innovative synthetic alternatives. According to recent insights, the leather goods market size was valued at USD 498.57 billion in 2024 and is expected to expand from USD 531.07 billion in 2025 to an impressive USD 855.36 billion by 2032 , registering a CAGR of 7.05% during the forecast period.

Request FREE Sample PDF Copy Leather Goods Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/leather-goods-market-104405

Key Market Highlights

- Europe dominates with a market share of 37.44% in 2024 , powered by luxury fashion houses, innovative product launches, and tourism-related retail activity.

- Footwear continues to lead as the largest product category, followed by apparel and handbags.

- The U.S. leather goods market alone is projected to reach USD 220.08 billion by 2032 .

- Sustainability trends are fueling growth in synthetic and vegan leather products, appealing to eco-conscious consumers.

Market Growth Drivers

1. Rising Demand for Luxury and Customized Goods

Luxury leather goods remain a symbol of style, status, and craftsmanship. Global brands such as Dior, Hermès, Prada, and Louis Vuitton continue to expand their product portfolios with exclusive collections and custom-made accessories. E-commerce has played a crucial role in boosting luxury sales, offering consumers convenient access to premium fashion.

Emerging economies like India and China are witnessing a surge in demand for branded leather goods due to the expanding middle class and rising disposable incomes. Moreover, the growing popularity of personalized, handcrafted leather products further strengthens the market’s momentum.

2. Innovation in Vegan and Synthetic Leather

Consumer preferences are shifting toward eco-friendly and cruelty-free alternatives . This has led to an upsurge in demand for synthetic and vegan leather made from plant-based sources like mushrooms, apples, and food waste.

Major players are investing heavily in research and partnerships. For example:

- Kering invested USD 46 million in VitroLabs to commercialize lab-grown leather.

- Hermès collaborated with MycoWorks to develop Fine Mycelium-based bags.

- Adidas introduced mushroom-based Stan Smith sneakers as part of its sustainability goals.

Such innovations not only attract conscious consumers but also reshape the industry’s future.

3. Strong E-commerce and Omnichannel Presence

The pandemic accelerated digital adoption, and luxury brands quickly pivoted to online retail channels . Social media marketing, influencer collaborations, and direct-to-consumer strategies have further expanded global reach. Additionally, omnichannel strategies —integrating physical stores with online platforms—are enabling brands to deliver personalized experiences and increase consumer loyalty.

Restraining Factors

While the outlook is positive, the leather industry faces challenges:

- Environmental impact : Leather production is associated with deforestation, water pollution, and greenhouse gas emissions. Chromium-based tanning, widely used in traditional processes, remains a concern.

- Regulatory pressures : Stricter environmental policies in Europe and North America have forced the closure of several tanneries.

- Health risks : Workers in tanneries are often exposed to harmful chemicals, raising concerns about occupational safety.

Brands that invest in sustainable leather processing methods and transparent supply chains are likely to gain a competitive edge.

Market Segmentation

By Source

- Full-grain leather continues to represent quality and luxury.

- Synthetic leather is gaining ground due to affordability, versatility, and rising awareness of animal cruelty. Companies like Coronet Spa are expanding their footprint with acquisitions to meet rising demand.

By Product

- Footwear dominates, with growing demand for durable, stylish, and customized shoes. For instance, Nike continues to innovate with leather-based sneaker launches.

- Apparel (jackets, skirts, and pants) remains a strong growth segment, driven by designer collections.

- Luggage and handbags are also witnessing a surge, especially with luxury players like Hermès expanding production facilities.

By End-user

- Men lead the market share due to higher demand for shoes, jackets, and luxury apparel. High-profile launches, such as Dior’s men’s winter 2022 collection , reflect this trend.

- Women drive strong demand for handbags, footwear, and fashion apparel, supported by continuous new product launches.

- Kids represent a smaller but steadily growing segment, with increasing availability of premium and stylish leather goods.

Read Full Insights: https://www.fortunebusinessinsights.com/leather-goods-market-104405

Regional Insights

- Europe : The largest market, valued at USD 186.69 billion in 2024 , remains a hub for luxury fashion with global influence from brands based in France and Italy.

- North America : Driven by luxury adoption, e-commerce penetration, and growth in men’s fashion.

- Asia Pacific : Emerging as a high-growth region thanks to rising disposable incomes, rapid urbanization, and increased footwear demand in China and India.

- South America & Middle East/Africa : Experiencing steady growth supported by urbanization, rising affluence, and luxury retail expansion in markets like Brazil and the UAE.

Competitive Landscape

The leather goods market is highly competitive, with global giants and emerging players investing in sustainability and innovation.

Leading Companies:

- Hermès International (France)

- LVMH Moët Hennessy Louis Vuitton (France)

- Kering (France)

- Prada (Italy)

- Capri Holdings (U.S.)

- VF Corporation (U.S.)

- Kuraray Co., Ltd. (Japan)

- H.R. Polycoats Pvt. Ltd. (India)

- Adriano Di Marti (Mexico)

- Broke Mate (India)

Key developments include acquisitions, sustainable product launches, and investments in vegan leather technologies.

Conclusion

The global leather goods market is set for robust growth through 2032, supported by strong consumer demand for luxury products, innovative vegan alternatives, and expanding digital sales channels. While environmental challenges remain, the industry is evolving with sustainable practices, new materials, and product innovation.

For stakeholders, the key opportunities lie in:

- Investing in vegan and synthetic leather technologies .

- Expanding into emerging markets with rising middle-class consumers.

- Leveraging e-commerce and omnichannel strategies to capture wider audiences.

With a blend of tradition, craftsmanship, and modern innovation, the leather goods market is poised to remain a cornerstone of the global fashion and lifestyle industry.

The global tobacco products market remains one of the world’s largest consumer goods sectors, driven by traditional cigarette consumption as well as the rapid growth of next-generation products (NGPs) like e-cigarettes, heated tobacco, and nicotine pouches.

According to Fortune Business Insights , the tobacco products market size was valued at USD 1,018.57 billion in 2024 and is projected to rise from USD 1,058.20 billion in 2025 to USD 1,260.59 billion by 2032, at a CAGR of 2.53%. The Asia Pacific region continues to dominate with a 48.87% market share in 2024, largely due to high cigarette consumption and retail expansion in China, India, and Southeast Asia.

- Asia Pacific witnessed tobacco products market growth from USD 475.84 billion in 2023 to USD 497.81 billion in 2024.

Request FREE Sample PDF Copy of Tobacco Products Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/tobacco-products-market-112987

What’s Driving the Tobacco Market?

1. Demand for Reduced-Risk & Next-Generation Products (NGPs)

Consumers are increasingly shifting from traditional smoking to reduced-risk alternatives like e-cigarettes, heated tobacco products, and nicotine pouches. These are marketed as less harmful than conventional cigarettes and are particularly popular among young adults and women.

For instance, Philip Morris International (PMI) launched BONDS by IQOS in late 2022, a heat-not-burn device designed to accelerate the shift toward smoke-free products. Similarly, British American Tobacco (BAT) invested USD 30 million in its Southampton R&D facility in 2024 to strengthen its NGP portfolio.

2. Rising Disposable Income Among Women

Changing social norms and financial independence are fueling higher tobacco use among women. A CRUK study (2024) found that smoking rates among U.K. women aged 18–45 rose from 12% to 15% over the past decade, particularly in hand-rolled cigarettes. This trend has widened the consumer base for both traditional and flavored tobacco products.

3. Popularity of Flavored Nicotine Products

The market has seen strong growth in flavored cigarettes, cigars, e-liquids, and pouches—with tastes like mint, fruit, coffee, chocolate, and mojito appealing to younger audiences. Brands are leveraging social media campaigns to push flavored options. For example, PMI’s ZYN nicotine pouch campaign on TikTok reached over 700 million followers, signaling the power of digital engagement.

Market Restraints & Challenges

Despite growth potential, the industry faces headwinds:

- Regulatory bans: Several countries—including India, Brazil, Thailand, and Egypt—have banned or restricted e-cigarette sales, limiting NGP adoption.

- Health concerns: Rising awareness of smoking-related diseases continues to pressure tobacco consumption. Governments are introducing higher taxes, plain packaging, and advertising restrictions to curb use.

- COVID-19 impact: Tobacco products were deemed non-essential in many countries during the pandemic, leading to a temporary sales decline.

Market Segmentation

By Product Type

- Traditional Tobacco Products :

- Cigarettes remain the largest revenue driver due to widespread addiction and availability.

- Cigars are growing steadily, boosted by premium flavored options like menthol, mint, and chocolate.

- Roll-your-own (RYO) tobacco appeals to cost-sensitive consumers in developing regions.

- Pipe tobacco & raw leaves are niche but growing in Asia and Africa, where flavored betel leaf shops are expanding.

- Next-Generation Products (NGPs) :

- Heated tobacco products (HTPs) are the fastest-growing subsegment, thanks to consumer perception of reduced harm.

- E-cigarettes rank second, popular among youth but facing regulatory bans in some countries.

- Nicotine pouches are gaining popularity in Europe and North America.

- Snus & others (herbal sticks, hookahs, dissolvables) provide diversification in emerging markets.

By Region

- Asia Pacific: Largest market, worth USD 497.81 billion in 2024, driven by China’s 291 million smokers and rising demand for slim e-cigarettes.

- North America: Strong uptake of e-cigarettes and pouches in the U.S., especially among teens and women. Disposable vapes dominate (54% share).

- Europe: Countries like the U.K. and Sweden lead in nicotine pouch and snus consumption, aided by growing social acceptance.

- South America: Brazil and Argentina witness a shift from traditional cigarettes to smoke-free products, supported by stricter taxation.

- Middle East & Africa: High traditional cigarette consumption persists, but demand for dokha, herbal tobacco, and HTPs is rising.

Read Summary here: https://www.fortunebusinessinsights.com/tobacco-products-market-112987

Competitive Landscape

The market is highly competitive, with global giants and regional players investing heavily in flavored innovations and reduced-risk alternatives.

Leading Companies:

- Philip Morris International Inc. (PMI)

- British American Tobacco plc. (BAT)

- Altria Group, Inc.

- Japan Tobacco Inc. (JT)

- Imperial Brands plc.

- ITC Limited (India)

- China National Tobacco Corporation (CNTC)

- KT&G Corporation (South Korea)

Key Developments

- Dec 2024 – PMI announced affordable NGPs targeting Africa’s price-sensitive markets.

- Sep 2024 – BAT launched its Smokeless World initiative and Omni™ platform to promote harm reduction.

- Nov 2024 – Imperial Brands unveiled Paramount cigarettes in the U.K., offering premium Virginia blends.

- Aug 2024 – VFLY launched its C1 e-cigarette in South Korea with customizable vaping modes.

- Jul 2024 – PMI partnered with KT&G to file U.S. regulatory submissions for heat-not-burn devices.

Opportunities Ahead

- Innovation in flavors & delivery systems will continue to attract younger audiences.

- Eco-friendly & less addictive alternatives can capture health-conscious consumers.

- Digital marketing & e-commerce provide a powerful growth channel, especially in regulated markets.

- Emerging markets in Africa & Asia present untapped opportunities for cost-effective NGPs.

Conclusion

The global tobacco products market is set to surpass USD 1.26 trillion by 2032, driven by the dual force of traditional cigarette demand and the accelerating adoption of next-generation products. While regulatory hurdles and health concerns remain significant, innovation, flavor diversification, and reduced-risk alternatives will shape the industry’s future.

Key takeaway: Companies that balance compliance, consumer safety, and product innovation will secure a stronger foothold in the evolving tobacco landscape.

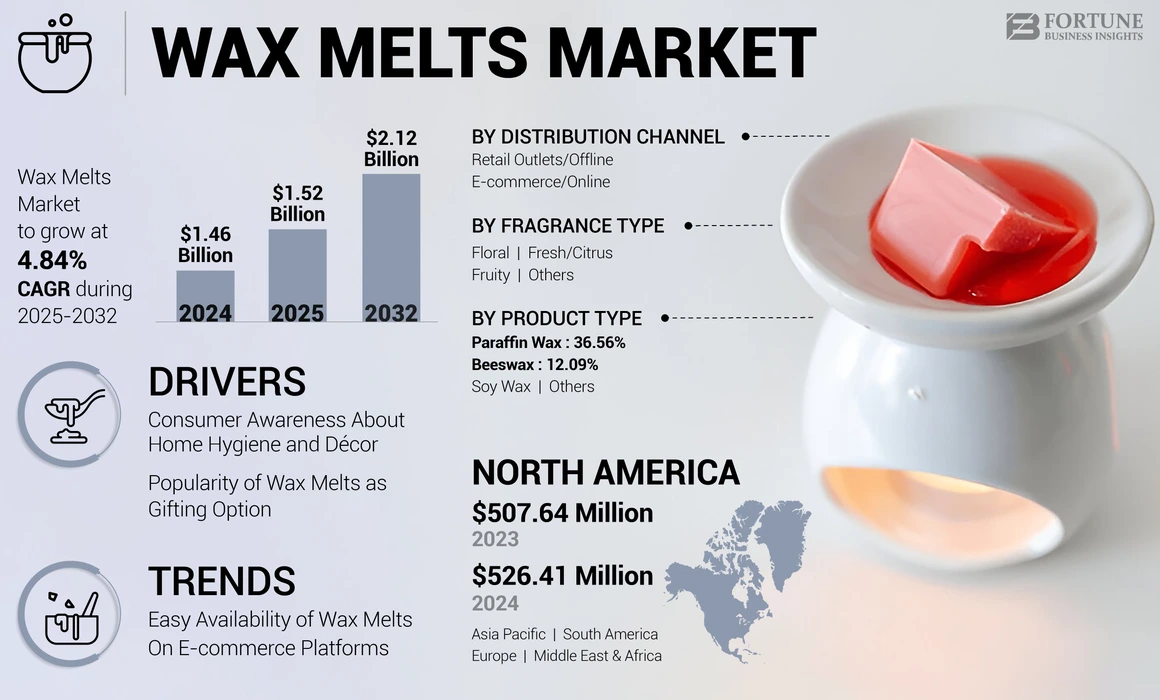

The global wax melts market is gaining strong traction as more consumers look for affordable, long-lasting, and stylish home fragrance options. According to Fortune Business Insights , the wax melt market size was valued at USD 1.46 billion in 2024 and is projected to grow from USD 1.52 billion in 2025 to USD 2.12 billion by 2032, reflecting a CAGR of 4.84%.

With demand fueled by home décor trends, aromatherapy, and eco-friendly lifestyle preferences, wax melts are fast becoming a staple in both residential and commercial spaces.

- North America witnessed wax melts market growth from USD 507.64 Million in 2023 to USD 526.41 Million in 2024.

Request FREE Sample PDF Copy of Wax Melts Market: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/wax-melts-market-112079

What Are Wax Melts and Why Are They Popular?

Wax melts are small, scented wax pieces that release fragrance when heated in a burner. Unlike traditional candles, they are wickless, versatile, and available in a wide range of shapes, colors, and fragrances—from floral and fruity to citrus, woody, and spicy.

Consumers love wax melts for several reasons:

- They are affordable and long-lasting.

- Safer than open-flame candles.

- Enhance home ambiance, relaxation, and mood.

- Ideal for gifting, thanks to their customizable packaging and design.

Market Drivers

1. Rising Demand for Home Hygiene & Décor

Growing awareness about home fragrance and hygiene products—such as sprays, essential oils, and candles—is fueling wax melts adoption. In developing countries like India, Brazil, and Vietnam, increasing home construction and urbanization are boosting product demand.

2. Wax Melts as a Gifting Trend

Wax melts are now seen as a thoughtful, stylish, and customizable gifting option. Brands are offering wax melts in personalized jars, boxes, and festive gift sets, making them popular for holidays, birthdays, and cultural celebrations.

3. E-commerce Driving Growth

The easy availability of wax melts on e-commerce platforms such as Amazon, Flipkart, and Alibaba has significantly expanded market reach. Online stores offer wide product variety, discounts, and easy price comparisons, attracting younger consumers to shop digitally.

Key Challenges

Despite strong growth, the market faces some hurdles:

- Substitute products like scented candles, room sprays, and essential oils compete strongly.

- Raw material price fluctuations due to inflation and supply chain issues increase costs for manufacturers.

- Counterfeit and low-quality products, especially in developing countries, affect consumer trust and brand reputation.

Opportunities Ahead

A major opportunity lies in the growing demand for eco-friendly wax melts. Consumers are increasingly shifting toward sustainable, chemical-free, and natural products made from soy wax, beeswax, or coconut wax. Brands that focus on eco-conscious production and packaging are expected to gain a competitive edge.

Segment Overview

By Product Type

- Paraffin Wax – holds the largest share (37%) due to its widespread use in homes, spas, and restaurants.

- Beeswax – expected to grow fastest, thanks to its natural honey-like aroma and eco-friendly appeal.

- Soy Wax & Others – gaining momentum as sustainable alternatives.

By Fragrance Type

- Fresh/Citrus dominates due to its popularity in aromatherapy and mood enhancement.

- Floral fragrances are expected to grow fastest, driven by their relaxing and calming effects.

By Distribution Channel

- Retail outlets (offline) remain dominant, contributing around 79% of market share in 2025.

- E-commerce is projected to grow fastest (CAGR 5.62%) as consumers prefer online shopping for convenience and variety.

Regional Insights

- North America leads the market with 36% share in 2024, driven by home fragrance popularity in the U.S. and Canada.

- Europe ranks second, with strong demand in the U.K., Germany, France, and Italy for organic and sustainable wax melts.

- Asia Pacific is emerging as a high-growth region due to urbanization, rising disposable income, and growing home sales in India, China, and Thailand.

- South America and Middle East & Africa are witnessing steady growth as consumers upgrade lifestyles and embrace eco-friendly décor products.

To get to know more about this market; please visit: https://www.fortunebusinessinsights.com/wax-melts-market-112079

Competitive Landscape

The wax melts market is competitive, with global and regional players focusing on innovation, eco-friendly product launches, and festive collections.

Leading Companies:

- The Yankee Candle Company, Inc. (U.S.)

- S.C. Johnson & Son, Inc. (U.S.)

- Procter & Gamble (U.S.)

- Hampshire Candles (U.K.)

- Shearer Candles (U.K.)

- East Coast Candles (U.S.)

- Bramble Bay Collections (Australia)

- Kana Creations (India)

Notable Industry Developments

- Oct 2024 – IRIS Home Fragrances launched new Diwali gift sets including wax melts and diffusers.

- Aug 2023 – Classic Candle (U.K.) launched MiniPot Wax Melts in signature packaging.

- Dec 2022 – EMME NYC expanded its product portfolio with seasonal wax melt scents.

- Feb 2022 – Yankee Candle introduced its Well Living Collection , made with soy-coconut blends and essential oils.

The wax melts market is on a steady growth path, expected to surpass USD 2.1 billion by 2032. With increasing consumer focus on home fragrance, eco-friendly lifestyles, and gifting trends, the market offers strong opportunities for both established players and new entrants.

Key takeaway: Brands that embrace sustainable production, innovative fragrances, and digital-first sales strategies will stay ahead in the evolving wax melts industry.