Category: Chemicals & Advanced Materials

Acrylonitrile Butadiene Styrene Market Opportunities, Companies, Global Analysis & Forecast 2032

By Sharvari, 2025-09-11

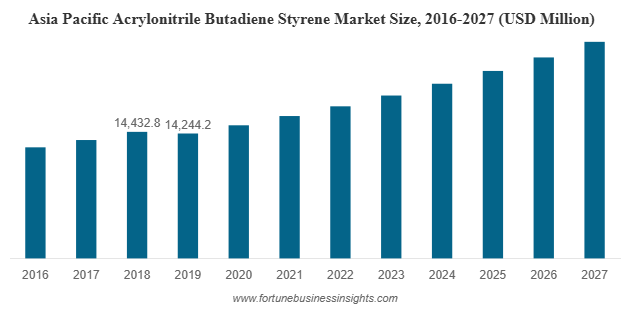

In 2019, the global acrylonitrile butadiene styrene (ABS) market was valued at USD 25,135.0 million and is expected to reach USD 42,809.5 million by 2027, growing at a compound annual growth rate (CAGR) of 6.9% during the forecast period. The Asia Pacific region led the market, accounting for 56.67% of the global share that year. Additionally, the ABS market in the United States is projected to reach USD 4,254.1 million by 2028, driven by increasing demand for durable and lightweight plastics, particularly in the automotive and consumer goods sectors.

Global Market Overview and Forecast

In a world where innovation and durability go hand in hand, the role of plastics in modern manufacturing continues to expand. One such versatile material is Acrylonitrile Butadiene Styrene (ABS) Market – a thermoplastic polymer that has quietly become a cornerstone in various industries including automotive, consumer electronics, construction, and healthcare. Known for its toughness, high impact resistance, and glossy finish, acrylonitrile butadiene styrene market is a preferred material for manufacturers who seek a balance between performance and cost-effectiveness.

The acrylonitrile butadiene styrene market has been witnessing steady growth over the past decade, with a promising future ahead. With increasing demand across key sectors, advancements in polymer technology, and the rising need for lightweight yet durable materials, ABS is expected to continue playing a vital role in global manufacturing.

This growth is being driven largely by increased demand in emerging economies, especially in Asia-Pacific, where industrialization, urbanization, and rising consumer income are pushing the consumption of electronics, vehicles, and home appliances. Asia-Pacific currently holds the largest share of the global ABS market and is expected to retain this lead well into the future.

List of Top Acrylonitrile Butadiene Styrene Companies:

- BASF (Ludwigshafen, Germany)

- 3M (Minnesota, United States)

- Covestro AG (Leverkusen, Germany)

- INEOS (London, UK)

- SABIC (Riyadh, Saudi Arabia)

- LG Chemicals (Seoul, South Korea)

- Chi Mei Corporation (Tainan City, Taiwan)

- Asahi Kasei Corp. (Tokyo, Japan)

What is Acrylonitrile Butadiene Styrene Market and Why is it Important?

Acrylonitrile butadiene styrene market is a terpolymer made by polymerizing three different monomers: acrylonitrile, butadiene, and styrene. Each of these components contributes distinct properties to the final product. Acrylonitrile provides chemical resistance and thermal stability, butadiene adds toughness and impact resistance, while styrene offers rigidity and a shiny finish.

This combination makes acrylonitrile butadiene styrene market extremely versatile. It can be easily molded into complex shapes, painted, and even plated with metals, making it ideal for applications where aesthetics meet functionality.

From the casing of your TV remote to the interior panels of your car, acrylonitrile butadiene styrene market is everywhere. Its wide range of applications and favorable properties have helped the material maintain a strong foothold in the global market.

Key Drivers Fueling Acrylonitrile Butadiene Styrene Market Growth

- Automotive Industry and Lightweighting Trends

The automotive sector is one of the most significant consumers of acrylonitrile butadiene styrene market. As car manufacturers around the world move toward lightweighting to improve fuel efficiency and reduce emissions, ABS has emerged as a go-to material. Its high impact resistance and strength-to-weight ratio make it ideal for use in interior trims, dashboards, consoles, and exterior body panels.

- Surge in Consumer Electronics and Appliances

The booming electronics and home appliance industries are also major contributors to acrylonitrile butadiene styrene market demand. acrylonitrile butadiene styrene market is widely used in the manufacturing of computer monitors, TVs, vacuum cleaners, and kitchen appliances due to its excellent finish and mechanical properties. As technology advances and consumers seek more stylish, durable products, the need for materials like acrylonitrile butadiene styrene market only grows stronger.

- Growth in the Construction Sector

ABS is also gaining traction in the construction industry, particularly in plumbing and fitting applications. It is used in pipes, wall panels, and various fixtures due to its resistance to corrosion, ease of installation, and long service life. Rapid urbanization and infrastructure development in developing countries further support this trend.

- Healthcare and Medical Devices

The global pandemic brought to light the critical importance of reliable medical equipment. acrylonitrile butadiene styrene market is frequently used in medical devices like nebulizers, syringe components, and diagnostic tools because it can withstand sterilization and has good mechanical properties. Even beyond the pandemic, the healthcare sector is expected to remain a strong growth driver.

Read More : https://www.fortunebusinessinsights.com/acrylonitrile-butadiene-styrene-abs-market-104538

Innovation and Sustainability: The Road Ahead

In response to environmental and regulatory pressure, companies are increasingly investing in recycling technologies and sustainable practices. Recycled acrylonitrile butadiene styrene market is gaining popularity, particularly in industries like automotive and electronics, where manufacturers aim to meet their sustainability goals without compromising product quality.

Innovations in acrylonitrile butadiene styrene market production, including bio-based formulations and enhanced grades with better heat and impact resistance, are also gaining traction. These advancements not only widen the application scope of ABS but also help address some of the material’s traditional limitations.

Additionally, acrylonitrile butadiene styrene market is making inroads into 3D printing, offering designers and engineers a durable and easy-to-print material for prototyping and even small-scale production.

Key Industry Developments:

- In June 2021 – Nexeo Plastics and Covestro launched the new Polycarbonate/ABS 3D printing filament Addigy FPB 2684 3D. This filament is available from now on via Nexeo Plastics’ distribution platform. With this launch, the company will continue to invest and expand their 3D printing product portfolio and support services.

- In January 2021 – INEOS Styrolution builds a demonstration plant at its Antwerp, Belgium, site to test production of ABS plastic from recycled feedstock. The project, called “LIFE ABSolutely Circular” aims at demonstrating the environmental and economic benefits of using advanced recycling technologies to close the loop of plastic recycling.

Challenges Facing the Acrylonitrile Butadiene Styrene Market

Despite its many advantages, the acrylonitrile butadiene styrene market is not without challenges. Growing environmental concerns about plastic waste are leading to stricter regulations and shifting consumer preferences. As sustainability becomes a major focus, industries are being pushed to explore recyclable or bio-based alternatives to traditional polymers like ABS.

Moreover, the volatility of raw material prices and supply chain disruptions can affect acrylonitrile butadiene styrene market production. Since acrylonitrile butadiene styrene market is derived from petrochemicals, fluctuations in oil prices and geopolitical tensions can have a direct impact on manufacturing costs.

Another emerging challenge is competition from other advanced polymers. In certain high-performance applications, materials like polycarbonate (PC), polypropylene (PP), and thermoplastic elastomers (TPEs) can replace ABS, depending on the required specifications.

Final Thoughts

The future of the acrylonitrile butadiene styrene market looks bright, driven by rising industrial demand, technological advancements, and evolving consumer lifestyles. As long as industries continue to seek reliable, versatile, and cost-effective materials, ABS will remain a valuable player.

However, sustainability will be key. Manufacturers that invest in eco-friendly solutions, recycling capabilities, and innovative product design will be better positioned to thrive in a market that’s becoming more conscious of environmental impacts.

For businesses, investors, and engineers alike, staying updated on ABS market trends isn’t just smart—it’s essential in navigating the next generation of manufacturing and product development.

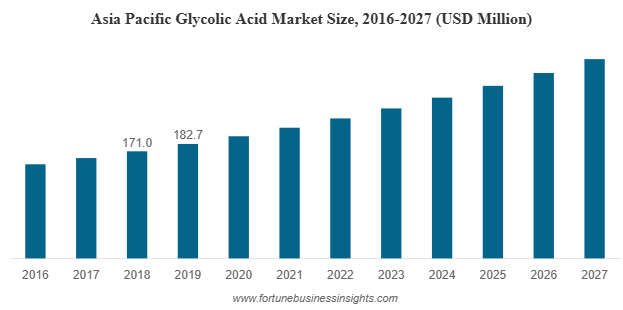

The global glycolic acid market was valued at USD 468.2 million in 2019 and is expected to reach approximately USD 820.3 million by 2027, growing at a CAGR of 7.3% over the forecast period. In 2019, Asia Pacific emerged as the leading region, accounting for 39.02% of the global market share. Meanwhile, the U.S. glycolic acid market is anticipated to hit USD 140.96 million by 2027, driven by strong demand across cosmetics, skincare, and industrial cleaning applications.

In recent years, glycolic acid market has moved from a niche skincare ingredient to a globally sought-after compound with wide-reaching applications. Whether you're browsing the label of your favorite facial cleanser or researching innovative industrial solutions, chances are glycolic acid is playing a silent but powerful role. What started as a cosmetic staple has now evolved into a multi-industry asset, gaining momentum across the globe.

The Beauty Industry : Glycolic Acid Market

No discussion of glycolic acid market is complete without highlighting its prominence in cosmetics and personal care. As the smallest alpha hydroxy acid (AHA), glycolic acid has the unique ability to penetrate the skin deeply and effectively. It promotes exfoliation, boosts collagen production, and improves skin texture—making it a favorite among dermatologists and beauty brands alike.

In the age of social media-driven beauty standards, consumers are constantly seeking products that deliver visible results. Glycolic acid fits perfectly into this narrative. Its role in anti-aging serums, exfoliating toners, acne treatments, and chemical peels continues to expand, especially in rapidly growing markets like Asia-Pacific, where the demand for premium skincare products is rising.

Furthermore, a growing awareness around skincare routines, especially among millennials and Gen Z, is pushing demand for effective and science-backed ingredients. As a result, beauty companies are launching new product lines centered around glycolic acid, helping to maintain its popularity in this highly competitive sector.

List Of Key Companies Profiled In Glycolic Acid Market:

- China Petrochemical Corporation (Sinopec Corp.), (China)

- The Chemours Company (U.S.)

- CABB Group (Germany)

- Saanvi Corp (India)

- Parchem Fine & Specialty Chemicals (U.S.)

- Water Chemical Co., Ltd (China)

- Shandong Xinhua Pharmaceutical Co., Ltd. (China)

- Mehul Dye Chem Industries (India)

- Avid Organics (India)

- Zhonglan Industry Co., Ltd. (China)

- Eastman Chemical Company (U.S.)

Beyond Beauty: Industrial and Pharmaceutical Applications

While the cosmetics industry remains a major consumer, glycolic acid is far from being a one-trick pony. It is a versatile chemical used across multiple industries. Its properties—being biodegradable, non-toxic, and water-soluble—make it an ideal component for various formulations beyond skincare.

In the pharmaceutical industry, glycolic acid is used in the manufacture of bio-absorbable sutures and controlled drug-release systems. Its effectiveness in creating biodegradable polymers is also gaining attention, particularly in the field of medical devices.

The textile and leather industries leverage glycolic acid during dyeing and tanning processes due to its efficient pH adjustment capabilities. Similarly, in food processing, it acts as a preservative and flavor enhancer.

Additionally, glycolic acid serves as an effective agent in cleaning and industrial solutions, especially for removing hard water deposits, rust, and mineral scale without damaging metal surfaces. Its increasing usage in household cleaning products and electronic component manufacturing is a testament to its adaptability.

Read More : https://www.fortunebusinessinsights.com/industry-reports/glycolic-acid-market-101922

Key Market Segments: Purity Levels and Their Uses

The glycolic acid market is segmented by purity level—primarily 99%, 70%, 30%, and others. Among these, the 99% purity segment holds the largest share, largely because it is used across high-demand sectors like pharmaceuticals, cosmetics, textiles, and food processing.

The 70% purity level is particularly used in medical applications, while 30% glycolic acid is popular in chemical peels and skincare treatments. These variations in concentration allow for customized applications across industries, ensuring that glycolic acid remains relevant across a broad spectrum of use cases.

Asia-Pacific: The Market Leader

When it comes to geographical dominance, the Asia-Pacific region leads the glycolic acid market, accounting for nearly 39% of the global share in 2019. Countries like China and India are experiencing rapid industrialization, urbanization, and economic growth, which in turn is boosting demand in both cosmetics and industrial applications.

Furthermore, the booming e-commerce landscape in these regions has made skincare products more accessible to consumers. Coupled with a growing middle-class population and increased disposable income, Asia-Pacific continues to be the most dynamic and lucrative market for glycolic acid.

Key Industry Developments:

- October 2018: CABB Group GmbH invested millions of Euros to increase the storage and production volume of monochloroacetic (MCA) acid & its derivatives at the Knapsack and Gersthofen facility. The expansion will be boosting the company’s production of glycolic acid at Gersthofen facility.

- January 2019 - Skinceuticals launched a new glycolic acid cream, Glycolic 10 Renew Overnight that improves skin glow by 36% while also maintaining tolerability. The cream effectively targets dullness, fine lines, and uneven texture of the skin. It stimulates cell regeneration for enriched tone, texture, and brighter complexion.

Market Challenges: Health, Safety, and Environmental Concerns

Despite its widespread use and benefits, glycolic acid does come with certain challenges. Overuse in cosmetics can lead to skin irritation, inflammation, and heightened sensitivity to sunlight. As a result, product developers and consumers alike must pay attention to recommended usage levels and combine glycolic acid with sun protection measures.

On the manufacturing side, the production of glycolic acid can involve hazardous byproducts such as phosgene—a compound that requires stringent regulatory control. Environmental regulations are becoming tighter, particularly in North America and Europe, which may pose challenges for manufacturers and increase compliance costs.

Additionally, the emergence of natural and plant-based alternatives such as lactic acid and salicylic acid is shifting some consumer preferences away from synthetic options, particularly in the clean beauty segment.

Competitive Landscape and Key Players

The glycolic acid market is moderately fragmented, with both global giants and regional players competing for market share. Some of the major players include:

- The Chemours Company

- CABB Group GmbH

- Water Chemical Co. Ltd.

- Parchem Fine & Specialty Chemicals

- Mehul Dye Chem Industries

- Avid Organics Pvt. Ltd.

- Zhonglan Industry Co. Ltd.

These companies are investing heavily in research and development, capacity expansion, and strategic collaborations to maintain a competitive edge.

Outlook

The growth of the glycolic acid market is not just a reflection of changing consumer habits but also a sign of how versatile and valuable this compound has become across industries. As awareness of its benefits continues to rise and innovation drives new formulations, glycolic acid is poised to remain a key ingredient in both personal care and industrial applications. For businesses looking to tap into a high-growth, high-impact market, glycolic acid market offers opportunities that extend well beyond the skincare aisle.

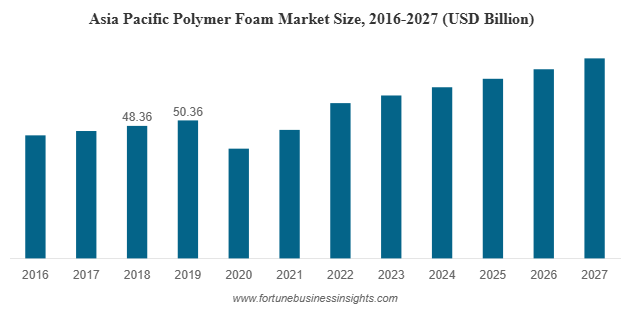

The global polymer foam market was valued at USD 114.88 billion in 2019 and is expected to grow to USD 157.63 billion by 2027, registering a CAGR of 7.73% during the forecast period. Asia Pacific led the market in 2019 with a 43.84% share, while the U.S. market is anticipated to reach USD 23.49 million by 2027, driven by rising applications in furniture, automotive, and construction insulation.

Market Snapshot: Growth at a Strong Pace

Polymer foam market might not be the first thing you think of when it comes to everyday life, but chances are you’re surrounded by them right now. From the cushion on your chair to the insulation in your walls, polymer foams play a role in comfort, safety, and energy efficiency. Their lightweight, bubble-filled structure makes them unique—offering durability, flexibility, and cushioning all in one material. In recent years, these versatile materials have become an essential part of industries like construction, automotive, packaging, and furniture. With growing demand across these sectors, the global polymer foam market is on a steady upward trajectory.

List Of Key Companies Covered:

- Sealed Air (U.S.)

- Arkema (France)

- Armacell International S.A. (Germany)

- Borealis AG (Austria)

- Polymer Technologies, Inc. (U.S.)

- Zotefoams plc (UK)

- Synthos (Poland)

- Sekisui Alveo (Switzerland)

- BASF SE (Germany)

Key Growth Drivers

- Comfort Meets Versatility

One of the strongest growth drivers of polymer foam demand is its use in furniture, bedding, and seating applications. Sofas, mattresses, office chairs, and even footwear rely on foams for comfort and support. In addition, automotive interiors like seats, armrests, and headrests have increasingly incorporated foams to enhance passenger comfort while reducing weight. This balance of strength and softness is hard to achieve with other materials. - Expanding Use in Construction

In the construction industry, polymer foams are invaluable for insulation, soundproofing, waterproofing, and flooring. With the global push toward energy-efficient buildings, foams are helping reduce energy consumption by improving thermal insulation. Their ability to act as sealants and fillers also makes them vital in creating durable, sustainable building structures. - Rising Popularity of Memory Foam

Memory foam, a form of polyurethane foam, has been one of the most significant contributors to market growth. Known for its ability to contour to body shape, memory foam has become a favorite in mattresses, pillows, and footwear. As consumers increasingly seek ergonomic solutions that improve comfort and reduce stress, the popularity of memory foam is expected to keep climbing. - Packaging and Transportation Needs

The packaging industry also leans heavily on polymer foams. Lightweight yet durable, foams are widely used to protect goods during transport. Their role in food packaging and medical product protection has become especially important, ensuring safety and extended shelf life.

Challenges in the Market

Despite the promising growth, the polymer foam industry faces challenges. One of the biggest hurdles is environmental sustainability. Most commonly used foams, such as polyurethane, polystyrene, and polyethylene, are not biodegradable. Concerns over plastic waste and stricter regulations in major economies are pushing the industry to rethink its practices. Recycling remains a challenge, although innovations in eco-friendly foams are gradually emerging.

Another challenge was seen during the COVID-19 pandemic. With lockdowns affecting construction and automotive industries, foam demand dropped temporarily. However, demand in packaging—particularly for food and healthcare products—helped offset some of the decline.

Regional Highlights

- Asia-Pacific dominates the market, holding nearly 43.84% of the global share as of 2019. Rapid industrialization, a growing middle-class population, and strong demand from construction and packaging industries in countries like China, India, and Japan are driving this dominance.

- North America also plays a significant role, with demand largely supported by the automotive, furniture, and insulation industries. The U.S. market in particular has shown resilience with its focus on comfort-based applications.

- Europe remains steady, driven by automotive interiors, home applications, and growing emphasis on sustainability in construction.

- Latin America and the Middle East & Africa are relatively smaller markets, facing slower growth due to import dependence and limited local foam production.

Read More : https://www.fortunebusinessinsights.com/industry-reports/polymer-foam-market-101698

Market Segmentation

By Type:

- Polyurethane (PU) leads the segment, widely used in construction, furniture, and bedding.

- Polystyrene (PS) is cost-effective and popular for packaging due to its insulation qualities.

- PVC foams are important in furniture manufacturing and construction boards.

- Others, such as PET and polyamide foams, serve specialized sectors including wind energy, transportation, and niche packaging.

By Application:

- Building & Construction stands as the largest segment, driven by insulation, fillers, and energy-saving requirements.

- Automotive applications continue to rise as lightweight foams help improve fuel efficiency.

- Packaging demand grows steadily, particularly in food safety and protective shipping.

- Furniture & Appliances remain strong consumers of foam materials.

- Apparel & Others cover areas such as footwear, toys, agriculture, and military products.

Key Industry Developments

- August 2019: Sheela Foam Limited, largest manufacturer of mattresses and foam based in India, acquired Interplasp SL, a Spanish Company, which has an annual production of 11,000 tons (total capacity 22,000 tons) of polyurethane foam for bedding and furniture applications.

- March 2019: Sika AG, a specialty chemical manufacturer of bonding, damping, sealing, reinforcing solutions for automotive and construction industries, acquired Belineco LLC, a Belarus-based producer of polyurethane foam systems. With this acquisition, Sika is further expected to develop its technology to manufacture polyurethane foams.

Industry Players and Developments

Global leaders in the polymer foam industry include companies like BASF, SABIC, Sealed Air, Arkema, Armacell, Zotefoams, Toray, and Celanese. These players are focusing on mergers, acquisitions, and new product launches to strengthen their foothold.

For example, Sheela Foam of India expanded its polyurethane business by acquiring Interplasp in Spain, while Sika AG of Switzerland strengthened its polyurethane systems through the purchase of Belineco in Belarus. Such strategic moves highlight how companies are striving to expand geographically and technologically.

The Road Ahead

Looking forward, the polymer foam market shows no signs of slowing down. Growth will continue to be driven by booming construction in emerging economies, rising demand for comfort-based products, and ongoing innovations in memory foam and other specialty foams. However, sustainability will be the key theme for the future. Companies that invest in eco-friendly materials, recycling technologies, and compliance with green regulations are likely to set themselves apart.

Future Outlook

The global polymer foam market is much more than a materials industry—it’s an innovation-driven sector that touches our daily lives in countless ways. From energy-efficient homes and safer packaging to more comfortable furniture and advanced automotive interiors, polymer foams have established themselves as essential. While challenges around sustainability remain, the industry’s strong growth prospects and adaptability ensure it will remain at the forefront of modern living and industrial progress.

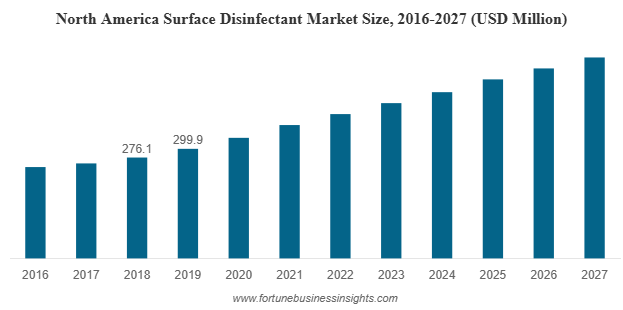

The global surface disinfectant market was valued at USD 770.6 million in 2019 and is expected to grow significantly, reaching USD 1,547.7 million by 2027. This reflects a robust compound annual growth rate (CAGR) of 9.1% during the forecast period from 2020 to 2027. In 2019, North America led the market, accounting for 38.92% of the global share. The United States, in particular, is projected to experience substantial growth, with the market expected to reach USD 524.4 million by 2027. This upward trend is largely fueled by increased awareness around hygiene and sanitation in the wake of the pandemic, especially across the healthcare, residential, and commercial sectors.

Market Snapshot: From Billions to Bigger Billions

Over the last few years, the global mindset around hygiene has undergone a massive shift. What was once considered a routine task has now become a top priority across homes, hospitals, public spaces, and workplaces. At the heart of this change lies one key product category: surface disinfectants market.

From kitchen countertops to operating room tables, surface disinfectants market have become an essential line of defense against harmful pathogens. But beyond their daily use, these products are also at the center of a booming global market—one that’s poised for remarkable growth in the coming years.

List of Top Surface Disinfectant Companies:

- 3M (U.S.)

- The Proctor & Gamble Company (U.S.)

- Kimberley-Clark Corporation (U.S.)

- SC Johnson Professional (U.S.)

- The Clorox Company (U.S.)

- Ecolab (U.S.)

- Metrex Research LLC(U.S.)

- Reckitt Benckiser Group Plc (U.K.)

- Diversey Inc.(U.S.)

The Role of Healthcare and HAIs

One of the largest consumers of surface disinfectants continues to be the healthcare sector. Hospitals, clinics, and diagnostic centers rely on disinfectants to minimize the risk of hospital-acquired infections (HAIs)—a serious concern that affects millions of patients globally every year. HAIs such as bloodstream infections, urinary tract infections, and ventilator-associated pneumonia are preventable to a large extent with strict disinfection protocols.

As healthcare systems become more advanced and patient safety takes center stage, the demand for high-performance disinfectants that can neutralize a broad range of pathogens is only expected to rise.

Breaking Down the Market: What’s in Demand?

Surface disinfectants are not a one-size-fits-all category. The market can be broadly segmented by type, composition, and application, each playing a unique role in how and where these products are used.

- By Type: Liquids Lead the Way

Liquid disinfectants currently dominate the market due to their widespread use in both residential and commercial settings. They offer versatility, cost-effectiveness, and ease of application across a variety of surfaces. However, wipes are quickly gaining popularity, especially in consumer and office environments. Their convenience, portability, and reduced cross-contamination risk make them an increasingly preferred choice.

- By Composition: Alcohol-Based Rules, But Alternatives Rise

Alcohol-based disinfectants remain the most widely used, especially in healthcare and public spaces, due to their proven effectiveness against bacteria and viruses. These products are fast-acting, evaporate quickly, and are generally approved by regulatory authorities worldwide.

That said, peracetic acid and hydrogen peroxide-based solutions are seeing significant growth, especially in industrial and food processing sectors. These alternatives offer high-level disinfection with less toxicity and are more environmentally friendly—an important consideration for the future of the market.

- By Application: Beyond Hospitals

While healthcare remains the largest segment, applications in commercial spaces, transportation, and homes are contributing heavily to the market’s growth. Offices, gyms, schools, and public transit systems are all embracing strict disinfection protocols. On the residential side, consumers have become more proactive in maintaining hygiene, stocking their homes with disinfectant sprays, wipes, and multi-surface cleaners as part of daily routines.

Regional Growth: Asia-Pacific on the Rise

While North America currently holds the largest market share, driven by strong healthcare infrastructure and high awareness levels, it’s the Asia-Pacific region that’s showing the fastest growth. Countries like India and China are witnessing a surge in demand due to increased healthcare spending, growing urban populations, and improved access to hygiene products.

Government campaigns focused on sanitation, coupled with rising consumer awareness, are accelerating the adoption of surface disinfectants across both urban and rural areas. Moreover, local manufacturing and distribution are expanding rapidly, making products more accessible and affordable.

Read More : https://www.fortunebusinessinsights.com/surface-disinfectant-market-103062

Innovation and Sustainability: The Future Focus

As the surface disinfectant market matures, innovation is becoming a key differentiator. Brands are focusing on developing eco-friendly, non-toxic, and biodegradable formulas that are safer for both people and the environment. Alcohol-free disinfectants, enzyme-based cleaners, and sustainable packaging are emerging trends to watch.

Additionally, smart disinfection technologies—such as automated dispensers, UV sanitizing devices, and antimicrobial coatings—are being integrated into larger sanitation ecosystems in healthcare and commercial buildings.

Key Industry Developments:

- January 2019 – Reckitt Benckiser formed a strategic alliance with Diversey to increase its presence in North America. This strategic alliance will help Reckitt Benckiser to expand its reach to educational institutes, food establishments, and hospitals.

- February 2020 – The Procter and Gamble Company launched a new line of antibacterial cleaners named Microban 24. The new product line is said to protect the applied surface for a complete 24 hours, even when the surface has been contacted multiple times.

Challenges to Consider

Despite the optimistic outlook, the market does face some challenges. The hazardous nature of certain chemicals used in disinfectants requires careful handling, storage, and disposal. Regulatory scrutiny is tightening, and companies must ensure compliance with safety standards while continuing to innovate.

Also, consumer misinformation about effectiveness, overuse of certain chemicals, and environmental concerns are pushing manufacturers to strike a balance between performance and sustainability.

Future Outlook

The surface disinfectant market is no longer a niche segment—it’s a central player in the global effort to maintain hygiene and prevent the spread of disease. As demand grows across healthcare, residential, and industrial sectors, this market offers significant opportunities for innovation, sustainability, and improved public health outcomes.

In a world where cleanliness is no longer optional, surface disinfectants market have earned their place as everyday essentials. The future belongs to brands that can deliver powerful protection—without compromising safety or sustainability.

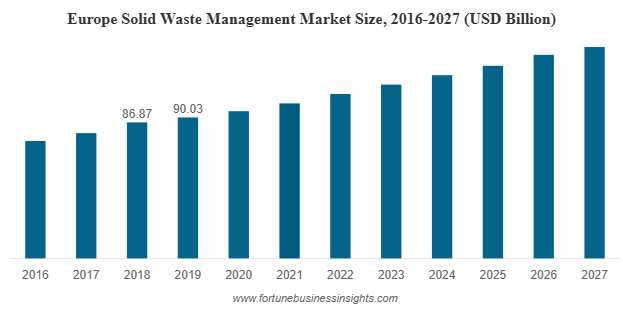

The global solid waste management market was valued at USD 285.16 billion in 2019 and is expected to reach approximately USD 366.52 billion by 2027, growing at a compound annual growth rate (CAGR) of 3.3% during the forecast period. In 2019, Europe led the market, accounting for 31.57% of the global share, driven by its advanced infrastructure and stringent environmental regulations. Meanwhile, the United States market is projected to experience significant growth, with its value expected to reach around USD 93.46 billion by 2032. This growth is largely attributed to the country’s robust collection, processing, and disposal systems, as well as the strong presence of major industry players such as Waste Management Inc., Covanta Holding Corporation, Clean Harbors Inc., and others.

The Market at a Glance

In a world that thrives on consumption, one unavoidable byproduct of modern life is waste. From overflowing landfills to plastic-laden oceans, improper waste disposal has become one of the most pressing environmental issues of our time. But the story doesn’t end there. A silent revolution is underway solid waste management market is transforming from a reactive necessity into a proactive industry driving innovation, sustainability, and economic growth.

List Of Key Players Profiled:

- Waste Management Inc. (USA)

- SUEZ Group (France)

- Veolia Environment S.A. (France)

- Biffa PLC (U.K.)

- Clean Harbors Inc. (USA)

- Covanta Holdings Corporation (USA)

- Hitachi Zosen Corporation (Japan)

- Remondis AG & Co. Kg (Germany)

- Republic Services Inc. (USA)

- Stericycle Inc. (USA)

Why the Industry is Booming

- Urbanization and Population Growth

With more people moving into urban areas, the volume of municipal and industrial waste is escalating rapidly. Cities generate enormous amounts of garbage daily—from household refuse and commercial waste to construction debris and hazardous materials. Managing this rising tide of waste requires robust systems and infrastructure, fueling demand for waste collection, recycling, and disposal services.

- Government Regulations and Environmental Policies

Governments worldwide are tightening environmental regulations and implementing new waste management policies. These include landfill bans on recyclable and compostable materials, mandatory recycling programs, and incentives for using clean technologies. Such regulations are pushing industries and municipalities to invest more in effective waste treatment and recycling facilities.

- The Shift Towards a Circular Economy

The traditional linear model of "take, make, dispose" is being replaced by the circular economy—an approach where resources are kept in use for as long as possible. Waste is no longer seen solely as a problem but as a resource that can be reused, recycled, or converted into energy. This shift is not just environmentally beneficial but also economically attractive, spurring innovation in waste processing technologies.

Market Segmentation: What’s Driving Growth?

By Waste Type

Among the different categories, industrial waste leads the global market. With the rise of manufacturing and heavy industries, especially in developing economies, the need for proper disposal of non-hazardous and hazardous industrial waste has become critical. These industries are under increasing pressure to manage waste in compliance with environmental standards.

Municipal solid waste, which includes everyday items discarded by the public, is also a major contributor. This includes organic waste, paper, plastics, glass, and metals. As urban populations grow, the volume of municipal waste is expected to rise steadily, further fueling the need for comprehensive waste management systems.

By Service

The market is also segmented by services such as collection, processing, disposal, and recycling. Waste collection dominates the segment, accounting for more than half of the market share. This service is critical, especially in densely populated urban centers where effective collection systems prevent public health hazards.

However, there is growing investment in waste processing and recycling. Technologies like composting, anaerobic digestion, incineration, and waste-to-energy conversion are gaining ground. These not only reduce the volume of waste sent to landfills but also generate electricity, heat, or fuel—making waste management more sustainable and profitable.

Read More : https://www.fortunebusinessinsights.com/solid-waste-management-market-103045

Geographic Landscape: Who’s Leading?

- Europe

Europe is a global leader in solid waste management market, with a highly developed infrastructure and strong government support. Many European countries have advanced waste-to-energy facilities, and recycling rates are among the highest in the world. Strict regulations and public awareness campaigns have contributed to Europe’s success in minimizing landfill use and promoting circular economy principles.

- North America

The United States is also a major player in the solidwaste management industry, with a highly organized collection system and a growing focus on sustainability. Public and private sector collaboration, along with technological innovation, is driving growth. Key players in the region are expanding their operations and investing in smart waste tracking, segregation technologies, and energy recovery systems.

- Asia-Pacific

Asia-Pacific represents the fastest-growing market, driven by rapid urbanization in countries like China, India, and Southeast Asian nations. However, the region also faces challenges such as underdeveloped infrastructure, limited public awareness, and lack of regulatory enforcement. Despite these hurdles, rising investments and government initiatives aimed at improving waste management are setting the stage for substantial growth in the coming years.

Key Industry Developments:

-

July 2019 – The consortium BCE led by SUEZ Group signed a 25 years contract with municipal company Beogradske Elektrane to sell heat produced from waste-to-energy in Belgrade, Serbia. By signing this contact, the municipal company is aiming to introduce renewable energy by reducing its energy dependency on natural gas. The plant operation will be handled by SUEZ Group and the plant will process 500 Kilo Tons of Municipal waste and 200 Kilo Tons of construction & demolition waste per year.

- December 2019 – Covanta Holdings Corporation agreed with Zhao County, China to build & operate a new Energy-from-waste facility. The project will offer sustainable waste management solutions to the county. With this agreement, the company is aiming to expand its geographical footprints into Chinese market.

Challenges Ahead

While the solid waste management market shows promise, several obstacles remain:

- High operational costs: Advanced equipment, labor, and technology require significant investment.

- Inadequate infrastructure: In many developing regions, basic collection and disposal systems are still lacking.

- Low public participation: Recycling and segregation rely heavily on citizen involvement, which is inconsistent across regions.

- Illegal dumping and informal sectors: In some areas, informal waste pickers dominate the industry, leading to unsafe and inefficient practices.

Addressing these challenges will require a combination of technological innovation, policy reform, and public education.

Looking Forward: The Future of Solid Waste Management Market

The future of solid waste management market lies in smart solutions, public-private partnerships, and green technologies. From AI-driven sorting systems to decentralized composting and real-time monitoring of collection routes, the industry is evolving at a rapid pace. As climate change continues to dominate global conversations, effective waste management will be key to achieving environmental sustainability.

Solid waste management market is no longer just about getting rid of garbage—it’s about rethinking our relationship with waste. The industry is shifting toward a more sustainable, circular, and tech-driven model. For investors, policymakers, entrepreneurs, and communities alike, this market presents not just an environmental imperative but also a growing economic opportunity.

Aerospace and Defense Materials Market Size, SWOT Analysis, Trends & Forecast 2032

By Sharvari, 2025-09-10

The aerospace and defense materials industry is one of the most technologically advanced and strategically critical sectors in the world. Behind every aircraft, spacecraft, and defense system lies a foundation of highly engineered materials that provide strength, resilience, and performance. From composites to super alloys, these materials are not just structural components—they are enablers of efficiency, innovation, and security. The aerospace and defense materials market has witnessed consistent growth over the past decade, and its trajectory looks promising as the demand for lighter, stronger, and more durable materials continues to rise.

Market Growth and Forecast

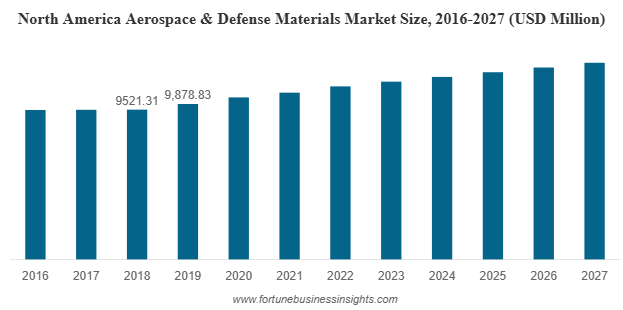

The global aerospace and defense materials market was valued at USD 18,411.83 million in 2019 and is anticipated to reach USD 23,825.45 million by 2027, registering a CAGR of 4.21% over the forecast period. North America led the market in 2019 with a 53.65% share, while the U.S. market alone is expected to generate USD 12,019.42 million by 2027, driven by advancements in lightweight and high-performance materials.

List Of Key Companies Profiled In Aerospace And Defense Materials Market:

- Arconic Inc. (US)

- Toray Composite Materials America, Inc. (US)

- Huntsman (US)

- Evonik Industries (Germany)

- Hexcel Corporation (US)

- Materion Corp. (US)

- AMI Metals Inc. (US)

- TATA Advanced Materials Limited. (India)

- Koninklijke Ten Cate BV (Netherlands)

Key Drivers of Market Growth

- Rising Aircraft Demand

The rapid growth of the global middle class and increasing disposable income have boosted the demand for air travel. Airlines are under pressure to expand their fleets with modern, fuel-efficient aircraft. This surge directly drives the demand for advanced materials such as composites, titanium alloys, and aluminum.

- Focus on Light weighting

Reducing aircraft weight has become a top priority for manufacturers, as lighter planes consume less fuel and emit fewer carbon emissions. Composites and titanium alloys are now widely used in aircraft structures and engines, replacing heavier traditional metals.

- Defense Spending

Geopolitical tensions and modernization programs are fueling growth in the military segment. Countries are investing in advanced fighter jets, drones, and helicopters—all of which require specialized high-performance materials.

- Technological Innovations

New generations of materials, from carbon-fiber composites to heat-resistant super alloys, are pushing the boundaries of aerospace engineering. More than 80% of titanium alloys used in aerospace are dedicated to engines alone, showcasing the importance of high-performance materials in critical components.

Material Segmentation: What’s Leading the Market?

- Composites: Currently the most valuable segment, composites dominate due to their exceptional strength-to-weight ratio. They are expected to grow the fastest in both value and volume, especially as next-generation aircraft integrate higher composite content.

- Aluminum: While newer materials are gaining traction, aluminum remains the most widely used by volume, especially in structural and interior components.

- Titanium Alloys: With superior corrosion resistance and high strength, titanium alloys are the second-fastest growing category, particularly in jet engines and defense applications.

- Super alloys: Accounting for over 16.6% of the market in 2019, super alloys are vital in engine components due to their ability to withstand extreme conditions.

End-User Insights: Commercial vs. Military

- Commercial Aircraft: This segment dominates the aerospace and defense materials market. With global airlines expanding fleets and replacing aging aircraft, commercial aviation accounts for the majority of material demand.

- Military Aircraft: Though smaller in volume, the military segment is growing at a faster pace. Rising defense budgets, territorial disputes, and the development of stealth and unmanned aircraft are driving demand for specialized, durable materials.

Read More : https://www.fortunebusinessinsights.com/aerospace-defense-materials-market-102980

Regional Landscape

- North America: In 2019, North America held more than 53.65% of the global market share. The region benefits from the presence of major aerospace companies such as Boeing, Lockheed Martin, and General Electric, alongside significant defense spending. By 2027, the U.S. aerospace and defense materials market alone is expected to cross USD 12,019.42 million.

- Europe: Europe ranks second, driven by strong aerospace manufacturing in France, Germany, and the U.K. Airbus, Safran, and Rolls-Royce continue to play pivotal roles in boosting demand.

- Asia-Pacific: Expected to be the fastest-growing region, thanks to indigenous aircraft programs in China and India, alongside collaborations with international aerospace players. COMAC’s C919 in China and India’s defense projects are notable drivers.

- Emerging Markets: Latin America, the Middle East, and Africa are also gaining momentum. Brazil, Mexico, Turkey, and Israel are investing in aerospace manufacturing, while the Gulf states are expanding defense capabilities.

Challenges in the Market

While the outlook is promising, the aerospace and defense materials market faces several challenges:

- Stringent Regulations: New materials undergo years of rigorous testing before being approved for aerospace use. This slows the adoption of innovative technologies.

- High Costs: Advanced materials like carbon composites and titanium alloys are significantly more expensive than traditional metals, posing challenges for cost-sensitive airlines and defense programs.

- Supply Chain Disruptions: Events like the COVID-19 pandemic highlighted vulnerabilities in global supply chains, delaying production and project timelines.

Key Industry Developments:

- April 2020 – Hexcel Corporation, an advanced composites manufacturer headquartered in the US, and Woodward, Inc., a key player providing designing, manufacturing and other services in the aerospace industry headquartered in the US, announced mutual termination of merger agreement, which was previously announced in January 2020. The disruption caused by the COVID-19 outbreak has forced the companies to announce the termination of the agreement.

- August 2019 – Teijin Ltd, a Japan-based manufacturer of advanced materials and chemicals, announced the successful acquisition of Renegade Materials Corporation, a key supplier of highly heat-resistant thermoset prepreg for the aerospace industry in North America. This has strengthened Tenjin’s position in the aerospace business and also increased its manufacturing capabilities.

Outlook

The aerospace and defense materials market is set to expand steadily as the aviation sector rebounds, military modernization accelerates, and new technologies enter the mainstream. With light weighting, efficiency, and performance at the core of material innovation, composites, titanium alloys, and super alloys will remain central to industry growth. At the same time, regulatory barriers and high costs may continue to test the pace of adoption.

The aerospace and defense materials market is more than just numbers and forecasts—it is the foundation of innovation in the skies and in defense systems. As manufacturers, suppliers, and governments invest in cutting-edge technologies, the demand for advanced materials will only intensify. By 2027, the market’s steady climb will reflect not just the growth of aviation and defense but also the evolving role of materials as the true backbone of aerospace engineering.

Agriculture has always been the backbone of human civilization. But in recent decades, farmers across the globe have faced mounting challenges—climate change, soil degradation, water scarcity, and a rapidly growing population with shifting dietary preferences. These factors are pushing the agricultural industry to adapt faster than ever before. Amid this transformation, one innovative solution has quietly emerged as a game-changer: agro-textiles market.

Agro-textiles market are specially engineered fabrics designed for agricultural applications. From protecting crops against harsh sunlight to conserving water and shielding plants from pests, these textiles are redefining the way we grow food. Beyond being a farming aid, they represent a sustainable, technologically advanced path toward a more resilient future in agriculture.

The Growing Agro-Textiles Market

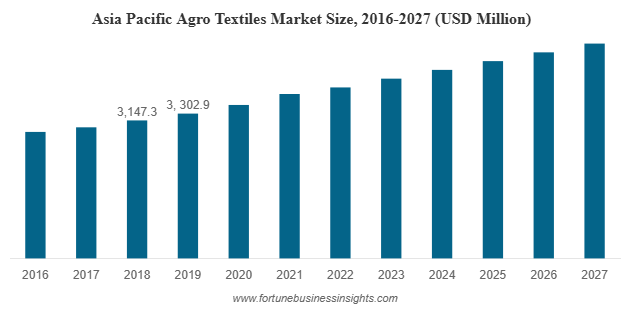

The global agro-textiles market was valued at USD 9,612.8 million in 2019 and is expected to reach USD 13,458.7 million by 2027, growing at a CAGR of 5.2% during the forecast period. Asia Pacific led the market in 2019, accounting for 34.36% of the share, while the U.S. market is anticipated to hit USD 1,766.4 million by 2027, driven by innovations in crop protection and the growing shift toward sustainable agriculture.

One of the key reasons for this growth is the rising global demand for food. With the world population expected to surpass 9 billion by 2050, farmers are under immense pressure to increase yield while maintaining environmental balance. Agro-textiles provide a practical answer—protecting crops, saving resources, and boosting production efficiency.

List of Top Agro Textiles Companies:

- SRF Limited (India)

- B&V Agro Irrigation Co. (India)

- (Japan)

- Beaulieu Technical Textiles. (Belgium)

- Meyabond Industry & Trading (Beijing) Co., Ltd. (China)

- Belton Industries. (U.S.)

- Neo Corp International Limited. (India)

- Hy-Tex (UK) Limited (U.K.)

Why Agro-Textiles Are on the Rise

Several interconnected factors are fueling the demand for agro-textiles market:

- Climate Challenges

Unpredictable rainfall, intense heatwaves, and frequent storms pose severe threats to farming. Agro-textiles like shade nets, crop covers, and windbreak fabrics help mitigate these risks by creating controlled microclimates. - Shift in Diets

As incomes rise globally, diets are shifting toward high-value foods like fruits, vegetables, and proteins. These crops often require greater care and protection, which agro-textiles readily provide. - Urbanization & Limited Farmland

With shrinking arable land, farmers must do more with less. Techniques like greenhouse cultivation and vertical farming rely heavily on agro-textile applications to maximize efficiency. - Sustainability Goals

Governments and organizations worldwide are pushing for eco-friendly farming solutions. Many agro-textiles today are developed using biodegradable or recyclable materials, aligning with sustainability targets.

Read More : https://www.fortunebusinessinsights.com/agro-textiles-market-102963

Key Applications Driving Growth

Agro-textiles have diverse uses across different agricultural segments. Let’s look at the most impactful applications:

- Shade Nets and Crop Covers

These are widely used to protect plants from excessive sunlight, wind, and frost. By regulating temperature and light, they improve crop quality and extend the growing season. - Fishing Nets and Aquaculture

Fishing nets remain one of the largest segments in the agro-textile industry. As global demand for fish and seafood rises, aquaculture relies heavily on durable and advanced textile solutions. - Ground Covers and Mulching Mats

Designed to suppress weeds, conserve soil moisture, and improve soil structure, these textiles reduce the need for chemical herbicides while promoting healthier soil. - Irrigation Solutions

Innovative fabrics like hydrating tubes with micropores allow water to reach plant roots directly, drastically improving water efficiency in drought-prone regions.

Regional Insights

While the agro-textiles market is global, certain regions are leading the way:

- Asia-Pacific holds the largest share, fueled by massive demand from China and India. Both countries use agro-textiles extensively in agriculture, aquaculture, and horticulture, driven by their large populations and food security goals.

- North America, especially the United States, is witnessing rapid adoption of advanced agro-textiles. The U.S. market alone is projected to exceed USD 1,766.4 million by 2027, supported by sustainability-driven farming innovations.

- Europe remains an important player, with a strong focus on eco-friendly materials and regulatory support for sustainable agricultural practices.

Key Industry Developments:

- January 2020– Diatex presented in the world’s leading trade fair IPM ESSEN 2020 for horticulture that took place in Germany. The company will present a tailor-made plant protection system and other crop field protection products at the IPM ESSEN 2020.

Innovation at the Core

The agro-textiles industry thrives on innovation. Some of the most exciting advancements include:

- UV-resistant and weatherproof fabrics that last longer and reduce maintenance costs.

- Biodegradable agro-textiles that prevent long-term soil and plastic pollution.

- Antibacterial coatings that keep plants healthier and extend shelf life post-harvest.

- Knitted shade fabrics tailored for specific crops, allowing farmers to fine-tune the growing environment.

These innovations not only improve performance but also make agro-textiles more environmentally responsible.

Challenges Along the Way

Despite its promising growth, the agro-textiles market faces some hurdles:

- Volatile raw material prices, particularly petroleum-based fibers like PET.

- High upfront costs for infrastructure and setup, which can discourage small-scale farmers.

- Lack of awareness in many regions, where traditional farming practices still dominate.

- Regulatory pressures on plastic-based materials, pushing companies to invest in sustainable alternatives.

Overcoming these challenges requires collaboration between governments, manufacturers, and farming communities.

Future Outlook

The future of agro-textiles market is bright. With growing awareness, rapid innovation, and stronger global emphasis on food security, these fabrics are set to become an integral part of modern agriculture. From small-scale farmers to large agribusinesses, agro-textiles offer a toolkit for tackling today’s farming challenges while preparing for tomorrow’s.

Thermal Paper Market Opportunities, Trends & Industry Analysis, Forecast 2032

By Sharvari, 2025-09-09

Thermal paper market is a specialized type of paper designed to change color when exposed to heat, eliminating the need for traditional inks. This effect is achieved by applying a coating of heat-sensitive dyes and color developers during the manufacturing process. The coating typically contains leuco dyes, organic acid developers, and sensitizers. Leuco dye, a colorless crystalline powder, melts when heated and reacts with an organic acid (the developer) to produce a visible color. Commonly, the developers used are Bisphenol-A (BPA) or Bisphenol-S (BPS).

- 2019 market size: USD 3.45 billion

- Forecast by 2027: USD 5.85 billion

- CAGR: 6.9%

- Leader: Europe

- Fastest growing region: Asia-Pacific

- Top application: Point-of-Sale systems

- Trend to watch: Sustainable, BPA-free alternatives

A Market on the Rise

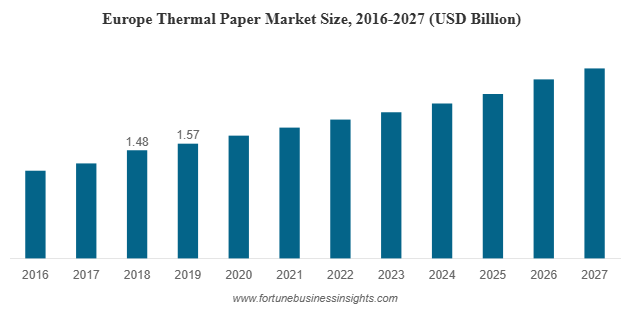

The global thermal paper market was valued at USD 3.45 billion in 2019 and is expected to climb to USD 5.85 billion by 2027, growing at a CAGR of 6.9% during the forecast period. Europe led the market in 2019, accounting for 42.03% of the share, supported by strong retail and POS adoption. Meanwhile, the U.S. market is projected to reach USD 1.01 billion by 2027, fueled by increasing use across POS terminals, ATMs, and ticketing systems, along with the rising need for affordable and efficient printing solutions.

List Of Key Companies Profiled:

- Lecta (Spain)

- Hansol Paper (Korea)

- Appvion Operations, Inc. (USA)

- Domtar Corporation (USA)

- Ricoh Industrie France SAS (France)

- Mitsubishi Hi-Tech Paper (Germany)

- Koehler Paper Group (Germany)

- Kanzaki Specialty Papers, Inc. (USA)

- Jujo Thermal Ltd. (Finland)

- Oji Paper Co., Ltd. (Japan)

Segments That Matter

One interesting aspect of this market is its segmentation.

- By Width: The 3.125” (80 mm) rolls are the most widely used, especially in retail POS machines and lottery systems. If you’ve swiped your card at a store and received a wide receipt, chances are it came from this size category.

- By Technology: Direct thermal printing holds the lion’s share. It’s cost-effective, portable, and efficient—qualities that make it a favorite in retail and logistics industries.

- By Application: The POS segment dominates the market, as every retail counter, restaurant, and shopping center needs quick, reliable printing. At the same time, the tags and labels segment is gaining traction, accounting for nearly a quarter of the market in 2019, thanks to the logistics and e-commerce boom.

The BPA Dilemma

It’s not all smooth sailing for the thermal paper industry. A key challenge lies in the use of BPA (Bisphenol-A), a chemical developer traditionally used in thermal coatings. BPA has been under scrutiny for potential health risks, including endocrine disruption. Regulatory bodies in Europe and North America are tightening rules, urging manufacturers to find safer alternatives.

This shift is sparking innovation. Alternatives like BPS (Bisphenol-S) and Pergafast-201 are being developed and adopted, signaling a move toward sustainable and safer thermal paper solutions. While this transition comes with costs, it also presents opportunities for companies to differentiate themselves in an increasingly eco-conscious market.

Read More : https://www.fortunebusinessinsights.com/thermal-paper-market-102811

Why Thermal Paper Isn’t Going Anywhere

Some might wonder if thermal paper will survive in an increasingly digital world. After all, don’t digital wallets, e-receipts, and paperless billing threaten its existence? The answer is nuanced. While digital options are growing, the need for physical receipts, labels, and documentation remains strong across many industries.

Think about logistics—shipping labels and barcodes aren’t going away anytime soon. Retail and foodservice sectors still rely heavily on printed receipts. Healthcare and pharmaceuticals demand reliable printed labels for medications, diagnostics, and patient tracking. In short, while the format may evolve, the core demand for thermal paper is here to stay.

The Regional Leaders

When it comes to regional dominance, Europe leads the thermal paper market. Back in 2019, it accounted for about 42.03% of the global share, thanks to its strong retail infrastructure, widespread adoption of POS technology, and growing need for reliable labels in healthcare and logistics.

The United States also plays a big role, with its market projected to cross USD 1.01 billion by 2027. Here, the massive volume of ATM withdrawals, paired with a culture of digital billing and retail receipts, keeps the demand for thermal paper high.

But the story doesn’t end there. Asia-Pacific is fast becoming a powerhouse in this sector. Countries like China and India are seeing explosive growth in online shopping, cashless transactions, and logistics services. As e-commerce giants expand, the need for shipping labels, order receipts, and retail billing systems is skyrocketing. Meanwhile, Latin America, the Middle East, and Africa are gradually expanding as well, driven by rising trade, transport networks, and retail activity.

Key Industry Developments:

- July 2019 – Lecta announced that all the thermal paper it supplies in the European Union will be BPA-free, to comply with the prohibition announced by the EU from January 2020.

- February 2020 – Domtar Corporation announced the acquisition of the POS paper business of Appvion Operations, Inc. The transaction includes acquirement of the coater and related equipment located at Appvion’s Ohio based facility. Domtar seeks to make a globally competitive POS paper business and open new avenues for the growth of the company via this acquisition.

Looking Ahead

The thermal paper market may not be flashy, but it’s resilient, innovative, and quietly expanding. Its growth is anchored in daily essentials—receipts, labels, and tickets—that keep businesses and consumers connected. As industries expand and commerce continues to evolve, thermal paper will remain a key enabler of smooth transactions and efficient logistics. The next time you collect a receipt, tag, or label, remember—it’s not just a slip of paper. It’s part of a global market that’s growing faster than most of us realize.

Aluminum Composite Panels Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-09-09

The face of modern architecture is changing rapidly, and one material at the heart of this transformation is the aluminum composite panels (ACP) market. These sleek, durable, and versatile panels are no longer just decorative finishes on skyscrapers; they’ve become essential to construction, automotive design, advertising, and even infrastructure projects. With global demand rising, the ACP market is on track to reach new heights over the next decade.

A Market on the Rise

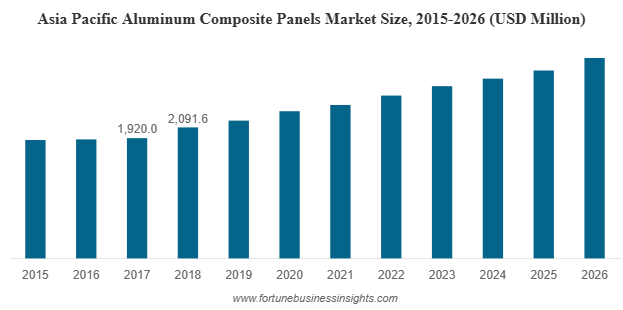

The global aluminum composite panels market was valued at USD 5.33 billion in 2018 and is expected to reach USD 8.71 billion by 2026, registering a CAGR of 6.1% during the forecast period. Asia Pacific led the market in 2018 with a 39.23% share, driven by rapid urbanization and large-scale infrastructure projects. In the U.S., the aluminum composite panels market is anticipated to witness strong growth, projected to reach USD 2.41 billion by 2032, supported by favorable policies and initiatives aimed at enhancing infrastructure across North America.

List Of Key Companies Profiled In Aluminum Composite Panels Market:

- 3A Composites GmbH

- Arconic

- Mitsubishi Chemical Corporation

- Hyundai Alcomax Co.,Ltd.

- Fairfield Metal LLC

- Jyi Shyang Industrial Co., Ltd.

- ALUMAX INDUSTRIAL CO., LTD.

- Yatai Industrial Group Co., Ltd.

- Shanghai Huayuan New Composite Materials Co., Ltd.

- Guangzhou Xinghe Aluminum Composite Panel Co., Ltd.

Segments That Shape the Market

The ACP market is diverse, catering to multiple applications and product types:

- By Product Type: Polyvinylidene fluoride (PVDF)-coated panels dominate due to their resistance to UV rays and long-lasting performance. Other types include polyester coatings, oxide films, and laminating coatings. Each comes with specific benefits suited to different industries.

- By Application: Building and construction remains the largest segment, followed by automotive and advertising. ACPs are also used in railways and other industrial applications, showing their versatility across sectors.

Why ACPs Are in Demand

- Boom in Construction: The construction industry is the backbone of ACP demand. Modern buildings require materials that are not only durable but also aesthetically pleasing. ACPs fit the bill perfectly with their smooth finishes, range of textures, and ability to mimic natural materials like wood, stone, or steel. They’re lightweight, easy to install, and offer insulation benefits—making them a favorite for facades, cladding, and interior applications.

- Outdoor Advertising: Billboards, signage, and digital displays increasingly use ACPs because of their ability to withstand harsh weather, resist corrosion, and deliver a sleek, professional finish. From highways to airports, ACPs have become the go-to medium for durable advertising structures.

- Automotive Industry: ACPs are also making their mark in mobility. From buses to luxury vehicles, they provide thermal insulation, reduce noise, and add to the visual appeal. Lightweight yet strong, they help improve efficiency without compromising on safety or design.

- Rapid Urbanization in Asia-Pacific: The Asia-Pacific region leads global ACP consumption, thanks to massive infrastructure development in countries like China and India. Affordable housing projects, metro rail systems, airports, and commercial complexes all rely heavily on ACPs.

- Sustainable and Energy-Efficient Construction: As sustainability becomes a priority, ACPs are favored for their recyclability and ability to improve building insulation, reducing energy consumption in both residential and commercial structures.

Read More : https://www.fortunebusinessinsights.com/aluminum-composite-panels-market-102304

Regional Highlights

- Asia-Pacific: The largest and fastest-growing region, driven by rapid urban development, infrastructure expansion, and government-backed housing projects.

- North America: Growth fueled by infrastructure modernization and an increasing preference for energy-efficient building materials.

- Europe: Known for stringent building regulations, Europe favors fire-safe and sustainable ACP variants, especially in retrofitting projects.

- Latin America and Middle East: Emerging markets with rising urban infrastructure needs and increasing adoption in commercial complexes and transport hubs.

Challenges Along the Way

While the growth story is impressive, ACPs are not without challenges. One of the biggest concerns is repair and maintenance costs. Once damaged, panels are often difficult to fix without replacing the entire sheet, which can be expensive. Additionally, raw material price fluctuations, especially in aluminum, pose a challenge for manufacturers trying to balance costs. Fire safety regulations are another hurdle. Certain types of ACP cores, such as those made from polyethylene, face restrictions in many regions due to fire hazards, pushing manufacturers to innovate with safer alternatives.

Key Industry Developments:

- July 2017 – Fairview Architectural acquired the Stryum business, an intelligent non-combustible aluminum cladding system, from Vitekk Industries. The company includes a variety of high-quality aluminum plate façade panels designed to provide durability and sustainability, complimenting Fairview's current portfolio of cladding solutions, including high-density cement fibre, natural stone, terracotta tiles and the leading non-combustible composite aluminum frame.

Future Outlook

The aluminum composite panels market is poised for sustained growth, with innovation at its core. In the coming years, expect to see:

- Fire-safe and eco-friendly cores that comply with strict regulations.

- Smart coatings with self-cleaning, anti-bacterial, and anti-static properties.

- Customization trends catering to both high-end architecture and budget-friendly housing.

With its ability to combine function, form, and affordability, ACP is no longer just a panel—it’s the face of modern infrastructure. From the sleek facades of skyscrapers to the billboards along highways, aluminum composite panels market are everywhere. They represent the perfect blend of design and durability, making them indispensable to modern construction and beyond. As the market grows from billions to tens of billions in value, one thing is clear: ACPs are not just building materials; they are the future of architectural expression and industrial design.

Automotive Composites Market Opportunities, Companies, Global Analysis & Forecast 2032

By Sharvari, 2025-09-08

The automotive composites market is expanding rapidly as automakers worldwide push for lighter, more efficient, and sustainable vehicles. Composite materials are revolutionizing the automotive industry by replacing conventional metals with lighter, stronger, and more durable alternatives. With growing emphasis on fuel efficiency, electric vehicle performance, and environmental regulations, the demand for composites in automotive applications is expected to accelerate significantly over the next decade.

Market Size and Forecast

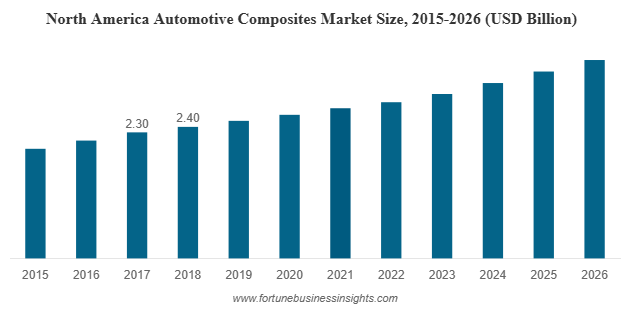

The global automotive composites market size was valued at USD 7.67 billion in 2018 and is anticipated to reach USD 13.5 billion by 2026, growing at a CAGR of 7.56% during the forecast period. North America held the leading position in 2018 with a 31.29% market share, while the U.S. market alone is expected to hit USD 3.22 billion by 2026, fueled by rising light weighting initiatives and the growing demand for improved fuel efficiency.

Asia Pacific currently leads the market, supported by strong automotive production bases in China, India, Japan, and South Korea. Europe follows closely, driven by sustainability regulations and advanced R&D, while North America continues to grow with rising electric vehicle demand and strict fuel-efficiency standards.

List of Top Automotive Composites Market Companies:

- Teijin Ltd.

- Mitsubishi Chemical Corporation

- Toray Industries, Inc.

- SGL Carbon

- RTP Company

- Plasan Carbon Composites

- Owens Corning

- Solvay S.A.

- UFP Technologies, Inc.

- BASF SE

- Other Players

Key Growth Drivers

- Light weighting and Fuel Efficiency

Vehicle manufacturers are under pressure to reduce vehicle weight in order to improve fuel economy and reduce emissions. Composites such as carbon fiber and glass fiber provide high strength-to-weight ratios, enabling automakers to design vehicles that are both lighter and more efficient without compromising performance.

- Growing Electric Vehicle Adoption

Electric vehicles (EVs) demand lightweight materials to extend battery range and improve efficiency. Automotive composites are playing a crucial role in EV design, helping manufacturers reduce overall vehicle weight while maintaining structural integrity and crash safety standards.

- Advanced Material Properties

Automotive composites offer several advantages over traditional materials. They provide dimensional stability, corrosion resistance, low thermal expansion, and design flexibility. These properties make composites suitable for a wide range of applications including body panels, bumpers, interior components, and under-the-hood parts.

- Sustainability and Recycling Potential

Environmental regulations and consumer preferences are pushing the automotive industry toward sustainable solutions. Thermoplastic composites, which are recyclable and energy-efficient to process, are gaining popularity as the industry seeks greener alternatives to traditional thermoset composites.

Market Segmentation

By Fiber Type

- Glass Fiber Composites: Cost-effective, widely used in body panels, bumpers, and structural parts.

- Carbon Fiber Composites: High-performance materials increasingly used in luxury vehicles, sports cars, and electric vehicles.

- Natural Fiber Composites: Emerging as sustainable alternatives, particularly in interior applications.

By Resin Type

- Thermoset Composites: Currently dominate the market due to high durability and cost efficiency.

- Thermoplastic Composites: Gaining momentum due to recyclability and potential for large-scale mass production.

By Application

- Exterior Components: The largest application segment, including bumpers, doors, and body panels, accounting for nearly half of composite use in vehicles.

- Interior Components: Growing adoption in dashboards, seat structures, and trim parts.

- Powertrain and Under-the-Hood Parts: Increasing integration in engine covers, intake manifolds, and other high-performance areas.

Read More : https://www.fortunebusinessinsights.com/automotive-composites-market-102711

Regional Insights

- Asia Pacific: The leading region due to large-scale automotive production, government initiatives, and rising EV manufacturing hubs.

- Europe: Driven by stringent emission regulations, sustainability trends, and strong research and development activities.

- North America: Growth supported by light weighting initiatives, EV adoption, and government policies focused on fuel efficiency.

Competitive Landscape

The automotive composites market is highly competitive with global leaders and regional players investing in innovation and capacity expansion. Prominent companies include Toray Industries, SGL Carbon, Teijin Limited, Mitsubishi Chemical, Hexcel Corporation, Gurit Holding, and Owens Corning. These players focus on developing advanced materials, expanding production facilities, and collaborating with automakers to deliver customized solutions.

Mergers, acquisitions, and partnerships remain key strategies to gain a competitive edge. Companies are also investing in R&D to reduce the cost of carbon fiber composites, making them more accessible for mass-market vehicles.

Key Industry Developments:

- February 2021 – Teijin Ltd. announced installation of glass fiber sheet molding compound line at the company’s automotive composites business named ‘Benet Automotive s.r.o’. The investment was done to meet growing demand for Teijin’s composite parts from European automotive manufacturers.

- January 2021 – SGL Carbon announced investment of USD 4.5 million at its Arkansas site to expand the production of carbon composites for electric vehicles. The company is engaged in the manufacturing of carbon and glass fiber reinforced products for automotive applications. The new capacity addition will be used to meet growing demand for composite battery enclosures of modern e-car chassis.

Future Outlook

The next decade promises strong growth for the automotive composites market. Key trends shaping the industry include:

- Rising Demand for Carbon Fiber: As prices fall and manufacturing processes improve, carbon fiber composites are expected to see greater adoption across mainstream vehicles, not just luxury and sports models.

- Shift Toward Thermoplastic Composites: Their recyclability and lower production costs align with global sustainability goals.

- Integration in Electric Vehicles: As EV adoption surges, composites will become essential in achieving the weight reduction needed to optimize battery range.

- Innovation in Manufacturing: 3D printing and automated processes are likely to accelerate composite adoption in mass production.

The automotive composites market is on a transformative path, fueled by global trends in light weighting, electric mobility, and sustainability. With robust growth forecasts, increasing investment, and technological innovations, composites are set to play a central role in shaping the future of the automotive industry. As automakers continue to prioritize efficiency and performance, the demand for advanced composite materials will only accelerate, making this sector one of the most promising opportunities in the global automotive supply chain.