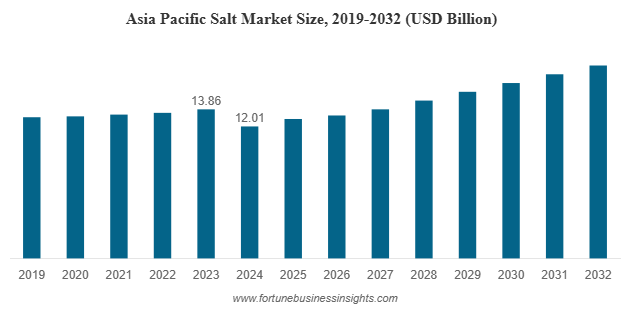

The global salt market was valued at USD 25.98 billion in 2024 and is expected to expand from USD 26.92 billion in 2025 to USD 36.12 billion by 2032, reflecting a CAGR of 4.29% over the forecast period. Asia Pacific led the market in 2024 with a 46.23% share, driven by robust industrial demand and rising consumption in the food sector. In the United States, the salt market is projected to reach USD 4.91 billion by 2032, supported by increasing demand for food-grade salt as well as extensive use in industrial processes and de-icing applications. Key players in the industry include Cargill Salt, Compass Minerals International, Inc., INEOS Enterprises, and American Rock Salt.

Salt market is one of the world’s oldest and most widely used commodities, and it continues to play a vital role in both daily life and industrial applications. Far beyond its use as a kitchen essential, salt market has become indispensable in chemical manufacturing, water treatment, de-icing, oil and gas, and agriculture. The global salt market is experiencing steady growth as industries expand, populations rise, and specialty salts gain consumer appeal.

List Of Key Salt Companies Profiled

- American Rock Salt (U.S.)

- Cargill Salt (U.S.)

- Compass Minerals International, Inc. (U.S.)

- INEOS Enterprises Salt (U.K.)

- K+S Aktiengesellchaft (Germany)

- China National Salt Industry (China)

- Chemetica (Poland)

- US Salt LLC (U.S.)

- Ahir Salt Industries (India)

- GHCL Limited (India)

Key Growth Drivers

- Industrial and Chemical Applications

The largest portion of global salt demand comes from industrial uses, particularly in chemical processing. Salt is essential in the production of chlorine, caustic soda, and soda ash, which serve as building blocks for industries ranging from plastics and paper to glass and textiles. The expansion of chemical manufacturing in emerging economies is a major driver of salt consumption, especially in Asia Pacific.

- De-icing in Cold Regions

In countries with harsh winters, salt is vital for public safety. Rock salt is widely used to melt snow and ice on roads, highways, and airport runways. This consistent demand makes North America and Europe strong regional markets, as municipalities and governments allocate significant budgets to maintain road safety during winter.

- Expanding Role in Water Treatment, Oil & Gas, and Agriculture

Beyond chemicals and de-icing, salt is a key material in water softening and treatment processes, which are critical for both municipal and industrial systems. In the oil and gas sector, salt is used in drilling operations and enhanced oil recovery. Agriculture also depends on salt for soil treatment and livestock feed supplements, ensuring stable demand from rural economies.

- Rising Popularity of Gourmet and Specialty Salts

Consumer preferences are evolving, and specialty salts are capturing growing attention. Solar salt, vacuum pan salt, and artisanal salts such as pink Himalayan or sea salt are being marketed as healthier or more natural alternatives. These products are increasingly popular in gourmet cooking, wellness markets, and premium retail outlets, creating opportunities for higher-margin sales.

Market Segmentation

The salt market can be categorized by type, source, and application.

- By Type: Rock salt dominates the market thanks to its large-scale use in de-icing and industrial processes. Other types include solar salt, vacuum pan salt, and salt in brine, each serving specific applications.

- By Source: Salt is primarily obtained either from brine or through mining. Mines hold the larger market share due to their ability to provide consistent quality and volume. Brine-based production, however, is still widely practiced in coastal areas.

- By Application: Chemical processing remains the largest application segment, followed by de-icing. Other key uses include water treatment, oil and gas, agriculture, and food flavoring.

Read More : https://www.fortunebusinessinsights.com/salt-market-103011

Regional Insights

- Asia Pacific

Asia Pacific leads the global market with a share exceeding 46% in 2024. Countries such as China, India, and Australia are major producers and consumers of salt. Industrial growth, population expansion, and rising demand for processed foods all contribute to this region’s dominance.

- North America

North America is a key market, driven by strong demand for both industrial salt and de-icing salt. The United States alone is expected to reach nearly USD 5 billion in salt market value by 2032. Harsh winters and a robust chemical sector fuel consistent demand.

- Europe

Europe also holds a significant share, particularly due to its chemical industry and extensive use of de-icing salts. However, environmental regulations are more stringent here, requiring companies to adopt sustainable mining and production practices.

- Rest of the World

Latin America and the Middle East & Africa are smaller but growing markets. Rising industrial activity and urbanization are expected to fuel gradual demand increases in these regions over the next decade.

Opportunities for Businesses

The salt market is evolving, and businesses that innovate will be best positioned to capture growth. Producers can focus on:

- Sustainable Production Methods: Eco-friendly mining and brine management will not only meet regulatory requirements but also attract environmentally conscious customers.

- Specialty Salt Branding: Premium salts marketed for their purity, origin, or unique mineral content can help companies differentiate and achieve higher margins.

- Diversification into Industrial Uses: Serving fast-growing industries such as chemicals, oil and gas, and water treatment ensures long-term stability.

- Regional Expansion: Asia Pacific continues to offer strong opportunities due to industrialization and population growth, making it a priority region for expansion.

Key Industry Developments

- December 2024: GHCL, a key salt manufacturer and part of the Dalmia Group, invested USD 40.44 million to create a salt field in Kutch. The Zara Zumara Salt Field will be developed in the Jara area of Kutch.

- May 2023: Cargill’s salt business signed an agreement with CIECH Group, a leading supplier of evaporated salt products. Through this agreement, Cargill extended its range of specialty and evaporated food salt solutions for European food manufacturers.

Opportunities

While growth opportunities are significant, the salt industry also faces notable challenges.

- Environmental Impact: Salt production, especially through large-scale evaporation or mining, can damage ecosystems. The disposal of brine and saline wastewater affects aquatic life and soil quality, raising sustainability concerns.

- Regulatory Hurdles: Stricter environmental and safety regulations are affecting salt producers, particularly those operating underground mines or near coastal ecosystems. Compliance costs can be high and may limit smaller producers.

- Climate and Supply Variability: Weather conditions influence production. For example, solar salt production depends on long dry seasons, making it vulnerable to climate change. Unpredictable weather can affect output and supply chains.

Future Outlook

Salt market may seem like a simple commodity, but its applications stretch across countless industries, making it a cornerstone of global trade and development. With the global market set to grow from USD 25.98 billion in 2024 to USD 36.12 billion by 2032, the industry is poised for steady expansion. Opportunities in specialty salts, sustainable production, and industrial demand highlight salt’s enduring relevance in the modern economy. Companies that align with these trends will be well-positioned to thrive in this growing market.

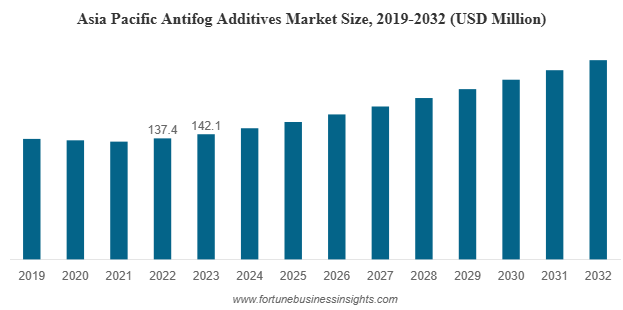

The global antifog additives market was valued at USD 370.0 million in 2023 and is projected to increase from USD 385.9 million in 2024 to USD 564.7 million by 2032, reflecting a compound annual growth rate (CAGR) of 4.8% over the forecast period. In 2023, Asia Pacific led the market, accounting for 38.41% of the global share.

In an age where consumer expectations for freshness, hygiene, and visual appeal are higher than ever, the smallest innovations can make a big impact. One such unsung hero of modern packaging and agriculture is the antifog additive market a chemical compound that prevents the formation of fog on plastic films. While often overlooked, these additives are essential in maintaining product visibility, ensuring food safety, and improving crop yields in controlled agricultural environments.

Types of Antifog Additives Market

Several types of antifog additives market are used based on the application, regulatory requirements, and the nature of the film. The most common types include:

- Glycerol esters

- Polyglycerol esters

- Sorbitan esters

- Ethoxylated sorbitan esters

- Polyoxyethylene esters

Each type has unique properties that influence how effectively it prevents fog, how long it lasts, and whether it’s safe for food contact. For instance, food-grade packaging requires additives that are non-toxic, FDA-approved, and do not migrate into the food over time.

List Of Key Companies Profiled:

- Croda International Plc (U.K.)

- Avient (U.S.)

- LyondellBasell Industries Holdings B.V. (U.S.)

- SABO S.p.A. (Italy)

- Emery Oleochemicals (U.S.)

- Corbion (Netherlands)

- Evonik Industries AG (Germany)

- Polyvel Inc. (U.S.)

- Primex Plastics Corporation (U.S.)

- Palsgaard (Denmark)

What Are Antifog Additives Market?

Antifog additives market are specialized chemicals integrated into plastic films used primarily in food packaging and agricultural applications. Their main function is to prevent water droplets (fog) from forming on the surface of these films. When moisture builds up due to temperature changes or humidity, it often condenses into small droplets that scatter light and obscure visibility. In food packaging, this fog can make the product look unappealing or even unsafe. In agriculture, fog on greenhouse films can reduce light transmission, affecting plant growth.

These additives work by reducing the surface tension of water on the film, causing moisture to spread out in a thin, transparent layer rather than forming droplets. This small chemical adjustment dramatically improves the clarity and usefulness of plastic films.

Why Is the Market Growing?

Several key factors are driving the steady rise in demand for antifog additives market:

- Rising Demand for Packaged Food

With rapid urbanization, growing middle-class populations, and busy lifestyles, the global appetite for packaged and ready-to-eat food continues to rise. Consumers want products that look fresh and clean on the shelf, and foggy packaging can diminish confidence in quality. Antifog additives market ensure the product remains visible, which is essential for maintaining consumer trust.

- Expansion of E-Commerce and Food Delivery

The growth of online grocery shopping and food delivery services has placed additional demands on packaging. Products often move through varying temperature zones during transport, increasing the risk of condensation. To ensure the food arrives looking its best, antifog films are being adopted more widely across cold-chain logistics.

- Growth in Protected Agriculture

Greenhouses and high-tunnel farming are becoming more common worldwide, especially in regions aiming to improve food security. These systems rely heavily on plastic films to control temperature and humidity. Antifog additives market help maintain optimal light transmission by preventing fog on these films, thus promoting better crop growth and yield.

- Changing Consumer Preferences

Today’s consumers are more conscious of hygiene, freshness, and presentation. Especially post-pandemic, clear and clean packaging plays a role in perceived food safety. The visual appeal of a product has a direct impact on purchasing decisions, further elevating the importance of antifog additives market technologies.

Read More : https://www.fortunebusinessinsights.com/antifog-additives-market-107642

Regional Insights

- Asia-Pacific

This region currently dominates the antifog additives market, holding the largest share as of 2023. Rapid industrialization, increasing packaged food consumption, and agricultural advancements in countries like China and India are major contributors. China, in particular, is projected to witness one of the highest growth rates in the coming years.

- North America and Europe

These mature markets are also witnessing healthy growth, driven by innovation in sustainable packaging and strict food safety regulations. The focus here is not just on performance but also on compliance with environmental and health standards.

Key Industry Developments:

- October 2022- Emery Oleochemicals announced a partnership with Sukano. The partnership aims to develop and launch the PET antifogging compound made from natural oils and fat.

- November 2022- SABO S.p.A. announced the acquisition of TAA derivative business of Evonik Industries. The acquisition aims to establish a presence in polymer additive manufacturing.

Challenges and Opportunities

Despite strong growth prospects, the market is not without challenges. Rising environmental concerns around plastic waste and chemical additives are pressuring manufacturers to innovate. There is growing demand for bio-based and biodegradable antifog additives market that offer the same performance without the environmental drawbacks.

Additionally, regulatory frameworks in Europe and North America are tightening around the use of certain chemicals, especially in food-contact materials. Manufacturers that can align with these regulations while maintaining effectiveness will be well-positioned for future success.

The industry also sees potential in developing long-lasting antifog solutions for reusable packaging and exploring antifog applications beyond food and agriculture, such as in automotive, optical films, and medical devices.

Future Outlook

As technology continues to evolve and the demand for smarter, safer packaging grows, antifog additives market will remain a crucial element in the packaging and agricultural industries. The future lies in sustainable innovation creating products that not only perform well but also align with global sustainability goals.

For companies operating in this space, the message is clear: invest in R&D, stay ahead of regulatory trends, and develop eco-friendly alternatives. The fog-free future of packaging and agriculture depends on it.

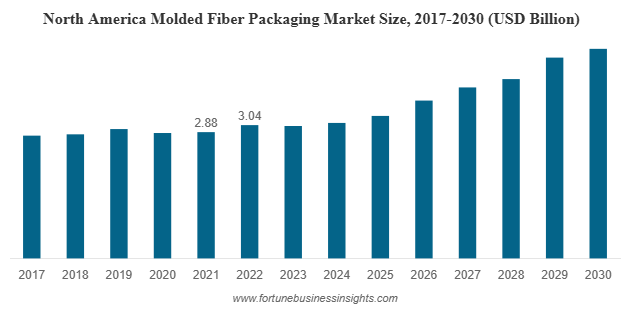

The global molded fiber packaging market was valued at USD 7.68 billion in 2022 and is expected to grow from USD 8.13 billion in 2023 to USD 12.56 billion by 2030, registering a compound annual growth rate (CAGR) of 6.41% over the forecast period. North America led the market in 2022, accounting for a 39.58% share. In particular, the United States is poised for strong growth, with the market projected to reach USD 4.35 billion by 2032. This growth is being fueled by advancements in packaging aesthetics and performance, especially for high-end products such as cosmetics and electronics.

In recent years, the packaging industry has undergone a significant transformation. As the world confronts the challenges of climate change, plastic pollution, and unsustainable manufacturing, businesses and consumers alike are turning toward greener alternatives. One of the most promising and rapidly growing solutions in this space is molded fiber packaging market an innovation that combines sustainability with strength, versatility, and cost-effectiveness.

Once seen as a niche product, molded fiber packaging market has now found its place at the forefront of the global packaging revolution. Backed by strong market growth, increasing regulatory pressure, and rising consumer awareness, this eco-conscious packaging method is no longer an option it’s becoming a necessity.

Market Growth and Projections

- A global push to reduce single-use plastics

- Stricter environmental regulations

- Increasing awareness among consumers about eco-friendly products

- Expanding demand from the food & beverage and e-commerce sectors

In short, molded fiber packaging market is no longer a fringe solution. It is becoming mainstream fast.

List Of Key Companies Profiled:

- Sonoco Product Company (U.S.)

- Robert Cullen Ltd (U.K.)

- Hartmann (Denmark)

- CKF Inc. (Canada)

- FiberCel Packaging LLC (U.S.)

- Huhtamäki Oyj (Finland)

- Green packing Environmental Protection Technology Co., Ltd. (China)

- Dongguan City Luheng Papers Company Ltd. (China)

- Keiding, Inc.(U.S.)

What Is Molded Fiber Packaging?

Molded fiber packaging market, often referred to as molded pulp packaging, is made from recycled paper, cardboard, or natural fibers like sugarcane bagasse and wheat straw. The process involves molding these materials into specific shapes using heat and pressure, resulting in a durable, biodegradable, and compostable product.

Commonly used for egg trays, food containers, electronics cushioning, and industrial packaging, molded fiber packaging offers several advantages over traditional plastic. It is lightweight, shock-absorbent, breathable, and fully recyclable making it a favorite among industries looking to reduce their environmental impact.

Key Industry Drivers

- Environmental Concerns and Regulation

Governments around the world are tightening their grip on plastic pollution. Many countries have introduced bans or restrictions on single-use plastics and are encouraging the use of sustainable alternatives. Molded fiber packaging market fits perfectly into this policy framework, offering a natural solution to one of the world's most pressing problems.

- Shifting Consumer Behavior

Modern consumers are more eco-conscious than ever before. Millennials and Gen Z, in particular, prefer brands that demonstrate environmental responsibility. This trend has pushed companies to redesign packaging strategies to align with sustainable values—and molded fiber offers both form and function without harming the planet.

- Growth in E-commerce

With the rise of online shopping, packaging needs have surged. Consumers expect products to arrive safely, but without excessive plastic. Molded fiber packaging market offers excellent shock resistance, making it ideal for protecting goods during transit, while still being environmentally friendly.

- Rising Demand from Food & Beverage Sector

From trays and drink carriers to takeaway boxes and clamshell containers, the food and beverage industry is one of the largest users of molded fiber packaging. Its breathability, compostability, and ability to handle moisture make it ideal for packaging perishable goods.

Read More : https://www.fortunebusinessinsights.com/molded-fiber-packaging-market-104894

Market Segmentation and Product Insights

The molded fiber packaging market is segmented based on pulp type, product type, and end-use applications.

- By pulp type, transfer molded fiber leads the pack. This method is commonly used to manufacture egg cartons and trays, due to its balance of cost and strength.

- By product, trays dominate the market. These are followed by clamshells, bowls, cartons, inserts, and protective packaging for electronics.

- By application, the food and beverage segment remains the largest consumer of molded fiber packaging, followed by electronics, healthcare, automotive, and industrial goods.

Regional Market Trends

The adoption of molded fiber packaging market varies by region, with North America currently holding the largest market share. The U.S. and Canada have embraced sustainable packaging solutions rapidly due to strong environmental awareness and strict regulations.

Asia-Pacific, on the other hand, is witnessing the fastest growth. Countries like China and India are seeing massive increases in demand due to expanding e-commerce markets, rapid urbanization, and rising environmental consciousness.

Europe also continues to see strong adoption, driven by policies like the European Green Deal and a cultural shift toward sustainability.

Key Industry Developments:

- September 2023 - Guamolsa, a part of Molpack Corporation, one of Latin America's leading providers of molded fiber packaging, partnered with HP to digitize and transform the industrial production of molded fiber products. Molpack is making significant progress in reducing carbon emissions and replacing single-use plastics with more sustainable packaging solutions through this revolutionary collaboration.

- June 2022 - Huhtamaki announced its plans to expand its molded fiber product manufacturing unit in Indiana, U.S., as a part of its investment in Fiber Solutions. The USD 100 million investment would help the company to better serve new and existing customers in North America. This financial commitment supported the development and production of a broad range of fully recyclable, sustainable, and compostable, fiber-based packaging solutions, all manufactured from 100% recycled North American raw materials.

Challenges to Watch

Despite its advantages, the molded fiber packaging industry isn’t without challenges:

- Raw Material Fluctuations: Supply chain issues for recycled paper or agricultural fibers can impact production consistency.

- Cost of Transition: Initial investments in molds, equipment, and production lines can be high especially for companies shifting from plastic.

- Design Limitations: While improving, molded fiber still has some design constraints compared to plastic, especially for high-end or luxury packaging.

However, ongoing R&D and increasing consumer demand are helping overcome these hurdles.

Future Outlook

The future of molded fiber packaging market looks promising. With technology improving, design capabilities expanding, and sustainability taking center stage in business strategies, this market is well-positioned for continued growth.

Companies that embrace molded fiber today are not only meeting current environmental standards they’re building future-ready brands. As the global community becomes more conscious of its ecological footprint, sustainable packaging won’t just be an option it will be an expectation.

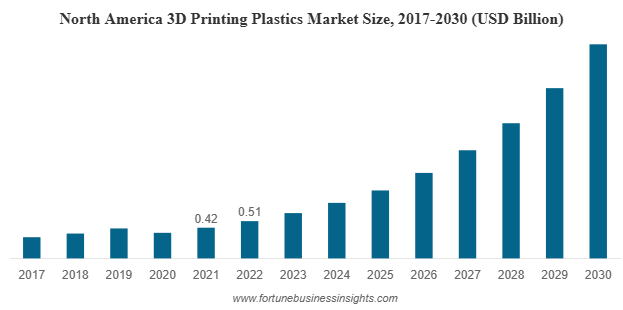

The global 3D printing plastics market was valued at USD 1.26 billion in 2022 and is expected to expand from USD 1.55 billion in 2023 to USD 7.46 billion by 2030, registering a strong CAGR of 25.1% over the forecast period. North America led the market in 2022 with a 40.48% share, while the U.S. market alone is anticipated to reach USD 2.71 billion by 2030, driven by rapid advancements in additive manufacturing and prototyping technologies.

Additive manufacturing, better known as 3D printing plastics market, has moved beyond its early days as a niche prototyping tool. Today, it is shaping how industries design, test, and manufacture products on demand. Among the wide range of materials used in this technology, plastics hold a crucial position. From aerospace to healthcare, 3D printing plastics market are transforming the way companies innovate and deliver solutions.

In recent years, the 3D printing plastics market has been experiencing remarkable growth. What was once valued at just over a billion dollars in 2022 is forecasted to multiply several times over by the end of this decade. With a compound annual growth rate exceeding 25.1%, the industry is expected to cross seven billion dollars by 2030. Such rapid expansion is being driven by material innovation, advances in printing technologies, and rising adoption across diverse sectors.

List Of Key Companies Profiled In 3d Printing Plastics Market:

- HP Development Company, L.P (U.S.)

- Evonik Industries AG. (Germany)

- Stratasys (U.S.)

- 3D Systems, Inc. (U.S.)

- Arkema S.A.(France)

- Henkel Corporation (Germany)

- EOS GmbH Electro Optical Systems (Germany)

- Solvay S.A.(Belgium)

- Huntsman Corporation (U.S.)

- SABIC (Saudi Arabia)

Why the Market Is Growing So Fast

- Innovation in Materials

One of the biggest factors pushing growth is the introduction of new plastic formulations designed specifically for 3D printing plastics market. Polylactic Acid (PLA), a biodegradable polymer derived from renewable resources such as corn starch, is gaining strong traction. It is not only eco-friendly but also easy to print, making it a preferred choice for beginners and professionals alike. Alongside PLA, other plastics such as ABS, polyamide, and polycarbonate are finding increasing demand due to their strength, flexibility, and durability.

- Technological Advancements

3D printing itself has seen major improvements in speed, resolution, and the ability to handle multiple materials and colors simultaneously. These advancements allow for the creation of complex geometries and high-performance components that were once impossible or too costly to manufacture using traditional methods. Better printers also mean faster turnaround times, which adds to the appeal of using plastics for both prototyping and end-use applications.

- Expanding End-User Applications

Industries are embracing 3D printing plastics market for very different reasons.

- Aerospace and defense companies are drawn to lightweight plastic components that reduce fuel consumption and overall costs.

- Healthcare is adopting these materials for customized implants, dental models, and patient-specific medical devices.

- Automotive manufacturers benefit from the ability to produce rapid prototypes and lightweight parts.

- Electronics and consumer goods industries use plastics for everything from functional components to creative product designs.

This diversity of applications ensures that demand is not concentrated in one sector but spread across multiple industries.

- Regional Expansion

North America currently leads the global market thanks to early adoption, technological expertise, and strong demand from aerospace and healthcare industries. However, Asia Pacific is emerging as the fastest-growing region. Countries such as China, India, Japan, and South Korea are investing heavily in additive manufacturing, supported by strong automotive, electronics, and consumer goods industries. Europe, too, continues to play a key role, driven by exports and advanced manufacturing systems.

Breaking Down the Market

The 3D printing plastics market can be segmented in several ways:

- By Material Type: PLA is the leading segment due to its eco-friendly nature and ease of use. ABS, polyamide, and polycarbonate also hold significant shares.

- By End-Use Industry: Aerospace and defense currently dominate the market, but healthcare is catching up quickly. Automotive, electronics, and consumer goods contribute steadily to overall demand.

- By Region: North America is the largest market, Asia Pacific is the fastest growing, and Europe continues to maintain a strong presence. Emerging markets in Latin America and the Middle East are also expected to expand gradually.

Read More : https://www.fortunebusinessinsights.com/3d-printing-plastics-market-108834

Opportunities for Businesses

For companies operating in this space, the growth trajectory offers immense opportunities. A few strategies stand out:

- Invest in R&D: There is room for breakthrough developments in material science. Plastics that combine multiple strengths—durability, lightness, sustainability, and affordability—will redefine the market.

- Focus on Compliance: Firms targeting aerospace or healthcare must be prepared for rigorous testing and certification processes. Building strong quality assurance systems will be key to long-term success.

- Strengthen Supply Chains: With global supply chains facing instability, localizing production and building partnerships for raw materials can provide resilience and cost advantages.

- Leverage Customization: 3D printing allows companies to offer tailor-made products with shorter lead times. Businesses that can capitalize on this demand for customization will stay ahead of the competition.

Key Industry Developments:

- March 2022: Evonik developed VESTAKEEP iC4800 3DF, a new osteoconductive PEEK filament that improves fusion between bone and implants. By developing this new filament, the company will further expand its portfolio of 3D-printable biomaterials for medical technology.

- March 2022: Evonik and Asiga, an Australian 3D printer manufacturer collaborated in photopolymer-based 3D printing. The companies aim to elevate the 3D printing industrial manufacturing at large-scale by increasing their competence in photo-curing technologies.

Challenges the Industry Faces

While the growth story is strong, the industry is not without its hurdles.

- Material Limitations: Developing plastics that meet all requirements—strength, heat resistance, flexibility, and biocompatibility—remains a challenge. Aerospace and medical industries, in particular, demand materials that can perform under extreme conditions.

- Certification and Regulation: Getting approval for 3D printed parts, especially in sensitive sectors such as healthcare and aerospace, involves stringent safety and quality checks. These add to costs and time before new materials or products can hit the market.

- Supply Chain Risks: Global disruptions in recent years have highlighted the vulnerability of raw material supply chains. Ensuring a steady and cost-effective supply of 3D printing plastics remains a critical concern.

Outlook

The future of the 3D printing plastics market looks bright. With projections crossing seven billion dollars by 2030 and applications expanding across industries, the sector is set for a dynamic decade. Growth in Asia Pacific, steady leadership in North America, and innovations across Europe will shape the global landscape.

Healthcare and aerospace are expected to deliver some of the most groundbreaking use-cases, especially as material limitations are overcome and regulatory hurdles are navigated. At the same time, eco-friendly materials such as PLA will become increasingly important as industries prioritize sustainability.

In short, 3D printing plastics market are not just materials for tomorrow they are already redefining how we create, customize, and consume products today.

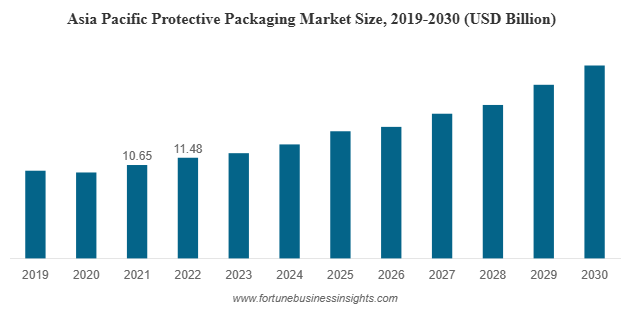

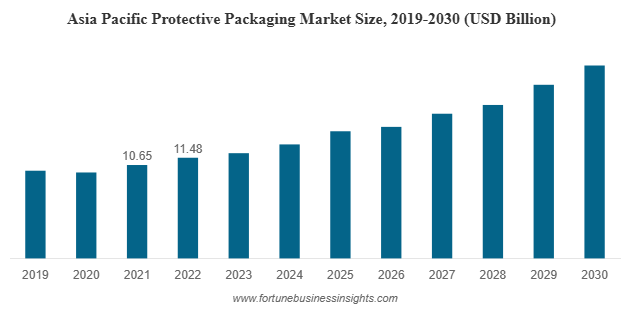

The global protective packaging market was valued at USD 36.31 billion in 2022 and is expected to grow from USD 38.52 billion in 2023 to USD 61.44 billion by 2030, reflecting a compound annual growth rate (CAGR) of 6.90% over the forecast period. Asia Pacific led the global market in 2022, accounting for 31.62% of the total share. In addition, the U.S. protective packaging market is anticipated to experience substantial growth, projected to reach approximately USD 14.80 billion by 2032, driven by the rising demand for protective packaging in international trade.

In today’s rapidly evolving global economy, the need for effective and reliable packaging has never been more critical. Protective packaging plays a vital role in ensuring that products reach consumers in perfect condition, whether they are delicate electronics, perishable foods, or pharmaceuticals. As e-commerce, international trade, and sustainability awareness grow, the protective packaging market has seen significant expansion and innovation. This article explores the key drivers behind this growth, the market’s current state, challenges it faces, and future opportunities.

List Of Key Companies Profiled In Protective Packaging Market:

- Smurfit Kappa (Ireland)

- Westrock Company (U.S.)

- Sealed Air Corporation (U.S.)

- Sonoco Product Company (U.S.)

- Huhtamaki (Finland)

- DS Smith PLC (U.K.)

- Pregis LLC (U.S.)

- Pro-Pac Packaging Limited (Australia)

- Storopack (Germany)

- Intertape Polymer Group (U.S.)

Market Growth and Size

This growth is not limited to a single geography. While regions like North America and Europe continue to have strong demand due to their mature retail and industrial bases, the Asia Pacific region is rapidly emerging as the largest market. Factors such as increasing industrial production, expanding e-commerce markets, and rising consumer spending are propelling demand in countries like China, India, and Southeast Asian nations.

Understanding Protective Packaging

Protective packaging market refers to materials and solutions designed to shield products from damage during storage, handling, and transportation. Unlike simple packaging that focuses on containment, protective packaging emphasizes safeguarding the product against shocks, vibrations, temperature variations, moisture, and contamination.

Some common types of protective packaging include:

- Cushioning materials such as foam, bubble wrap, and air pillows.

- Void fillers that prevent movement within a package.

- Wrapping films that protect surfaces.

- Insulation materials to maintain temperature-sensitive goods.

- Rigid inserts and containers for heavy or fragile items.

These protective solutions are widely used across industries such as consumer electronics, food and beverage, pharmaceuticals, cosmetics, and automotive parts.

Key Drivers of Market Expansion

Several factors are fueling the growth of the protective packaging market, making it an exciting sector for businesses, marketers, and content creators alike:

1. E-commerce Boom

The exponential rise of online shopping is arguably the most significant catalyst behind the protective packaging surge. With more consumers ordering products online, the need to secure these items during transit has never been higher. Packages must withstand longer shipping distances and more handling points, creating demand for advanced protective solutions.

2. Increasing Consumer Expectations

Modern consumers expect their products to arrive undamaged and in pristine condition. This expectation has pushed brands and retailers to invest in superior packaging solutions. Damaged goods not only lead to financial loss but also harm customer trust and brand reputation.

3. Sustainability and Eco-Friendly Packaging

The environmental impact of packaging waste, particularly plastics, has come under intense scrutiny worldwide. Governments, consumers, and businesses alike are demanding sustainable alternatives. As a result, the protective packaging industry is innovating with biodegradable materials, recyclable paper-based solutions, and reusable packaging systems.

4. Technological Innovations

Protective packaging is no longer just about physical protection; it’s evolving with technology. Smart packaging that incorporates sensors to monitor temperature, humidity, or shocks during transit is becoming increasingly prevalent, especially in pharmaceuticals and food logistics.

Read More : https://www.fortunebusinessinsights.com/protective-packaging-market-107319

Market Segmentation Insights

Breaking down the market helps businesses and content creators understand where the biggest opportunities lie:

- Material Types: Plastic materials dominate due to their cushioning properties and cost-effectiveness, but paper and paperboard materials are gaining traction because of sustainability trends.

- Product Types: Flexible packaging, including wraps and films, continues to grow thanks to its versatility and lightweight properties. Rigid packaging remains essential for heavy or extremely fragile items.

- Functions: Cushioning remains the most crucial function, followed by void filling, insulation, and bracing.

- End-Use Industries: Food and beverage represent the largest application segment, given the need for freshness and contamination protection. E-commerce, pharmaceuticals, and consumer electronics are also key sectors.

Opportunities

The future of the protective packaging market is bright, with several promising opportunities on the horizon:

- Sustainability Leadership: Companies that invest in green packaging materials and circular economy models can differentiate themselves and meet increasing regulatory and consumer demands.

- Customization and Personalization: With advances in manufacturing technology, tailored protective packaging solutions can better serve unique product needs, enhancing brand value.

- Smart Packaging Growth: Integration of IoT and sensor technologies will improve supply chain visibility and product safety, especially for sensitive items like pharmaceuticals.

- Emerging Markets: Rapid urbanization and digital adoption in emerging economies will continue to drive demand for protective packaging solutions.

Key Industry Developments:

- August 2023 – Ranpack launched Wrap’n Go converter for protective honeycomb paper. The company brought its Geami Wrap’n Go converter, which turns kraft paper into protective, pack-in-store packaging for fragile items, to the North American market, providing an alternate option to the plastic solution.

- February 2023 – The circular materials company Cruz Foam announced the launch of a revolutionary new product family of environmentally protective packaging, introducing highly efficient solutions that meet the specific needs of customers in transporting sensitive and temperature-sensitive goods to consumers and businesses.

Challenges in Protective Packaging

Despite the optimistic growth outlook, the industry faces several challenges:

- Regulatory Pressure: Increased regulations around plastic use and waste management require manufacturers to adapt quickly to new standards.

- Raw Material Price Volatility: Fluctuating prices of plastics, paper, and other raw materials can squeeze margins.

- Supply Chain Disruptions: Global events and logistics bottlenecks can impact material availability and delivery timelines.

Addressing these challenges demands innovation, strategic sourcing, and strong partnerships across the supply chain.

Future Outlook

The protective packaging market is a dynamic and rapidly growing sector critical to modern commerce. Driven by e-commerce growth, rising consumer expectations, and sustainability imperatives, protective packaging solutions are more important than ever. Businesses that understand these trends and innovate accordingly are well-positioned to thrive.

For anyone interested in free content submissions or marketing strategies, protective packaging presents an excellent topic to explore. Writing insightful, data-backed articles about this booming market can help attract attention, build authority, and rank highly in search engines.

U.S. Antimicrobial Plastics Market Global Trend, Size, Share, Growth & Forecast 2030

By Sharvari, 2025-09-16

The U.S. antimicrobial plastics market size was valued at USD 6.68 billion in 2022 and is projected to grow at a CAGR of 7.5% during the forecast period.

In today’s fast-paced, hygiene-conscious world, industries are evolving to prioritize cleanliness, safety, and sustainability like never before. One standout example of this evolution is the rapid growth of the U.S. antimicrobial plastics market. As concerns over infection control, food safety, and environmental impact continue to rise, antimicrobial plastics have carved out a vital space across industries ranging from healthcare to consumer goods.

List Of Key Companies Profiled:

- BASF SE (Germany)

- LyondellBasell Industries Holdings B.V. (Netherlands)

- DuPont de Nemours, Inc (U.S.)

- INEOS Group Limited (U.K.)

- Avient Corporation (U.S.)

- SABIC (Saudi Arabia)

- Palram Industries Ltd. (Israel)

- RTP Company (U.S.)

- Microban International, Ltd. (U.S.)

- King Plastic Corporation (U.S.)

Market Size and Growth Trends

The U.S. antimicrobial plastics market is experiencing robust growth and shows no signs of slowing down. Fueled by increasing demand in healthcare, packaging, and automotive industries, the market has seen a steady upward trajectory in both volume and value.

Over the next few years, industry experts forecast a strong compound annual growth rate (CAGR), supported by ongoing innovations, rising public health awareness, and stringent hygiene regulations. With the global spotlight on health post-pandemic, antimicrobial materials are no longer a luxury—they are a necessity.

What Are Antimicrobial Plastics?

U.S. antimicrobial plastics market are plastic materials that have been infused with active agents that inhibit the growth of microorganisms such as bacteria, mold, mildew, and even some viruses. These agents can be either inorganic, like silver or copper, or organic, and they help keep surfaces cleaner for longer periods, reducing the risk of contamination and the spread of infections.

These plastics are particularly important in environments where hygiene is non-negotiable—such as hospitals, food processing facilities, and high-touch consumer products.

Why the Market Is Growing So Fast

There are several key factors contributing to the rising demand for antimicrobial plastics in the United States:

- Healthcare Sector Demand

The medical and healthcare industry remains the largest consumer of antimicrobial plastics. With a growing number of hospitals, clinics, and diagnostic labs, the demand for sterile and contamination-resistant materials has never been higher. From surgical instruments to IV components and bed rails, antimicrobial plastics are critical in maintaining a sterile environment and minimizing hospital-acquired infections.

- Packaging and Food Safety

The food industry is under constant pressure to ensure safety and longevity of its products. Antimicrobial plastics are now widely used in food packaging to extend shelf life and reduce spoilage. Consumers are increasingly seeking packaging that not only protects their food but also ensures hygienic handling from production to table.

- Rise in Consumer Awareness

Post-pandemic, awareness about germ transmission through surfaces has skyrocketed. Consumers are now actively seeking products that offer antimicrobial properties—from smartphone cases and kitchen countertops to gym equipment and children’s toys. This behavioral shift is directly influencing manufacturers to integrate antimicrobial technology into everyday items.

- Automotive and Building Applications

Car interiors, door handles, seat belts, and HVAC systems are all high-touch points that can benefit from antimicrobial treatment. Similarly, the construction industry is adopting antimicrobial plastics in areas like wall panels, handrails, and bathroom fittings to meet hygiene standards, especially in commercial buildings and public facilities.

Dominance of Inorganic Additives

Inorganic antimicrobial agents, particularly silver-based compounds, currently dominate the market due to their long-lasting effectiveness and stability under various conditions. These additives are known to be highly effective against a broad spectrum of microorganisms and can be integrated into a wide range of polymer types.

Read More : https://www.fortunebusinessinsights.com/u-s-antimicrobial-plastics-market-108257

Market Segmentation Insights

The U.S. antimicrobial plastics market is segmented by:

- Type of Plastic: Commodity plastics like polyethylene and polypropylene are widely used due to their cost-effectiveness and versatility.

- Additives Used: Inorganic agents like silver and copper dominate, while research continues on safer, more eco-friendly organic alternatives.

- End-Use Industries: The major consumers include medical & healthcare, packaging, automotive, consumer goods, and building & construction.

Each segment has its own unique demands and regulatory frameworks, making innovation and adaptability key to long-term success.

What’s Next for the U.S. Antimicrobial Plastics Market?

Looking ahead, the market is poised for continued expansion driven by:

- Biodegradable and Sustainable Options: There’s rising demand for antimicrobial plastics that are also biodegradable or made from recycled materials.

- Smart Antimicrobial Surfaces: Innovations may soon bring self-cleaning, UV-reactive, or even sensor-embedded antimicrobial plastics into the mainstream.

- Consumer-Led Design: As awareness grows, consumers will increasingly push for safer, germ-resistant materials in everything from home appliances to school supplies.

- Government Regulations: Policy changes and stricter hygiene protocols will further stimulate adoption in critical sectors like transportation, healthcare, and food processing.

Key Industry Developments:

- November 2021 – Sunbeam Products, Inc. and Microban International have announced a strategic partnership to develop a premium-quality product portfolio under the Calphalon brand to produce knife handles by innovating the Microban silver shield platform, which features product protection against microbes.

- May 2021 – Avient Corporation has launched a new antimicrobial technology by enlarging its product portfolio to protect against bacterial microbes. The new technology GLS TPE is expected to extend the organization's market presence into more extensive applications for gadgets, cars, and air conditioning seals.

Challenges Facing the Market

Despite the promising growth, the U.S. antimicrobial plastics market does face a few challenges:

- Cost of Raw Materials: Antimicrobial additives can significantly increase production costs, especially for low-margin industries like food packaging.

- Environmental Concerns: With growing awareness around plastic pollution, companies must balance antimicrobial performance with recyclability and sustainability.

- Regulatory Compliance: Manufacturers need to navigate complex regulations regarding the use of biocidal agents, labeling, and safety certifications.

- Performance Durability: Ensuring that antimicrobial properties last for the full product lifecycle is crucial. Degradation over time can result in reduced effectiveness and consumer dissatisfaction.

Outlook

The U.S. antimicrobial plastics market is not just a trend—it’s a pivotal part of the future of materials science. As industries and consumers alike place more value on cleanliness, safety, and sustainability, antimicrobial plastics will play a central role in shaping safer environments.

For businesses, now is the time to invest in antimicrobial innovation, adapt to changing consumer expectations, and build products that deliver not just performance, but peace of mind.

Whether you’re a manufacturer, distributor, or simply an informed consumer, understanding this market opens up a world of opportunity—and it’s only just beginning.

Saudi Arabia Refractories Market Size, Share, Companies & Future Outlook 2029

By Sharvari, 2025-09-16

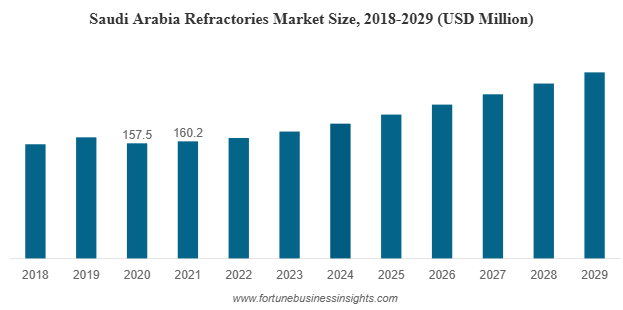

The Saudi Arabia refractories market was valued at USD 160.2 million in 2021 and is expected to expand from USD 164.8 million in 2022 to USD 254.6 million by 2029, registering a CAGR of 6.4% during the forecast period. The COVID-19 pandemic had a significant impact on the industry, with demand falling short of expectations across the country. In fact, the market recorded a 4.9% decline in 2020 compared to 2019, highlighting the challenges faced during the crisis.

Market Size and Forecast

The Saudi Arabia Refractories Market is undergoing rapid transformation, driven by industrial expansion, government initiatives, and rising demand from core industries such as steel, cement, glass, and non-ferrous metals. As the Kingdom works toward its Vision 2030 objectives, refractories are emerging as a crucial component in supporting industrial infrastructure, manufacturing, and construction.

This article explores the size of the market, major growth drivers, challenges, and the future outlook, offering insights for businesses, investors, and stakeholders aiming to understand this fast-growing industry.

List Of Key Companies Profiled:

- Saudi Refractory Industries (Dammam)

- AOSCO Refractory (Dammam)

- FSN Company (Dammam)

- Arabian Refractories Factory Company (Dammam)

- Q & E Company Ltd. (Al Jubail)

- Alfran (Amman)

- Thermal Insulation UAE (Sharjah)

Importance of Saudi Arabia Refractories Market

Saudi Arabia Refractories Market are specialized, heat-resistant materials used to line furnaces, kilns, reactors, and other equipment that must endure extreme heat, chemical corrosion, and mechanical wear. They are indispensable in industries such as iron and steel, cement, glass, and petrochemicals. Without quality refractory linings, these industries cannot achieve efficiency, safety, or cost-effectiveness in their operations.

In Saudi Arabia, where large-scale industrialization is central to economic diversification, the demand for high-performance refractories is expanding at a steady pace.

Key Segments of the Market

By Form

- Bricks and shaped refractories dominate the market, thanks to their extensive use in furnaces, kilns, and metal processing units.

- Monolithic and unshaped refractories are gaining popularity due to their versatility in lining irregular shapes and complex industrial equipment.

By Product Type

- Clay refractories, including fireclay and other affordable compositions, lead in terms of volume because of their cost-effectiveness and wide availability.

- Non-clay refractories, such as high alumina, silica, magnesia, and specialty compositions, are increasingly in demand for high-temperature and high-stress applications.

By End-Use Industry

- Iron and steel remains the largest consumer segment, as steelmaking processes rely heavily on refractory linings for converters, blast furnaces, and ladles.

- Cement and glass industries also contribute significantly, with glass furnaces requiring advanced materials to withstand continuous high-temperature melting operations.

- Non-ferrous metals and petrochemicals represent growing opportunities, especially as Saudi Arabia strengthens its energy and industrial base.

Read More : https://www.fortunebusinessinsights.com/saudi-arabia-refractories-market-106924

Growth Drivers

- Vision 2030 and Industrial Diversification

Saudi Arabia’s Vision 2030 blueprint focuses on diversifying the economy beyond oil. The plan emphasizes boosting steel production, automotive manufacturing, construction, and renewable energy—all sectors that rely heavily on refractory applications. - Megaprojects and Infrastructure Development

Projects like NEOM City, the Red Sea Project, and new industrial hubs are fueling demand for steel, cement, and glass. This directly translates into higher consumption of refractories for production units and industrial infrastructure. - Rising Steel Production

Saudi Arabia is investing heavily in steel plants to meet domestic and export demand. Since steelmaking is one of the most refractory-intensive processes, this sector will remain the backbone of market growth. - Technological Advancements

Innovations in refractory materials—such as non-clay compositions with superior thermal, mechanical, and chemical resistance—are gaining traction. These advanced materials improve efficiency, reduce downtime, and comply with stricter environmental standards.

Challenges Facing the Market

- Raw Material Dependence: Saudi Arabia imports a significant portion of refractory raw materials, making the market vulnerable to global supply chain disruptions and fluctuating costs.

- High Energy and Production Costs: Refractory manufacturing is energy-intensive, and rising energy prices can impact margins for producers.

- Environmental Regulations: As the Kingdom advances its sustainability agenda, manufacturers must adopt eco-friendly production processes, which require additional investment.

- Skilled Workforce Needs: Operating advanced refractory technologies and installations requires technical expertise, which remains a challenge in certain regions.

Future Outlook

The future of the Saudi Arabia refractories market looks highly promising. Between 2022 and 2029, steady growth is expected across all major end-use industries. Steel will continue to dominate demand, while the glass and cement industries are set to expand further due to construction megaprojects.

Advanced non-clay refractories are anticipated to capture greater market share, supported by industries that require superior performance under corrosive and high-temperature conditions. Moreover, local manufacturing capabilities are likely to expand as the Kingdom reduces dependency on imports and promotes domestic production facilities.

The Saudi Arabia Refractories Market is on a growth trajectory, fueled by industrialization, megaprojects, and rising steel and cement production. While challenges such as raw material dependency and environmental regulations persist, the outlook remains highly positive through 2029.

For businesses, this market presents opportunities to innovate, localize production, and align with Vision 2030’s goals. For investors and stakeholders, refractories are not just heat-resistant materials they are the backbone of Saudi Arabia’s industrial transformation.

The global protective packaging market was valued at USD 36.31 billion in 2022 and is expected to expand from USD 38.52 billion in 2023 to USD 61.44 billion by 2030, reflecting a compound annual growth rate (CAGR) of 6.90% during the forecast period. In 2022, the Asia Pacific region led the market, accounting for 31.62% of the global share. Meanwhile, the U.S. protective packaging market is also anticipated to witness strong growth, with projections estimating it will reach USD 14.80 billion by 2032. This growth is largely driven by the rising demand for protective packaging in international trade activities.

In an era dominated by online shopping, global logistics, and heightened consumer expectations, protective packaging has emerged as one of the most critical components in product delivery. From fragile electronics to perishable foods, protective packaging ensures that goods reach customers safely and in top condition.

List Of Key Companies Profiled In Protective Packaging Market:

- Smurfit Kappa (Ireland)

- Westrock Company (U.S.)

- Sealed Air Corporation (U.S.)

- Sonoco Product Company (U.S.)

- Huhtamaki (Finland)

- DS Smith PLC (U.K.)

- Pregis LLC (U.S.)

- Pro-Pac Packaging Limited (Australia)

- Storopack (Germany)

- Intertape Polymer Group (U.S.)

Growth Drivers

- The E-Commerce Explosion

E-commerce has reshaped the way we shop. With products shipped directly to doorsteps, the demand for protective packaging has surged. Customers now expect their orders to arrive in pristine condition—whether it's a smartphone, skincare product, or a frozen meal. Packaging that fails to protect leads to returns, dissatisfaction, and brand damage. As online shopping becomes the default, businesses are investing heavily in durable, lightweight, and cost-effective packaging solutions.

- Expanding Applications Across Industries

Protective packaging market is no longer confined to just electronics or fragile goods. It’s now an essential requirement in industries such as:

- Food and Beverage: Ensures freshness and prevents contamination during transport.

- Pharmaceuticals: Maintains the integrity and safety of sensitive medical products.

- Automotive and Electronics: Shields against mechanical damage, moisture, and dust.

- Cosmetics and Personal Care: Protects aesthetic packaging and preserves shelf appeal.

The more industries that rely on long-distance shipping, the more critical packaging becomes to business operations.

- Rising Demand in Developing Regions

Asia-Pacific currently holds the largest market share and continues to be the fastest-growing region. Countries like China and India are experiencing massive e-commerce growth, expanding manufacturing bases, and urbanization—all of which contribute to increased demand for protective packaging. Additionally, Latin America and the Middle East & Africa are witnessing steady growth as global trade increases and consumer purchasing power rises.

Trends Shaping the Market

- Sustainable Packaging Solutions

Plastic continues to dominate the market due to its low cost, durability, and efficiency. However, growing environmental concerns are pushing both companies and consumers toward greener alternatives. There is a strong trend toward the use of recyclable materials, biodegradable films, and molded pulp packaging. Businesses are under pressure to strike a balance between functionality and sustainability—without sacrificing protection.

- Growth in Flexible and Wrapping Packaging

Among the various product types, flexible packaging solutions are seeing the fastest growth. These include bubble wrap, paper wraps, and foam-in-place solutions, which offer excellent cushioning while being adaptable to various product sizes and shapes. Wrapping packaging is especially popular for its lightweight nature, ease of customization, and cost efficiency. These solutions are essential for reducing shipping weight and protecting irregularly shaped items.

- Advanced Protective Functions

Today’s protective packaging does more than just prevent breakage. Key functions include:

- Void Fill: Prevents products from moving during transit.

- Cushioning: Absorbs shock and vibration.

- Insulation: Maintains product temperature (especially in food and pharma sectors).

- Blocking and Bracing: Secures products in place inside the container.

These multifunctional aspects of protective packaging are becoming essential for meeting increasingly complex logistical requirements.

Read More : https://www.fortunebusinessinsights.com/protective-packaging-market-107319

What Businesses Should Focus On

For companies that manufacture, ship, or sell physical products, the rise of the protective packaging market presents both a challenge and an opportunity. Here are a few key takeaways:

- Invest in R&D: Stay ahead by developing or using sustainable and advanced packaging materials.

- Optimize Packaging Design: Go beyond protection—design for space efficiency, brand identity, and user experience.

- Partner Strategically: Work with reliable suppliers who offer innovative, compliant, and cost-effective packaging solutions.

- Educate Consumers: Highlight your sustainable packaging efforts as part of your brand story. Today’s consumers care.

Key Industry Developments:

- August 2023 – Ranpack launched Wrap’n Go converter for protective honeycomb paper. The company brought its Geami Wrap’n Go converter, which turns kraft paper into protective, pack-in-store packaging for fragile items, to the North American market, providing an alternate option to the plastic solution.

- February 2023 – The circular materials company Cruz Foam announced the launch of a revolutionary new product family of environmentally protective packaging, introducing highly efficient solutions that meet the specific needs of customers in transporting sensitive and temperature-sensitive goods to consumers and businesses.

Challenges and Opportunities

- Regulation and Compliance

Governments worldwide are enacting stricter regulations on single-use plastics and non-recyclable materials. As sustainability becomes non-negotiable, packaging manufacturers are investing in R&D to develop eco-friendly solutions that comply with international standards. This opens doors for innovation and differentiation in the market.

- Supply Chain Resilience

The COVID-19 pandemic exposed the fragility of global supply chains. Delays in raw materials and disruptions in manufacturing highlighted the need for more robust and localized packaging solutions. Companies are now diversifying their supplier base and investing in supply chain resilience to avoid future setbacks.

- Technological Innovation

Technological advancements such as smart packaging (which can monitor temperature and tampering), automation in packaging lines, and the integration of AI for packaging design are becoming game-changers. These innovations not only improve efficiency but also reduce waste and costs in the long run.

Outlook

Protective packaging market is no longer just a backend logistics concern—it’s a strategic asset. With the market set to nearly double over the next decade, businesses that prioritize innovation, sustainability, and adaptability in their packaging strategies will be better positioned to thrive in an increasingly competitive landscape.

From cushioning to compliance, the future of protective packaging is dynamic, and it’s reshaping how products are shipped, received, and experienced around the world.