The non-stick cookware market is heating up as more households and chefs prefer stylish, durable, and easy-to-clean cooking solutions. According to Fortune Business Insights , the non-stick cookware market size was valued at USD 7.33 billion in 2022 and is projected to reach USD 11.73 billion by 2030 , growing at a healthy CAGR of 6.4% . Asia Pacific dominated the non-stick cookware market with a market share of 31.74% in 2024.

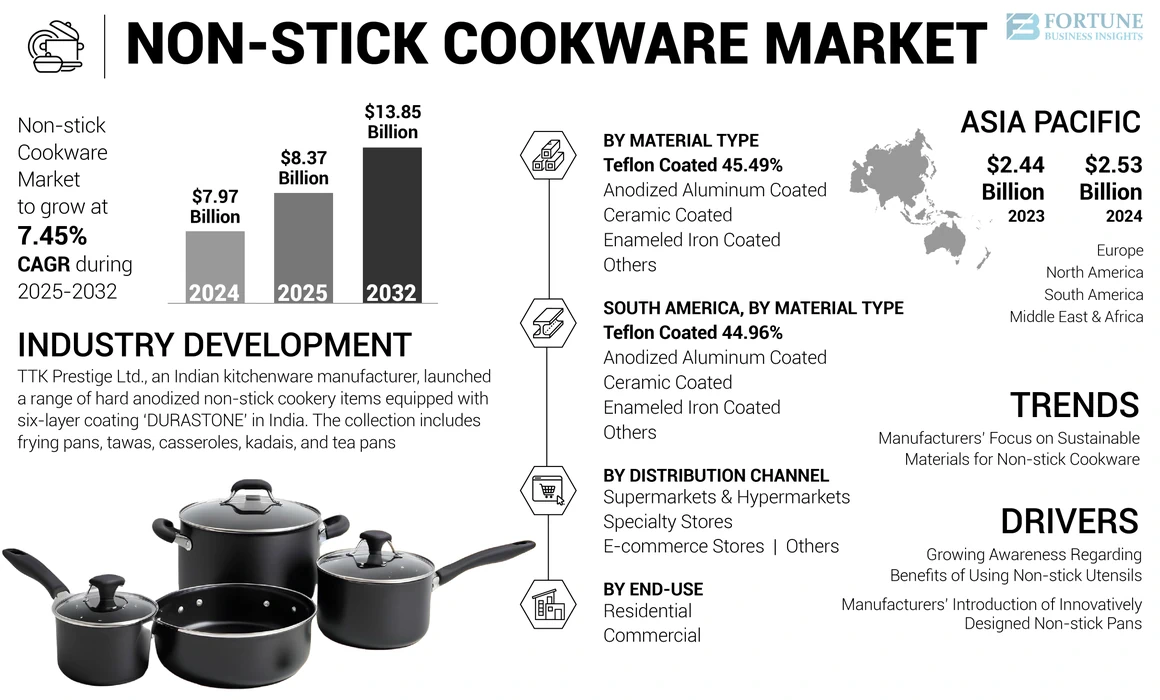

- Asia Pacific witnessed non-stick cookware market growth from USD 2.44 Billion in 2023 to USD 2.53 Billion in 2024.

Request FREE Sample PDF Copy of Non-stick Cookware Market Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/non-stick-cookware-market-105006

Why Non-stick Cookware is in High Demand

Cooking trends have shifted from plain metal pots to modern, scratch-resistant, and vibrant non-stick pans. Homeowners increasingly look for cookware that not only performs well but also complements their kitchen décor .

Some of the key reasons driving this demand include:

- Easy cleaning compared to conventional utensils.

- Durability of Teflon and anodized aluminum coatings.

- Modern designs and color options to match evolving lifestyle trends.

COVID-19 Impact: A Temporary Slowdown

Like many industries, the cookware sector faced challenges during the COVID-19 pandemic . Trade restrictions, raw material shortages, and factory shutdowns disrupted production and supply chains. However, as economies reopened, consumer spending on home and kitchen products rebounded strongly, helping the market get back on track.

Key Market Trends

1. Rise of Teflon and Anodized Cookware

The Teflon/PTFE coated segment continues to dominate due to its corrosion resistance and usability . Meanwhile, hard anodized cookware is gaining popularity in Asia Pacific thanks to its strength and performance.

2. Residential Segment Leads the Way

More households are investing in modern cookware due to urbanization, home renovation projects, and rising interest in stylish kitchens . This makes the residential segment the largest consumer base.

3. Supermarkets & Hypermarkets Dominate Distribution

While online sales are growing, supermarkets and hypermarkets remain the top choice for buyers because they offer a wide range of cookware options in one place.

Regional Insights

- Asia Pacific is the fastest-growing region, valued at USD 2.36 billion in 2022 . Countries such as India, China, and Japan are expanding manufacturing capacities, boosting availability and affordability of non-stick cookware.

- North America and Europe show steady growth, with consumers leaning toward premium and sustainable cookware solutions .

Challenges to Market Growth

Despite the positives, the market faces some hurdles. Damaged or overheated Teflon cookware has been linked to health concerns, ranging from minor symptoms like headaches to severe issues such as kidney cancer. This has prompted both consumers and manufacturers to look for safer, eco-friendly alternatives .

To get to know more this market; please visit: https://www.fortunebusinessinsights.com/non-stick-cookware-market-105006

Competitive Landscape

Leading players are focusing on innovation, recycling initiatives, and production capacity expansion to strengthen their market presence.

- Groupe SEB launched its “Recycle with Tefal” campaign in the UAE, promoting eco-friendly cookware.

- Wonderchef Home Appliances partnered with Sixth Sense Ventures in 2021, investing over USD 20 million to boost its online presence and manufacturing in India.

Key Companies in the Market

- Groupe SEB (France)

- TTK Prestige Ltd. (India)

- Newell Brands (U.S.)

- Moneta Cookware (Italy)

- Bradshaw International (U.S.)

- StoveKraft (India)

KEY INDUSTRY DEVELOPMENTS:

- November 2022: TTK Prestige Ltd., an Indian kitchenware manufacturer, launched a range of hard anodized non-stick cookery items equipped with six-layer coating ‘DURASTONE’ in India. The range includes frying pans, tawas, casseroles, kadais, and tea pans.

- April 2022: Meyer Corporation, a U.S.-based kitchenware maker, introduced the Meyer Accent collection, including 16 hard-anodized aluminum non-stick and stainless steel-based utensils in the U.S. market.

The Future of Non-stick Cookware

With rising awareness about healthy cooking, sustainable materials, and premium kitchen aesthetics, the non-stick cookware industry is set for strong growth through 2030. Innovation in scratch-resistant coatings, eco-friendly materials, and colorful product designs will continue shaping the market.

✅ Key Takeaway: The non-stick cookware market is on track to cross USD 11.7 billion by 2030, driven by modern kitchen trends, product innovation, and strong demand from households worldwide.

Kids Casual Wear Industry Growth, Market Share & Size Forecast 2025–2032

By Industry Outlook, 2025-08-28

According to Fortune Business Insights , the global kids casual wear market size was valued at USD 117.57 billion in 2024 and is projected to grow from USD 124.93 billion in 2025 to USD 196.16 billion by 2032, registering a CAGR of 6.66% during the forecast period. In 2024, Asia Pacific dominated the market with a 35.16% market share, fueled by urbanization, increasing consumer spending, and the adoption of global fashion trends in countries such as China, India, and Southeast Asia.

Growth is driven by rising disposable incomes, fashion-conscious parents, expanding e-commerce penetration, and the growing influence of digital and social media platforms. Growing demand for stylish, functional, and sustainable kidswear is reshaping industry dynamics. Consumers increasingly prefer cotton-rich, eco-friendly, and gender-neutral outfits, while global brands and regional players are responding with trend-driven, customizable, and ethically produced collections.

Request FREE Sample PDF Copy of Kids Casual Wear Market Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/kids-casual-wear-market-113158

Key Market Insights

- Market Size (2024): USD 117.57 billion

- Market Size (2025): USD 124.93 billion

- Forecast Size (2032): USD 196.16 billion

- CAGR (2025–2032): 6.66%

- Regional Leader (2024): Asia Pacific – 35.16% market share

- Asia Pacific witnessed kids casual wear market growth from USD 39.19 billion in 2023 to USD 41.34 billion in 2024.

Segmental Highlights:

- Product: Top wear dominates due to mix-and-match flexibility and higher turnover.

- End-User: Boys segment leads bulk utility purchases; girls segment grows fastest, driven by trend adoption.

- Age Group: Above 10 years dominates as kids become more fashion-conscious; below 5 years grows fastest due to rising infant wear demand.

- Distribution: Offline channels dominate; online grows fastest due to rising mobile commerce.

Market Dynamics

Drivers

- Social Media & Digital Exposure

Platforms such as Instagram, YouTube, and TikTok are shaping children’s fashion choices. Kid influencers and family content channels accelerate demand for trendy apparel. According to Sprout Social , the influencer marketing industry will reach USD 32.55 billion in 2025 , directly boosting kids fashion visibility. - Rising Urbanization & Disposable Income

Emerging economies such as India, China, and Brazil are witnessing higher disposable incomes, enabling parents to spend more on branded, stylish, and functional kidswear. - Seasonal Collections & Mini-Me Fashion

Seasonal launches, character licensing (e.g., Disney collaborations), and adult-inspired "mini-me" trends drive consistent demand for casual wear.

Restraints

- High Price Sensitivity

Parents remain cautious about spending on children’s clothing due to rapid growth spurts, leading to frequent replacements. This limits the scalability of premium and luxury kidswear in price-sensitive markets.

Opportunities

- Sustainable Fashion Adoption

Growing awareness about environmental impact presents a major opportunity. Brands adopting organic fabrics, recycled materials, and transparent supply chains gain consumer trust and loyalty. - Technological Advancements in Fabrics

Moisture-wicking, breathable, and high-performance materials are gaining traction, especially in regions where parents prioritize comfort alongside style.

Market Segmentation

By Product

- Top Wear (Dominant): Jackets, sweaters, shirts, tops, dresses. High frequency of replacement and wide variety fuel growth.

- Bottom Wear (Fastest Growing): Pants, jeans, skirts. Gender-neutral and sustainable designs boost segment demand.

- Others: Accessories, footwear, and seasonal items.

By End-User

- Boys (Largest Share): Driven by bulk, utility-based purchases.

- Girls (Fastest Growing): Fashion-forward, trend-conscious parents and demand for variety support higher growth.

By Age Group

- Above 10 Years (Largest Share): Growing independence and fashion consciousness drive demand.

- Below 5 Years (Fastest Growing): Infant and toddler wear rising due to higher birth rates and demand for eco-friendly baby apparel.

- 6–10 Years: Stable growth supported by schoolwear and casual comfort.

By Distribution Channel

- Offline (Dominant): Touch-and-feel advantage, sizing accuracy, and urgent purchase needs.

- Online (Fastest Growing): E-commerce and mobile commerce adoption provide convenience, variety, and competitive pricing.

Regional Outlook

- Asia Pacific (41.34 Billion in 2024): Largest market; urbanization, rising incomes, and e-commerce adoption fuel growth in India, China, and Southeast Asia.

- North America: Strong presence of licensed character apparel, premium brands, and holiday-driven demand.

- Europe: Fastest growth rate; sustainability and mini-me fashion trends dominate consumer behavior.

- South America & Middle East & Africa: Growing birth rates, urban migration, and rising brand awareness drive steady demand.

To get to know more about this market; please visit: https://www.fortunebusinessinsights.com/kids-casual-wear-market-113158

Competitive Landscape

The kids casual wear market is highly competitive with global brands and regional players leveraging innovation, partnerships, and sustainability to gain market share.

Key Players:

- Nike (U.S.)

- Adidas (Germany)

- H&M (Sweden)

- Zara (Spain)

- Gap Inc. (U.S.)

- Uniqlo (Japan)

- Carter’s (U.S.)

- The Children’s Place (U.S.)

- Tommy Hilfiger (U.S.)

- Under Armour (U.S.)

Key Developments:

- Jan 2025: Zara launched a Paddington Bear-inspired kidswear collection.

- Sep 2024: Disney & Gap Inc. introduced a varsity-inspired collection featuring Disney characters.

- Nov 2023: Gap Inc. expanded kids’ clothing lines with sweatpants and accessories.

- Sep 2023: KKCL launched Junior Killer brand in India, targeting ages 4–16.

- Nov 2022: Adidas expanded its kidswear footprint in India with a new flagship store.

The kids casual wear market is poised for robust growth, driven by rising fashion awareness, digital influence, and sustainable fashion adoption. While price sensitivity remains a challenge, opportunities in eco-friendly apparel, e-commerce expansion, and trend-driven collections are expected to propel the industry forward through 2032 .

Veterinary Care Industry Growth, Market Share & Size Forecast 2025–2032

By Industry Outlook, 2025-08-28

According to Fortune Business Insights , the global veterinary care market size was valued at USD 39.37 billion in 2024 and is projected to grow from USD 41.07 billion in 2025 to USD 59.56 billion by 2032, exhibiting a CAGR of 5.45% during the forecast period. North America led the market with a 37.82% market share in 2024, driven by high pet ownership, awareness, and spending on animal health.

Veterinary care encompasses medical treatment, diagnosis, prevention, and surgery for animals, including dogs, cats, horses, pigs, and livestock. Services range from emergency surgeries to spaying, neutering, vaccinations, and orthopedic procedures. Importantly, veterinarians also play a key role in preventing zoonotic diseases (animal-to-human infections), which has gained significant attention post-pandemic. Major players such as Zoetis Services, LLC, Merck & Co., IDEXX Laboratories, and Ceva are focusing on innovation, advanced diagnostics, and telehealth integration to remain competitive.

Get FREE Sample PDF Copy of Veterinary Care Market Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/kids-casual-wear-market-113158

GLOBAL MARKET SNAPSHOT

- 2024 Market Size: USD 39.37 Billion

- 2025 Market Size: USD 41.07 Billion

- 2032 Forecast: USD 59.56 Billion

- CAGR (2025–2032): 5.45%

- Regional Leader: North America (37.82% share in 2024)

- North America witnessed veterinary care market growth from USD 14.31 billion in 2023 to USD 14.89 billion in 2024.

Key Segment Insights

- Animal Type: Dogs & cats dominate, fueled by pet adoption and wellness demand.

- Service Type: Preventive & routine care leads, while diagnostic care is the fastest-growing segment.

- Distribution: Telehealth and online platforms are transforming access and affordability.

MARKET DYNAMICS

Drivers

- Surge in Global Pet Adoption

Rising pet adoption across developed and developing economies has significantly increased veterinary care demand. Pets are increasingly valued for companionship, mental health support, and stress relief. In the U.S., 70% of households owned pets in 2021–2022 , a major driver of veterinary care spending. Emerging economies like India, Brazil, and Vietnam are witnessing rapid adoption due to urbanization, lifestyle changes, and digital awareness campaigns. - Rising Awareness of Animal Health

Governments, NGOs, and veterinary clinics are conducting awareness campaigns about vaccinations, preventive checkups, and zoonotic disease control. Regular health camps and community outreach programs are boosting the uptake of veterinary services worldwide.

Restraints

- Rising Cost of Veterinary Services

The cost of care is increasing due to labor shortages, regulatory burdens, and advanced training requirements for specialized services. According to the Independent Veterinary Practitioners Association , service costs have risen over 60% in the last decade , restricting access for cost-sensitive pet owners.

Opportunities

- Integration of Advanced Technology

The growing adoption of MRI, ultrasound, laparoscopy, and AI-based diagnostics is enhancing veterinary care quality. Telehealth is emerging as a cost-effective solution, improving access and client compliance. Additionally, social media marketing has become a powerful tool for veterinary clinics to attract new clients and retain existing ones, creating growth opportunities in both urban and rural markets.

SEGMENTATION ANALYSIS

By Animal Type

- Dogs & Cats: Largest segment due to rising adoption rates. The U.S. reported 59.8 million dog-owning households in 2024 , nearly double 1996 levels, while cat ownership also rose significantly.

- Horses: Expected to grow fastest, supported by government welfare initiatives and easier adoption via online platforms.

- Pigs & Others: Gradual growth as livestock health gains more attention for food safety and productivity.

By Service Type

- Preventive & Routine Care: Largest segment, supported by growing awareness of vaccinations, deworming, and annual wellness checkups.

- Diagnostic Care: Poised for highest CAGR, driven by early detection tools such as x-rays, biopsies, and lab testing.

- Emergency & Specialized Care: Rising demand for orthopedic surgeries, oncology, and critical care as pet owners increasingly treat pets like family members.

REGIONAL ANALYSIS

- North America: Largest market, valued at USD 14.89 billion in 2024 . Growth driven by high pet ownership, advanced veterinary infrastructure, and premium care trends. The U.S. leads, with 90.5 million households owning pets in 2021–2022.

- Europe: Projected to grow steadily due to advanced diagnostic services and strong awareness of pet health. Over 90 million households owned pets in 2021 , with cats being the most popular. Germany, France, and the U.K. dominate regional demand.

- Asia Pacific: Witnessing fastest adoption growth due to rising disposable income, urbanization, and pet humanization trends . India, in particular, is emerging as a significant market, supported by a growing middle-class population.

- South America: Countries like Brazil and Argentina show rising adoption rates, boosted by NGO-led campaigns and expanding veterinary infrastructure.

- Middle East & Africa: Market growth is fueled by increasing pet ownership in UAE and Saudi Arabia , where premium veterinary care is gaining popularity.

Get to know more about this market; please visit: https://www.fortunebusinessinsights.com/kids-casual-wear-market-113158

COMPETITIVE LANDSCAPE

Prominent players in the veterinary care market include:

- Zoetis Services, LLC

- Merck & Co., Inc.

- IDEXX Laboratories

- Ceva

- Crown Veterinary Services Pvt. Ltd.

Recent Developments

- Companies are expanding geographic presence through mergers and acquisitions.

- Key players are investing in AI-driven diagnostics and telehealth platforms to improve efficiency.

- Increasing emphasis on wellness services, preventive care, and luxury pet healthcare offerings to cater to high-income pet owners.

The veterinary care market is set for steady growth, fueled by rising pet ownership, preventive care awareness, and technological advancements . While high service costs remain a challenge, the increasing adoption of telehealth, AI-based diagnostics, and social media outreach is making veterinary care more accessible. North America remains the market leader, but Asia Pacific and emerging economies represent high-growth regions. With pets increasingly considered part of the family, the demand for quality, advanced, and preventive veterinary services will continue to accelerate through 2032.

Handloom Sarees Industry Growth, Market Share & Size Forecast 2025–2032

By Industry Outlook, 2025-08-28

According to Fortune Business Insights , the global handloom sarees market size was valued at USD 3.72 billion in 2024 and is expected to grow from USD 3.99 billion in 2025 to USD 7.29 billion by 2032, registering a CAGR of 8.99% during the forecast period. Asia Pacific dominated the market with a 68.82% market share in 2024, primarily driven by strong domestic demand, cultural heritage, and supportive government initiatives such as India’s “ Vocal for Local ” campaign.

Handloom sarees, woven using traditional methods, are cherished for their craftsmanship, exclusivity, and regional diversity. Iconic varieties include Kanjeevaram sarees (Tamil Nadu), Maheshwari sarees (Madhya Pradesh), and Banarasi sarees (Uttar Pradesh). Market players such as Maheshwari Handloom, BHOLI SAREES, Ajmera Fashion Limited, and HMR Handlooms are actively investing in eco-friendly raw materials, sustainable packaging, and innovative designs to remain competitive.

Request FREE Sample Copy of Handloom Sarees Market Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/handloom-sarees-market-113034

GLOBAL MARKET SNAPSHOT

- 2024 Market Size: USD 3.72 Billion

- 2025 Market Size: USD 3.99 Billion

- 2032 Forecast: USD 7.29 Billion

- CAGR (2025–2032): 8.99%

- Regional Leader (2024): Asia Pacific (68.82% share)

Key Segment Insights

- Material: Cotton sarees dominate due to breathability and festive demand.

- Distribution Channel: Retail outlets/offline remain dominant, though e-commerce is expanding rapidly among urban and younger consumers.

- Geography: India remains the largest hub, while international markets such as the U.S., U.K., Canada, and Middle East are witnessing rising demand from diaspora communities.

- Asia Pacific witnessed handloom sarees market growth from USD 2.38 billion in 2023 to USD 2.56 billion in 2024 .

MARKET DYNAMICS

Drivers

- Rising Popularity of Traditional Handloom Sarees

Handloom sarees are gaining popularity globally for their unique craftsmanship, cultural heritage, and exclusivity . Unlike machine-made fabrics, these sarees feature intricate weaves, natural dyes, and luxury finishes, appealing to consumers seeking premium and sustainable fashion . Revived weaving techniques such as Khadi, Banarasi, and Kanjeevaram are now marketed as luxury goods, especially to younger consumers reconnecting with cultural traditions. - Government and Private Sector Investment

Government support through subsidies, welfare schemes, and marketing initiatives has strengthened the handloom sector. Private companies are also investing in eco-friendly products and collaborating with designers to blend tradition with modern fashion trends , enhancing market reach.

Restraints

- High Cost of Production

Handloom sarees are labor-intensive and time-consuming , relying on skilled artisans and expensive raw materials such as silk, zari, and natural dyes. Limited production quantities and exclusivity further increase costs, restricting mass-market adoption.

Opportunities

- Rising Social Media Marketing

Manufacturers are leveraging Instagram, Facebook, TikTok, and e-commerce platforms to reach younger consumers. Social media campaigns help build brand awareness, loyalty, and customer engagement , while digital marketplaces provide affordable global reach. This trend is expected to accelerate export demand for Indian handloom sarees across Europe, the Middle East, and North America.

SEGMENTATION ANALYSIS

By Material

- Cotton Sarees: Hold the largest share, especially popular during festivals and weddings due to comfort and durability.

- Silk Sarees: Considered luxury items, in high demand for occasions and exports.

- Linen Sarees: Expected to grow fastest, driven by lightweight and breathable fabric demand.

- Wool Sarees: Niche adoption in colder regions.

By Distribution Channel

- Retail Outlets/Offline: Dominant segment, supported by specialty stores, malls, and hypermarkets offering fabric inspection and personalized service .

- E-commerce/Online: Fastest-growing channel, offering variety, affordability, discounts, and doorstep delivery , especially appealing to urban millennials.

REGIONAL ANALYSIS

- Asia Pacific: Largest market, valued at USD 2.56 billion in 2024 . India is the key hub, supported by government schemes, revival campaigns, and export expansion to 20+ countries . Cultural festivals and rising middle-class income further fuel growth.

- North America: Strong CAGR projected, driven by the South Asian diaspora and increasing interest in luxury silk sarees such as Banarasi and Mysore silk.

- Europe: Growing demand for sustainable and artisanal fashion enhances saree imports. Consumers value ethical and handcrafted goods.

- Middle East & Africa: Social media advertising and availability on platforms like Amazon, Noon, and Namshi are fueling rising demand.

- South America: Niche but expanding market, supported by growing cultural exposure through festivals and Indian communities.

To get to know more about this market; please visit: https://www.fortunebusinessinsights.com/handloom-sarees-market-113034

COMPETITIVE LANDSCAPE

Key players in the handloom sarees market include:

- Maheshwari Handloom (India)

- BHOLI SAREES (U.S.)

- Ajmera Fashion Limited (India)

- HMR Handlooms (India)

- Albeli (India)

- KTC Fashion (India)

- Jagg Hastakala (India)

- Dhananjay Creations Private Limited (India)

- Sameer Handloom (India)

- Mrignayani (India)

Recent Developments

- Leading brands are focusing on new product launches with eco-friendly fibers and sustainable packaging.

- Collaborations with fashion designers and artisans are boosting premium and luxury saree demand internationally.

- Companies are also expanding digital presence through online-exclusive collections and influencer-led campaigns .

The global handloom sarees market is on a strong growth trajectory, fueled by cultural heritage revival, government initiatives, social media influence, and international demand . Cotton sarees remain dominant, while silk and linen sarees are gaining traction in premium and modern categories. With Asia Pacific leading production and global exports expanding, the market presents lucrative opportunities for manufacturers embracing sustainability, digital marketing, and product innovation .

Global Knee High Boots Market Size, Share & Demand Forecast 2025–2032

By Industry Outlook, 2025-08-26

According to Fortune Business Insights , the global knee high boots market is witnessing strong growth, driven by evolving fashion trends, rising disposable incomes, and growing urbanization. Knee-high boots, which extend just below or above the knee, have become a staple fashion item for women, valued for their style, comfort, and seasonal adaptability. These boots are increasingly worn not only in cold regions but also as statement footwear at social events, music festivals, and professional gatherings.

The growing influence of celebrities, models, and influencers across television, magazines, movies, and social media has significantly shaped consumer preferences, fueling the adoption of knee-high boots worldwide. According to the International Labour Organization (ILO), women’s employment has been steadily increasing, and in 2019, the global female employment rate was 64%, up from 58.3% in 2009. This rise in the number of working women, combined with increased spending power, has boosted sales of fashion-forward footwear, including knee-high boots.

Moreover, seasonal demand remains a key growth factor. In colder regions, these boots are widely preferred for their warmth, insulation, and durability, making them both a fashionable and functional choice.

Get FREE Sample Copy of Knee High Boots Market Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/knee-high-boots-market-104143

Key Market Drivers

1. Growing Fashion Industry and Trends

The fashion industry continues to expand globally, with revenues estimated at USD 2.4 trillion in 2017 (Forbes, 2019). As fashion shows and events increasingly showcase knee-high boots in multiple designs and styles, consumer interest and market demand rise.

2. Rising Urbanization and Consumer Spending

Rapid urbanization and higher disposable incomes are creating strong consumer bases in metropolitan areas. Fashion-conscious urban dwellers seek premium and trendy products, further fueling demand.

3. Celebrity and Media Influence

Celebrity endorsements and media exposure, particularly in reality shows, movies, and online platforms, drive the popularity of knee-high boots. Consumers are heavily influenced by these trends, directly impacting purchase behavior.

Key Market Restraints

1. Competition from Substitute Products

Intense competition from alternatives such as high heels, Chelsea boots, chunky boots, wedge heels, and biker boots poses a major challenge. These substitutes often provide similar aesthetics at competitive price points.

2. Price Sensitivity in Emerging Markets

In developing regions, affordability plays a significant role, with consumers often preferring budget alternatives over premium knee-high boots, hampering market penetration.

Market Segmentation

By Material Use

- Leather – Dominant segment due to durability, elasticity, comfort, and premium appeal. Leather boots also offer long-lasting wear, making them a popular choice.

- Wool – Favored for winter wear and cold regions.

- Polyester – Preferred for lightweight, affordable alternatives.

- Others – Includes blends and synthetic materials designed for affordability and fashion flexibility.

By Type

- Classic Boots – Timeless designs favored across age groups.

- Motorcycle Boots – Popular among niche segments for rugged style.

- Riding Boots – Functional yet fashionable, gaining traction among equestrian and outdoor consumers.

- Dressy Boots – Largest segment; versatile and suitable for both casual and formal occasions, pairing well with jeans, dresses, and skirts.

By Sales Channel

- Mall Retail – Dominant distribution channel, offering multiple brands under one roof and high footfall exposure.

- Online – Fastest-growing channel, fueled by e-commerce penetration, influencer marketing, and convenience of doorstep delivery.

- Shoe Stores – Stable segment catering to traditional buyers who prefer in-store trials.

Regional Analysis

North America

- Expected to dominate the market through 2032.

- Strong consumer spending on apparel and fashion accessories supports growth.

- The U.S., home to New York City (global fashion capital), drives demand as fashion-conscious consumers embrace seasonal and trendy footwear.

- TV reality shows, social media campaigns, and celebrity culture play a major role in popularizing knee-high boots.

Europe

- Anticipated to show significant market presence, supported by fashion-centric cities (Paris, Milan, London) and wide availability of malls and shopping centers.

- High prevalence of nightlife culture (clubs, pubs, concerts, festivals) boosts demand for stylish boots.

- Rising shopping addiction also contributes to higher consumption. According to UK Rehab, 3% of European adults and 8% of young people show compulsive shopping behaviors.

Asia Pacific

- Strong growth expected due to rising disposable incomes, rapid urbanization, and increasing adoption of Western fashion styles in countries like China, India, and Japan.

- Growing e-commerce platforms further accelerate product accessibility and adoption.

South America & Middle East & Africa

- Emerging regions with increasing urbanization and consumer awareness.

- Limited by affordability concerns, but expanding fashion retail stores and international brand entry are expected to drive future growth.

To get to know more about this market; please visit: https://www.fortunebusinessinsights.com/knee-high-boots-market-104143

Competitive Landscape

Key Players Covered

- The Frye Company

- Stuart Weitzman

- Jimmy Choo PLC

- Loeffler Randall

- Edelman Shoe Inc.

These companies compete on product design, brand image, quality, and distribution reach. Luxury positioning and influencer collaborations are common strategies.

Recent Industry Developments

- Nov 2017: Everlane launched its first knee-high boots featuring cushioned insoles, walkable two-inch heels, and easy-wear design.

- Oct 2019: Tamara Mellon introduced its “Icon Boot” in multiple calf sizes (small, medium, large). The brand partnered with models and actresses to create an inclusive marketing campaign.

Future Outlook (2025–2032)

The knee high boots market is expected to maintain strong growth momentum, fueled by:

- Increasing global fashion consciousness.

- Expansion of e-commerce and social media influence.

- Rising participation of women in the workforce and higher purchasing power.

- Seasonal demand in cold regions.

While competition from substitutes remains a challenge, innovation in design, sustainable materials, and inclusive sizing options will help brands differentiate and capture consumer loyalty.

According to Fortune Business Insights , the global boxing gloves market is set to witness strong growth during the forecast period (2025–2032), driven by the rising popularity of combat sports, increasing participation in fitness activities, and technological advancements in sports equipment. Boxing gloves are essential gear for professional matches, amateur tournaments, and fitness training, symbolizing strength, endurance, and discipline.

While the market witnessed a slowdown in 2020 due to COVID-19 restrictions on gyms, sports facilities, and global supply chains, recovery since 2021 has been robust. With gyms reopening, tournaments resuming, and the growth of mixed martial arts (MMA) and fitness boxing, demand for high-quality gloves has surged.

Get FREE Sample Copy of Boxing Gloves Market Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/boxing-gloves-market-112542

Key Market Drivers

1. Popularity of MMA and Combat Sports

The increasing global reach of boxing and MMA is a prime driver. Rising awareness of health benefits such as cardiovascular improvement, calorie burning, and stress relief has made boxing a preferred workout activity. Expanding training facilities, global tournaments, and fitness leagues further boost demand.

2. Technological Advancements

Manufacturers are focusing on lightweight materials, superior shock absorption, and hi-tech gloves with sensors that track performance and health metrics. These innovations enhance safety and functionality for both professionals and enthusiasts.

3. Fitness and Social Media Influence

Celebrity endorsements, fitness influencers, and social media trends have positioned boxing as a mainstream fitness activity. The growing culture of at-home workouts and personalized training routines has fueled the sales of boxing gloves among recreational users.

Market Restraints

1. Counterfeit Products

The influx of counterfeit and low-quality gloves, particularly from unregulated markets, poses a safety risk and threatens established brands. Inferior gloves fail to meet safety standards, increasing injury risks.

2. Raw Material Price Fluctuations

The volatility of raw material costs (leather, foam, synthetic fabrics) impacts manufacturers’ margins and pricing strategies, creating challenges for premium brands.

Market Opportunities

1. At-Home and Community Boxing

The rise of amateur and recreational boxing is creating new opportunities. Fitness-focused boxing routines at gyms, homes, and community centers appeal to casual users. Gloves tailored for entry-level and fitness training have become highly profitable segments.

2. Eco-Friendly and Sustainable Materials

The growing demand for sustainable sportswear is opening avenues for eco-friendly gloves. Recent innovations in vegan and plant-based leather alternatives are expected to gain traction among environmentally conscious consumers.

Market Segmentation

By Type

- Training Gloves – Largest market share; versatile for sparring, fitness training, and recreational boxing.

- Competition Gloves – Primarily used in professional and amateur tournaments.

- Bag Gloves – Expected to grow at the fastest CAGR due to rising popularity of at-home punching bags and individual workouts.

By Technology

- Traditional Gloves – Dominant segment; affordable, durable, and widely available.

- Hi-Tech Gloves – Fastest-growing category; equipped with performance sensors, improved padding, and smart connectivity.

By End User

- Fitness Enthusiasts – Largest consumer group, driven by the popularity of boxing for fitness, stress management, and weight control.

- Amateur Boxers – Projected to grow rapidly with the rise of community leagues and training academies.

- Professional Athletes – Stable demand, focusing on premium and competition-specific gloves.

Regional Analysis

North America

- Holds the largest market share, supported by the U.S.’s strong sports culture and wellness spending estimated at USD 1.8 trillion.

- High per capita fitness expenditure (USD 5,000+) sustains demand for premium gloves.

Europe

- Ranked second, with Germany (USD 269 billion) and the U.K. (USD 224 billion) leading the market.

- Post-pandemic recovery has pushed demand 120% above pre-COVID levels, driven by fitness awareness and government-backed health initiatives.

Asia Pacific

- Expected to grow at a rapid pace, fueled by increasing participation in boxing and MMA across China, Japan, and India.

- China leads with a wellness industry value of USD 790 billion, while Japan contributes USD 241 billion.

- Affordable local brands and rising middle-class fitness spending accelerate adoption.

South America & Middle East & Africa

- Emerging markets with growing recreational boxing communities.

- Economic constraints and counterfeit products remain challenges but rising awareness is expected to improve penetration.

Read Full Report Summary Hear: https://www.fortunebusinessinsights.com/boxing-gloves-market-112542

Competitive Landscape

Key Players

- Everlast Worldwide, Inc. (U.S.)

- Adidas AG (Germany)

- Winning Co., Ltd. (Japan)

- Cleto Reyes (Mexico)

- Hayabusa Fightwear Inc. (Canada)

- RDX Sports (U.K.)

- Twins Special Co., Ltd. (Thailand)

- Fairtex Equipment Co., Ltd. (Thailand)

- Top King Boxing (Thailand)

- Venum (France)

Recent Developments

- Dec 2024: Hit N Move launched innovative boxing gloves featuring DR-T cushioning technology, highlighted in the film Creed III . The company has grown 200% annually since 2020, focusing on premium protective gear.

- Nov 2024: Adidas partnered with Mexican biomaterial brand DESSERTO to launch vegan cactus leather boxing gloves. This aligns with the trend toward eco-friendly sports gear and expands Adidas’s sustainability portfolio.

Industry Insights

- The market is witnessing supply chain restructuring post-COVID.

- SWOT and Porter’s Five Forces analysis indicate high competition, with opportunities lying in innovation, branding, and eco-friendly manufacturing.

- Advanced 3D manufacturing and smart sensors are set to redefine boxing glove design and safety.

Future Outlook (2025–2032)

The global boxing gloves market is projected to expand steadily, driven by:

- Growing participation in combat sports and fitness boxing.

- Increasing demand for eco-friendly and hi-tech gloves.

- Expansion of recreational boxing leagues and home workouts.

While counterfeit products and raw material fluctuations remain hurdles, strategic innovations, brand differentiation, and sustainable practices will ensure strong market growth through 2032.

According to Fortune Business Insights , the global diabetic socks market is witnessing steady growth due to rising cases of diabetes, increasing health awareness, and growing demand for preventive healthcare products. Diabetic socks are specifically designed to reduce foot injuries, improve blood circulation, and keep feet dry. These products feature anti-bacterial properties, moisture-wicking material, and fungal infection prevention, making them essential for patients with diabetic neuropathy, plantar fasciitis, bunions, and other foot-related disorders.

According to the Centers for Disease Control and Prevention (CDC), an estimated 88 million adults in the U.S. have prediabetes, representing 34.5% of the population. This rising health risk is fueling the demand for diabetic care products, including diabetic socks.

Get FREE Sample Copy of Diabetic Socks Market Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/diabetic-socks-market-104128

Key Market Insights

- Growing global health expenditure on primary healthcare (PHC) supports market growth.

- Introduction of smart diabetic socks with features such as temperature monitoring, injury detection, and smartphone connectivity is creating new opportunities.

- Lack of awareness in developing and underdeveloped regions acts as a restraint to market expansion.

Market Drivers and Restraints

Key Market Driver

- Rising Health Spending: Increasing healthcare expenditure worldwide is boosting the adoption of diabetic socks. For instance, the World Health Organization (WHO) reported that PHC spending accounted for 33–88% of health budgets in 2018 across 88 countries.

Key Market Restraint

- Lack of Awareness: Limited knowledge about the benefits of diabetic socks, especially in emerging economies, hampers growth potential.

Market Segmentation

By Product Type

- Regular Socks – Larger market share due to affordability and ease of use, particularly among the elderly population.

- Smart Socks – Growing demand with features like foot health monitoring, injury detection, and smartphone connectivity.

By Material Use

- Cotton – Expected to dominate due to breathability, lightweight nature, moisture absorption, and long-lasting quality.

- Polyester

- Nylon

- Wool

By Quality

- Standard – Leading segment, offering durability, insulation, hypoallergenic properties, and moisture control at affordable prices.

- Low

- Premium

Regional Analysis

North America

- Holds the largest market share and is projected to maintain dominance through 2032.

- High prevalence of obesity and diabetes is driving demand. According to the National Diabetes Statistics Report (2020), nearly 89% of obese individuals in the U.S. suffer from diabetes.

- Strong awareness about diabetes-related complications and preventive products supports growth.

Asia Pacific

- Poised for significant growth due to rising diabetes cases across China, India, Bangladesh, and Sri Lanka.

- According to the International Diabetes Federation (2019–2020):

- China: 116.45 million cases

- India: 77 million cases

- Bangladesh: 8.4 million cases

- Sri Lanka: 1.2 million cases

- Increasing presence of domestic brands like Syounaa, Ista Healthcare LLP, Zhejiang Fele Sports Co., Ltd. is accelerating product adoption.

Europe, South America, Middle East & Africa

- Europe shows stable demand due to aging population.

- South America and ME&A regions are gradually growing but face challenges due to low awareness and affordability issues.

Get Full Summary Here: https://www.fortunebusinessinsights.com/diabetic-socks-market-104128

Key Players in the Market

- Simcan Enterprises Inc.

- Sigvaris

- BSN Medical

- Cresswell Socks Mill

- Intersocks S.R.L

- Dr. Scholl’s

Recent Industry Developments

- March 2018 – Siren Care launched smart diabetic socks connected to a smartphone app, capable of monitoring foot health and detecting inflammation.

- October 2019 – Handok Pharm partnered with a fashion hosiery brand to launch diabetic socks. For every pair sold, one pair was donated to diabetes patients.

Future Outlook

The diabetic socks market is expected to witness robust growth between 2025 and 2032, driven by:

- Increasing diabetic population worldwide.

- Advancements in smart wearable healthcare products.

- Growing consumer inclination towards preventive healthcare solutions.

While lack of awareness in emerging economies remains a challenge, rising urbanization, healthcare reforms, and increasing digital health adoption are anticipated to bridge the gap and expand the market globally.

According to Fortune Business Insights , the global bra market size was valued at USD 25.18 billion in 2024 and is projected to grow from USD 27.38 billion in 2025 to USD 51.09 billion by 2032, registering a strong CAGR of 9.32% during the forecast period. The Asia Pacific bra market dominated the global industry with a massive 91.19% market share in 2024.

The rising demand for comfort, inclusivity, functionality, and innovative designs in women’s intimate apparel is fueling this market expansion. This regional dominance is expected to strengthen further, supported by rising disposable incomes, growing awareness of body-positive and inclusive lingerie, and the increasing impact of global fashion trends.

As consumer preferences shift toward sustainable fabrics, stylish designs, and supportive lingerie, the bra industry is witnessing rapid product innovations from both established brands and new entrants. The integration of eco-friendly materials, seamless designs, and adaptive fits is reshaping the market, catering to the evolving needs of women across diverse age groups.

With the global lingerie market expanding, the bra segment is set to remain a key driver, offering significant opportunities for manufacturers, retailers, and e-commerce platforms worldwide.

Request FREE Sample Copy of Bra Market Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/bra-market-107937

Market Trends

Fitness and Sports Engagement

The growing inclination of women towards fitness is increasing the demand for high-impact and supportive sports bras. Features such as moisture-wicking fabric, bounce control, and anti-chafing designs are driving product innovation.

- Asia Pacific witnessed bra market growth from USD 7.35 Billion in 2023 to USD 8.06 Billion in 2024.

Competitive Landscape

The global bra market is highly competitive with both heritage brands and new entrants focusing on innovation, inclusivity, and eco-conscious products.

Key Players Profiled

- Victoria’s Secret (U.S.)

- Hanesbrands Inc. (U.S.)

- Chantelle (France)

- Wacoal (Japan)

- Triumph International (Switzerland)

- Calvin Klein Underwear (U.S.)

- Maidenform (U.S.)

- La Perla (Italy)

- Savage X Fenty (U.S.)

Key Strategies:

- Partnerships & M&A : Brands like Victoria’s Secret, PVH Corp., and Triumph International are forming collaborations and acquisitions to expand market share.

- Franchise Expansion : Many brands are exploring franchise models for greater market penetration.

- Targeted Offerings : Launch of demi-cup bras to appeal to younger demographics (18–30 age group), and full-coverage styles for older customers.

Market Drivers

- Evolving Consumer Preferences

Modern consumers are increasingly prioritizing comfort, fit, and body inclusivity in intimate wear. Styles such as wireless bras, sports bras, and bralettes are seeing heightened demand due to their adaptability and comfort.

- Technological Innovations

Advancements such as AI-driven size recommendations, virtual try-ons, and subscription models are revolutionizing how consumers shop for bras, enhancing personalization and satisfaction.

- Rise in Health and Fitness Consciousness

The surge in female participation in sports and physical activities is propelling demand for sports bras, which now serve both functional and fashion purposes.

Market Restraints

- Sizing inconsistencies across brands and regions continue to challenge the industry, resulting in high return rates and customer dissatisfaction.

- Limited size inclusivity in many offerings deters potential buyers, restraining growth despite the push for body positivity.

Market Opportunities

Social Media Influence

Platforms like Instagram and TikTok play a pivotal role in shaping lingerie trends. Influencer marketing, brand collaborations, and lifestyle content have made social media a powerful tool for boosting awareness and sales. As of 2021, over 4.48 billion people were active social media users—an opportunity brands are actively capitalizing on.

Segmentation Analysis

By Product

- Others (Underwired, Bralette, Push-up, etc.) : Dominates the segment due to fashion versatility and increasing breast surgery cases fueling demand for post-operative bras.

- Sports Bras : Expected to grow rapidly as athletic engagement and activewear trends rise.

- Maternity/Nursing Bras : Gaining popularity as consumers seek functionality during pregnancy and postpartum stages.

By Material

- Cotton : Leads the market due to its breathability, comfort, and suitability across climates.

- Satin : Fastest-growing segment, appreciated for its affordability, luxurious look, and gentleness on skin—ideal for nightwear and self-care lingerie.

By Distribution Channel

- Specialty/Branded Stores : Largest share in 2024 due to expert assistance, brand trust, and in-store experience.

- Online Retail : Poised for fastest growth due to convenience, AR-based virtual fitting tools, privacy, and broader size range availability.

To get to know more about this Market: https://www.fortunebusinessinsights.com/bra-market-107937

Regional Insights

Asia Pacific

Largest and fastest-growing market, driven by Western brand penetration, rising awareness, and investment in textile technology (e.g., Bangladesh’s RMG industry upgrades).

North America

Strong presence of established brands like Victoria’s Secret, Jockey, and Calvin Klein. Fitness and fashion culture significantly influence product adoption.

Europe

Second-largest region, thriving on fast fashion, sustainability, and innovation from local brands like Hunkemöller and Triumph.

South America & Middle East & Africa

Growing due to increasing beach and sports activities. Brazilian lingerie trends and international brand entry are catalyzing regional growth.

Recent Developments

- July 2023 : La Vie en Rose entered the Indian market via partnership with Apparel Group.

- June 2023 : Victoria’s Secret launched over 4,000 SKUs on Amazon Fashion.

- Sept 2022 : Maikai Clothing introduced biodegradable cotton sports bras in India.

- May 2022 : CALIDA GROUP acquired Cosabella to enhance U.S. market presence.

- April 2021 : Parade launched a new sustainable bralette line with inclusive sizing up to 3X.

The global bra market is poised for substantial growth through 2032, driven by rising consumer awareness, product diversification, inclusive marketing, and digital retail innovations. Key players continue to evolve through strategic partnerships, product launches, and eco-conscious innovation to cater to a diverse and fashion-forward global audience.