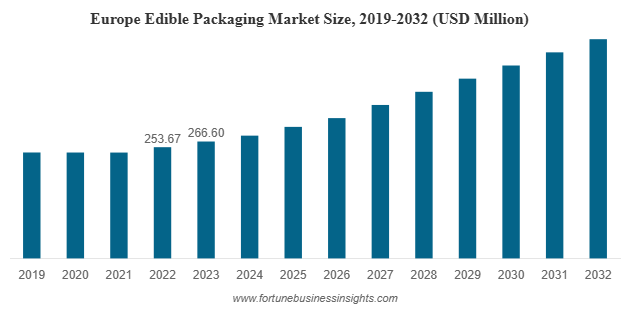

The global edible packaging market was valued at USD 711.09 million in 2023 and is expected to rise from USD 748.06 million in 2024 to nearly USD 1,193.98 million by 2032, registering a CAGR of 6.02% during the forecast period. Europe led the market in 2023 with a 37.49% share, while the U.S. market is projected to reach USD 282.59 million by 2032, fueled by growing awareness of plastic pollution and the shift toward sustainable, eco-friendly packaging solutions.

Market Overview

The edible packaging industry is undergoing a remarkable transformation as eco-conscious innovations reshape the way products are wrapped, preserved, and delivered. Among these, edible packaging has emerged as one of the most promising solutions to global concerns around plastic waste and environmental degradation. This innovative packaging is not only biodegradable but also consumable, offering dual benefits of reducing waste and enhancing consumer convenience. With strong growth projections and rising demand across the globe, the edible packaging market is stepping into a new era of expansion.

Key Trends Driving the Market

- Rising Demand for Biodegradable Films:

With global attention on plastic waste reduction, edible films are increasingly viewed as the next-generation sustainable packaging solution. Their potential to replace single-use plastics in food wraps, cutlery coatings, and beverage pouches is driving adoption. - Nanotechnology in Packaging:

Innovations in nanotechnology are enhancing the performance of edible packaging. Features like nano-encapsulation and controlled release systems improve barrier properties, shelf life, and nutritional benefits. Intelligent packaging with indicators for freshness and oxygen levels is also becoming a reality. - Health and Hygiene Focus:

Post-pandemic, consumer demand for hygienic and safe packaging has grown significantly. Edible packaging offers portion-controlled, contamination-resistant solutions that align with this demand while cutting down on packaging waste. - Shift Towards Plant-Based Materials:

The surge in plant-based diets and vegan lifestyles is fueling the use of plant-derived ingredients in packaging. Edible wraps made from seaweed, rice, and potato starch are now being explored by startups and established players alike.

List of Top Edible Packaging Companies:

- XAMPLA (U.K.)

- Notpla Ltd. (U.K.)

- JRF Technology (U.S.)

- MonoSol, LLC (U.S.)

- Evoware (Indonesia)

- Biome Bioplastics (U.K.)

- Decomer Technology OÜ (Estonia)

- Lactips (France)

- FlexSea (U.K.)

- Nagase America (U.S.)

Material Insights

By material, protein-based packaging dominates the edible packaging landscape. Derived from sources such as soy protein, whey protein, gluten, and casein, these materials are favored for their superior gas barrier properties and biodegradability. Their ability to maintain product freshness without altering taste makes them particularly suitable for perishable goods.

Polysaccharides such as starch and cellulose are also gaining traction due to their availability and versatility. Lipid-based packaging, although less common, is used for applications requiring moisture resistance. Together, these materials represent the innovation at the heart of edible packaging, balancing sustainability with functionality.

Product Insights

Among product types, films account for the largest share, holding more than 44% of the market in 2023. Edible films are widely used to coat food products, preserve freshness, and reduce microbial contamination. Their transparent and tasteless nature makes them attractive to both manufacturers and consumers.

Other product categories include capsules and coatings, often used in pharmaceuticals and nutraceuticals. These not only enhance dosage accuracy but also provide controlled release of active ingredients. Such diversity in applications ensures that edible packaging is not confined to the food industry but extends into healthcare and personal care as well.

Read more : https://www.fortunebusinessinsights.com/edible-packaging-market-107722

Regional Insights

Europe currently leads the edible packaging market, holding more than 37.49% of global revenue in 2023. This dominance is supported by strong environmental policies, consumer awareness, and significant research investments. Countries across the region are actively encouraging industries to adopt biodegradable and edible options, thereby setting benchmarks for sustainability.

North America is another fast-growing region, with the United States expected to contribute significantly to future growth. The U.S. edible packaging sector alone is projected to reach over USD 282.59 million by 2032, fueled by rising demand for sustainable solutions in food and beverages as well as pharmaceuticals. Meanwhile, Asia Pacific markets such as India and China are witnessing rapid adoption due to increasing population, growing food industries, and rising environmental consciousness. Emerging economies in Latin America and Africa are also stepping up, driven by their rising middle class and government-backed initiatives to curb plastic pollution.

Challenges Facing the Industry

Despite its potential, edible packaging faces several hurdles. Production costs remain higher compared to conventional plastic packaging, which limits scalability. The need for secondary packaging to ensure hygiene and safety often undermines the eco-friendly benefits. Additionally, regulatory challenges, particularly in markets like the United States, pose obstacles for faster adoption.

Consumer acceptance is another factor. While sustainability-conscious buyers are enthusiastic, others may hesitate to consume packaging directly, raising awareness and education as crucial steps for wider acceptance.

Key Industry Developments:

- September 2023 – Xampla announced the launch of a remarkable consumer brand, Morro, to develop bio-based and edible packaging solutions that can compete with plastics. The launch of this brand will enable food brands to make an easy switch from single-use plastics and use the company’s breakthrough material.

- August 2022 – Nippon Paint China, the premier coatings company, partnered with BASF to introduce new eco-friendly edible packaging embraced by the Nippon Paint dry-mixed mortar series products.

Opportunities

The edible packaging market holds immense promise across multiple sectors. In the food and beverage industry, it offers a way to reduce plastic waste and enhance consumer appeal. In pharmaceuticals, edible capsules and films provide functional benefits such as controlled drug release and improved dosage accuracy. The cosmetics industry is also exploring edible packaging for innovative applications.

With continuous advancements in material science, nanotechnology, and biodegradable solutions, the industry is expected to overcome many of its current challenges. Collaborations between startups, research institutions, and large corporations will further accelerate development and commercialization.

Outlook

Edible packaging market is not just a trend; it represents a significant step towards solving the global plastic waste crisis. By combining innovation, sustainability, and functionality, this market is set to redefine packaging standards for the future. Though challenges such as cost and regulations persist, the long-term outlook remains optimistic. With steady growth projected and rising demand across industries, edible packaging is poised to become an integral part of the global sustainability movement.

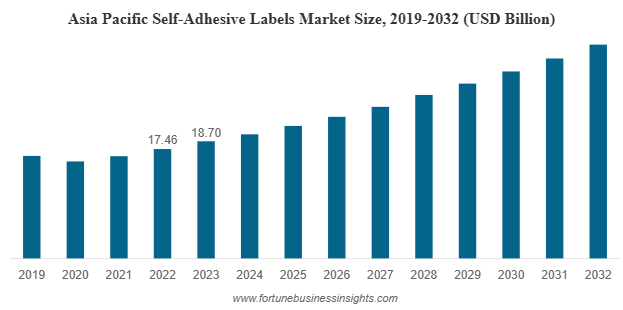

The global self-adhesive labels market size was valued at USD 48.03 billion in 2023 and is expected to reach USD 50.65 billion in 2024, before expanding to USD 82.17 billion by 2032 at a CAGR of 6.1% during the forecast period. In 2023, Asia Pacific led the market, accounting for 38.93% of the global share, driven by robust growth in food, beverage, and retail sectors. Meanwhile, the U.S. market is set to witness substantial expansion, projected to reach USD 9.47 billion by 2032, fueled by rising demand for consumables, ready-to-eat meals, and packaged food and beverages.

Market Overview

The global self-adhesive labels market is witnessing remarkable growth, driven by rising demand across industries such as food and beverages, pharmaceuticals, personal care, logistics, and retail. Self-adhesive labels, also known as pressure-sensitive labels, are widely used for product identification, branding, tracking, and conveying critical product information. They are easy to apply, versatile in design, and available in a variety of materials, making them a preferred choice for manufacturers worldwide.

List Of Key Companies Profiled

- 3M Company (U.S.)

- Axicon Labels (U.K.)

- Avery Products Corporation (U.S.)

- ETIS Slovakia (Slovakia)

- UPM Raflatac (Finland)

- Müroll GmbH (Austria)

- Royston Labels Ltd (U.K.)

- S&K LABEL (U.S.)

- SVS Etikety (Czech Republic)

- Mondi Group (Austria)

- B Fuller (U.S.)

Key Market Drivers

- Rising Demand for Packaged Foods and Beverages

The packaged food industry is among the largest consumers of self-adhesive labels. With urbanization, rising disposable incomes, and busy lifestyles, the consumption of ready-to-eat, frozen, and processed foods has surged. Self-adhesive labels are crucial for displaying nutritional information, expiry dates, barcodes, and branding elements. Beverage companies also rely heavily on these labels for durable and visually appealing packaging.

- Growth in the Pharmaceutical and Healthcare Sector

The pharmaceutical sector requires precise labeling to ensure regulatory compliance and patient safety. Self-adhesive labels are extensively used for medicine bottles, syringes, diagnostic kits, and medical devices. They provide features such as tamper-evidence, chemical resistance, and the ability to withstand extreme conditions. As global healthcare spending increases and demand for medicines grows, the pharmaceutical sector will remain a key growth driver for this market.

- Expansion of E-commerce and Logistics

E-commerce has transformed global trade, and with it, the logistics industry has experienced unprecedented growth. Self-adhesive labels play a critical role in shipping and distribution, where they are used for barcoding, tracking, and ensuring timely deliveries. As online shopping continues to expand worldwide, the demand for logistics labels is expected to rise substantially.

- Increasing Importance of Branding and Aesthetics

Modern consumers are heavily influenced by attractive packaging. Companies use self-adhesive labels not just for information, but also as a tool for marketing and differentiation. Innovations in printing technology, including digital printing, allow manufacturers to produce vibrant, customizable labels that enhance product appeal and brand recognition.

- Sustainability and Eco-Friendly Materials

With growing environmental concerns, manufacturers are shifting toward recyclable and biodegradable label materials. Eco-friendly adhesives and the use of sustainable paper or film-based substrates are becoming increasingly common. This trend is creating new opportunities in the market as companies look to align with consumer preferences and regulatory guidelines for sustainable packaging.

Market Segmentation

- By Type:

- Permanent labels (widely used for durability and tamper resistance).

- Removable and repositionable labels (gaining traction in retail and promotional applications).

- Food and beverages

- Pharmaceuticals and healthcare

- Personal care and cosmetics

- Logistics and transportation

- Retail and consumer goods

- Digital printing

- Flexographic printing

- Lithography

- Others

Among these, digital printing is gaining rapid popularity due to its ability to provide cost-effective, high-quality, and customizable designs in shorter lead times.

Read More : https://www.fortunebusinessinsights.com/self-adhesive-labels-market-104289

Key Industry Developments

- February 2024 – Mondi collaborated with multiple stakeholders along the value chain to recycle and release liner production waste. These stakeholders include Soprema, WEPA, and Vwyzle. They are working together to convert Mondi’s coated paper waste produced at its release liner plants into secondary raw material for a range of applications.

- May 2021 - Herma, a German self-adhesive technology specialist launched 52W, a new wash-off label adhesive developed especially for PET bottles.

Regional Insights

- Asia-Pacific leads the global market, accounting for nearly 39% of the total share in 2023. Countries such as China, India, and Japan are driving growth due to expanding consumer markets, urbanization, and the rise of organized retail. The region’s booming e-commerce and FMCG industries make it a hub for label manufacturers.

- North America is another significant market, fueled by high demand for customized and innovative labels in the food, beverage, and healthcare sectors. The United States and Canada are witnessing steady growth due to strong logistics networks and the rise of private-label brands.

- Europe is focusing heavily on sustainability, with stringent regulations on packaging and labeling. This has led to innovation in recyclable adhesives and eco-friendly materials, further shaping market growth.

- Latin America and the Middle East & Africa are emerging markets where rising consumer awareness, industrial growth, and urbanization are increasing the demand for self-adhesive labels.

Future Opportunities

The future of the self-adhesive labels market lies in smart labeling technologies such as RFID-enabled and QR-code labels that enhance product tracking, authenticity, and customer engagement. With the integration of digitalization and sustainability, manufacturers are likely to focus on developing intelligent, eco-friendly labeling solutions to cater to evolving consumer demands. Emerging economies also present significant opportunities for expansion as modern retail and organized trade gain momentum.

Market Challenges

While the outlook is promising, the self-adhesive labels market faces some challenges. Rising raw material prices, particularly for paper and adhesives, can affect production costs. Additionally, the trend of direct printing on packaging is emerging as an alternative to labeling, which could limit growth in certain applications. However, continuous innovation, especially in smart and eco-friendly labels, is expected to mitigate these challenges.

Outlook

The global self-adhesive labels market is on a growth trajectory, supported by strong demand from key industries and the rising importance of packaging in consumer decision-making. With advancements in printing technology, increased emphasis on sustainability, and expansion in emerging markets, the industry is poised for steady growth in the coming years. While challenges like fluctuating raw material costs and competition from direct printing exist, innovation and eco-friendly practices are expected to drive long-term success.

The global organic cotton market size was valued at USD 1,113.5 million in 2023 and is expected to expand from USD 1,585.5 million in 2024 to USD 25,890.2 million by 2032, registering a robust CAGR of 40.0% during 2024–2032. Asia Pacific led the market in 2023 with a 65.7% share, while the U.S. market is projected to reach USD 504.56 million by 2032, driven by rising consumer preference for sustainable and eco-friendly textiles.

Market Dynamics

Organic cotton market differs from conventional cotton as it is cultivated without the use of synthetic pesticides, fertilizers, or genetically modified seeds. This makes it safer for the environment, farmers, and end consumers. Over the last decade, the textile industry has been under growing scrutiny for its environmental impact, pushing both brands and consumers to explore sustainable alternatives. Organic cotton has emerged as a natural solution, aligning with the values of eco-conscious shoppers and companies aiming to meet sustainability targets.

One of the strongest drivers of growth is the rising awareness about sustainability in the apparel industry. Fashion brands across the globe are incorporating organic cotton into their collections to reduce their ecological footprint. Additionally, organic cotton is gaining traction in industries beyond apparel, including packaging, medical textiles, and personal care products. Its antibacterial properties, UV protection, and biodegradability make it ideal for applications ranging from hospital gowns to eco-friendly packaging materials.

List Of Key Companies Profiled

- Cargill Incorporated (U.S.)

- Plexus Cotton Ltd. (U.K.)

- Staple Cotton Cooperative Association (U.S.)

- Calcot Ltd. (U.S.)

- The Rajlakshmi Cotton Mills (P) Limited (India)

- Remei AG (Switzerland)

- Arvind Limited(India)

- Noble Ecotech (India)

- Louis Dreyfus Company (Netherlands)

- Texas Organic Cotton Marketing Cooperative (U.S.)

Key Growth Drivers

- Sustainable Consumer Trends

Modern consumers are increasingly favoring environmentally responsible products. With growing awareness about fast fashion’s impact, organic cotton products are seen as healthier, safer, and ethically produced alternatives. - Dominance of Apparel Segment

Apparel remains the leading application of organic cotton, with brands launching premium collections using organic fibers. From casual wear to luxury fashion, the adoption of organic cotton has been significant. - Rising Medical Applications

The global pandemic highlighted the need for safer medical textiles. Organic cotton, being hypoallergenic and chemical-free, is being increasingly used in medical supplies such as gowns, masks, and bandages. - Packaging Innovations

With the shift toward eco-friendly packaging, organic cotton is finding use in wrapping, carrying solutions, and as part of sustainable packaging materials. - Transparency and Traceability

End-to-end traceability has become crucial in supply chains. Consumers want to know where their products come from, and organic cotton certifications provide the assurance of ethical and sustainable production.

Read More : https://www.fortunebusinessinsights.com/organic-cotton-market-106612

Segmentation Insights

- By Type: Middle-staple cotton dominates the market, especially for everyday apparel. Extra-long and long-staple varieties are used for premium textiles, while short-staple cotton finds applications in packaging and medical fields.

- By Quality: Upland cotton leads in volume, catering to mass apparel production. Supima/Pima and Giza cotton serve the luxury segment due to their superior quality and softness.

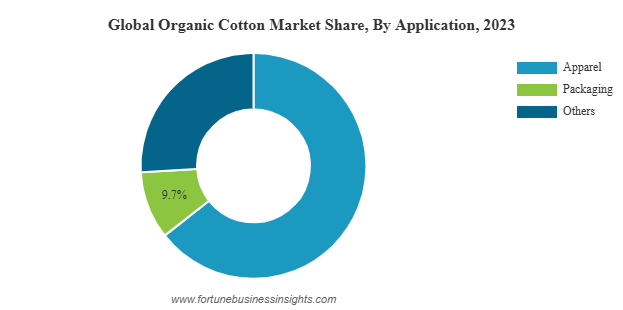

- By Application: Apparel remains the largest application segment, while packaging and medical textiles are growing at a faster pace, creating new opportunities for manufacturers.

Regional Highlights

- Asia Pacific: This region leads the global organic cotton market, accounting for nearly two-thirds of the total share in 2023. Countries like India and China play a critical role due to high cotton cultivation, expanding textile industries, and growing domestic demand for sustainable products. The regional market was valued at over USD 730 million in 2023 and is set for robust growth.

- North America: The U.S. market is forecasted to reach around USD 504 million by 2032. Strong consumer awareness and the adoption of organic products in fashion, cosmetics, and healthcare drive growth in this region.

- Europe: European countries are focusing on luxury and high-quality textiles, making the region an attractive hub for premium organic cotton products. The emphasis on sustainability regulations also fuels demand.

- Latin America and Middle East & Africa: These regions are gradually expanding their presence in the market, supported by agricultural potential, rising disposable incomes, and awareness about sustainable lifestyles.

Competitive Landscape

The organic cotton market is fragmented, with several global and regional players competing through innovation, collaborations, and sustainability-driven initiatives. Leading companies include Cargill Inc., Plexus Cotton Ltd., Staple Cotton Cooperative Association, Calcot Ltd., Rajlakshmi Cotton Mills, Remei AG, Arvind Limited, Noble Ecotech, Louis Dreyfus Company, and Texas Organic Cotton Marketing Cooperative. These players are focusing on expanding their product portfolios, strengthening supply chains, and investing in sustainable farming practices to meet rising demand.

Market Challenges

Despite its rapid growth, the organic cotton market faces challenges. High production costs remain a barrier, as organic farming requires more labor and careful crop management compared to conventional methods. Limited yields and seed availability also restrict supply, leading to a gap between demand and production. Many regions still lack the infrastructure to scale up organic farming, which could hinder long-term supply stability.

Future Outlook

The future of the organic cotton market looks promising, as industries and consumers increasingly align with sustainability goals. Apparel will continue to dominate, but medical and packaging applications are expected to expand significantly. With growing investments in organic farming and government support in certain regions, supply challenges are likely to ease over time.

Furthermore, as global fashion brands commit to using organic and sustainable materials, the organic cotton market is set to become an integral part of the textile industry’s transformation. Technological advancements in farming and better certification practices will also help in bridging the gap between supply and demand.

The organic cotton market is no longer a niche—it is rapidly becoming mainstream. With an exceptional growth rate and rising global awareness about sustainability, organic cotton stands at the forefront of the textile industry’s green revolution. Although high costs and supply limitations pose challenges, innovation, investment, and consumer-driven demand are paving the way for a brighter, more sustainable future.

The global concrete admixtures market size was valued at USD 22.78 billion in 2024 and is set to expand steadily in the coming years. The market is forecast to increase from USD 24.90 billion in 2025 to nearly USD 42.90 billion by 2032, reflecting a robust CAGR of 8.9% over the forecast period. In 2024, Asia Pacific emerged as the leading region, accounting for 64.57% of the global market share. Meanwhile, the market in the United States is expected to witness notable growth, reaching approximately USD 3.08 billion by 2032, supported by the rising adoption of high-performance concrete solutions.

This upward trajectory reflects rising demand for improved construction materials that can withstand harsh environmental conditions, meet sustainability goals, and support the surge in global infrastructure development.

Market Overview and Growth Drivers

Concrete admixtures market are ingredients added to concrete before or during mixing to modify its properties. They enhance workability, strength, durability, and setting time, making concrete more versatile for diverse applications. The increasing adoption of water-reducing admixtures is a key driver of growth. These additives reduce water requirements without compromising strength, ensuring higher-quality concrete and cost efficiency.

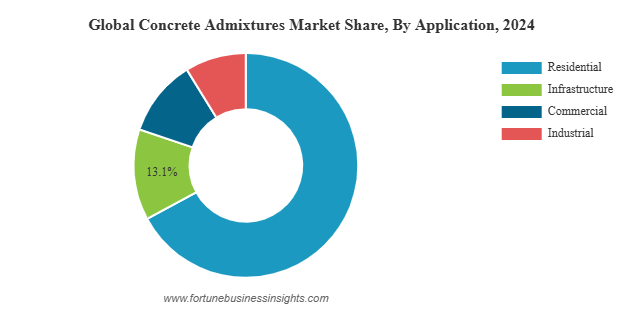

Urbanization, housing demand, and government investments in infrastructure are fueling rapid market expansion. The residential construction sector dominates consumption, with homeowners and developers alike seeking stronger, longer-lasting, and more sustainable structures. At the same time, infrastructure projects—ranging from highways and bridges to airports and railways—are accounting for a significant share of demand. In 2024, infrastructure applications are projected to represent about 13.1% of global consumption by volume.

List of Top Concrete Admixtures Companies:

- Buildtech Products (India)

- Sika AG (Switzerland)

- RAZON ENGINEERING COMPANY PRIVATE LIMITED (India)

- Flowcrete Group Ltd. (U.K.)

- CEMEX S.A.B. de C.V. (Mexico)

- BASF SE (Germany)

- GCP Applied Technologies (U.S.)

- RPM International Inc. (U.S.)

Segment Insights: Products and Applications

The market can be segmented by product type and application, each contributing uniquely to the industry’s momentum.

Product Trends

- Water-reducing admixtures remain the largest and most influential category. Their ability to reduce water demand while improving concrete strength and durability makes them indispensable in both residential and commercial projects.

- Other products such as retarding agents, accelerating admixtures, and air-entraining agents are also gaining traction, especially in regions where climate extremes necessitate better control over setting time and freeze-thaw resistance.

Application Trends

- Residential construction remains the largest application segment, supported by global housing demand, urban population growth, and easier access to housing credit.

- Infrastructure is the fastest-growing segment, with massive government-led projects creating demand for specialized admixtures that can deliver long-lasting performance under heavy loads and challenging conditions.

- Commercial construction also contributes significantly, particularly in developed economies where commercial real estate continues to expand.

Read More : https://www.fortunebusinessinsights.com/concrete-admixtures-market-102832

Regional Dynamics: Asia Pacific Leads the Way

The Asia Pacific region stands as the undisputed leader in the concrete admixtures market, commanding over 64.57% of global share in 2024. The market here is expanding rapidly, rising from USD 13.38 billion in 2023 to USD 14.71 billion in 2024, largely driven by construction booms in China, India, and Southeast Asia.

- China continues to be a powerhouse, supported by large-scale infrastructure investments and a strong focus on urban development. With a 13.3% share in 2024, China remains a cornerstone of the global market.

- India is seeing rapid growth as housing demand escalates, driven by population migration to urban areas and government-backed affordable housing initiatives.

- Southeast Asian nations are also contributing significantly, with smart city projects and infrastructure upgrades playing a crucial role.

Elsewhere, North America and Europe are also showing strong momentum. The United States market is forecast to reach USD 3.08 billion by 2032, as infrastructure rehabilitation, smart city development, and demand for high-performance concrete increase. In Germany and other European markets, sustainability regulations are encouraging the adoption of low-VOC and eco-friendly admixtures, signaling a move toward greener construction practices.

In Latin America, particularly Brazil and Mexico, government-backed infrastructure development programs are supporting market expansion. Meanwhile, the Middle East is witnessing robust demand, spurred by mega-projects such as Saudi Arabia’s NEOM and the UAE’s Vision 2030 initiatives, which are reshaping skylines with modern, technologically advanced infrastructure.

Key Industry Developments:

- November 2023: Sika AG announced that the group had expanded its concrete admixture capacity in the U.S. The company continues to invest in its polymer production at its Sealy site in the U.S. state of Texas. Sika’s latest move marks its second polymer investment in the state of Texas in just five years. The company requires polymers for chemical building blocks that are needed to produce Sika ViscoCrete, a high-performance, resource-saving concrete admixture. The company initiated this expansion to meet the growing demand for its products in the U.S. and Canada.

- June 2023: Fosroc India launched a state-of-the-art Concrete Lab in Chennai that will provide advanced building material testing facilities to developers, contractors, and other construction professionals.

Opportunities and Challenges Ahead

The market outlook for concrete admixtures is highly promising, but it also comes with challenges. Rising raw material prices and stringent regulations regarding chemical usage can increase production costs and affect supply chains. However, these challenges are being met with innovation. Leading manufacturers are focusing on developing eco-friendly, high-performance admixtures that align with sustainability goals and regulatory requirements.

Another key opportunity lies in emerging markets, where rapid industrialization and urbanization continue to fuel massive construction activity. Countries in Asia, Africa, and Latin America present significant untapped potential for admixture producers, especially those offering products tailored to local environmental and regulatory conditions.

Outlook

The global concrete admixtures market is set to nearly double in size by 2032, powered by strong demand across housing, infrastructure, and commercial construction. Asia Pacific will continue to dominate, but North America, Europe, and the Middle East are also poised for substantial growth, driven by sustainability initiatives, smart infrastructure projects, and regulatory shifts.

Concrete admixtures market may be small in proportion compared to cement or aggregates, but their impact is enormous. By improving performance, reducing costs, and enabling sustainable construction, they are shaping the future of the built environment. As the world moves toward greener cities and resilient infrastructure, admixtures will play an increasingly vital role in laying the foundation for growth and innovation.

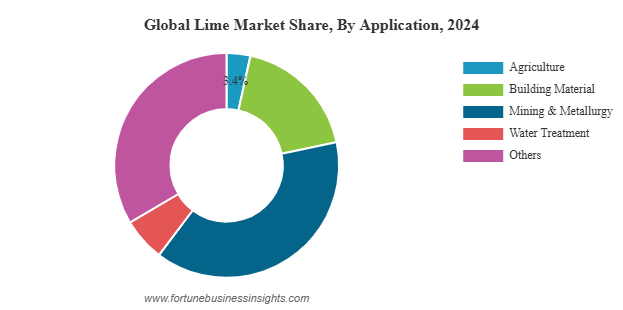

The global lime market size was valued at USD 46.68 billion in 2024 and is anticipated to expand from USD 47.40 billion in 2025 to nearly USD 56.64 billion by 2032, reflecting a compound annual growth rate (CAGR) of 2.6% during the forecast period. In 2024, Asia Pacific emerged as the leading region, accounting for 66.67% of the overall market share.

Market Dynamics and Trends

The lime market’s growth is being propelled by several converging trends:

- Infrastructure Development: Rapid urbanization, particularly in emerging economies, is fueling construction activity. This directly increases demand for lime in cement and building materials.

- Environmental Regulations: Countries like the U.S., China, and India are implementing stricter pollution control measures, boosting lime consumption in flue gas and wastewater treatment.

- Steel Industry Demand: With global steel demand projected to rise steadily, lime’s role as a flux ensures its continued necessity.

- Agricultural Needs: Population growth and the need for sustainable food production are increasing the use of lime to improve soil health and crop yields.

List Of Key Lime Companies Profiled

- Carmeuse (Belgium)

- Lhoist Group (Belgium)

- Graymont Limited (Canada)

- Mississippi Lime Company (U.S.)

- United States Lime & Minerals Inc. (U.S.)

- Afrimat (South Africa)

- Linwood Mining & Minerals Corporation (U.S.)

- Minerals Technologies, Inc. (U.S.)

- Cheney Lime & Cement Company (U.S.)

Key Applications

The versatility of lime is a cornerstone of its global demand. Among its most notable applications:

- Steel Industry: Lime acts as a flux in steelmaking, helping remove impurities such as silica, sulfur, and phosphorus. Its role in both basic oxygen and electric arc furnaces is indispensable.

- Construction: Lime is a vital ingredient in cement, mortar, and plaster. It improves workability, enhances durability, and supports eco-friendly building practices. With infrastructure and housing demand surging globally, lime’s importance in construction continues to grow.

- Agriculture: By neutralizing soil acidity and enriching calcium content, lime significantly improves soil health and crop productivity. This function is particularly vital in regions facing soil degradation.

- Environmental Applications: Lime is increasingly used in wastewater treatment and flue gas desulfurization. It efficiently removes pollutants such as lead, phosphorus, and sulfur dioxide, supporting global efforts to reduce industrial emissions.

Interestingly, lime’s use in building materials is projected to grow at a striking CAGR of over 2.6% during 2025–2032, underscoring the rising importance of construction and sustainable housing developments.

Regional Market Performance

- Asia Pacific: The Powerhouse

Asia Pacific dominates the lime market, commanding more than two-thirds of global revenue in 2024. This regional strength is largely driven by rapid industrialization and surging demand across steel, paper, chemical, and construction industries. China remains the largest contributor, owing to its leadership in global steel production. India and Japan are also significant players, with projections estimating their lime markets to surpass USD 0.75 million and USD 1.27 billion, respectively, by 2025. Strong infrastructure projects, rising urbanization, and strict environmental regulations in the region further fuel demand.

- Europe: Steady Growth Backed by Industry

Europe holds the second-largest share of the lime market. Valued at more than USD 8.32 billion in 2025, the region benefits from a strong presence of steel and automotive industries. Lime continues to serve as a critical material in steel refining, construction, and wastewater treatment across key economies such as Germany, France, and Italy. Moreover, Europe’s ambitious climate goals and emphasis on reducing carbon emissions are driving additional demand for lime in environmental applications, particularly in flue gas desulfurization.

- North America: Expanding with Infrastructure

North America, led by the United States, is forecasted to reach nearly USD 0.33 billion in lime market value by 2025. Demand is largely supported by infrastructure investments, water treatment initiatives, and the mining sector. Stringent regulations surrounding environmental safety and the growing push for sustainable building materials further support lime consumption in this region.

- Emerging Regions

Latin America and the Middle East & Africa present moderate but promising growth. Construction projects, oil and gas developments, and increasing steel consumption in countries like Brazil, South Africa, and the Gulf nations are laying the foundation for long-term opportunities. These regions are expected to gradually increase their market

Read More : https://www.fortunebusinessinsights.com/lime-market-104548

Key Industry Developments

- January 2024 – Mississippi Lime Company (MLC) has invested in constructing a state-of-the-art, sustainable kiln at its newly acquired lime operation in Bonne Terre, Missouri. The construction began in early 2024, and commissioning will be completed by 2026.

- September 2023 – Lohist Group announced its decision to expand its lime production capacity in Texas, U.S. The purpose of the production expansion was to establish the company’s business presence in the U.S. and maximize its revenue from the lime segment.

- September 2023 – Graymont Limited announced its plans to expand its business in Southeast Asia. For this, the company acquired Compact Energy, a major lime processing facility in Malaysia. Through this move, the company is expected to produce 600,000 tons of quicklime and 170,000 tons of hydrated lime annually.

- September 2023 – Carmeuse and Tallman Technologies Inc. announced a strategic partnership to enhance the lime injection offerings. Together with Carmeuse’s expertise in raw materials and lime handling and Coperion’s expertise in dense phase conveyance, Tallman Technologies will bring design and engineering expertise in supersonic injection to enable Carmeuse to offer a complete lime injection system from truck offloading.

Competitive Landscape

The lime market is highly competitive, with several global and regional players shaping its direction. Leading companies include:

- Lhoist Group

- Graymont Limited

- Mississippi Lime Company

- Carmeuse

- United States Lime & Minerals Inc.

- Afrimat

- Sigma Minerals Ltd.

These companies are actively expanding their production capacities, investing in sustainable practices, and exploring mergers and acquisitions to strengthen their market presence. For example, Mississippi Lime Company enhanced its capabilities by acquiring Valley Minerals, a producer of dolomitic quicklime in Missouri. Such strategic moves highlight the ongoing consolidation and growth within the sector.

Outlook

Looking ahead, the lime market is poised for steady expansion. Its crucial role across diverse industries ensures consistent demand, while global megatrends such as urbanization, sustainability, and food security create new avenues for growth. By 2032, with a projected market value of more than USD 56.64 billion, lime will continue to prove itself as a foundational material for modern economies.

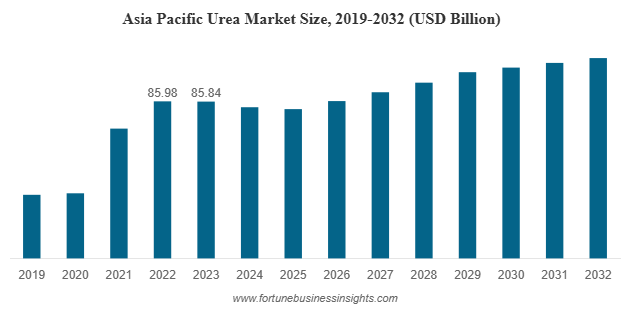

The global urea market size was valued at USD 128.92 billion in 2023 and is anticipated to expand from USD 123.95 billion in 2024 to USD 160.67 billion by 2032, reflecting a CAGR of 2.2% over the forecast period. Asia Pacific emerged as the leading region, accounting for 66.58% of the market share in 2023. Meanwhile, the U.S. market is expected to witness substantial growth, projected to reach USD 14.40 billion by 2032, fueled by the rising demand for nitrogen-based fertilizers to enhance crop production.

The Role of Urea in Modern Agriculture

Urea market is the backbone of modern farming practices due to its high nitrogen content, which is crucial for plant growth and soil fertility. Farmers across the world rely on urea market to boost crop yields, particularly in staple crops such as rice, wheat, maize, and other cereals that form the foundation of food security.

In 2023, agriculture dominated the application segment of the urea market, reinforcing its status as the key driver of demand. As global population growth accelerates, the pressure to increase agricultural productivity has never been greater. Fertilizer efficiency and affordability make urea the preferred choice for large-scale farming, ensuring it remains the cornerstone of the sector.

List of Top Urea Companies:

- SABIC (Saudi Arabia)

- Qatar Fertilizer Company (Qatar)

- EuroChem (Switzerland)

- Yara International ASA (Norway)

- Nutrien AG (Canada)

- OCI N.V. (Netherlands)

- Acron Group (Russia)

- CF Industries Holdings (U.S.)

Key Market Drivers

Several factors are shaping the growth trajectory of the urea market:

- Population Growth and Food Security

Rising global population continues to drive demand for staple crops, reinforcing the importance of urea in boosting agricultural productivity. - Government Policies and Subsidies

Many countries, particularly in Asia-Pacific, support fertilizer consumption through subsidies and incentives, ensuring steady demand for urea. - Industrial Diversification

Expanding use of urea in industries such as resins, adhesives, plastics, and emissions control is diversifying the market beyond agriculture. - Technological Advancements

Precision agriculture and improved fertilizer application techniques are enhancing efficiency, ensuring that urea remains a critical tool for farmers.

Industrial Applications of Urea

While agriculture accounts for the largest share, urea’s role in industrial applications is equally important. Urea is widely used in the manufacture of melamine, adhesives, plastics, and resins. It also serves as a raw material in the production of urea-formaldehyde resins, which are employed in particleboard, plywood, and other wood products.

Additionally, the chemical is gaining prominence in environmental applications, such as diesel exhaust fluid (DEF), which helps reduce harmful nitrogen oxide emissions from vehicles. With increasing emphasis on sustainability and environmental compliance, the demand for urea in these emerging applications is expected to remain strong.

Asia-Pacific The Growth Powerhouse

Asia-Pacific leads the global urea market, contributing 66.58% of the total share in 2023. Several factors explain the region’s dominance. Population growth, coupled with rapid urbanization, continues to fuel demand for food, leading to an increase in agricultural activities. Countries like China and India are at the forefront of this growth, with government support and favorable policies encouraging fertilizer consumption to enhance food security.

Beyond agriculture, Asia-Pacific is also witnessing rising industrial consumption of urea. The chemical is used in resins, adhesives, coatings, and as a feedstock in various industries. This dual role—supporting both farming and industrial needs—solidifies the region as the epicenter of global urea production and consumption.

The U.S. Market Emerging Opportunities

Although smaller in comparison to Asia-Pacific, the U.S. urea market is set to witness notable growth. By 2032, the market is expected to reach USD 14.40 billion, driven by rising demand for nitrogen-based fertilizers to support crop production. Increasing emphasis on agricultural sustainability, efficient farming techniques, and productivity enhancement are expected to further bolster the role of urea in the U.S. farming landscape.

Domestic production and imports are both likely to grow as farmers seek reliable and cost-effective fertilizer solutions. The U.S. also benefits from technological advancements in precision farming, which may influence the efficient use of urea and create additional opportunities for innovation in the sector.

Read More : https://www.fortunebusinessinsights.com/urea-market-106850

Challenges to Growth

Despite its widespread use, the urea market faces several challenges. Overuse of nitrogen fertilizers can lead to soil degradation, water pollution, and greenhouse gas emissions. Environmental concerns and regulatory restrictions are pushing the industry to adopt more sustainable practices.

Additionally, fluctuating natural gas prices—since urea is produced using natural gas as a feedstock—can impact production costs and profitability. Market participants must balance affordability with sustainable production to maintain growth momentum.

Key Industry Developments

- March 2023: SABIC announced that it is collaborating with two U.S.-based companies, BiOWiSH Technologies and ADM, to supply Bio-Enhanced Urea to farmers for 2023’s growing season to support sustainable agriculture.

- June 2022: Nutrien Ag announced that it is increasing its fertilizer production capability. This move is expected to enable the company to respond to changes in global energy, agriculture, and fertilizer markets.

- March 2022: EuroChem announced that it has entered into exclusive negotiations to acquire the nitrogen business of the Borealis group after having submitted a binding offer.

- March 2022: Egypt-based Misr Fertilizers Production Company (MOPCO) announced plans to improve its overall annual carbamide production capacity to 70 kilo tons. The company also announced investment to build a new melamine plant. With this investment, MOPCO aimed to strengthen its position in Egypt and overseas markets.

The Road Ahead

Looking toward 2032, the urea market is expected to grow steadily, reaching nearly USD 160.67 billion. Agriculture will continue to dominate demand, but industrial applications and environmental uses are likely to gain more prominence. Asia-Pacific will retain its position as the global leader, while the U.S. and other regions will see incremental opportunities driven by food demand and industrial expansion.

Stakeholders—from fertilizer manufacturers and farmers to industrial users and policymakers—must collaborate to ensure that urea’s potential is harnessed sustainably. Investment in research and development, improved application methods, and greener production techniques will play a pivotal role in shaping the future of this market.

Outlook

The urea market is a vital component of the global economy, serving as both a cornerstone of agricultural productivity and a versatile material for industrial applications. With a projected CAGR of 2.2% from 2024 to 2032, the market’s growth reflects the essential role urea plays in feeding the world and supporting diverse industries.

As the world grapples with the twin challenges of feeding a growing population and ensuring environmental sustainability, urea will remain at the heart of solutions. Its journey from the farm to the factory floor highlights not only its versatility but also its enduring relevance in shaping the future of agriculture and industry.

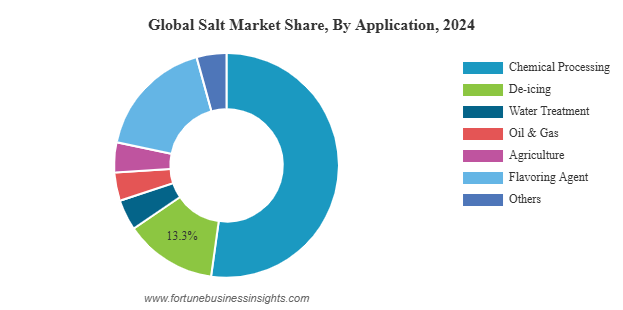

The global salt market size was valued at USD 25.98 billion in 2024 and is expected to expand from USD 26.92 billion in 2025 to USD 36.12 billion by 2032, reflecting a steady CAGR of 4.29% throughout the forecast period. In 2024, Asia Pacific emerged as the leading region, capturing a 46.23% share of the market. Meanwhile, the U.S. salt market is projected to reach USD 4.91 billion by 2032, supported by rising demand for food-grade salt as well as increased use in industrial processes and de-icing. Key industry players include Cargill Salt, Compass Minerals International, Inc., INEOS Enterprises, and American Rock Salt, all of whom play a vital role in shaping the competitive landscape.

Salt is one of the world’s most essential commodities, deeply rooted in human civilization for centuries. From preserving food and seasoning meals to powering chemical industries and ensuring road safety during winter, salt continues to prove its versatility in the modern world. While it may appear to be a simple mineral, the global salt market tells a story of growth, innovation, and evolving demand across multiple sectors.

Global Market Dynamics

The salt market is not confined to kitchen tables. In fact, the largest share of global demand comes from industries, with chemical processing leading the way. Salt is an indispensable raw material in the production of chlorine, caustic soda, and soda ash—all of which serve as critical inputs in the manufacturing of plastics, glass, textiles, paper, and detergents. The continued expansion of industrial applications is expected to sustain the upward momentum of the market over the forecast period.

At the same time, the food and beverage sector continues to be a strong driver. Salt market remains a staple in diets worldwide, both as a flavor enhancer and a preservative. The rising popularity of specialty salts such as sea salt, Himalayan pink salt, and smoked salts reflects shifting consumer preferences toward premium, natural, and gourmet food products.

List Of Key Salt Companies Profiled

- American Rock Salt (U.S.)

- Cargill Salt (U.S.)

- Compass Minerals International, Inc. (U.S.)

- INEOS Enterprises Salt (U.K.)

- K+S Aktiengesellchaft (Germany)

- China National Salt Industry (China)

- Qemetica (Poland)

- US Salt LLC (U.S.)

- Ahir Salt Industries (India)

- GHCL Limited (India)

Growth Drivers

Several factors are fueling the expansion of the global salt market:

- Industrial Demand: The chlorine-alkali industry remains one of the largest consumers of salt. As demand for plastics, detergents, and glass continues to grow globally, so too does the requirement for salt as a key raw material.

- Food and Nutrition Trends: Beyond basic seasoning, consumers are gravitating toward natural and specialty salts. The wellness movement has spurred interest in minimally processed sea salts, Himalayan pink salt, and other varieties perceived as healthier alternatives.

- Infrastructure and Safety: In colder countries, rock salt remains vital for de-icing roads, sidewalks, and airport runways. The ongoing need for public safety during winter ensures consistent demand for this segment.

- Population Growth: With rising populations worldwide, especially in developing regions, demand for processed and packaged food continues to rise—directly boosting the need for salt as both a preservative and a flavoring agent.

Read More : https://www.fortunebusinessinsights.com/salt-market-103011

Market Segmentation

The salt market can be segmented in several ways, highlighting the diversity of its applications:

- By Type: Rock salt leads the market, particularly in de-icing and chemical processing. Other forms, including solar salt and vacuum salt, also hold importance for different industries.

- By Source: Salt extracted from mines accounts for the largest share, given the accessibility of underground reserves and the efficiency of mining operations. Sea salt production, while smaller in volume, caters to niche markets and health-conscious consumers.

- By Application: Chemical processing dominates global demand, followed by food-grade uses, water treatment, and de-icing. While de-icing may seem seasonal, it contributes significantly to annual salt consumption in colder climates.

Regional Highlights

- Asia-Pacific: The Global Leader

The Asia-Pacific region dominates the global salt market, accounting for nearly half of total revenue in 2024. Countries like China, India, and Australia are at the forefront, benefiting from vast natural reserves, growing populations, and strong industrial demand. Expanding chemical industries in China and India, in particular, are creating sustained demand for large volumes of salt, while the food processing sector continues to grow alongside urbanization and changing dietary habits.

- United States: A Key Growth Market

In the U.S., the salt market is projected to increase around USD 4.91 billion by 2032. This growth is driven by demand across three primary areas: food-grade salt, industrial applications, and de-icing. Every winter, millions of tons of rock salt are spread on American roads to improve safety during snow and ice storms. At the same time, the country’s robust food industry ensures consistent demand for table and processed salts.

- Europe and Beyond

European markets are also significant, particularly in countries with cold winters where road de-icing is essential. Meanwhile, the Middle East and Africa show potential growth due to ongoing industrial developments and the availability of abundant salt deposits.

Key Industry Developments

- December 2024: GHCL, a key salt manufacturer and part of the Dalmia Group, invested USD 40.44 million to create a salt field in Kutch. The Zara Zumara Salt Field will be developed in the Jara area of Kutch.

- May 2023: Cargill’s salt business signed an agreement with CIECH Group, a leading supplier of evaporated salt products. Through this agreement, Cargill extended its range of specialty and evaporated food salt solutions for European food manufacturers.

- April 2022: Tata Salt, one of India's most trusted brands and pioneers of the salt iodization movement, launched Tata Salt Immuno. This innovative product, a first of its kind in the Indian edible salt segment. Along with mandated iodization, the product has added zinc, which is known to support a healthy immune system.

Challenges and Considerations

Despite its steady growth, the salt market faces some challenges. Health concerns related to excessive sodium intake have prompted governments and health organizations to encourage reduced salt consumption in diets. This could slightly impact demand in the food sector, particularly in developed countries.

Additionally, environmental concerns surrounding salt mining and large-scale de-icing are prompting industries to explore more sustainable solutions. Nevertheless, these challenges also create opportunities for innovation, such as low-sodium salt alternatives and eco-friendly de-icing products.

The Future of the Salt Market

Looking ahead, the salt market will continue to evolve in response to both traditional and emerging demands. Industrial uses will remain a cornerstone, while consumer trends toward specialty and premium salts will add new dimensions of growth. At the same time, technological advancements in mining, production, and sustainability practices are likely to shape the industry’s trajectory over the next decade.

What remains clear is that salt market an age-old mineral once valued as “white gold”—still holds immense importance in shaping modern economies and daily life. From the roads we drive on in winter to the food we eat and the products we use, salt remains as relevant as ever, with a global market poised for steady expansion in the years to come.

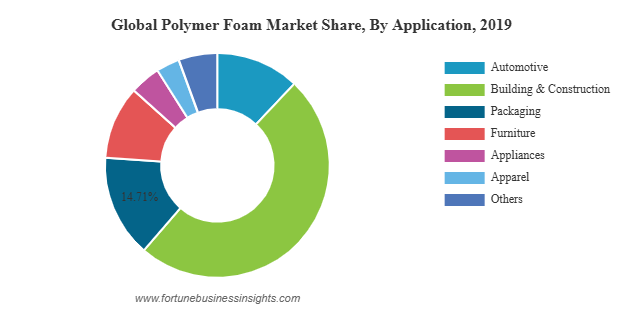

The global polymer foam market size was valued at USD 114.88 billion in 2019 and is expected to grow to USD 157.63 billion by 2027, registering a CAGR of 7.73% over the forecast period. In 2019, Asia Pacific led the market, accounting for a 43.84% share. Additionally, the U.S. polymer foam market is anticipated to reach USD 23.49 billion by 2027, driven by its widespread application in furniture, automotive, and construction insulation.

Market Overview

Polymer foam market are versatile materials widely recognized for their combination of strength and low density. They are used in applications where cushioning, thermal insulation, soundproofing, and impact absorption are critical. The material’s adaptability allows it to be used in a broad range of products such as mattresses, seating cushions, insulation panels, protective packaging, and automotive interiors.

The manufacturing of polymer foam market involves various techniques, including blow molding, injection molding, extrusion, and slab-stock pouring. Each method offers specific advantages, such as uniform density, precise shapes, and the ability to produce complex designs. Additionally, quality standards and testing protocols ensure that polymer foams meet safety, durability, and performance requirements across industries.

List Of Key Companies Covered:

- Sealed Air (U.S.)

- Arkema (France)

- Armacell International S.A. (Germany)

- Borealis AG (Austria)

- Polymer Technologies, Inc. (U.S.)

- Zotefoams plc (UK)

- Synthos (Poland)

- Sekisui Alveo (Switzerland)

- BASF SE (Germany)

- Total SA (France)

Market Segmentation

By Type:

Polyurethane (PU) foam dominates the polymer foam market due to its extensive application in bedding, furniture, insulation, and automotive sectors. PU foam is highly valued for its softness, comfort, resilience, and ability to conform to ergonomic designs. Other types of polymer foams include polystyrene (PS) foam, polyethylene (PE) foam, and PVC foam. Polystyrene foam is widely used for packaging and insulation due to its excellent thermal insulation and lightweight nature. Polyethylene foam is used primarily in protective packaging and automotive parts, while PVC foam finds applications in construction and decorative materials.

By Application:

The polymer foam market is driven by key applications in automotive, construction, packaging, furniture, appliances, and apparel industries. In the automotive sector, polymer foams are used for seat cushioning, headrests, door panels, and insulation materials, contributing to vehicle comfort and safety while reducing overall weight. In construction, polymer foams serve as thermal and acoustic insulation in walls, roofing, and flooring systems, helping buildings achieve energy efficiency and improved occupant comfort. Packaging applications benefit from the shock-absorbing and protective properties of polymer foams, especially in the e-commerce and electronics sectors. Furniture and bedding industries rely on polymer foams to provide comfort, durability, and ergonomic support in mattresses, cushions, and upholstered furniture.

By Region:

Asia Pacific is the largest regional market for polymer foams, accounting for approximately 43.84% of the market share in 2019. The growth in this region is fueled by rapid urbanization, increasing disposable incomes, and a boom in construction and manufacturing activities, particularly in countries such as China, India, and Japan. North America and Europe are also significant markets, driven by technological advancements, high automotive production, and demand for premium construction materials.

Read More : https://www.fortunebusinessinsights.com/industry-reports/polymer-foam-market-101698

Key Industry Developments

- August 2019: Sheela Foam Limited, largest manufacturer of mattresses and foam based in India, acquired Interplasp SL, a Spanish Company, which has an annual production of 11,000 tons (total capacity 22,000 tons) of polyurethane foam for bedding and furniture applications.

- March 2019: Sika AG, a specialty chemical manufacturer of bonding, damping, sealing, reinforcing solutions for automotive and construction industries, acquired Belineco LLC, a Belarus-based producer of polyurethane foam systems. With this acquisition, Sika is further expected to develop its technology to manufacture polyurethane foams.

- July 2019: Huntington Solutions, LLC, a North American provider of protective packaging solutions and energy management components, acquired Texas Foam, a company based in Bastrop, Texas, to increase and broaden its production capabilities.

Key Growth Drivers

Construction and Urbanization:

Rapid urbanization and infrastructure development in emerging economies have significantly boosted the demand for polymer foams. The material’s use in thermal and acoustic insulation contributes to energy-efficient buildings, which is a growing priority in construction projects worldwide.

Automotive Industry:

The global automotive sector increasingly seeks lightweight materials to improve fuel efficiency, reduce emissions, and enhance passenger safety. Polymer foam market, particularly polyurethane foams, are widely used in automotive interiors, seating, and structural components, creating substantial growth opportunities for the market.

Packaging Solutions:

The rise of e-commerce and the need for protective packaging have driven the demand for polymer foams in shipping and transportation. Shock-absorbing foams protect delicate items such as electronics, glassware, and consumer goods, reducing damage during transit.

Challenges

Environmental Concerns:

The production and disposal of certain polymer foams can pose environmental challenges, especially in the case of non-biodegradable materials. Growing awareness about environmental sustainability is encouraging manufacturers to explore eco-friendly alternatives and recycling initiatives.

Regulatory Compliance:

Manufacturers must comply with stringent regulations related to material safety, flammability, and environmental impact. Adhering to these standards may increase production costs and require continuous innovation in material formulation and manufacturing processes.

Future Outlook

The polymer foam market is expected to experience steady growth in the coming years due to ongoing technological advancements and increasing demand from end-use industries. Innovation in foam manufacturing techniques and the development of eco-friendly and biodegradable foam alternatives are likely to drive market expansion further. In addition, the rising trend of smart and multifunctional foams, which provide additional features such as fire resistance, thermal regulation, or antimicrobial properties, is expected to create new opportunities for market players.

Overall, the global polymer foam market is poised for robust growth as industries continue to prioritize lightweight, durable, and efficient materials. With increasing urbanization, technological innovation, and consumer demand for comfort and safety, polymer foams will remain a critical material across multiple sectors for years to come.