Aluminum Composite Panels Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-19

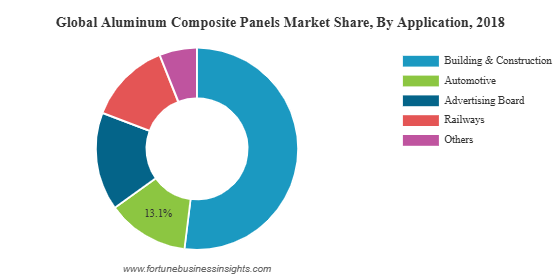

The global aluminum composite panels market was valued at USD 5.33 billion in 2018 and is expected to reach USD 8.71 billion by 2026, registering a CAGR of 6.1% over the forecast period. Asia Pacific led the market in 2018 with a 39.23% share, supported by rapid urbanization and infrastructure development. In the United States, the market is projected to expand notably, reaching USD 2.41 billion by 2032, driven by supportive policies and initiatives aimed at strengthening infrastructure across North America.

The global construction and infrastructure landscape has been evolving rapidly with increasing emphasis on modern architecture, sustainable design, and energy-efficient materials. Among the materials transforming the building and design industry, Aluminum Composite Panels (ACPs) stand out for their versatility, durability, and cost-effectiveness. These panels consist of two thin aluminum sheets bonded to a non-aluminum core, typically polyethylene or fire-retardant material, creating a lightweight yet strong solution for exterior and interior applications. With their adaptability in cladding, façades, signage, and even the automotive industry, ACPs have become a cornerstone of contemporary construction.

List Of Key Companies Profiled In Aluminum Composite Panels Market:

- 3A Composites GmbH

- Arconic

- Mitsubishi Chemical Corporation

- Hyundai Alcomax Co.,Ltd.

- Fairfield Metal LLC

- Jyi Shyang Industrial Co., Ltd.

- ALUMAX INDUSTRIAL CO., LTD.

- Yatai Industrial Group Co., Ltd.

- Shanghai Huayuan New Composite Materials Co., Ltd.

- Guangzhou Xinghe Aluminum Composite Panel Co., Ltd.

Market Drivers

- Rapid Urbanization and Infrastructure Growth

The increasing pace of urbanization, especially in Asia-Pacific, has created massive demand for affordable housing, commercial complexes, and modern public infrastructure. Governments in countries like China, India, and Indonesia are heavily investing in smart cities and urban housing schemes, directly boosting ACP demand. The material’s ability to provide weather resistance, insulation, and design flexibility makes it ideal for large-scale projects.

- Rising Popularity of Modern Building Aesthetics

Architectural trends are shifting toward sleek, innovative, and energy-efficient designs. ACPs offer endless possibilities in color, texture, and finish—ranging from metallic to stone or wood-like appearances—allowing architects to balance functionality with creativity. Their lightweight property also makes them easier to install compared to traditional materials.

- Expanding Automotive Applications

While construction is the dominant sector, ACPs are also making significant inroads into the automotive industry, where they accounted for about 13.1% of usage in 2018. Automakers are adopting ACPs for insulation, noise reduction, padding, and stylish body panels in vehicles, buses, and vans. With the rise of electric vehicles (EVs), demand for lightweight, heat-resistant, and customizable materials is expected to further accelerate ACP adoption.

- Growing Signage and Advertising Industry

From billboards and hoardings to transit advertising, ACPs are widely used in signage due to their durability, smooth finish, and flexibility. With expanding retail and advertising industries worldwide, ACP demand in signage and branding applications is projected to rise consistently.

Read More : https://www.fortunebusinessinsights.com/aluminum-composite-panels-market-102304

Regional Insights

- Asia-Pacific – Market Leader

In 2018, Asia-Pacific dominated the global ACP market with nearly 39.2% share. Strong construction growth, infrastructure projects, and rising demand for affordable urban housing are the key drivers. China and India lead the region, supported by rapid economic development, government-backed smart city projects, and expanding commercial real estate. Southeast Asian countries like Vietnam and Indonesia are also emerging as growth hotspots due to large-scale urban expansion.

- North America

The United States remains a major market, with ACP demand projected to reach USD 2.41 billion by 2032. Growth is driven by infrastructure modernization, commercial real estate projects, and rising adoption of ACPs in the automotive and electric vehicle industries. Strict building codes are also pushing the shift toward fire-safe ACP variants.

- Europe

In Europe, countries such as Germany, France, and the United Kingdom are seeing strong adoption of ACPs in modern office buildings, airports, and renovation projects. The push for green buildings and eco-friendly materials is particularly boosting demand for advanced, recyclable ACP products.

- Other Regions

In Japan, demand is supported by eco-friendly and durable construction needs, especially in urban centers. Latin America, including Brazil and Chile, is experiencing growth driven by expanding infrastructure and real estate development. Meanwhile, Middle East & Africa are witnessing demand from mega construction projects, hospitality infrastructure, and urban expansion plans.

Key Industry Developments:

July 2017 – Fairview Architectural acquired the Stryum business, an intelligent non-combustible aluminum cladding system, from Vitekk Industries. The company includes a variety of high-quality aluminum plate façade panels designed to provide durability and sustainability, complimenting Fairview's current portfolio of cladding solutions, including high-density cement fibre, natural stone, terracotta tiles and the leading non-combustible composite aluminum frame.

Market Challenges

Despite their numerous benefits, ACPs face certain challenges that may hinder growth. Maintenance and repair remain key concerns. If a panel is damaged, it is difficult to patch or replace without affecting the aesthetics of the entire façade. This adds to lifecycle costs for building owners. Additionally, environmental concerns regarding polyethylene-core ACPs, particularly their fire-safety issues, have led to stricter regulations in several countries. Manufacturers are therefore shifting toward fire-retardant and eco-friendly core materials, which are slightly costlier but offer long-term benefits.

Future Outlook

The ACP market outlook is highly promising, with several trends shaping its future:

- Sustainability focus: Eco-friendly and fire-retardant ACPs will gain greater market acceptance as regulations tighten and environmental awareness rises.

- Customization and design innovation: Manufacturers are investing in advanced coatings, digital printing, and smart surface technologies to meet evolving architectural needs.

- Automotive growth: As electric and hybrid vehicles demand lighter materials, ACPs will see increasing adoption beyond construction.

- Regional expansion: Emerging economies in Asia-Pacific, Latin America, and Africa will continue to dominate growth due to urbanization and infrastructure investments.

The aluminum composite panels market is at the crossroads of innovation and necessity. As cities grow taller, vehicles become lighter, and advertising becomes more dynamic, ACPs are expected to remain a material of choice across multiple industries. With their unique blend of durability, aesthetic versatility, and cost-effectiveness, ACPs are not just building materials but enablers of modern design and sustainable development.

By 2032, as manufacturers continue to enhance safety standards and embrace eco-friendly innovations, the global ACP market will be positioned as a critical pillar in construction, transportation, and design industries worldwide.

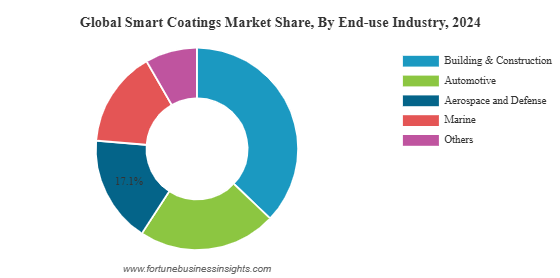

The global smart coatings market size was valued at USD 7.17 billion in 2024. It is projected to grow from USD 8.34 billion in 2025 to USD 26.15 billion by 2032 at a CAGR of 17.7% during the forecast period of 2025-2032. Asia Pacific dominated the smart coatings market with a market share of 45.33% in 2024.

Market Size and Growth Potential

Smart coatings market have emerged as one of the most innovative and high-potential materials in the global chemical and manufacturing industries. Unlike conventional coatings that serve only as protective layers, smart coatings are engineered to respond to external stimuli such as temperature, pressure, light, or electrical signals. These intelligent coatings not only protect surfaces but also provide additional functionalities like self-healing, anti-corrosion, anti-microbial, self-cleaning, and energy-saving properties.

With applications expanding across sectors including automotive, aerospace, construction, electronics, and healthcare, the global smart coatings market is poised for rapid growth. As industries increasingly seek sustainable, efficient, and long-lasting solutions, smart coatings are gaining attention as the future of surface protection and performance enhancement.

List Of Key Smart Coating Companies Profiled

- 3M (U.S.)

- AkzoNobel N.V. (Netherlands)

- Axalta Coating Systems LLC (U.S.)

- DuPont (U.S.)

- Hempel AS (Denmark)

- Jotun Group (Norway)

- NEI Corporation (U.S.)

- PPG Industries, Inc. (U.S.)

- RPM International Inc. (U.S.)

- The Sherwin-Williams Company (U.S.)

Key Drivers of Market Growth

- Superior Functional Properties

Smart coatings market provide unique capabilities that set them apart from conventional coatings. Self-healing coatings, for instance, contain microcapsules that release repair agents when damage occurs, sealing cracks automatically. Anti-icing coatings prevent ice buildup on wind turbines, aircraft wings, and power lines, reducing energy waste and operational risks. Stimuli-responsive coatings like thermochromic glass adjust transparency depending on sunlight exposure, significantly improving energy efficiency in buildings. These advanced features are driving strong adoption across industries.

- Rising Demand for Corrosion Resistance

Corrosion is a major concern in industries such as oil and gas, marine, automotive, and aerospace. The ability of smart coatings to resist corrosion and extend the lifespan of assets is a key growth factor. As environmental regulations tighten and the cost of equipment maintenance continues to rise, industries are turning to corrosion-resistant smart coatings to minimize downtime and reduce overall expenses.

- Infrastructure Development and Urbanization

The surge in urbanization and infrastructure investments worldwide is also boosting the demand for advanced coatings. Modern construction projects increasingly require self-cleaning, heat-reflective, and environmentally friendly coatings for facades, windows, and other surfaces. These coatings help lower energy consumption while reducing maintenance needs, aligning with global trends toward sustainability and smart cities.

Read More : https://www.fortunebusinessinsights.com/smart-coatings-market-113374

Challenges Restraining Market Expansion

While the smart coatings market is growing rapidly, it also faces a few challenges:

- High Costs of Raw Materials: Smart coatings market often rely on advanced raw materials such as nanomaterials, rare-earth elements, and specialty polymers. Their high costs and complex manufacturing processes limit adoption, especially in small and medium-scale industries.

- Durability Issues: Ensuring long-term performance under real-world conditions such as UV exposure, extreme temperatures, and mechanical wear is a challenge for manufacturers. Continuous R&D is essential to improve the resilience of smart coatings.

- Limited Awareness in Emerging Markets: In some developing regions, the lack of awareness about smart coatings’ benefits compared to conventional alternatives still holds back large-scale adoption.

Innovation and Future Opportunities

Ongoing research and development are paving the way for exciting opportunities in the smart coatings market:

- Self-Healing Polymers: Advanced coatings that use polymers activated by light or heat to repair themselves are expected to gain traction in automotive and aerospace applications.

- Antimicrobial Coatings: With growing concerns about hygiene and infection control, antimicrobial smart coatings are becoming increasingly relevant in healthcare, food processing, and consumer electronics.

- IoT-Integrated Coatings: Future smart coatings market may be embedded with sensors capable of monitoring structural health, corrosion, or environmental conditions, providing real-time data to users.

- Sustainability Focus: Eco-friendly coatings with low volatile organic compounds (VOCs) and recyclable materials are gaining attention as industries shift toward greener solutions.

Key Industry Developments

- July 2024 – AkzoNobel expanded its portfolio with Resicoat EV powder coatings, designed for electric vehicle components to enhance insulation, corrosion resistance, and thermal management.

- November 2023 – Covestro AG launched Impranil CQ DLU, a bio-based polyurethane dispersion with 34% plant-derived carbon, targeting sports, automotive, and technical textiles. This replaces petroleum-based alternatives while maintaining durability.

Regional Insights

- Asia Pacific: Leads the global smart coatings market due to strong industrial growth, especially in construction, automotive, and electronics. Government initiatives supporting green buildings and sustainable materials further accelerate adoption.

- North America: Strong presence of leading manufacturers and significant demand from aerospace, defense, and healthcare industries drive growth.

- Europe: Increasing regulatory pressure on environmental safety and sustainability fuels the demand for eco-friendly smart coatings. Countries like Germany, France, and the U.K. are key markets.

- Middle East & Africa: Rising investments in infrastructure and oil & gas projects open opportunities for corrosion-resistant and self-healing coatings.

Outlook

The global smart coatings market is on the verge of a transformation, fueled by technological advancements, sustainability needs, and growing demand across diverse industries. From reducing maintenance costs in construction to enhancing safety in aerospace and improving energy efficiency in buildings, smart coatings are redefining how we protect and optimize surfaces.

As research deepens and manufacturing costs decline, smart coatings will become more accessible, unlocking their potential in even more sectors. With a forecast CAGR of 17.7% through 2032, the future of this market promises groundbreaking innovations, making it a key pillar in the evolution of modern materials science.

Carbon Fiber Reinforced Plastics Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-18

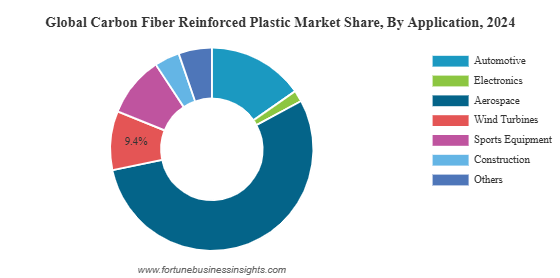

The global carbon fiber reinforced plastic (CFRP) market was valued at USD 18.92 billion in 2024 and is expected to increase from USD 20.72 billion in 2025 to USD 38.02 billion by 2032, registering a CAGR of 9.1% during the forecast period. Asia Pacific led the market in 2024, holding a 34.36% share.

Market Overview and Growth Outlook

The global demand for advanced materials has been rising steadily as industries push toward higher performance, efficiency, and sustainability. Among these materials, Carbon Fiber-Reinforced Plastics (CFRPs) market have emerged as a game changer. Known for their exceptional strength-to-weight ratio, corrosion resistance, and versatility, CFRPs are increasingly being adopted across aerospace, automotive, wind energy, construction, and sports equipment industries. With global emphasis on lightweighting, clean energy, and high-performance engineering, the CFRP market is projected to witness robust growth in the coming years.

This upward trajectory is primarily driven by surging demand in aerospace and defense, where weight reduction directly translates to fuel savings and reduced emissions, and in the automotive sector, where electric vehicles (EVs) are transforming material choices for lightweight, efficient designs. Additionally, the wind energy industry is increasingly utilizing CFRPs for turbine blades, adding momentum to market growth.

List Of Key Market Players Profiled In The Report

- Hexcel Corporation (U.S.)

- TORAY INDUSTRIES, INC. (Japan)

- SGL Carbon (Germany)

- Mitsubishi Chemical Group Corporation. (Japan)

- TEIJIN LIMITED. (Japan)

- Solvay (Belgium)

- Formosa Plastics (Taiwan)

- DowAksa (Turkey)

- Zhongfu Carbon Fiber Core Cable Technology Co., Ltd (China)

- HS HYOSUNG ADVANCED MATERIALS (South Korea)

Market Drivers

- Aerospace Demand: CFRPs market are a critical material in aircraft design, helping reduce weight and fuel consumption. Every kilogram saved translates to lower operating costs and reduced emissions, aligning with aviation’s sustainability goals.

- Electric Vehicle Revolution: With governments imposing strict emission standards, automakers are adopting CFRPs market to make lighter, more efficient electric vehicles. Reducing vehicle weight directly extends battery life and driving range, giving CFRPs market a central role in the EV era.

- Wind Energy Growth: The renewable energy sector, particularly wind energy, is a major driver. CFRP-based blades enable longer, more durable turbine designs that generate greater power efficiency.

- Material Innovation: Advances in manufacturing, such as automated fiber placement and rapid-curing resins, are making CFRPs market more cost-efficient and accessible, accelerating adoption across industries.

Regional Leadership

Asia Pacific dominates the global CFRP market, holding a market share of over 34% in 2024. The region’s value increased from USD 5.88 billion in 2023 to USD 6.50 billion in 2024. This leadership is largely attributed to China, which continues to be at the forefront of both production and application. The country’s rapid deployment of wind turbines has significantly boosted CFRP market demand, while its booming automotive and aerospace industries further drive consumption.

Beyond China, countries like Japan and South Korea are heavily investing in advanced composites to strengthen their presence in aerospace and automotive manufacturing. Europe follows closely, with Germany, France, and the U.K. spearheading CFRP market adoption in luxury automotive, aviation, and industrial applications. Meanwhile, North America continues to demonstrate strong growth, led by the United States, where aerospace giants and automotive innovators are pushing material innovation.

Read More : https://www.fortunebusinessinsights.com/carbon-fiber-reinforced-plastics-cfrps-market-110101

Key Market Segments

The CFRP market can be segmented by type, resin, and application:

- By Type: PAN-based CFRP market dominates due to its superior tensile strength, durability, and performance characteristics, making it suitable for aerospace and automotive applications. Pitch-based CFRP market, while more expensive, finds niche usage in high-end structural and industrial components.

- By Resin: Thermosetting resins, especially epoxy, continue to lead the market. These resins provide excellent stiffness, heat resistance, and structural stability, making them the preferred choice in aerospace and wind energy. Thermoplastic resins are gaining traction due to their recyclability and faster processing cycles.

- By Application: Aerospace and defense remain the largest segment, followed by automotive and transportation. Wind energy has emerged as one of the fastest-growing application areas, with turbine manufacturers increasingly relying on CFRPs market for stronger, lighter, and more efficient blades. Sports equipment, construction materials, and medical devices also account for a significant share.

Key Industry Developments

- March 2025: Hexcel and FIDAMC have partnered to advance composite materials for aerospace and industrial applications. Their collaboration focuses on developing innovative manufacturing processes to enhance lightweight, high performance composites. This partnership aims to improve efficiency and sustainability in composite production.

- November 2024: Toray advanced composites expanded its thermoplastic composites portfolio by acquiring Gordon Plastics assets in Colorado. The new 47,000 sq.ft facility enhances R&D and scalable production of high-performance composite tapes for aerospace, sports, oil & gas, and industrial markets.

Challenges

- High Costs: Production of carbon fibers and composite parts remains expensive, limiting use in cost-sensitive industries.

- Recycling Issues: CFRPs market are difficult to recycle due to their complex structure, posing environmental and economic concerns.

- Processing Complexity: Manufacturing CFRP market components requires specialized machinery and expertise, which can increase lead times and costs.

Competitive Landscape

The CFRP market is highly competitive, with leading players focusing on innovation, strategic partnerships, and capacity expansion. Major companies include Toray Industries, Hexcel Corporation, SGL Carbon, Mitsubishi Chemical Holdings, and Solvay. These firms are investing in next-generation CFRP market technologies, exploring recyclable composites, and strengthening their supply chains to meet rising global demand.

Collaborations with aerospace manufacturers, automotive companies, and renewable energy developers are shaping the market, as players aim to deliver cost-effective solutions without compromising performance.

Future Outlook

Looking ahead, the CFRP market will continue to grow rapidly, fueled by sustainability goals, energy transition, and industrial innovation. As industries move toward greener, lighter, and more efficient technologies, CFRPs will play an increasingly vital role.

The convergence of electric mobility, renewable energy expansion, and next-generation aerospace projects positions CFRPs as a cornerstone of future engineering. While challenges in cost and recycling remain, ongoing R&D and manufacturing advances are expected to create new opportunities for widespread adoption.

Carbon Fiber-Reinforced Plastics market are no longer confined to niche, high-performance applications. They are becoming mainstream solutions that align with global priorities of sustainability, efficiency, and innovation. From lighter cars and planes to more powerful wind turbines, CFRPs market are shaping the next era of engineering and manufacturing. With strong market growth ahead and continuous material advancements, CFRPs stand as a critical material for the industries of tomorrow.

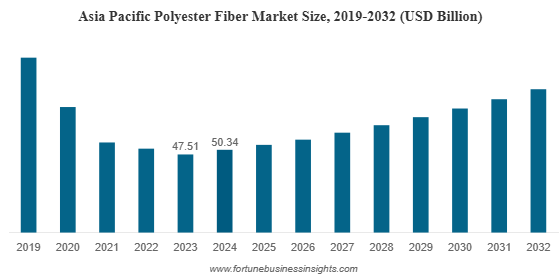

The global polyester fiber market was valued at USD 77.07 billion in 2024 and is expected to increase from USD 82.07 billion in 2025 to USD 129.97 billion by 2032, reflecting a CAGR of 6.8% over the forecast period. Asia Pacific led the market in 2024, accounting for 65.32% of the global share.

Market Growth Drivers

Several factors are fueling the growth of the polyester fiber market. First, the rising demand for cost-effective, durable, and easy-care textiles continues to push polyester ahead of natural fibers such as cotton. Its ability to resist shrinking, wrinkling, and stretching makes it the preferred choice for modern lifestyles. Secondly, the expansion of industries such as automotive, construction, and home décor has amplified demand for polyester in applications like seat upholstery, curtains, carpets, and geotextiles. Another driver is the strong supply chain support, with consistent availability of raw materials ensuring large-scale production at competitive costs. Technological advancements in fiber processing are also enhancing polyester’s performance characteristics, making it suitable for more specialized applications such as sportswear and technical textiles.

List Of Key Polyester Fiber Companies Profiled

- Reliance Industries Limited. (India)

- Indorama Ventures Public Company Limited. (Thailand)

- Toray Industries, Inc. (Japan)

- Sinopec Yizheng Chemical Fibre Limited Liability Company (China)

- Zhejiang Hengyi Group Co., Ltd (China)

- Tongkun Holding Group (China)

- Sanfame Group (China)

- Far Eastern New Century Corporation (Taiwan)

- Alpek Polyester. (Mexico)

- ADVANSA (Turkey)

Industry Shifts and Trends

- Rise of Recycled Polyester: The demand for recycled polyester, often sourced from PET bottles, is gaining momentum. This trend is particularly strong in regions where sustainability initiatives and consumer awareness are driving changes in textile sourcing.

- Shift in Global Supply Chains: Countries like India are actively positioning themselves as alternatives to China by expanding their man-made fiber capacity. Regions such as Tirupur, known for knitwear exports, are setting ambitious targets to increase their share of man-made fiber products by 2030.

- Technical and Functional Textiles: Polyester fibers are increasingly used in specialized applications like geotextiles, filtration, protective clothing, and medical textiles. These high-performance segments are expected to grow faster than conventional apparel and furnishing markets.

- Innovation in Fiber Processing: Advancements in chemical and mechanical recycling technologies, along with new dyeing and finishing techniques, are enhancing both the performance and sustainability of polyester products.

Read More : https://www.fortunebusinessinsights.com/polyester-fiber-market-111384

Regional Insights

- Asia Pacific

Asia Pacific is the undisputed leader in the polyester fiber market, holding a market share of more than 65% in 2024. This dominance is driven by massive production and consumption in countries like China and India. The region’s large textile manufacturing base, cost advantages, and growing domestic demand position it as the hub of polyester production. Additionally, favorable government policies and expanding industrial capacity ensure that Asia Pacific will remain the growth engine for the global market in the coming years.

- North America and Europe

North America and Europe are also important markets, though their growth is more moderate compared to Asia. In these regions, the demand is largely driven by technical applications, automotive textiles, and high-end apparel. However, these markets are also where sustainability concerns are shaping consumer preferences and regulatory frameworks. Manufacturers operating in these regions are under growing pressure to incorporate recycled polyester and invest in environmentally friendly production practices.

- Middle East, Africa, and Latin America

Emerging markets in the Middle East, Africa, and Latin America are gradually increasing their footprint in polyester consumption. Rapid urbanization, infrastructure development, and rising disposable incomes are boosting demand for polyester textiles and furnishings. While these regions currently represent smaller shares of the global market, they offer significant growth opportunities for the future.

Key Industry Developments

- March 2025 - ADVANSA’s ADVAtex is a 100% recycled polyester fiber made from pre-consumer textile waste. It reduces reliance on virgin materials while maintaining quality. The process transforms textile waste into durable fibers for furniture and mattresses, addressing global textile waste challenges. Certified by GRS and Oeko-Tex.

- July 2024 - Indorama Ventures has joined a consortium of seven companies across five countries to establish a sustainable polyester fiber supply chain. This initiative utilizes CO₂-derived, renewable, and bio-based materials, replacing traditional fossil resources. The resulting polyester fiber is planned for use in THE NORTH FACE products in Japan.

Challenges

Despite strong growth, the polyester fiber market faces notable challenges, particularly regarding sustainability. Polyester is derived from petroleum, a non-renewable resource, and its synthetic nature has raised concerns about environmental impact. Microplastic pollution and low recyclability of polyester waste have put pressure on manufacturers to find sustainable alternatives. The growing emphasis on circular economy models and eco-friendly fibers is pushing the industry to adopt recycling technologies and reduce carbon footprints. While recycled polyester is gaining traction, its adoption still represents a small fraction of overall production. Thus, scaling up sustainable fiber solutions remains one of the industry’s biggest hurdles.

Future Outlook

The polyester fiber market is on track to nearly double its value over the next decade. Its growth will be supported by rising consumption in emerging economies, diversification into technical applications, and the ongoing affordability advantage it holds over natural fibers. However, the industry’s ability to balance growth with sustainability will determine its long-term trajectory. Governments, manufacturers, and consumers are all playing key roles in accelerating the transition toward greener polyester solutions.

Polyester fiber market continues to dominate the global textile industry due to its durability, affordability, and adaptability across a wide range of applications. From clothing and upholstery to automotive interiors and industrial uses, polyester’s presence is deeply embedded in everyday life. The market’s expected growth from USD 77.07 billion in 2024 to nearly USD 130 billion by 2032 highlights its resilience and adaptability in the face of changing global dynamics. At the same time, the industry must address sustainability challenges by scaling up recycling, investing in eco-friendly technologies, and reducing its environmental footprint. Companies that embrace innovation and sustainability will be best positioned to thrive in this evolving market landscape.

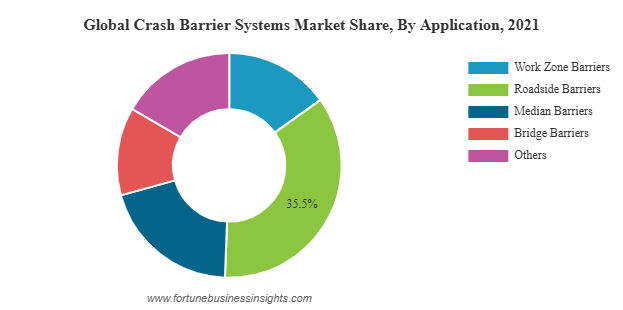

The global crash barrier systems market was valued at USD 6.79 billion in 2021 and is expected to increase from USD 7.01 billion in 2022 to USD 9.35 billion by 2029, growing at a CAGR of 4.2% during the forecast period. In 2021, Asia Pacific led the market with a 32.84% share. Additionally, the U.S. market is projected to expand significantly, reaching an estimated USD 2.23 billion by 2032, driven by technological innovations and advancements in construction methods.

Market Overview

Crash barrier systems market are a vital component of road safety infrastructure. They primarily consist of steel or other high-strength materials, engineered to prevent vehicles from veering off roads, colliding with fixed objects, or crossing medians into oncoming traffic. These systems include various designs and technologies tailored for specific applications, such as roadside barriers, median barriers, bridge barriers, and temporary work zone barriers. With global vehicular traffic increasing and road networks expanding, the demand for crash barriers has become more urgent to minimize fatalities and vehicle damage caused by accidents.

List of Top Crash Barrier Systems Companies:

- Tata Steel (India)

- Lindsay Corporation. (U.S.)

- Transpo Industries Inc. (U.S.)

- Hill and Smith (UK)

- RoadSafe Traffic Systems, Inc. (U.S.)

- Trinity Highway Products, LLC. (U.S.)

- Valmont Industries (U.S.)

- Pinax Steel Industries (India)

- Volkmann Rossbach GmbH Co. KG (Germany)

Key Market Drivers

One of the primary drivers of market growth is the rising number of road accidents worldwide. According to global traffic safety statistics, millions of road accidents occur annually, leading to significant human and economic losses. The increasing awareness of road safety among governments, organizations, and the general public has prompted higher investments in preventive measures, including advanced crash barrier systems.

Infrastructure development and urbanization are also fueling the market. Rapid economic growth in emerging economies has led to extensive highway construction and urban transport projects. Governments are focusing on modernizing road infrastructure to accommodate rising traffic volumes while ensuring the safety of commuters. Consequently, the adoption of crash barrier systems has increased in both urban and rural areas.

Stricter government regulations and standards regarding road safety further drive market expansion. Many countries have implemented mandatory guidelines for highway safety, including the installation of crash barriers in high-risk areas. Compliance with these regulations ensures that roads meet international safety standards, which in turn boosts the demand for reliable and durable crash barrier systems.

Read More : https://www.fortunebusinessinsights.com/crash-barrier-system-market-106084

Market Segmentation

The crash barrier systems market is segmented based on type, technology, and application. By type, it includes fixed barriers and portable barriers. Fixed barriers are permanently installed along highways, bridges, and medians, offering long-term protection. Portable barriers, on the other hand, are used in temporary setups such as construction sites or work zones, providing flexibility and rapid deployment.

By technology, crash barriers are categorized into rigid, semi-rigid, and flexible systems. Rigid barriers are strong and resistant to deformation, effectively redirecting vehicles but often transferring high forces upon impact. Semi-rigid barriers provide a balance between strength and energy absorption, reducing vehicle damage and occupant injury. Flexible barriers, such as cable or wire rope systems, absorb energy by deflecting upon impact, making them suitable for locations with limited space or specific safety requirements.

Applications of crash barrier systems include roadside barriers, median barriers, bridge barriers, and work zone barriers. Roadside barriers prevent vehicles from leaving the road and protect pedestrians and roadside infrastructure. Median barriers separate opposing traffic flows to prevent head-on collisions. Bridge barriers protect vehicles from falling off elevated structures, while work zone barriers safeguard construction workers and temporary road users.

Regional Insights

Asia Pacific emerged as the leading regional market, accounting for a substantial share of global revenue. This growth is driven by extensive infrastructure projects, rapid urbanization, and increasing vehicular population in countries like China and India. North America and Europe also hold significant market shares due to stringent safety regulations, advanced transportation networks, and high government spending on road infrastructure. In these regions, the adoption of technologically advanced crash barriers, including systems integrated with sensors and monitoring capabilities, is rising to enhance road safety further.

Key Industry Developments:

- June 2021 : Trinity Highway Products, LLC signed an agreement with Highway Care Ltd. to produce, sell, and rent the MASH-tested HighwayGuard Barrier in North America. With this partnership, Trinity Highway broadened its commitment to offer innovative roadway solutions of HighwayGuard to Mexico, the U.S., and Canada.

- August 2019 : Lindsay Corporation launched ABSORB-M, a new, non-redirective, water-filled crash cushion system. The product is suited for unanchored and anchored barriers. With this launch, the company would expand its product line.

Challenges and Opportunities

Despite strong growth prospects, the market faces challenges such as high installation costs, maintenance requirements, and space constraints in urban areas. Ensuring durability against environmental factors such as corrosion and extreme weather conditions also poses engineering challenges. However, opportunities abound in the development of smart crash barriers equipped with IoT devices, sensors, and automated monitoring systems. These innovations enable real-time accident detection, vehicle monitoring, and predictive maintenance, enhancing overall safety while creating new revenue streams for manufacturers.

Future Outlook

The crash barrier systems market is poised for steady growth over the next decade. Rising traffic volumes, government initiatives for safer highways, and increasing awareness of road safety will continue to drive demand. Technological advancements, such as the integration of digital monitoring systems and sustainable materials, are expected to reshape the market, making crash barriers not only safer but also more cost-effective and environmentally friendly. As urbanization and infrastructure development continue worldwide, the adoption of robust crash barrier solutions will remain a top priority for governments and transportation authorities.

In summary, crash barrier systems market are an indispensable element of modern road safety infrastructure. Their growing adoption across highways, bridges, and urban roads reflects the global commitment to minimizing traffic accidents and ensuring the protection of human lives. With continuous innovations, regulatory support, and increasing investments in road safety, the market is set to experience sustainable growth in the coming years, reinforcing the importance of reliable and efficient crash barrier solutions worldwide.

Cold Chain Packaging Materials Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-14

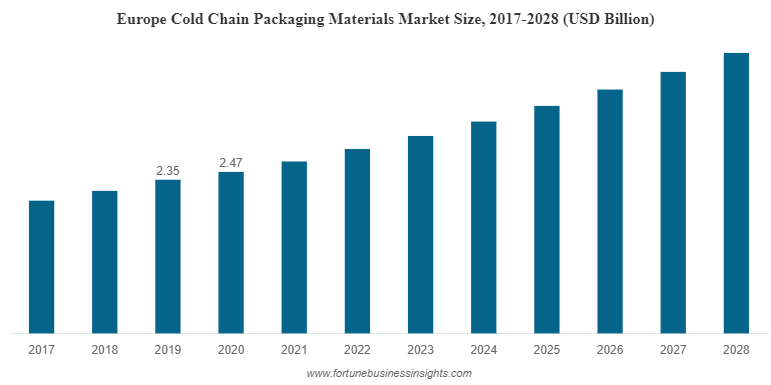

The global cold chain packaging materials market was valued at USD 7.74 billion in 2020 and is expected to expand from USD 8.19 billion in 2021 to USD 13.17 billion by 2028, growing at a CAGR of 7.0% during the forecast period. In 2020, Europe led the market with a 31.91% share. In the United States, the market is projected to reach approximately USD 2.63 billion by 2032, supported by advanced technologies and well-established supply chain networks.

The global cold chain packaging materials market has been witnessing substantial growth, driven primarily by the rising demand for temperature-sensitive products across pharmaceuticals, food, and other sectors. Cold chain packaging plays a critical role in maintaining the integrity and quality of products that are highly sensitive to temperature fluctuations. With consumers increasingly demanding fresh, safe, and high-quality products, the reliance on advanced cold chain packaging solutions has intensified.

Market Overview

In recent years, the market for cold chain packaging materials market has expanded significantly due to the surge in pharmaceutical shipments, frozen food consumption, and e-commerce logistics. Pharmaceuticals, particularly vaccines and biologics, require strict temperature controls during storage and transportation. The global COVID-19 pandemic further emphasized the importance of cold chain systems, as vaccines needed to be distributed worldwide under precise temperature conditions. This has led to investments in innovative packaging materials such as insulated boxes, gel packs, phase-change materials, and vacuum-insulated panels, all designed to ensure temperature stability over long distances.

The food industry has also contributed substantially to market growth. The demand for frozen, ready-to-eat, and perishable foods has surged, driven by the growing population, urbanization, and changing lifestyles. Consumers increasingly prefer food products that retain freshness, flavor, and nutritional value, which necessitates the use of reliable cold chain packaging solutions. Additionally, the expansion of food delivery services and online grocery platforms has placed more emphasis on efficient cold chain systems, ensuring products reach consumers without spoilage.

List Of Key Companies Profiled In Cold Chain Packaging Materials Market:

- Huntsman Corporation (U.S.)

- Dow Chemical Company (U.S.)

- Covestro AG (Germany)

- Armstrong Brands Inc. (U.S.)

- Cascades Inc. (Canada)

- Drew Foam (U.S.)

- Versalis Eni's chemical company (Italy)

- Plymouth Foam (U.S.)

- Creative Packaging (U.S.)

- Bonded Logic Inc. (U.S.)

- TemperPack (U.S.)

Key Materials and Technologies

Cold chain packaging materials market include a wide range of substances such as expanded polystyrene (EPS), polyurethane (PUR), polyethylene, cardboard with insulating liners, and vacuum-insulated panels. Each material offers unique benefits depending on the product type and transportation requirements. EPS, for example, is lightweight and provides excellent thermal insulation, making it popular for both pharmaceuticals and food items. Polyurethane-based materials offer enhanced durability and superior insulation performance, suitable for long-distance shipments.

Innovations in phase-change materials (PCMs) and gel packs have further enhanced the effectiveness of cold chain packaging. PCMs can absorb or release heat to maintain desired temperatures, extending the life of temperature-sensitive products. The integration of smart technologies, such as temperature sensors and tracking devices, allows real-time monitoring of products throughout the supply chain. These technological advancements ensure compliance with regulatory standards and minimize product losses due to temperature deviations.

Read More : https://www.fortunebusinessinsights.com/cold-chain-packaging-materials-market-102830

Regional Insights

The cold chain packaging materials market is witnessing significant growth across multiple regions. Europe has historically held a dominant position due to stringent regulatory requirements, advanced logistics infrastructure, and high adoption of cold chain technologies in pharmaceuticals and food industries. North America, led by the United States, is also a key market, with technological advancements, strong supply chains, and increasing pharmaceutical exports contributing to growth. The Asia-Pacific region is emerging as a high-growth market, driven by rising pharmaceutical manufacturing, food processing industries, and e-commerce expansion in countries such as China, India, and Japan.

Market Drivers

Several factors are driving the growth of the cold chain packaging materials market. First, the global rise in pharmaceutical production, particularly vaccines and biologics, requires reliable packaging solutions to ensure product efficacy. Second, increasing consumer awareness regarding food safety and quality is pushing food manufacturers to invest in advanced cold chain solutions. Third, the growth of online food delivery and grocery services demands rapid and reliable transportation of perishable goods, further boosting market demand. Finally, ongoing research and development in packaging materials, such as biodegradable and sustainable insulation options, are enhancing market prospects while addressing environmental concerns.

Key Industry Developments:

-

March 2021: The International Paper Company purchased two state-of-the-art corrugated box plants in Spain, growing its capabilities in Catalonia and Madrid. Corrugated packaging is an important business segment for International Paper in EMEA, offering packaging solutions in the fresh fruit and vegetable, industrial and e-commerce segments. The two businesses will become part of International Paper.

- May 2020: Vegware’s new composting collection service will see Paper Round collect Vegware compostable disposables in London, Brighton and the surrounding area and deliver the compostable to an in-vessel composting facility enVar, in Cambridgeshire. Here, it will be processed over seven weeks into compost compliant with the PAS 100 quality specification.

Challenges and Opportunities

Despite strong growth, the market faces challenges, including high manufacturing costs, complex logistics requirements, and strict regulatory compliance. Cold chain packaging solutions often involve significant capital investment, especially when incorporating advanced insulation and tracking technologies. Additionally, companies must adhere to international standards and maintain compliance across multiple regions, which can increase operational complexity.

However, these challenges present opportunities for innovation. Companies are increasingly exploring sustainable and recyclable packaging materials to reduce environmental impact. Advancements in smart packaging and IoT-enabled solutions provide real-time monitoring, reducing product loss and improving efficiency. Furthermore, collaborations between packaging providers, logistics companies, and manufacturers can create more integrated and cost-effective cold chain solutions, meeting the growing global demand.

Future Outlook

The cold chain packaging materials market is expected to continue its upward trajectory over the coming years. Growth will be driven by the ongoing expansion of the pharmaceutical and food industries, increasing consumer expectations, and technological advancements in packaging solutions. The integration of sustainability practices and smart technologies will further shape the market landscape, offering opportunities for companies to differentiate themselves and gain competitive advantages.

As global trade and e-commerce continue to rise, the need for reliable cold chain packaging will become even more critical. Companies that invest in innovative, sustainable, and technologically advanced solutions are likely to thrive in this dynamic and rapidly evolving market.

Europe Plastic Cosmetic Packaging Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-14

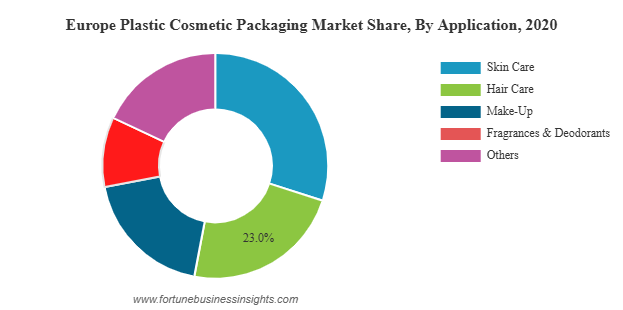

The Europe plastic cosmetic packaging market was valued at USD 1,266.7 million in 2020 and is expected to grow from USD 1,299.6 million in 2021 to USD 1,584.0 million by 2028, registering a CAGR of 2.9% during the 2021–2028 period. The relatively modest growth rate reflects the market’s recovery to pre-pandemic levels following the unprecedented disruption caused by COVID-19. The pandemic led to a significant negative demand shock across all countries, resulting in a 2.97% decline in the European market in 2020.

The Europe plastic cosmetic packaging market has been witnessing steady growth over the past few years, driven by the rising demand for cosmetic and personal care products across the region. The market is projected to continue expanding in the coming years, supported by changing consumer preferences, innovations in packaging materials, and the increasing focus on sustainability.

Market Overview

Europe plastic cosmetic packaging market remains one of the most popular choices for cosmetic products due to its versatility, durability, and cost-effectiveness. In Europe, cosmetic brands are increasingly leveraging plastic packaging to improve product protection, enhance aesthetic appeal, and facilitate easy handling and transportation. Commonly used plastics in the cosmetic industry include polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET), which provide lightweight, durable, and visually appealing packaging solutions.

The growth of the cosmetic industry itself significantly influences the plastic packaging market. Europe has a strong cosmetic market, with increasing demand for skincare, haircare, fragrances, and makeup products. As consumer awareness regarding hygiene, product safety, and preservation grows, the need for high-quality and reliable packaging solutions has become more critical. Additionally, e-commerce channels have expanded the reach of cosmetic products, making packaging an essential factor in protecting products during shipping and enhancing the unboxing experience.

List Of Key Companies Profiled:

- Amcor plc (Switzerland)

- Huhtamäki Oyj (Finland)

- ALPLA Group (Austria)

- Albea Group (France)

- Aptar, Inc. (U.S.)

- Berry Global (U.S.)

- HCP Packaging (China)

- Berlin Packaging (U.S.)

- DS Smith (UK)

- Cosmopak Ltd. (U.S.)

- LIBO Cosmetics (Taiwan)

- Other Key Players

Market Segmentation

The Europe plastic cosmetic packaging market can be segmented based on material, product type, and application.

By Material:

- Polyethylene (PE) is widely used for its flexibility, lightweight nature, and cost efficiency. PE is commonly employed in bottles, tubes, and containers for lotions, creams, and other skincare products.

- Polypropylene (PP) is valued for its durability and chemical resistance, making it ideal for packaging products such as creams, balms, and haircare items.

- Polyethylene Terephthalate (PET) offers high clarity and strength, often used for premium cosmetic bottles, jars, and containers.

By Product Type:

- Bottles are extensively used for liquid and semi-liquid products such as lotions, shampoos, and serums.

- Tubes are preferred for creams, gels, and ointments due to their ease of dispensing.

- Jars and Containers are commonly used for creams, balms, and masks, providing both functionality and an aesthetic appeal.

By Application:

- Skincare remains the largest segment, driven by increasing consumer spending and awareness about personal care routines.

- Haircare products also contribute significantly to market demand, with shampoos, conditioners, and serums requiring durable and visually appealing packaging.

- Makeup products, including foundations, lipsticks, and powders, rely heavily on innovative and attractive packaging to influence consumer purchase decisions.

- Fragrances and Deodorants utilize high-quality plastic packaging to maintain product integrity and create a premium look.

Read More : https://www.fortunebusinessinsights.com/europe-plastic-cosmetic-packaging-market-105171

Trends Driving Market Growth

- Sustainability Initiatives:

European consumers are increasingly environmentally conscious, prompting cosmetic brands to adopt sustainable packaging solutions. Recyclable plastics, biodegradable materials, and refillable containers are becoming popular choices. Brands are investing in innovative designs that reduce plastic usage without compromising functionality or aesthetics. - Technological Advancements:

Advances in plastic manufacturing technologies have allowed for more intricate and functional packaging designs. Airless pumps, dropper bottles, and tamper-evident closures enhance product safety, convenience, and shelf appeal. - E-commerce Influence:

With the growth of online retail, packaging has become a crucial factor in product presentation. Protective and attractive packaging ensures products reach consumers intact while creating a memorable unboxing experience, which is a key factor for cosmetic brands in gaining customer loyalty. - Premiumization of Packaging:

Luxury cosmetic products often use high-quality plastic packaging that mimics glass or other premium materials. This trend has led to the development of innovative plastic formulations and finishing techniques, such as frosted textures, metallic coatings, and customized shapes.

Challenges

Despite strong growth, the market faces challenges, primarily due to regulatory pressures and environmental concerns. European regulations increasingly focus on reducing plastic waste and promoting recycling, compelling manufacturers to innovate and shift toward eco-friendly materials. Additionally, the high cost of sustainable packaging solutions can be a barrier for some brands.

Key Industry Developments:

- October 2020: Berry Global Inc. introduced new Divinity HDPE 2-inch flip-top tube closure that is made from high-density polyethylene (HDPE), and when paired with squeezable polyethylene (PE) tubes, creates a sustainable single-substrate packaged product.

- June 2020: Berry Bramlage, part of Berry Global’s CPI division, introduced a new range of premium jars for cosmetic and beauty products. These jars will be available in 50ml and 75ml sizes.

Competitive Landscape

Key players in the European plastic cosmetic packaging market are focusing on innovation, sustainability, and strategic collaborations to maintain competitiveness. Major companies are investing in research and development to create environmentally friendly packaging and improve production efficiency. Partnerships with cosmetic brands also allow packaging manufacturers to offer customized solutions that meet both functional and aesthetic requirements.

Future Outlook

The Europe plastic cosmetic packaging market is poised for moderate yet steady growth, with an increasing focus on sustainability, premiumization, and technological innovation. As consumers continue to demand high-quality, visually appealing, and environmentally responsible packaging, manufacturers are likely to expand their product portfolios, introduce new materials, and adopt advanced manufacturing techniques.

The combination of rising cosmetic consumption, growth of online retail channels, and evolving regulatory landscapes will shape the market dynamics in the coming years. Overall, the future of plastic cosmetic packaging in Europe appears promising, offering ample opportunities for innovation, growth, and sustainable development.

Construction Chemicals Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-13

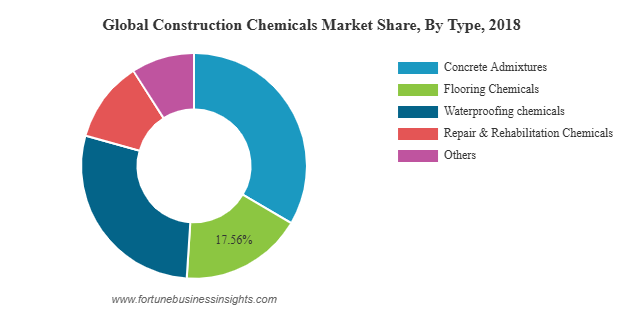

In 2018, the global construction chemicals market was valued at USD 42.32 billion and is expected to grow to USD 70.91 billion by 2026, registering a CAGR of 6.7% during the forecast period. North America held the largest regional share at 23.28% in 2018, with the U.S. market alone anticipated to reach USD 12.73 billion by 2026, fueled by rapid urbanization and expanding infrastructure projects.

Market Size and Growth Outlook

The construction chemicals market is experiencing robust growth as infrastructure expansion, rapid urbanization, and sustainable building practices reshape the global construction landscape. These specialized chemical products are integral to modern construction, enhancing strength, durability, workability, and environmental performance of buildings and infrastructure. As governments and private developers invest in residential, commercial, and industrial projects, the demand for high-performance construction chemicals is rising across all regions.

List Of Key Companies Profiled In Construction Chemicals Market:

- BuildCore Chemicals

- Croda International Plc

- ACC Limited

- Evonik

- BASF SE

- Fosroc, Inc.

- CHRYSO India

- SWC Brother Company Limited.

- Sika AG

- 3M Company

- Other Key Players

Key Growth Drivers

- Infrastructure Development Initiatives

Governments worldwide are prioritizing large-scale infrastructure projects, including roads, bridges, railways, airports, and water management systems. These projects require advanced materials that can withstand heavy loads, harsh weather, and long service life. Construction chemicals such as concrete admixtures, sealants, and protective coatings are essential for ensuring project longevity and reducing maintenance costs. - Rapid Urbanization and Housing Demand

Urban population growth is leading to increased demand for both residential and commercial buildings. In Asia-Pacific, particularly in countries like India and China, mass housing initiatives and smart city developments are creating a strong market for a wide range of construction chemicals, from waterproofing agents to adhesives. - Sustainability and Green Building Standards

Environmental regulations and green certification programs are encouraging the adoption of eco-friendly construction chemicals. Products with low volatile organic compound (VOC) content, high energy efficiency, and recyclable components are increasingly preferred. This shift is driving innovation in biodegradable additives, water-based coatings, and energy-saving insulation materials. - Technological Advancements

Innovation is transforming the sector with the introduction of self-healing concrete, smart sealants that adapt to structural movements, and nano-enhanced coatings for improved performance. These technologies not only enhance structural integrity but also reduce long-term repair and maintenance needs.

Market Segmentation

The construction chemicals market can be segmented by product type, application, and geography:

- By Product Type: Concrete admixtures, waterproofing chemicals, flooring compounds, adhesives & sealants, protective coatings, and others.

- By Application: Residential, commercial, industrial, and infrastructure projects.

- By Region: Asia-Pacific, North America, Europe, Middle East & Africa, and Latin America.

Concrete admixtures remain the largest segment, as they improve the workability, strength, and durability of concrete, making them indispensable in almost every construction project. Waterproofing chemicals are critical for protecting structures against moisture damage, especially in regions with high rainfall or humidity.

Read More : https://www.fortunebusinessinsights.com/construction-chemicals-market-102539

Regional Insights

- Asia-Pacific dominates the global market, with rapid construction activities in China, India, and Southeast Asia driving demand. Affordable housing programs, government-led infrastructure projects, and expanding urban centers are key growth catalysts in this region.

- North America is witnessing growth driven by infrastructure modernization and the adoption of sustainable building practices. In the United States and Canada, renovation and retrofitting activities are boosting the demand for advanced sealants, adhesives, and protective coatings.

- Europe is shaped by stringent environmental regulations, pushing the industry toward eco-friendly formulations. Countries such as Germany, France, and the UK are leading in adopting green construction chemicals that align with energy efficiency and carbon reduction goals.

- Middle East & Africa is seeing a surge in demand due to ambitious mega-projects, especially in Gulf countries. These include smart cities, large-scale tourism infrastructure, and advanced transportation networks. Africa’s growing urban centers are also emerging as potential markets.

- Latin America is gradually expanding, supported by infrastructure improvements and housing projects in Brazil, Mexico, and Chile.

Key Industry Developments:

- In July 2021 – Saint-Gobain entered into an agreement to acquire Chryso, a leading global player in the construction chemicals market. The acquisition of Chryso perfectly fits within Saint-Gobain’s strategic vision of worldwide leadership for sustainable construction. It will further expand the Group’s presence in the growing construction chemicals market with combined sales of more than €3 billion across 66 countries.

- In June 2021 – JSW Cement, India’s leading Green cement company, has entered the Construction Chemical sector with the launch of a unique green product range in the category. The Construction Chemical category offers new opportunities for JSW Cement to combine innovation in concrete mix products with responsible construction. With this development, the company will expand its business.

Challenges Facing the Market

While the outlook is promising, the market faces challenges such as fluctuating raw material prices, compliance with evolving environmental regulations, and the need for skilled application of specialized chemicals. Additionally, the high initial cost of advanced eco-friendly products can be a barrier in price-sensitive markets.

Future Trends and Opportunities

- Digital Integration: Building Information Modeling (BIM) and other digital tools are expected to streamline the selection and application of construction chemicals, improving efficiency and reducing waste.

- Recycling and Circular Economy: The reuse of construction materials and the development of recyclable chemical products will gain momentum.

- Smart Infrastructure Solutions: Demand for chemicals that enhance resilience against climate change effects—such as extreme heat, flooding, and freeze-thaw cycles—will grow.

- Emerging Markets Expansion: Africa, Southeast Asia, and parts of Latin America present untapped opportunities for market players, especially in infrastructure and affordable housing segments.

Outlook

The global construction chemicals market stands at the crossroads of growth, innovation, and sustainability. With infrastructure needs mounting and environmental considerations becoming more urgent, the sector is poised to evolve rapidly. Companies that invest in research, embrace eco-friendly innovations, and cater to region-specific needs will be best positioned to thrive in this competitive landscape. As cities rise and infrastructure networks expand, construction chemicals will remain the invisible yet indispensable force shaping the built environment of the future.