The global sodium lactate market was valued at USD 358.9 million in 2023 and is expected to rise from USD 388.0 million in 2024 to USD 746.6 million by 2032, reflecting a CAGR of 8.5% during the forecast period. In 2023, North America led the market, accounting for a 35.72% share.

Market Leadership and Regional Trends

In 2023, North America dominated the sodium lactate market, holding a market share of 35.72%. This leadership is supported by the region’s well-established healthcare and pharmaceutical industries, coupled with strong growth in the food processing and personal care sectors. The demand for sodium lactate in North America is also fueled by increasing consumer awareness about ingredient safety, clean-label products, and multifunctional additives that can enhance product performance.

Asia Pacific is emerging as a fast-growing market, driven by rising consumer incomes, urbanization, and increased spending on processed food, cosmetics, and healthcare products. Countries such as China, India, and Japan are becoming key markets due to expanding manufacturing capabilities and growing domestic consumption. Europe also maintains a strong presence, with a focus on sustainable production and regulatory compliance, especially in food safety and cosmetic standards.

List Of Top Sodium Lactate Companies:

- JIAAN BIOTECH (India)

- Musashino Chemical Laboratory, Ltd. (Japan)

- Jungbunzlauer Suisse AG, Basel (Switzerland)

- Fengchen Group Co., Ltd (China)

- Hawkins, Inc. (U.S.)

- Junsei Chemical Co.,Ltd. (Japan)

- Kishida Chemical Co.,Ltd. (Japan)

- Avanschem (India)

Key Growth Drivers

Several factors are fueling the expansion of the sodium lactate market:

- Clean-Label Demand – Consumers are increasingly seeking products made from safe, naturally derived ingredients. Sodium lactate’s renewable sourcing and multifunctional nature make it an ideal fit for this trend.

- Versatility – Its diverse applications, from skincare hydration to food preservation and medical use, make sodium lactate a valuable ingredient across multiple industries.

- Rising Healthcare Demand – The growing use of intravenous solutions and electrolyte-replacement therapies is boosting demand in the medical sector.

- Expanding Cosmetics Industry – The personal care sector’s focus on natural, sustainable ingredients is accelerating the use of sodium lactate in premium and mass-market skincare products.

- Globalization of Food Processing – Increased production of packaged and processed foods in emerging economies is driving growth in food-grade sodium lactate.

Read More : https://www.fortunebusinessinsights.com/sodium-lactate-market-110698

Form Insights

The market is segmented by form into liquid and powder sodium lactate. The liquid form currently dominates due to its high solubility, ease of blending, and wide use in applications such as intravenous solutions, meat preservation, and skincare products. Liquid sodium lactate is especially popular in food and pharmaceutical applications because it integrates seamlessly into formulations without requiring additional processing.

The powder form, while holding a smaller share, is steadily gaining traction, particularly in the cosmetics and personal care industry. Its longer shelf life and ease of storage make it an attractive choice for manufacturers seeking stable, high-quality ingredients for lotions, creams, and other beauty products.

Application Insights

By application, the cosmetics and personal care segment accounts for the largest market share. Sodium lactate is valued for its humectant properties, helping to maintain skin hydration and improve texture in products such as moisturizers, body lotions, facial creams, and serums. With growing interest in natural and clean-label skincare products, sodium lactate is increasingly being used as a safer alternative to synthetic moisturizers.

The pharmaceutical sector is another significant consumer, making use of sodium lactate in intravenous fluids, electrolyte solutions, and dialysis treatments. Its role in maintaining pH balance and hydration levels in medical applications is vital, particularly in critical care settings. In 2023, this segment accounted for nearly 29.8% of the market share.

In the food and beverage industry, sodium lactate serves as a natural preservative and flavor enhancer. It extends the shelf life of meat products, prevents bacterial growth, and improves product safety without compromising taste. The rising demand for processed meat and ready-to-eat meals is driving greater adoption of sodium lactate in this sector.

Challenges

Despite its growth potential, the sodium lactate market faces certain challenges:

- Raw Material Costs – Fluctuations in raw material availability and prices can impact manufacturing costs.

- Regulatory Variations – Different regions have varying regulations for the use of sodium lactate in food, cosmetics, and pharmaceuticals, requiring careful compliance strategies.

- Competition from Alternatives – Other preservatives and humectants can compete with sodium lactate in certain applications, requiring continuous innovation to maintain market share.

Opportunities

The future offers multiple opportunities for market players:

- Product Innovation – Development of high-purity grades and customized formulations can meet the specific needs of specialized industries.

- Sustainability Initiatives – Leveraging environmentally friendly production methods can appeal to eco-conscious consumers and brands.

- Emerging Markets – Expanding distribution networks in Asia, Latin America, and Africa can unlock new revenue streams.

- Brand Collaborations – Partnering with cosmetics, pharmaceutical, and food brands to develop innovative products can enhance market visibility and demand.

Outlook

The sodium lactate market is set for robust growth, fueled by strong demand across multiple industries, rising health and wellness trends, and ongoing product development. North America will likely maintain its leading position, while Asia Pacific will see the fastest growth, thanks to expanding industrial capacity and consumer demand. With a strong focus on clean-label, multifunctional, and sustainable solutions, sodium lactate is poised to become an even more integral ingredient in the global supply chain.

In 2023, the global self-adhesive labels market was valued at USD 48.03 billion. It is expected to rise to USD 50.65 billion in 2024 and further expand to USD 82.17 billion by 2032, registering a CAGR of 6.1% over the forecast period. Asia Pacific led the market in 2023, holding a 38.93% share. In the United States, the market is anticipated to witness notable growth, reaching approximately USD 9.47 billion by 2032, fueled by increasing demand for consumables, ready-to-eat meals, and packaged food and beverages.

Strong Market Growth

The self-adhesive labels market has evolved from a simple product identification tool into a vital component of modern packaging and branding strategies. With increasing demand across multiple sectors, the market is on an upward growth trajectory, supported by innovations, sustainability trends, and strong industrial activity worldwide.

List Of Key Companies Profiled

- 3M Company (U.S.)

- Axicon Labels (U.K.)

- Avery Products Corporation (U.S.)

- ETIS Slovakia (Slovakia)

- UPM Raflatac (Finland)

- Müroll GmbH (Austria)

- Royston Labels Ltd (U.K.)

- S&K LABEL (U.S.)

- SVS Etikety (Czech Republic)

- Mondi Group (Austria)

Key Growth Drivers

Several factors are driving the expansion of the self-adhesive labels market:

- Growing Packaging Industry – The rise of consumerism and global trade has elevated packaging from a functional necessity to a strategic branding tool.

- E-commerce Boom – Increasing online retail sales require efficient, durable labeling for order processing, tracking, and brand presentation.

- Regulatory Compliance – Stricter global regulations in food and pharmaceuticals mandate clear, accurate labeling to ensure consumer safety.

- Cost-Effectiveness – Compared to alternative labeling methods, self-adhesive labels are easy to apply, scalable, and versatile.

Trends Shaping the Future

Sustainability is a defining trend. Environmental concerns have prompted a shift toward recyclable, biodegradable, and linerless labels that reduce waste and carbon footprint. Paper-based labels are gaining traction in sectors aiming to replace plastic packaging components.

Smart labels are another growing trend. By integrating technologies such as RFID, NFC, and QR codes, labels now serve as gateways to product information, authentication, and supply chain transparency. This is particularly valuable in industries combating counterfeiting, such as luxury goods and pharmaceuticals.

Digital printing advancements are also transforming the market. These technologies allow for shorter runs, faster turnaround times, and customization, enabling brands to respond quickly to changing market demands.

Read More : https://www.fortunebusinessinsights.com/self-adhesive-labels-market-104289

Product Types Driving Demand

By type, release liner labels dominate the market. These labels feature a backing layer that protects the adhesive until application, making them suitable for industries requiring clean, dust-free, and efficient labeling. They are particularly popular in food, beverage, and pharmaceutical applications.

In terms of label form, permanent labels hold the largest share. These are known for their strong adhesion and durability, making them ideal for packaging that requires long-lasting branding or critical safety information. Industries such as automotive, chemicals, and consumer goods rely heavily on this type for product identification and hazard warnings.

Leading Applications

- The food and beverage sector accounts for the largest share of the market. Rising demand for packaged and ready-to-eat meals has led to greater use of labels for branding, nutritional transparency, and tamper evidence. The growth of online food delivery platforms has further boosted demand, as tamper-proof labels are essential for ensuring product safety.

- Pharmaceuticals form another key application area. Strict regulations require detailed labeling for medicines, from dosage instructions to safety warnings. Self-adhesive labels are preferred for their precision, reliability, and ability to integrate advanced features such as serialization and anti-counterfeiting measures.

- Logistics and e-commerce also represent a rapidly growing segment. The sector requires durable labels that can withstand handling, moisture, and temperature variations during shipping, while ensuring clear barcode scanning for tracking and inventory control.

Asia Pacific Leads the Way

Asia Pacific held the largest share of the global market in 2023, commanding nearly 39% of the total value. Countries such as China, India, Indonesia, and Japan have witnessed significant growth in manufacturing, retail, and logistics, which in turn fuels the demand for self-adhesive labels.

China, with its extensive manufacturing capacity and thriving e-commerce industry, is a dominant contributor. India is emerging as one of the fastest-growing markets due to expansion in the food processing, pharmaceuticals, and personal care industries. Government initiatives promoting organized retail and stricter labeling regulations are further accelerating adoption.

Key Industry Developments

- February 2024 – Mondi collaborated with multiple stakeholders along the value chain to recycle and release liner production waste. These stakeholders include Soprema, WEPA, and Vwyzle. They are working together to convert Mondi’s coated paper waste produced at its release liner plants into secondary raw material for a range of applications.

- May 2021 - Herma, a German self-adhesive technology specialist launched 52W, a new wash-off label adhesive developed especially for PET bottles.

Challenges to Overcome

Despite its strong growth potential, the market faces certain challenges. Volatility in raw material prices, particularly adhesives, films, and specialty papers, can impact profitability. Regulatory hurdles in terms of food-safe inks and adhesives require continuous compliance efforts. Additionally, competition from numerous regional players often results in pricing pressures.

Competitive Landscape

The global market is characterized by the presence of leading companies such as 3M, Avery Dennison Corporation, Mondi Group, UPM Raflatac, H.B. Fuller, and CCL Industries. These players are focusing on product innovation, sustainable material development, and strategic collaborations to strengthen their market position.

Recent developments in the industry include collaborations between label manufacturers and recycling companies to repurpose release liner waste into usable raw materials. Such initiatives not only address environmental concerns but also create opportunities for circular economy practices within the labeling industry.

Opportunities Ahead and Outlook

Looking forward, the self-adhesive labels market is well-positioned to capitalize on the convergence of sustainability, technology, and consumer expectations. Brands that adopt eco-friendly materials, leverage smart label capabilities, and invest in design innovation will be able to enhance both their environmental credentials and customer engagement.

As packaging continues to serve as a primary touchpoint between brands and consumers, the role of self-adhesive labels will only expand. Whether in a supermarket aisle, a pharmacy shelf, or a courier package, these labels are not just identifiers—they are storytellers, quality markers, and trust builders in the modern marketplace.

The global organic cotton market was valued at USD 1,113.5 million in 2023 and is expected to rise from USD 1,585.5 million in 2024 to USD 25,890.2 million by 2032, registering an impressive CAGR of 40.0% during the forecast period (2024–2032). Asia Pacific led the market in 2023, accounting for 65.7% of the global share. In the United States, the organic cotton market is anticipated to witness substantial growth, reaching approximately USD 504.56 million by 2032, fueled by the rising consumer preference for sustainable and eco-friendly textiles.

Market Size and Growth Outlook

The global organic cotton market is experiencing unprecedented growth as environmental awareness, ethical fashion trends, and sustainable supply chain practices gain momentum worldwide. Once considered a niche segment of the textile industry, organic cotton has now emerged as a key driver in the transition toward eco-friendly and socially responsible manufacturing.

List Of Key Companies Profiled

- Cargill Incorporated (U.S.)

- Plexus Cotton Ltd. (U.K.)

- Staple Cotton Cooperative Association (U.S.)

- Calcot Ltd. (U.S.)

- The Rajlakshmi Cotton Mills (P) Limited (India)

- Remei AG (Switzerland)

- Arvind Limited(India)

- Noble Ecotech (India)

- Louis Dreyfus Company (Netherlands)

- Texas Organic Cotton Marketing Cooperative (U.S.)

Key Market Drivers

Several factors are contributing to the rapid expansion of the organic cotton market:

- Sustainability Trends in Fashion – Consumers are becoming more conscious of the environmental footprint of their clothing. Organic cotton is grown without synthetic pesticides, fertilizers, or genetically modified seeds, making it a cleaner and greener alternative to conventional cotton.

- Brand Commitments to Ethical Sourcing – Many leading apparel brands and retailers have committed to increasing the share of organic cotton in their supply chains. These commitments are often part of larger sustainability targets aimed at reducing environmental impact.

- Supportive Government and NGO Initiatives – Policies promoting organic agriculture, financial incentives for farmers, and the growing network of certification bodies have helped expand organic cotton cultivation worldwide.

- Consumer Health Awareness – Organic cotton products are free from harmful chemicals, making them safer for consumers with sensitive skin or allergies, further enhancing their appeal.

Emerging Trends

One of the most notable trends shaping the market is the push toward supply chain transparency. Brands are increasingly investing in technologies that trace the journey of organic cotton from farm to finished product. This not only assures consumers of authenticity but also promotes fair trade and ethical labor practices.

Another trend is the integration of circular economy principles into organic cotton production. This includes recycling cotton waste, promoting durability and repairability in clothing, and encouraging textile take-back programs to reduce waste.

Read More : https://www.fortunebusinessinsights.com/organic-cotton-market-106612

Market Potential in the United States

The United States is projected to see substantial growth in the organic cotton market, with its value expected to reach approximately USD 504.56 million by 2032. The surge is being driven by a sharp rise in demand for sustainable and eco-friendly textiles, increasing consumer awareness of environmental issues, and the willingness of major U.S. retailers to integrate organic cotton into their apparel, home textiles, and lifestyle products. The presence of prominent sustainable fashion brands in North America further boosts the adoption of organic cotton in the region.

Applications Across Industries

The largest application segment for organic cotton is apparel, covering everyday wear, activewear, children’s clothing, and high-end fashion collections. Brands are integrating organic cotton into their main product lines to cater to environmentally conscious shoppers.

Beyond fashion, organic cotton is increasingly used in home textiles such as bed linens, towels, and curtains, as well as personal care items including baby clothing, wipes, and hygiene products. The demand for organic cotton in eco-friendly packaging is also on the rise, as brands aim to align their packaging materials with their sustainability messaging.

Regional Leadership: Asia Pacific at the Forefront

Asia Pacific dominated the market in 2023, accounting for a commanding 65.7% share. This dominance can be attributed to the region’s strong textile manufacturing base, availability of agricultural land for organic farming, and rising consumer awareness regarding sustainable clothing. Countries such as India, China, and Turkey have emerged as major producers and exporters of organic cotton, supplying both domestic and international markets.

India, in particular, has positioned itself as a global leader in organic cotton cultivation, supported by favorable climatic conditions, government subsidies, and certification programs. Meanwhile, China continues to strengthen its role in organic cotton processing and garment manufacturing, meeting the growing demand from global fashion retailers.

Challenges to Overcome

Despite the strong growth outlook, the organic cotton market faces several challenges:

- Higher Production Costs – Organic farming is more labor-intensive and requires strict compliance with certification standards, which can make organic cotton more expensive than its conventional counterpart.

- Lower Yields – Organic cotton generally produces lower yields per acre compared to conventionally grown cotton, affecting scalability.

- Seed Supply Limitations – Access to high-quality organic cotton seeds remains a challenge for farmers in some regions.

- Market Price Sensitivity – While demand is growing, higher retail prices for organic cotton products can limit adoption in price-sensitive markets.

Competitive Landscape

The organic cotton market is moderately fragmented, with a mix of large multinational textile producers and smaller regional players. Leading companies are focusing on vertical integration, from farming to finished garments, to ensure quality control and supply consistency. Strategic partnerships between brands and farmer cooperatives are also becoming common, as they help secure long-term organic cotton supply and provide farmers with better income stability.

Investments in research and development are aimed at improving organic farming techniques, enhancing yields, and developing innovative organic cotton blends for specialized applications.

Outlook

The future of the organic cotton market looks exceptionally promising. Rising environmental awareness, growing consumer demand for sustainable products, and the willingness of brands to adopt ethical sourcing practices are creating a strong foundation for continued growth. While challenges such as cost and yield limitations remain, ongoing innovations in farming, processing, and supply chain management are expected to make organic cotton increasingly competitive with conventional cotton.

In the coming years, the industry will likely witness greater collaboration among farmers, manufacturers, brands, and policymakers to ensure the organic cotton sector not only grows in scale but also maintains its environmental and social integrity.

Water Soluble Polymers Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-07

The global water soluble polymers market was valued at USD 38.56 billion in 2023 and is expected to increase from USD 40.66 billion in 2024 to USD 62.96 billion by 2032, registering a CAGR of 5.5% during the forecast period. In 2023, Asia Pacific led the market, accounting for a dominant 43.23% share. In the United States, the market is anticipated to witness substantial growth, reaching approximately USD 10.19 billion by 2032. This growth is primarily driven by the increasing demand from the oil and gas sector, where water soluble polymers offer enhanced customizability compared to other injection fluids used in enhanced oil recovery (EOR) processes.

Water soluble polymers market are macromolecules that dissolve, disperse, or swell in water and alter the physical properties of aqueous systems in terms of thickening, gel formation, emulsification, flocculation, and stabilization. These characteristics have made them indispensable in industries where performance, environmental sustainability, and safety are paramount.

Key Market Drivers

One of the primary drivers for this market is the growing global emphasis on water treatment. As freshwater scarcity increases and regulatory norms around water pollution become stricter, municipalities and industries are investing heavily in water purification systems. Water soluble polymers, especially polyacrylamides, are used extensively as flocculants and coagulants to remove impurities and suspended solids from wastewater. These polymers improve filtration efficiency and enable compliance with environmental standards.

Another major factor fueling market expansion is their application in the oil and gas sector, particularly in enhanced oil recovery (EOR). Polymers like partially hydrolyzed polyacrylamide (PHPA) improve oil mobility and sweep efficiency, enhancing yield during tertiary recovery processes. As global oil reserves become harder to extract and more companies focus on cost-effective recovery techniques, the use of water soluble polymers in EOR is expected to rise significantly.

In addition, the food processing and pharmaceutical industries are increasingly utilizing natural and synthetic water soluble polymers. In food applications, they serve as thickeners, stabilizers, emulsifiers, and texture modifiers. In pharmaceuticals, these polymers are widely employed in drug formulation and delivery systems, including controlled-release tablets, suspensions, and gels.

List Of Key Companies Profiled

- Arkema SA (France)

- Ashland (U.S.)

- DuPont (U.S.)

- LG Chem (South Korea)

- The Dow Chemical (U.S.)

- Nitta Gelatin, NA Inc. (Japan)

- BASF SE (Germany)

- SNF (France)

- Kuraray Co., Ltd. (Japan)

- Kemira (Finland)

Polymer Types and Application Segments

Among the various types of water soluble polymers, polyacrylamide holds the largest market share due to its high effectiveness as a flocculant in water treatment and EOR. Polyvinyl alcohol (PVA) is also gaining traction owing to its excellent film-forming and adhesive properties. In the pharmaceutical industry, PVA is used in contact lenses and drug formulations. Other significant types include guar gum, gelatin, methylcellulose, xanthan gum, and carboxymethyl cellulose—mostly used in food, cosmetic, and pharmaceutical applications.

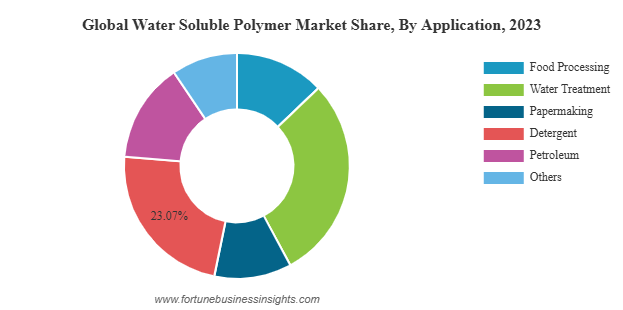

From an application standpoint, the water treatment segment dominates the global market. Governments across developing and developed regions are adopting advanced wastewater management policies, and this trend is projected to continue. Other notable application areas include detergents and personal care products, where water soluble polymers enhance product performance and texture.

Regional Insights

Asia Pacific emerged as the leading regional market in 2023, accounting for over 43% of the global market share. Rapid industrialization, growing urban populations, and increasing investments in water infrastructure across countries like China, India, and Southeast Asian nations are fueling demand in the region. India alone witnessed strong growth, with its market expected to grow at a CAGR of over 4% during the forecast period, driven by expansion in wastewater treatment plants, packaged food consumption, and pharmaceutical production.

North America and Europe also hold significant shares, supported by stringent environmental regulations, advanced oil recovery techniques, and robust healthcare sectors. In the United States, the emphasis on sustainable industrial practices and bio-based product development is encouraging polymer manufacturers to innovate with eco-friendly alternatives.

Read More : https://www.fortunebusinessinsights.com/water-soluble-polymers-market-106175

Key Industry Developments

- March 2022 – Kemira bolstered its position as a prominent provider of sustainable chemical solutions for water-reliant industries by launching the world’s first full scale production of its recently designed bioderived polymers. Helsinki Region Environmental Services (HSY) received the first volumes for trials at one of their wastewater treatment facilities.

- September 2020 – BASF expanded its business in a water-soluble polyacrylate manufacturing unit at Ludwigshafen, Germany. The manufacturing unit will allow customers in the home and commercial cleaning sector and chemical and formulator industries to benefit from increased specialized chemical capacity.

Sustainability and Innovation

Sustainability remains at the forefront of product development in this market. With rising environmental concerns and pressure to reduce carbon footprints, manufacturers are exploring bio-based and biodegradable polymers. Natural polymers such as starch derivatives, chitosan, and plant-based gums are gaining popularity as replacements for synthetic polymers in various applications.

Furthermore, innovations in polymer chemistry are leading to the creation of high-performance, multi-functional polymers that can operate effectively in challenging industrial environments. Companies are also investing in research to develop water soluble polymers that offer enhanced recyclability and reduced ecological impact.

Challenges and Future Outlook

Despite its promising growth trajectory, the water soluble polymers market faces challenges such as price volatility of raw materials, limited availability of certain natural polymers, and performance trade-offs in bio-based alternatives. Additionally, environmental concerns associated with synthetic polymers like polyacrylamide continue to drive regulatory scrutiny.

However, the future outlook remains optimistic. As industries worldwide transition toward sustainable practices and invest in efficient resource management, the demand for water soluble polymers is expected to soar. Emerging technologies, increasing focus on eco-design, and supportive government policies are set to bolster market expansion in the years ahead.

The water soluble polymers market stands at a pivotal moment of growth, innovation, and sustainability. With their versatile properties and crucial applications across water treatment, oil recovery, food, pharmaceuticals, and personal care, these polymers are poised to shape the next decade of industrial and environmental advancements. As consumer awareness and regulatory standards evolve, the market will continue to move toward greener, more efficient, and safer polymer solutions.

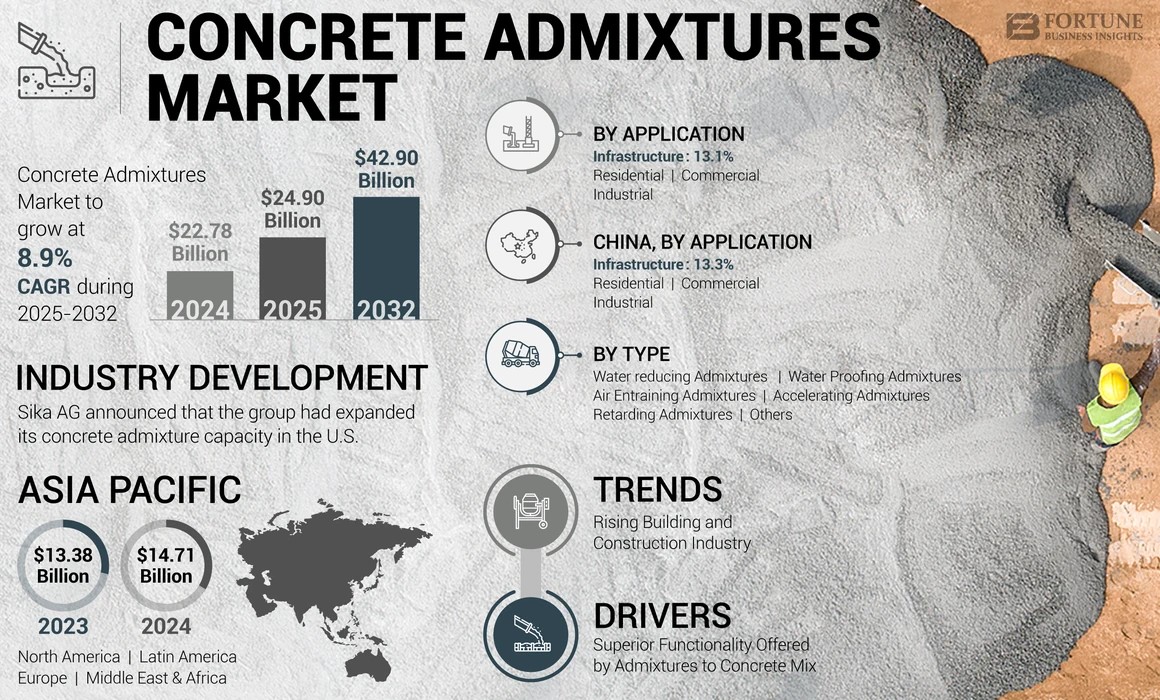

The global concrete admixtures market is undergoing rapid transformation, fueled by booming construction activities, rising demand for high-performance concrete, and increasing emphasis on sustainability. As the backbone of modern infrastructure, concrete must meet a wide range of performance requirements—and concrete admixtures play a critical role in achieving these. These chemical additives are mixed with concrete to modify its properties and improve workability, durability, strength, and other performance parameters. As urbanization accelerates and environmental concerns deepen, the concrete admixtures market is poised for substantial growth.

The global concrete admixtures market was valued at USD 22.78 billion in 2024 and is expected to expand from USD 24.90 billion in 2025 to USD 42.90 billion by 2032, registering a CAGR of 8.9% during the forecast period. Asia Pacific led the market in 2024, accounting for 64.57% of the global share. In the United States, the market is anticipated to witness strong growth, reaching approximately USD 3.08 billion by 2032, fueled by increasing adoption of high-performance concrete solutions.

Key Growth Drivers

Multiple factors are contributing to the sustained expansion of the concrete admixtures market. The most significant growth driver is the unprecedented rise in construction activity worldwide. Both public and private sector investments in infrastructure, coupled with supportive government policies, are creating a favorable environment for market expansion.

Another major driver is the increasing awareness around the benefits of using admixtures to enhance concrete performance. Contractors and developers are increasingly opting for value-added solutions that provide long-term durability, improved workability, and lower maintenance costs. Admixtures also enable the use of recycled materials and low-grade aggregates, thereby contributing to cost-efficiency and sustainability.

Environmental concerns and strict regulatory norms have also encouraged the adoption of eco-friendly admixtures. Many manufacturers are innovating to offer bio-based, non-toxic, and low-carbon formulations that align with green building certifications such as LEED and BREEAM. The push toward circular economy practices is further boosting demand for products that reduce concrete waste, extend structure life, and minimize energy consumption.

List of Top Concrete Admixtures Companies:

- Buildtech Products (India)

- Sika AG (Switzerland)

- RAZON ENGINEERING COMPANY PRIVATE LIMITED (India)

- Flowcrete Group Ltd. (U.K.)

- CEMEX S.A.B. de C.V. (Mexico)

- BASF SE (Germany)

- GCP Applied Technologies (U.S.)

- RPM International Inc. (U.S.)

Product Insights and Market Segmentation

Concrete admixtures can be broadly categorized based on their functions—water-reducing, retarding, accelerating, air-entraining, plasticizers, and others. Among these, water-reducing admixtures are leading the market and held the largest share in 2024. These admixtures enhance the flow characteristics of concrete while maintaining its strength and durability, making them highly desirable across applications.

High-range water reducers, also known as superplasticizers, are gaining traction in the construction of high-rise buildings and complex infrastructure that require superior strength and performance. Air-entraining admixtures are also in demand, especially in regions prone to freeze-thaw conditions, as they improve concrete’s resistance to environmental stressors.

From an application standpoint, the residential sector emerged as the leading end-user in 2024. The segment has benefitted from growing urban housing demand, increased homeownership, and government-backed affordable housing programs. However, the commercial and infrastructure segments are expected to witness faster growth in the coming years due to rising investment in roads, bridges, airports, water treatment plants, and public utilities.

Read More : https://www.fortunebusinessinsights.com/concrete-admixtures-market-102832

Dominance of Asia Pacific and Regional Trends

Asia Pacific continues to dominate the global concrete admixtures market, accounting for approximately 64.6% of the total market share in 2024. The region’s leadership is primarily driven by massive infrastructure investments in countries such as China, India, Indonesia, and Vietnam. Rapid urbanization, population growth, and government-led infrastructure projects have significantly increased the consumption of concrete admixtures across residential, commercial, and industrial segments.

India, for example, is witnessing a surge in smart city development, highway expansion, metro rail projects, and affordable housing schemes. Similarly, China remains a global construction powerhouse, with ambitious urban planning and transportation infrastructure fueling sustained demand for advanced construction materials. Southeast Asia is also emerging as a promising market, supported by favorable policy frameworks and increasing foreign direct investment in construction and real estate.

Meanwhile, North America and Europe are seeing moderate but steady growth, primarily driven by renovation of aging infrastructure, energy-efficient building mandates, and rising focus on environmentally friendly construction. The United States, in particular, is expected to witness considerable growth in demand for concrete admixtures, especially in infrastructure modernization, bridge rehabilitation, and commercial construction.

Key Industry Developments:

- November 2023: Sika AG announced that the group had expanded its concrete admixture capacity in the U.S. The company continues to invest in its polymer production at its Sealy site in the U.S. state of Texas. Sika’s latest move marks its second polymer investment in the state of Texas in just five years. The company requires polymers for chemical building blocks that are needed to produce Sika ViscoCrete, a high-performance, resource-saving concrete admixture. The company initiated this expansion to meet the growing demand for its products in the U.S. and Canada.

- June 2023: Fosroc India launched a state-of-the-art Concrete Lab in Chennai that will provide advanced building material testing facilities to developers, contractors, and other construction professionals.

Innovation and Future Outlook

The future of the concrete admixtures market will be shaped by innovation and technological advancements. Self-healing concrete, nanotechnology-based admixtures, and crystalline waterproofing solutions are gaining popularity for their superior performance and environmental benefits. Automation and digital construction technologies are also influencing product usage, as real-time monitoring of concrete behavior becomes more feasible on-site.

Leading companies in the market are focusing on expanding their geographic footprint, developing sustainable products, and forming strategic collaborations to tap into emerging markets. Research and development efforts are increasingly directed toward admixtures that cater to the specific climatic and structural needs of different regions.

As construction standards evolve and infrastructure becomes more complex, the demand for specialized and high-performance concrete admixtures will continue to rise. The market offers immense opportunities for product innovation, regional expansion, and sustainable solutions that align with the future of construction.

Saudi Arabia Refractories Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-07

The Saudi Arabia refractories market was valued at USD 160.2 million in 2021 and is expected to grow from USD 164.8 million in 2022 to USD 254.6 million by 2029, registering a CAGR of 6.4% during the forecast period. The COVID-19 pandemic had a significant impact on the market, leading to lower-than-expected demand across the country compared to pre-pandemic projections. In 2020, the market experienced a 4.9% decline compared to 2019, highlighting the disruption caused by the global health crisis.

Key Growth Drivers

One of the primary factors fueling market growth is the rapid expansion of the steel industry. Saudi Arabia is currently the largest steel-producing country in the Gulf Cooperation Council (GCC) region, with more than 40 steel manufacturing facilities operating across the country. These facilities have an estimated production capacity of over 18 million tons per year, and refractories are essential materials in their operations. They are used to line high-temperature furnaces, kilns, and reactors, ensuring structural integrity and efficiency.

Alongside steel, sectors such as cement and glass manufacturing are also contributing significantly to demand for refractory products. Mega projects like NEOM, the Red Sea Development, and various other infrastructure programs are creating long-term demand for cement and construction materials. These projects require refractory linings in the production process of essential materials, which further accelerates consumption.

Additionally, the petrochemical and non-ferrous metal industries are becoming prominent end users of refractories. These sectors rely heavily on high-temperature processes for refining, smelting, and processing, all of which demand high-performance refractory materials that can withstand extreme environments.

List Of Key Companies Profiled

- Arkema SA (France)

- Ashland (U.S.)

- DuPont (U.S.)

- LG Chem (South Korea)

- The Dow Chemical (U.S.)

- Nitta Gelatin, NA Inc. (Japan)

- BASF SE (Germany)

- SNF (France)

- Kuraray Co., Ltd. (Japan)

- Kemira (Finland)

Market Segmentation and Trends

The Saudi refractories market is broadly segmented based on form, chemistry, and end-use industries.

By form, the market includes shaped and unshaped refractories. Shaped refractories—typically in the form of bricks and blocks—dominate the market due to their widespread application in large furnaces and kilns. However, unshaped refractories, also known as monolithic refractories, are gaining popularity because of their ease of installation and ability to form complex shapes. These are often used for repair purposes or in custom high-temperature applications.

By chemical composition, refractories are divided into acidic, basic, and neutral types. Basic refractories, such as those made with magnesia and dolomite, are highly sought after due to their resistance to alkaline slags, making them ideal for steel and cement industries. Acidic refractories made from silica and fireclay are also in demand, especially in glass manufacturing.

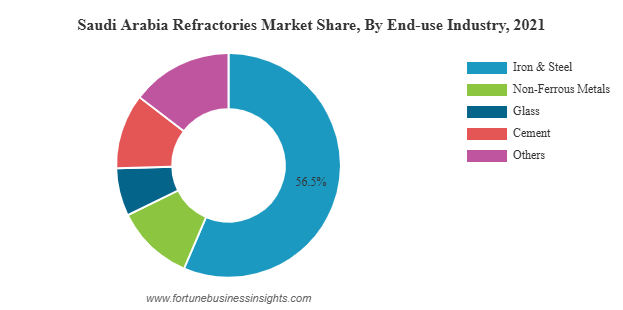

In terms of end-use, the iron and steel industry remains the largest consumer of refractories in the Saudi market. Frequent replacement of refractory linings due to wear and tear from constant exposure to high temperatures ensures steady demand. Other key industries include cement, petrochemical, glass, power generation, and non-ferrous metallurgy.

Read More : https://www.fortunebusinessinsights.com/saudi-arabia-refractories-market-106924

Opportunities in Localization and Sustainability

A significant opportunity in the Saudi Arabia refractories market lies in the localization of production. The government is increasingly focused on reducing dependence on imports by promoting local manufacturing. This creates strong prospects for both domestic and international players willing to establish production facilities within the country. Establishing local production can also help tackle issues such as supply chain disruptions and long lead times.

Sustainability is another growing focus area. As part of the Saudi Green Initiative and its broader commitment to carbon neutrality by 2060, there is increasing emphasis on energy-efficient and eco-friendly refractories. Manufacturers are exploring the use of recycled raw materials and developing products that reduce heat loss, thereby conserving energy during industrial processes.

Furthermore, advancements in refractory technology such as nanotechnology-enhanced materials and longer-lasting linings are creating added value for end users. These innovations improve performance, reduce maintenance frequency, and lower operational costs, making them attractive in the context of rising raw material prices.

Key Industry Developments

- March 2022 – Kemira bolstered its position as a prominent provider of sustainable chemical solutions for water-reliant industries by launching the world’s first full scale production of its recently designed bioderived polymers. Helsinki Region Environmental Services (HSY) received the first volumes for trials at one of their wastewater treatment facilities.

- September 2020 – BASF expanded its business in a water-soluble polyacrylate manufacturing unit at Ludwigshafen, Germany. The manufacturing unit will allow customers in the home and commercial cleaning sector and chemical and formulator industries to benefit from increased specialized chemical capacity.

Challenges Ahead

Despite the promising outlook, the market faces certain challenges. Volatility in the prices of raw materials such as bauxite, alumina, and magnesia can affect the cost of production and profitability. Additionally, the reliance on imports for some critical raw materials exposes the market to global supply chain uncertainties.

Environmental regulations are also becoming more stringent, particularly concerning emissions and waste disposal. Refractory manufacturers will need to adapt their production processes to comply with new standards while maintaining cost efficiency.

Future Outlook

The Saudi Arabia refractories market is set on a strong growth trajectory, supported by industrial expansion, mega infrastructure projects, and favorable government policies. As industries evolve and shift toward more sustainable and efficient production methods, the demand for advanced refractory solutions will continue to rise. Companies that invest in innovation, localization, and sustainable manufacturing will be best positioned to capitalize on the growing opportunities in this dynamic market.

The global polymer foam market was valued at USD 114.88 billion in 2019 and is projected to grow to USD 157.63 billion by 2027, registering a CAGR of 7.73% during the forecast period. Asia Pacific held the largest share of the market in 2019, accounting for 43.84%. In the United States, the polymer foam market is expected to reach USD 23.49 million by 2027, driven by increasing demand across furniture, automotive, and construction insulation applications.

Market Growth and Forecast

The global polymer foam market is witnessing a significant transformation as industries increasingly seek lightweight, durable, and energy-efficient materials. Polymer foams, thanks to their diverse applications and material benefits, are being rapidly adopted across sectors such as construction, automotive, packaging, furniture, and consumer appliances. This shift is fueling consistent growth and driving innovation within the industry.

The market volume is also expanding rapidly, with increasing tonnage expected due to higher utilization in infrastructure and manufacturing applications. The ongoing focus on reducing carbon emissions and improving fuel efficiency further elevates the use of polymer foams in sectors like automotive and building insulation.

List Of Key Companies Covered:

- Sealed Air (U.S.)

- Arkema (France)

- Armacell International S.A. (Germany)

- Borealis AG (Austria)

- Polymer Technologies, Inc. (U.S.)

- Zotefoams plc (UK)

- Synthos (Poland)

- Sekisui Alveo (Switzerland)

- BASF SE (Germany)

Key Market Segments

- By Type

Polymer foams are broadly categorized by the type of polymer used in their production. Among these, polyurethane (PU) foams dominate the market due to their superior flexibility, cushioning properties, and insulation capabilities. PU foams are widely used in furniture, mattresses, automotive seating, and thermal insulation.

Polystyrene foams, including both expanded (EPS) and extruded (XPS) types, hold a significant share owing to their lightweight, cost-effectiveness, and extensive use in packaging and construction insulation. Polyolefin and PVC foams are also gaining traction in automotive and industrial applications due to their chemical resistance and mechanical strength.

- By Form

Flexible and rigid foams cater to different industrial needs. Flexible foams are preferred for applications requiring softness and resilience, such as furniture, bedding, and vehicle interiors. Rigid foams, on the other hand, are extensively used in structural insulation panels, refrigeration systems, and protective packaging due to their high thermal resistance and durability.

- By Application

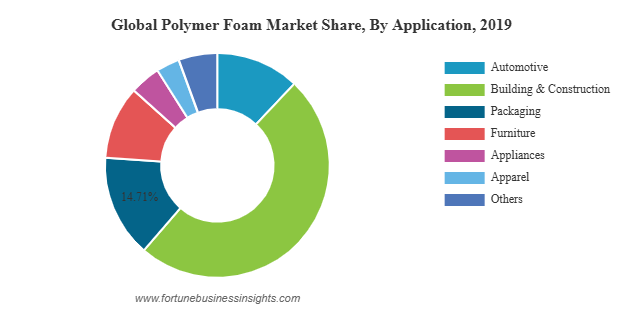

Construction is the leading application segment in the polymer foam market. The need for thermal and acoustic insulation in residential and commercial buildings has spurred the demand for various foam products. As global building codes increasingly require energy-efficient structures, the role of polymer foams becomes even more critical.

In the automotive sector, foams contribute to weight reduction and improved fuel economy while enhancing passenger comfort and safety. Additionally, the packaging industry utilizes polymer foams for their cushioning and protective properties. Other notable applications include footwear, sports equipment, wind turbines, marine products, and appliances.

Read More : https://www.fortunebusinessinsights.com/industry-reports/polymer-foam-market-101698

Regional Insights

- Asia Pacific remains the largest and fastest-growing region in the global polymer foam market. Countries like China, India, Japan, and South Korea are driving demand due to rapid urbanization, industrial growth, and increasing infrastructure investments. Government initiatives supporting energy efficiency and green buildings further contribute to market expansion in the region.

- North America continues to hold a strong position, led by technological advancements, high standards in construction, and a well-established automotive industry. The region is also witnessing increased adoption of bio-based and recycled foam products, aligning with sustainability goals.

- Europe follows closely, with demand driven by stringent energy efficiency regulations, sustainable construction practices, and a mature automotive market. The Middle East & Africa and Latin America regions are also showing steady growth as industrialization and urban development accelerate.

Key Industry Developments

- August 2019: Sheela Foam Limited, largest manufacturer of mattresses and foam based in India, acquired Interplasp SL, a Spanish Company, which has an annual production of 11,000 tons (total capacity 22,000 tons) of polyurethane foam for bedding and furniture applications.

- March 2019: Sika AG, a specialty chemical manufacturer of bonding, damping, sealing, reinforcing solutions for automotive and construction industries, acquired Belineco LLC, a Belarus-based producer of polyurethane foam systems. With this acquisition, Sika is further expected to develop its technology to manufacture polyurethane foams.

Key Drivers of Market Growth

- Sustainability and Energy Efficiency

As energy conservation becomes a global priority, the demand for polymer foams in insulation and fuel-saving applications is rising. Foams help reduce energy loss in buildings and improve vehicle performance by minimizing weight. - Technological Advancements

The development of innovative foaming technologies, such as microcellular and nanocellular foams, allows for improved performance, customization, and environmental compliance. Advanced manufacturing methods are also making foam production more cost-effective and efficient. - Consumer Lifestyle Changes

The growing middle class and changing lifestyles are increasing the demand for high-quality consumer goods like furniture, appliances, and footwear—all of which use polymer foams extensively. - Automotive Lightweighting Trends

Automakers are investing heavily in lightweight materials to meet emission regulations and boost electric vehicle efficiency. Polymer foams are key to achieving these objectives without compromising on comfort or safety. - Boom in E-Commerce and Packaging

The surge in online shopping and logistics services has created a significant need for protective and flexible packaging materials. Polymer foams offer an ideal solution for safeguarding goods during transport.

Challenges and Restraints

Despite its strong outlook, the polymer foam market faces certain challenges. Fluctuations in raw material prices, particularly petroleum-based derivatives, can impact production costs. Environmental concerns regarding foam waste and disposal are prompting stricter regulations, especially on single-use and non-biodegradable foams.

Additionally, the transition to bio-based and recyclable alternatives requires substantial investment in R&D and production infrastructure. Companies need to balance innovation with cost management to stay competitive.

Competitive Landscape

The polymer foam market is highly competitive, with several global and regional players. Major companies such as BASF SE, Covestro AG, Recticel Group, Dow Inc., Huntsman Corporation, and Armacell International S.A. are focusing on product development, strategic collaborations, and sustainability initiatives. These companies are leveraging their technical expertise and manufacturing capacities to meet growing global demand while also addressing environmental and regulatory challenges.

Future Outlook

The future of the polymer foam market looks promising, with sustained growth expected over the coming years. Market players are increasingly focusing on circular economy practices, including recycling and reusing foam materials. Innovations in green chemistry, biodegradable foams, and low-emission manufacturing processes are also shaping the future landscape.

As industries prioritize performance, efficiency, and environmental responsibility, polymer foams will continue to play a pivotal role across a wide range of applications. The market is well-positioned for long-term expansion, supported by technological innovation, regulatory compliance, and rising global demand.

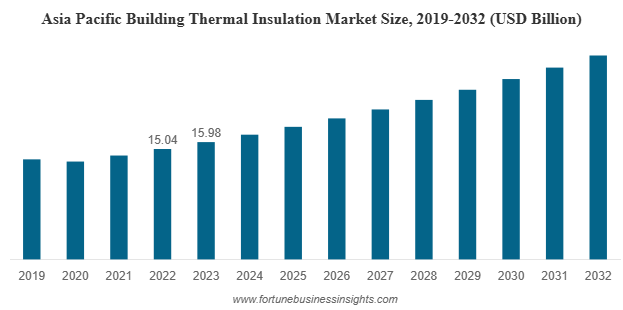

Building Thermal Insulation Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-06

The global building thermal insulation market was valued at USD 32.53 billion in 2023 and is anticipated to rise from USD 33.98 billion in 2024 to USD 48.60 billion by 2032, registering a CAGR of 4.5% during the 2024–2032 forecast period. Asia Pacific led the market in 2023 with a dominant 49.12% share. In the United States, the market is expected to witness substantial growth, reaching approximately USD 7.60 billion by 2032, supported by strong government initiatives promoting energy-efficient technologies in the building and construction sector.

Market Size and Growth Projection

The global building thermal insulation market is undergoing a significant transformation, driven by growing awareness of energy efficiency, sustainability goals, and government regulations promoting green construction practices. As urbanization accelerates and climate concerns mount, the demand for effective insulation in both residential and commercial buildings is surging across developed and emerging economies alike.

List Of Top Building Thermal Insulation Companies:

- BASF (Germany)

- Atlas Roofing Company (U.S.)

- Cellofoam North America Inc. (U.S.)

- DuPont (U.S.)

- Knauf Insulation (U.S.)

- Owens Corning (U.S.)

- Armacell S.A. (Luxembourg)

- Beijing New Building Material (Group) Co., Ltd. (China)

- Evonik (Germany)

- Bondor Indonesia (Indonesia)

- BYUCKSAN (South Korea)

- Huamei Energy-saving Technology Group Co., Ltd. (China)

- Johns Manville (U.S.)

Key Market Drivers

Several factors are contributing to the growth of the building thermal insulation market. First and foremost is the rising emphasis on reducing energy consumption in buildings, which account for a large share of global energy use. Thermal insulation plays a critical role in maintaining indoor temperature, reducing reliance on heating and cooling systems, and thereby lowering energy bills and greenhouse gas emissions.

Another major driver is the implementation of stringent regulations and energy efficiency standards across countries. Governments in North America, Europe, and parts of Asia are introducing mandates that require new buildings and renovations to incorporate insulation solutions that meet performance benchmarks. The push toward net-zero buildings and sustainable urban development is also encouraging builders and developers to invest in high-quality insulation materials.

In addition, increasing consumer awareness about indoor comfort, air quality, and sustainability is leading homeowners and businesses to prioritize thermal insulation as part of building upgrades. The growing popularity of green building certifications such as LEED, BREEAM, and ENERGY STAR further amplifies the adoption of thermal insulation solutions.

Material Trends and Innovations

The building thermal insulation market encompasses a wide variety of materials, each offering unique thermal, acoustic, and environmental benefits. Mineral wool, including glass wool and stone wool, is the most widely used insulation material, owing to its excellent thermal resistance, non-combustibility, and sound-absorbing properties. Mineral wool held the largest market share in 2024 and is expected to retain its dominance throughout the forecast period.

Foamed plastics, such as expanded polystyrene (EPS), extruded polystyrene (XPS), polyurethane (PU), and polyisocyanurate (PIR), are also gaining traction due to their lightweight nature, low thermal conductivity, and ease of installation. These materials are especially popular in commercial and industrial buildings where performance requirements are stringent.

Emerging insulation materials like aerogels, vacuum insulated panels (VIPs), and bio-based cellulose are gaining attention for their superior thermal performance and eco-friendliness. Aerogels, for instance, offer unmatched insulation in ultra-thin profiles, making them ideal for space-constrained applications. Recycled materials and natural fibers are also being explored to align with the growing demand for circular economy practices in construction.

Read More : https://www.fortunebusinessinsights.com/building-thermal-insulation-market-102708

Application and End-Use Segmentation

- Thermal insulation is applied in various parts of a building envelope, including roofs, walls, floors, ceilings, and basements. Roof insulation accounted for the highest market share in 2024, driven by the large surface area exposed to direct sunlight and the need to prevent heat gain or loss. Wall insulation is also a crucial segment, particularly in colder regions where heat retention is a priority.

- In terms of end-use, the residential sector dominates the market with a significant share. This is due to rising homeownership rates, government subsidies for energy-efficient housing, and consumer preference for comfortable living environments. However, the commercial segment is witnessing rapid growth, especially in office buildings, hotels, hospitals, and educational institutions that seek to reduce operational costs through energy-efficient retrofits.

Regional Market Insights

- Asia Pacific leads the global building thermal insulation market in terms of volume and is expected to maintain its dominance due to booming construction activities in China, India, and Southeast Asia. Rapid urbanization, rising middle-class income, and supportive government initiatives are boosting insulation adoption in both new builds and refurbishments.

- Europe is another major market, supported by stringent energy performance directives, widespread use of green building certifications, and a strong focus on decarbonizing the building sector. Countries like Germany, France, and the Nordic nations are investing heavily in thermal renovation of old building stock.

- North America, particularly the United States, is showing robust growth driven by infrastructure modernization, energy efficiency incentives, and heightened awareness about building sustainability. The U.S. market is projected to reach USD 7.60 billion by 2032, fueled by the adoption of advanced materials and smart insulation technologies.

Key Industry Developments:

- April 2021 – Atlas Roofing Company introduced SureSlope prefabricated tapered products. The new product family of polyiso roof insulation components is ideal for roofing applications, reducing job site waste and decreasing installation time.

- March 2021 - Owens Corning acquired vliepa GmbH, a company specializing in coating, printing, and finishing nonwovens, film, and paper for the construction industry. The acquisition widens the company’s nonwovens portfolio for European customers working in the regional construction industry.

Challenges and Opportunities

Despite strong growth prospects, the building thermal insulation market faces certain challenges. Fluctuating raw material prices, labor shortages in the construction industry, and limited awareness in developing countries may hinder growth to some extent. Moreover, some insulation materials face scrutiny due to their environmental impact, prompting manufacturers to innovate toward greener alternatives.

However, the opportunities far outweigh the challenges. Innovations in prefabricated and modular construction, smart building technologies, and high-performance insulation systems are opening new avenues for market expansion. The shift toward energy-neutral and sustainable buildings will continue to create strong demand for advanced insulation solutions globally.

Future Outlook

The global building thermal insulation market is poised for sustainable long-term growth, driven by energy efficiency mandates, consumer demand for comfort, and the transition toward low-carbon construction. As insulation technologies evolve and become more accessible, they will play an even more crucial role in shaping the buildings of the future—ones that are smarter, greener, and more energy efficient.