Personal Protective Equipment Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-13

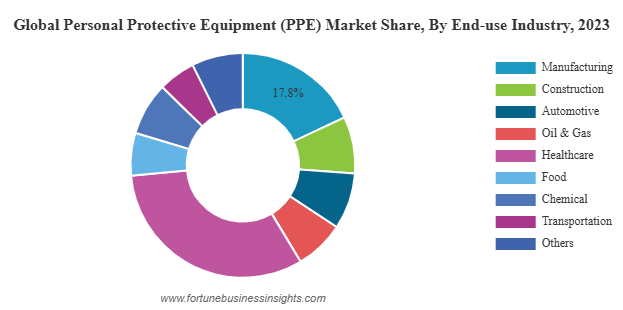

The global personal protective equipment (PPE) market was valued at USD 83.91 billion in 2023 and is expected to increase from USD 87.69 billion in 2024 to USD 128.57 billion by 2032, registering a CAGR of 4.9% during the forecast period. North America led the market in 2023 with a 33.69% share, while the U.S. market is projected to reach USD 37.98 billion by 2032, fueled by expanding infrastructure and construction activities.

The global Personal Protective Equipment (PPE) market has emerged as a vital component of workplace safety, driven by stringent occupational safety regulations, rising awareness about worker health, and the increasing prevalence of industrial hazards. PPE encompasses a wide range of products designed to safeguard workers from physical, chemical, electrical, and biological risks, including protective clothing, helmets, gloves, safety footwear, eye protection, and respiratory protection equipment. The market has experienced substantial growth in recent years, fueled by expanding industrialization, construction activities, healthcare sector advancements, and heightened preparedness for infectious disease outbreaks.

Market Overview

In recent years, the PPE market has grown from being a compliance-driven industry to a safety-first approach, where companies view protective equipment not just as a legal requirement but as an integral part of productivity and employee well-being. This transformation has been further accelerated by global health crises, such as the COVID-19 pandemic, which significantly increased demand for masks, face shields, gloves, and full-body protective suits across multiple sectors. The heightened demand extended beyond healthcare into manufacturing, retail, and public services.

Government bodies worldwide have strengthened workplace safety standards, leading to a rise in the adoption of advanced protective solutions. The International Labour Organization (ILO) and various national regulatory authorities emphasize the importance of providing PPE in high-risk work environments, driving sustained demand.

List Of Top PPE Companies:

- 3M (U.S.)

- Ansell Ltd. (Australia)

- Alpha ProTech (Canada)

- DuPont (U.S.)

- Avon Rubber p.l.c. (U.K.)

- Mallcom (India) Limited (India)

- Bullard (U.S.)

- Delta Plus Group (France)

- Supermax Corporation Berhad (Malaysia)

- MSA Safety (U.S.)

- Honeywell International, Inc. (U.S.)

Key Market Drivers

- Stringent Safety Regulations – Governments and industry bodies mandate the use of PPE in sectors such as oil & gas, mining, construction, and manufacturing to minimize occupational hazards. These regulations directly boost PPE consumption.

- Industrial Expansion – Rapid growth in construction projects, infrastructure development, and manufacturing activities in emerging economies increases the need for PPE to ensure workforce safety.

- Healthcare Sector Growth – Rising healthcare infrastructure investment, coupled with the threat of infectious diseases, supports consistent demand for medical PPE, including gowns, gloves, and masks.

- Technological Advancements – The industry is witnessing innovations in materials and design, such as lightweight, breathable fabrics, enhanced ergonomic features, and integrated safety monitoring systems.

- Awareness & Training Programs – Organizations increasingly invest in employee safety awareness and training, leading to better compliance with PPE usage guidelines.

Read More : https://www.fortunebusinessinsights.com/personal-protective-equipment-ppe-market-102015

Segment Analysis

The PPE market can be broadly segmented into product type, end-use industry, and geography.

- By Product Type: Head protection, eye and face protection, hearing protection, protective clothing, respiratory protection, hand protection, and foot protection. Among these, hand protection and protective clothing dominate due to widespread use across industries.

- By End-Use Industry: Construction, manufacturing, oil & gas, healthcare, mining, chemicals, food processing, and transportation. Healthcare witnessed exponential demand growth during the pandemic, while construction remains a long-term driver.

- By Geography: North America leads in PPE adoption, driven by strict workplace safety regulations and strong healthcare infrastructure. Europe follows closely, emphasizing compliance with EU safety standards. Asia Pacific is the fastest-growing region, with countries like China and India expanding manufacturing and construction activities.

Regional Insights

- North America: The region maintains a strong market share due to OSHA-enforced safety guidelines and high awareness levels.

- Europe: Sustainability trends are influencing PPE production, with a focus on recyclable and eco-friendly materials.

- Asia Pacific: Rapid industrial growth, urbanization, and rising worker safety awareness drive strong market potential.

- Latin America & Middle East: Ongoing oil & gas exploration and infrastructure projects support steady PPE demand.

Key Industry Developments:

- March 2023: Ansell opened its Greenfield Manufacturing Plant in India, investing USD 80 million in the plant. The new facility aims at providing the most innovative and highest quality surgical gloves to healthcare professionals across the country.

- April 2022: Honeywell acquired Norcross Safety Products L.L.C., a manufacturer of PPE, for USD 1.2 billion. This acquisition would provide the company with a platform in the fragmented global business projected to provide significant growth opportunities. This investment in Norcross allows the company to enter into a highly regulated industrial safety market completely.

Challenges Facing the Market

While growth opportunities are abundant, the PPE market faces certain challenges:

- Cost Constraints – High-quality PPE can be expensive, limiting adoption in small-scale industries and low-income regions.

- Comfort vs. Protection Trade-offs – Users sometimes avoid PPE due to discomfort, especially in hot climates, prompting manufacturers to focus on ergonomic design improvements.

- Counterfeit Products – The presence of low-quality, uncertified products in the market poses risks to worker safety and undermines trust in legitimate PPE brands.

Future Outlook

The PPE market is set to witness robust growth through 2032, with increasing integration of smart technologies such as wearable sensors that monitor environmental conditions and worker vitals. Additionally, sustainability will become a central theme, with manufacturers investing in eco-friendly materials and recycling programs.

The demand for PPE market will remain strong across traditional sectors like manufacturing, mining, and oil & gas, while newer opportunities will arise in industries such as renewable energy and biotechnology. E-commerce platforms are also expanding PPE accessibility, enabling smaller companies to source quality equipment with ease.

The global PPE market stands at the intersection of safety, innovation, and compliance. As industries evolve and new workplace risks emerge, the demand for high-quality, comfortable, and technologically advanced PPE will continue to grow. With ongoing innovation and government support, the sector is well-positioned for sustained expansion, ensuring the protection and well-being of workers worldwide.

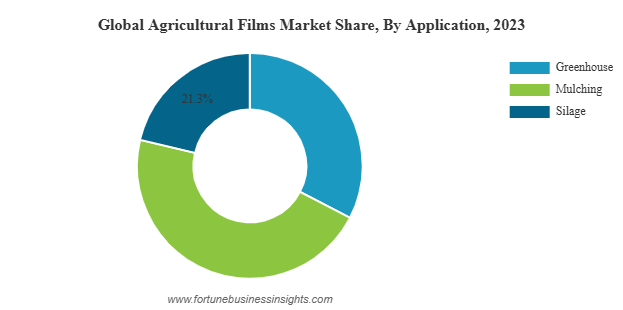

The global agricultural films market was valued at USD 11.28 billion in 2023 and is expected to increase from USD 11.96 billion in 2024 to USD 19.66 billion by 2032, registering a CAGR of 6.3% over the forecast period. Asia Pacific led the market in 2023 with a 53.81% share, while the U.S. market is projected to reach USD 2.57 billion by 2032, fueled by rising demand across diverse plasticulture agricultural applications.

Market Size & Growth Outlook

The global agricultural films market has emerged as a key contributor to modern farming efficiency, helping farmers boost productivity, conserve resources, and adopt sustainable practices. These films, which include mulching films, greenhouse films, and silage films, play a vital role in crop protection, water conservation, soil health management, and yield enhancement. With increasing pressure to feed a growing global population and combat climate challenges, demand for advanced agricultural films is steadily rising across regions.

List Of Key Companies Profiled:

- Rani Plast (Finland)

- Armando Alvarez (Spain)

- BASF SE (Germany)

- Berry Global Inc. (U.S.)

- Kuraray Co., Ltd. (Japan)

- Coveris (U.K.)

- rkw Group (Germany)

- Trioworld Industrier AB (Sweden)

- Exxon Mobil Corporation (U.S.)

- Groupe Barbier (France)

- Novamont S.p.A (Italy)

Key Market Drivers

- Rising Food Demand

Global population growth continues to put pressure on the agricultural sector to produce more food with limited resources. Agricultural films improve crop yields by creating optimal growing conditions, extending growing seasons, and reducing the risks of pests, weeds, and adverse weather.

- Technological Advancements

Modern agricultural films now incorporate multi-layer structures, UV-blocking agents, infrared filters, and anti-drip properties. These innovations enable farmers to better control temperature, humidity, and light exposure for crops, directly improving quality and productivity.

- Water Conservation Efforts

In water-scarce regions, agricultural films help retain soil moisture, reduce evaporation, and minimize irrigation requirements. This function is particularly important in areas facing drought and water management challenges.

- Sustainability Trends

Environmental concerns are pushing the market toward biodegradable and recyclable film solutions. These alternatives help reduce plastic waste while maintaining the benefits of traditional films, making them increasingly popular among environmentally conscious farmers and regions with strict environmental regulations.

Read More : https://www.fortunebusinessinsights.com/agricultural-films- market-102701

Market Segmentation

By Application

- Mulching Films: Represent the largest segment, accounting for more than 40% of the market in 2023. They are widely used for weed suppression, soil temperature control, and moisture retention.

- Greenhouse Films: Expected to see the fastest growth due to increasing greenhouse farming, particularly in regions with harsh climatic conditions. These films enable year- round cultivation and protect crops from pests and extreme temperatures.

- Silage Films: Used primarily for preserving animal feed, ensuring high nutritional value for livestock throughout the year.

By Material

- LLDPE (Linear Low-Density Polyethylene): Dominates the market due to its flexibility, durability, and cost-effectiveness.

- LDPE (Low-Density Polyethylene): Valued for its transparency and ease of processing, used in specific applications like greenhouse covers.

- EVA (Ethylene Vinyl Acetate): Anticipated to grow rapidly because of its clarity, UV resistance, and compatibility with biodegradable formulations.

- Others: Including biodegradable plastics and specialty polymers tailored for niche farming needs.

Regional Insights

- Asia-Pacific: The largest and fastest-growing market, holding over 50% of global share in 2023. Countries such as China, India, and Japan lead adoption due to expanding agricultural activity, government support for modern farming methods, and the growing use of protected cultivation.

- North America: A mature market with high adoption of advanced and eco-friendly agricultural films. Demand is supported by technological innovation and the shift toward sustainable farming practices.

- Europe: Driven by stringent environmental regulations and increasing popularity of organic farming. European farmers are adopting biodegradable films at a faster pace compared to other regions.

- Middle East & Africa: Growth is fueled by the need to maximize productivity in arid climates and the expansion of greenhouse farming to combat extreme weather conditions.

- Latin America: Countries like Brazil and Argentina are adopting agricultural films to support large-scale farming operations and improve crop yields in both staple and cash crops.

Opportunities & Challenges

Opportunities

- Development of fully biodegradable films that match the performance of traditional plastics.

- Integration of “smart” films that monitor and adjust growing conditions automatically.

- Expansion in emerging markets with untapped potential for protected agriculture.

Challenges

- High initial costs for advanced films can deter small-scale farmers.

- Limited recycling infrastructure in certain regions, causing environmental concerns for non-biodegradable films.

- Fluctuating raw material prices affecting production costs.

Key Industry Developments:

- March 2023– Rani Plast and eight other progressive companies announced collaboration on a novel nation-wide recycling collection system. The move is expected to help reduce

- difficulties in the disposal of used agricultural plastic.

- May 2022 – Berry Global announced a collaboration with CleanFarms and Poly-Ag Recycling on a close-loop method for Canada’s Circular economy.

Future Trends

- Sustainable Materials: The push for eco-friendly products will drive research and investment into biodegradable polymers and recyclable plastics.

- Precision Agriculture Integration: Films embedded with sensors could provide real- time data on soil moisture, temperature, and crop health.

- Multi-Functional Films: Combining multiple benefits such as pest resistance, nutrient delivery, and light diffusion in a single product.

- Government Incentives: Subsidies and grants encouraging adoption of agricultural films, especially in developing countries.

Outlook

The agricultural films market is set for strong growth over the next decade, supported by population growth, climate challenges, and the need for sustainable farming practices. As technology evolves, films are becoming more advanced, offering better protection, higher yields, and improved environmental performance. With Asia-Pacific leading the charge, other regions are also stepping up adoption, making agricultural films a vital component of global food security and modern agriculture.

Aerospace and Defense Materials Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-12

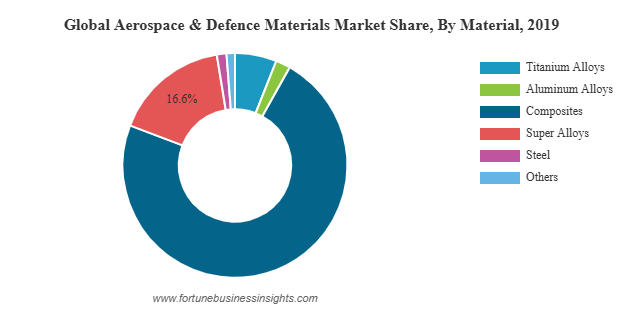

In 2019, the global aerospace and defense materials market was valued at USD 18,411.83 million and is expected to reach USD 23,825.45 million by 2027, registering a CAGR of 4.21% over the forecast period. North America led the market in 2019 with a 53.65% share, while the U.S. market alone is anticipated to hit USD 12,019.42 million by 2027, driven by advancements in lightweight and high-performance materials.

Market Size & Forecast

The aerospace and defense materials market is witnessing substantial growth as advancements in technology, manufacturing processes, and material science reshape the sector. From next-generation fighter jets to commercial aircraft and space exploration vehicles, the demand for lighter, stronger, and more durable materials is accelerating. Governments, defense organizations, and private aerospace companies are investing heavily in advanced materials that enhance performance, reduce weight, improve fuel efficiency, and meet stringent safety standards.

List Of Key Companies Profiled In Aerospace And Defense Materials Market:

- Arconic Inc. (US)

- Toray Composite Materials America, Inc. (US)

- Huntsman (US)

- Evonik Industries (Germany)

- Hexcel Corporation (US)

- Materion Corp. (US)

- AMI Metals Inc. (US)

- TATA Advanced Materials Limited. (India)

- Koninklijke Ten Cate BV (Netherlands)

- Sofitec (Spain)

- Teijin Ltd. (Renegade Materials Corp.) (Japan)

- Others

Key Growth Drivers

- Rising Aircraft Production

The surge in passenger travel, growth in low-cost carriers, and replacement of aging fleets are increasing the production rates of commercial aircraft. This directly boosts the demand for lightweight and high-performance materials. - Military Modernization Programs

Defense budgets are rising in many nations, with modernization programs focusing on stealth technology, high-speed maneuverability, and survivability. These requirements drive the use of specialized alloys, composites, and advanced ceramics. - Fuel Efficiency & Sustainability

Airlines and defense forces are under pressure to reduce carbon emissions and operating costs. Lightweight materials, particularly composites and advanced aluminum alloys, enable fuel savings while maintaining structural integrity. - Space Exploration & Satellites

The renewed interest in lunar missions, Mars exploration, and satellite deployment increases the demand for materials capable of withstanding extreme temperatures, radiation, and vacuum conditions.

Future Trends

- Sustainability Initiatives

The shift toward recyclable materials and energy-efficient manufacturing processes will continue to shape R&D efforts. - Additive Manufacturing

3D printing is enabling cost-effective production of complex aerospace parts using advanced alloys and composites. - Nanomaterials

The incorporation of nanotechnology can enhance strength, reduce weight, and improve resistance to heat and wear. - Smart Materials

Self-healing composites and shape-memory alloys could revolutionize aerospace maintenance and durability.

Material Segmentation

- Composites

Composites have emerged as the dominant material category, offering exceptional strength-to-weight ratios and corrosion resistance. Carbon fiber reinforced polymers are extensively used in aircraft fuselages, wings, and interior components. - Aluminum Alloys

Aluminum alloys remain critical for aerospace structures due to their light weight, recyclability, and cost-effectiveness. Advanced grades, such as the 7000 series, provide high strength for load-bearing applications. - Titanium Alloys

Titanium is preferred for components exposed to high stress and temperatures, such as landing gear, engine parts, and airframes. Its corrosion resistance makes it valuable for both aerospace and naval defense applications. - Super Alloys & Advanced Metals

Nickel-based and cobalt-based superalloys are essential for high-temperature environments like jet engines and rocket propulsion systems. - Ceramic Matrix Composites (CMCs)

These advanced materials are gaining attention for their lightweight nature and ability to withstand extreme heat, particularly in engine components.

Read More : https://www.fortunebusinessinsights.com/aerospace-defense-materials-market-102980

Regional Insights

- North America

Home to major aerospace manufacturers and defense contractors, North America dominates the global market. The presence of companies involved in both commercial and military aircraft production ensures strong demand for advanced materials. - Europe

With leading players in aircraft manufacturing and defense systems, Europe maintains a strong market share. Strict environmental regulations in the EU drive innovations in lightweight and recyclable materials. - Asia-Pacific

This region is experiencing the fastest growth, driven by rising air passenger traffic, increasing defense budgets, and growing domestic manufacturing capabilities in countries like China, India, and Japan. - Middle East & Africa

Investments in aviation hubs, defense procurement, and infrastructure development are gradually expanding the market presence in these regions.

Challenges Facing the Industry

While growth prospects are strong, several challenges could impact market expansion:

- High Production Costs: Advanced materials, particularly composites and titanium alloys, can be expensive to produce and process.

- Complex Certification Processes: Aerospace materials must meet rigorous safety and performance standards, requiring lengthy testing and approval procedures.

- Supply Chain Vulnerabilities: Dependence on specialized suppliers and raw material sources can create disruptions.

- Geopolitical Risks: Trade restrictions, tariffs, and international tensions can impact material availability and pricing.

Key Industry Developments:

- April 2020 – Hexcel Corporation, an advanced composites manufacturer headquartered in the US, and Woodward, Inc., a key player providing designing, manufacturing and other services in the aerospace industry headquartered in the US, announced mutual termination of merger agreement, which was previously announced in January 2020. The disruption caused by the COVID-19 outbreak has forced the companies to announce the termination of the agreement.

- August 2019 – Teijin Ltd, a Japan-based manufacturer of advanced materials and chemicals, announced the successful acquisition of Renegade Materials Corporation, a key supplier of highly heat-resistant thermoset prepreg for the aerospace industry in North America. This has strengthened Tenjin’s position in the aerospace business and also increased its manufacturing capabilities.

Outlook

The aerospace and defense materials market is on a steady growth trajectory, powered by advancements in technology, rising global defense spending, and the relentless pursuit of lighter, stronger, and more sustainable materials. Companies that focus on innovation, cost efficiency, and sustainability are well-positioned to capture growth opportunities in the years ahead. As commercial aviation, defense modernization, and space exploration continue to expand, the demand for cutting-edge materials will only intensify, making this sector one of the most dynamic in the global economy.

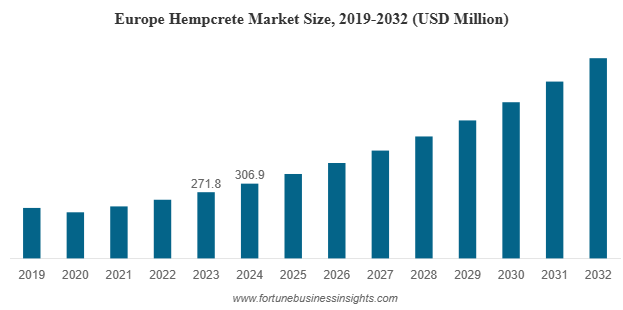

In 2024, the global hempcrete market was valued at USD 804.8 million and is anticipated to expand from USD 910.1 million in 2025 to USD 2,183.3 million by 2032, registering a CAGR of 13.3% during 2025–2032.

The global hempcrete market has been expanding rapidly in recent years and is set to maintain a strong growth trajectory in the coming decade. Rising awareness of green building materials, combined with stringent environmental regulations, is driving demand across residential, commercial, and public infrastructure projects.

Market Overview and Growth Potential

The construction industry is undergoing a transformation as sustainability takes center stage. Among the innovative materials emerging in this space, hempcrete market has garnered significant attention for its eco-friendly, durable, and energy-efficient properties. Made from the woody core of the hemp plant mixed with a lime-based binder, hempcrete market offers an alternative to traditional concrete that not only performs well but also has a negative carbon footprint.

The rising cost of energy has also strengthened the case for hempcrete market. Its superior thermal insulation properties help reduce heating and cooling needs, lowering energy bills and improving overall building efficiency. As a result, it is increasingly being chosen for projects where operational cost savings and sustainability go hand in hand.

List Of Key Hempcrete Companies Profiled

- Australian Hemp Masonry Company (Australia)

- Sativa Building Products (U.S.)

- IsoHemp (Belgium)

- Hempitecture (U.S.)

- Hemp Homes Australia (Australia)

- Carmeuse Group (Belgium)

- Rare Earth Global (U.K.)

- UK Hempcrete (U.K.)

- Hempbuild Sustainable Products Ltd. (Ireland)

- The Hempcrete Co. (Australia)

- The Hemp Block Company (U.K.)

Key Market Drivers

- Carbon-Negative Properties

Unlike traditional cement-based concrete, which emits significant amounts of carbon dioxide during production, hempcrete market absorbs carbon over its lifecycle. The hemp plant captures CO₂ during its growth, and the lime binder continues to absorb carbon as it sets. This makes hempcrete market one of the few building materials that can actively reduce the carbon footprint of a project. - Thermal and Acoustic Performance

Hempcrete’s porous structure allows it to provide excellent insulation, regulating indoor temperatures and reducing reliance on heating or air conditioning systems. Additionally, it offers effective soundproofing, making it ideal for urban residential and office spaces. - Health and Comfort

Hempcrete market is a breathable material, meaning it allows moisture to pass through without trapping it inside walls. This helps prevent mold growth and improves indoor air quality, creating a healthier living environment. - Supportive Regulatory Environment

Governments across Europe, North America, and parts of Asia-Pacific are encouraging the use of low-carbon building materials through subsidies, tax incentives, and stricter green building codes. This has opened new opportunities for hempcrete producers and builders. - Innovation in Application

The industry is seeing advances such as pre-cast hempcrete blocks, spray-applied hempcrete for faster installation, and hybrid mixes that enhance strength and durability. These innovations are expanding the range of projects where hempcrete can be used.

Regional Insights

- North America: The United States and Canada are leading the adoption of hempcrete in the region. The legalization of industrial hemp cultivation and growing interest in sustainable construction have boosted market growth.

- Europe: This region has been at the forefront of hempcrete usage, driven by ambitious carbon-reduction targets and mature hemp farming sectors in countries like France, the UK, and the Netherlands.

- Asia-Pacific: Markets such as China and India are emerging as important players. China benefits from large-scale hemp cultivation, while India’s growing construction sector and sustainability initiatives present significant potential.

- Latin America and Middle East & Africa: These regions are in the early stages of hempcrete adoption but show promise due to increasing urban development and interest in affordable, eco-friendly housing.

Read More : https://www.fortunebusinessinsights.com/hempcrete-market-110107

Applications

- Residential Construction

Hempcrete is gaining popularity in residential projects for its fire resistance, non-toxic composition, and energy efficiency. Homeowners are increasingly opting for hempcrete walls, insulation, and flooring to create comfortable, sustainable living spaces. - Commercial and Public Buildings

Office complexes, schools, and community centers are adopting hempcrete to meet green building certifications and reduce operational costs. Its acoustic insulation makes it particularly suitable for spaces where noise reduction is essential. - Restoration and Retrofitting

Hempcrete is being used in heritage building restoration due to its compatibility with older materials and ability to enhance thermal performance without compromising structural integrity.

Key Industry Developments

- March 2024: The Australian Hemp Masonry Company reported a significant increase in their hempcrete production, tripling their annual supply to 120 homes from 40 homes per year over the past decade. This growth highlights the increasing demand for sustainable and eco-friendly building materials such as hempcrete.

- January 2024: The International Code Council (ICC) added an appendix on hemp-lime construction to its 2024 International Residential Code (IRC). Such developments are helpful for builders to obtain permits and approvals to use hempcrete.

Challenges Facing the Market

While the hempcrete market outlook is positive, certain challenges remain:

- Higher Upfront Costs: Although hempcrete can lead to long-term savings through reduced energy use, its initial costs are often higher than traditional materials.

- Limited Structural Strength: Hempcrete is non-load-bearing, meaning it requires a structural frame. This can limit its application in some large-scale projects.

- Awareness and Training Gaps: Many builders and architects are still unfamiliar with hempcrete, market and specialized training is often needed to use it effectively.

- Supply Chain Limitations: In some regions, industrial hemp cultivation and processing infrastructure are underdeveloped, leading to inconsistent availability.

Future Outlook

The hempcrete market is poised for sustained growth as more stakeholders recognize its environmental and functional benefits. Continued innovation in material science and manufacturing processes is likely to address current limitations, such as structural strength and cost efficiency. Expanding hemp cultivation globally will also help stabilize supply and reduce material costs over time.

As cities and countries work toward net-zero emission targets, hempcrete’s market carbon-negative credentials will become even more valuable. Combined with its ability to improve indoor comfort, reduce energy use, and support healthier living environments, hempcrete market is set to play a vital role in the future of sustainable construction.

Hempcrete market is more than just a niche alternative—it is a practical, scalable, and environmentally responsible material that meets the demands of modern construction. Its combination of durability, insulation, breathability, and eco-friendliness positions it as a key player in the green building revolution. With supportive policies, growing public awareness, and ongoing technological advancements, the hempcrete market is expected to remain on a strong upward path in the years ahead.

Aluminum Composite Panels Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-12

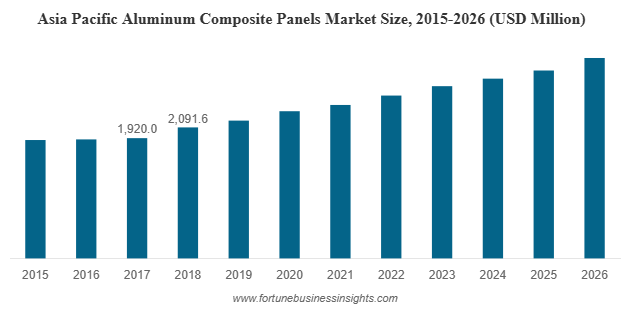

The global aluminum composite panels market was valued at USD 5.33 billion in 2018 and is anticipated to reach USD 8.71 billion by 2026, reflecting a CAGR of 6.1% over the forecast period. In 2018, Asia Pacific led the market with a 39.23% share. In the United States, the market is expected to witness strong growth, projected to reach USD 2.41 billion by 2032, supported by favorable policies and initiatives aimed at enhancing infrastructure across North America.

Market Overview

The aluminum composite panels (ACP) market has been witnessing significant growth in recent years, driven by the rapid pace of urbanization, rising construction activities, and increasing demand for lightweight yet durable building materials. ACPs, which consist of two thin layers of aluminum bonded to a non-aluminum core, are known for their excellent structural strength, flexibility, and aesthetic appeal. They are widely used in applications such as building facades, signage, interior decoration, and transportation.

List Of Key Companies Profiled In Aluminum Composite Panels Market:

- 3A Composites GmbH

- Arconic

- Mitsubishi Chemical Corporation

- Hyundai Alcomax Co.,Ltd.

- Fairfield Metal LLC

- Jyi Shyang Industrial Co., Ltd.

- ALUMAX INDUSTRIAL CO., LTD.

- Yatai Industrial Group Co., Ltd.

- Shanghai Huayuan New Composite Materials Co., Ltd.

- Guangzhou Xinghe Aluminum Composite Panel Co., Ltd.

Key Market Drivers

- Boom in the Construction Industry

Urbanization and industrial development, particularly in Asia-Pacific countries, have created a surge in demand for modern building materials. ACPs are increasingly preferred in the construction of commercial complexes, high-rise buildings, airports, and residential projects due to their lightweight nature, ease of installation, and ability to withstand extreme weather conditions. - Aesthetic Versatility

Architects and designers appreciate ACPs for their wide range of colors, textures, and finishes. Whether replicating the look of natural stone, wood, or metallic surfaces, ACPs provide cost-effective solutions without compromising visual appeal. This versatility has made them a go-to material for both new construction and renovation projects. - Safety and Functional Improvements

Growing awareness about building safety has pushed demand for fire-resistant ACPs. Manufacturers are introducing mineral-filled cores and advanced coatings that enhance fire resistance, corrosion protection, and UV stability. Antibacterial and anti-toxic panels are also gaining traction, particularly in healthcare, food processing, and public infrastructure projects. - Rising Demand in Signage and Advertising

Beyond construction, ACPs are widely used in outdoor advertising and signage due to their smooth surface, durability, and ability to withstand exposure to sunlight and rain without fading. This segment has seen robust growth with the expansion of retail spaces, transport hubs, and commercial branding. - Technological Advancements

Digital printing technology, nano-coatings for self-cleaning surfaces, and eco-friendly production methods are expanding ACP capabilities. These innovations are making the panels more durable, sustainable, and adaptable to custom design requirements.

Read More : https://www.fortunebusinessinsights.com/aluminum-composite-panels-market-102304

Regional Insights

- Asia-Pacific remains the dominant market for ACPs, accounting for the largest share globally. China, India, and Southeast Asian nations are driving this growth through massive infrastructure projects, affordable housing initiatives, and rapid industrialization. The region’s focus on modernizing city skylines has kept demand high for premium-grade panels.

- North America is experiencing steady growth, supported by infrastructure upgrades, energy-efficient building designs, and increased adoption of ACP in both commercial and residential segments. In the United States, the market benefits from a combination of technological innovation and strong demand from the automotive and transport sectors.

- Europe is focusing on sustainable building solutions, with ACPs playing a key role in energy-efficient facades and renovation projects. Strict building regulations and fire safety standards in countries like Germany, France, and the UK have fueled demand for high-quality, fire-rated panels.

- Latin America and the Middle East & Africa are emerging as promising markets. Economic development, rising construction investment, and urban population growth are creating opportunities for ACP suppliers in these regions.

Market Challenges

Despite its growth potential, the ACP market faces certain challenges:

- Price Volatility of Raw Materials: Fluctuations in the price of aluminum can impact production costs, making it challenging for manufacturers to maintain competitive pricing.

- Regulatory Pressure: Stricter fire safety regulations in some countries have led to increased scrutiny of ACPs with polyethylene cores. While safer mineral-core panels meet compliance standards, they come at a higher cost.

- Competition from Alternative Materials: Glass, fiber cement, and other cladding materials offer alternative solutions, requiring ACP manufacturers to continuously innovate to maintain market share.

Key Industry Developments:

- July 2017 – Fairview Architectural acquired the Stryum business, an intelligent non-combustible aluminum cladding system, from Vitekk Industries. The company includes a variety of high-quality aluminum plate façade panels designed to provide durability and sustainability, complimenting Fairview's current portfolio of cladding solutions, including high-density cement fibre, natural stone, terracotta tiles and the leading non-combustible composite aluminum frame.

Future Outlook

The future of the ACP market appears promising, with several trends shaping its evolution:

- Sustainability and Eco-Friendly Panels: Growing environmental consciousness is pushing manufacturers to develop recyclable ACPs and use eco-friendly production processes.

- Integration with Smart Building Technologies: Panels with integrated solar capabilities and advanced coatings that respond to environmental changes are expected to gain traction.

- Customization and Niche Applications: Demand for custom designs, special finishes, and tailored panel sizes will continue to grow as architects seek more creative freedom.

- Global Expansion of Urban Infrastructure: Mega-projects in emerging economies and renovations in developed nations will ensure a stable flow of demand.

Aluminum composite panels market have evolved from being a niche building material to a core component in modern construction, signage, and transportation industries. Their blend of lightweight strength, design flexibility, and evolving safety features makes them indispensable in today’s market. As global cities continue to expand and building regulations become stricter, ACPs are well-positioned to meet the demands of safety, sustainability, and style. With continuous innovation, the industry is set to maintain its upward trajectory and unlock new opportunities worldwide.

Thermoplastic Elastomer (TPE) Market Demand, Drivers & Global Growth, Forecast 2032

By Sharvari, 2025-08-11

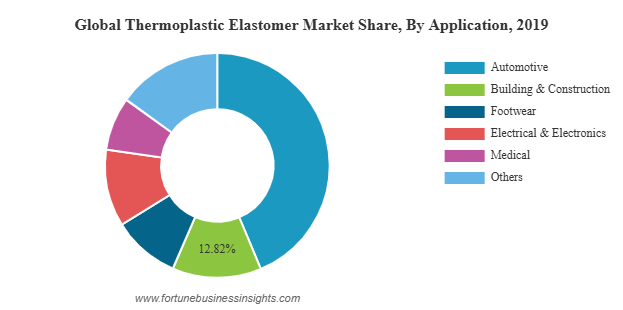

The global thermoplastic elastomer (TPE) market was valued at USD 26,856.8 million in 2019 and is expected to grow to USD 39,424.6 million by 2027, registering a CAGR of 5.7% during the forecast period. In 2019, Asia Pacific led the market, holding a dominant 52.97% share. In the United States, the TPE market is anticipated to reach USD 6,045 million by 2027, fueled by rising demand for lightweight and durable materials across automotive and consumer goods sectors.

Market Size and Growth Outlook

The global Thermoplastic Elastomer (TPE) market is on a strong growth trajectory, driven by increasing demand from automotive, construction, medical, footwear, electronics, and other key industries. TPEs are unique materials that combine the elasticity of rubber with the processability of plastics, offering flexibility, durability, and recyclability. This combination of properties makes them an ideal choice for a wide range of applications, particularly in industries looking for high-performance and sustainable material solutions.

The automotive industry remains the largest consumer of TPEs, using them in products such as seals, gaskets, bumpers, interior components, and weatherproofing materials. Construction, electronics, medical devices, and consumer goods industries are also increasingly adopting TPEs due to their superior performance characteristics.

List Of Key Companies Profiled In Thermoplastic Elastomer Market:

- Arkema SA (Colombes, France)

- Covestro AG (Leverkusen, Germany)

- Evonik Industries AG (Essen, Germany)

- Teknor APEX Company (Rhode Island, U.S.)

- BASF SE (Ludwigshafen, Germany)

- Huntsman Corporation (Texas, U.S.)

- Sinopec Group (Beijing, China)

- Lubrizol Corporation (Ohio, U.S.)

- Kraton Corporation (Texas, U.S.)

- Tosoh Corporation (Tokyo, Japan)

- Other Key Players

Applications Driving Demand

- Automotive Industry – The largest application segment for TPEs. Automakers are increasingly using TPEs for interior trims, instrument panels, seals, and under-the-hood components. These materials not only reduce vehicle weight, which improves fuel efficiency, but also enhance comfort and aesthetics.

- Medical Sector – TPEs are widely used in medical tubing, seals, syringe plungers, and various device housings due to their biocompatibility and sterilization capabilities. The demand for medical-grade TPEs surged during the COVID-19 pandemic, and this segment continues to see growth due to rising healthcare needs.

- Construction Industry – TPEs are used in roofing membranes, seals, and weatherproofing applications thanks to their flexibility and resistance to harsh environmental conditions.

- Footwear Industry – The flexibility, cushioning, and durability of TPEs make them ideal for shoe soles and sports footwear.

- Electronics and Electrical Applications – TPEs are used for cable insulation, connectors, and various protective casings because of their excellent electrical insulation properties and resistance to heat and chemicals.

Read More : https://www.fortunebusinessinsights.com/thermoplastic-elastomer-tpe-market-104515

Key Market Trends

- Shift Toward Bio-based and Recyclable Materials – Growing environmental awareness and stricter regulations are pushing manufacturers to develop bio-based and fully recyclable TPE products.

- Technological Innovations – Advances in polymer chemistry are leading to improved performance characteristics, making TPEs suitable for more demanding applications.

- Lightweighting in Transportation – As the automotive and aerospace industries strive for greater fuel efficiency, lightweight materials like TPEs are gaining more importance.

- Medical-Grade TPE Development – The healthcare industry is demanding materials that are safe, compliant with global regulations, and suitable for repeated sterilization, leading to innovation in medical-grade TPEs.

Regional Insights

- Asia Pacific is the leading regional market for TPE, accounting for over half of the global share in recent years. Countries like China, India, Japan, and South Korea have robust manufacturing bases, particularly in automotive, footwear, electronics, and industrial products. Rapid urbanization, growing infrastructure projects, and increasing disposable incomes in these countries continue to drive demand for TPE products.

- North America is another significant market, with the United States playing a central role due to its advanced automotive and medical sectors. The region is seeing steady growth, supported by consumer demand for high-performance and sustainable products.

- Europe, led by Germany, France, Italy, and the UK, is focusing on lightweighting in vehicles, environmental compliance, and energy efficiency, all of which favor increased use of TPEs. Meanwhile, emerging markets in Latin America, the Middle East, and Africa are projected to see gradual but consistent growth, spurred by industrial expansion and rising consumer goods manufacturing.

Key Industry Developments:

- August 2020: Lubrizol invested in the thermoplastic polyurethane business globally. The investments include the increased production capabilities of surface paint protection film (PPF) and protection. At the same time, it would provide additional benefits to PPF manufacturers and supply chains.

- November 2020: Evonik announced the cooperation with HP for developing a new co-branded1 elastomer, a flexible high-performance specialty powder based on a thermoplastic amide grade (TPA) for 3D printing.

Challenges in the Market

Despite the strong growth outlook, the TPE market faces certain challenges. Volatility in raw material prices, particularly those derived from petroleum, can affect production costs. In addition, competition from alternative materials, such as cheaper plastics or thermoset rubbers, can slow adoption in cost-sensitive markets. Recycling, while possible with TPEs, is still not widely implemented in many regions, limiting the full realization of their sustainability potential.

Leading Industry Players

Major companies operating in the global TPE market include Arkema SA, BASF SE, Covestro AG, Evonik Industries, Huntsman Corporation, Kraton Corporation, Sinopec, Lubrizol Corporation, Teknor Apex, and Tosoh Corporation. These companies are investing heavily in research and development to create advanced, sustainable TPE products, expand production capacity, and strengthen their market positions through strategic partnerships and acquisitions.

Future Outlook

The future of the TPE market looks promising. Growing environmental regulations, increased focus on recyclability, and the need for high-performance materials will continue to push demand upward. As more industries embrace sustainable manufacturing practices, the role of TPEs will expand, particularly in automotive, healthcare, and electronics sectors.

With ongoing innovations, expanding applications, and strong growth in emerging markets, the TPE industry is set to remain a dynamic and competitive sector over the coming decade. Manufacturers that can balance cost, performance, and sustainability are likely to capture the largest share of the market’s future growth.

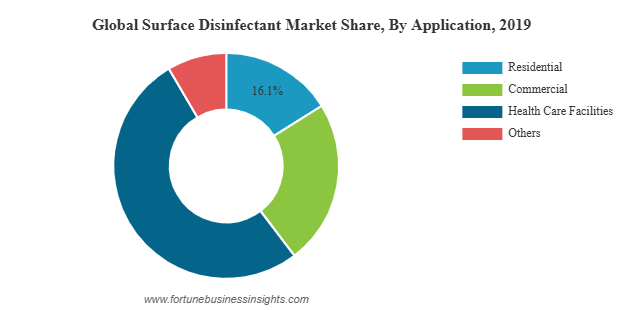

In 2019, the global surface disinfectant market was valued at USD 770.6 million and is anticipated to grow to USD 1,547.7 million by 2027, reflecting a CAGR of 9.1% from 2020 to 2027. North America led the market that year with a 38.92% share. In the U.S., the market is expected to experience substantial expansion, projected to reach USD 524.4 million by 2027. This growth is fueled by rising awareness of sanitation and hygiene, particularly in the aftermath of the pandemic, driving demand across healthcare, residential, and commercial sectors.

Market Size and Growth

The global surface disinfectant market has undergone a remarkable transformation over the past few years, evolving from a primarily healthcare-focused segment into an essential component of public health, commercial hygiene, and household cleaning practices. The COVID-19 pandemic served as a catalyst for unprecedented demand, but even beyond the crisis, awareness of hygiene and sanitation has become deeply embedded in both institutional policies and consumer habits.

North America dominated the global market in 2019, accounting for 38.92% of total revenue. The U.S., in particular, is forecast to experience significant growth, with the market expected to reach USD 524.4 million by 2027. The region’s advanced healthcare infrastructure, rigorous hygiene standards, and strong retail distribution networks have positioned it as a leader in both consumption and innovation.

List of Top Surface Disinfectant Companies:

- 3M (U.S.)

- The Proctor & Gamble Company (U.S.)

- Kimberley-Clark Corporation (U.S.)

- SC Johnson Professional (U.S.)

- The Clorox Company (U.S.)

- Ecolab (U.S.)

- Metrex Research LLC(U.S.)

- Reckitt Benckiser Group Plc (U.K.)

- Diversey Inc.(U.S.)

- STERIS plc (Ireland)

- Whiteley Corporation (Australia)

- Other Key Players

Key Market Drivers

- Post-Pandemic Hygiene Awareness

The global health crisis fundamentally changed public attitudes toward cleanliness. Disinfecting surfaces is no longer viewed as an occasional precaution but as an integral part of daily routines for both households and businesses. Schools, offices, hotels, and restaurants have institutionalized frequent cleaning schedules, driving consistent demand for surface disinfectants. - Healthcare Sector Requirements

Hospitals and clinics are under constant pressure to prevent hospital-acquired infections (HAIs). Regular disinfection of high-touch surfaces such as doorknobs, bed rails, and examination tables is a crucial preventive measure. As healthcare services expand globally, the use of surface disinfectants continues to rise proportionally. - Regulatory Standards

Governments and health authorities have implemented stringent hygiene regulations across multiple sectors. From food processing plants to public transportation hubs, mandatory sanitation protocols ensure steady market demand. - Commercial and Industrial Adoption

Beyond healthcare, industries such as manufacturing, retail, and hospitality have adopted robust disinfection protocols to protect both employees and customers. This widespread adoption has expanded the application base far beyond its traditional boundaries.

Product and Composition Insights

Surface disinfectants are available in multiple forms, each suited to specific applications:

- Liquid Disinfectants dominate the market due to their versatility and ease of application across a wide range of surfaces. They are commonly used in spray bottles, mop buckets, and automated cleaning systems.

- Wipes offer convenience and portability, making them ideal for quick disinfection of personal workspaces, electronic devices, and public seating areas.

- Sprays and Aerosols are gaining traction for their ability to cover large areas quickly and evenly.

In terms of composition, alcohol-based disinfectants lead the market due to their rapid action and proven effectiveness against a broad spectrum of pathogens. However, other formulations, such as chlorine compounds, hydrogen peroxide, quaternary ammonium compounds, and phenolic agents, are also widely used depending on the specific requirements of the application. Increasingly, there is a push toward eco-friendly and less toxic alternatives that meet both efficacy and environmental safety standards.

Read More : https://www.fortunebusinessinsights.com/surface-disinfectant-market-103062

Application Areas

- Healthcare Facilities – Hospitals, clinics, and long-term care centers remain the largest end-users due to the critical need for infection prevention.

- Residential Use – Post-pandemic consumer habits have cemented the role of surface disinfectants in households for everyday cleaning.

- Commercial Establishments – Retail stores, offices, gyms, and hotels use disinfectants to maintain hygiene and instill customer confidence.

- Industrial and Institutional Settings – Schools, transportation systems, and manufacturing plants require large-scale disinfection solutions.

Key Industry Developments:

- January 2019 – Reckitt Benckiser formed a strategic alliance with Diversey to increase its presence in North America. This strategic alliance will help Reckitt Benckiser to expand its reach to educational institutes, food establishments, and hospitals.

- February 2020 – The Procter and Gamble Company launched a new line of antibacterial cleaners named Microban 24. The new product line is said to protect the applied surface for a complete 24 hours, even when the surface has been contacted multiple times.

Regional Overview

- North America: The largest market, driven by strong institutional demand, regulatory enforcement, and high consumer awareness.

- Europe: Focuses on environmentally friendly disinfectants and compliance with strict safety regulations, particularly in healthcare and food industries.

- Asia Pacific: Expected to register the fastest growth, fueled by expanding healthcare infrastructure, urbanization, and increased public health spending in countries such as China and India.

- Latin America and Middle East & Africa: Gradual adoption of advanced disinfection practices, supported by improving public health awareness and infrastructure investments.

Challenges and Opportunities

While the market outlook is positive, it faces certain challenges:

- Raw Material Price Volatility: Fluctuations in the cost of key ingredients can impact production costs and profit margins.

- Health and Safety Concerns: Some chemical disinfectants may pose risks to human health or the environment if not used correctly.

- Competition from Alternative Cleaning Methods: Technologies like UV disinfection and steam cleaning may reduce reliance on chemical solutions in certain environments.

Opportunities exist in developing biodegradable and non-toxic disinfectants, enhancing formulation efficiency, and leveraging automation in large-scale cleaning systems. Innovation in packaging, such as refillable containers and concentrated solutions, can also appeal to eco-conscious consumers.

Competitive Landscape

The market is highly competitive, with leading companies focusing on expanding their product portfolios, improving efficacy, and meeting sustainability goals. Key players are investing in research and development to introduce advanced formulations capable of addressing emerging pathogens while minimizing environmental impact.

Future Outlook

The surface disinfectant market is poised for sustained growth well beyond the pandemic era. Rising global health standards, ongoing threat of infectious diseases, and consumer preference for cleanliness will ensure steady demand. In the coming years, advancements in sustainable chemistry, improved delivery systems, and increased accessibility in emerging markets are likely to define the next phase of market development.

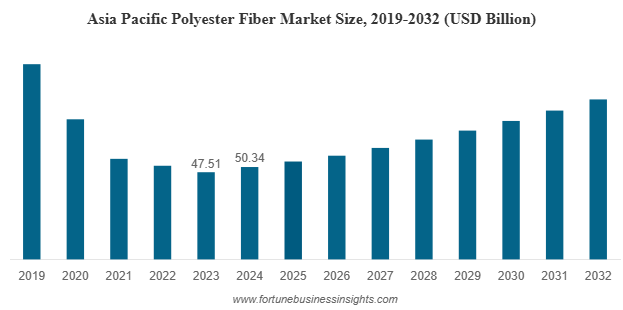

The global polyester fiber market was valued at USD 77.07 billion in 2024 and is expected to increase from USD 82.07 billion in 2025 to USD 129.97 billion by 2032, reflecting a CAGR of 6.8% during the forecast period. In 2024, Asia Pacific led the market, holding a 65.32% share.

Polyester fiber market is one of the most widely used synthetic fibers in the world. Its ability to mimic natural fibers while offering improved durability and affordability makes it the preferred choice in textiles, home furnishings, industrial applications, and even specialized fields like medical textiles.

Growth Drivers

Several factors are contributing to the expansion of the polyester fiber market:

- Rising Apparel Consumption: Fast fashion trends and an increasing global population are driving high volumes of textile production, with polyester as a key raw material.

- Durability and Performance: Polyester’s resistance to wrinkles, shrinking, and stretching makes it a go-to choice for both consumers and manufacturers.

- Industrial Demand: The fiber’s strength and resilience make it ideal for heavy-duty industrial applications, further boosting its market share.

- Cost-Effectiveness: Polyester is cheaper to produce than many natural fibers, making it a competitive option for mass production.

- Technological Advancements: Innovations in fiber engineering have improved polyester’s comfort, breathability, and sustainability, expanding its market reach.

List Of Key Polyester Fiber Companies Profiled

- Reliance Industries Limited. (India)

- Indorama Ventures Public Company Limited. (Thailand)

- Toray Industries, Inc. (Japan)

- Sinopec Yizheng Chemical Fibre Limited Liability Company (China)

- Zhejiang Hengyi Group Co., Ltd (China)

- Tongkun Holding Group (China)

- Sanfame Group (China)

- Far Eastern New Century Corporation (Taiwan)

- Alpek Polyester. (Mexico)

- ADVANSA (Turkey)

Emerging Trends

- Sustainable Polyester: Environmental concerns are pushing manufacturers to focus on recycled polyester, often made from post-consumer PET bottles. This shift aligns with global sustainability goals and appeals to eco-conscious consumers.

- Blended Fabrics: Blending polyester with natural fibers creates fabrics that combine the best qualities of both materials, expanding the fiber’s versatility.

- High-Performance Textiles: Advances in processing technology have led to specialized polyester fibers with moisture-wicking, UV-resistant, and antibacterial properties, catering to sportswear and outdoor gear markets.

- Digital Textile Printing: Polyester’s compatibility with digital printing methods is making it popular in the fashion and home décor industries, enabling more customization and faster turnaround.

Regional Landscape

The Asia Pacific region dominates the global polyester fiber market, accounting for 65.32% of the total market share in 2024. Countries such as China, India, Japan, and South Korea have established themselves as major production hubs due to the availability of raw materials, advanced manufacturing facilities, and cost-effective labor. China, in particular, plays a significant role not only as a leading producer but also as a top consumer, thanks to its robust textile and garment industry.

Asia Pacific’s dominance is expected to continue in the coming years as infrastructure for polyester production and processing improves further. Additionally, growing middle-class populations in these countries are fueling demand for apparel, home décor, and automotive textiles, all of which require large volumes of polyester fiber.

North America and Europe also hold substantial market shares, driven by strong demand in apparel, home furnishing, and technical textile segments. In these regions, the focus is shifting toward sustainable and recycled polyester due to increasing environmental awareness and regulatory requirements.

Product Segmentation

Polyester fiber is typically categorized into two main types: polyester staple fiber (PSF) and polyester filament yarn (PFY).

- Polyester Staple Fiber (PSF): PSF is short-length fiber often blended with natural fibers like cotton or wool to enhance fabric performance. It is widely used in clothing, upholstery, and nonwoven products like diapers, wipes, and filtration materials. In 2024, PSF holds the largest share of the market due to its versatility and cost advantages.

- Polyester Filament Yarn (PFY): PFY consists of continuous strands of fiber, ideal for making fabrics with smooth textures and high strength. It is extensively used in sportswear, home textiles like curtains and bed linens, and industrial applications. PFY demand is growing steadily as fashion trends lean toward lightweight yet durable fabrics.

Read More : https://www.fortunebusinessinsights.com/polyester-fiber-market-111384

Key Industry Developments

- March 2025 - ADVANSA’s ADVAtex is a 100% recycled polyester fiber made from pre-consumer textile waste. It reduces reliance on virgin materials while maintaining quality. The process transforms textile waste into durable fibers for furniture and mattresses, addressing global textile waste challenges. Certified by GRS and Oeko-Tex.

- July 2024 - Indorama Ventures has joined a consortium of seven companies across five countries to establish a sustainable polyester fiber supply chain. This initiative utilizes CO₂-derived, renewable, and bio-based materials, replacing traditional fossil resources. The resulting polyester fiber is planned for use in THE NORTH FACE products in Japan.

Applications

Polyester fiber’s wide-ranging applications are a major driver of its market growth. Key segments include:

- Textiles and Apparel: Polyester’s wrinkle resistance, durability, and color retention make it a preferred choice in clothing, from casual wear to high-performance sportswear. Its affordability compared to natural fibers like cotton adds to its appeal.

- Home Furnishings: Used in carpets, curtains, bed linens, and upholstery, polyester offers durability and easy maintenance, which is especially attractive in the home décor sector.

- Industrial Applications: Polyester fibers are used in conveyor belts, tire cords, ropes, safety belts, and geotextiles due to their high strength and resistance to stretching and shrinking.

- Nonwoven Fabrics: Polyester plays a critical role in producing hygiene products, insulation materials, and filtration media.

- Medical Textiles: Its ability to be engineered for specific properties makes polyester valuable in surgical gowns, drapes, and other healthcare products.

Competitive Landscape

The market is characterized by intense competition among key players, including Reliance Industries Limited, Indorama Ventures, Toray Industries, Sinopec Yizheng Chemical Fibre, and Zhejiang Hengyi Group. These companies are investing in capacity expansions, technological innovations, and sustainable practices to strengthen their market positions.

Mergers, acquisitions, and partnerships are common strategies to enhance production capabilities and expand into new geographic markets. Many leading manufacturers are also increasing their focus on recycled polyester to meet environmental targets and regulatory requirements.

Future Outlook

The global polyester fiber market is expected to maintain a steady growth trajectory over the next decade. Asia Pacific will likely remain the largest and fastest-growing regional market, while North America and Europe will see increased demand for sustainable and high-performance polyester products.

With its adaptability, cost advantages, and continuous innovations, polyester fiber is well-positioned to meet the evolving needs of industries and consumers worldwide. The transition toward recycled and eco-friendly fibers will further reshape the market, offering opportunities for forward-thinking manufacturers to lead in both volume and sustainability.