The global surface disinfectant market was valued at USD 770.6 million in 2019 and is expected to grow to USD 1,547.7 million by 2027, registering a CAGR of 9.1% during the 2020–2027 forecast period. North America led the market with a 38.92% share in 2019, with the U.S. surface disinfectant market projected to reach USD 524.4 million by 2027. This growth is primarily driven by increased awareness of hygiene and sanitation across healthcare, residential, and commercial settings, especially in the aftermath of the pandemic.

Market Size and Growth Projections

The global surface disinfectant market is witnessing significant growth, fueled by rising hygiene awareness, healthcare-associated infection prevention, and increasing demand for effective and safe cleaning solutions. Over the past few years, surface disinfectants have evolved from niche healthcare products to household essentials, particularly in the wake of the COVID-19 pandemic. With robust growth projections ahead, the market is poised to expand both in value and application scope across sectors.

The pandemic served as a key catalyst, significantly boosting demand across all regions and industries. However, even in the post-pandemic phase, the elevated focus on cleanliness and safety has remained, ensuring steady demand for disinfectant products worldwide.

List of Top Surface Disinfectant Companies:

- 3M (U.S.)

- The Proctor & Gamble Company (U.S.)

- Kimberley-Clark Corporation (U.S.)

- SC Johnson Professional (U.S.)

- The Clorox Company (U.S.)

- Ecolab (U.S.)

- Metrex Research LLC(U.S.)

- Reckitt Benckiser Group Plc (U.K.)

- Diversey Inc.(U.S.)

Drivers of Market Growth

One of the primary growth drivers is the global rise in hospital-acquired infections (HAIs). With the burden of healthcare costs and patient safety risks increasing, healthcare facilities are under greater pressure to adopt rigorous disinfection practices. As a result, hospitals, clinics, and laboratories are major consumers of surface disinfectants.

Additionally, regulatory mandates from organizations such as the World Health Organization (WHO), Centers for Disease Control and Prevention (CDC), and the Environmental Protection Agency (EPA) have established stringent hygiene protocols in public and private spaces. This has boosted the demand for high-efficacy disinfectants that can eliminate a broad spectrum of pathogens.

Consumer awareness has also played a vital role. From schools and offices to transportation systems and homes, end-users are becoming more conscious of the importance of regular surface sanitation. Moreover, the expansion of e-commerce channels has made disinfectant products more accessible, contributing to rising global consumption.

Market Segmentation Trends

Surface disinfectants are generally segmented by type, composition, application, and end-use.

- By type, liquid disinfectants dominate the market due to their broad applications, cost-effectiveness, and ease of use. Liquids are particularly favored in hospitals and commercial buildings for cleaning larger surface areas. However, disinfectant wipes are emerging as the fastest-growing segment. Their convenience, portability, and ability to reduce cross-contamination are making them highly desirable in both medical and household settings.

- By composition, alcohol-based disinfectants hold the largest market share. They are known for their rapid action and effectiveness against a wide range of microorganisms, making them a go-to choice in medical facilities and homes alike. Chlorine-based compounds and peracetic acid formulations are also gaining traction, especially in food processing and industrial environments due to their strong antimicrobial properties.

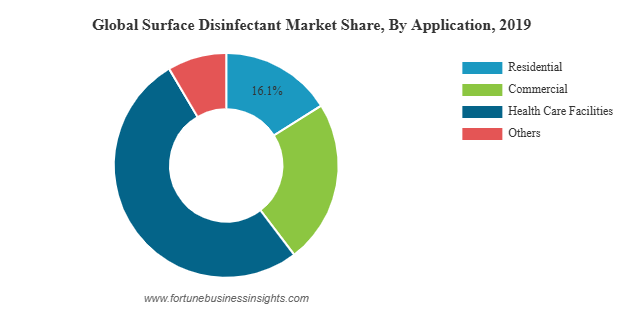

- By application, the healthcare sector accounts for the largest portion of the market, driven by strict hygiene standards and frequent disinfection needs. Residential usage is also growing significantly. In fact, residential applications accounted for over 16% of the market in 2019, and this share continues to rise as consumers maintain post-pandemic cleaning routines.

Read More : https://www.fortunebusinessinsights.com/surface-disinfectant-market-103062

Regional Insights

North America currently leads the global surface disinfectant market, with the United States being a major contributor. The region benefits from a strong healthcare infrastructure, high awareness levels, and strict regulatory compliance. Europe follows closely, driven by widespread infection control policies and rising healthcare expenditure.

Asia Pacific is anticipated to witness the fastest growth during the forecast period. Countries like China, India, and Japan are investing heavily in healthcare infrastructure, and public awareness of cleanliness is rising rapidly. The region is also seeing increased demand from the food & beverage industry, public transit systems, and educational institutions.

Key Industry Developments:

- January 2019 – Reckitt Benckiser formed a strategic alliance with Diversey to increase its presence in North America. This strategic alliance will help Reckitt Benckiser to expand its reach to educational institutes, food establishments, and hospitals.

- February 2020 – The Procter and Gamble Company launched a new line of antibacterial cleaners named Microban 24. The new product line is said to protect the applied surface for a complete 24 hours, even when the surface has been contacted multiple times.

Competitive Landscape and Innovations

The surface disinfectant market is relatively consolidated, with a handful of global companies holding significant market shares. Leading players include 3M, Procter & Gamble, Clorox Company, Reckitt Benckiser, Ecolab, STERIS, Diversey, and Kimberly-Clark. These companies are continuously innovating to develop new product formulations, expand into emerging markets, and strengthen distribution networks.

Product innovation is a key competitive strategy. For instance, several companies have launched long-lasting antimicrobial sprays and disinfectants that continue working even after drying. Biodegradable and eco-friendly formulations are also entering the market in response to concerns about chemical residues and environmental impact.

Emerging Trends and Opportunities

A notable trend is the shift toward sustainable disinfectants. Consumers and industries alike are showing interest in products that are non-toxic, biodegradable, and safe for children and pets. This has led to the development of botanical-based and alcohol-free disinfectants that maintain high efficacy without harsh chemical ingredients.

Another promising development is the integration of disinfection technologies such as UV-C light systems, electrostatic sprayers, and antimicrobial coatings. These advanced solutions are being adopted in hospitals, airports, and public transport systems to enhance safety and reduce manual cleaning requirements.

Automation and IoT-enabled sanitation monitoring systems are also being introduced in smart buildings, offering real-time insights into cleanliness levels and helping facilities maintain high hygiene standards efficiently.

Outlook

The global surface disinfectant market is set for sustained growth, supported by heightened awareness, regulatory backing, and ongoing innovations. With increasing demand across healthcare, residential, commercial, and industrial sectors, the industry is expected to remain a critical part of global health and safety infrastructure in the years to come. The push toward safer, sustainable, and tech-enabled solutions will further shape the market landscape, creating new opportunities for businesses and consumers alike.

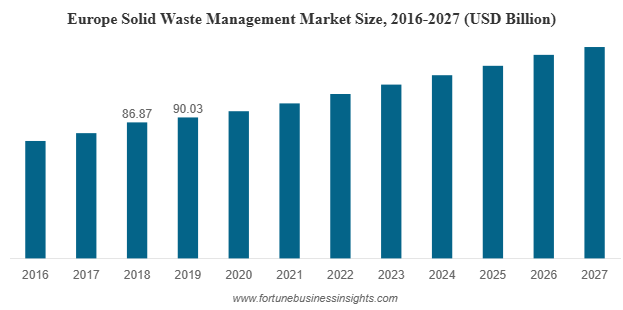

The global solid waste management market was valued at USD 285.16 billion in 2019 and is anticipated to grow to USD 366.52 billion by 2027, registering a CAGR of 3.3% during the forecast period. In 2019, Europe held the largest share of the market at 31.57%, driven by strong regulatory frameworks and advanced waste processing systems. Meanwhile, the U.S. solid waste management market is expected to see substantial growth, with projections indicating it could reach USD 93.46 billion by 2032. This growth is supported by the country’s well-established infrastructure for waste collection, processing, and disposal, along with the presence of major industry players.

Market Size and Growth Outlook

Solid waste management market plays a vital role in maintaining environmental health, public sanitation, and sustainable urban living. With the rise in global population, urbanization, and industrialization, the need for efficient and sustainable solid waste management solutions has become more crucial than ever. The market for solid waste management is witnessing rapid growth, supported by technological advancements, increased governmental efforts, and growing awareness about environmental conservation.

List Of Key Players Profiled:

- Waste Management Inc. (USA)

- SUEZ Group (France)

- Veolia Environment S.A. (France)

- Biffa PLC (U.K.)

- Clean Harbors Inc. (USA)

- Covanta Holdings Corporation (USA)

- Hitachi Zosen Corporation (Japan)

- Remondis AG & Co. Kg (Germany)

- Republic Services Inc. (USA)

- Stericycle Inc. (USA)

Regional Insights

Europe led the solid waste management market in 2019, accounting for a market share of 31.57%. The region benefits from strong regulatory frameworks, well-established recycling infrastructure, and proactive government initiatives focused on circular economy practices. Countries like Germany, the Netherlands, and Sweden are considered leaders in sustainable waste disposal and recycling technologies.

In North America, particularly the United States, the market is also projected to witness significant growth. By 2032, the solid waste management market in the U.S. is expected to reach an estimated USD 93.46 billion. This growth is supported by the country’s robust infrastructure for waste collection, processing, and disposal, as well as the presence of prominent industry players that are actively investing in advanced solutions.

Key Drivers of Market Growth

- Urbanization and Industrial Development

The rapid pace of urban expansion and industrial activity worldwide has led to a surge in waste generation, making effective management practices a necessity. - Government Regulations and Policies

Stringent environmental regulations and policies promoting waste segregation, recycling, and landfill diversion are encouraging municipalities and private firms to upgrade their waste management systems. - Technological Advancements

The adoption of technologies such as AI-powered waste sorting, automated waste collection systems, and smart bins is enhancing operational efficiency and improving the sustainability of solid waste management services. - Public Awareness and Sustainability Goals

With increasing public awareness regarding environmental degradation and climate change, there is a growing demand for sustainable waste management solutions. Many corporations are also aligning their waste disposal strategies with ESG (Environmental, Social, and Governance) goals.

Read More : https://www.fortunebusinessinsights.com/solid-waste-management-market-103045

Segmentation Overview

The solid waste management market can be segmented into various categories based on waste type, service, and end-user applications:

- By Waste Type: Municipal Solid Waste, Industrial Waste, Hazardous Waste

- By Service: Collection, Transportation, Processing, Disposal

- By End User: Residential, Commercial, Industrial

Challenges in the Industry

Despite the positive growth outlook, the industry faces several challenges. These include the high cost of advanced waste processing technologies, limited public-private partnerships in emerging markets, lack of consumer awareness in certain regions, and inadequate segregation at source. Addressing these issues will be crucial to achieving a sustainable waste management ecosystem globally.

Key Industry Developments:

- July 2019 – The consortium BCE led by SUEZ Group signed a 25 years contract with municipal company Beogradske Elektrane to sell heat produced from waste-to-energy in Belgrade, Serbia. By signing this contact, the municipal company is aiming to introduce renewable energy by reducing its energy dependency on natural gas. The plant operation will be handled by SUEZ Group and the plant will process 500 Kilo Tons of Municipal waste and 200 Kilo Tons of construction & demolition waste per year.

- December 2019 – Covanta Holdings Corporation agreed with Zhao County, China to build & operate a new Energy-from-waste facility. The project will offer sustainable waste management solutions to the county. With this agreement, the company is aiming to expand its geographical footprints into Chinese market.

Future Trends

- Growing adoption of waste-to-energy (WTE) technologies

- Increased investment in circular economy infrastructure

- Expansion of digital platforms for tracking and managing waste streams

- Rising use of AI and machine learning in waste sorting and recycling

- Strengthening of zero-waste initiatives across industries and communities

Outlook

The global solid waste management market is poised for steady growth in the coming years, driven by a combination of environmental, technological, and policy-driven factors. As awareness around sustainability continues to grow, and as countries invest in greener infrastructure, the focus on improving waste collection, processing, and recycling methods will only intensify. Stakeholders in this space, including public authorities, private companies, and consumers, will play a vital role in shaping the future of global waste management.

The global aluminum composite panels market was valued at USD 5.33 billion in 2018 and is expected to grow to USD 8.71 billion by 2026, registering a CAGR of 6.1% during the forecast period. In 2018, Asia Pacific led the market with a dominant share of 39.23%. Meanwhile, the U.S. market is anticipated to witness strong growth, projected to reach approximately USD 2.41 billion by 2032, supported by favorable infrastructure development policies and initiatives across North America.

Market Size and Growth Forecast

Aluminum Composite Panels (ACP) market have emerged as a preferred material in modern construction and architectural design. Comprising two thin aluminum sheets bonded to a non-aluminum core, these panels offer a unique blend of durability, lightweight, aesthetic appeal, and ease of maintenance. They are widely used in exterior cladding, signage, interior decoration, and transportation applications. The increasing demand for energy-efficient and sustainable building materials is driving the expansion of this market across the globe.

List of Key Companies Profiled In Aluminum Composite Panels Market:

- 3A Composites GmbH

- Arconic

- Mitsubishi Chemical Corporation

- Hyundai Alcomax Co.,Ltd.

- Fairfield Metal LLC

- Jyi Shyang Industrial Co., Ltd.

- ALUMAX INDUSTRIAL CO., LTD.

- Yatai Industrial Group Co., Ltd.

- Shanghai Huayuan New Composite Materials Co., Ltd.

- Guangzhou Xinghe Aluminum Composite Panel Co., Ltd.

Regional Insights

- Asia Pacific

Asia Pacific dominated the aluminum composite panels market in 2018, accounting for a 39.23% share of the global market. The region is expected to maintain its dominance throughout the forecast period. Rapid urbanization, increasing infrastructure development, and growing construction activities in countries like China, India, and Southeast Asia are contributing to the strong demand for ACPs. Additionally, rising awareness about energy-efficient buildings and increasing government investments in smart city projects are further propelling the market in the region.

- North America

North America is also a significant market for aluminum composite panels. In 2018, the market size in the United States was estimated at USD 1.46 billion and is projected to grow substantially in the coming years. The growth in this region is attributed to rising renovation activities, stringent regulations regarding energy-efficient buildings, and increased demand for advanced cladding solutions. The presence of established players and their continuous investment in product innovation are also supporting market expansion in the region.

- Europe

Europe is witnessing steady growth in the aluminum composite panels market due to rising demand for green and sustainable construction materials. Countries like Germany, the UK, and France are at the forefront of adopting ACPs, driven by strict building codes and increasing investments in modern infrastructure. The market is also benefiting from growing demand in the transportation and advertising sectors.

Market Drivers

- Increasing Construction Activities

One of the primary drivers of the ACP market is the booming construction sector worldwide. With rapid industrialization and urbanization, there is a growing need for modern and aesthetically appealing buildings. ACPs are widely used in both residential and commercial construction projects for exterior cladding, curtain walls, and interior applications, thanks to their flexibility and ease of installation.

- Rising Demand for Durable and Lightweight Materials

Aluminum composite panels are lightweight yet highly durable, making them ideal for a range of applications. Their resistance to weather, fire, and corrosion adds to their suitability in harsh environmental conditions. The combination of strength and reduced weight also contributes to lower structural loads and transportation costs, which is especially important in large-scale construction and transportation projects.

- Focus on Energy Efficiency

With growing concerns about climate change and energy consumption, there is an increasing emphasis on sustainable building practices. ACPs help enhance energy efficiency by providing effective insulation and reducing heat transfer, which can lower energy consumption for heating or cooling. This characteristic aligns with global efforts to reduce carbon footprints and improve energy performance in buildings.

- Advancements in Coating Technologies

Advancements in coating technologies, such as the use of PVDF (polyvinylidene fluoride) and FEVE (fluoroethylene vinyl ether) coatings, have significantly improved the performance and lifespan of aluminum composite panels. These coatings provide excellent UV resistance, color retention, and protection against harsh weather conditions, thereby increasing the appeal of ACPs in various applications.

Read More : https://www.fortunebusinessinsights.com/aluminum-composite-panels-market-102304

Market Challenges

Despite the strong growth prospects, the aluminum composite panels market faces certain challenges. One of the major concerns is the flammability of low-grade ACPs, particularly those with polyethylene cores. Incidents of fire accidents in buildings clad with such materials have led to stricter regulations and increased scrutiny. As a result, manufacturers are now focusing on developing fire-retardant and non-combustible panel variants to meet safety standards.

Additionally, fluctuations in raw material prices and the environmental impact of aluminum production could pose challenges to market growth. However, ongoing research into recyclable and eco-friendly materials is expected to provide solutions to these issues in the long term.

Key Industry Developments:

- July 2017 – Fairview Architectural acquired the Stryum business, an intelligent non-combustible aluminum cladding system, from Vitekk Industries. The company includes a variety of high-quality aluminum plate façade panels designed to provide durability and sustainability, complimenting Fairview's current portfolio of cladding solutions, including high-density cement fibre, natural stone, terracotta tiles and the leading non-combustible composite aluminum frame.

Application Insights

The building and construction sector remains the largest application segment for aluminum composite panels, accounting for the majority of market share. ACPs are extensively used for exterior facades, partitions, ceilings, and interior decorations. The transportation sector is another key application area, where ACPs are used in the manufacturing of buses, trains, and aircraft to reduce weight and improve fuel efficiency.

The advertising industry also represents a significant market for ACPs, as they are commonly used for signage and billboards due to their smooth surface, vibrant colors, and ease of customization.

Future Outlook

The future of the aluminum composite panels market looks promising, with continuous advancements in material science, growing awareness about energy efficiency, and expanding applications across industries. As governments and private sectors increasingly invest in infrastructure development and smart city initiatives, the demand for innovative building materials like ACPs is expected to soar.

Furthermore, with increasing regulations focusing on fire safety and sustainability, manufacturers are likely to invest more in the development of advanced, eco-friendly, and compliant panel solutions. These trends are set to drive the market forward and create new growth opportunities in the years to come.

The global protective clothing market continues to expand steadily, reflecting an increasing global emphasis on occupational safety, regulatory mandates, and technological advances in material science. Protective garments safeguard workers against diverse hazards—including chemical exposure, thermal and flame risks, mechanical injury, biological contamination, and radiation—across sectors such as oil & gas, healthcare, construction, manufacturing, and firefighting.

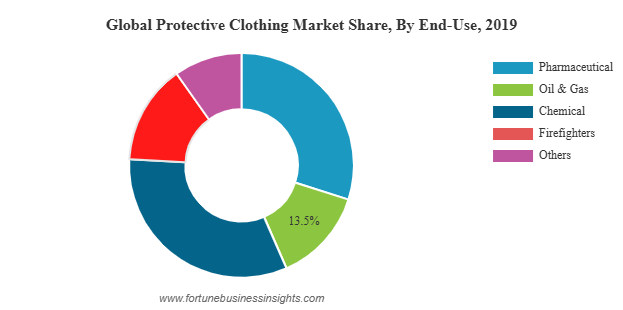

The global protective clothing market was valued at USD 12.48 billion in 2019 and is anticipated to reach USD 34.31 billion by 2027, growing at a CAGR of 14% over the forecast period. In 2019, North America led the global market, accounting for a 37.4% share, with a regional market size of USD 4.34 billion in 2018. The U.S. market alone is expected to rise to USD 10.45 billion by 2027, driven by stricter workplace safety regulations and increasing demand from the healthcare sector.

Key Market Drivers

- Regulatory Requirements & Safety Enforcement

Stringent health and safety regulations worldwide have made protective clothing a legal requirement in many industries. Organizations operating in high-risk environments—such as chemical processing, mining, construction, or healthcare—are obligated to provide protective garments tailored to specific hazards, prompted by both legal frameworks and liability considerations.

- Industrial Expansion & Workplace Exposure

Industrial sectors with heightened exposure to hazards—like oil & gas, pharmaceuticals, heavy industry, firefighting, and mining—are fueling demand for specialized protective gear. Emerging economies, especially in Asia-Pacific and Latin America, are rapidly developing infrastructure, manufacturing, and urban projects that further elevate protective clothing requirements.

- Innovations in Material & Design

Protective garments are increasingly incorporating advanced materials like aramid fibers, PBI blends, coated synthetics, and breathable composites. Innovations include flame-retardant textiles, chemical-resistant coatings, anti-static fabrics, and wearable sensors for environmental or physiological monitoring. Ergonomic designs that provide greater comfort, flexibility, and fit are becoming essential for longer wear durations.

- Rising Demand from Healthcare & Life Sciences

The healthcare and pharmaceutical industries have become significant adopters of protective clothing, focusing on infection control and biohazard protection. Emergency situations and global health crises reinforce the need for specialized attire such as lab suits, gowns, and respirator-integrated outerwear.

List of Top Protective Clothing Companies:

- Honeywell International Inc. (U.S.)

- Lakeland Inc. (U.S.)

- L. Gore & Associates, Inc. (U.S.)

- PBI Performance Products, Inc. (U.S.)

- TenCate Protective Fabrics (U.S.)

- Kimberly-Clark Corporation (U.S.)

- Ansell Microgard Ltd. (U.K.)

- DuPont (U.S.)

- Bennett Safetywear Ltd. (U.K.)

- TEIJIN LIMITED (Japan)

Market Segmentation

By Material Type

- Aramid & Blended Fabrics: Ideal for extreme heat, fire, and chemical resistance.

- High-Performance Fibers (e.g., PBI): Provide protection in severe environments like firefighting or petrochemical operations.

- Polyolefin & Polyester Blends: Offer general protection in industrial settings.

- Cotton & Laminated Textiles: Cost-effective options for lightweight protection or use in controlled environments.

By Application

- Thermal/Flame Protection

- Chemical Protection

- Mechanical Protection (Cuts, Abrasion, Impacts)

- Biological & Radiological Protection

- Cleanroom Apparel

By End‑Use Industry

- Oil & Gas, Chemicals & Petrochemicals

- Construction & Industrial Manufacturing

- Pharmaceuticals & Healthcare

- Firefighting & Emergency Services

- Law Enforcement & Defense

- Energy, Mining & Utilities

By Distribution Channel

Sales occur via trade distributors, direct procurement contracts (especially with large enterprises or government bodies), industrial safety suppliers, and increasingly, through digital channels.

Read More : https://www.fortunebusinessinsights.com/protective-clothing-market-102707

Regional Breakdown

- North America

Leading global revenue share, supported by mature safety standards, rigorous enforcement, strong industry presence, and high adoption of wearable technologies—such as sensor-integrated suits and fatigue monitoring.

- Asia‑Pacific

Fastest-growing region, driven by industrial expansion, urban development, and increasing occupational safety awareness. Countries like China, India, and Southeast Asia exhibit surging demand across manufacturing, oil, construction, and mining.

- Europe

Stable growth led by strict safety regulations, sustainable material mandates, and a focus on ergonomic design and performance textiles. European markets show rapid adoption of reusable and recyclable protective garments.

- Latin America, Middle East & Africa

These emerging regions show rising demand due to growing infrastructure investment, investments in oil & gas and utilities, and gradually improving workplace safety frameworks.

Challenges & Restraints

- High Production Costs

Specialized materials and complex certifications raise production expenses, which can limit adoption, especially among smaller businesses in cost-sensitive regions.

- Technical Complexity & Expertise

Tailoring protective garments to specific hazard conditions requires specialized design capabilities. Lack of technical resources in some regions can delay adoption.

- Supply Chain & Raw Material Volatility

Fluctuating prices of high-performance fibers and disruptions in sourcing can impact product pricing and availability.

- Recycling & Sustainability Hurdles

Durable protective materials are often not recyclable in conventional systems. Designing garments that can be sanitized, reused, or recycled presents logistical challenges.

Key Industry Developments:

- In March 2020 - Protective Industrial Products (PIP) announced the expansion of salesforce in Latin America for industrial protective products. This will help the company in expanding the supply chain and support the growing demand of customers through better distribution network to the local market.

- In February 2019 - Protective Industrial Products Inc. acquired West Chester Protective Gear. The company specializes in the manufacturing of protective apparel for industrial purposes. This acquisition will help in strengthening product portfolio and complement the customer base.

Key Innovations & Market Opportunities

- Smart & Connected Protective Clothing

Integration of sensors into garments enables detection of exposure to chemicals, temperature stress, fatigue, or hazardous conditions. This real-time monitoring enhances safety and operational responsiveness.

- Eco-Friendly & Reusable Materials

Demand is rising for protective gear made from reusable or biodegradable fabrics. Particularly in healthcare and industrial sectors, initiatives support garments that meet hygiene and safety standards yet reduce environmental impact.

- Enhanced Ergonomics & Adaptive Designs

Flexible layering systems, breathable fabrics, and adjustable fittings are improving wearer comfort without compromising safety—especially important for long-duration use.

- Sectoral Expansion

Applications are expanding into robotics, aerospace, utilities, and off-shore operations where combined technical fabrics and wearable electronics provide multi-level protection.

Strategic Outlook

The global protective clothing market is poised for consistent growth over the next decade. Demand is being shaped by tightening regulatory requirements, increasing exposure to hazardous work environments, and technological innovation in textiles. Smart and sensor-embedded garments, sustainable fabric alternatives, and advanced visibility and protection standards offer critical growth pathways.

Providers that invest in R&D, sustainable manufacturing, and ergonomic integration—while partnering with industries to tailor solutions—will likely lead future market development. As industries continue to globalize and safety standards evolve, protective clothing remains an essential investment in mitigating risk and safeguarding human resources worldwide.

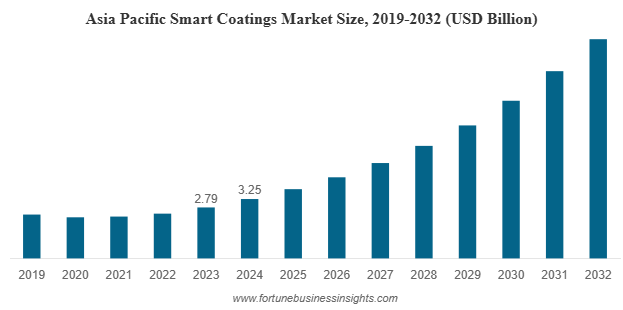

The global smart coatings market was valued at USD 7.17 billion in 2024 and is projected to rise from USD 8.34 billion in 2025 to USD 26.15 billion by 2032, registering a strong CAGR of 17.7% during the 2025–2032 forecast period. In 2024, Asia Pacific led the market with a dominant share of 45.33%.

Smart coatings are advanced materials engineered to offer enhanced functionalities such as self-healing, anti-corrosion, anti-microbial, anti-icing, and self-cleaning properties. These materials react to environmental stimuli such as temperature, pressure, pH, and electrical or magnetic fields, making them valuable in applications where conventional coatings fall short.

Market Drivers

One of the key drivers fueling the smart coatings market is the growing demand for sustainable and efficient surface protection across industries. These coatings are instrumental in reducing maintenance costs, increasing durability, and extending the lifespan of equipment and infrastructure. The construction and automotive industries, in particular, benefit from the use of anti-corrosion and self-cleaning coatings, which minimize wear and enhance performance over time.

Technological advancements in nanotechnology and materials science have significantly contributed to the development of smart coatings. Nano-coatings, for instance, provide ultra-thin layers with high functionality and are widely adopted in electronics and automotive applications. The ability to embed sensors and responsive elements into coatings enables real-time monitoring and predictive maintenance, providing added value to users.

Moreover, environmental concerns and regulations aimed at reducing volatile organic compounds (VOCs) in conventional coatings have spurred interest in smart coatings that offer low environmental impact while delivering superior performance.

List Of Key Smart Coating Companies Profiled

- 3M (U.S.)

- AkzoNobel N.V. (Netherlands)

- Axalta Coating Systems LLC (U.S.)

- DuPont (U.S.)

- Hempel AS (Denmark)

- Jotun Group (Norway)

- NEI Corporation (U.S.)

- PPG Industries, Inc. (U.S.)

- RPM International Inc. (U.S.)

- The Sherwin-Williams Company (U.S.)

Regional Insights

- Asia Pacific dominated the global smart coatings market in 2024, accounting for the largest share of 45.33%. This dominance is attributed to rapid industrialization, infrastructure development, and the growing adoption of advanced materials across various end-use sectors. Countries such as China, Japan, and India are key contributors to this regional growth due to their expanding automotive and construction industries.

- North America also holds a significant market share, supported by strong research and development initiatives and high demand from aerospace, defense, and marine sectors. In this region, the emphasis on sustainability and smart infrastructure continues to boost the adoption of smart coatings in both public and private projects.

- Europe, with its focus on energy efficiency and regulatory support for green technologies, has emerged as another important market for smart coatings. The region’s automotive and electronics industries are key drivers of demand.

Segmentation Overview

- The smart coatings market can be segmented based on functionality, end-use industry, and technology.

- By functionality, the market includes self-healing, anti-corrosion, anti-icing, anti-microbial, self-cleaning, and other types of smart coatings. Among these, anti-corrosion coatings hold a significant share, particularly in sectors like oil & gas, marine, and construction, where metal surface protection is crucial.

- In terms of end-use industries, the market serves construction, automotive, aerospace, marine, consumer electronics, and healthcare. The construction sector leads in usage due to the need for long-lasting, low-maintenance coatings on buildings and infrastructure. Meanwhile, the automotive and aerospace sectors are increasingly adopting smart coatings to enhance performance, reduce weight, and improve fuel efficiency.

- From a technology perspective, the market includes multi-layer coatings, single-layer coatings, and nanostructured coatings. Nano-coatings, in particular, have gained popularity due to their high efficiency in small thicknesses and multifunctionality.

Read More : https://www.fortunebusinessinsights.com/smart-coatings-market-113374

Challenges

Despite the promising outlook, the smart coatings market faces several challenges. High production costs and complex manufacturing processes pose barriers to widespread adoption. Additionally, a lack of standardized testing methods and regulatory frameworks can hinder market penetration, especially in emerging economies.

Moreover, integrating smart functionalities into traditional coating systems requires specialized knowledge and equipment, which may not be readily available to all manufacturers. These constraints could slow the transition from conventional to smart coatings in some regions.

Key Industry Developments

- July 2024 – AkzoNobel expanded its portfolio with Resicoat EV powder coatings, designed for electric vehicle components to enhance insulation, corrosion resistance, and thermal management.

- November 2023 – Covestro AG launched Impranil CQ DLU, a bio-based polyurethane dispersion with 34% plant-derived carbon, targeting sports, automotive, and technical textiles. This replaces petroleum-based alternatives while maintaining durability.

Opportunities

On the positive side, the market presents numerous opportunities. Smart coatings are gaining traction in the healthcare industry for applications such as anti-microbial surfaces in hospitals and self-sanitizing equipment. The renewable energy sector is another area where smart coatings can play a critical role in improving the efficiency and durability of solar panels and wind turbines.

The Internet of Things (IoT) integration with smart coatings is opening new avenues in predictive maintenance and asset management. As industries move toward automation and smart infrastructure, the demand for intelligent coatings capable of responding to environmental changes and providing real-time data is expected to grow.

Future Outlook

The future of the smart coatings market looks promising, with innovation and sustainability acting as the central themes. As research in materials science advances, new formulations and functionalities are expected to emerge, further expanding the scope of applications. Strategic partnerships among manufacturers, research institutions, and government bodies will play a crucial role in fostering growth and addressing current challenges.

In summary, the smart coatings market is poised for rapid expansion, driven by technological innovation, increasing industrial demand, and the global shift toward sustainable and intelligent materials. With robust growth across Asia Pacific, North America, and Europe, the market is expected to continue evolving, offering smarter, more efficient solutions for a wide range of applications.

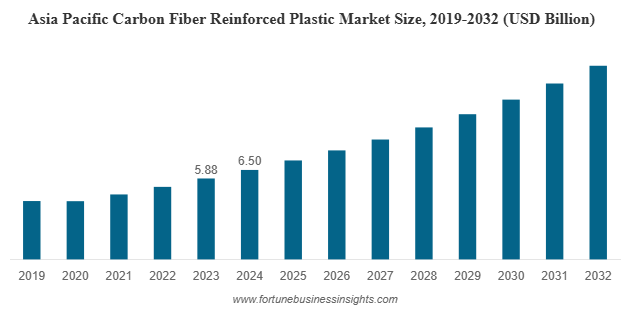

Carbon Fiber Reinforced Plastics (CFRPs) have become a cornerstone material across high-performance industries due to their superior strength-to-weight ratio, exceptional rigidity, and resistance to corrosion and fatigue. Composed of carbon fibers embedded within a polymer matrix, CFRPs are increasingly used in industries such as aerospace, automotive, wind energy, sports equipment, and construction, where both strength and lightweight characteristics are essential.

In 2024, the global carbon fiber reinforced plastic (CFRP) market was valued at USD 18.92 billion. It is expected to rise to USD 20.72 billion in 2025 and further reach USD 38.02 billion by 2032, registering a CAGR of 9.1% over the forecast period. Asia Pacific led the market with a dominant 34.36% share in 2024.

Market Drivers

The rising adoption of CFRP materials is primarily driven by growing demand for lightweight, fuel-efficient components in the transportation and energy sectors. In aerospace, CFRPs are used extensively in fuselage panels, wings, and other structural parts to reduce aircraft weight and improve fuel economy. The automotive sector, particularly the electric vehicle (EV) segment, is integrating CFRP into body frames, battery housings, and interior components to extend vehicle range and improve performance.

Wind energy is another significant growth area, where CFRP is utilized in turbine blades due to its durability and ability to withstand extreme environmental stress while keeping structural weight low. In civil construction, CFRP is increasingly used for bridge reinforcement, seismic retrofitting, and advanced façade applications.

List Of Key Market Players Profiled In The Report

- Hexcel Corporation (U.S.)

- TORAY INDUSTRIES, INC. (Japan)

- SGL Carbon (Germany)

- Mitsubishi Chemical Group Corporation. (Japan)

- TEIJIN LIMITED. (Japan)

- Solvay (Belgium)

- Formosa Plastics (Taiwan)

- DowAksa (Turkey)

- Zhongfu Carbon Fiber Core Cable Technology Co., Ltd (China)

- HS HYOSUNG ADVANCED MATERIALS (South Korea)

Material Trends and Segmentation

- The CFRP market can be segmented by raw material, resin type, form, application, and region. Based on raw materials, PAN-based carbon fibers dominate the market due to their superior mechanical properties, making them ideal for high-performance applications. Pitch-based fibers are used in specific sectors requiring higher thermal and electrical conductivity.

- In terms of resin, thermosetting resins, particularly epoxy, hold the largest share, known for their excellent bonding strength and thermal stability. However, thermoplastic CFRPs are gaining traction due to faster manufacturing times, recyclability, and better impact resistance.

- Form-wise, CFRP is available in different types including prepregs (pre-impregnated fibers), woven fabrics, and chopped fibers, each suited to specific applications ranging from aerospace to sporting goods. By application, aerospace and defense remain the largest consumers, followed by automotive, wind energy, construction, and consumer electronics.

Regional Insights

- Asia Pacific

The Asia Pacific region is the largest and fastest-growing market, led by countries such as China, Japan, and South Korea. The region’s dominance is supported by a robust manufacturing base, growing renewable energy capacity, and rising demand for lightweight materials in transportation and electronics.

- North America

North America follows closely, with strong contributions from the U.S., which is a major hub for aerospace, defense, and EV manufacturing. Technological advancements and high investments in innovation are driving adoption across various sectors.

- Europe

Europe holds a significant market share with strong support from automotive manufacturers and renewable energy developers. The region is home to several key players in the wind energy and luxury automotive sectors, both of which heavily rely on CFRP.

- Rest of the World

Regions such as Latin America, the Middle East, and Africa are in the early stages of CFRP adoption but show potential due to infrastructure development, urbanization, and rising investment in energy and transportation.

Read More : https://www.fortunebusinessinsights.com/carbon-fiber-reinforced-plastics-cfrps-market-110101

Key Industry Developments

- March 2025: Hexcel and FIDAMC have partnered to advance composite materials for aerospace and industrial applications. Their collaboration focuses on developing innovative manufacturing processes to enhance lightweight, high performance composites. This partnership aims to improve efficiency and sustainability in composite production.

- November 2024: Toray advanced composites expanded its thermoplastic composites portfolio by acquiring Gordon Plastics assets in Colorado. The new 47,000 sq.ft facility enhances R&D and scalable production of high-performance composite tapes for aerospace, sports, oil & gas, and industrial markets.

Challenges and Restraints

Despite its advantages, CFRP adoption faces several barriers. The high cost of production and raw materials remains a significant challenge, especially for cost-sensitive applications. In addition, recycling and disposal of thermosetting composites are technically difficult, limiting their environmental sustainability.

Manufacturing CFRPs also requires specialized skills and equipment, which increases production time and cost. Further, limited availability of carbon fiber manufacturing infrastructure in some regions restricts market growth.

Future Outlook and Opportunities

The CFRP market is poised for significant expansion as industries shift toward sustainability, efficiency, and innovation. The rise of electric mobility, the global push for renewable energy, and advancements in construction and infrastructure development are expected to fuel demand.

Emerging innovations such as automated fiber placement, recyclable thermoplastic composites, and low-cost manufacturing technologies will help overcome current challenges and enhance adoption. Governments and private players are investing heavily in R&D to improve recycling technologies and to develop cost-effective production methods.

Furthermore, with CFRP applications expanding into robotics, medical devices, marine structures, and consumer electronics, the material’s versatility continues to be a key growth driver.

The global carbon fiber reinforced plastic (CFRP) market is on a dynamic growth path, driven by increasing demand for lightweight and high-strength materials across various sectors. While the market faces challenges such as high costs and limited recyclability, ongoing innovations and investments are likely to address these constraints. With robust growth expected across Asia Pacific, North America, and Europe, CFRPs are set to become even more integral to modern industrial applications in the years to come.

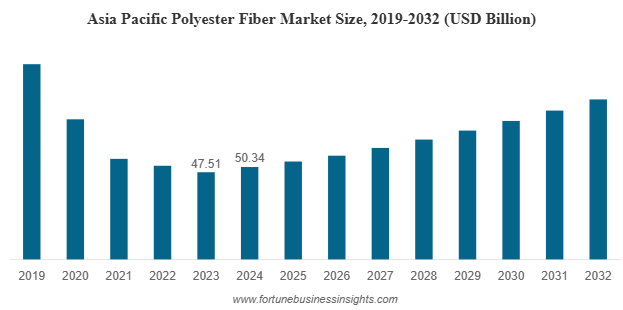

The global polyester fiber market was valued at USD 77.07 billion in 2024 and is expected to increase to USD 82.07 billion in 2025, reaching USD 129.97 billion by 2032, with a projected CAGR of 6.8% during the forecast period. In 2024, Asia Pacific led the market, accounting for 65.32% of the global share.

Market Drivers

Polyester fiber is widely favored due to its cost-efficiency, durability, wrinkle resistance, and quick-drying properties. As the textile and apparel industries grow—especially in developing economies—so does the demand for polyester. Its ability to mimic natural fibers while offering superior performance makes it highly versatile in numerous applications, including fashion, furnishings, and technical textiles.

One of the significant factors driving the growth of the polyester fiber market is its increasing adoption in automotive interiors, industrial insulation, and packaging materials. The lightweight nature of polyester also contributes to fuel efficiency, making it a preferred material in automotive manufacturing.

List Of Key Polyester Fiber Companies Profiled

- Reliance Industries Limited. (India)

- Indorama Ventures Public Company Limited. (Thailand)

- Toray Industries, Inc. (Japan)

- Sinopec Yizheng Chemical Fibre Limited Liability Company (China)

- Zhejiang Hengyi Group Co., Ltd (China)

- Tongkun Holding Group (China)

- Sanfame Group (China)

- Far Eastern New Century Corporation (Taiwan)

- Alpek Polyester. (Mexico)

- ADVANSA (Turkey)

Sustainability and Recycling Trends

With global attention shifting toward sustainability, recycled polyester (rPET) is gaining traction. Manufacturers are increasingly focusing on eco-friendly production methods to reduce their carbon footprints. Recycled polyester, derived from post-consumer PET bottles and textile waste, is finding widespread application across apparel and industrial fabrics. The growth of rPET is helping balance environmental concerns associated with synthetic fiber use while meeting consumer demand for greener alternatives.

Governments and regulatory bodies across several regions are promoting the use of recycled materials, giving a significant boost to innovation in recycling technologies. While virgin polyester still dominates market share, the rPET segment is expanding rapidly and expected to play a crucial role in shaping future demand.

Regional Insights

- Asia Pacific dominated the polyester fiber market in 2024, accounting for a substantial 32% of the global share. This region benefits from large-scale textile manufacturing hubs such as China, India, and Vietnam, supported by cost-effective labor, abundant raw materials, and government initiatives promoting synthetic textile industries. The rise of e-commerce and fast fashion in the region has further increased polyester demand.

- North America and Europe also contribute significantly to market revenue. These regions emphasize sustainable practices and circular economy models, accelerating the adoption of recycled fibers. Technological advancements and high consumer awareness in these regions are pushing companies toward low-impact production and sustainable product lines.

- Emerging markets in Latin America, Africa, and the Middle East are expected to witness moderate growth, driven by infrastructural development, urbanization, and expanding middle-class populations. The increasing penetration of global textile brands in these markets will also contribute to polyester consumption.

Read More : https://www.fortunebusinessinsights.com/polyester-fiber-market-111384

Key Industry Developments

- March 2025 - ADVANSA’s ADVAtex is a 100% recycled polyester fiber made from pre-consumer textile waste. It reduces reliance on virgin materials while maintaining quality. The process transforms textile waste into durable fibers for furniture and mattresses, addressing global textile waste challenges. Certified by GRS and Oeko-Tex.

- July 2024 - Indorama Ventures has joined a consortium of seven companies across five countries to establish a sustainable polyester fiber supply chain. This initiative utilizes CO₂-derived, renewable, and bio-based materials, replacing traditional fossil resources. The resulting polyester fiber is planned for use in THE NORTH FACE products in Japan.

Market Segmentation

The polyester fiber market can be segmented by type, application, and source:

- By Type: The market is divided into staple fibers and filament fibers. Staple fibers are often used in filling, insulation, and blended fabrics, whereas filament fibers are preferred for weaving and knitting high-performance textiles.

- By Source: This includes virgin polyester and recycled polyester. While virgin polyester continues to lead due to its stable supply chain, the shift toward recycled alternatives is becoming more evident with rising environmental awareness.

- By Application: Polyester fibers are used in apparel, home furnishing, automotive, construction, and industrial sectors. Apparel remains the largest application segment, followed by home furnishings and automotive interiors.

Challenges

Despite its wide usage, polyester fiber production is energy-intensive and heavily reliant on petroleum-based raw materials. Environmental concerns such as microplastic pollution and non-biodegradability present ongoing challenges for the industry. Additionally, fluctuations in crude oil prices can affect production costs and supply stability.

Moreover, the increasing scrutiny from environmental organizations and consumers is pressuring manufacturers to innovate and transition toward greener processes. Companies that fail to adapt may struggle to maintain their competitiveness.

Opportunities Ahead

There are ample growth opportunities in technical textiles, including geotextiles, filtration fabrics, medical textiles, and fire-retardant fabrics, where polyester’s performance features make it an ideal choice. Moreover, the evolution of smart textiles—which respond to temperature, moisture, or light—opens new doors for polyester fiber applications.

Investments in bio-based polyester and advanced polymer technologies are expected to pave the way for next-generation sustainable fibers. Brands integrating closed-loop recycling and traceability in their supply chains are gaining market preference.

Future Outlook

The global polyester fiber market is on a growth trajectory, driven by versatile applications, rising consumer demand, and increasing industrial usage. While challenges related to sustainability and raw material volatility persist, the shift toward recycling, innovation, and environmentally responsible production offers new opportunities. With Asia Pacific at the forefront, and North America and Europe advancing in sustainable practices, the global market is poised for continued expansion. Companies investing in circular models and performance enhancement technologies are likely to emerge as industry leaders in the coming decade.

The global dairy packaging market was valued at USD 24.52 billion in 2024 and is expected to grow to USD 25.58 billion in 2025, reaching USD 35.46 billion by 2032, with a projected CAGR of 4.77% during the forecast period. In 2024, North America held the largest market share at 33.48%.

One of the key factors fueling the market’s expansion is the rising global consumption of dairy products such as milk, yogurt, cheese, butter, and cream. As dietary preferences shift toward protein-rich and nutritious food items, dairy products have become a staple across households worldwide. To meet the growing consumption, the dairy industry increasingly relies on advanced packaging solutions that ensure product longevity, hygiene, convenience, and regulatory compliance.

Demand Drivers and Market Dynamics

Urbanization, changing lifestyles, and a growing preference for convenience food are key factors boosting the need for innovative and user-friendly packaging solutions. Products such as single-serve milk cartons, resealable yogurt containers, and on-the-go flavored milk bottles are gaining traction in both developed and developing regions. Additionally, advancements in cold chain logistics and food-grade packaging technologies have enabled the safe transportation and storage of perishable dairy products over longer distances.

Packaging plays a crucial role in protecting the integrity of dairy products, which are highly sensitive to temperature, light, and contamination. Innovations such as aseptic packaging, vacuum-sealed pouches, and modified atmosphere packaging (MAP) have significantly improved the shelf life and safety of dairy products without compromising their taste or nutritional value.

List of Key Dairy Packaging Companies Profiled

- Amcor (Switzerland)

- Sonoco (U.S.)

- Sealed Air (U.S.)

- Berry Global (U.S.)

- Tetra Pak International (Switzerland)

- Silgan Holdings (U.S.)

- Constantia Flexibles (Austria)

- DS Smith (U.K.)

- ProAmpac LLC (U.S.)

- Mondi (U.K.)

- International Paper (U.S.)

Sustainable Packaging on the Rise

Another major trend driving market growth is the increasing focus on sustainability. With rising concerns over plastic waste and environmental pollution, manufacturers and packaging providers are investing in biodegradable, recyclable, and reusable packaging solutions. Paper-based cartons, mono-material laminates, plant-based plastics, and compostable packaging are gaining popularity among environmentally conscious consumers and businesses.

Governments and regulatory bodies across the globe are implementing stricter packaging regulations and waste management policies, further encouraging the use of eco-friendly materials. This shift toward sustainable packaging not only aligns with consumer values but also enhances brand reputation and compliance in the long term.

Read More : https://www.fortunebusinessinsights.com/dairy-packaging-market-108071

Market Segmentation

- The dairy packaging market is segmented by packaging type, material type, product application, and region. In terms of packaging type, flexible packaging such as pouches and sachets leads the segment due to its lightweight, cost-effective, and space-saving characteristics. Rigid packaging, including bottles, tubs, cups, and cartons, also holds a significant share, particularly in liquid dairy products like milk and cream.

- By material type, plastic remains the most widely used material due to its versatility and durability. However, paper and paperboard are rapidly gaining ground due to their recyclability and lower environmental impact. Glass and metal are niche segments, primarily used for premium or traditional dairy products.

- In terms of product application, milk holds the largest share of the market, followed by yogurt, cheese, butter, and ice cream. Each dairy product has specific packaging requirements based on its texture, shelf life, and handling needs. As consumer preferences diversify, packaging formats are also evolving to cater to flavored, probiotic, lactose-free, and plant-based dairy variants.

Regional Insights

- Geographically, North America dominated the global dairy packaging market in 2024, accounting for the largest share. This dominance can be attributed to the presence of established dairy processing infrastructure, widespread adoption of advanced packaging technologies, and high consumer demand for packaged dairy goods. Furthermore, innovations in smart packaging, such as QR codes and freshness indicators, are gaining popularity in this region.

- The Asia Pacific region is expected to witness the fastest growth during the forecast period. Factors such as a growing population, increasing disposable incomes, urbanization, and changing dietary habits are driving demand for packaged dairy products in countries like China, India, Japan, and Southeast Asian nations. Expansion of modern retail formats, cold chain networks, and e-commerce is further supporting market growth.

- Europe maintains steady growth, supported by strong regulatory frameworks around food safety, sustainability, and consumer transparency. The region’s emphasis on biodegradable and recyclable packaging materials makes it a significant contributor to eco-friendly packaging innovation. Latin America and the Middle East & Africa are emerging markets with growing dairy consumption and investments in processing and packaging infrastructure.

Key Industry Developments :

- August 2024- CCL Label introduced an enhanced version of its EcoFloat low-density polyolefin sleeve material, referred to as EcoFloat WHITE. The innovative technology is set to be a game-changing solution for the dairy sector, especially regarding high-density polyethylene (HDPE) containers typically utilized yogurt, probiotic beverages, and related items.

- July 2024- MilkyMist collaborated with SIG and AnaBio Technologies and introduced the world's first long-lasting probiotic buttermilk in aseptic carton packaging. The revolutionary product provides consumers with a nutritious and healthy choice while guaranteeing a long shelf-life without refrigeration.

Challenges and Opportunities

Despite positive growth trends, the dairy packaging market faces challenges such as fluctuating raw material prices, recycling complexities of multi-layered materials, and stringent regulatory requirements. Nevertheless, these challenges present opportunities for innovation in packaging materials, smart technologies, and circular economy initiatives.

Companies are increasingly adopting digital printing, intelligent labeling, and traceability solutions to enhance packaging functionality and improve supply chain efficiency. Personalized and interactive packaging is also gaining traction as brands seek to engage consumers and communicate nutritional and product information more effectively.

Future Outlook

The global dairy packaging market is poised for continued growth, driven by rising dairy consumption, advancements in packaging technologies, and increasing demand for sustainable and convenient packaging solutions. As the industry adapts to evolving consumer preferences and environmental regulations, innovation and strategic partnerships will play a key role in shaping the future of dairy packaging worldwide